Embed Size (px)

Citation preview

1

Demand for Health Insurance

2

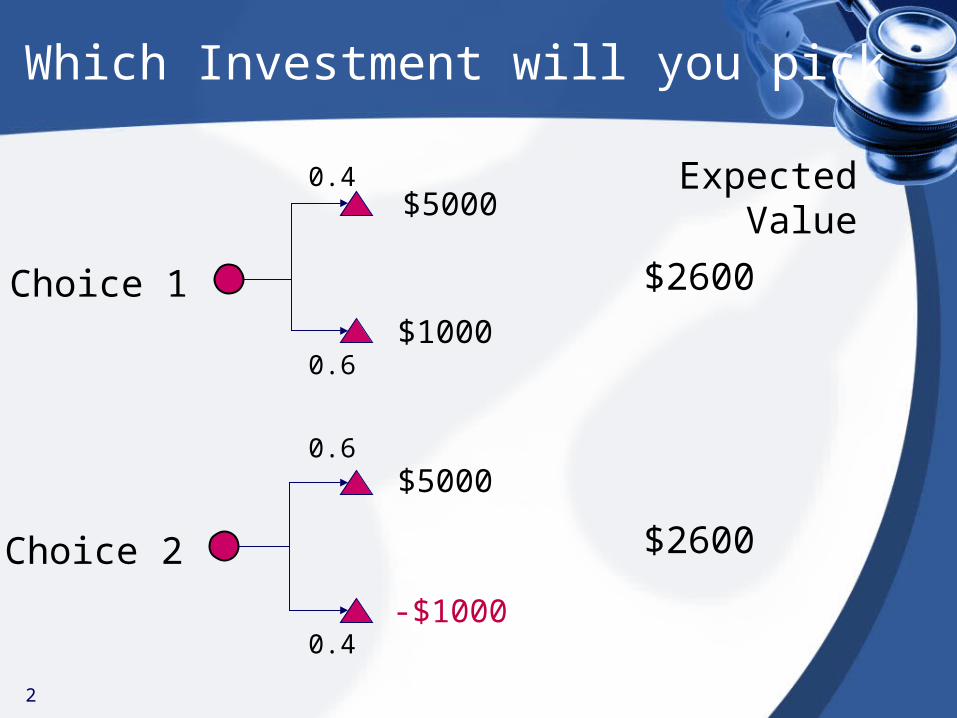

Which Investment will you pick

Expected Value

$2600

$2600Choice 2

$5000

-$1000

0.6

0.4

Choice 1

$5000

$1000

0.4

0.6

3

Attitude towards risk

• In the absence of any objective criteria, how an individual or organization deals with uncertainty depends ultimately on their attitude towards risk and whether they are risk averse, risk neutral or a risk taker.

4

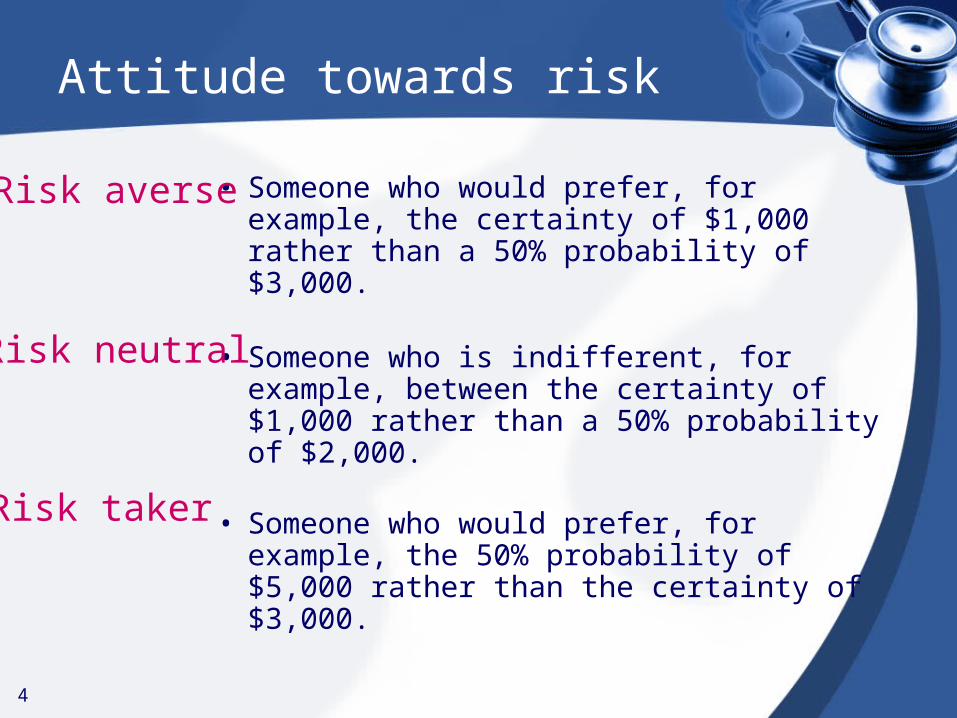

Attitude towards risk

• Someone who would prefer, for example, the certainty of $1,000 rather than a 50% probability of $3,000.

• Someone who is indifferent, for example, between the certainty of $1,000 rather than a 50% probability of $2,000.

• Someone who would prefer, for example, the 50% probability of $5,000 rather than the certainty of $3,000.

Risk averse

Risk neutral

Risk taker

5

Different Approaches to Risk:

• Expected Value

• Maximin

• Maximax

• Hurwicz alpha index rule

6

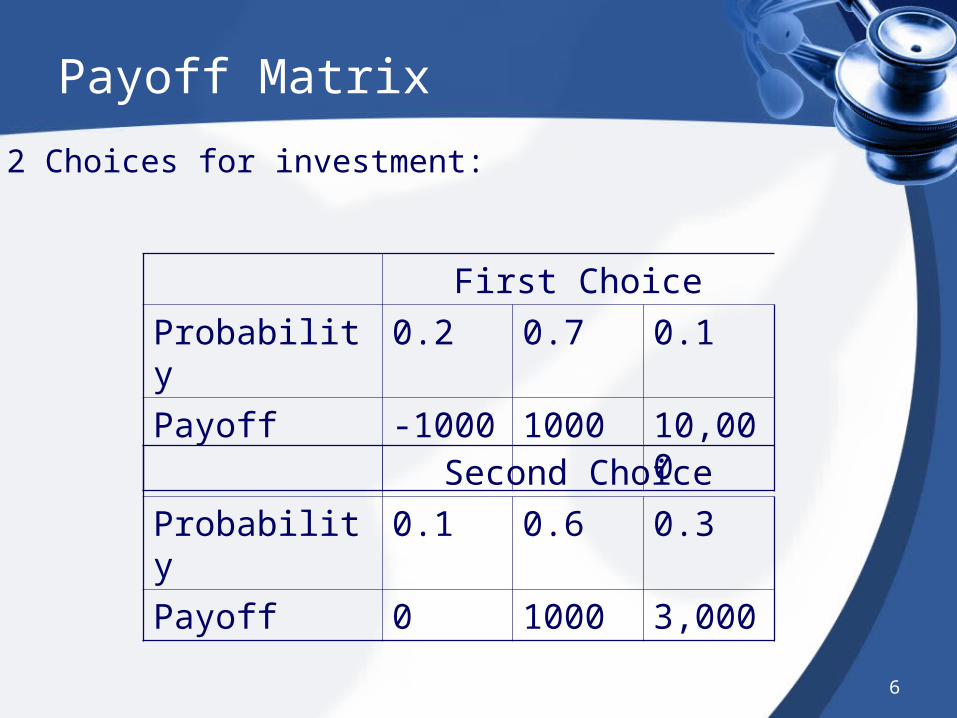

Payoff Matrix

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

2 Choices for investment:

7

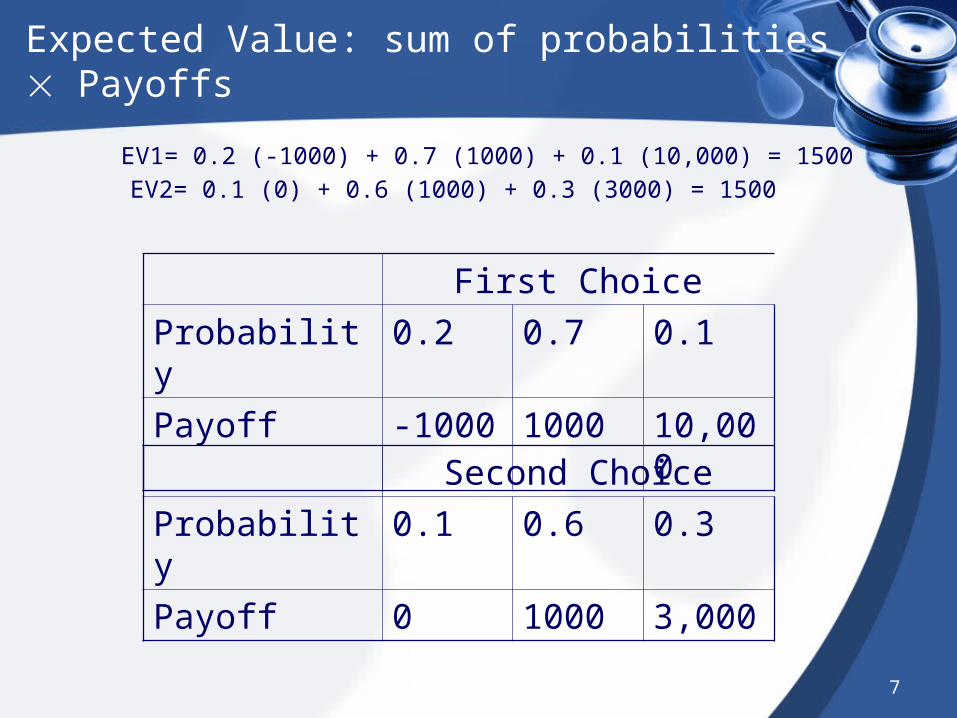

Expected Value: sum of probabilities Payoffs

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

EV1= 0.2 (-1000) + 0.7 (1000) + 0.1 (10,000) = 1500

EV2= 0.1 (0) + 0.6 (1000) + 0.3 (3000) = 1500

8

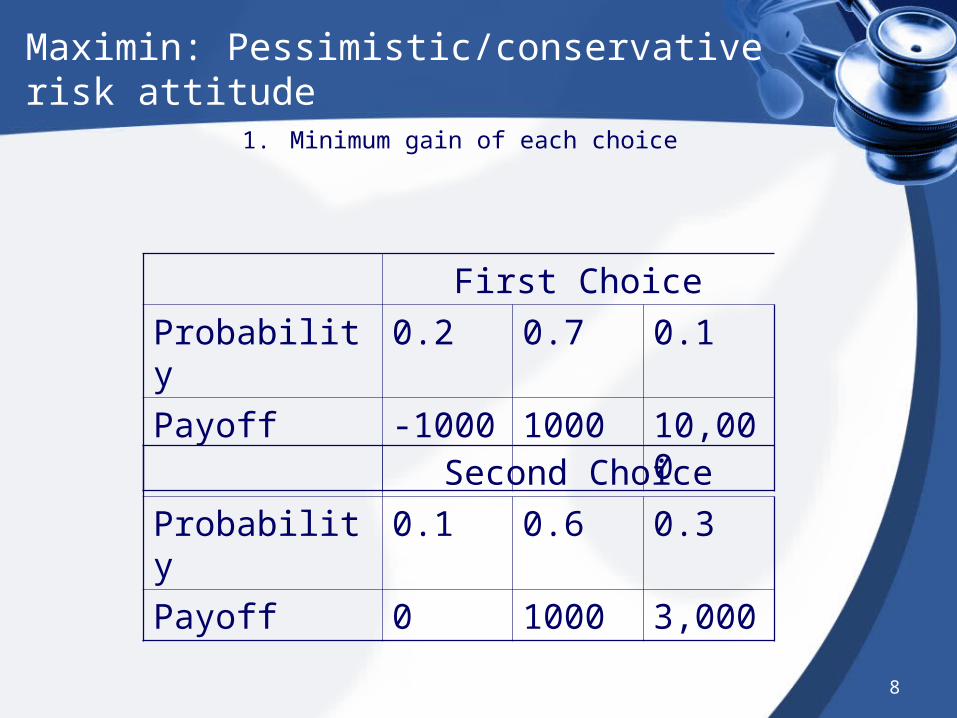

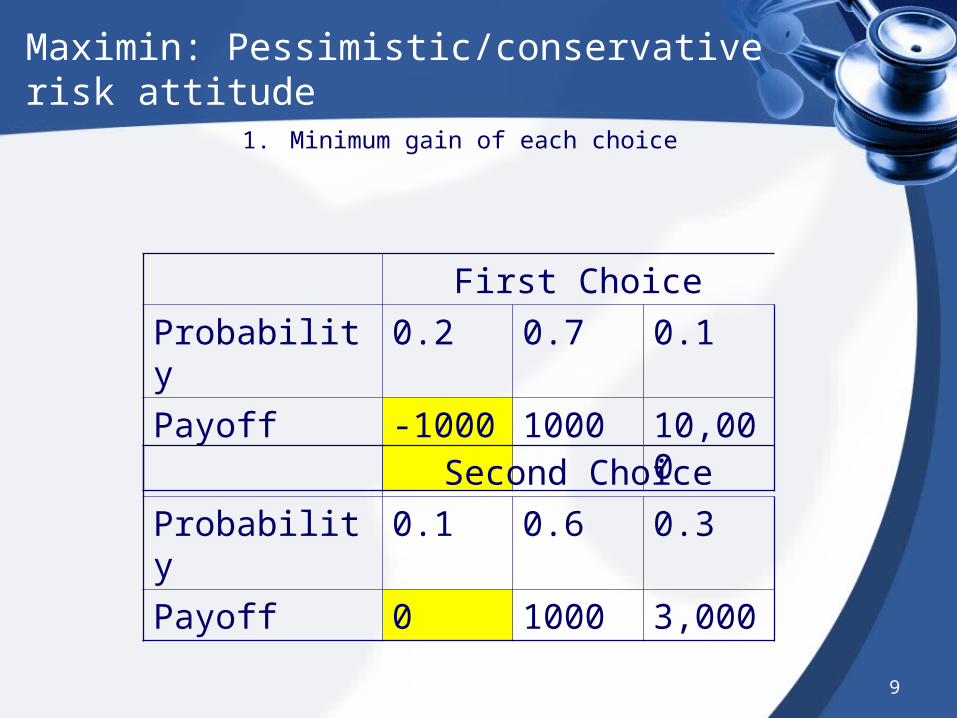

Maximin: Pessimistic/conservative risk attitude

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Minimum gain of each choice

9

Maximin: Pessimistic/conservative risk attitude

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Minimum gain of each choice

10

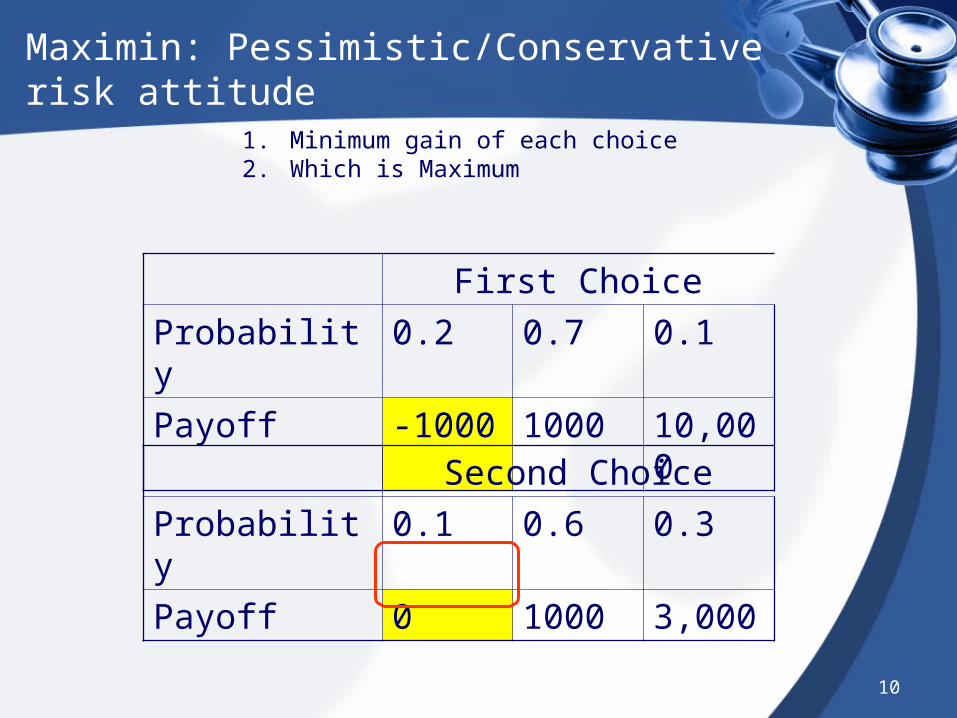

Maximin: Pessimistic/Conservative risk attitude

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Minimum gain of each choice2. Which is Maximum

11

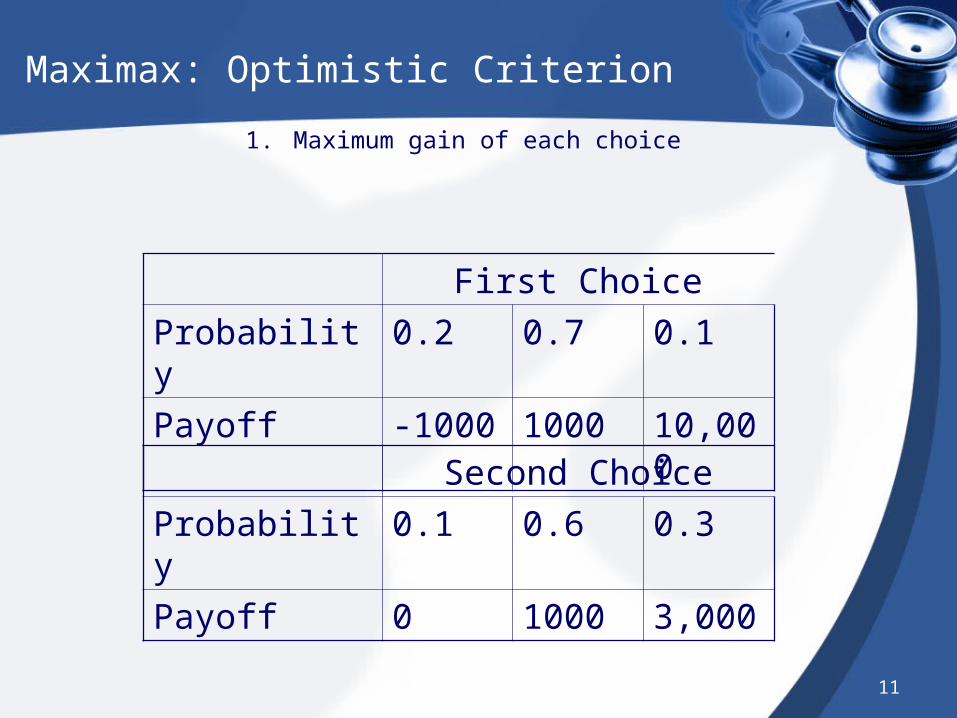

Maximax: Optimistic Criterion

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Maximum gain of each choice

12

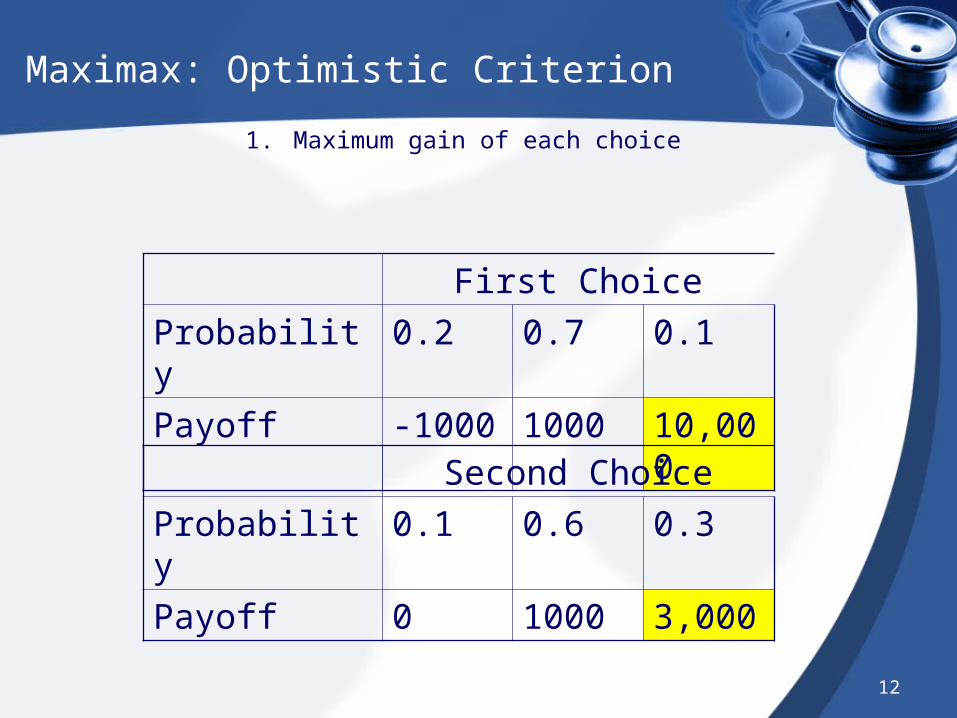

Maximax: Optimistic Criterion

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Maximum gain of each choice

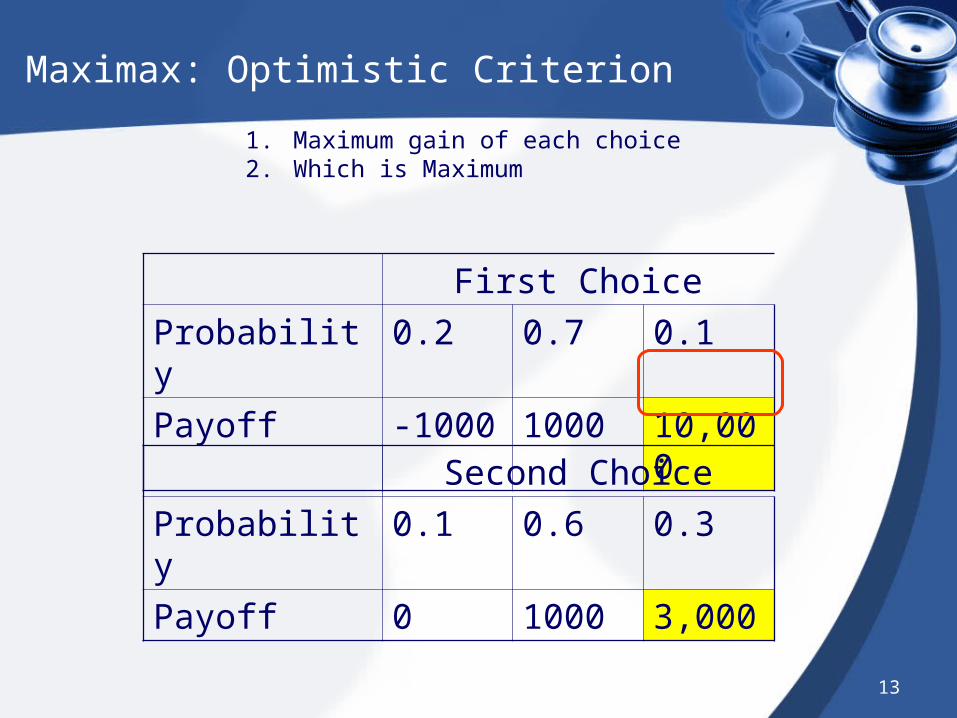

13

Maximax: Optimistic Criterion

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Maximum gain of each choice2. Which is Maximum

14

Hurwicz alpha index rule:

• The Hurwicz alpha variable is a measure of attitude to risk. It can range from = 1 (optimist) to = 0 (pessimist). A value of = 0.5 would correspond to risk neutrality.

• The Hurwicz criterion = maximum value x + minimum value x (1 – )

15

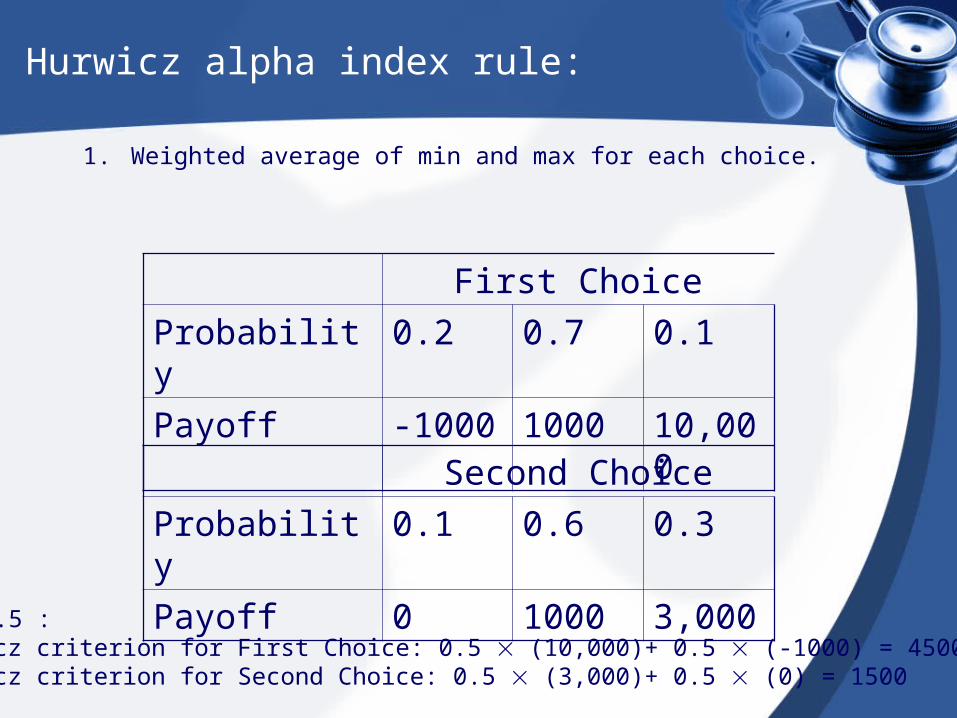

Hurwicz alpha index rule:

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Weighted average of min and max for each choice.

For = 0.5 :The Hurwicz criterion for First Choice: 0.5 (10,000)+ 0.5 (-1000) = 4500The Hurwicz criterion for Second Choice: 0.5 (3,000)+ 0.5 (0) = 1500

16

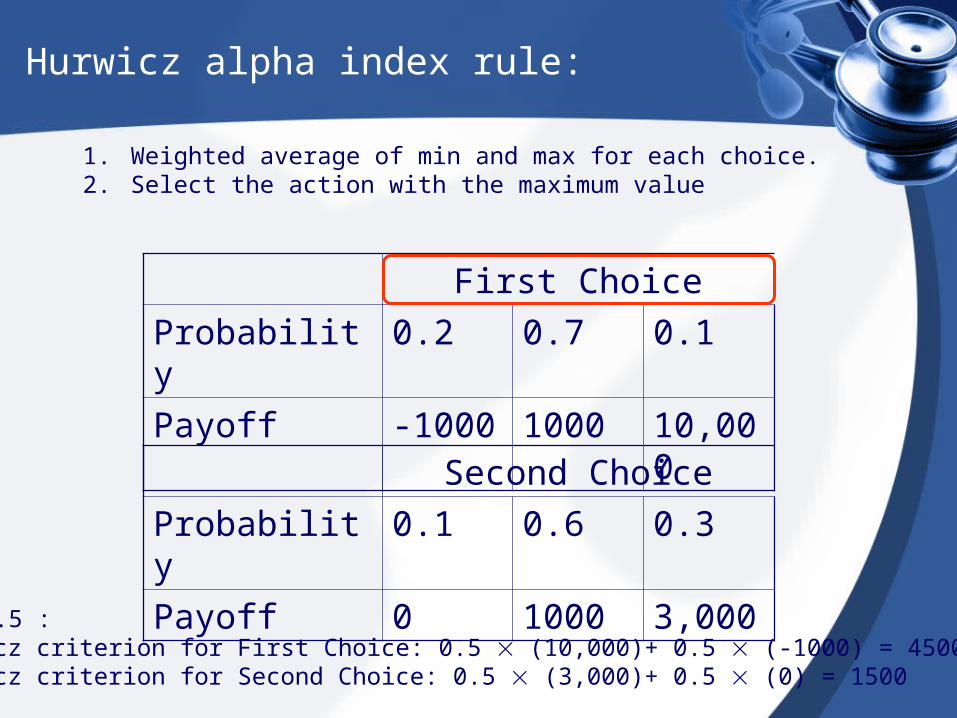

Hurwicz alpha index rule:

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Weighted average of min and max for each choice. 2. Select the action with the maximum value

For = 0.5 :The Hurwicz criterion for First Choice: 0.5 (10,000)+ 0.5 (-1000) = 4500The Hurwicz criterion for Second Choice: 0.5 (3,000)+ 0.5 (0) = 1500

17

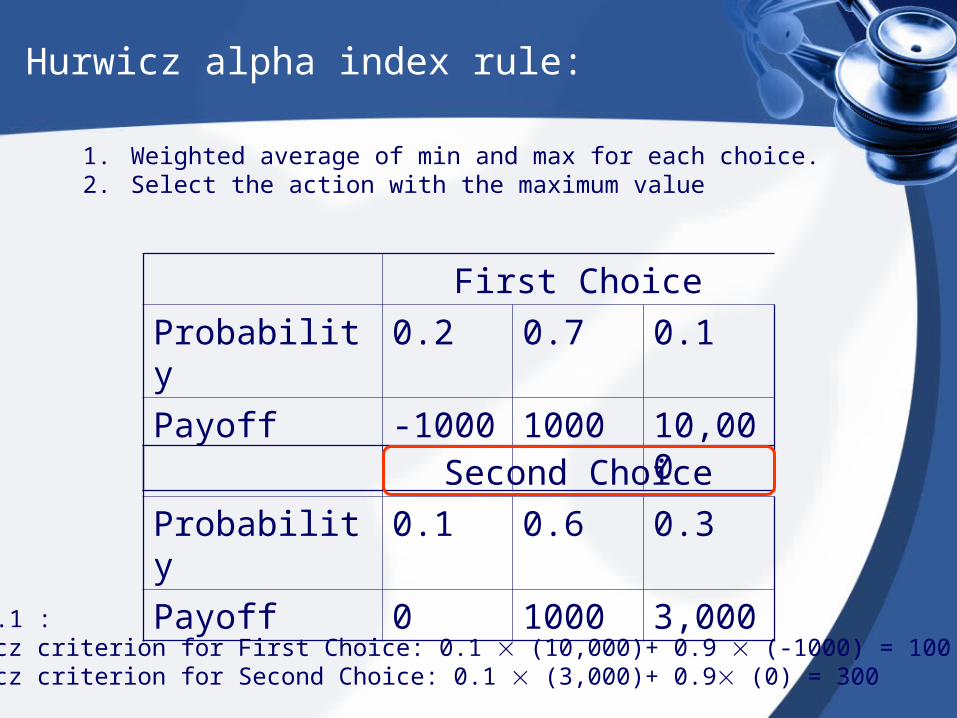

Hurwicz alpha index rule:

First Choice

Probability 0.2 0.7 0.1

Payoff -1000 1000 10,000

Second Choice

Probability 0.1 0.6 0.3

Payoff 0 1000 3,000

1. Weighted average of min and max for each choice. 2. Select the action with the maximum value

For = 0.1 :The Hurwicz criterion for First Choice: 0.1 (10,000)+ 0.9 (-1000) = 100The Hurwicz criterion for Second Choice: 0.1 (3,000)+ 0.9 (0) = 300

18

Hurwicz alpha index rule:

• The maximin strategy equates to the Hurwicz approach with a value of = 0.

• The maximax strategy corresponds to = 1.

Insurance Logic

• The consumer pays insurer a premium to cover medical expenses in coming year.– For any one consumer, the premium will

be higher or lower than medical expenses.

• But the insurer can pool or spread risk among many insurees.– The sum of premiums will exceed the sum

of medical expenses.

Characterizing Risk Aversion

• Recall the consumer maximizes utility, with prices and income given.– Utility = U (health, other goods)– health = h (medical care)

• Insurance doesn’t guarantee health, but provides $ to purchase health care.

• We assumed diminishing marginal utility of “health” and “other goods.”

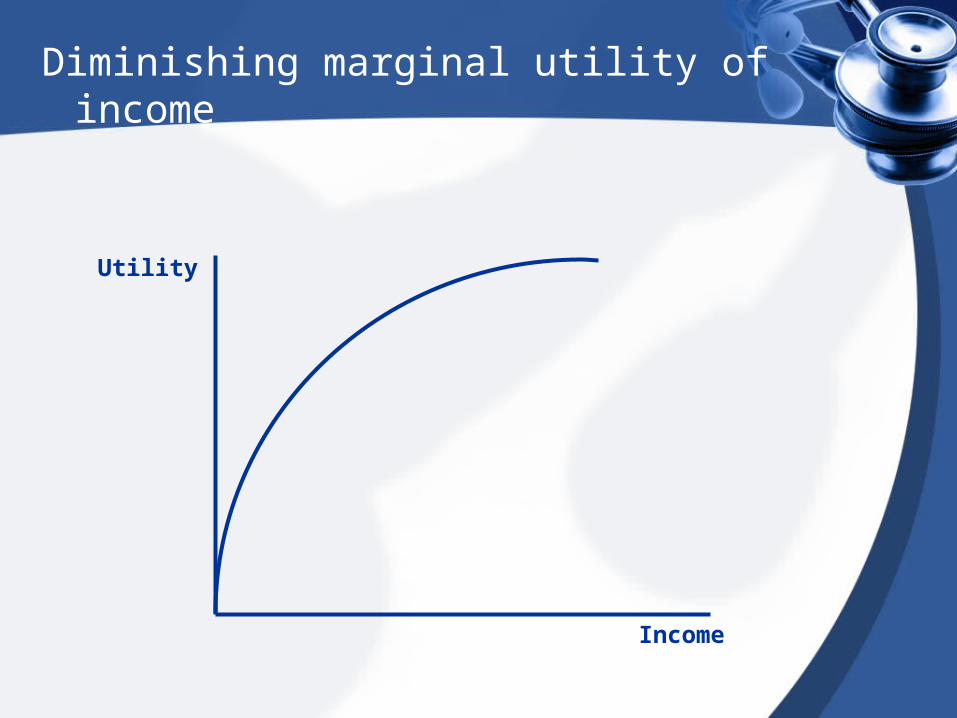

Diminishing marginal utility of income

Utility

Income

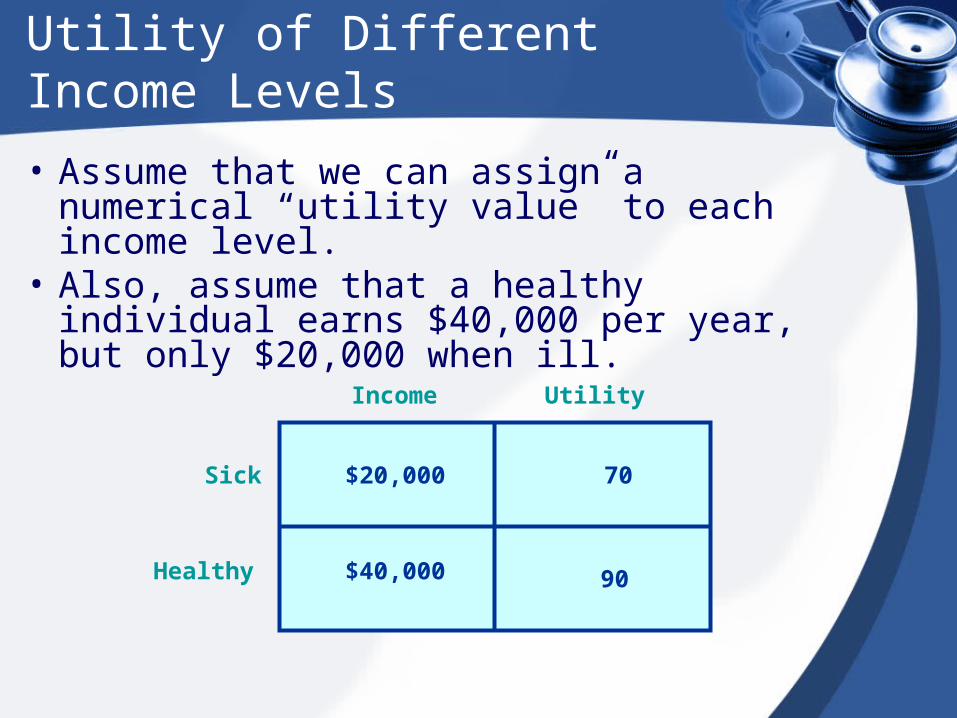

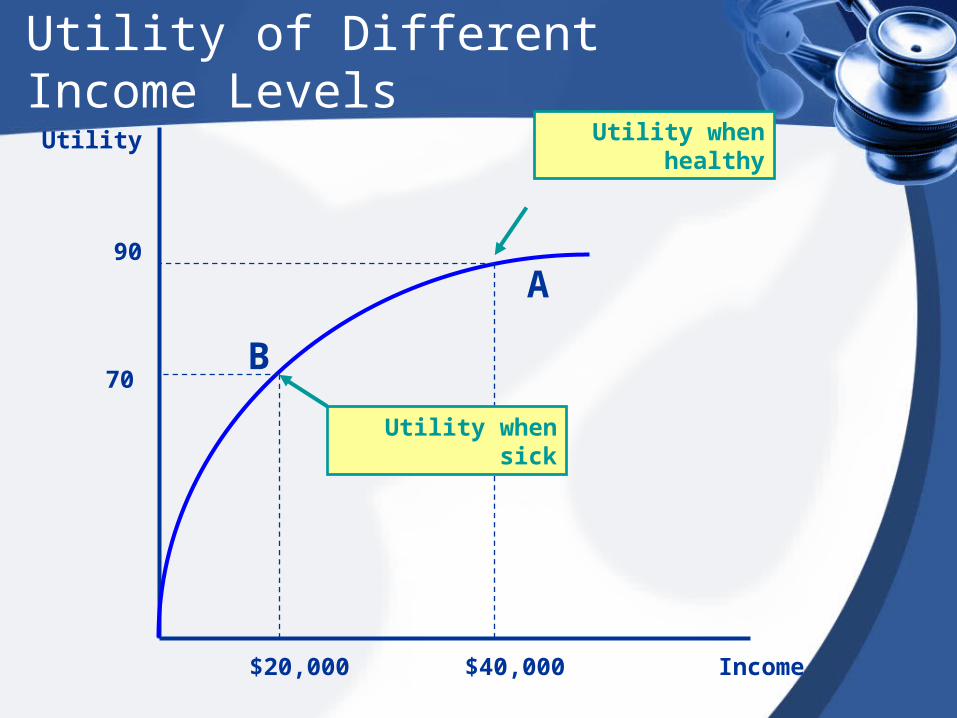

Utility of Different Income Levels

• Assume that we can assign a numerical “utility value” to each income level.

• Also, assume that a healthy individual earns $40,000 per year, but only $20,000 when ill.

$20,000

$40,000

70

90

Income Utility

Sick

Healthy

Utility

Income$20,000 $40,000

90

70

Utility when healthy

Utility when sick

A

B

Utility of Different Income Levels

Probability of Being Healthy or Sick

• Individual doesn’t know whether she will be sick or healthy.

• But she has a subjective probability of each event.– She has an expected value of her utility in the

coming year.

• Define: P0 = prob. of being healthy P1 = prob. of being sick

P0 + P1 = 1

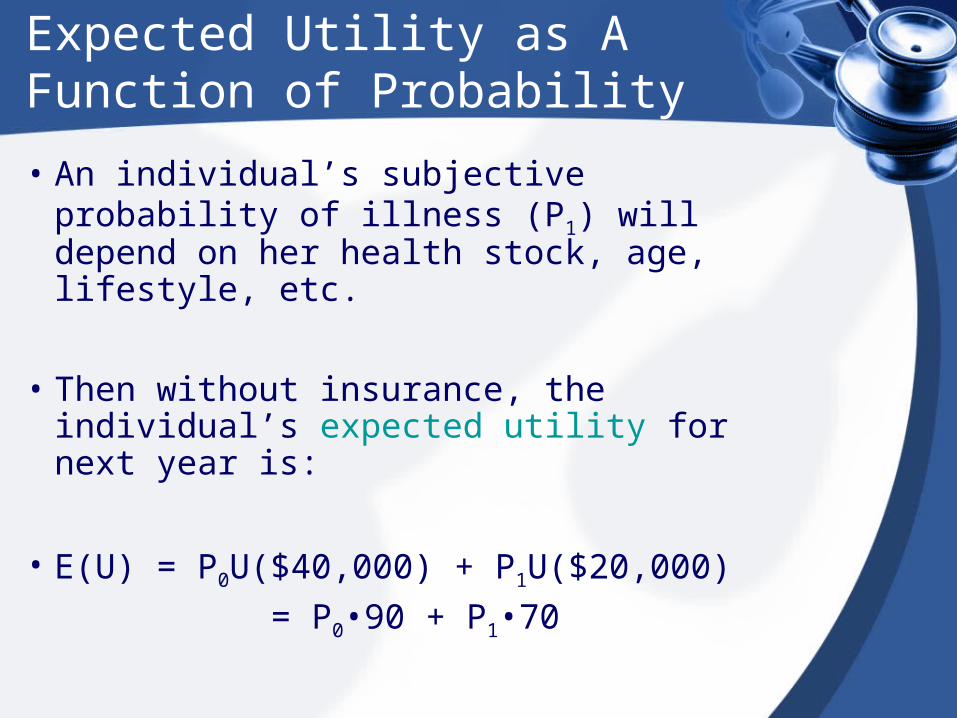

Expected Utility as A Function of Probability

• An individual’s subjective probability of illness (P1) will depend on her health stock, age, lifestyle, etc.

• Then without insurance, the individual’s expected utility for next year is:

• E(U) = P0U($40,000) + P1U($20,000)

= P0•90 + P1•70

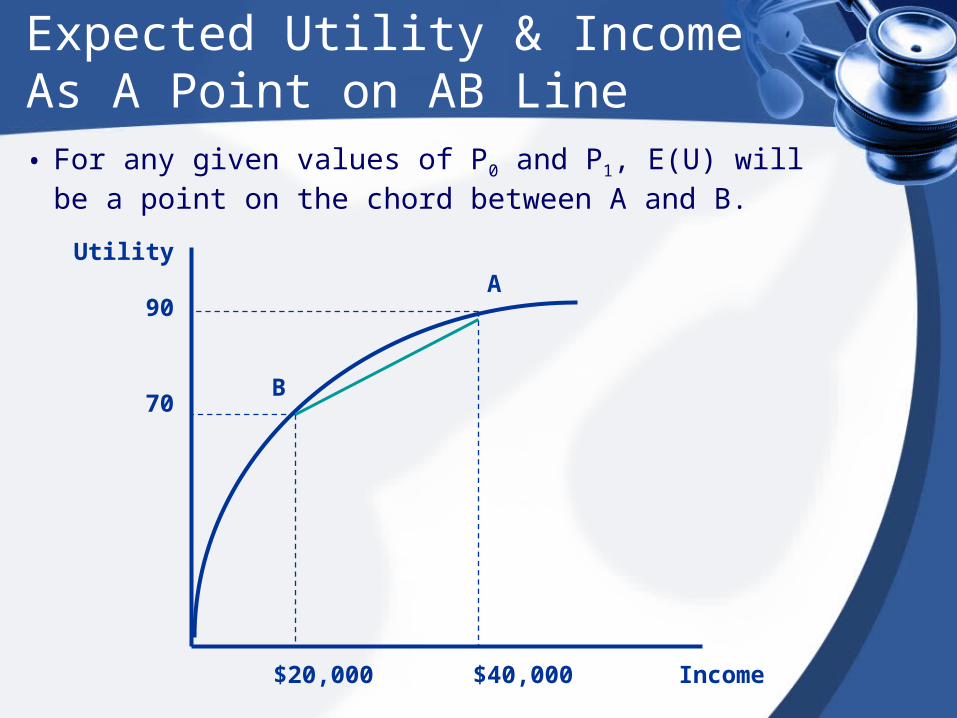

Expected Utility & Income As A Point on AB Line

• For any given values of P0 and P1, E(U) will be a point on the chord between A and B.

Utility

Income$20,000 $40,000

70

90A

B

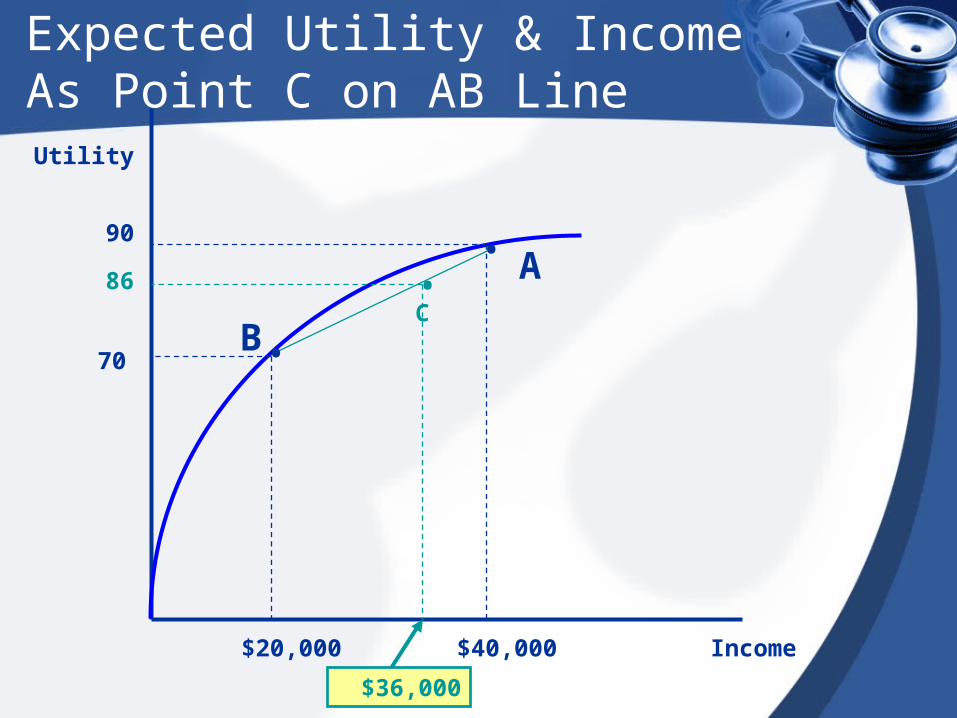

Expected Utility & Income As A Point on AB Line

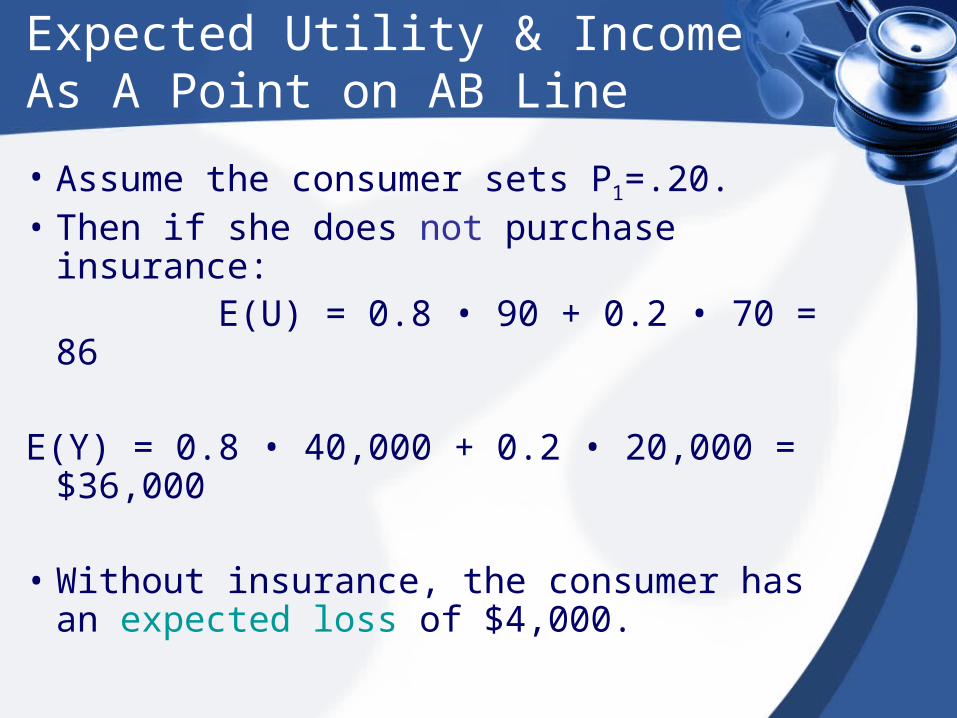

• Assume the consumer sets P1=.20.• Then if she does not purchase insurance: E(U) = 0.8 • 90 + 0.2 • 70 = 86

E(Y) = 0.8 • 40,000 + 0.2 • 20,000 = $36,000

• Without insurance, the consumer has an expected loss of $4,000.

Utility

Income$20,000 $40,000

90

70

A

B

$36,000

C•

•

•86

Expected Utility & Income As Point C on AB Line

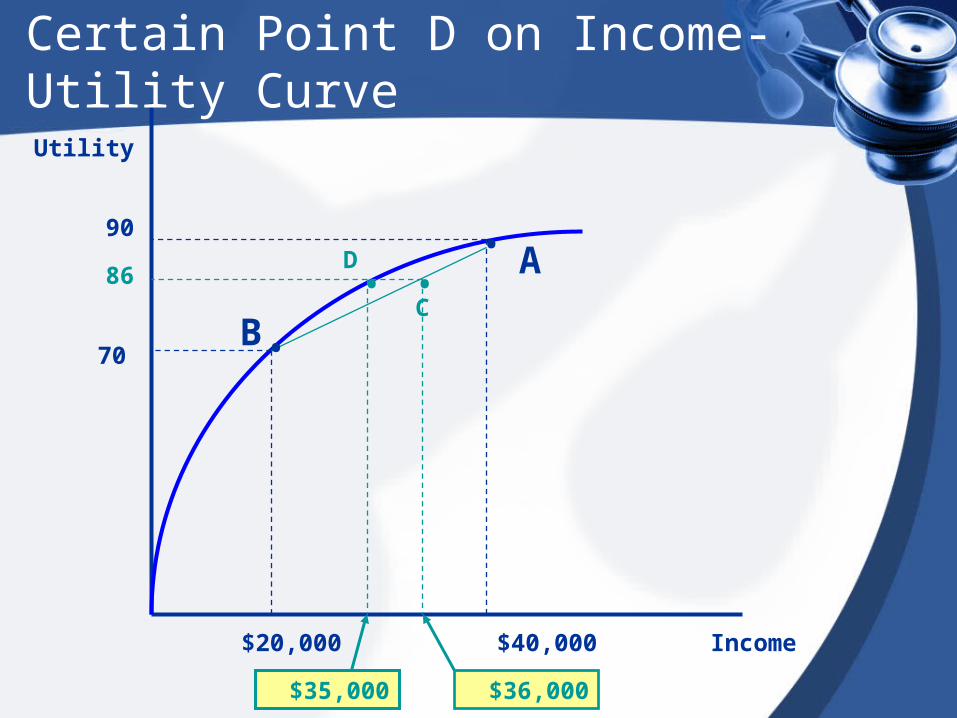

Certain Point on Income-Utility Curve

• The consumer’s expected utility for next year without insurance = 86 “utils.”

• Suppose that 86 “utils” also represents utility from a certain income of $35,000.– Then the consumer could pay an insurer

$5,000 to insure against the probability of getting sick next year.

– Paying $5,000 to insurer leaves consumer with 86 utils, which equals E(U) without insurance.

Utility

Income$20,000 $40,000

90

70

A

B

$36,000

C•

•

•86

$35,000

•D

Certain Point D on Income-Utility Curve

Price of Insurance and Loading Fee

• At most, the consumer is willing to pay $5,000 in insurance premiums to cover $4,000 in expected medical benefits.

• $1,000 loading fee price of insurance

• Covers– profits

– administrative expenses

– taxes

Thank You !Any Question ?