Embed Size (px)

Citation preview

1

CHAPTER M8CHAPTER M8

The Operating The Operating BudgetBudget

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

2

Learning Objective Learning Objective 1:1:

Describe some of Describe some of the benefits of the the benefits of the operating budget.operating budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

3

Operating BudgetOperating Budget

The The operating budgetoperating budget,, (also called the (also called the master operating budgetmaster operating budget,, or simply the or simply the master budgetmaster budget) is a plan that focuses on ) is a plan that focuses on the day-to-day operations of a firm.the day-to-day operations of a firm.

It is usually prepared for a one-year time It is usually prepared for a one-year time period, but could be for prepared for period, but could be for prepared for several years at a time.several years at a time.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

4

What is It?What is It?

The operating budget is essentially a set of The operating budget is essentially a set of forecasted financial statements. It also forecasted financial statements. It also includes several detailed schedules that includes several detailed schedules that provide the backup documentation for the provide the backup documentation for the financial statements.financial statements.

Forecasted financial statements are also Forecasted financial statements are also called called pro formapro forma statements. statements.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

5

Benefits of Benefits of BudgetingBudgeting

Budgeting serves as a guide.Budgeting serves as a guide. Budgeting helps allocate resources.Budgeting helps allocate resources. Budgeting encourages communication and Budgeting encourages communication and

coordination.coordination. Budgeting sets performance standards or Budgeting sets performance standards or

benchmarks.benchmarks.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

6

Serves as a GuideServes as a Guide

A budget is a plan, and a plan can help A budget is a plan, and a plan can help guide you through the future.guide you through the future.

A household budget can be a great aide in A household budget can be a great aide in helping a family control its spending.helping a family control its spending.

Likewise, an operating budget will help a Likewise, an operating budget will help a business to anticipate and handle the little business to anticipate and handle the little bumps in the road as they occur.bumps in the road as they occur.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

7

Helps Allocate Helps Allocate ResourcesResources

An operating budget helps the managers An operating budget helps the managers to determine the best possible allocation of to determine the best possible allocation of the company’s scarce resources (such as the company’s scarce resources (such as money, materials, labor, etc.).money, materials, labor, etc.).

The budgeting process may lead to the The budgeting process may lead to the discovery of potential bottlenecks before discovery of potential bottlenecks before they occur, thus allowing managers to take they occur, thus allowing managers to take action to alleviate the bottleneck.action to alleviate the bottleneck.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

8

Encourages Encourages Communication and Communication and

CoordinationCoordination An effective budgeting process requires that An effective budgeting process requires that

managers from all of the functional areas managers from all of the functional areas within the firm work together as a whole.within the firm work together as a whole.

The manufacturing department needs to The manufacturing department needs to know what the marketing department is doing know what the marketing department is doing and vice versa. By preparing the operating and vice versa. By preparing the operating budget, managers become more aware of the budget, managers become more aware of the firm’s other functional areas.firm’s other functional areas.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

9

Sets Performance Sets Performance StandardsStandards

A budget can also be thought of as a goal. A budget can also be thought of as a goal. After a goal has been set, you can then After a goal has been set, you can then measure your success in meeting that measure your success in meeting that goal.goal.

Managers are often rewarded for meeting Managers are often rewarded for meeting or exceeding their budgeted performance or exceeding their budgeted performance standards.standards.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

10

Learning Objective Learning Objective 2:2:

Describe the three Describe the three budgeted financial budgeted financial

statements contained in statements contained in the operating budget and the operating budget and

the other budgets that the other budgets that support the budgeted support the budgeted financial statements.financial statements.© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

11

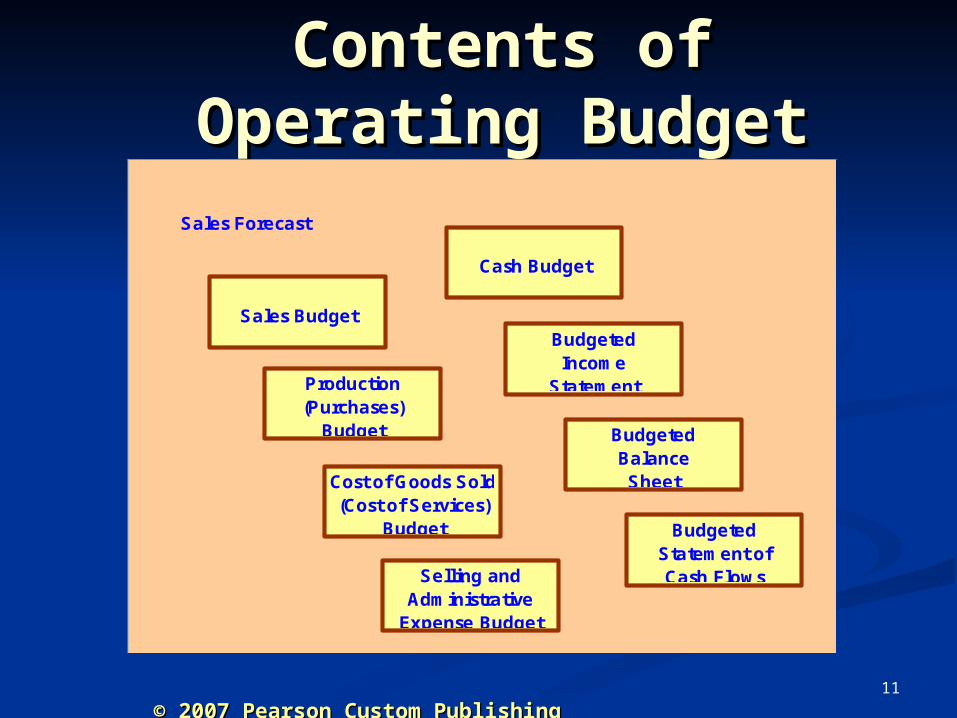

Contents of Contents of Operating BudgetOperating BudgetSales Forecast

Sales Budget

Production(Purchases)

Budget

Cost of Goods Sold(Cost of Services)

Budget

Selling andAdministrative

Expense Budget

Cash Budget

BudgetedStatement ofCash Flows

BudgetedBalanceSheet

BudgetedIncome

Statement

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

12

Sales BudgetSales Budget The first budget prepared is the The first budget prepared is the sales sales

budget.budget. The sales budget is based upon The sales budget is based upon the sales forecast.the sales forecast.

Information from the sales budget has an impact upon almost every other aspect of the operating budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

13

Production/Production/Purchases BudgetPurchases Budget

A manufacturing firm needs to prepare a A manufacturing firm needs to prepare a Production BudgetProduction Budget as well as a as well as a Purchases Purchases BudgetBudget for the materials used in production. for the materials used in production.

A merchandising firm needs to prepare a A merchandising firm needs to prepare a purchases budget for the inventory items that purchases budget for the inventory items that they sell.they sell.

The production and purchases budgets are The production and purchases budgets are very similar in format.very similar in format.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

14

Cost of Goods Sold Cost of Goods Sold BudgetBudget

The The Cost of Goods Sold BudgetCost of Goods Sold Budget is an is an integral part of the budgeted income integral part of the budgeted income statement for a manufacturing or statement for a manufacturing or merchandising firm. merchandising firm.

There is nothing unusual about preparing this There is nothing unusual about preparing this budget, it looks just like a normal cost of budget, it looks just like a normal cost of goods sold schedule. The only difference is goods sold schedule. The only difference is the use of estimated amounts. A service the use of estimated amounts. A service company uses a Cost of Services Budget.company uses a Cost of Services Budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

15

Selling and Selling and Administrative Administrative Expense BudgetExpense Budget

Another important part of the budgeted Another important part of the budgeted income statement is the income statement is the Selling and Selling and Administrative Expense Budget.Administrative Expense Budget.

Items included in this budget are advertising Items included in this budget are advertising and promotion, administrative and sales and promotion, administrative and sales salaries, and the expenses related to the salaries, and the expenses related to the corporate and sales offices.corporate and sales offices.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

16

Budgeted Income Budgeted Income StatementStatement

The The Budgeted Income StatementBudgeted Income Statement looks looks very much like any other income very much like any other income statement. The main difference is that the statement. The main difference is that the numbers being reported are expected numbers being reported are expected future results, rather than historical data.future results, rather than historical data.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

17

Cash BudgetCash Budget

The The Cash BudgetCash Budget shows an analysis of shows an analysis of the expected cash receipts and cash the expected cash receipts and cash disbursements for the company. Only the disbursements for the company. Only the cash flows from operating activities would cash flows from operating activities would typically appear in the cash budget.typically appear in the cash budget.

For example, the cash outflow for a capital For example, the cash outflow for a capital budgeting project would not be shown on budgeting project would not be shown on the cash budget.the cash budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

18

Budgeted Balance Budgeted Balance SheetSheet

A A Budgeted Balance SheetBudgeted Balance Sheet is prepared in is prepared in exactly the same manner as a standard exactly the same manner as a standard balance sheet, with the only exception being balance sheet, with the only exception being the use of estimated future amounts rather the use of estimated future amounts rather than historical amounts for assets, liabilities, than historical amounts for assets, liabilities, and owners’ equity.and owners’ equity.

Most of the numbers in the budgeted balance Most of the numbers in the budgeted balance sheet come from the other budgets. sheet come from the other budgets.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

19

Budgeted Statement Budgeted Statement of of

Cash FlowsCash Flows The The Budgeted Statement of Cash FlowsBudgeted Statement of Cash Flows is is

a comprehensive projection of all the cash a comprehensive projection of all the cash flows for the company during the period flows for the company during the period covered by the operating budget.covered by the operating budget.

Expected cash flows from operating Expected cash flows from operating activities, investing activities, and financing activities, investing activities, and financing activities would all be shown in this budget.activities would all be shown in this budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

20

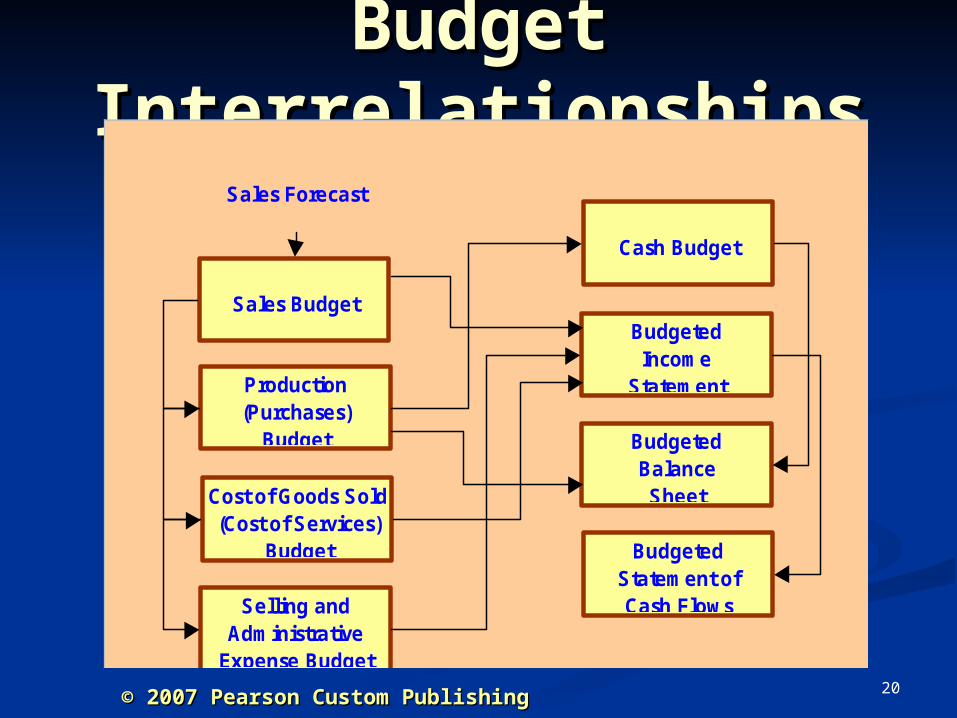

Budget Budget InterrelationshipsInterrelationships

Sales Forecast

Sales Budget

Production(Purchases)

Budget

Cost of Goods Sold(Cost of Services)

Budget

Selling andAdministrative

Expense Budget

Cash Budget

BudgetedStatement ofCash Flows

BudgetedBalanceSheet

BudgetedIncome

Statement

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

21

Learning Objective Learning Objective 3:3:

Compare and contrast Compare and contrast various approaches to various approaches to the preparation and the preparation and use of the operating use of the operating

budget.budget.© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

22

Different Approaches Different Approaches to Budgetingto Budgeting

There are many different approaches and There are many different approaches and theories that have been used for the theories that have been used for the budgeting process. Not any one approach budgeting process. Not any one approach is always best. What works well for one is always best. What works well for one company may not work well for the next.company may not work well for the next.

We will look at seven different approaches We will look at seven different approaches to budgeting.to budgeting.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

23

Perpetual BudgetingPerpetual Budgeting The first budgeting approach is The first budgeting approach is perpetual perpetual

budgetingbudgeting,, also called also called continual budgeting.continual budgeting.

With this approach, the operating budget is continually updated and extended. As one month or quarter ends, another month or quarter is added to the end of the budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

24

Incremental Incremental BudgetingBudgeting

The second approach is called The second approach is called incremental incremental budgeting.budgeting. In this case, the prior year’s In this case, the prior year’s budget is used as a starting point for the budget is used as a starting point for the current year. Only the changes (increments) current year. Only the changes (increments) need to be justified.need to be justified.

Incremental budgets are often used by Incremental budgets are often used by governmental agencies, including colleges governmental agencies, including colleges and universities.and universities.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

25

Zero-Based Zero-Based BudgetingBudgeting

The third approach is The third approach is zero-based zero-based budgeting.budgeting. This is an alternative to This is an alternative to incremental budgeting. The prior year’s incremental budgeting. The prior year’s budget is NOT used as a starting point for budget is NOT used as a starting point for the current year.the current year.

Each year, the full amount of each budget Each year, the full amount of each budget item needs to be justified. This is much item needs to be justified. This is much more time consuming, but probably leads more time consuming, but probably leads to a better budget.to a better budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

26

Top-Down Top-Down BudgetingBudgeting

The fourth approach to budgeting The fourth approach to budgeting is known as is known as top-down top-down budgeting.budgeting.

Top-down budgeting occurs Top-down budgeting occurs when the budget is prepared by when the budget is prepared by the top managers of the firm, and the top managers of the firm, and the budget is implemented by the the budget is implemented by the lower-level managers in the firm.lower-level managers in the firm.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

27

Imposed BudgetImposed Budget

Many top-down budgets are also Many top-down budgets are also imposed imposed budgets.budgets. This fifth approach to budgeting This fifth approach to budgeting occurs when top managers set the budget occurs when top managers set the budget amounts without any input from the lower amounts without any input from the lower level managers.level managers.

Low- and middle-level managers must Low- and middle-level managers must strive to meet the goals set forth by the strive to meet the goals set forth by the budget, not matter how unreasonable they budget, not matter how unreasonable they might be.might be.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

28

Bottom-Up Bottom-Up BudgetingBudgeting

The sixth approach to budgeting The sixth approach to budgeting is known as is known as bottom-up bottom-up budgeting.budgeting. As the name implies, As the name implies, this is a budget prepared by the this is a budget prepared by the lower-level managers of the firm.lower-level managers of the firm.

These managers then These managers then communicate their ideas to the communicate their ideas to the higher levels of management for higher levels of management for final approval.final approval.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

29

Participative Participative BudgetingBudgeting

The seventh approach to budgeting is known The seventh approach to budgeting is known as a as a participative budget.participative budget. In this approach, In this approach, managers and employees at all levels are managers and employees at all levels are included in the budgeting process.included in the budgeting process.

A bottom-up budget is also participatory in A bottom-up budget is also participatory in nature. However, you can have a top-down nature. However, you can have a top-down budget that is participatory if the top budget that is participatory if the top managers seek input from the lower levels.managers seek input from the lower levels.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

30

Learning Objective Learning Objective 4:4:

Describe the role of Describe the role of the sales forecast in the sales forecast in

the budgeting the budgeting process.process.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

31

Sales ForecastSales Forecast A A sales forecastsales forecast is an informed prediction is an informed prediction

of the level of sales that can be achieved in of the level of sales that can be achieved in future periods.future periods.

A reasonably accurate sales forecast is A reasonably accurate sales forecast is crucial to the overall operating budget. All crucial to the overall operating budget. All of the different parts of the operating budget of the different parts of the operating budget depend upon the sales forecast, thus it is depend upon the sales forecast, thus it is often called the cornerstone of the budget.often called the cornerstone of the budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

32

Sales Forecast Sales Forecast AccuracyAccuracy

Factors that influence the accuracy of the Factors that influence the accuracy of the sales forecast include:sales forecast include: General economy: inflation, recession, etc.?General economy: inflation, recession, etc.? Industry conditions: strength or weakness?Industry conditions: strength or weakness? Actions of competitors: increase or decrease Actions of competitors: increase or decrease

market share?market share? Technological developments: are you on the Technological developments: are you on the

cutting edge or being left behind?cutting edge or being left behind?

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

33

Learning Objective Learning Objective 5:5:

Prepare the budgets Prepare the budgets included in the included in the

operating budget.operating budget.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

34

Preparing the Preparing the Operating BudgetOperating Budget

To illustrate the preparation of the operating To illustrate the preparation of the operating budget, let’s use the example of a merchandising budget, let’s use the example of a merchandising company that sells baseball caps. This is their company that sells baseball caps. This is their only product. only product.

We will prepare the monthly operating budgets for We will prepare the monthly operating budgets for the first quarter of 2007. We will start with the the first quarter of 2007. We will start with the actual balance sheet for Dec. 31, 2006, and then actual balance sheet for Dec. 31, 2006, and then the sales forecast and sales budget for the first the sales forecast and sales budget for the first quarter of 2007.quarter of 2007.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

35

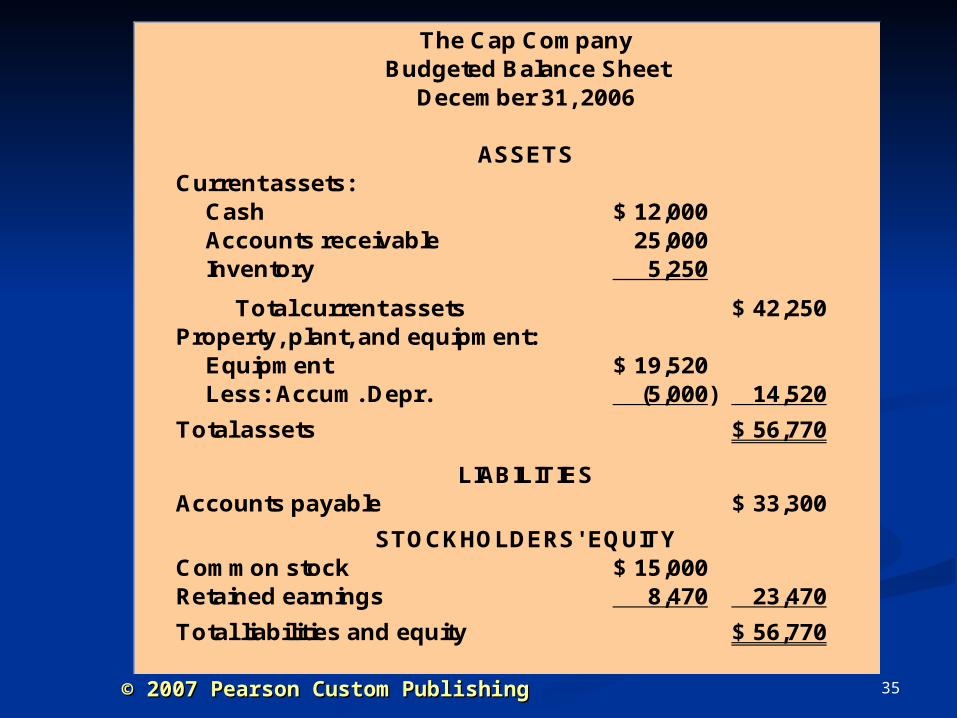

The Cap CompanyBudgeted Balance Sheet

December 31, 2006

ASSETSCurrent assets:

Cash 12,000$ Accounts receivable 25,000 Inventory 5,250

Total current assets 42,250$ Property, plant, and equipment:

Equipment 19,520$ Less: Accum. Depr. (5,000) 14,520

Total assets 56,770$

LIABILITIESAccounts payable 33,300$

STOCKHOLDERS' EQUITYCommon stock 15,000$ Retained earnings 8,470 23,470

Total liabilities and equity 56,770$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

36

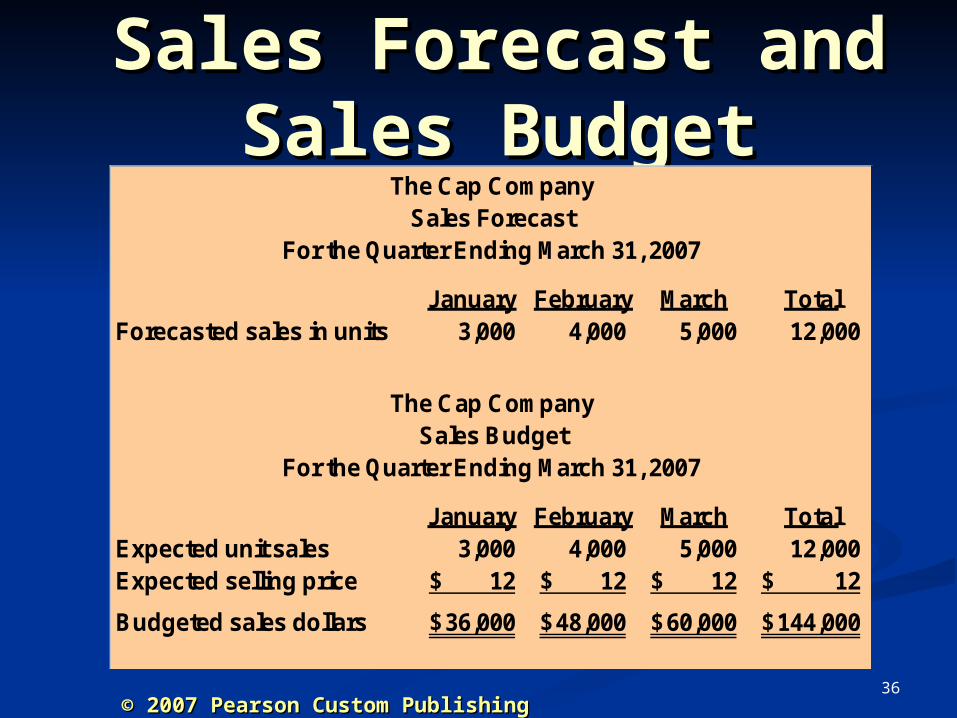

Sales Forecast and Sales Forecast and Sales BudgetSales Budget

The Cap CompanySales Forecast

For the Quarter Ending March 31, 2007

January February March TotalForecasted sales in units 3,000 4,000 5,000 12,000

The Cap CompanySales Budget

For the Quarter Ending March 31, 2007

January February March TotalExpected unit sales 3,000 4,000 5,000 12,000 Expected selling price 12$ 12$ 12$ 12$

Budgeted sales dollars 36,000$ 48,000$ 60,000$ 144,000$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

37

Cost of Goods Sold Cost of Goods Sold BudgetBudget

The Cap Company purchases the baseball The Cap Company purchases the baseball caps for $7.00 each.caps for $7.00 each.

The Cap CompanyCost of Goods Sold Budget

For the Quarter Ending March 31, 2007

January February March TotalExpected unit sales 3,000 4,000 5,000 12,000 Expected purchase cost 7$ 7$ 7$ 7$

Budgeted sales dollars 21,000$ 28,000$ 35,000$ 84,000$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

38

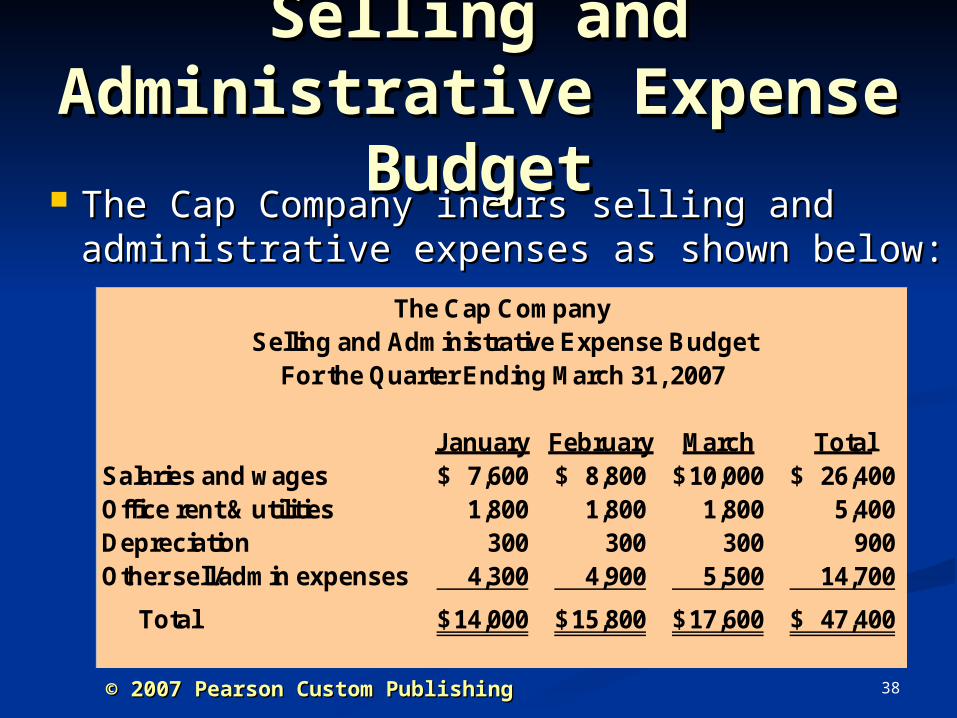

Selling and Selling and Administrative Expense Administrative Expense

BudgetBudget The Cap Company incurs selling and The Cap Company incurs selling and

administrative expenses as shown below:administrative expenses as shown below:The Cap Company

Selling and Administrative Expense BudgetFor the Quarter Ending March 31, 2007

January February March TotalSalaries and wages 7,600$ 8,800$ 10,000$ 26,400$ Office rent & utilities 1,800 1,800 1,800 5,400 Depreciation 300 300 300 900 Other sell/admin expenses 4,300 4,900 5,500 14,700

Total 14,000$ 15,800$ 17,600$ 47,400$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

39

Budgeted Income Budgeted Income StatementStatement

Using the information from the three Using the information from the three previous budgets, we can prepare the previous budgets, we can prepare the budgeted income statement.budgeted income statement.

Notice how the sales forecast drives the Notice how the sales forecast drives the budgeted income statement. If we change budgeted income statement. If we change the sales forecast, all of the other budgets the sales forecast, all of the other budgets would need to be changed also.would need to be changed also.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

40

Budgeted Income Budgeted Income StatementStatement

The Cap CompanyBudgeted Income Statement

For the Quarter Ending March 31, 2007

January February March TotalSales 36,000$ 48,000$ 60,000$ 144,000$ Cost of goods sold 21,000 28,000 35,000 84,000

Gross profit 15,000$ 20,000$ 25,000$ 60,000$ Selling and admin. expenses 14,000 15,800 17,600 47,400

Net income 1,000$ 4,200$ 7,400$ 12,600$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

41

Purchases BudgetPurchases Budget

The purchases budget was not needed to The purchases budget was not needed to prepare the budgeted income statement. prepare the budgeted income statement. However, it is needed to prepare the However, it is needed to prepare the budgeted balance sheet.budgeted balance sheet.

In particular, the budgeted purchases will In particular, the budgeted purchases will have an impact on three major balance have an impact on three major balance sheet items: cash, inventory, and accounts sheet items: cash, inventory, and accounts payable.payable.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

42

Purchases BudgetPurchases Budget Let’s assume that The Cap Company tries Let’s assume that The Cap Company tries

to maintain an inventory equal to 25% of to maintain an inventory equal to 25% of the next month’s budgeted sales volume.the next month’s budgeted sales volume.

In other words, at the end of December In other words, at the end of December they should have had an inventory equal they should have had an inventory equal to 25% of the caps they expected to sell in to 25% of the caps they expected to sell in January.January.

The ending inventory for March will be The ending inventory for March will be 25% of the expected April sales of 4,400 25% of the expected April sales of 4,400 units.units.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

43

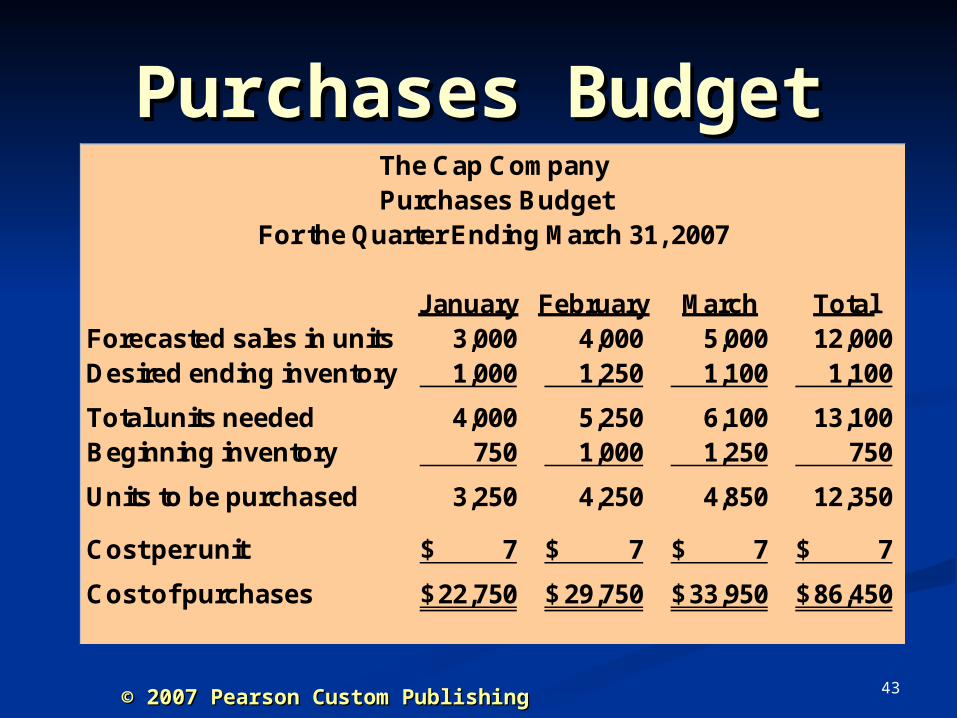

Purchases BudgetPurchases BudgetThe Cap CompanyPurchases Budget

For the Quarter Ending March 31, 2007

January February March TotalForecasted sales in units 3,000 4,000 5,000 12,000 Desired ending inventory 1,000 1,250 1,100 1,100

Total units needed 4,000 5,250 6,100 13,100 Beginning inventory 750 1,000 1,250 750

Units to be purchased 3,250 4,250 4,850 12,350

Cost per unit 7$ 7$ 7$ 7$

Cost of purchases 22,750$ 29,750$ 33,950$ 86,450$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

44

Budgeting Cash Budgeting Cash FlowsFlows

We need to determine an estimated We need to determine an estimated ending cash balance before we can ending cash balance before we can prepare the budgeted balance sheet. prepare the budgeted balance sheet.

Another factor that could impact the Another factor that could impact the balance sheet is the possibility of needing balance sheet is the possibility of needing some short-term financing due to a some short-term financing due to a shortage of cash.shortage of cash.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

45

Cash BudgetCash Budget The preparation of a cash budget is an The preparation of a cash budget is an

important step in the operating budget important step in the operating budget process. process.

The cash budget provides information not The cash budget provides information not readily available on the other budgets readily available on the other budgets previously prepared. Keep in mind that the previously prepared. Keep in mind that the budgeted income statement is based on budgeted income statement is based on accrual accounting concepts, not cash flows.accrual accounting concepts, not cash flows.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

46

Cash BudgetCash Budget For The Cap Company, let’s make the For The Cap Company, let’s make the

following assumptions about cash flows:following assumptions about cash flows: Cash receipts from sales tend to be collected Cash receipts from sales tend to be collected

50% in the month of sale and 50% in the 50% in the month of sale and 50% in the following month.following month.

Cash disbursements for purchases are always Cash disbursements for purchases are always made in the month following the purchase.made in the month following the purchase.

Other cash disbursements are made in the Other cash disbursements are made in the month that the expense is incurred.month that the expense is incurred.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

47

Cash BudgetCash Budget

Additional information needed about The Additional information needed about The Cap Company:Cap Company: A minimum balance of $10,000 should be A minimum balance of $10,000 should be

maintained. Any shortfall can be borrowed maintained. Any shortfall can be borrowed from the local bank at 12% annual interest.from the local bank at 12% annual interest.

December purchases totaled $33,300.December purchases totaled $33,300. December sales totaled $50,000.December sales totaled $50,000.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

48

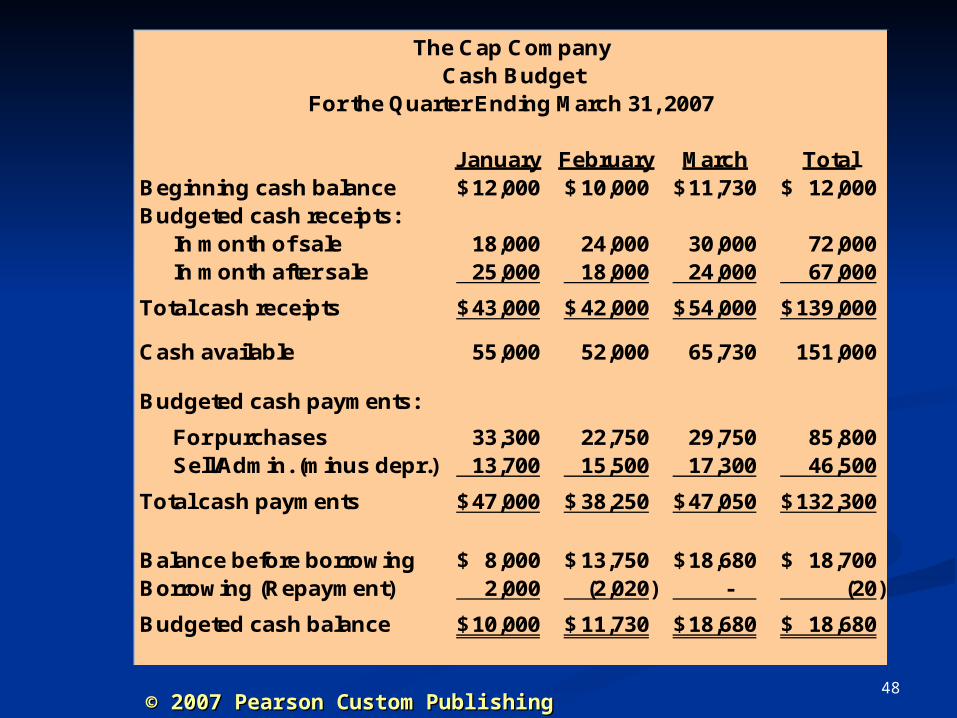

The Cap CompanyCash Budget

For the Quarter Ending March 31, 2007

January February March TotalBeginning cash balance 12,000$ 10,000$ 11,730$ 12,000$ Budgeted cash receipts:

In month of sale 18,000 24,000 30,000 72,000 In month after sale 25,000 18,000 24,000 67,000

Total cash receipts 43,000$ 42,000$ 54,000$ 139,000$

Cash available 55,000 52,000 65,730 151,000

Budgeted cash payments:

For purchases 33,300 22,750 29,750 85,800 Sell/Admin. (minus depr.) 13,700 15,500 17,300 46,500

Total cash payments 47,000$ 38,250$ 47,050$ 132,300$

Balance before borrowing 8,000$ 13,750$ 18,680$ 18,700$ Borrowing (Repayment) 2,000 (2,020) - (20)

Budgeted cash balance 10,000$ 11,730$ 18,680$ 18,680$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

49

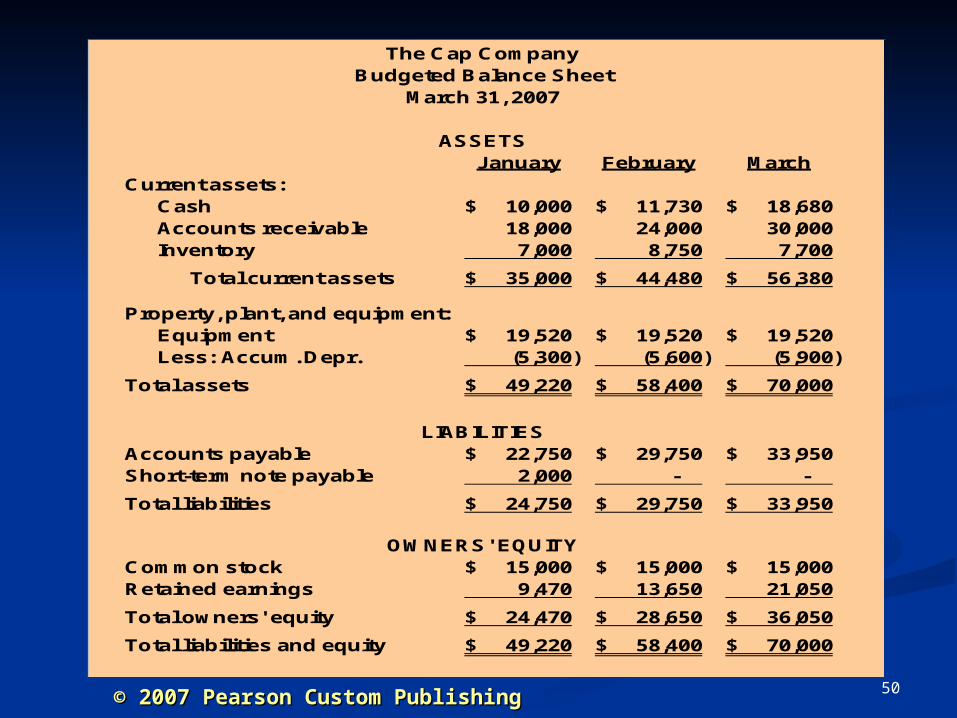

Building the Balance Building the Balance SheetSheet

We now have enough information to prepare We now have enough information to prepare the budgeted balance sheet for The Cap the budgeted balance sheet for The Cap Company. We can determine the accounts Company. We can determine the accounts receivable and accounts payable balances receivable and accounts payable balances from the information used to prepare the cash from the information used to prepare the cash budget.budget.

Information about owners’ equity and equipment Information about owners’ equity and equipment comes from the Dec. 31 balance sheet.comes from the Dec. 31 balance sheet.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

50

The Cap CompanyBudgeted Balance Sheet

March 31, 2007

ASSETSJanuary February March

Current assets:Cash 10,000$ 11,730$ 18,680$ Accounts receivable 18,000 24,000 30,000 Inventory 7,000 8,750 7,700

Total current assets 35,000$ 44,480$ 56,380$

Property, plant, and equipment:Equipment 19,520$ 19,520$ 19,520$ Less: Accum. Depr. (5,300) (5,600) (5,900)

Total assets 49,220$ 58,400$ 70,000$

LIABILITIESAccounts payable 22,750$ 29,750$ 33,950$ Short-term note payable 2,000 - -

Total liabilities 24,750$ 29,750$ 33,950$

OWNERS' EQUITYCommon stock 15,000$ 15,000$ 15,000$ Retained earnings 9,470 13,650 21,050

Total owners' equity 24,470$ 28,650$ 36,050$

Total liabilities and equity 49,220$ 58,400$ 70,000$

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

51

Discussion Discussion QuestionsQuestions

Can you verify the accounts receivable Can you verify the accounts receivable balance for March 31? Where do you find balance for March 31? Where do you find the necessary information?the necessary information?

Can you verify the accounts payable Can you verify the accounts payable balance for March 31? Where do you find balance for March 31? Where do you find the necessary information?the necessary information?

Can you verify the accumulated Can you verify the accumulated depreciation for all three months?depreciation for all three months?

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

52

Discussion Discussion QuestionsQuestions

Question: Can you verify the retained Question: Can you verify the retained earnings balance for January 31, 2007?earnings balance for January 31, 2007?

Answer: Take the Dec. 31 balance of $8,470 Answer: Take the Dec. 31 balance of $8,470 and add the $1,000 January income.and add the $1,000 January income.

Question: Can you verify the retained Question: Can you verify the retained earnings balance for February 28, 2007?earnings balance for February 28, 2007?

Hint: There is a “little” item in the cash Hint: There is a “little” item in the cash budget that you need to include.budget that you need to include.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

53

Learning Objective Learning Objective 6:6:

Describe the Describe the appropriate use of appropriate use of

the operating budget the operating budget in the overall in the overall

management process.management process.© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

54

Using the BudgetUsing the Budget The budget has an impact on all areas of The budget has an impact on all areas of

management performance. management performance. Preparing the budget is part of the Preparing the budget is part of the

planningplanning process. process. Day-to-day efforts to achieve budgeted Day-to-day efforts to achieve budgeted

amounts are part of the amounts are part of the operating operating process.process. Comparison of actual results with budgeted Comparison of actual results with budgeted

results is part of the results is part of the controlcontrol process.process.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

55

Performance to Performance to Budget EvaluationBudget Evaluation

A major part of the control function of A major part of the control function of management is the management is the performance to performance to budgetbudget evaluation. evaluation.

The main instrument used in this The main instrument used in this evaluation is the evaluation is the budget budget performance report.performance report. This report This report indicates any variances between actual indicates any variances between actual results and budgeted results.results and budgeted results.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

56

The Cap Company The Cap Company Budget ReportBudget Report

Assume the following results for The Cap Assume the following results for The Cap Company for the first quarter of 2007.Company for the first quarter of 2007.

The Cap CompanyJanuary - March, 2007

Budget Performance Report

Description Budget Actual VarianceSales 144,000 148,000 4,000 F Salaries/Wages 26,400 28,000 1,600 U Other sell/admin 14,700 14,000 700 F

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

57

Three Truths About Three Truths About BudgetingBudgeting

Since all of the budgets are interrelated and Since all of the budgets are interrelated and all of the budgets stem from the sales all of the budgets stem from the sales forecast, there are forecast, there are three truths about three truths about budgetingbudgeting that should be kept in mind: that should be kept in mind:

1. If the sales forecast is inaccurate, the 1. If the sales forecast is inaccurate, the operating budget will be inaccurate.operating budget will be inaccurate.

2. The sales forecast will be inaccurate.2. The sales forecast will be inaccurate. 3. The operating budget will be inaccurate.3. The operating budget will be inaccurate.

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing

58

End of Chapter M8End of Chapter M8

© 2007 Pearson Custom Publishing© 2007 Pearson Custom Publishing