Embed Size (px)

Citation preview

1

FFY2011

Presented at FFY2011 EAP Annual Training August 11 & 12, 2010

Section 2 content: Chapter 1

Program Control Environment

Chapter 2 Overview of Service Provider Responsibility

Chapter 3 Vendor

EAP EAP Annual Annual TraininTraininggSection 2Section 2 (Of 6)(Of 6)

2

Program Description EAP Business Strategy Model EAP Internal Controls Framework (ICF)

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

Chapter ContentChapter Content

3

Program ManagementProgram Management

A number of concepts have been developed over time Each added to EAP improvements & made a good

program even better Lately we have tried to more fully integrate these

concepts into whole comprehensive approach We are not yet done, further work is ahead

Incremental Development Of EAP Business Incremental Development Of EAP Business Models & StrategiesModels & Strategies

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

4

The Minnesota ModelThe Minnesota Model EAP employs a “Coordinated Responsibility Model” The Model assumes households, vendors, and the program all have a

role in assuring heat for low-income households during the winter. Program responsibility includes providing heating payment

supplements, case management and advocacy for households, and maintaining influence with vendors.

Energy Vendor responsibility is to be as flexible as possible so energy payments leverage the highest possible level of service to the household.

Household responsibility is to make reasonable and planned payments for energy service, access government aid when necessary and communicate with vendors and government service providers.

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

5

EAP Management ApproachEAP Management ApproachProven Process Including Project Plans Tools Continuous Improvement

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

6

Formal & Documented Project Formal & Documented Project PlansPlans Built with stakeholder input

PAC EACA JAD State Staff Policy makers

Puts a well-understood and accepted process in place for reaching the project’s results

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

7

Approach by Advanced Approach by Advanced StrategiesStrategies Used to develop eHEAT Trained all EAP State Staff Developed Internal Plans

Master Plan Project Plans

Conducted JADs Issues Management Broadened application

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

8

Project (Effort) DefinitionsProject (Effort) Definitions Intentions: Goals or outcomes intended Values: Principles, standards and ideals incorporated

into the project or effort Focus: What’s included and excluded Context: Situations existing around the project, not

part of it but can affect it

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

9

Business Strategy ModelBusiness Strategy ModelWhy Do We Need a BSM?Provides a Shared Vision Gives people a sense we are all serving the same goals ... we

are all working together Helps build a high-performing team Helps provide consistent messages to key stakeholders Helps guide day-to-day decisions and actions BSM Intention Statement is our Mission – State Plan, Local Plan We know you have heard it before but this is our basic

foundation/strategy/mission

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

10

EAP BSM Intention EAP BSM Intention StatementStatementMaintain affordable, continuous, and safe home energy for low-income Minnesota households

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

11

VisionVisionWhat happens if we don’t have a shared vision? We each have a vision that underlies our behavior If it is not shared – we appear to be

Out of sync Disorganized Inefficient Inconsistent Selfish Ultimately not worthy of confidence Appear unreliable (different responses from different individuals)

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

12

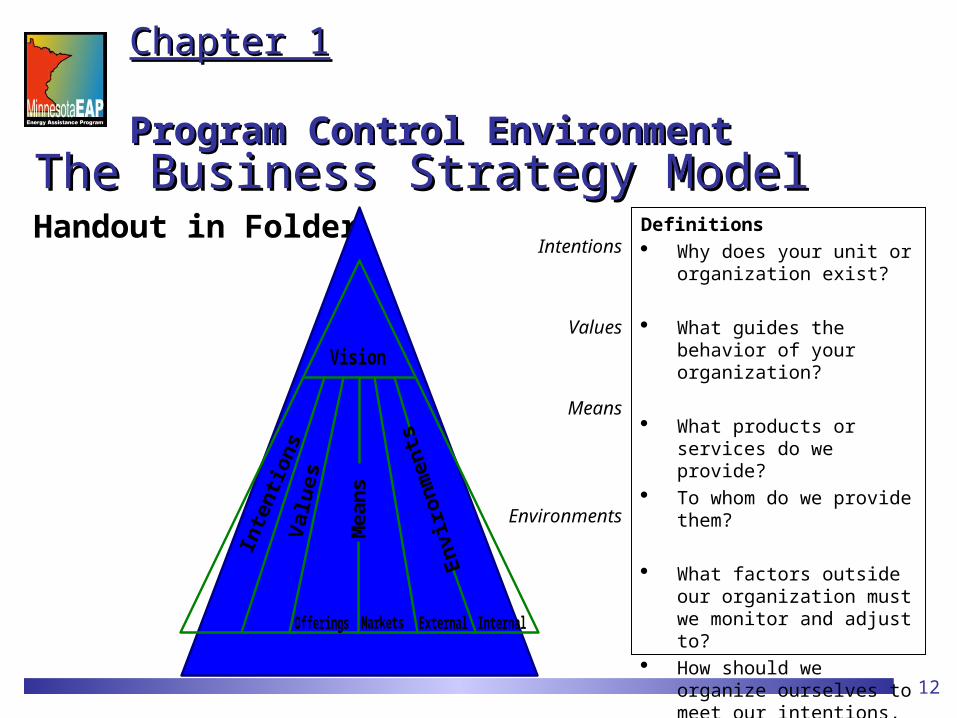

The Business Strategy ModelThe Business Strategy Model Handout in Folder

Vision

Offerings Markets External Internal

Means

Definitions Why does your unit or organization

exist?

What guides the behavior of your organization?

What products or services do we provide?

To whom do we provide them?

What factors outside our organization must we monitor and adjust to?

How should we organize ourselves to meet our intentions, within our values?

Intentions

Values

Means

Environments

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

13

Program ManagementProgram ManagementEAP and PAC BSM SharedEAP & PAC BSM are same except means, but share Intentions Values Means (Offerings & Markets) Environments

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

14

Program ManagementProgram ManagementPAC BSM- Background

How we got here Developed for the program by the State Staff Extracted PAC specific content from a combination of program

BSM and PAC effort definition

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

15

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

EAP BSM - ValuesEAP BSM - Values

4 categories1. Overall2. Regarding Households3. Regarding Collaboration4. Regarding Policy Direction

16

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

EAP BSM - ValuesEAP BSM - Values1. Overall

a. Affordable, safe, and dependable energy b. Advocacy c. Good stewardship of resources d. Being realistic about limitationse. Qualityf. Partners and Partnerships (see Coordinated Responsibility Model)g. Understanding the program in the context of broader public policy

and other needs of low-income Minnesotans h. Being the compass but not the mapi. Reward positive, proactive behavior by all energy stakeholders

17

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

EAP BSM - ValuesEAP BSM - Values2. Regarding Households

a. Dignity and privacy b. Participation (see Coordinated Responsibility Model)c. Empower people to make informed decisions regarding

their energy use and needsd. Serving the most in need – balancing total number of

participants makeup of participants, and levels of service

18

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

EAP BSM - ValuesEAP BSM - Values3. Regarding Collaboration

a. The responsibility to provide a safety netb. Working towards the same goalsc. Stakeholders personal commitment and accountability d. Represent our own personal perspective, the views of our

stakeholder group, and the world from multiple perspectives

e. Actively coordinate across programs and departments

19

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

EAP BSM - ValuesEAP BSM - Values4. Regarding Policy Direction

a. Creative and flexible approaches b. Consistency c. Balance of simplicity and fairness d. Recommendations based on a sound community analysise. More strategic than operationald. Timely and proactive in order to mitigate emerging

problems

20

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

EAP BSM - Means OfferingsEAP BSM - Means OfferingsOfferings (Program Products & Services) Energy bill payment Furnace repair or replacement Energy related crisis intervention Advocacy Outreach Referral Information Education Conservation, coordination and collaboration Demonstrate effectiveness of investment

21

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

EAP BSM - Means OfferingsEAP BSM - Means OfferingsState Staff Offerings Oversight, monitoring and quality control Compliance with Federal and State requirements Policy Decision making Planning Training and Technical Support Stakeholder involvement and communication Program advocacy and information

22

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

Markets (Customers) Households, emphasizing low-

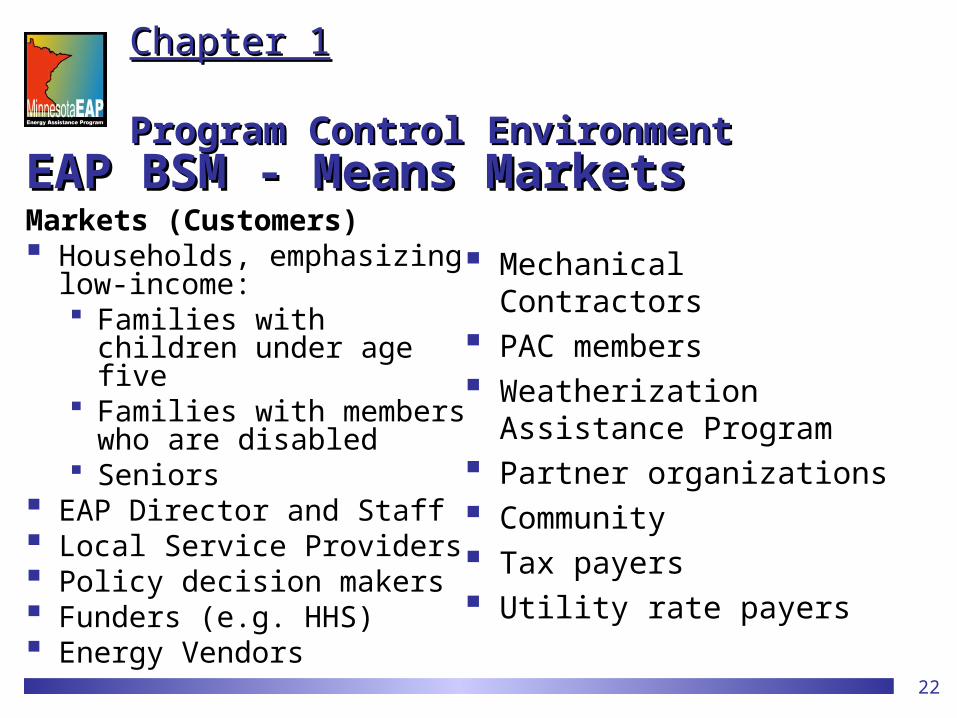

income: Families with children under

age five Families with members who

are disabled Seniors

EAP Director and Staff Local Service Providers Policy decision makers Funders (e.g. HHS) Energy Vendors

Mechanical Contractors PAC members Weatherization Assistance

Program Partner organizations Community Tax payers Utility rate payers

EAP BSM - Means MarketsEAP BSM - Means Markets

23

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

PAC BSM - OfferingsPAC BSM - Offerings Direction Oversight Advocacy, education and outreach

24

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

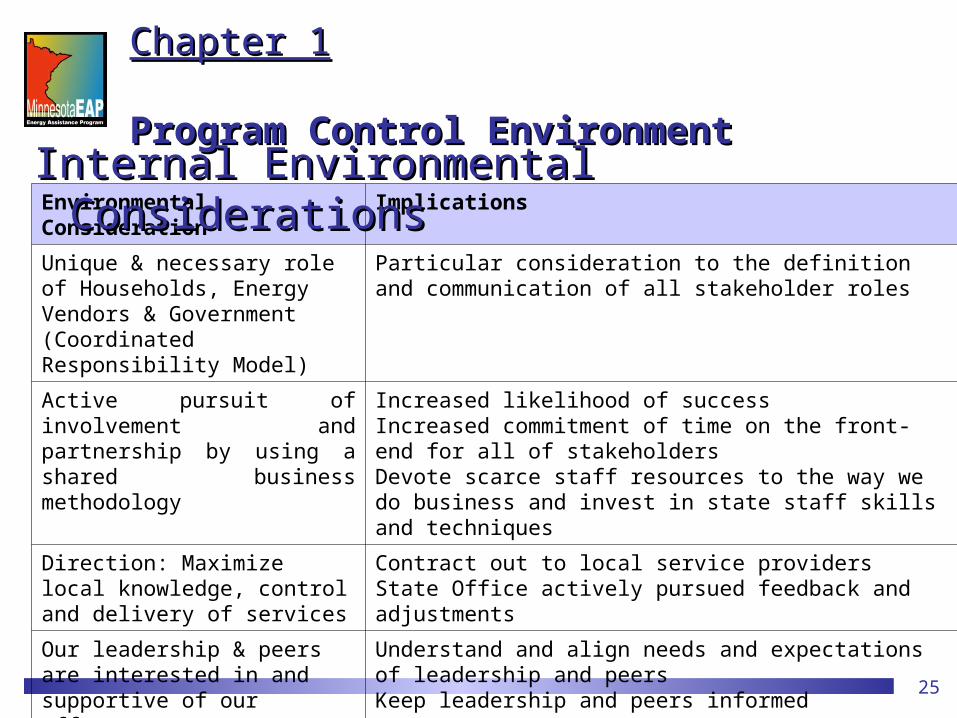

BSM EnvironmentsBSM Environments Internal External

25

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

Environmental Consideration Implications

Unique & necessary role of Households, Energy Vendors & Government (Coordinated Responsibility Model)

Particular consideration to the definition and communication of all stakeholder roles

Active pursuit of involvement and partnership by using a shared business methodology

Increased likelihood of success Increased commitment of time on the front-end for all of stakeholders Devote scarce staff resources to the way we do business and invest in state staff skills and techniques

Direction: Maximize local knowledge, control and delivery of services

Contract out to local service providersState Office actively pursued feedback and adjustments

Our leadership & peers are interested in and supportive of our efforts

Understand and align needs and expectations of leadership and peers Keep leadership and peers informed

Our partners & community are interested in & supportive of our efforts

Understand & align needs and expectations of partners and community Keep partners and community informed

We have custom developed technology tools to support our business

We can directly influence what our tools do/not support – constrained to resources Increased consistency of the program – less local control

Internal Environmental ConsiderationsInternal Environmental Considerations

26

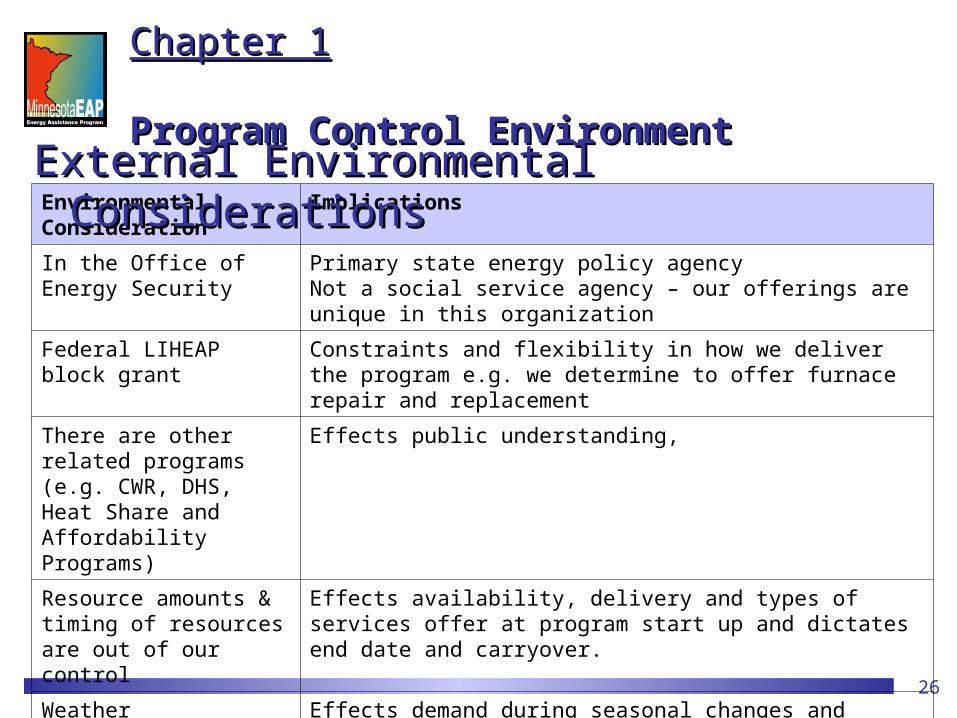

Chapter 1Chapter 1Program Control EnvironmentProgram Control Environment

Environmental Consideration Implications

In the Office of Energy Security Primary state energy policy agency Not a social service agency – our offerings are unique in this organization

Federal LIHEAP block grant Constraints and flexibility in how we deliver the program e.g. we determine to offer furnace repair and replacement

There are other related programs (e.g. CWR, DHS, Heat Share and Affordability Programs)

Effects public understanding,

Resource amounts & timing of resources are out of our control

Effects availability, delivery and types of services offer at program start up and dictates end date and carryover.

Weather Effects demand during seasonal changes and effects consumption amounts

Economy Increase demand on program services

Fuel prices Changes impact of benefits and need for services

External Environmental ConsiderationsExternal Environmental Considerations

Chapter Description

Chapter outlines at a high level activities required of the EAP Coordinator & SP leadership.

It outlines using Internal Controls Framework (ICF). Summarizes information detailed in the Policy

Manual, referring to the appropriate chapter for policy details.

Chapter 2Overview of Service Provider ResponsibilityOverview of Service Provider Responsibility

Page 1

Chapter Contents

Control Environment Risk Assessment Control Activities Communication and Information Monitoring

Chapter 2Overview of Service Provider ResponsibilityOverview of Service Provider Responsibility

Page 1

Training Topics Advance EAP internal Controls & Frameworkby Reviewing ICF understanding? Reviewing where EAP is with ICF Discussing what is next with ICF?

Chapter 2Overview of Service Provider ResponsibilityOverview of Service Provider Responsibility

What is ICF? The Framework is used assess the Internal Controls maturity to determine how competently an organization

Identifies its risks Documents & assigns its control procedures How it monitors performance & effectiveness its procedures

Chapter 2Overview of Service Provider ResponsibilityOverview of Service Provider Responsibility

Internal Control DefinitionDefines internal control as a process, effected by individuals within an organization, designed to provide reasonable assurance regarding the achievement of these objectives:

1. Effectiveness & efficiency of operations2. Reliability of financial reporting 3. Compliance with applicable laws & regulations.

Chapter 2Overview of Service Provider Responsibility

Page 1

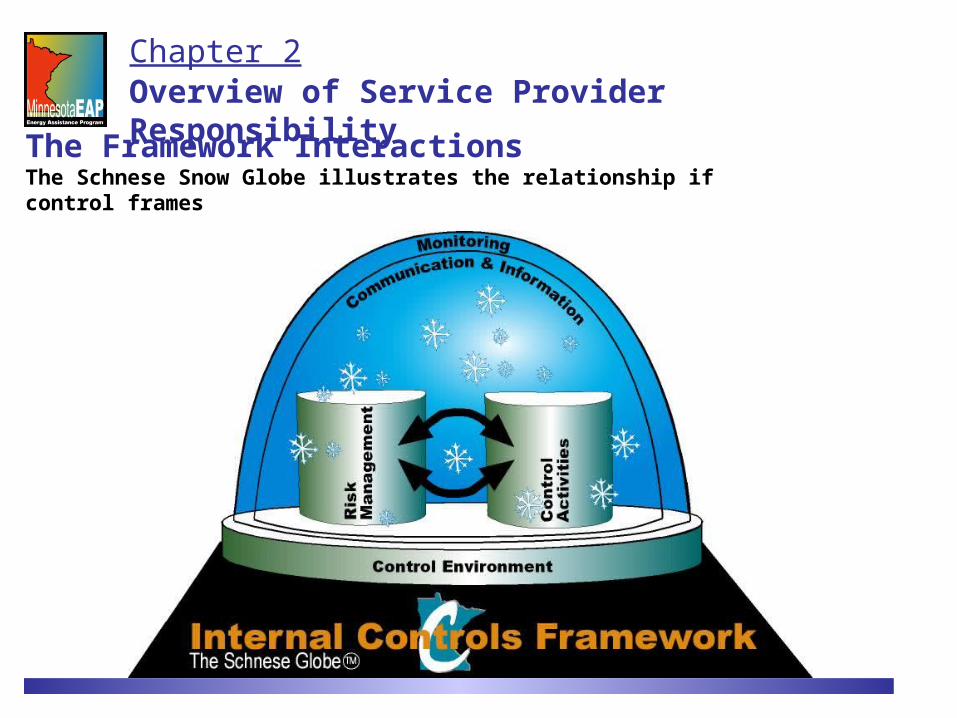

The Framework InteractionsThe Schnese Snow Globe illustrates the relationship if control frames

Chapter 2Overview of Service Provider Responsibility

1. Control Environment

Service Providers should establish and maintain an ethical and procedural work environment throughout the organization that sets a positive and supportive attitude toward internal control and conscientious management.

Chapter 2Overview of Service Provider Responsibility

Page 1

Service Provider EAP Organizational CompetenceService Providers should assure: Service Provider human resource materials A reasonable EAP resourcing model EAP staff have functional position description EAP staff have proper agency knowledge EAP staff have proficient eHEAT competencies EAP staff demonstrate knowledge of Service Provider policies and

procedures Formal and new staff training Support of technical environment necessary to deliver EAP Training for staff to work with diverse populations

Chapter 2Overview of Service Provider Responsibility

Page 2

Implementations Control EnvironmentLocal Plan, contracts gives assurances by documenting internal

controls competenciesSP connects Business Strategy Model (BSM) & SP MissionSP participates in EAP management methodology including

joint approach to development, EACA, JADs, training etc.SP have realistic staffing model, structure of authority and show

a commitment to EAPService Providers participates in EAP training and trains staff

Chapter 2Overview of Service Provider Responsibility

2. Risk Management

Chapter 2Overview of Service Provider Responsibility

Risk planning is geared toward events that occur when things are different than planned. Service Providers should have procedures in place to deal with unplanned events. . . .

. . .The goal is assuring the Service Provider’s ability to maintain financial strength, a positive public image, and the overall quality of its products and government services.

Page 2

Risk CompetenceSP has risk a assessment process Indentifying Internal and external risk Assessing the impact and the likelihood these risks

might occur Selecting whether to avoid, reduce, share, or accept

various risks Considers controls to mitigate risk or to contain it to

an acceptable level

Chapter 2Overview of Service Provider Responsibility

Implementations Risk Management SP conduct risk assessment & mitigation activitiesState and SP conduct oversight activities including:

Data, file and other checks Data & Technology practices (eHEAT user management)

SP make a maintain disaster plansLocal Employee Applications processes and utilization of state

requirementsSP uses incident reporting processSP uses error & fraud processes

Chapter 2Overview of Service Provider Responsibility

3. Control Activities

Service Provider should design and implement internal control in processing applications, determining eligibility and delivering benefits. These procedures assure program services are timely, accurate, uniform and equally available throughout the State. They address essential EAP required procedures

Chapter 2Overview of Service Provider Responsibility

Page 3

Control Activities Competence There are realistic policies & procedures to help

ensure management directives are carried out Control activities occur throughout the organization

at all levels in all functions

Chapter 2Overview of Service Provider Responsibility

Implementation Control Environment SP processes have approvals & authorizations for benefit

determination & payments (Separation of duties) SP conduct and support verifications for:

Income eligibility & documentation vendor registration payment process for ERR contractors. Household check points

SP conducts analytical procedures or quality controls SP conducts reconciliations like allocation and FSR

Chapter 2Overview of Service Provider Responsibility

4. Information & CommunicationService Provider’s should communicate the internal control policies and procedures to all staff and stakeholders so they understand what is expected of them and the scope of their freedom to act in relation to program participants and partners.

Chapter 2Overview of Service Provider Responsibility

Page 6

Information & Communication Competence Organization identifies, captures & communicates pertinent

information in a timely manner to the right people to enable them to carry out their responsibilities

Information systems are effective Internal information, and external events, activities &

conditions are communicated to enable management to make informed business decisions and employees & partners to perform their roles & duties

Chapter 2Overview of Service Provider Responsibility

Implementation Communication & Information SP has communication plan to dissemination information SP has routines, like meetings, to inform staff and partners SP conducts appropriate and effective outreach SP retains information over time SP is up to date with routine EAP communication:

Weekly newsletter The Energizer & Ad hoc email Web information and program tools Association meetings (Executive Directors & Coordinators)

T&TA SP is responsive to reporting & other deadlines

Chapter 2Overview of Service Provider Responsibility

5. Monitoring

Monitoring relates to Service Provider’s separate evaluations of internal control, such as control self-assessments or internal procedures and performance . . .

Page 6

Chapter 2Overview of Service Provider Responsibility

Monitoring Competence: Monitoring is performed by management & supervisors on a

continuous or periodic basis Identifying control deficiencies and reporting to top

management and are remedied in a timely manner with appropriate corrective actions

Is periodic follow-up on corrective actions taken to ensure control weaknesses are strengthened and no longer exist

Chapter 2Overview of Service Provider Responsibility

Implementation Monitoring SP uses performance goals like WACT to adjust resources SP measures average days from log to paid to monitor

efficiency SP uses customer feedback SP monitors effect on production when implementing new

tools or processes (Ex: Scanning)

Chapter 2Overview of Service Provider Responsibility

What is Controls Maturation Internal Controls mature as people become more

aware of them It becomes the culture and language Results in improvement of Control Activities in a

continuous improvement process Risk management is strengthened

Chapter 2Overview of Service Provider ResponsibilityOverview of Service Provider Responsibility

Our Responsibility Advance our understanding ICF Understand how existing EAP controls fit ICF Continue to implement new ICF activities Strengthening controls when weaknesses are detected Provide supervision to ensure controls operate effectively Obtain ICF information & training for selves & staff necessary

to meaningfully take responsibility for internal controls Share these Chapters with SP leadership

Chapter 2Overview of Service Provider ResponsibilityOverview of Service Provider Responsibility

ICF Improvements Next In FFY2011 EAP will focus on: Advancing Risk Management Improvement of self monitoring internal controls for continuous

improvement Continue framing is a way of organizing existing & then making

improvement if needed Everything you see is organized through ICF & this will

continue

Chapter 2Overview of Service Provider ResponsibilityOverview of Service Provider Responsibility

Training Topics 1. Context2. Chapter Structure3. Policy & Procedure Changes

Refund Checks received After September 30 Sharing Data Vendor Agreement Improvements

4. Vendor Monitoring and Issues Management

Chapter 3Vendors

More scrutiny on vendor management from: Events in Pennsylvania General Account Office (GAO) Investigator General (IG) Federal & State continue to greater Internal Controls Vendor controls are the major area of transactions

Important Context

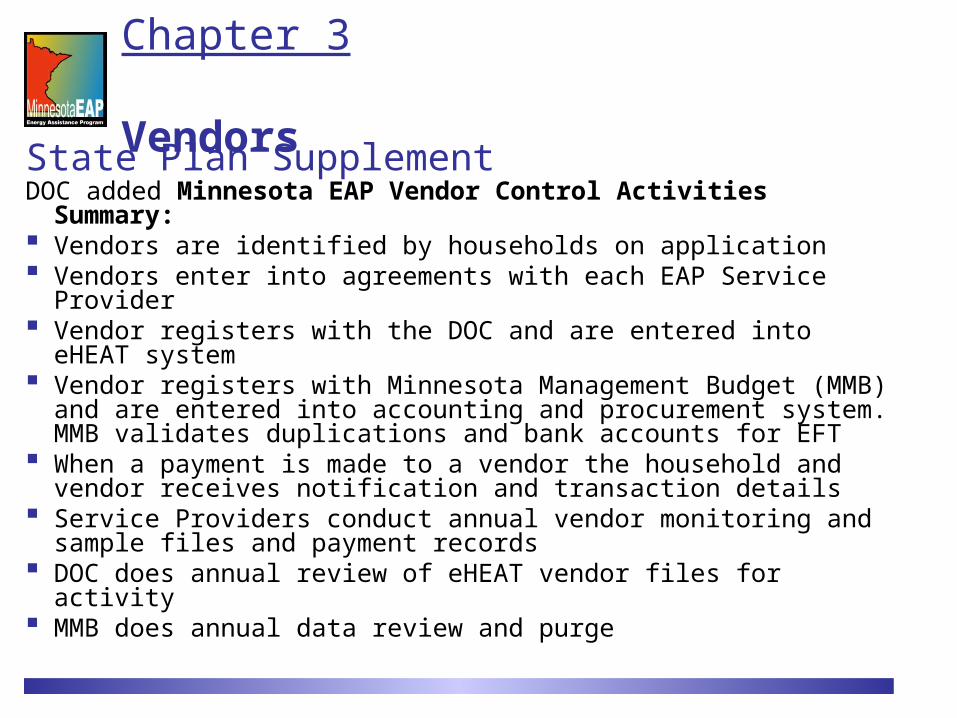

Chapter 3Vendors

State Plan Supplement DOC added Minnesota EAP Vendor Control Activities Summary: Vendors are identified by households on application Vendors enter into agreements with each EAP Service Provider Vendor registers with the DOC and are entered into eHEAT system Vendor registers with Minnesota Management Budget (MMB) and are

entered into accounting and procurement system. MMB validates duplications and bank accounts for EFT

When a payment is made to a vendor the household and vendor receives notification and transaction details

Service Providers conduct annual vendor monitoring and sample files and payment records

DOC does annual review of eHEAT vendor files for activity MMB does annual data review and purge

Chapter 3Vendors

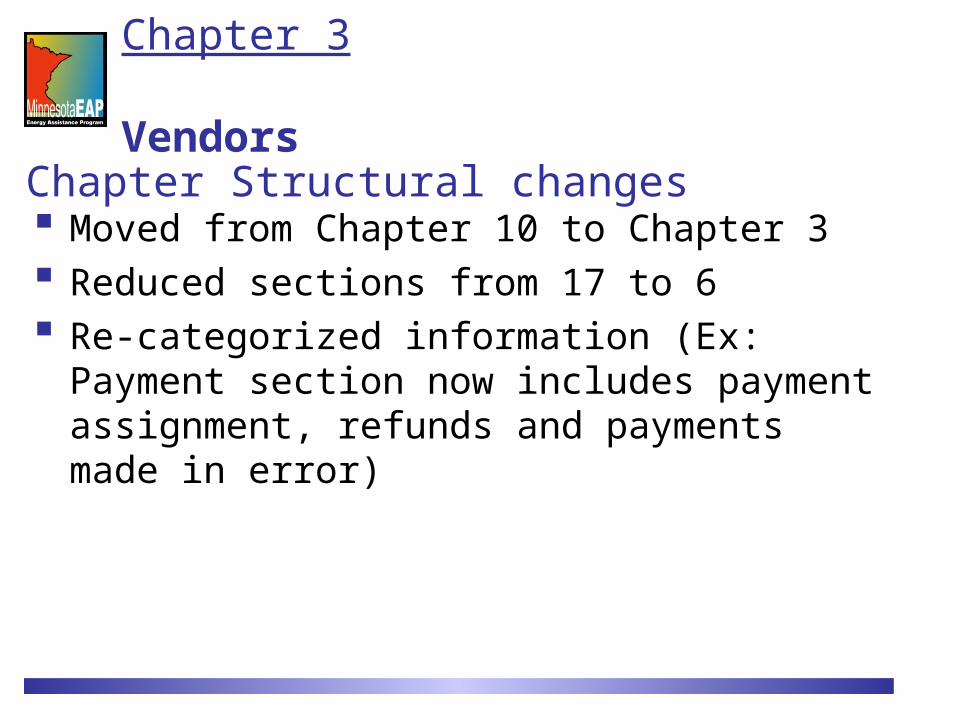

Chapter Structural changes Moved from Chapter 10 to Chapter 3 Reduced sections from 17 to 6 Re-categorized information (Ex: Payment section now

includes payment assignment, refunds and payments made in error)

Chapter 3Vendors

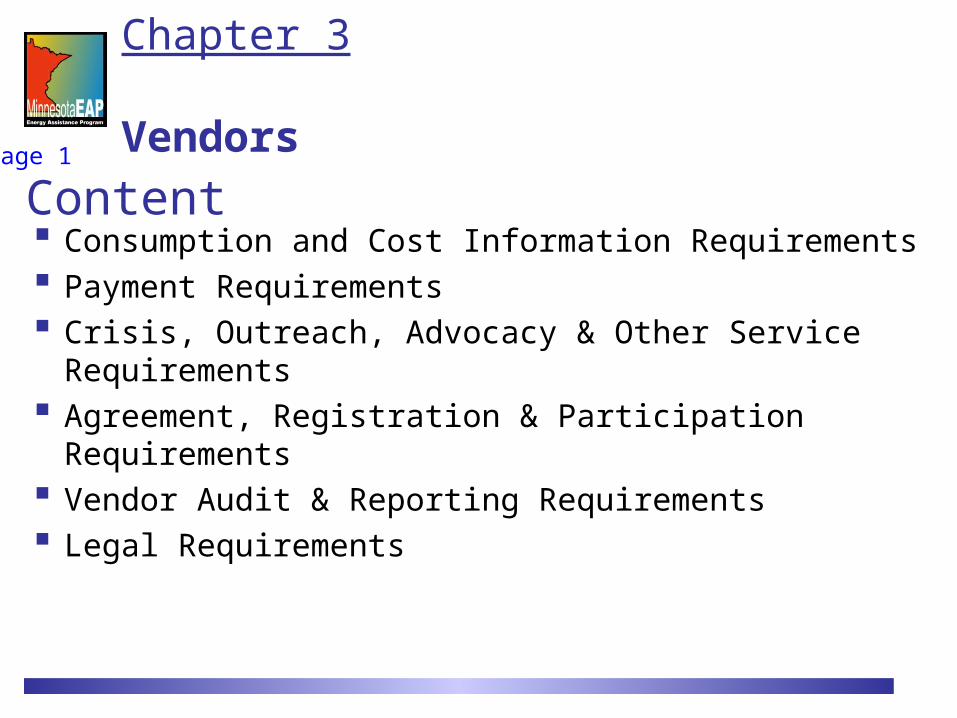

Content Consumption and Cost Information Requirements Payment Requirements Crisis, Outreach, Advocacy & Other Service Requirements Agreement, Registration & Participation Requirements Vendor Audit & Reporting Requirements Legal Requirements

Chapter 3Vendors

Page 1

Policy Manual Clarification

Chapter 3Vendors

Page 4

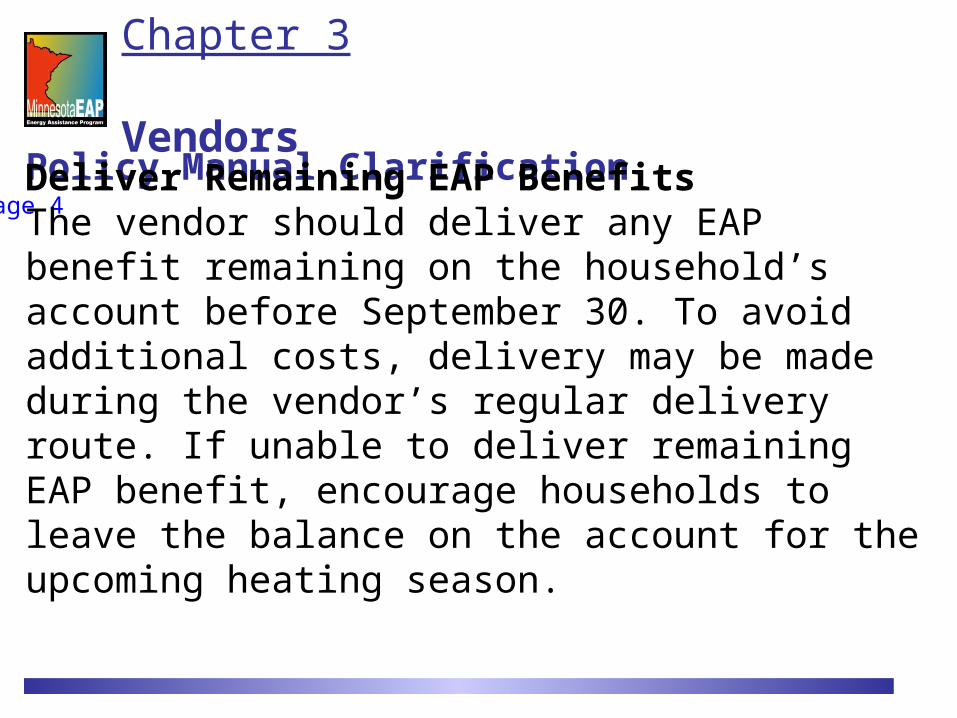

Deliver Remaining EAP BenefitsThe vendor should deliver any EAP benefit remaining on the household’s account before September 30. To avoid additional costs, delivery may be made during the vendor’s regular delivery route. If unable to deliver remaining EAP benefit, encourage households to leave the balance on the account for the upcoming heating season.

Delivered Fuels Refunds After September 30Part of overall efforts intended to: Optimize the use of funds for fuel, Reduce adverse public perception of the program

Approach Taken: Reduced promotion: Removed statement on letter saying household can

ask for refund after September 30 Advice HHD to use: SP & Vendors encourage households to keep EAP

credits in active vendor accounts for future energy costs. Deliver Credits pre-Sept. 30: SP work with delivered fuel vendors to

identify EAP households with credits and use remaining credits during the program year.

Chapter 3 (Also in Chapter 11)

Vendors

Delivered Fuels Refunds After September 30Coming Soon DOC will collect information to understand the size & nature in early

September This information will be used to report to stakeholders and to determine if

any future action is needed

Chapter 3 Vendors

Policy Manual Vendor Data Practices

Chapter 3Vendors

Page 8

Sharing EAP Private Data With Vendors . . . The private household data collected by EAP has restricted uses. Generally, an EAP household’s consent allows their data only to be used for determining and delivering EAP services. . . .

Any request for information must include an Informed Consent to Release Private Data signed by the household before requesting and receiving the information unless they are included in the EAP Application Permissions.

Additional information is available in Chapter 14: Data Practices and Records of the EAP Policy Manual.

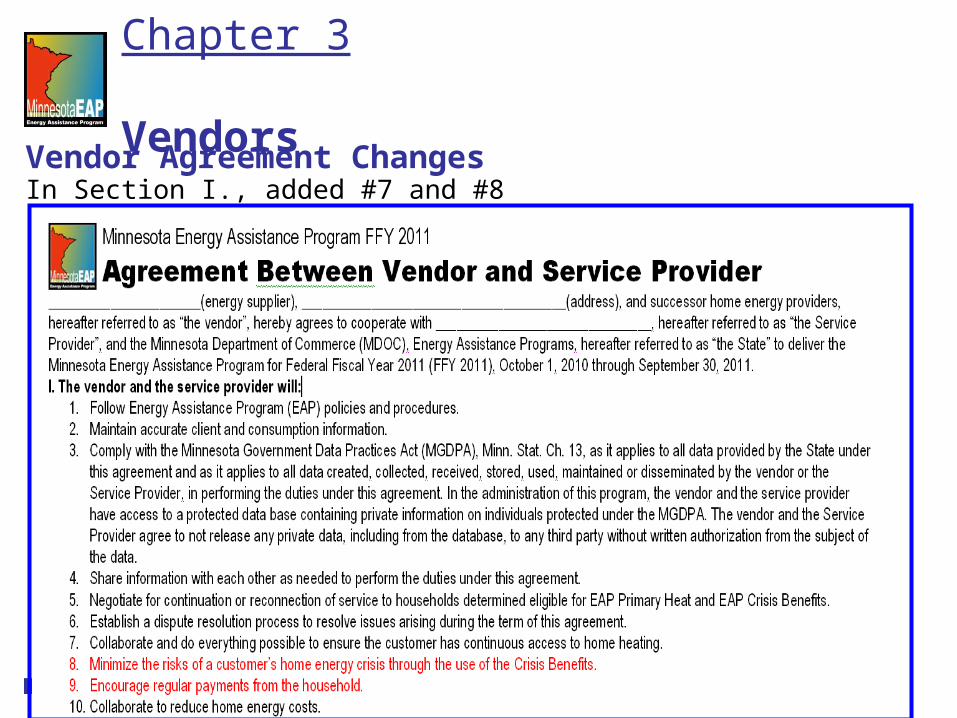

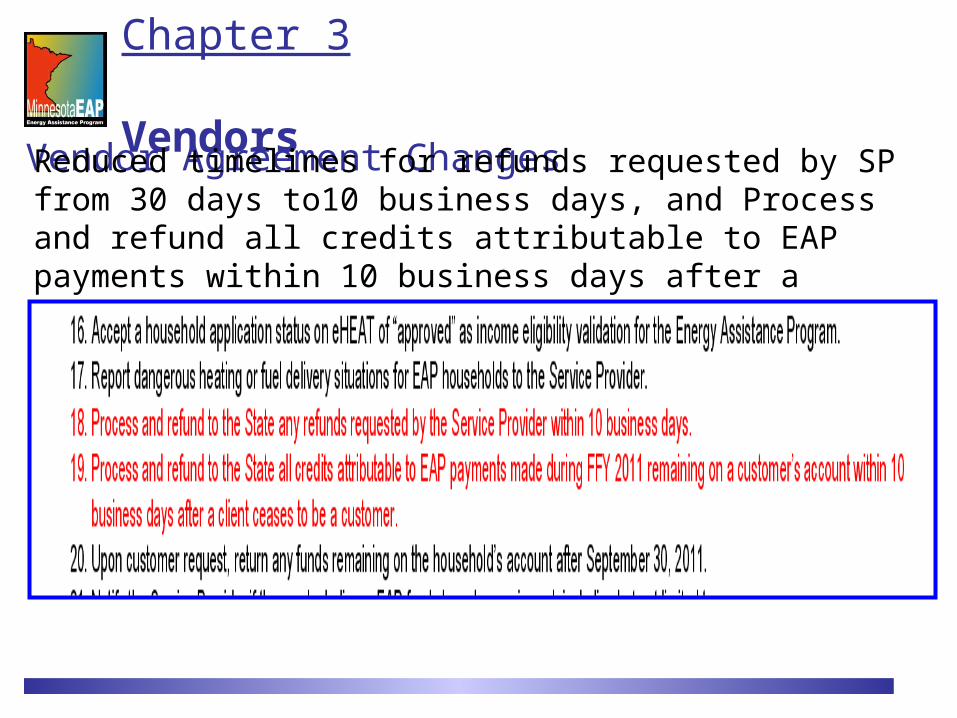

Vendor Agreement Changes

Chapter 3Vendors

In Section I., added #7 and #8

Vendor Agreement Changes

Chapter 3Vendors

Reduced timelines for refunds requested by SP from 30 days to10 business days, and Process and refund all credits attributable to EAP payments within 10 business days after a client ceases to be a customer.

Vendor Agreement Changes

Chapter 3Vendors

Removed statement about Vendor reporting difference of number of HHD members from App

Vendors Monitoring

Monitoring vendors is essential to ensure program quality and integrity. An EAP vendor is bound by the requirements of the LIHEAP Act and the Vendor Agreement. Monitoring can also assure vendors follow these rules. Service Providers are required to monitor vendors.

Chapter 3Vendors

Page 6

SP Monitoring HatSP Monitoring Hat SP act as a monitoring agent for EAP SP validate key transaction SP document findings, actions & outcomes Looking for incidents of error or fraud

Chapter 3Vendors

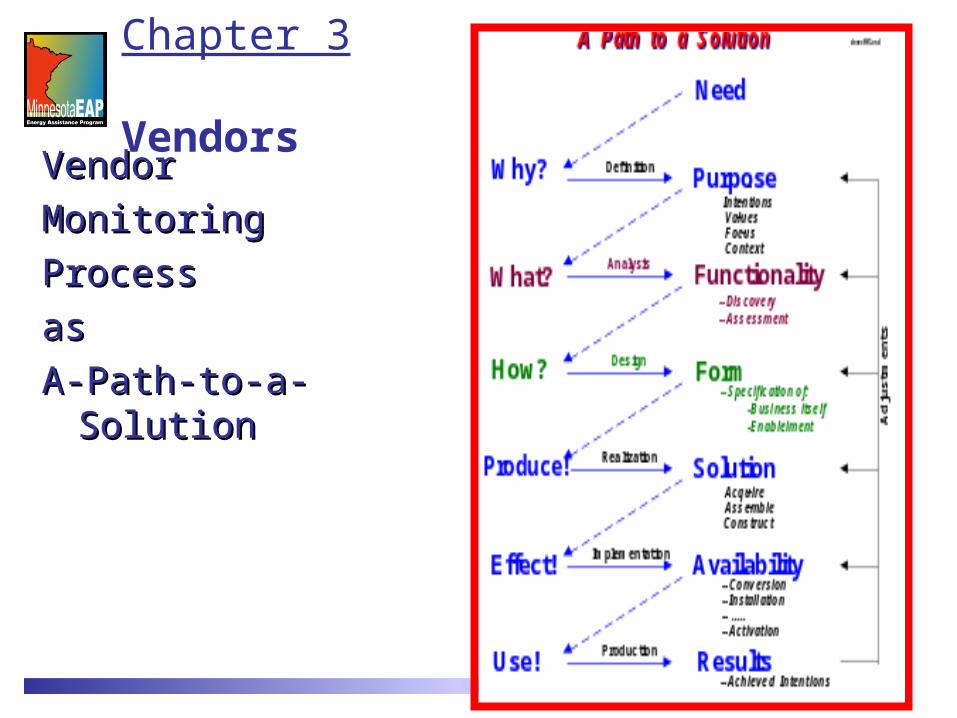

VendorVendor

Monitoring Monitoring

Process Process

as as A-Path-to-a- SolutionA-Path-to-a- Solution

Chapter 3Vendors

Definition Definition to ensure quality & Integrityto ensure quality & Integrity

Chapter 3Vendors

Steps, on Page 6, help detail scope

Vendors must allow the Service Provider and DOC access to their records for compliance monitoring. Monitoring includes verifying transactions between the vendor and the Service Provider. Including but not limited to cost information, application of payments to household accounts, billing to eligible households, providing equal services to EAP eligible households, and any or all other activities agreed to in the Vendor Agreement.

Page 6

Analysis Analysis is discovery & Assessmentis discovery & Assessment

Chapter 3Vendors

Take initial random sample If sample has issue, ask for larger sample. Additional

discovery as needed can include: Asking for explanation (In writing preferably) Monitor determines the size in discovery depends on the vendor or

risk level

Assess and specify the findings and their nature Errors can be one-off or systemic Do not start with fraud, if intent is questioned it is an investigation

Design Design is determining actionsis determining actions

Chapter 3Vendors

Design actions based on findings: If a one-off error occurrence, document and close If problem is systemic determine appropriate corrective

action If effect requires reparations to HHD harmed, determine

process If suspected fraud, develop an investigation and escalate

(Incident Report) and pursue as related to policy Document your requests and judgments

Realize Realize is acquiring solutionsis acquiring solutions

Chapter 3Vendors

Ask vendor to acquire, assemble or construct corrective actions

Vendor must construct solution SP can support and validate SP documents

Implement Implement is determining actionsis determining actions

Chapter 3Vendors

The vendor is responsible to implement solution SP Monitoring is responsible to support Vendor should communicate when it has been implemented SP should document vendor communication

Production Production is desired effectis desired effect

Chapter 3Vendors

Follow up to determine if issue is corrected May be next years visit or soon into the program year Follow up depends on the risk related to severity of

impact and probability of occurrence

Rules of thumb Vendors Monitoring Documentation is key

Keep to the facts and have vendor document responses SP files are the program records

Team with other SP when effective Follow up (Next year or sooner as needed) Ask Field Representatives for help Escalate as needed. May need to at any step in

process

Chapter 3Vendors

Issue ManagementIssue Management (Vendor)Vendor) Vendors need to work directly with SP It is not effective for DOC manage local relationships Talk it through, describe what you are seeing Work issues through the “Path” (but less formal) Team with other SP Escalate as needed. (FR can help ID these times to

escalate)

Chapter 3Vendors

If you find a record has changed during year or during monitoring Ask the vendor for the explanation Do discover and assessment Follow “Path” based on findings

Consumption Record Changes

Chapter 3Vendors

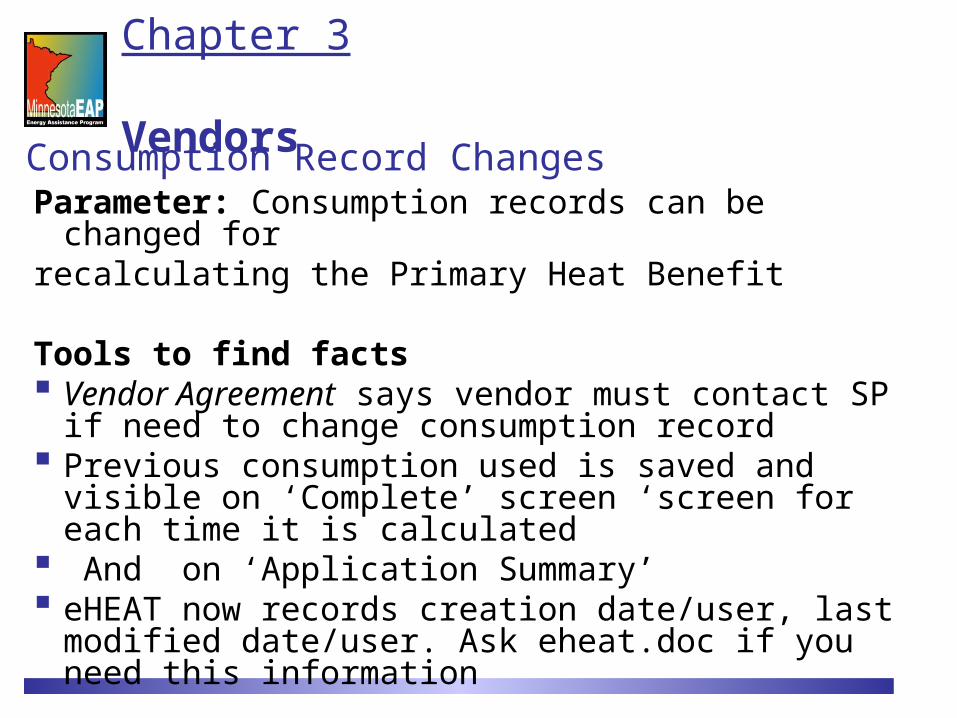

Parameter: Consumption records can be changed forrecalculating the Primary Heat Benefit

Tools to find facts Vendor Agreement says vendor must contact SP if need

to change consumption record Previous consumption used is saved and visible on

‘Complete’ screen ‘screen for each time it is calculated And on ‘Application Summary’ eHEAT now records creation date/user, last modified

date/user. Ask eheat.doc if you need this information

Consumption Record Changes

Chapter 3Vendors

Ken Benson

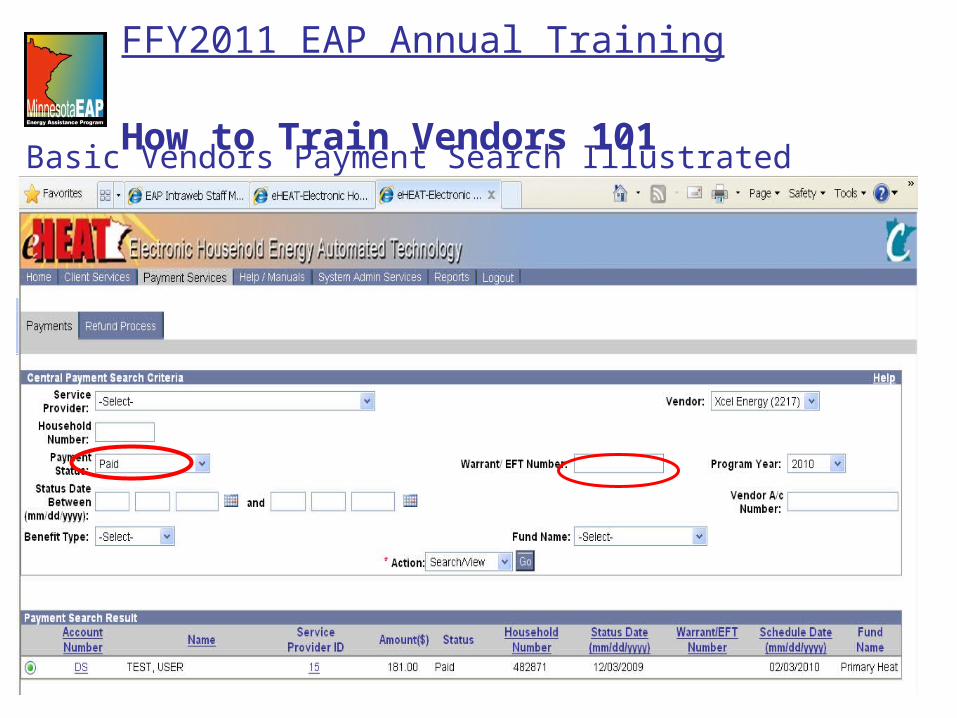

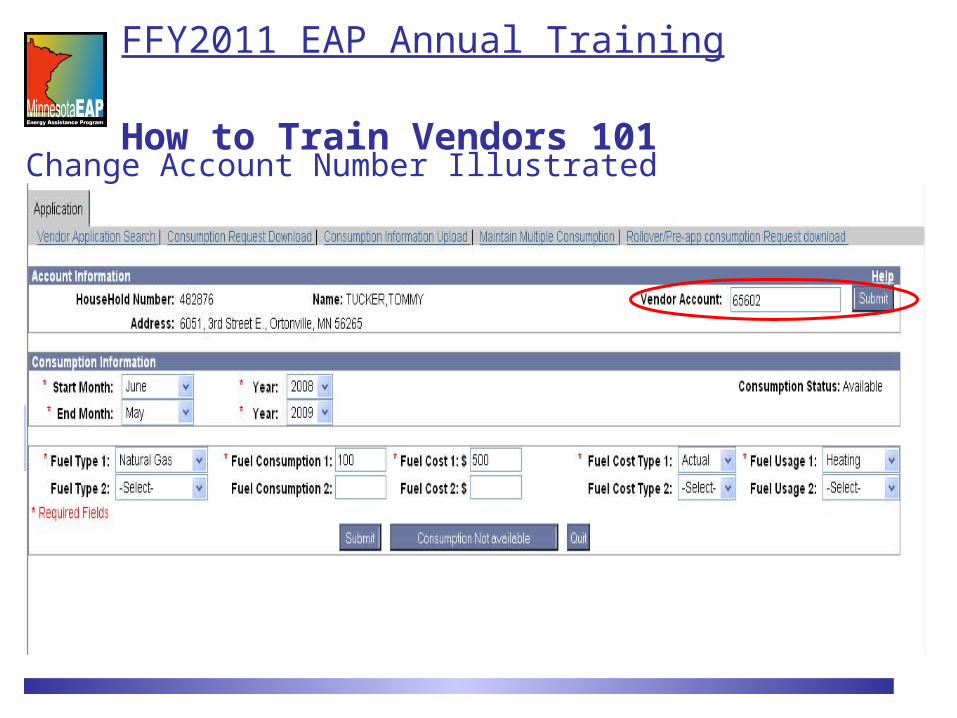

FFY2011 EAP Annual TrainingHow to Train Vendors 101

Go to ‘Payments’ menu Demonstrate one criteria Explain other criteria only if you think they are relevant

to the particular vendor Demonstrate export (if relevant) Look at results – point out EFT # Show how to enter EFT in search criteria

FFY2011 EAP Annual TrainingHow to Train Vendors 101

Basic Payment Step-By-Step

Basic Vendors Payment Search Illustrated

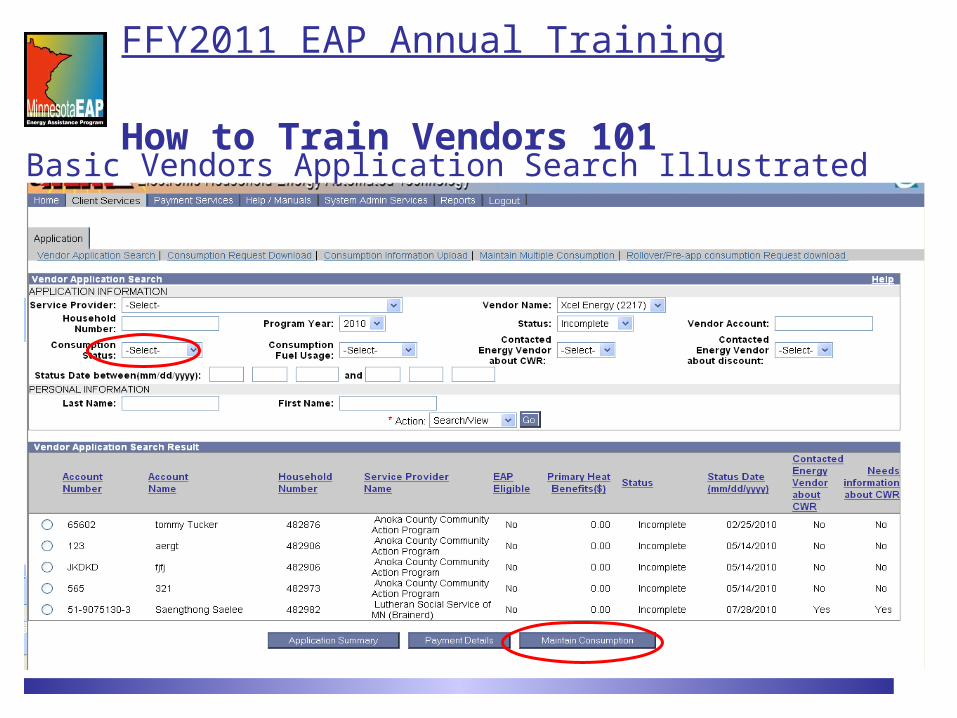

FFY2011 EAP Annual TrainingHow to Train Vendors 101

Go to ‘Application’ tab Click go Be specific about what Benefits mean Consumption Vendor customer number edit

FFY2011 EAP Annual TrainingHow to Train Vendors 101

Basics Application Step-By-Step

Basic Vendors Application Search Illustrated

FFY2011 EAP Annual TrainingHow to Train Vendors 101

FFY2011 EAP Annual TrainingHow to Train Vendors 101

Change Account Number Illustrated

Cold Weather RuleEnergy Assistance Program Fall TrainingAugust 11, 2010

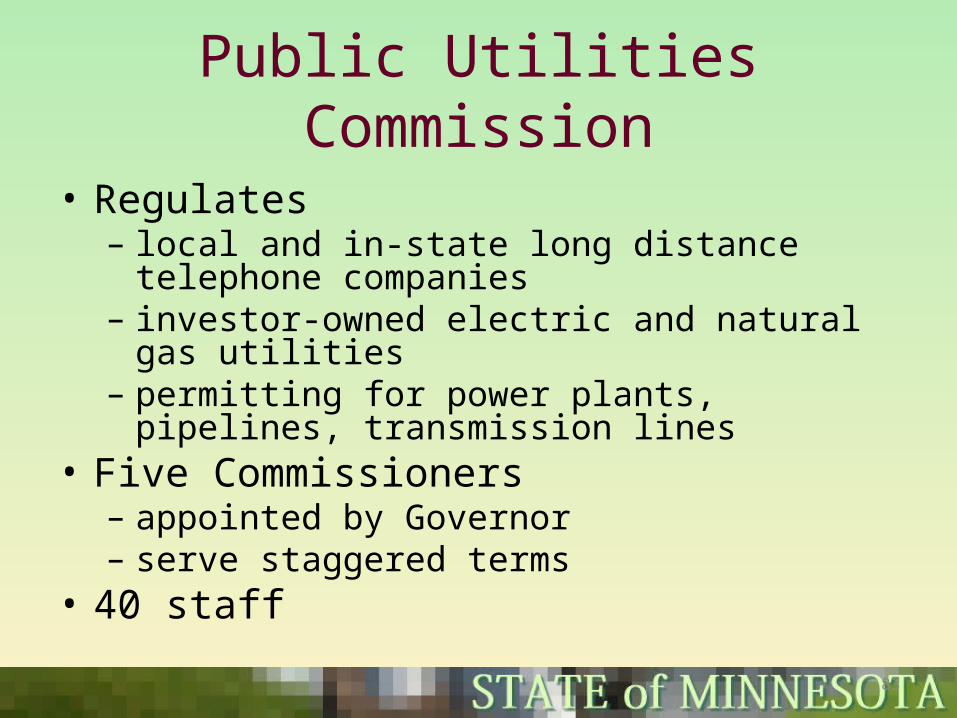

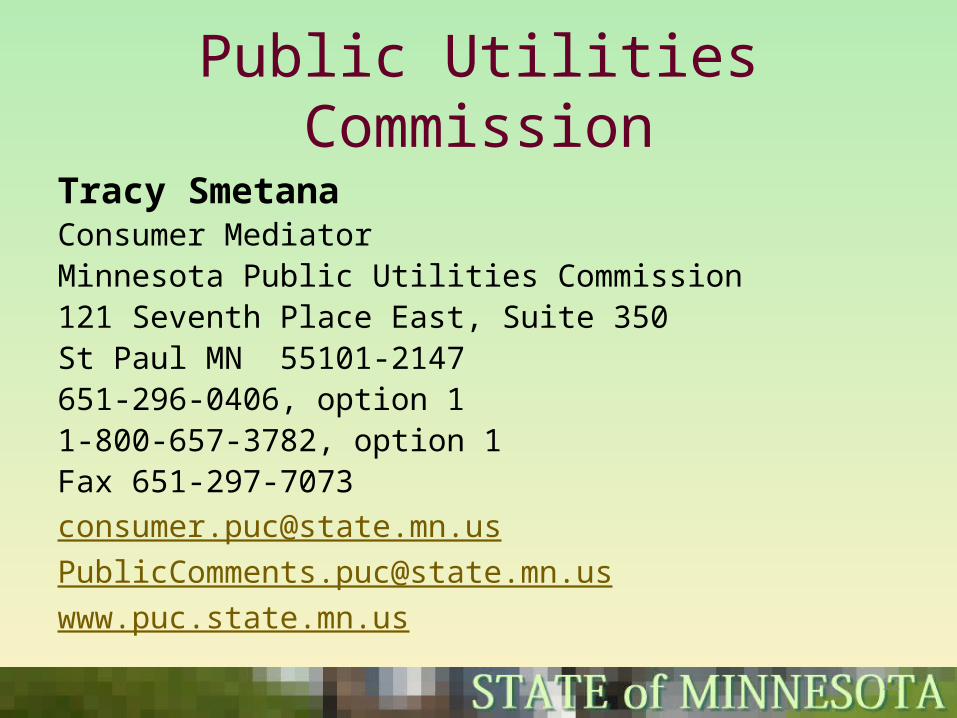

Public Utilities CommissionTracy Smetana

82

Public Utilities Commission

• Regulates – local and in-state long distance telephone

companies– investor-owned electric and natural gas

utilities– permitting for power plants, pipelines,

transmission lines• Five Commissioners – appointed by Governor– serve staggered terms

• 40 staff

83

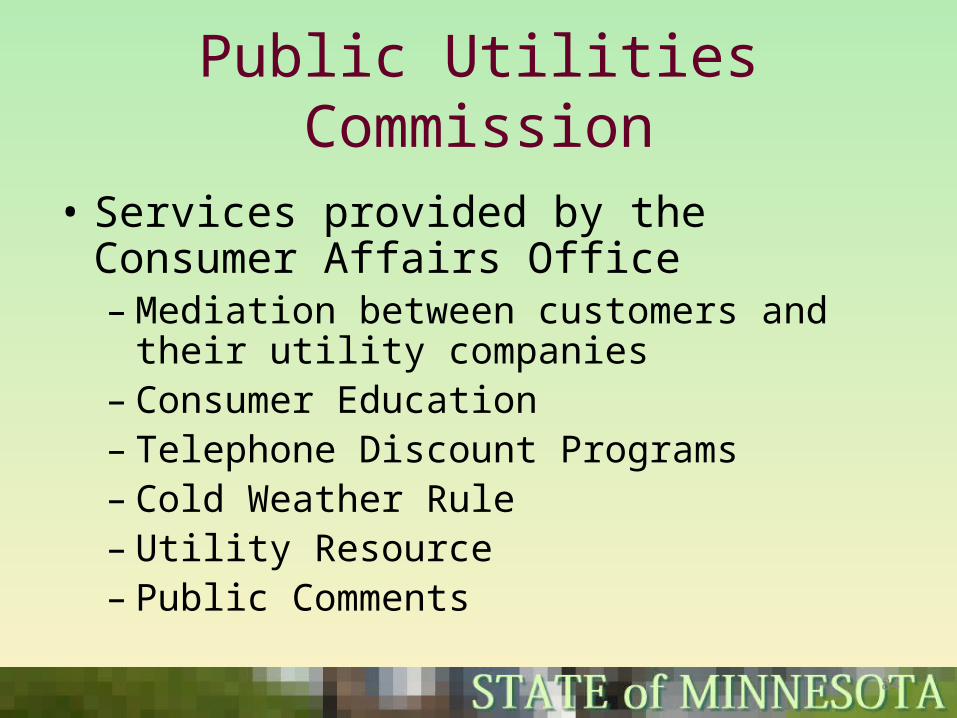

Public Utilities Commission

• Services provided by the Consumer Affairs Office–Mediation between customers and their

utility companies– Consumer Education– Telephone Discount Programs– Cold Weather Rule– Utility Resource– Public Comments

84

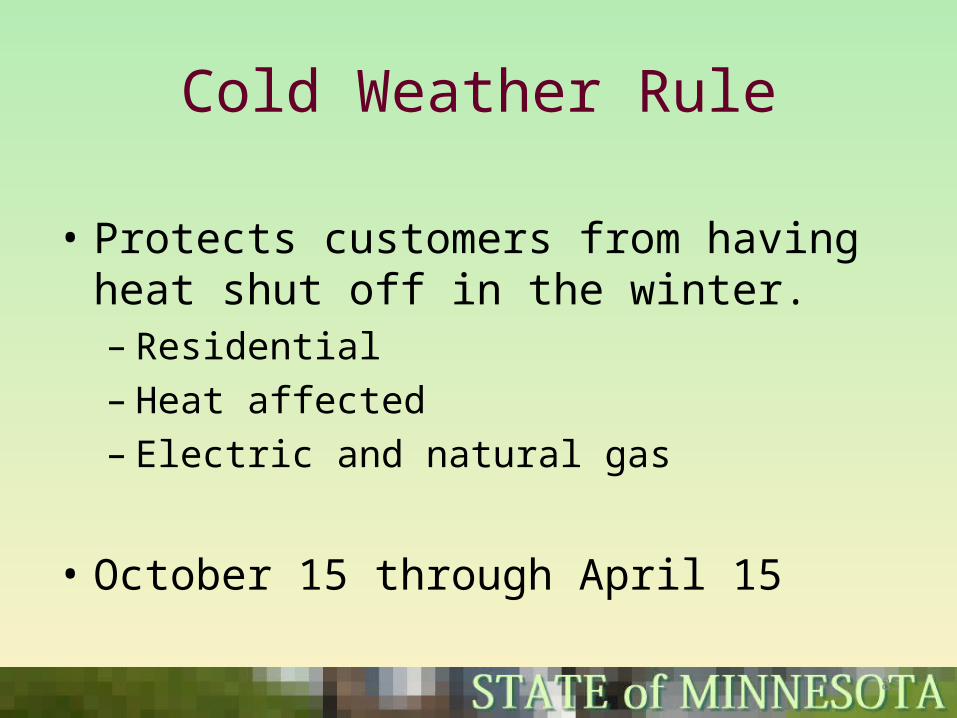

Cold Weather Rule

• Protects customers from having heat shut off in the winter.– Residential– Heat affected– Electric and natural gas

• October 15 through April 15

85

Cold Weather Rule

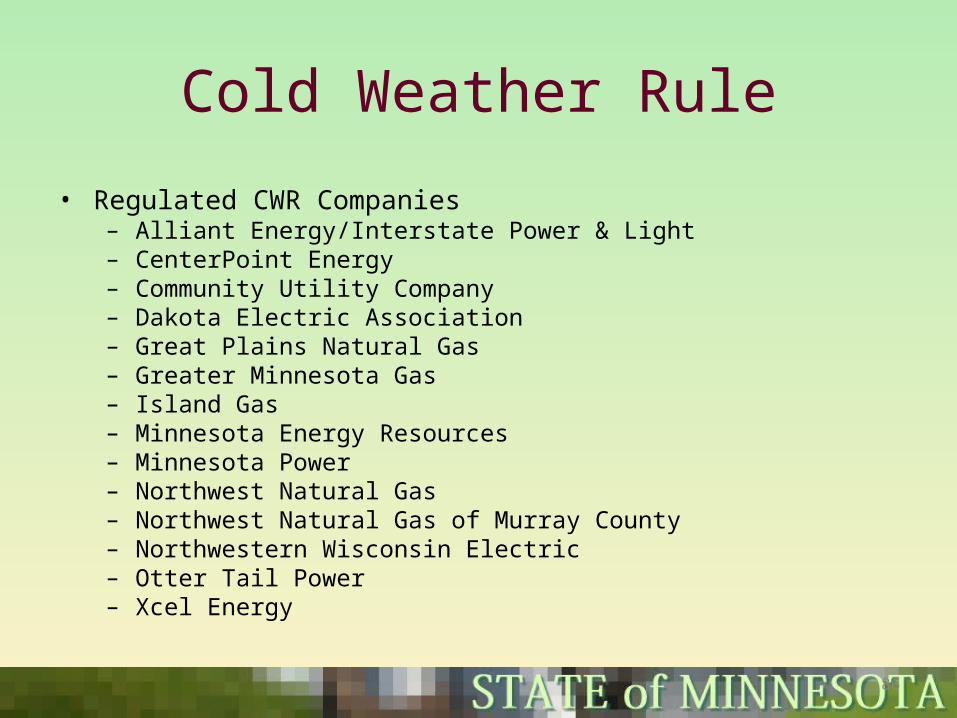

• Regulated CWR Companies– Alliant Energy/Interstate Power & Light– CenterPoint Energy– Community Utility Company– Dakota Electric Association– Great Plains Natural Gas– Greater Minnesota Gas– Island Gas– Minnesota Energy Resources– Minnesota Power– Northwest Natural Gas– Northwest Natural Gas of Murray County– Northwestern Wisconsin Electric– Otter Tail Power– Xcel Energy

86

Cold Weather Rule

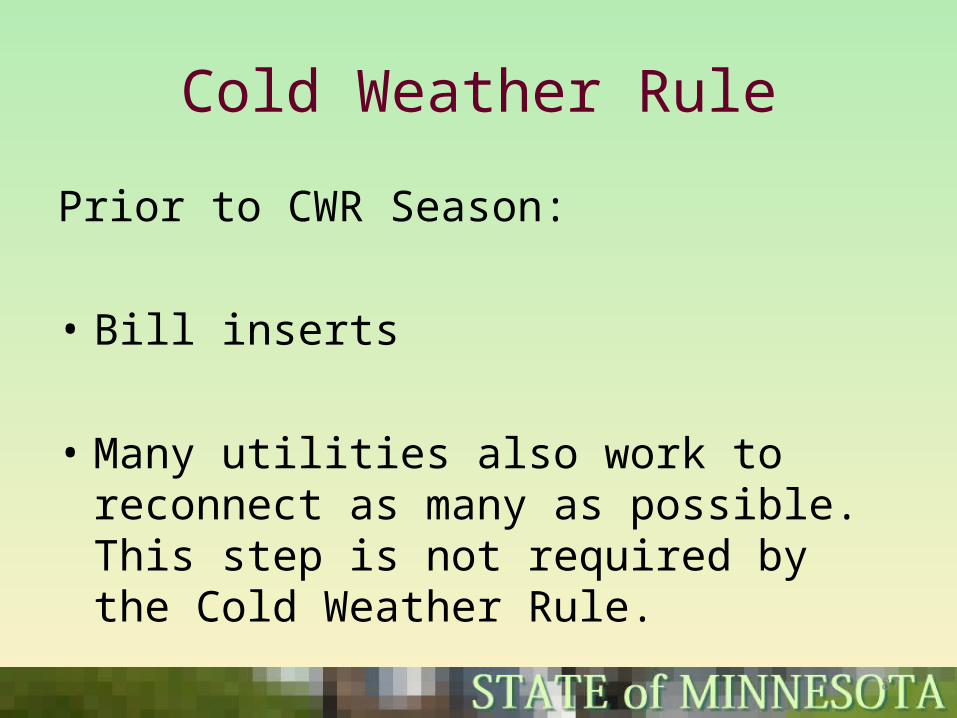

Prior to CWR Season:

• Bill inserts

• Many utilities also work to reconnect as many as possible. This step is not required by the Cold Weather Rule.

87

Cold Weather Rule

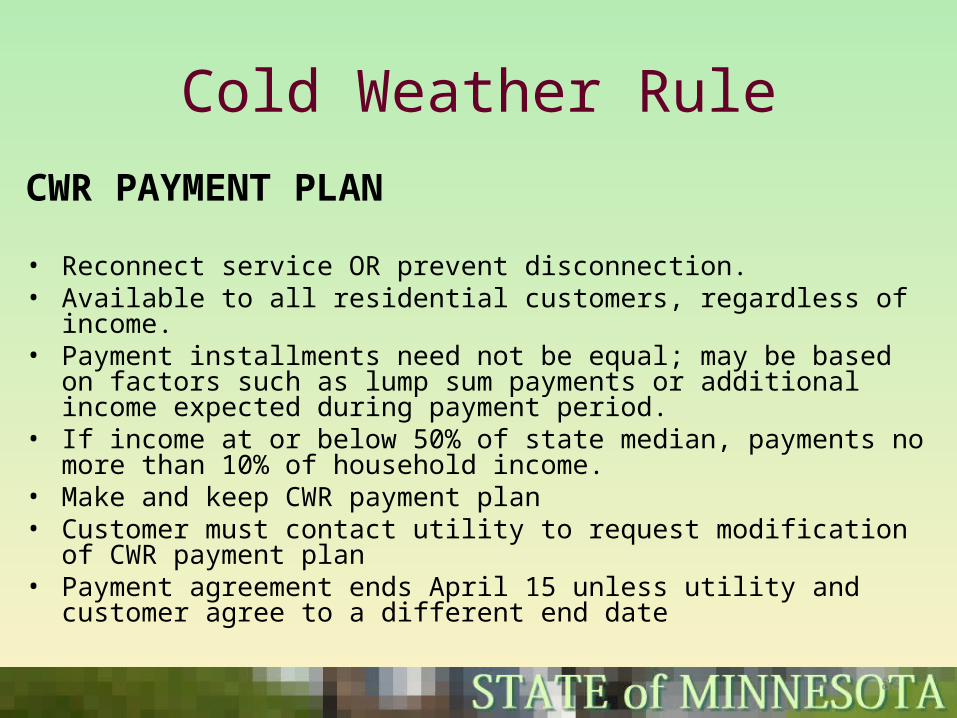

CWR PAYMENT PLAN

• Reconnect service OR prevent disconnection.• Available to all residential customers, regardless of income.• Payment installments need not be equal; may be based on

factors such as lump sum payments or additional income expected during payment period.

• If income at or below 50% of state median, payments no more than 10% of household income.

• Make and keep CWR payment plan• Customer must contact utility to request modification of CWR

payment plan• Payment agreement ends April 15 unless utility and customer

agree to a different end date

88

Cold Weather Rule

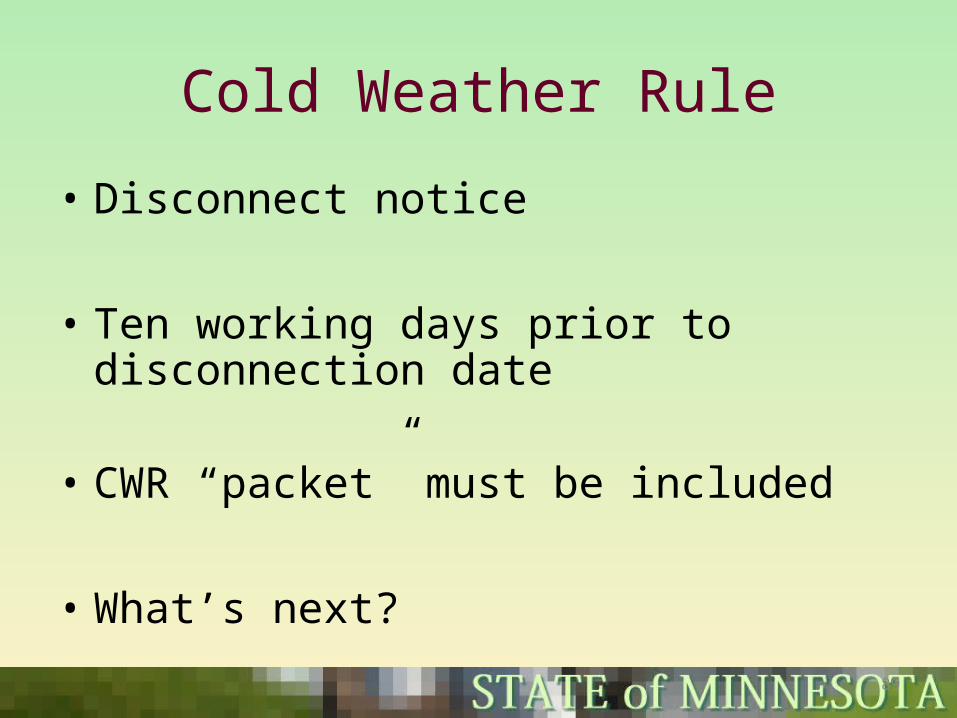

• Disconnect notice

• Ten working days prior to disconnection date

• CWR “packet” must be included

• What’s next?

89

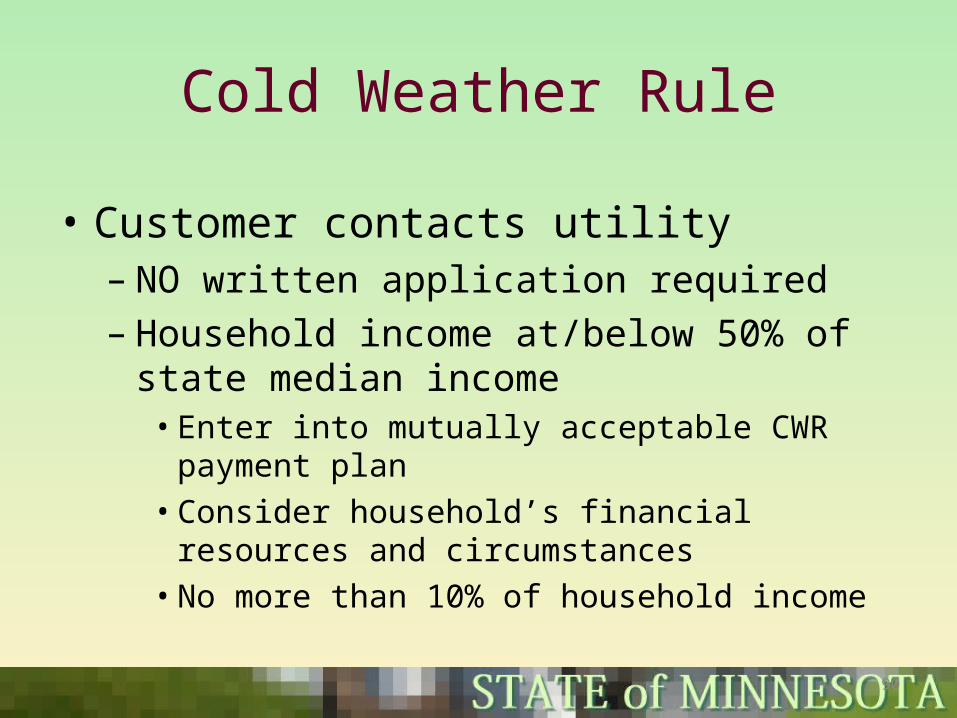

Cold Weather Rule

• Customer contacts utility– NO written application required– Household income at/below 50% of state

median income• Enter into mutually acceptable CWR

payment plan• Consider household’s financial resources

and circumstances• No more than 10% of household income

90

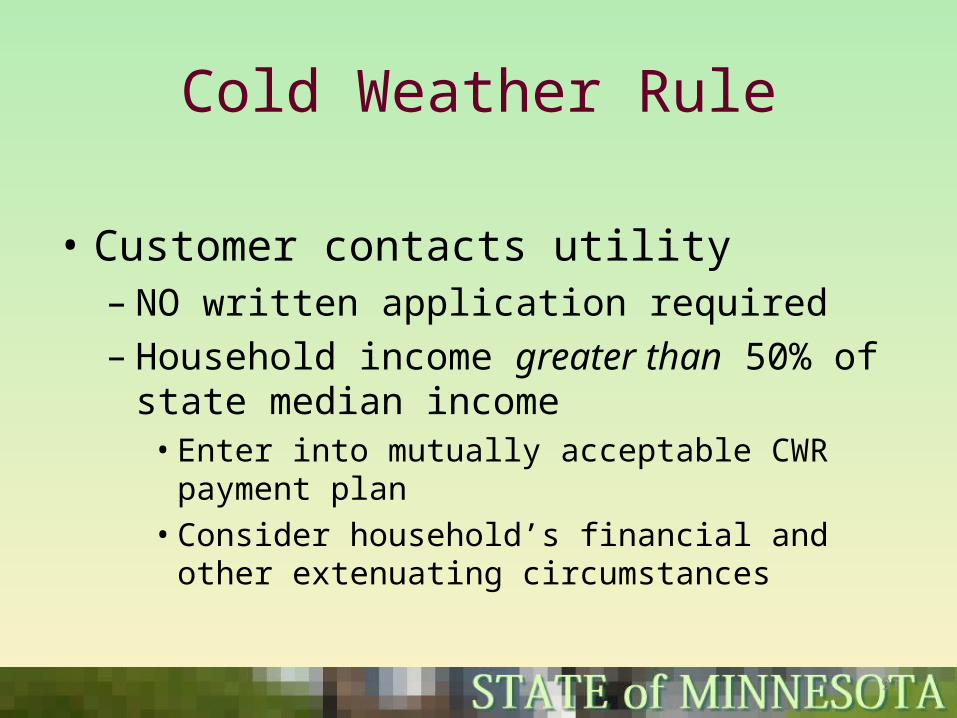

Cold Weather Rule

• Customer contacts utility– NO written application required– Household income greater than 50% of

state median income• Enter into mutually acceptable CWR

payment plan• Consider household’s financial and other

extenuating circumstances

91

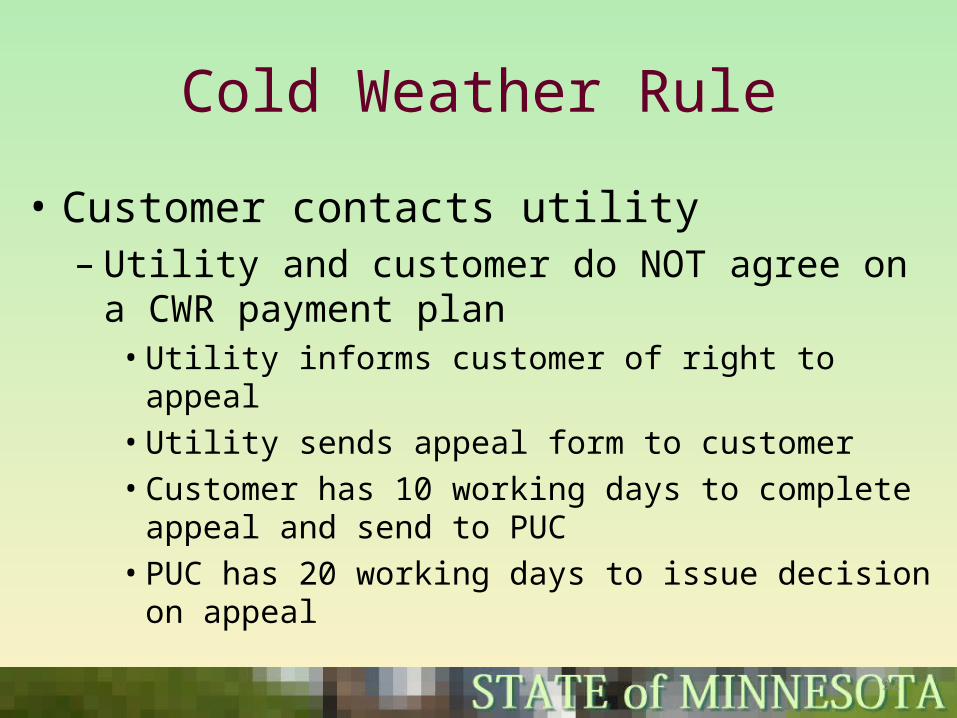

Cold Weather Rule

• Customer contacts utility– Utility and customer do NOT agree on a

CWR payment plan• Utility informs customer of right to appeal• Utility sends appeal form to customer• Customer has 10 working days to complete

appeal and send to PUC• PUC has 20 working days to issue decision on

appeal

92

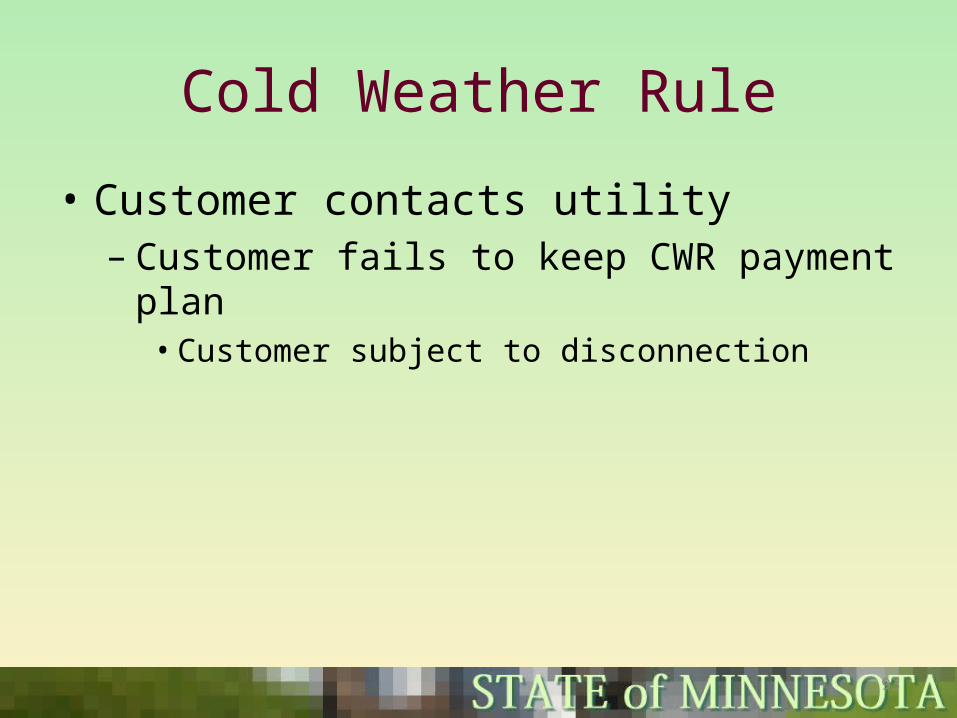

Cold Weather Rule

• Customer contacts utility– Customer fails to keep CWR payment

plan• Customer subject to disconnection

93

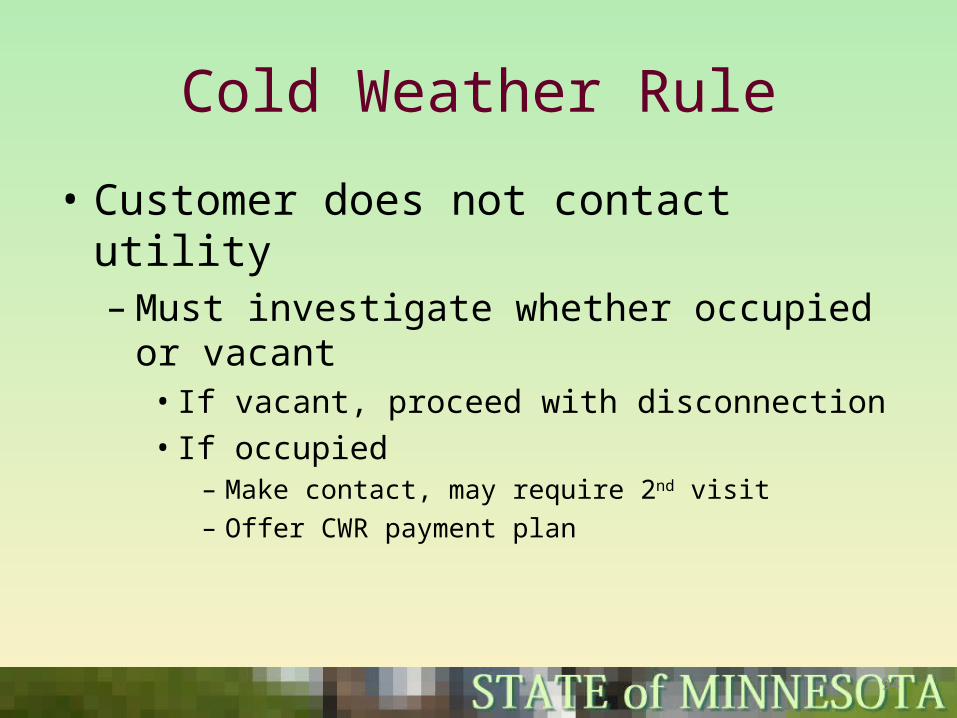

Cold Weather Rule

• Customer does not contact utility–Must investigate whether occupied or

vacant• If vacant, proceed with disconnection• If occupied

– Make contact, may require 2nd visit– Offer CWR payment plan

94

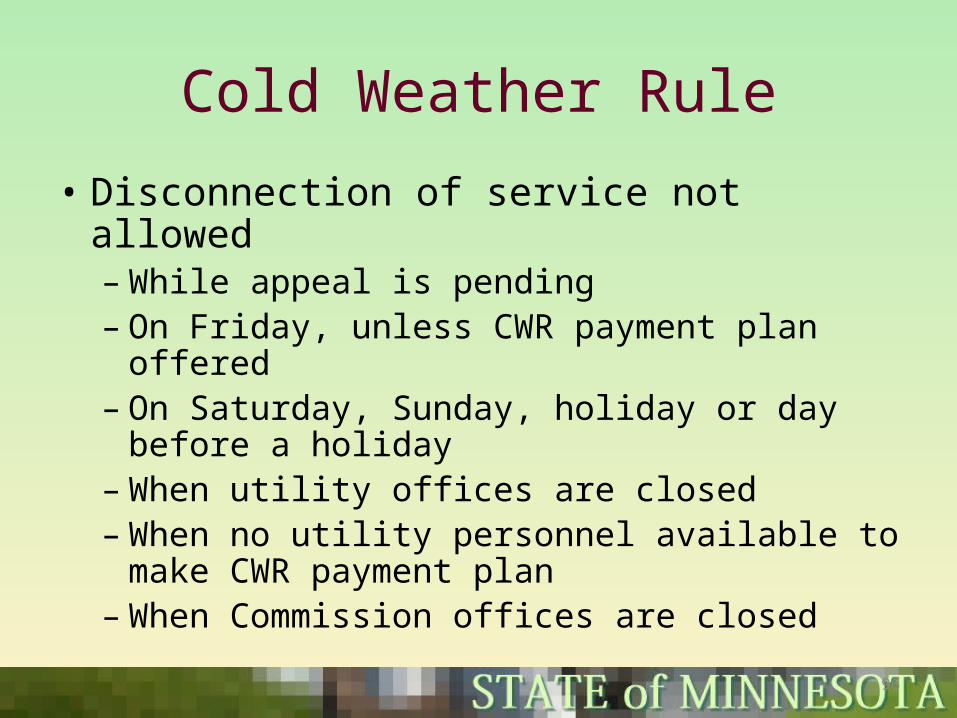

Cold Weather Rule

• Disconnection of service not allowed –While appeal is pending– On Friday, unless CWR payment plan

offered – On Saturday, Sunday, holiday or day

before a holiday–When utility offices are closed–When no utility personnel available to

make CWR payment plan–When Commission offices are closed

96

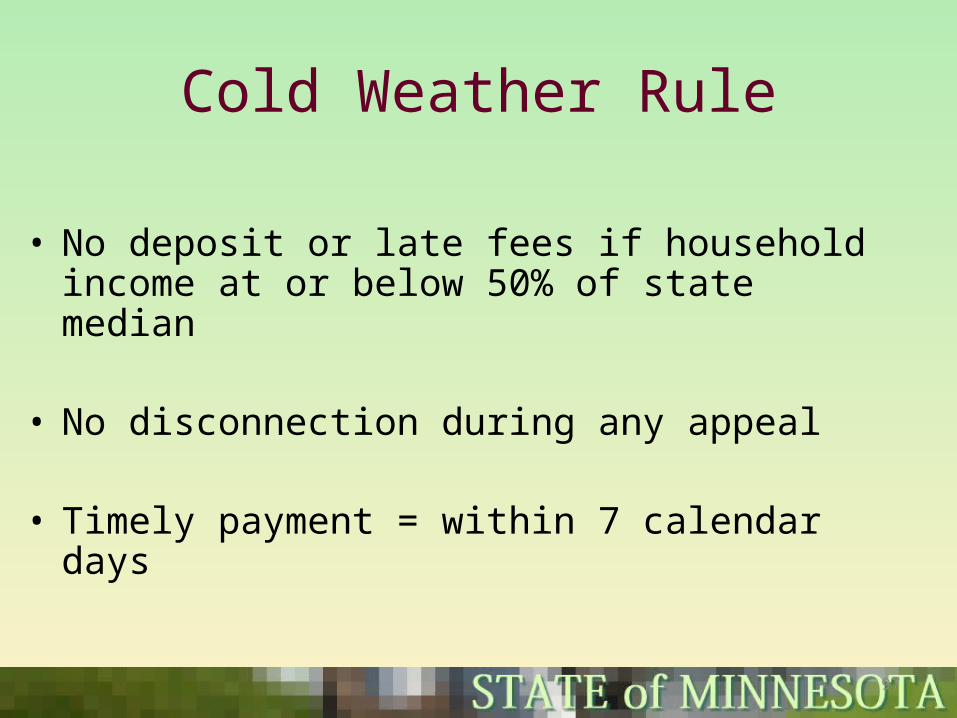

Cold Weather Rule

• No deposit or late fees if household income at or below 50% of state median

• No disconnection during any appeal

• Timely payment = within 7 calendar days

97

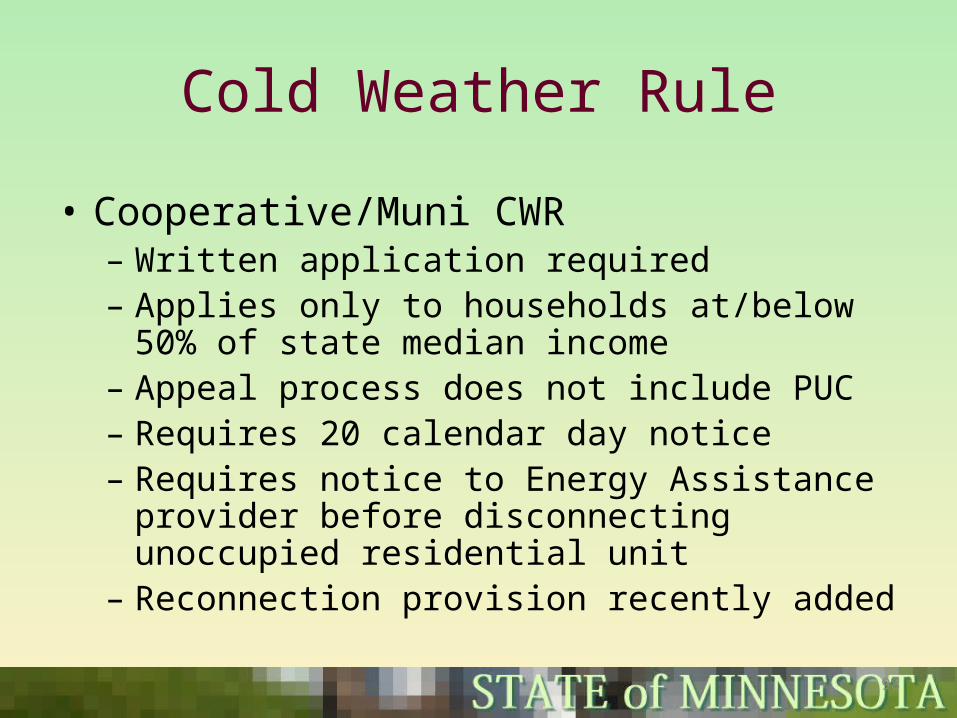

Cold Weather Rule

• Cooperative/Muni CWR– Written application required– Applies only to households at/below 50% of

state median income– Appeal process does not include PUC– Requires 20 calendar day notice– Requires notice to Energy Assistance

provider before disconnecting unoccupied residential unit

– Reconnection provision recently added

98

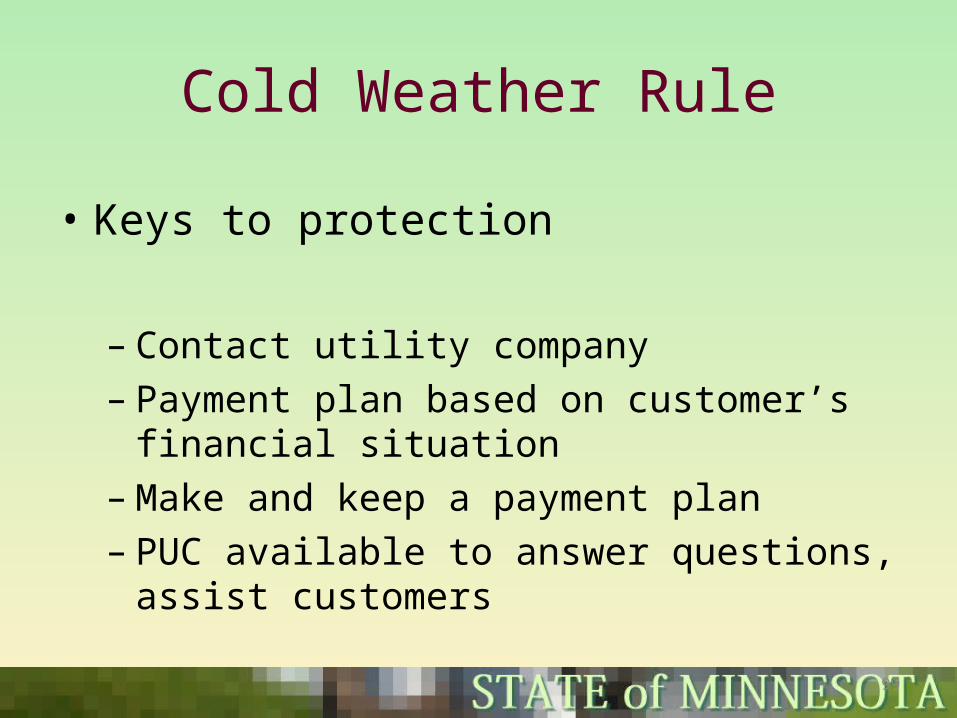

Cold Weather Rule

• Keys to protection

– Contact utility company– Payment plan based on customer’s

financial situation–Make and keep a payment plan– PUC available to answer questions,

assist customers

99

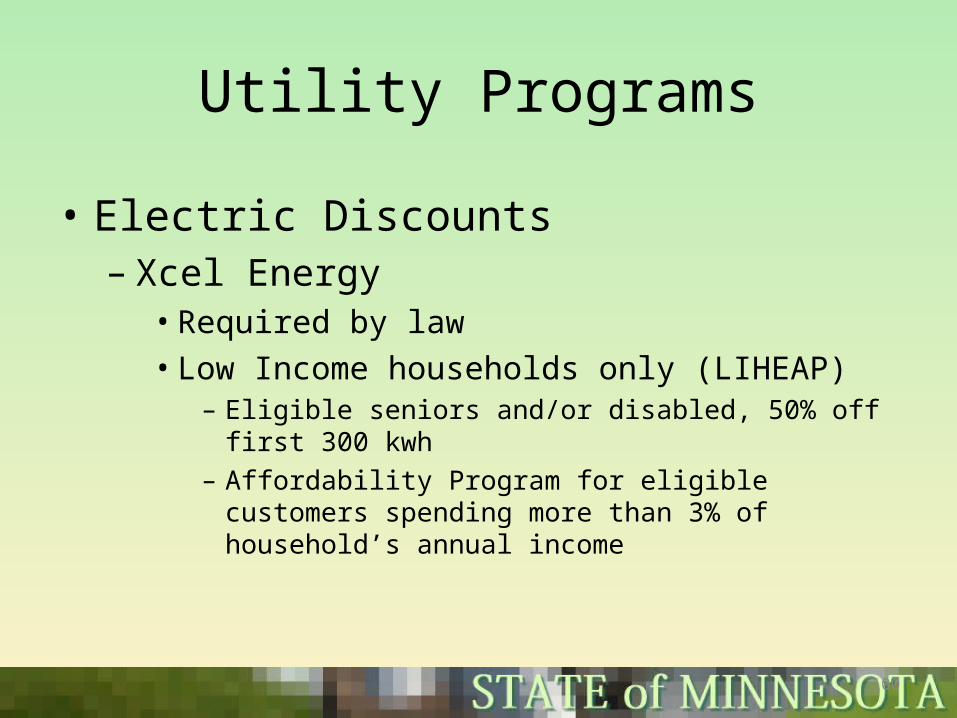

Utility Programs

• Electric Discounts– Xcel Energy• Required by law• Low Income households only (LIHEAP)

– Eligible seniors and/or disabled, 50% off first 300 kwh

– Affordability Program for eligible customers spending more than 3% of household’s annual income

100

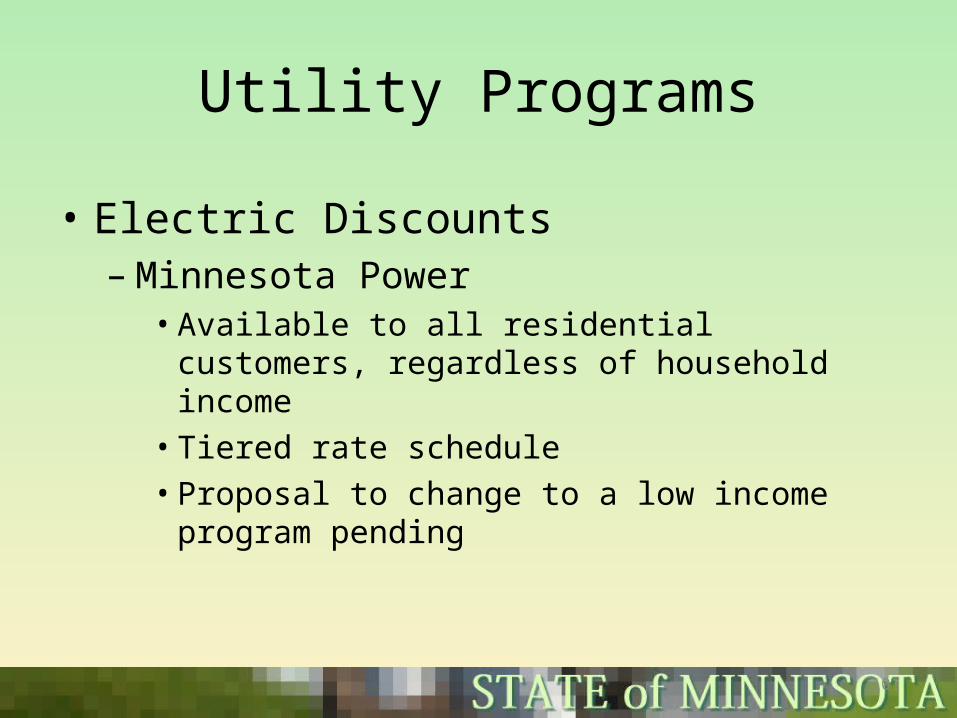

Utility Programs

• Electric Discounts–Minnesota Power• Available to all residential customers,

regardless of household income• Tiered rate schedule• Proposal to change to a low income program

pending

101

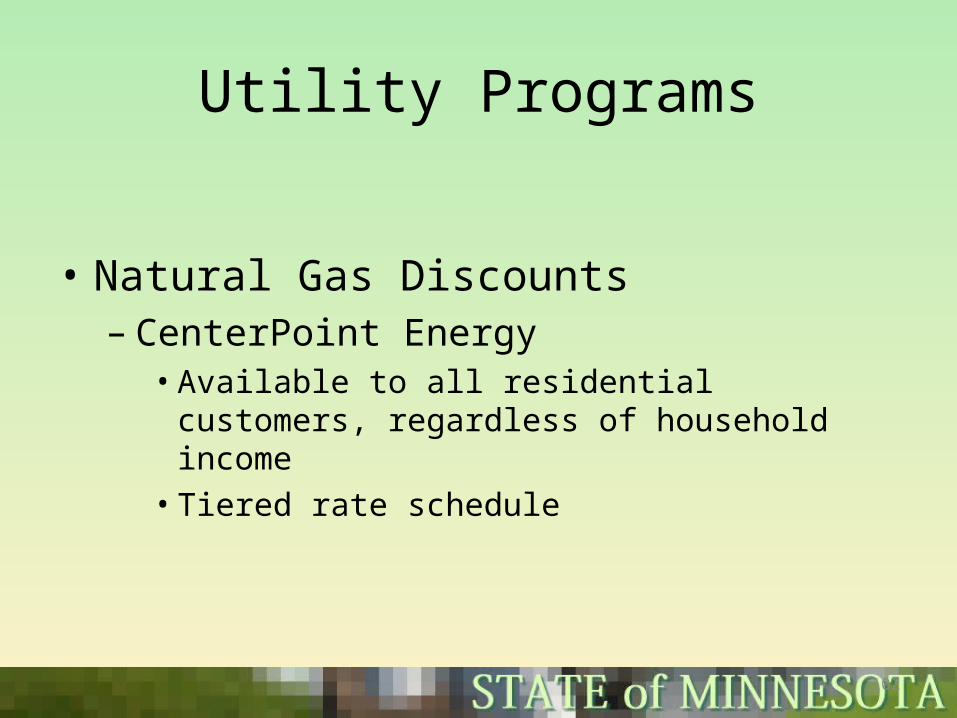

Utility Programs

• Natural Gas Discounts– CenterPoint Energy• Available to all residential customers,

regardless of household income• Tiered rate schedule

102

Utility Programs

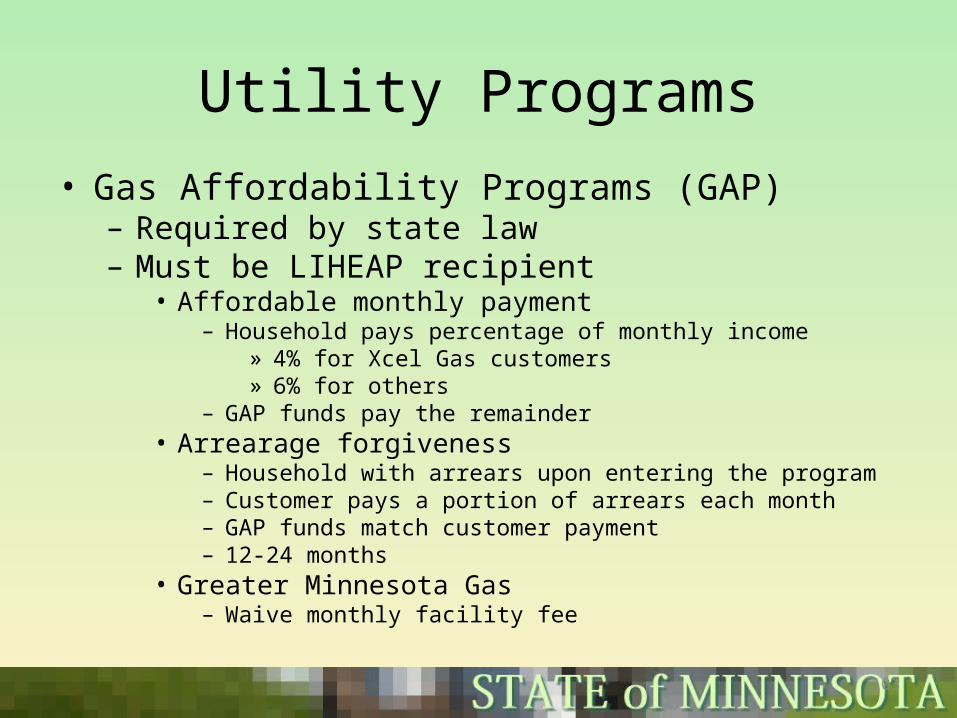

• Gas Affordability Programs (GAP)– Required by state law– Must be LIHEAP recipient

• Affordable monthly payment– Household pays percentage of monthly income

» 4% for Xcel Gas customers» 6% for others

– GAP funds pay the remainder• Arrearage forgiveness

– Household with arrears upon entering the program– Customer pays a portion of arrears each month– GAP funds match customer payment– 12-24 months

• Greater Minnesota Gas– Waive monthly facility fee

103

Utility Programs

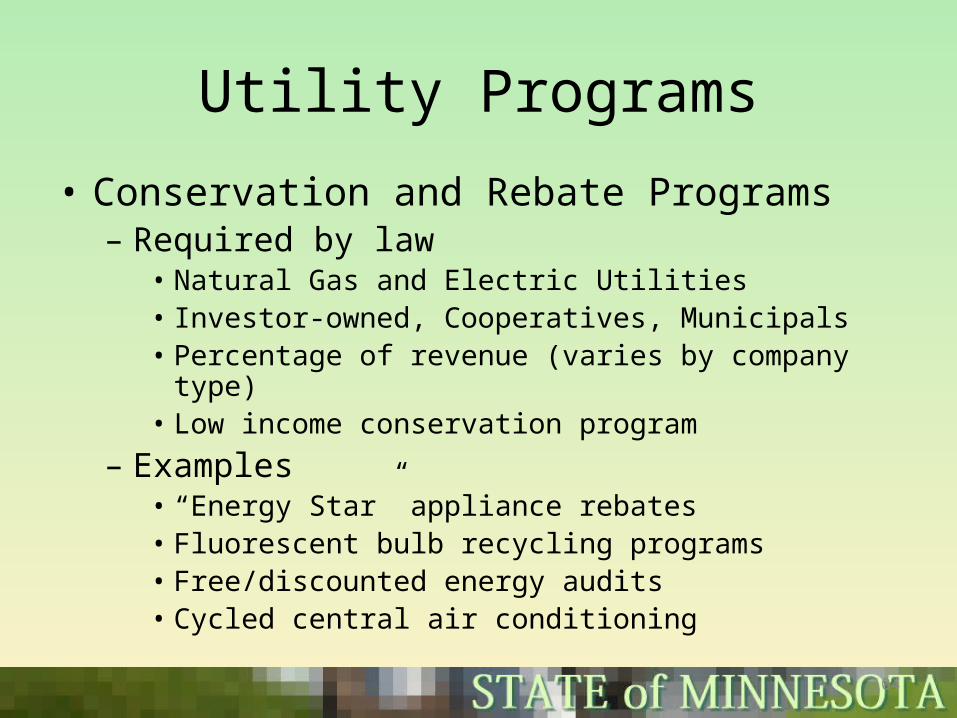

• Conservation and Rebate Programs– Required by law

• Natural Gas and Electric Utilities• Investor-owned, Cooperatives, Municipals• Percentage of revenue (varies by company type)• Low income conservation program

– Examples• “Energy Star” appliance rebates• Fluorescent bulb recycling programs• Free/discounted energy audits• Cycled central air conditioning

104

Life Support Households

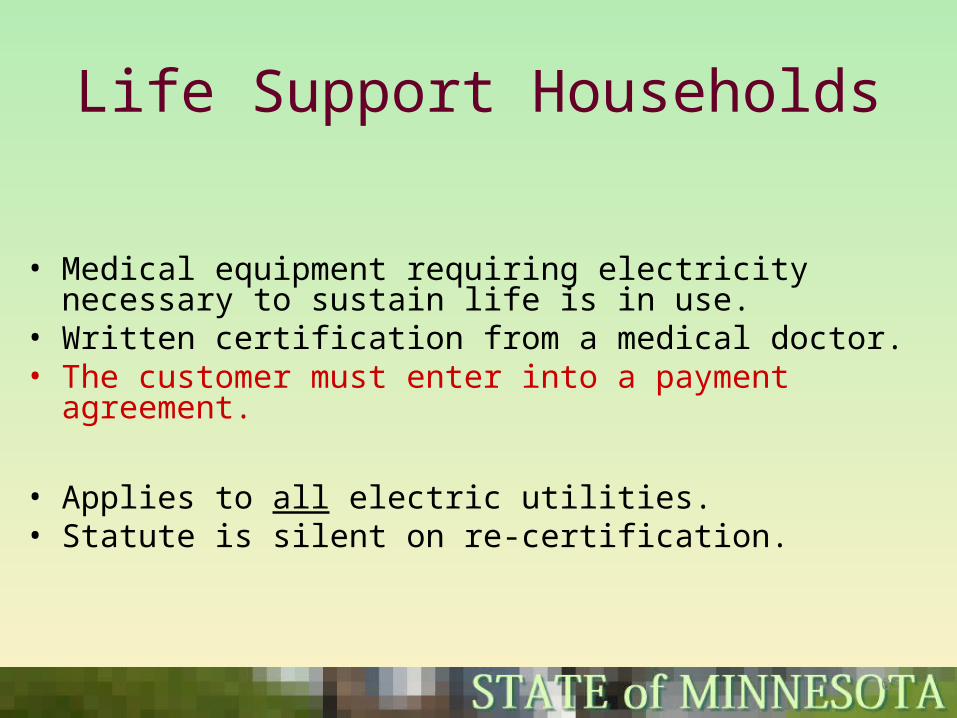

• Medical equipment requiring electricity necessary to sustain life is in use.

• Written certification from a medical doctor. • The customer must enter into a payment

agreement.

• Applies to all electric utilities.• Statute is silent on re-certification.

105

Hot Weather Rule

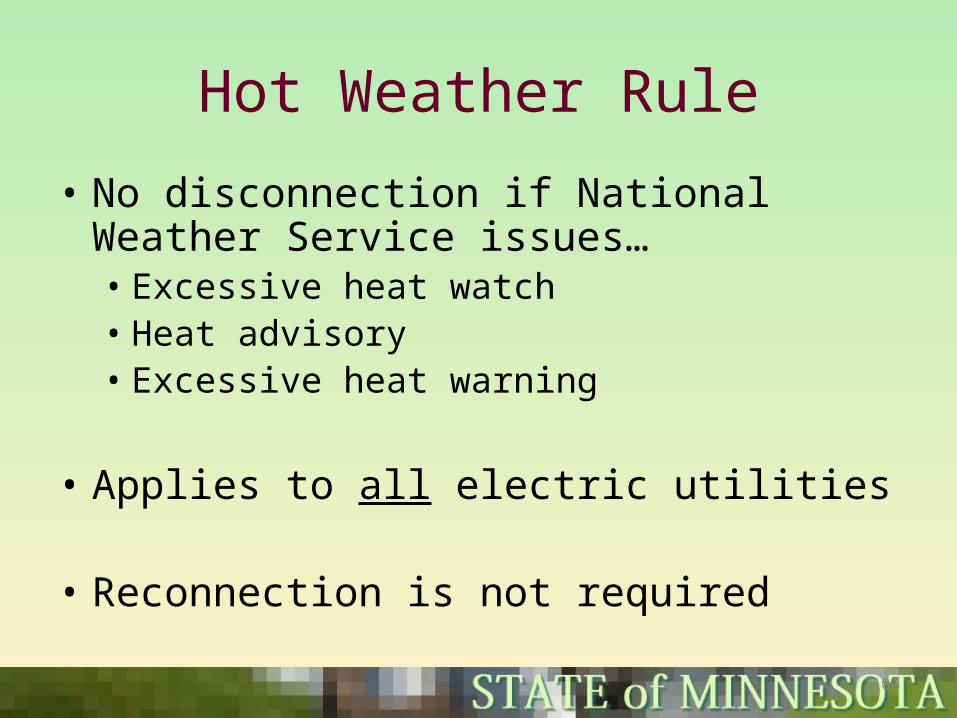

• No disconnection if National Weather Service issues…• Excessive heat watch• Heat advisory• Excessive heat warning

• Applies to all electric utilities

• Reconnection is not required106

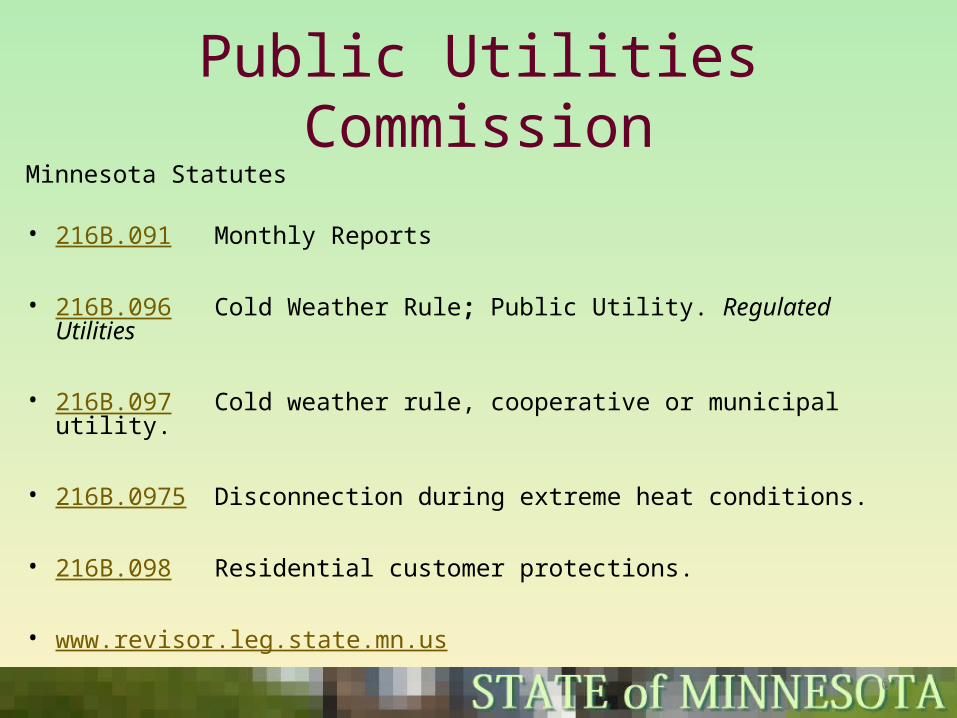

Public Utilities CommissionMinnesota Statutes

• 216B.091 Monthly Reports

• 216B.096 Cold Weather Rule; Public Utility. Regulated Utilities

• 216B.097 Cold weather rule, cooperative or municipal utility.

• 216B.0975 Disconnection during extreme heat conditions.

• 216B.098 Residential customer protections.

• www.revisor.leg.state.mn.us 107

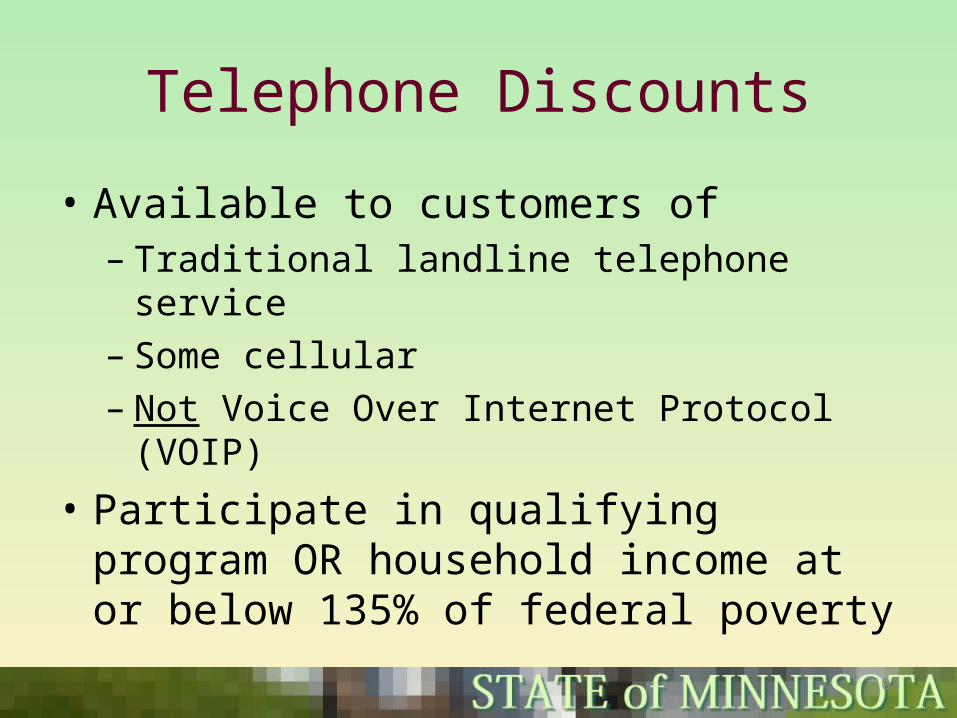

Telephone Discounts

• Available to customers of – Traditional landline telephone service– Some cellular– Not Voice Over Internet Protocol (VOIP)

• Participate in qualifying program OR household income at or below 135% of federal poverty

108

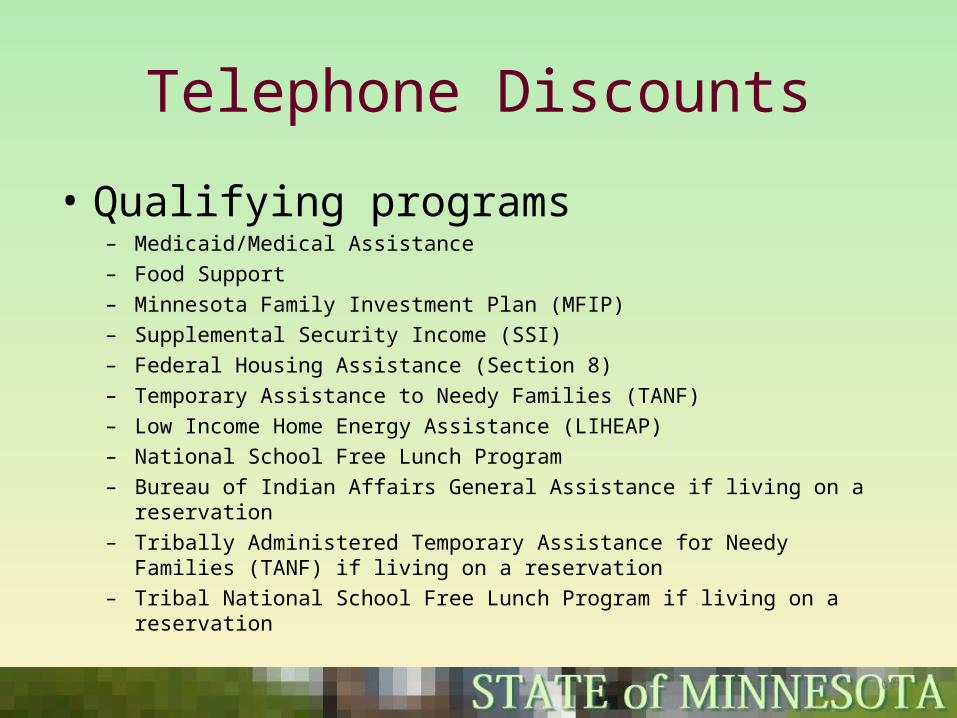

Telephone Discounts

• Qualifying programs– Medicaid/Medical Assistance– Food Support– Minnesota Family Investment Plan (MFIP)– Supplemental Security Income (SSI)– Federal Housing Assistance (Section 8)– Temporary Assistance to Needy Families (TANF)– Low Income Home Energy Assistance (LIHEAP)– National School Free Lunch Program– Bureau of Indian Affairs General Assistance if living on a reservation– Tribally Administered Temporary Assistance for Needy Families (TANF) if

living on a reservation– Tribal National School Free Lunch Program if living on a reservation

109

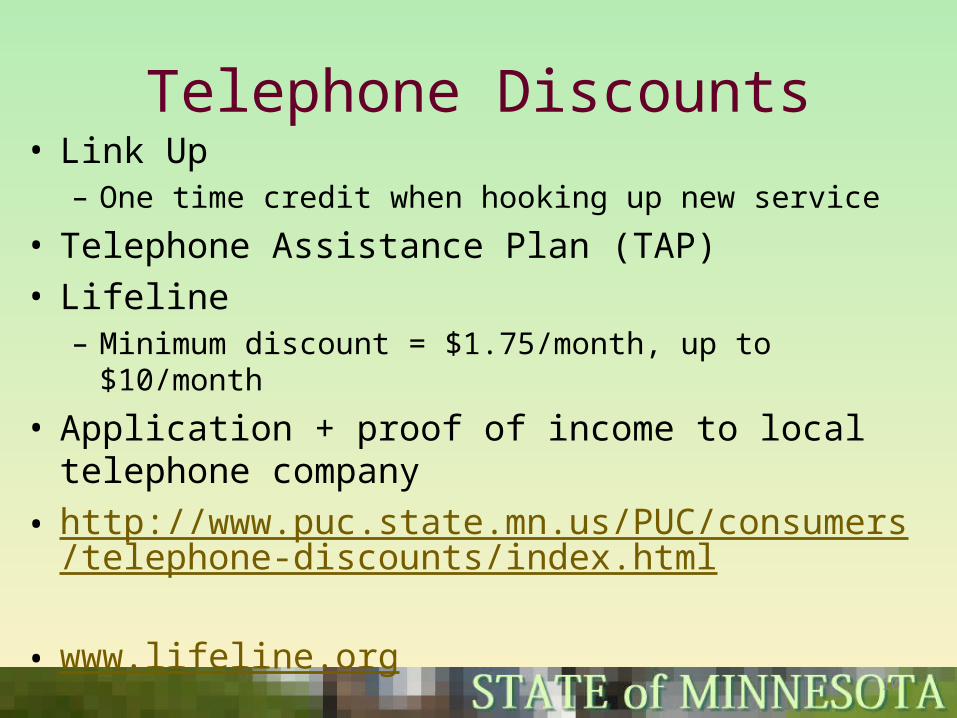

Telephone Discounts• Link Up– One time credit when hooking up new service

• Telephone Assistance Plan (TAP)• Lifeline– Minimum discount = $1.75/month, up to

$10/month

• Application + proof of income to local telephone company

• http://www.puc.state.mn.us/PUC/consumers/telephone-discounts/index.html

• www.lifeline.org 110

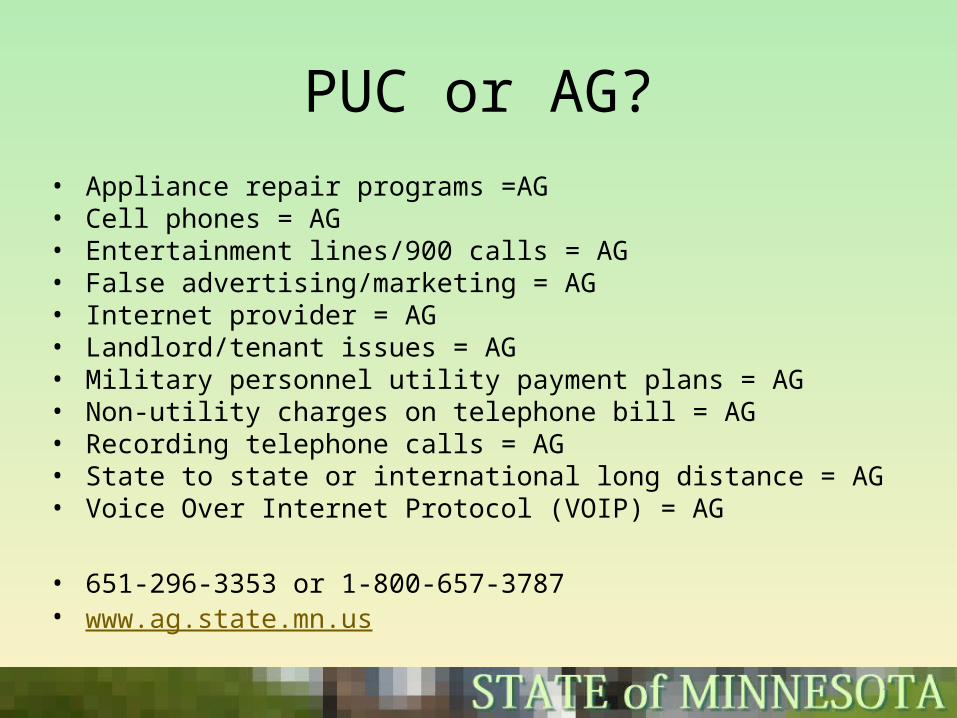

PUC or AG?

• Appliance repair programs =AG• Cell phones = AG• Entertainment lines/900 calls = AG• False advertising/marketing = AG• Internet provider = AG• Landlord/tenant issues = AG• Military personnel utility payment plans = AG• Non-utility charges on telephone bill = AG• Recording telephone calls = AG• State to state or international long distance = AG• Voice Over Internet Protocol (VOIP) = AG

• 651-296-3353 or 1-800-657-3787• www.ag.state.mn.us

111

Public Utilities Commission

Tracy SmetanaConsumer MediatorMinnesota Public Utilities Commission121 Seventh Place East, Suite 350St Paul MN 55101-2147651-296-0406, option 1 1-800-657-3782, option 1Fax [email protected]@state.mn.uswww.puc.state.mn.us

112