Embed Size (px)

Citation preview

1

Employer-Sponsored Health Insurance: Stable Pools and the

Quality of Coverage

Keith J. CrockerThe William Elliott Chaired Professor of Insurance and

Risk Management

Smeal College of Business

Pennsylvania State University

University Park, PA 16802

2

Employer-Sponsored Health InsuranceIn 2006, approximately 90% of privately- insured, nonelderly Americans received coverage through an employer-sponsored plan

2010: Patient Protection and Affordable Care Act “Obamacare” Beginning in 2014, prohibits pre-existing condition

exclusions in which will eliminate the individual and small-employer group market

Employers with >50 employees will have to offer health insurance or pay a fine

Most employers will pay the fine and drop coverage

3

Why Employer-Sponsored Health Care?

• Favorable tax treatment– Premiums deducted as a business

expense (pre-tax dollars!)• Economies of Scale in the purchase and

administration of group policies

4

The Big Question:

• Why is there virtually no market for individual insurance policies?– Contrast with the vibrant individual market

for life insurance which co-exists with the employer-sponsored life insurance benefit

– In 2003, for example, only ¼ of the 20% of Americans without access to an employer plan or public insurance were covered by an individual policy

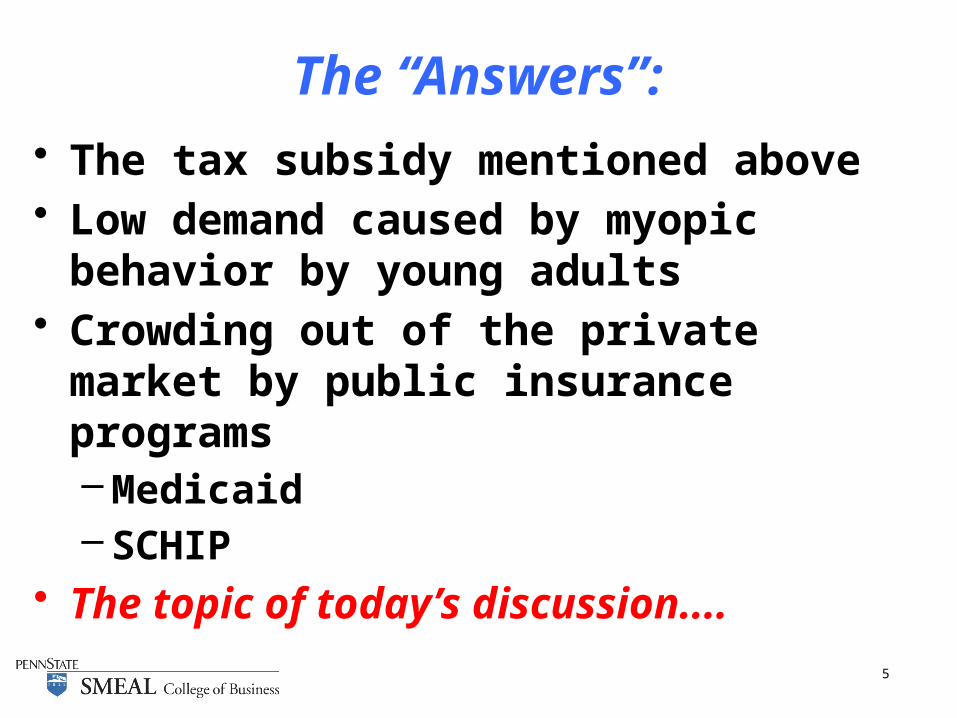

5

The “Answers”:• The tax subsidy mentioned above• Low demand caused by myopic behavior

by young adults• Crowding out of the private market by

public insurance programs– Medicaid– SCHIP

• The topic of today’s discussion....

6

My 2003 RAND Journal Article with John Moran:

“Contracting with Limited Commitment: Evidence from Employment-Based Health Insurance Contracts, RAND Journal of Economics, Winter 2003.

7

Classification Risk

All Consumers are Healthy

Consumers Purchase

Insurance at the “healthy” premium;Some claims paid

Over Time, Some Stay Healthy

While Others Develop“chronic” conditions

Depart the RiskPool to be Re-Underwritten

Stay in the Pool and Pay High

Premiums

“ClassificationRisk”

8

How Do We Keep the Healthy Individuals in the Risk Pool?

• Have consumers sign long-term contracts to remain with the insurer– Historically, non-enforceable

• Charge front-loaded premiums, as in whole life insurance– This is a lot more difficulty in health care

where future technologies and costs are uncertain

9

A Third Solution….

• Tie Health Insurance to Employment• If it is costly for employees to switch

jobs, then it is difficult to move to another employer for a better health insurance deal

• The Key Insight: Job market frictions create job attachment which translates into more stable insurance pools.

10

Job Attachment and Stable Insurance Pools

• The ability of the healthy to depart and be medically re-underwritten is constrained by their Job Attachment

• Healthy workers find it less onerous to be pooled with the unhealthy when there are coverage restrictions

• The Hypothesis: There should be a positive relationship between job attachment and the generosity of the health care plan

11

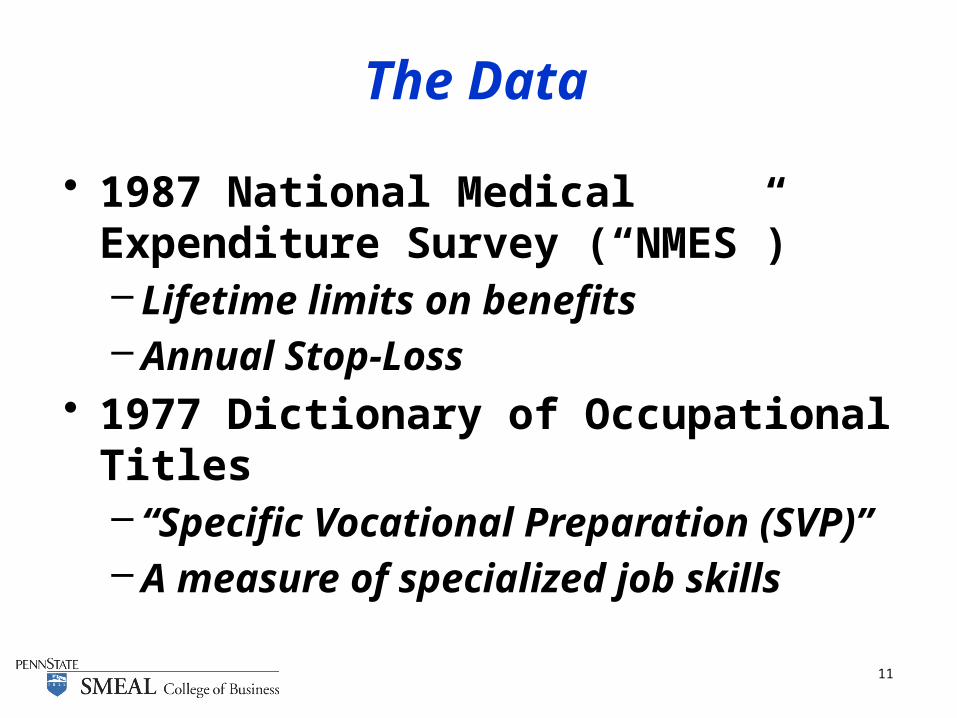

The Data

• 1987 National Medical Expenditure Survey (“NMES”)– Lifetime limits on benefits– Annual Stop-Loss

• 1977 Dictionary of Occupational Titles– “Specific Vocational Preparation (SVP)”– A measure of specialized job skills

12

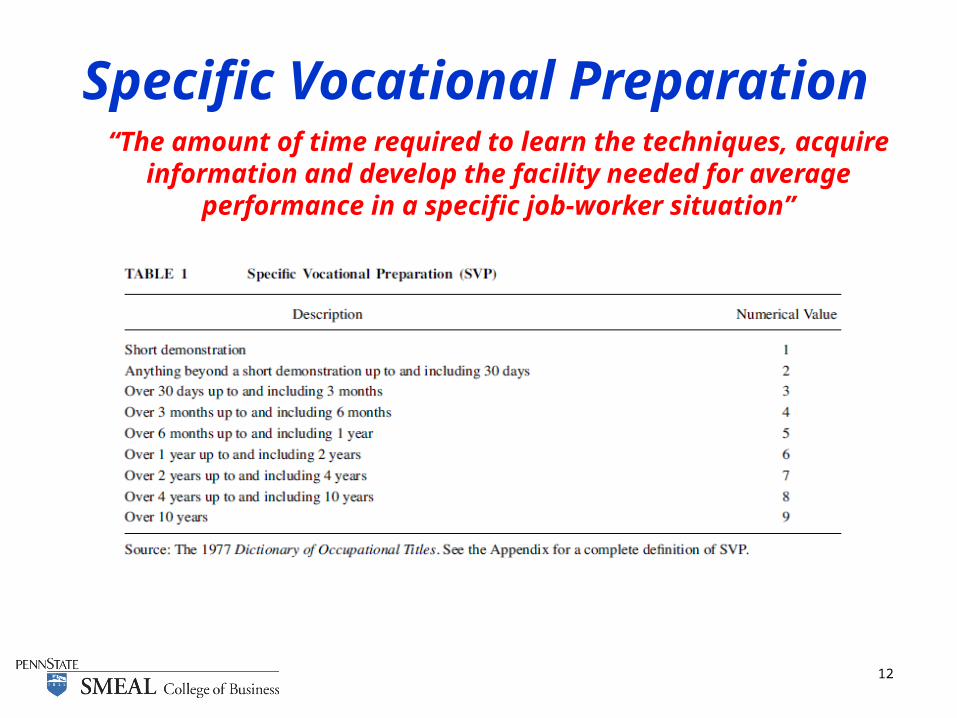

Specific Vocational Preparation“The amount of time required to learn the techniques, acquire

information and develop the facility needed for average performance in a specific job-worker situation”

13

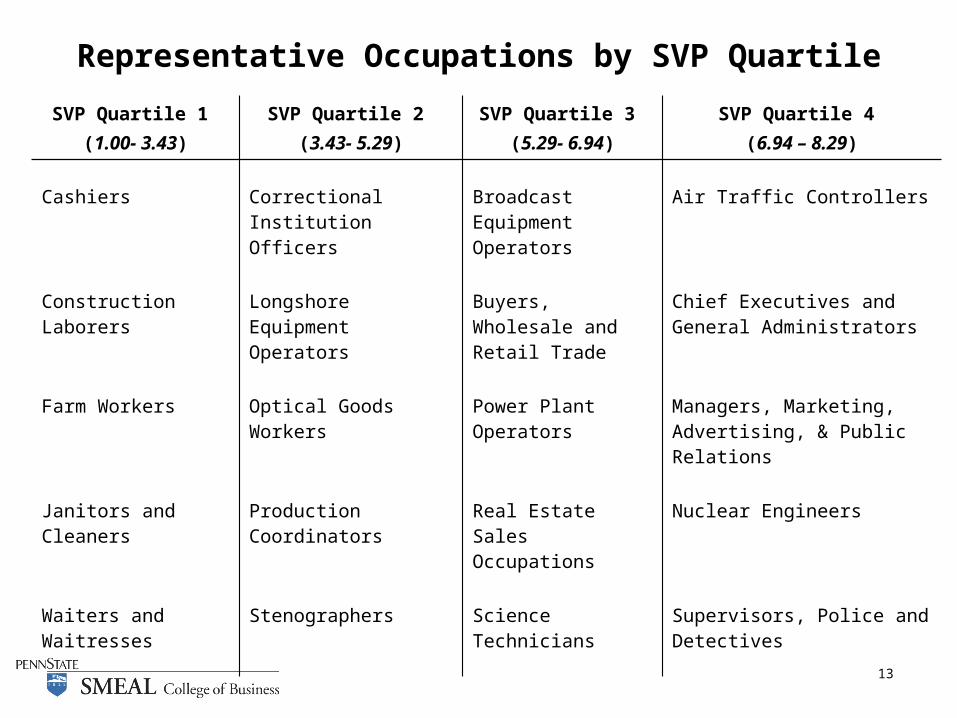

Representative Occupations by SVP Quartile

SVP Quartile 1 (1.00- 3.43)

SVP Quartile 2 (3.43- 5.29)

SVP Quartile 3 (5.29- 6.94)

SVP Quartile 4 (6.94 – 8.29)

Cashiers Correctional Institution Officers

Broadcast Equipment Operators

Air Traffic Controllers

Construction Laborers Longshore Equipment Operators

Buyers, Wholesale and Retail Trade

Chief Executives and General Administrators

Farm Workers Optical Goods Workers Power Plant Operators

Managers, Marketing, Advertising, & Public Relations

Janitors and Cleaners Production Coordinators Real Estate Sales Occupations

Nuclear Engineers

Waiters and Waitresses

Stenographers Science Technicians Supervisors, Police and Detectives

14

15

minimum (3.02)

25th pctile (4.34)

50th pctile (5.12)

75th pctile (5.55)

maximum (6.77)

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$659,216

$809,694

$899,924$948,628

$1,087,458

Predicted Lifetime Benefit

Job Attachment

1987

do

llars

16

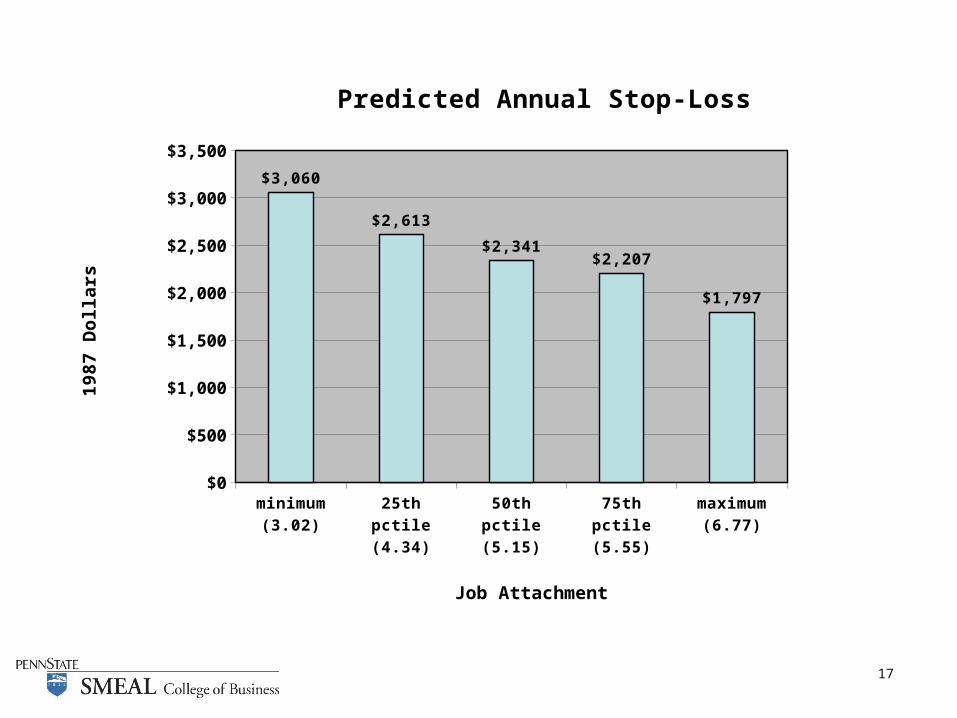

17

minimum (3.02)

25th pctile (4.34)

50th pctile (5.15)

75th pctile (5.55)

maximum (6.77)

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$3,060

$2,613

$2,341$2,207

$1,797

Predicted Annual Stop-Loss

Job Attachment

1987

Do

llars

18

Conclusions

• There is a clear and strong relationship between the stability of the pool, as measured by job attachment, and the ability of insurers to offer more generous healthcare coverage

• Proposals to supplant employee group plans with individual market alternatives should be viewed with caution