Embed Size (px)

Citation preview

1

Chapter 6

Managements’ Assertions

Financial Statement Assertions

Page 58 - 61

2

What is the overall objective of the independent auditor in conducting an audit?

Pei

3

Overall ObjectiveAU-C Section 200 Overall Objectives of the Independent Auditor and Conduct of an Audit in

.11 The overall objectives of the auditor, in conducting an audit of financial statements, are to

a. obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, thereby enabling the auditor to express an opinion on whether the financial statements are presented fairly, in all material respects, in accordance with an applicable financial reporting framework; and

b. report on the financial statements, and communicate as required by GAAS, in accordance with the auditor's findings.

4

What is a misstatement ?

David

5

misstatement

A difference between the amount, classification, presentation, or disclosure of a reported financial statement item and the amount, classification, presentation, or disclosure that is required for the item to be presented fairly in accordance with the applicable financial reporting framework (GAAP).

6

Audit objectives

7

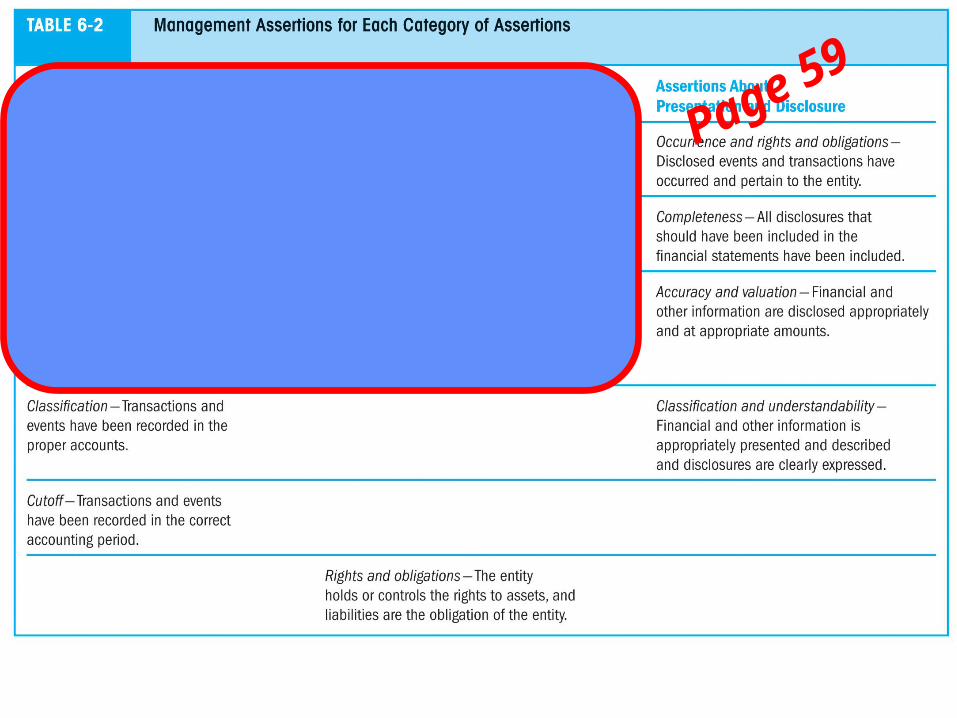

Page 59

8

9

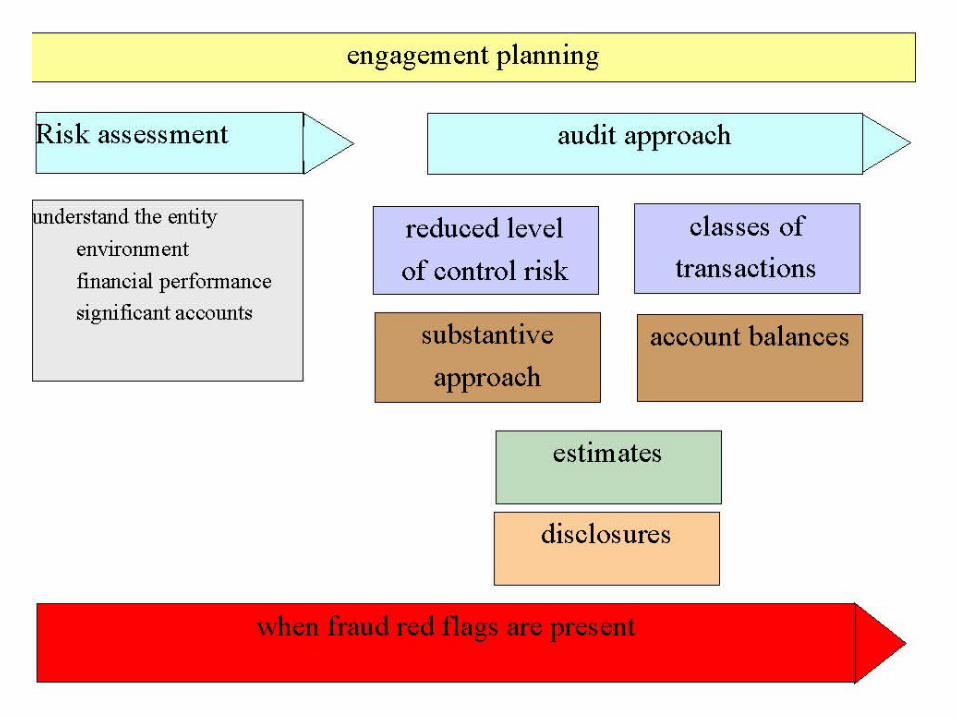

We typically audit transactions

differently than account balances

differently than disclosures

10

Priya

Describe 2 Significant Classes of Transactions

11

Classes of Transactions

Accounts receivable xxx.xx

Salesxxx.xx

Cash xxx.xx

Accounts receivablexxx.xx

12

sales journal

date customer invoice post amount1750 (120/401)

8/4 Grace Miller 418 1008/6 Ben Rogers 419 858/7 James Hollis 420 20

8/15 Susan Harper 421 908/18 Sally Rogers 422 2008/21 Robert Tanner 423 4508/27 William Fisher 424 808/30 Becky Thatcher 425 180

1205 (120/401)

13

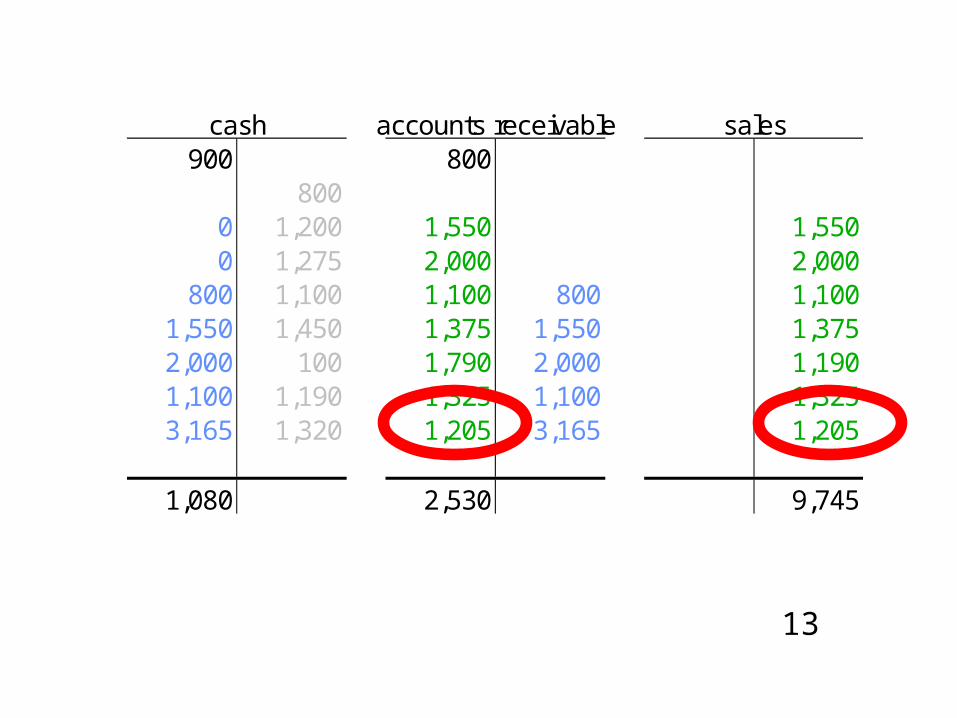

cash accounts receivable sales900 800

8000 1,200 1,550 1,5500 1,275 2,000 2,000

800 1,100 1,100 800 1,1001,550 1,450 1,375 1,550 1,3752,000 100 1,790 2,000 1,1901,100 1,190 1,325 1,100 1,3253,165 1,320 1,205 3,165 1,205

1,080 2,530 9,745

14

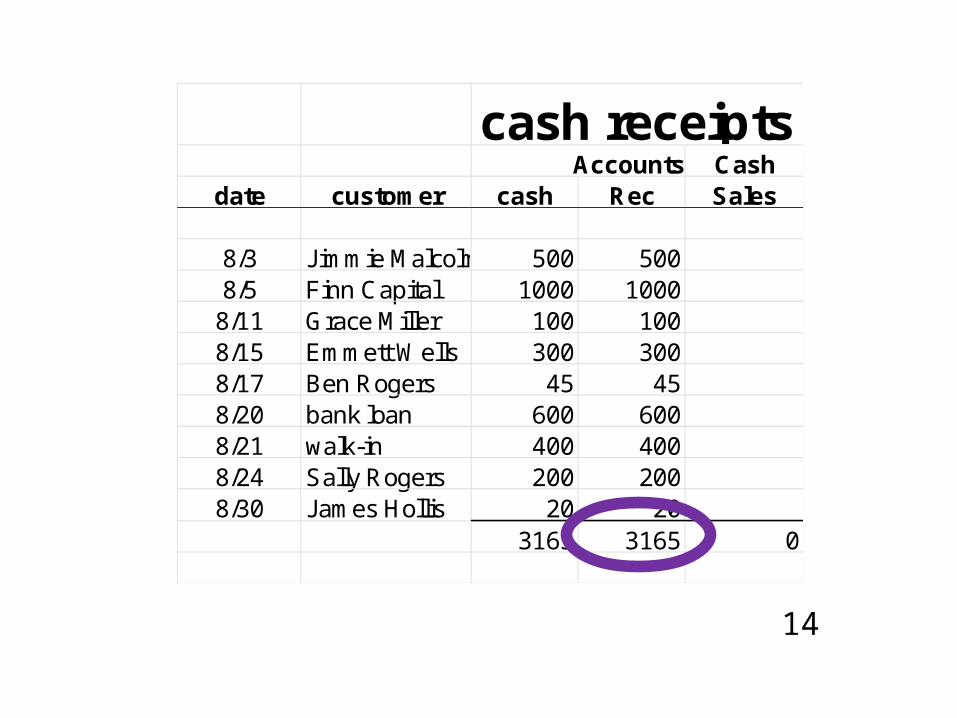

cash receipts jnlAccounts Cash

date customer cash Rec Sales

8/3 Jimmie Malcolm 500 5008/5 Finn Capital 1000 1000

8/11 Grace Miller 100 1008/15 Emmett Wells 300 3008/17 Ben Rogers 45 458/20 bank loan 600 6008/21 walk-in 400 4008/24 Sally Rogers 200 2008/30 James Hollis 20 20

3165 3165 0

15

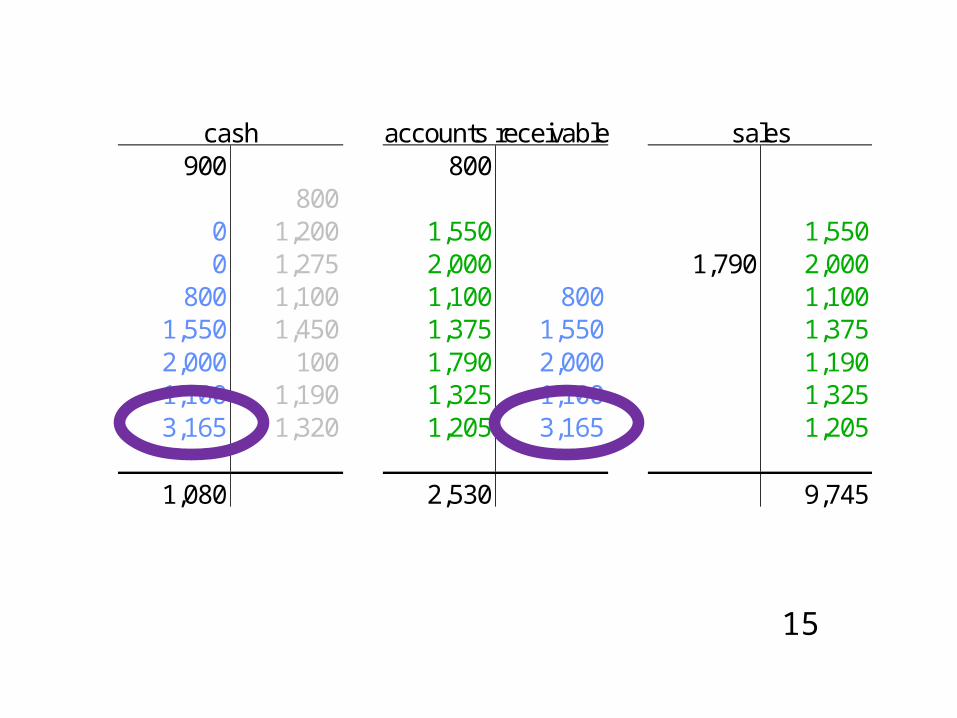

cash accounts receivable sales900 800

8000 1,200 1,550 1,5500 1,275 2,000 1,790 2,000

800 1,100 1,100 800 1,1001,550 1,450 1,375 1,550 1,3752,000 100 1,790 2,000 1,1901,100 1,190 1,325 1,100 1,3253,165 1,320 1,205 3,165 1,205

1,080 2,530 9,745

16

Name three management assertions that relate to transactions.

Algernon

17

Name three managements’ assertions that relate to account balances.

Cody

18

Reflecting on the Vouch & Trace example

To which assertion would the following situation relate?

There is a balance in the Sales Journal for which there is no underlying Invoice

Emily

19

Reflecting on the Vouch & Trace example

To which assertion would the following situation relate?

There is a balance in the Sales Journal for which there is no underlying Shipping Document

Jeffrey

20

Reflecting on the Vouch & Trace example

To which assertion would the following situation relate?

The price on the Invoice exceeds the price on the Sales Order

Bart

21

Reflecting on the Vouch & Trace example

To which assertion would the following situation relate?

The quantities on the Invoice exceed the quantities on the Shipping Document

Jo Ellen

22

Reflecting on the Vouch & Trace example

To which assertion would the following situation relate?

You locate a Sales Order, Shipping Document and Invoice for which there is no entry in the Sales Journal

Jordan

23

Reflecting on Inventory

The audit client’s records indicate they have 187 cars in inventory but they only locate 184 cars when they take their physical inventory

Joseph

24

Reflecting on Inventory

The audit client’s Inventory records indicate each new car cost $28,500 but the Vendor Invoices indicate each car actually cost $27,500.

Juancarlos

25

Reflecting on Inventory

The client failed to adjust their inventory balance to Lower of Cost or Market even though cost exceeds the replacement cost

Meredith

26

Reflecting on Notes Payable

The balance sheet includes 3 Notes Payable at the local bank but a confirmation letter from the bank indicates there are actually 4 outstanding Notes Payable

Garren

![S.D.spiegeleire, Et Al. (the Hague C. for Strategic S.) (2014)[55][61] Assessing Assertions of Assertiveness the Chinese and Russian Cases (Google eBook)](https://img.pdfslide.us/doc/110x75/55cf8ead550346703b947ea9/sdspiegeleire-et-al-the-hague-c-for-strategic-s-20145561-assessing.jpg)