Embed Size (px)

Citation preview

1

Clients going abroad

to work or live

This presentation is intended for qualified financial advisers only and must not be relied upon by anyone else.

© 2009 Standard Life International

2

Emigration facts

• More than 1 million UK citizens have left the UK since the beginning of 2000 according to the Office of National Statistics (Source: ONS)

• 406,000 British residents left UK for long term in 12 months to mid 2008 (Source: ONS)– what was their wealth value?

• Most popular were Australia, Spain, New Zealand, USA, France

3

Future trends?

• Survey of 560 UK students aged 11-18 – 7 out of 10 want to live/work abroad one day – US, Australia, Spain, Italy, France, New Zealand– 62% cited "better weather“, 53% lower cost of living

Source: PCP Research

4

Moving or retiring abroad – Govt advice

• Direct.gov.uk & FCO.gov.uk websites provide help on– Living abroad– Working abroad

Information • UK nationals right to live in EEA countries• British Embassy websites other countries• State pension• Tax liabilities• Healthcare• Welfare benefits• Employment rights• Checklists

Standard Life International is not responsible for the content of external websites.

5

Moving/working abroad

• Increasing no. of people spend time living/working abroad– expat employees on international assignments doubled

over last 3 years (Source: Mercers 2008/9 Benefits survey for Expats & Globally Mobile Employees)

• Can take advantage of a tax relief which only applies to Offshore Bonds – Time Apportionment Relief

6

Time Apportionment Relief

• Applies to gains on a 'foreign policy'

• Policyholder non-UK res for periods prior to chargeable gain

• Gain subject to reduction for periods of non residence

• Policy period is no of days in force prior to chargeable event

• Gain reduced by 'appropriate fraction', equal to A/B, where A = no of days which policyholder not UK residentB = total number of days in the policy period

7

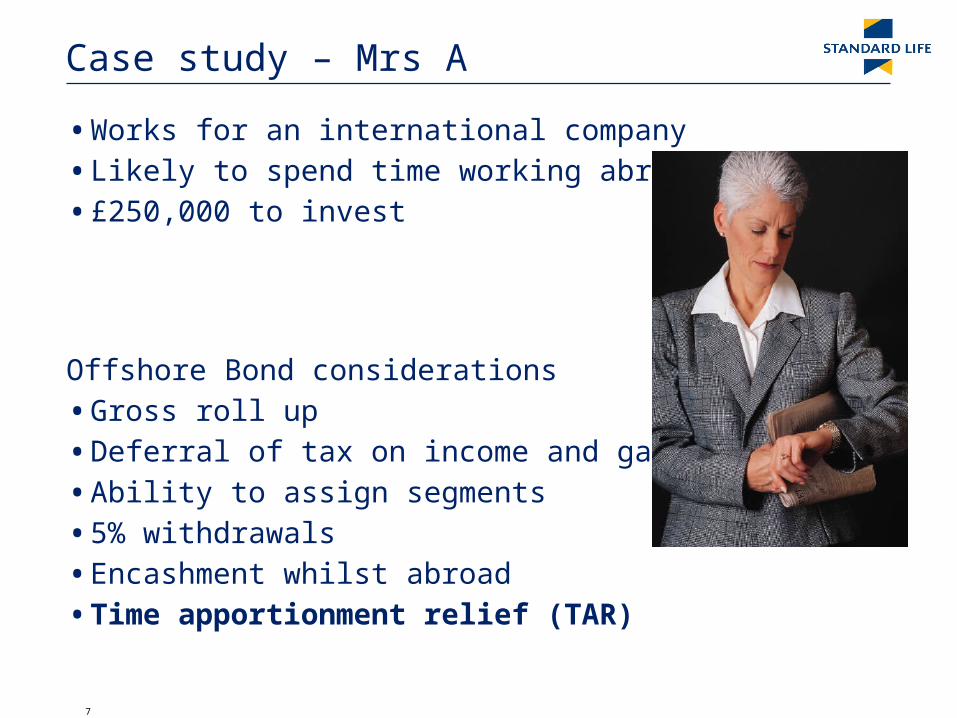

Case study – Mrs A

• Works for an international company

• Likely to spend time working abroad

• £250,000 to invest

Offshore Bond considerations

• Gross roll up

• Deferral of tax on income and gain

• Ability to assign segments

• 5% withdrawals

• Encashment whilst abroad

• Time apportionment relief (TAR)

8

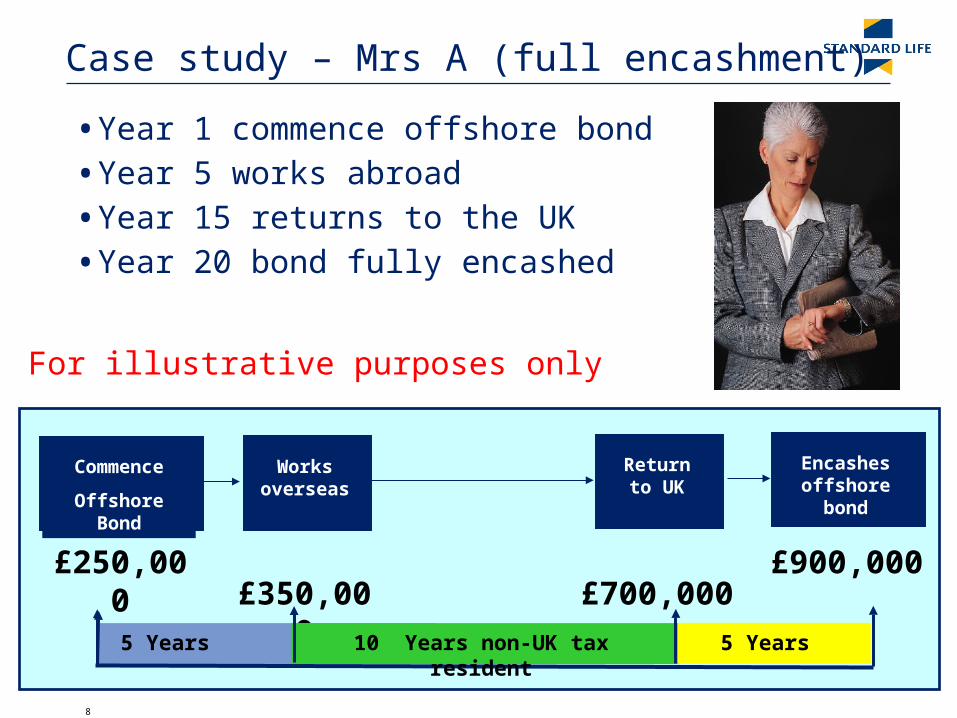

Case study – Mrs A (full encashment)

• Year 1 commence offshore bond

• Year 5 works abroad

• Year 15 returns to the UK

• Year 20 bond fully encashed

Commence

Offshore Bond

Works overseas

Return to UK

Encashes offshore

bond

£900,000£250,000£350,000 £700,000

5 Years 10 Years non-UK tax resident 5 Years

For illustrative purposes only

9

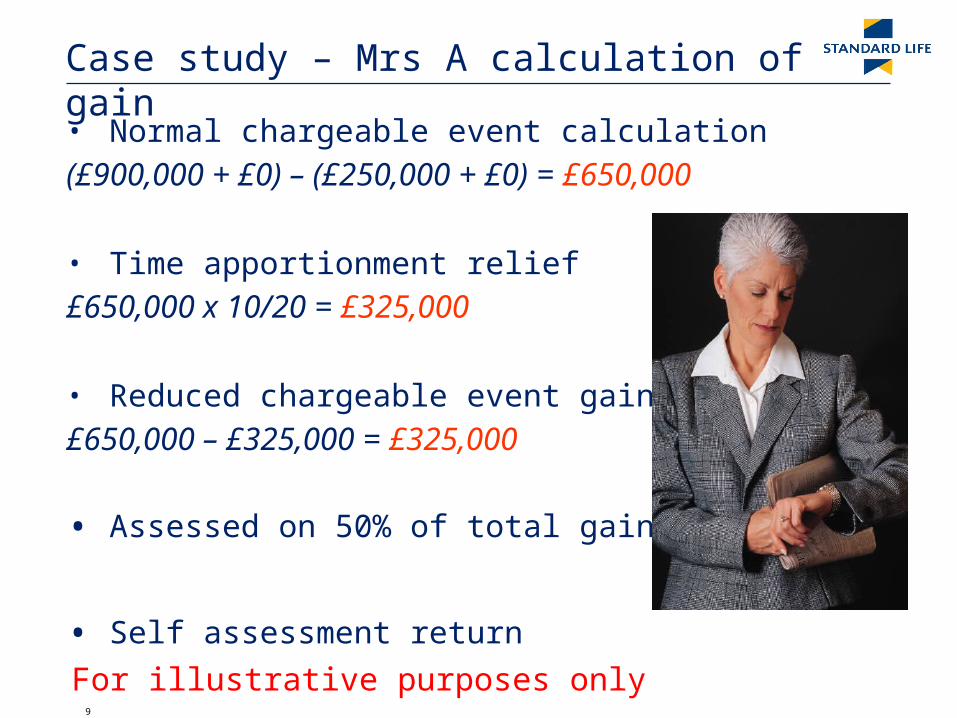

Case study – Mrs A calculation of gain

• Normal chargeable event calculation(£900,000 + £0) – (£250,000 + £0) = £650,000

• Time apportionment relief£650,000 x 10/20 = £325,000

• Reduced chargeable event gain£650,000 – £325,000 = £325,000

• Assessed on 50% of total gain

• Self assessment return

For illustrative purposes only

10

Pre-emigration tax planning considerations

• Is Time Appointment Relief of benefit to people moving abroad?

• What percentage of people emigrating return?

11

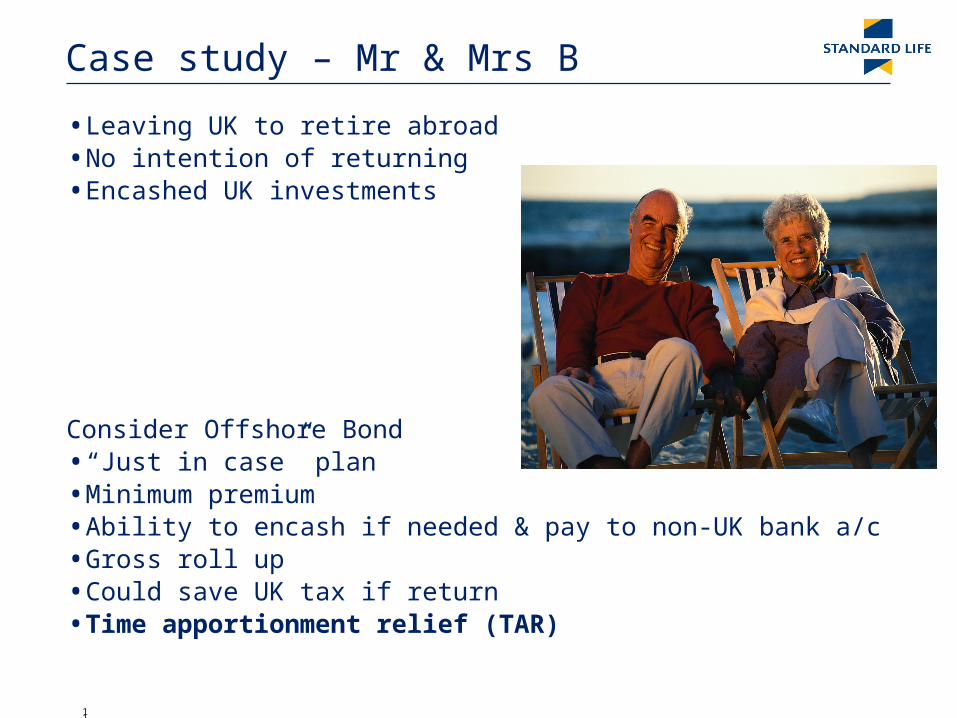

Case study – Mr & Mrs B

• Leaving UK to retire abroad• No intention of returning• Encashed UK investments

Consider Offshore Bond• “Just in case” plan• Minimum premium• Ability to encash if needed & pay to non-UK bank a/c• Gross roll up• Could save UK tax if return• Time apportionment relief (TAR)

12

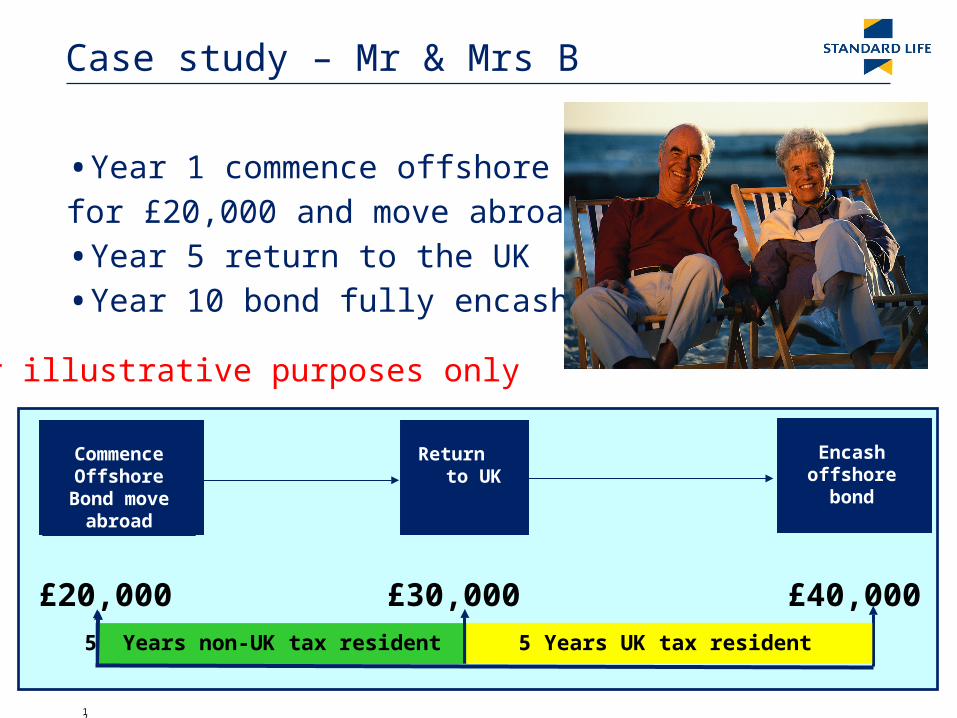

Case study – Mr & Mrs B

• Year 1 commence offshore bondfor £20,000 and move abroad

• Year 5 return to the UK

• Year 10 bond fully encashed

For illustrative purposes only

Commence Offshore Bond move abroad

Return to UK

Encash offshore

bond

£40,000£20,000 £30,0005 Years non-UK tax resident 5 Years UK tax resident

13

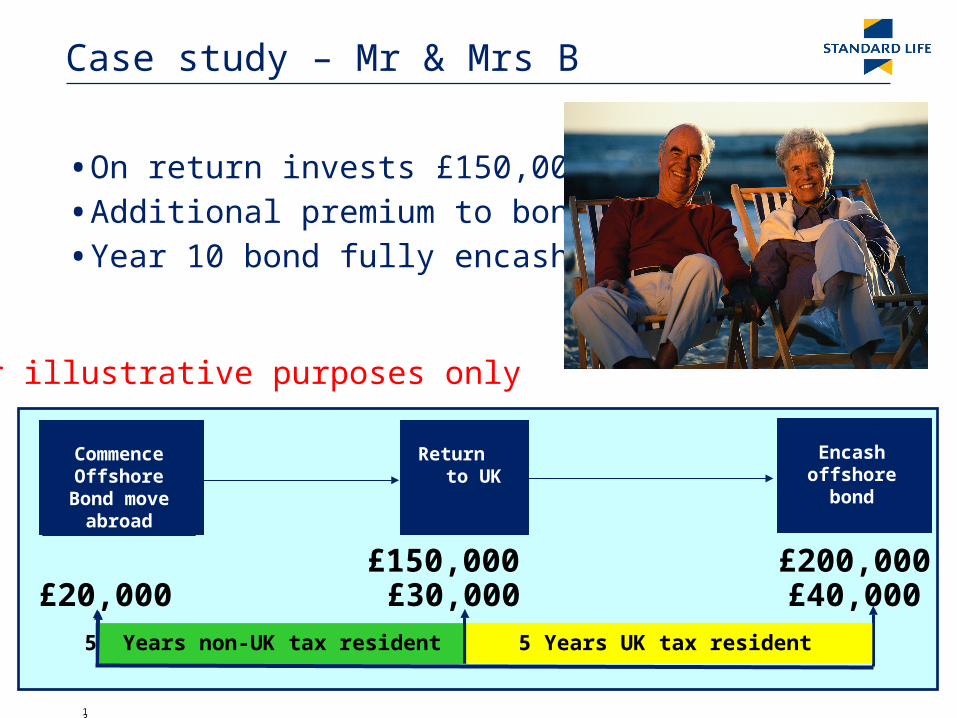

Case study – Mr & Mrs B

• On return invests £150,000

• Additional premium to bond

• Year 10 bond fully encashed

£200,000£150,000

For illustrative purposes only

Commence Offshore Bond move abroad

Return to UK

Encash offshore

bond

£40,000£20,000 £30,0005 Years non-UK tax resident 5 Years UK tax resident

14

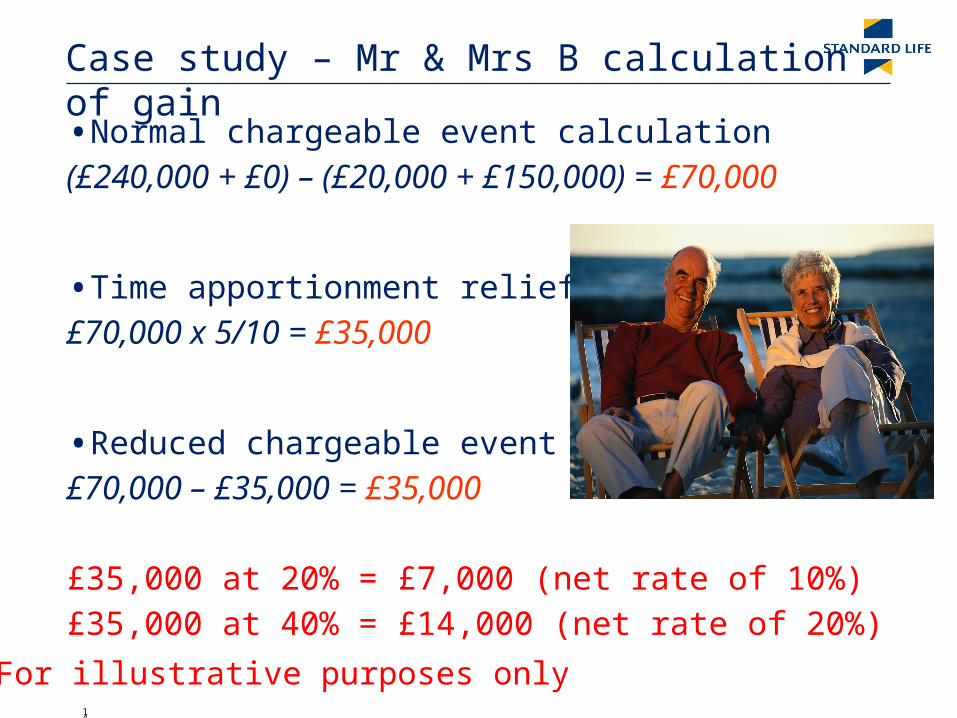

Case study – Mr & Mrs B calculation of gain

• Normal chargeable event calculation(£240,000 + £0) – (£20,000 + £150,000) = £70,000

• Time apportionment relief£70,000 x 5/10 = £35,000

• Reduced chargeable event gain£70,000 – £35,000 = £35,000

£35,000 at 20% = £7,000 (net rate of 10%)£35,000 at 40% = £14,000 (net rate of 20%)

For illustrative purposes only

15

Pre-emigration tax planning considerations

• Aim to maximise growth whilst UK resident– No tax on capital– No extra tax on fund yield

• Aim to maximise income when abroad– Tax efficiency

16

Tax planning considerations

• Taxation of 5% withdrawals

• Unused 5%s

• Maximise number of segments

• Additional premiums

• Local country tax rules

17

Moving/Retiring Abroad

• EU provider benefits– If a person leaves the UK to live in another EU country then

the Offshore Bond taxed as if a “home country” life policy

• Specific tax advantages for pre-emigration planning – e.g. France* – investing in an Offshore Bond today could

potentially save French income tax on the gains and French Inheritance Tax on the bond’s value on death*based on legal opinion received February 2009

18

Other considerations moving abroad

• Individuals party to a Trust– Settlor, Trustee or Beneficiary

• Valid wills

• Inheritance Tax

19

Important information

This presentation is for professional advisers only and should not be distributed to third parties.

The value of investments and any income from them may fall as well as rise and investors may not get back the amount originally invested. In addition, the value of investments may increase or decrease as a result of changes in exchange rates between currencies. Past performance is not a reliable guide to future performance.

Any reference to legislation and tax is based on Standard Life International’s understanding of law and tax practice in Ireland and the UK at May 2009. Tax reliefs mentioned are those currently available and may be subject to change.

No guarantees are given regarding the effectiveness of any arrangements entered into on the basis of this presentation. The value of tax reliefs to the investor depends on their financial circumstances and may vary.

20

Standard Life International

Standard Life International Limited is a company registered in Ireland (number 408507) with its Registered Office at 90 St Stephen's Green, Dublin 2. Telephone number 00353 16397766. Calls may be recorded/monitored.

Authorised and regulated by the Irish Financial Regulator for the conduct of Linked Long Term Insurance Business and subject to limited regulation by the Financial Services Authority. Details about the extent of our regulation by the Financial Services Authority are available from us on request.

Issued by: Standard Life International Limited© 2009 Standard Life