Embed Size (px)

Citation preview

1

Financial education and Financial education and awareness: OECD work awareness: OECD work and perspectives and perspectives

Budapest, 2nd October Budapest, 2nd October 20082008

André Laboul, Head of OECD Financial André Laboul, Head of OECD Financial Affairs DivisionAffairs Division

outline• The framework: increasing risks• This calls for financial education and

awareness• OECD principles• OECD good practices in pensions,

insurance and credit• Other OECD work, including the Network

and the gateway• Behavioral issues• Conclusions

2

3

OECD TrendsWe observe that individuals face increasing

financial risks and costs due to:• reduced public and/or corporate pension

benefits• increased health costs borne by ageing

individuals in the framework of reduced public health generosity

• increased longevity (good news which can become a nightmare)

• increased frequency and magnitude of natural and man-made catastrophes

• increased financial instability (see current crisis)

Past gains in longevity Life expectancy

at birth has increased an average of 2.2 years per decade over the last century in OECD countries.

Financial risks are more and more transferred to individuals

• Households are taking on more financial risk and responsibility. This is true for both credit decisions and retirement savings.

– The shift to defined contribution pension schemes transfers both investment and longevity risks to individuals. Will they make the right decisions?

– The market for adjustable, variable, interest only mortgage loans (sometimes also in foreign currency) has exploded in several countries and transfer interest rates risk on households

19/04/23 AMF - titre de la présentation 6

ExampleShare of mortgage loans on variable interest rates

Percent of mortgage loans with adjustable and fixed rates in percent of total mortgage loans

Source: OECD Economic Outlook 78, “Recent house price developments: the role of fundamentals”, p. 131.

0

10

20

30

40

50

60

70

80

90

100

Finlan

d

Spain

Austra

lia

Germ

any

United

King

dom

Irelan

dIta

ly

Sweden

United

Sta

tes

Canad

a

Franc

e

Denm

ark

Nethe

rland

s

Pe

r ce

nt

of

all

loa

ns

Short- and long-term fixed

Variable

Increasing financial risks and transfer of risks to households

• This calls for a new regulatory approach• New focus on market conduct and not

only on prudential regulation of financial institutions

• Focus on access, competition, consumer protection and financial education and awareness

• Awareness is key

7

Lack of awareness• The problem is that households may not be

aware of the risk they face• Households may not understand the need to

be protected or overestimate their protection

• Thus, they do not seek protection• Consumers may not understand the products

which are offered and may not be able to compare

• They may overestimate their understanding• That they may…just not care

Call for further information and awareness

• Transparent information and disclosure is key. This is the minimum

• Information should be understandable; plain language should be used

• Information is necessary but not sufficient: individuals need to understand the information

9

Call for financial education

– Many individuals are ill-equipped to face risks and make proper financial decisions

– This calls for improved financial education and awareness on • Risks• Financial ,pensions , insurance products• Their rights and responsibilities

– The goal of financial education is to improve financial literacy

Broader impact of financial education

• Financial education will help build more efficient financial markets by: —improving confidence —encouraging the development of new products

and services —and thus increase competition, innovation and

product quality

• Financial education can also help to reduce poverty and improve social cohesion

The situation is serious

• Recent surveys show that the level of financial education is low in most countries, including in developed countries.

• Worse: consumers often overestimate their financial understanding and thus do not seek to improve it

• This is all the more important as the process of financial education takes time

• Financial education is not just for investors. It is essential for the average family trying to balance its budget, save for children’s education and save for retirement

Solutions are encouraging

• We have found that good financial education programmes are effective: they can increase workers participation in pension plans, reduce mortgage and credit delinquency, and more generally, increase consumers confidence in themselves and in financial institutions.

A role for all stakeholders• Governments and financial authorities

working hand in hand with parliament (including national campaigns, coordination)

• Schools• Financial institutions• Employers• Trade unions• NGO’s, etc.

There is a strong call for national strategy and public-private

partnership14

Win-win strategy for financial industry

• When objectively promoting financial education and awareness, financial institutions help:

• Improve confidence and trust in financial markets, products and institutions

• Improve risk awareness and thus increase demand for protection

• Improve understanding of products and their advantages and thus increase demand

• Reduce losses through better prevention and mitigation

15

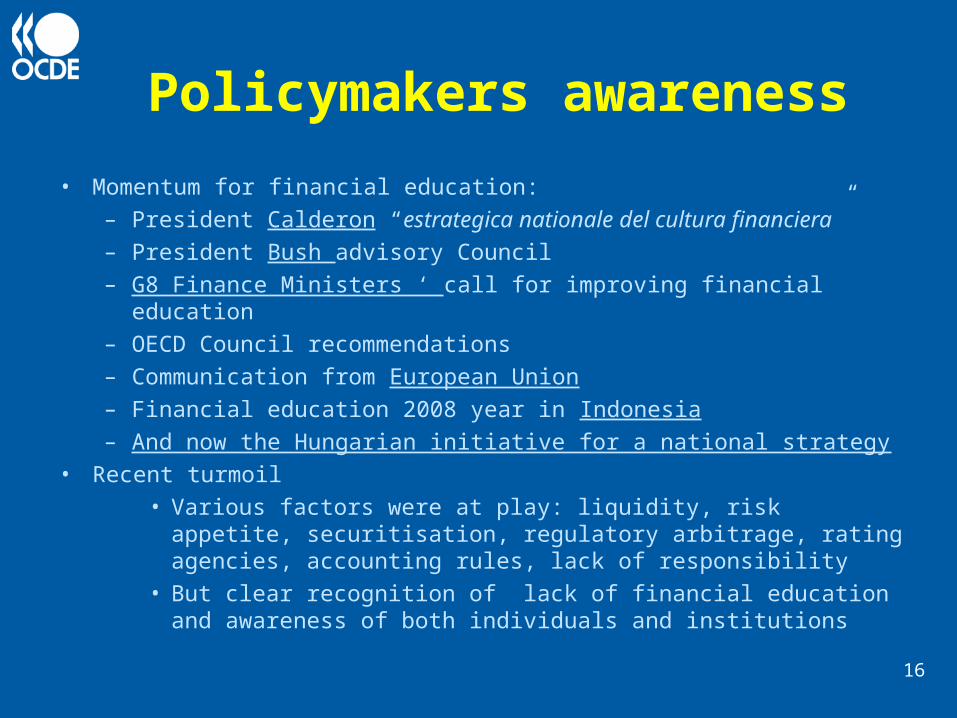

Policymakers awareness

• Momentum for financial education:– President Calderon “estrategica nationale del cultura financiera”– President Bush advisory Council – G8 Finance Ministers ‘ call for improving financial education– OECD Council recommendations– Communication from European Union – Financial education 2008 year in Indonesia– And now the Hungarian initiative for a national strategy

• Recent turmoil• Various factors were at play: liquidity, risk appetite,

securitisation, regulatory arbitrage, rating agencies, accounting rules, lack of responsibility

• But clear recognition of lack of financial education and awareness of both individuals and institutions

16

17

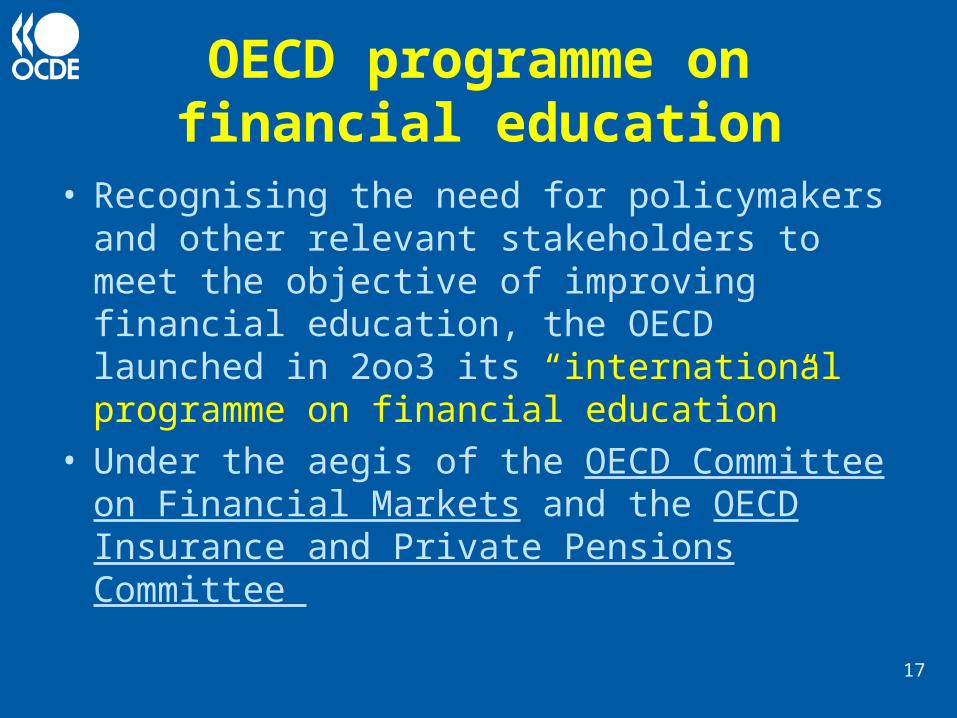

OECD programme on financial education

• Recognising the need for policymakers and other relevant stakeholders to meet the objective of improving financial education, the OECD launched in 2oo3 its “international programme on financial education”

• Under the aegis of the OECD Committee on Financial Markets and the OECD Insurance and Private Pensions Committee

OECD issued the first international publication on financial education

Analytical and comparative framework

Assessment of the Financial Literacy of consumers

Some specific issues: o Investment/retiremento Financial education on credit and debto the unbanked

19

A capacity building process

““Financial education is the process by which Financial education is the process by which financial consumers/investors improve their financial consumers/investors improve their understandingunderstanding of financial/insurance products and of financial/insurance products and concepts; and through information, instruction concepts; and through information, instruction and/or objective advice develop the and/or objective advice develop the skills and skills and confidence confidence to become more aware of financial risks to become more aware of financial risks and opportunities to make informed choices, to know and opportunities to make informed choices, to know where to go for help, and take other effective actions where to go for help, and take other effective actions to improve their financial well-being and protection”.to improve their financial well-being and protection”.

OECD Definition of financial education

OECD Principles on financial education

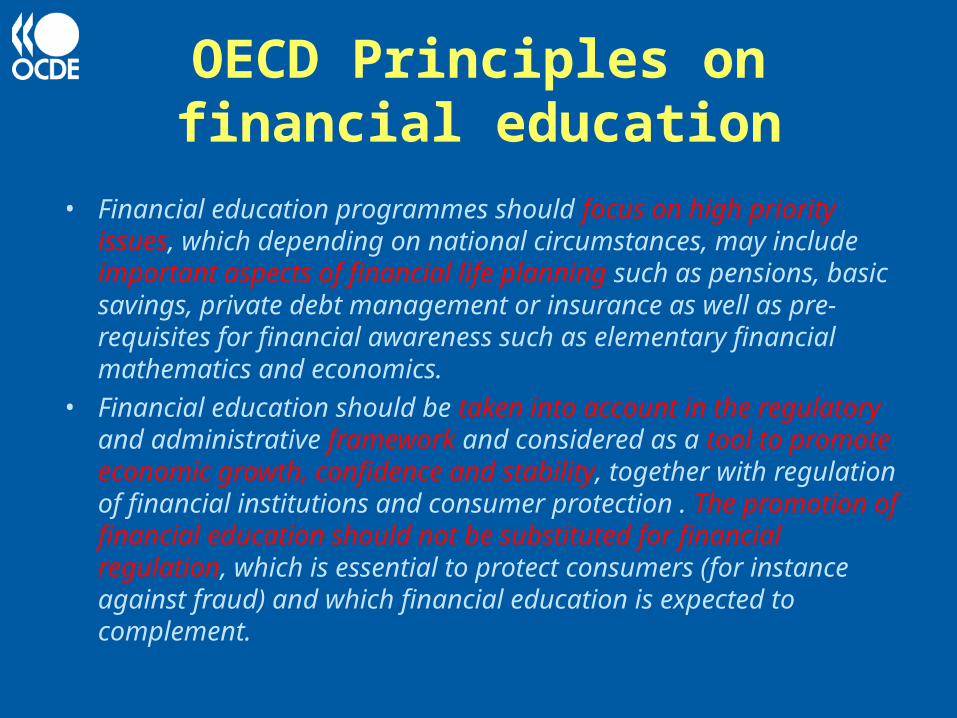

• Financial education programmes should focus on high priority issues, which depending on national circumstances, may include important aspects of financial life planning such as pensions, basic savings, private debt management or insurance as well as pre-requisites for financial awareness such as elementary financial mathematics and economics.

• Financial education should be taken into account in the regulatory and administrative framework and considered as a tool to promote economic growth, confidence and stability, together with regulation of financial institutions and consumer protection . The promotion of financial education should not be substituted for financial regulation, which is essential to protect consumers (for instance against fraud) and which financial education is expected to complement.

OECD Principles on financial education

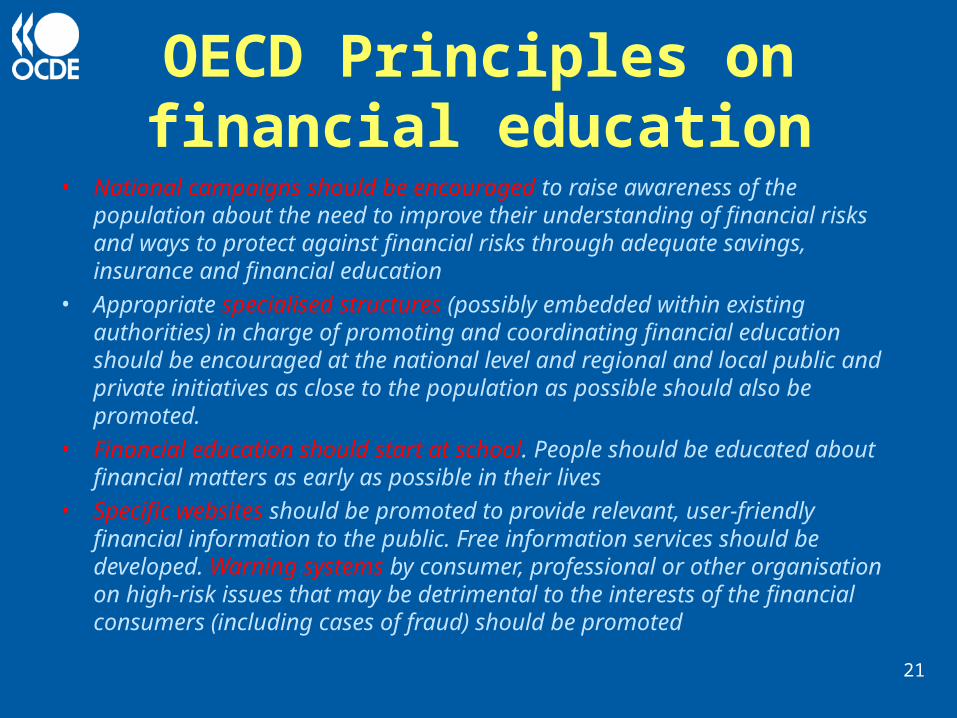

• National campaigns should be encouraged to raise awareness of the population about the need to improve their understanding of financial risks and ways to protect against financial risks through adequate savings, insurance and financial education

• Appropriate specialised structures (possibly embedded within existing authorities) in charge of promoting and coordinating financial education should be encouraged at the national level and regional and local public and private initiatives as close to the population as possible should also be promoted.

• Financial education should start at school. People should be educated about financial matters as early as possible in their lives

• Specific websites should be promoted to provide relevant, user-friendly financial information to the public. Free information services should be developed. Warning systems by consumer, professional or other organisation on high-risk issues that may be detrimental to the interests of the financial consumers (including cases of fraud) should be promoted

21

OECD Principles on financial education

• The role of financial institutions in financial education should be promoted and become part of their good governance with respect to their financial clients. Financial institutions’ accountability and responsibility should be encouraged not only in providing information and advice on financial issues, but also in promoting financial awareness of their clients, especially for long-term commitments and commitments which represent a substantial proportion of current and future income. For the latter two, financial institutions should be encouraged to check that the information provided to their clients is read and understood

• Requirements to specify the types of information (including where to find information and the provision of general comparative and objective information on the risks and returns of different kinds of products) that financial institutions need to provide to clients on financial products and services, should be encouraged.

22

OECD Principles on financial education

• Financial institutions should be encouraged to train their staff on financial education and develop codes of conduct for the provision of general advice about investment and borrowing, not linked to the supply of a specific product

• The development of methodologies to assess existing financial education programmes should be promoted. Official recognition of financial education programmes

which fulfil relevant criteria should be considered. Further research on behavioural economics should be promoted.

23

OECD Principles on financial education

• In order to achieve a wider coverage and exposure, the use of all available media for the dissemination of education messages should be promoted.

• In order to take into account the diverse backgrounds of investors/consumers, financial education that creates different programmes for specific sub-groups of investors/consumers (i.e. young people, the less educated, disadvantaged groups) should be promoted. Financial education should be related to the individual circumstance, through financial education seminars and personalised financial counselling programmes.

• Small print and abstruse documentation should be discouraged Information should be in as clear and simple a format as possible

24

OECD Principles on financial education

• According to the needs of the jurisdiction, evaluation processes should inter alia involve:

• Evaluation on a more systematic basis of the risks that could affect individuals and their relatives, along with analysis of risks and populations that are particularly exposed;

• Evaluation of the population’s degree of literacy and more or less active behaviour as regards their risk exposure, protective or risk mitigation actions;

• Identification and assessment of the education needs of the population with respect to specific groups, risks, products and players as well as the reasons for any shortcomings;

• Systematic evaluation of measures and programmes intended to enhance education on risk and insurance issues, based on predefined criteria and including a cost-benefit assessment.

25

OECD good practices (building on comparative analysis)

• Good practices for financial education on pensions (endorsed by OECD Council in 2008)

• Good practices for risk awareness on insurance (endorsed by OECD Council in 2008)

• Good practices for Financial education on credit

• (to be submitted to the OECD Council in 2009)

Pensions

• Major source of income for retirees• Major lack of understanding• Long-term and complex contracts• Important for public pensions, DB

schemes and even more for DC• Transfers of longevity and

investment risks

Pensions

• Governments and other public authorities should explain public policy clearly (particularly where mandatory savings are involved) – including any pension reforms taking place, the changes in the pension environment, increased individual responsibility and demographic and other changes requiring individuals to save more for their retirement – in order to maintain transparency and confidence in the pension system and thereby encourage individual saving for retirement.

• Governments and other public authorities should direct public awareness campaigns as broadly as possible, given the widespread lack of understanding of pension issues. In addition, specific programmes targeted at the most vulnerable groups (migrants or those with the lowest income and savings levels) can also have a significant impact.

• Governments and other public authorities should work towards making individuals aware of their limited knowledge of financial matters, and pension products in particular, stressing the risks of not having an adequate income in retirement, and should provide information on where to seek further information and advice on how to mitigate these risks.

Pensions

• Governments and other public authorities should strive to ensure that reliable information of projected public pension income is delivered on a regular basis by public pension providers in order for individuals to have a clear and prudent projection of potential retirement income.

• Plan sponsors should inform employees of any pension plan offered to them, its broad structure, a projection of what benefits can be expected and any responsibilities which it entails for them.

• Plan sponsors should be encouraged to provide financial education for pension plan members, or should at least provide plan members with information on where they can find such training

• Where plan members take responsibility for investment decisions, such as in defined contribution type pension plans, plan sponsors should at least ensure that workers are aware of this responsibility and have access to information which can help them make informed investment decisions

•

Pensions

• Where a plan sponsor’s role in the provisioning of the pension plan allows, and where they are aware that employees’ or members’ contributions to their defined contribution pension plans are significantly insufficient to ensure an adequate retirement income, they should alert employees or members to this risk.

• Where employees or members are offered a range of investment options, plan sponsors should consider limiting, in a well-structured fashion, the number of investment choices available (or provide a ‘two tier’ choice between a basic system and a system offering more sophisticated investment choices) and should provide a suitably structured default option in order to help employees or members make optimal pension investment decisions.

Pensions

• Pension funds, fiduciaries, providers and intermediaries should produce information for individuals on the design, operation and performance of pension funds and retirement products which is timely, accurate and accessible.

• They should be encouraged to supply prudent projections of retirement income which can be expected from pension funds and retirement products.

• Any institution providing information should check that the information has been understood.

• In defined contribution schemes, a single source with clear and comparable information on the types of investment, including risk and return profiles, and the costs involved is required

• Financial education should be encouraged for trustees and other pension fund fiduciaries to ensure they have the necessary skills (over and above any ‘fit and proper’ requirements) to make suitable decisions and fulfil their fiduciary duty. Information and suggested questions could be provided to individuals to help overcome asymmetries of information and allow them to evaluate advice from financial intermediaries successfully.

Insurance

• Governments’ involvement in this education process should be mainly aimed at enhancing awareness of major risks and the need for adequate protection, including through various insurance instruments, and at enabling individuals to attain a sufficient level of knowledge, understanding and skills in order to adopt a responsible stance and make sensible choices as regards insurance issues. In this connection, a series of actions should be encouraged, including:

• Promoting a “culture” of responsibility for personal protection, in particular by educating people about notions relating to risk, risk mitigation and compensation including possibilities offered by insurance tools and basic insurance mechanisms and products:

• School curricula, in particular at the secondary level, should encompass more specific notions relating to risk and insurance (taught separately or within finance or economics classes), including, inter alia, basic insurance mechanisms and products and the major dynamics and components of the insurance market;

• Promoting and developing prevention and information programmes and campaigns regarding seriously damaging risks, vulnerable populations, innovative or complex insurance products and products implying a greater transfer of risks to individuals- such as unit-linked-, possible underinsurance, overlapping and/or over insurance, key contract clauses and conditions as well as applicable rights and obligations of consumers as regards insurance products and insurance market players.

Insurance

• Good selling practices should include the development of mechanisms for the assessment by sales staff or agents of clients’ level of understanding, who should be adequately qualified and trained in this respect. This should particularly apply to complex insurance products, insurance products involving long-term commitments or commitments which represent a substantial proportion of current and future income or products which involve an important transfer of risks to policyholders.

• Depending on the country context, associations of insurance market players, consumers’ associations, employers, trade unions, other NGOS and institutes specialised in insurance issues, should also contribute to financial education programmes. For instance, these social and business partners should be encouraged to conduct surveys on the needs of consumers as regards risk awareness and education on insurance issues and on how consumers prefer to receive such information.

Insurance

• Programmes aimed at improving the level of awareness and education on risk and insurance should consider making use of a large variety of means so as to ensure that a wide audience - including targeted and vulnerable groups- may be appropriately and effectively reached.

• This should imply, according to national circumstances, encouraging:

• Broad media coverage (i.e. radio, television, print journalism, billboard advertising and internet), and the organisation of events to raise awareness on insurance issues and on the importance of financial education in this area. In this perspective, risk awareness and knowledge of insurance issues of the main players in the information and instruction channels (i.e. the media, teachers, educators and parents) should be reinforced;

• The development of high-profile sources of reliable, objective and free information and/or specific bodies or centres through which insurance stakeholders could - possibly - co-ordinate to offer consumers information, education, assistance and advice on insurance issues;

Insurance

• The development of various tools - internet sites, but also guides, brochures, leaflets and other available traditional or modern communication methods - enabling consumers to consult reliable sources for comparisons of the products offered by various insurance market players and to assess their level of protection against potential risks - e.g. through calculators and quizzes -, as well as their own knowledge of their insurance requirements and of how their policies operate.

• For the most severe risks, without limiting the freedom to contract, under and/or inappropriately-covered risks, default mechanisms, which take into account potential temporary or long-term deficiencies in financial education or the passive behaviour of consumers, should be considered and properly regulated.

• Similarly, the insurance and financial sectors should also be encouraged to develop innovative insurance products (e.g. microinsurance) and tailored distribution channels that can best meet the need for protection of consumers particularly of the most vulnerable segments of the population.

Credit

• Governments should work towards making individuals aware of their limited knowledge on credit-related issues, stressing the risks and implications of. having bad credit behaviour and of making inadequate credit decisions, and should provide information for where to seek further information and advice on how to mitigate those risks and how to file complains and seek redress if they think their rights have not been respected.

• Government toll-free hotlines should be promoted and available to consumers as source of neutral information and as a means of obtaining impartial answers to questions they may have about their rights, responsibilities or about credit options that may be available to them.

• Governments should develop tools to assist citizens self-assess the appropriateness of them entering into certain types of loans or credit products given their personal circumstances. Tools and calculators should also be developed to help consumers evaluate the costs and consequences of bad decisions or behaviours

Credit

• To facilitate product comparison by consumers, governments should promote the use by all creditors and lenders, in their advertising campaigns and marketing and disclosure documents, of a unique and standardized, effective interest rate that takes into account any fees, in addition to interest charges, that may be associated with the credit product or loan. (In neighbour countries, or countries that are part of an economic union, whereby citizens of one county can freely apply for loans or credit products in another country, governments should agree on a common approach to calculating this effective interest rate).

• To enhance consumers’ awareness, governments should promote the use by all creditors and lenders, and for any type of loan or credit product, of a box or table prominently displayed in the loan or credit agreement, and clearly summarizing the important terms and conditions of the loan or credit product.

• Any public policy promoting asset building through consumers’ use of credit products should be accompanied, as an integral part, by a broad public consumer education strategy, tools and programmes to allow consumers make wise, rational and informed credit decisions.

• Financial information sharing platforms (such as credit bureaus or credit reporting agencies) should be promoted to allow consumers to receive the benefits of credit ratings And, where such platforms are in place, governments should promote consumers’ free access to their credit reports.

Credit

• Any market player involved in the provision of loans or credit products to consumers should be suitably trained, qualified and regulated.

• As a rule, the role and responsibilities of all credit market players in the financial education process should be clearly defined and promoted and should become part of their good governance with respect to their credit holders and/or customers. The accountability of credit market players, and in particular of independent intermediaries who represent their clients in this respect, should encompass accurate provision of quality information that can be distinguished from advertising and promotion.

• Any credit provider should use due diligence in assessing consumers’ profile. Consumers should receive objective and relevant explanations and advice commensurate with their degree of sophistication and needs from sales staff or agents who should be adequately qualified and trained in this respect. This should particularly apply to complex credit products, products involving long-term commitments, or commitments which represent a substantial proportion of current and future income or which feature important penalty clauses in case of default or contract termination by the consumer.

Credit

• Credit market players should be encouraged to post, on their Internet sites, complete information on their credit products and loans, including their characteristics and a fee table.

• Credit market players should be encouraged to engage in further initiatives to increase individuals’ awareness of their rights and responsibilities as credit holders, of the importance of good credit behaviour and the implication making bad credit decisions, of tools available to help them shop around for the best option, as well as providing unbiased information on credit related issues. These activities should be clearly distinguished from marketing promotion and advertising.

• Intermediaries or third parties engaged in the credit markets, which have direct interactions with consumers (through advertisement or direct credit transactions) should be subject to the same requirements and expectations regarding consumers’ awareness and education, and have the same liabilities in that respect, as any market participant.

•

Credit

• Mortgages are for many consumers the most important debt they will take in their lifetime. Because of their long term nature, their size, and their unique and often complex characteristics, special consideration should be given to the protection and awareness of consumers entering into a mortgage agreement.

• Mortgage lenders and intermediaries should clearly state to potential lenders the implications of them providing inaccurate information or making misrepresentations on their loan applications.

• Consumers should not be prevented from, or limited in their ability to, comparing mortgage options or products and from obtaining quotes from many loan or credit product providers and/or intermediaries.

Credit

• According to national circumstances, legislation should encourage clear, transparent and plain language disclosure on mortgage agreements. For instance, lenders should be required to prominently display, in their mortgage agreements, a summary of key terms and conditions of the loan (e.g., amount, amortization period and term, interest rate and variable rate features, description and cost of optional services that the consumer accepted, any fee and charge associated with the loan, and how the penalty – if any – will be calculated in case of prepayment, etc).

• According to national circumstances, financial education material dealing with mortgage issues should include information about the benefits for consumers, when they can afford it, of paying off their mortgage faster and about ways of doing so without extra costs or penalties.

• Regulatory considerations should be given to making mortgage lenders and intermediaries responsible for ascertaining consumers’ credit needs and for determining whether consumers have the capacity to repay a loan that satisfies those needs, especially in a variable interest rate environment.

42

Current OECD work

• OECD has become the international leader on the development of guidelines and standards in financial education • G8 Financial Ministers recognised, in June 2006,

OECD work on financial education and requested the Organisation to further develop financial literacy guidelines based on best practices

• recently supported by policymakers like Secretary of US Treasury Paulson (May 2008) the Council of the European Parliament (June 2008) or the Mexican Minister of Finance (July 2008)

Current OECD work• Current development of guidelines

on • Financial education on credit • Policy handbook on risk awareness • Pension information • Annuities• Insurance and financial intermediaries• financial education at school, etc.

• In-depth comparative policy analysis on related topics

43

Current OECD work

• New methodology to assess financial literacy and financial education programmes

• Survey on financial literacy (including at school, possibly through PISA)

• Creation of a governmental international network (with representatives from financial authorities from more than 60 countries)

44

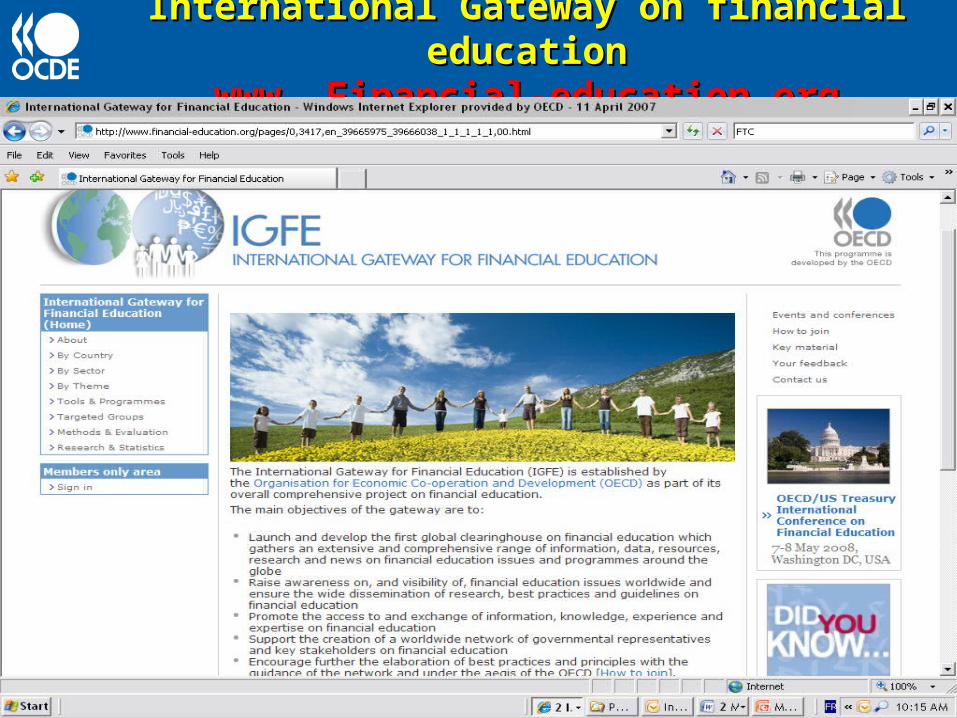

Current OECD work

• Setting up of an international Gateway at www.financial-education.org

• Numerous international conferences– India, Russia, Turkey– Most recent one in USA: 6-8 May 2008, co-sponsored

with US Treasury (230 participants from more than 50 countries)

– Next one in Indonesia: 21-22 October 2008– Supporting national events: Querétaro, 11 July 2008

• Co-operation with other international organisations (WB, IMF, EU, etc.)

45

International Gateway on financial educationInternational Gateway on financial educationwww. Financial-education.orgwww. Financial-education.org

Need to assess financial education

– It is important to provide financial education, however it is essential to provide efficient and effective financial education programmes

– This calls for systematic assessment and related methodology (also an OECD project)

– But difficult especially for long term products: pensions, mortgage credit, insurance

– Lack of comparable data47

Financial education is not enough

– Other measures are needed to overcome consumers myopia and passive behaviour– To deal with fraud, miss-selling– To protect consumers against bankruptcies– And more generally to protect consumers’ rights

–

Behavioural factors like inertia or passivity may block consumers

Additional mechanisms may be needed…

• A number of studies in behavioural finance relate financial behaviour to psychological factors. These studies show, for example, that due to inertia and procrastination, individuals will not sign up for a retirement savings plan even though they know they should

• As a consequence of inertia, individuals tell themselves they will enrol “tomorrow”. Tomorrow, however, never comes. Other studies find that employees often do what is easiest, which may be doing nothing. Or they rely on state intervention (samaritan dilemnia)

Combating inertia

• Automatic enrolment/default mechanisms which transfer the options from opt in to opt out

• Similarly, plans can be designed such that workers commit to increasing their contribution rate in these savings plans each time they get a raise. Plans such as the Save More Tomorrow plan, implemented in the United States, is based on research showing that individuals prefer future opportunities to save over current ones, that inertia and procrastination keep individuals in programmes once enrolled, and that loss aversion makes individuals reluctant to increase retirement savings if this reduces take-home pay.

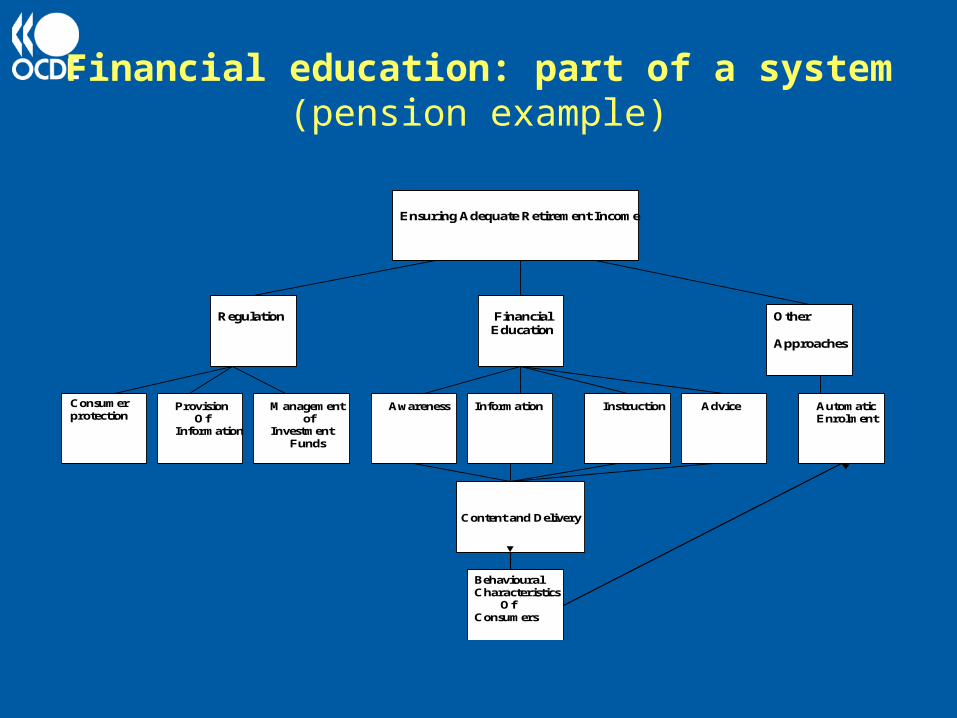

Financial education: part of a system(pension example)

Consumer protection

Ensuring Adequate Retirement Income

Regulation Financial Other Education Approaches Provision Management Awareness Information Instruction Advice Automatic Of of Enrolment Information Investment Funds Content and Delivery Behavioural Characteristics Of Consumers

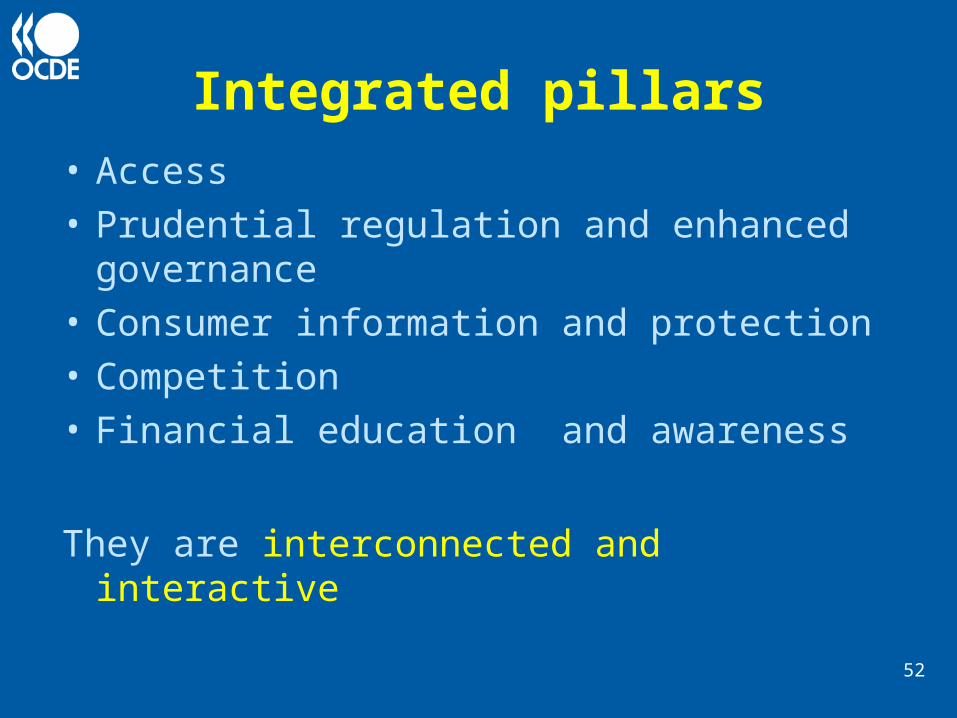

Integrated pillars

• Access• Prudential regulation and enhanced

governance• Consumer information and protection• Competition• Financial education and awareness

They are interconnected and interactive

52

53

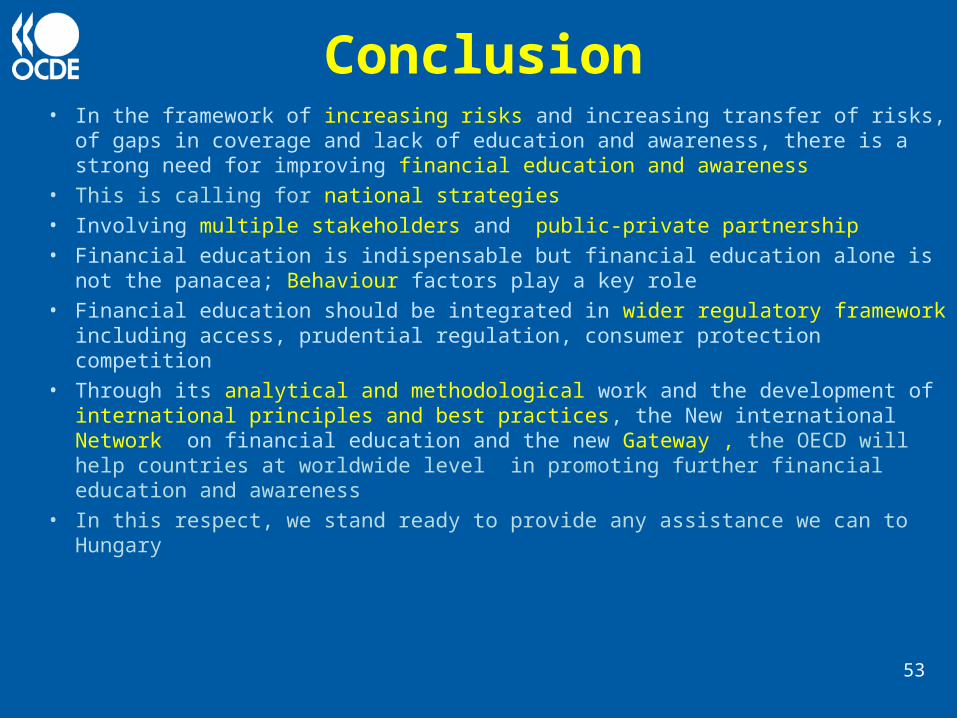

Conclusion• In the framework of increasing risks and increasing transfer of risks, of

gaps in coverage and lack of education and awareness, there is a strong need for improving financial education and awareness

• This is calling for national strategies • Involving multiple stakeholders and public-private partnership• Financial education is indispensable but financial education alone is not

the panacea; Behaviour factors play a key role• Financial education should be integrated in wider regulatory framework

including access, prudential regulation, consumer protection competition• Through its analytical and methodological work and the development of

international principles and best practices, the New international Network on financial education and the new Gateway , the OECD will help countries at worldwide level in promoting further financial education and awareness

• In this respect, we stand ready to provide any assistance we can to Hungary

THANK YOU

more information at:

www.oecd.org/daf/financialeducation

and www.financial-education.org54