Embed Size (px)

Citation preview

1

Chapter 05Chapter 05 Time Value of Money 2:Analyzing Annuity Cash Flows

McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Introduction

• Time Value of Money calculations– Can deal with either single cash flows (Chapter 4)– or multiple cash flows over time (Chapter 5)

5-2

Future Value of Multiple Cash Flows

• Multiple cash flows– Regular, evenly-spaced

• Car loans and home mortgage loans• Saving for retirement• Companies paying interest on debt• Companies paying dividends

5-3

Future Value – Several Cash Flows• Concept: Compounding

– Value in the future– Different cash flows paid in at different times

...

5-4

Finding FV – Several Cash FlowsExample

...

• Assumptions– Invest $100 today (compounds for 3 years)– Invest $125 at end of year 2 (compounds for 2

years)– Invest $150 at end of year 3 (compounds for 1

year)– Interest rates: 7%

5-5

FV Several Cash Flows Time Line Example

...

Several (Different) Cash Flow Values

5-6

Future Value – Level Cash Flows• Concept: Compounding• Also called “annuities”

– Value in the future– Same cash flows paid in every period

...

5-7

Finding FV – Level Cash Flows/Annuity Example

...

• Assumptions:– Invest $100 at the end of each year for 5 years– Interest rates: 8%

5-8

Level Cash Flows Time Line Example

...Level (same) Cash Flows Each Period

5-9

Future Value – Multiple Annuities• Concept: Compounding – annuity equation to

compute future value – two levels of cash flows• To solve for multiple annuities, compute FV for

each separately and add them together

...

5-10

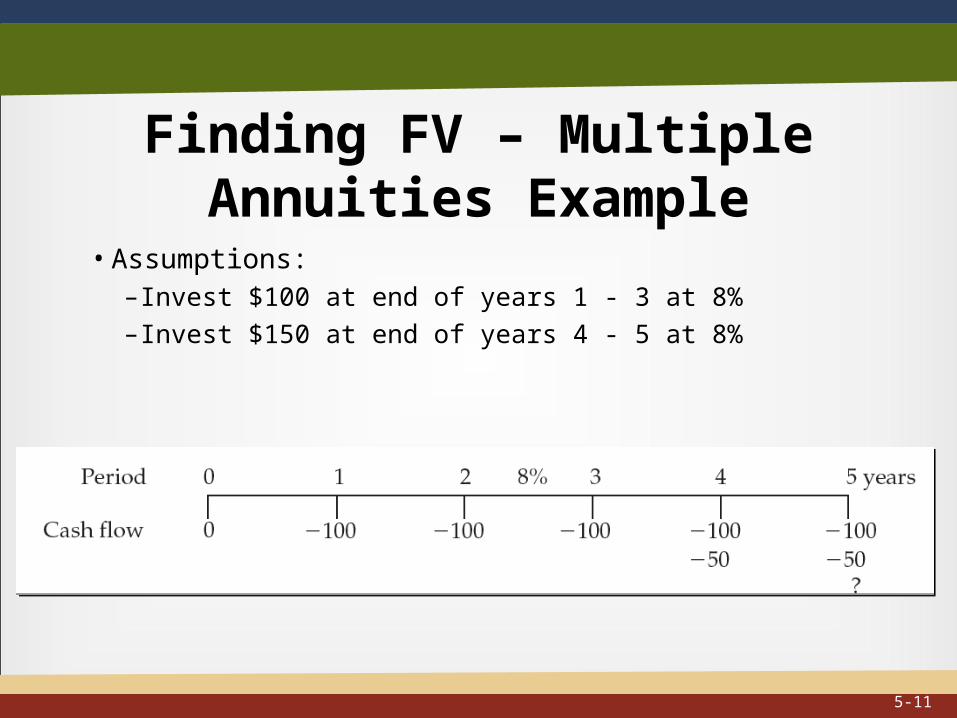

Finding FV – Multiple Annuities Example

...

• Assumptions:– Invest $100 at end of years 1 - 3 at 8%– Invest $150 at end of years 4 - 5 at 8%

5-11

Future Value – Multiple AnnuitiesStep 1 (same as FV of Level Cash Flows Calculation)

Step 2

Add two sums together – FV of both is $690.66

Step 3

5-12

Present Value of Multiple Cash Flows

• Multiple cash flows:– Car loans and home mortgage loans– Determining value of business opportunities

5-13

Present Value – Several Cash Flows• Concept: Discounting

– Value of future sum today– Different cash flows paid in at different times

...

5-14

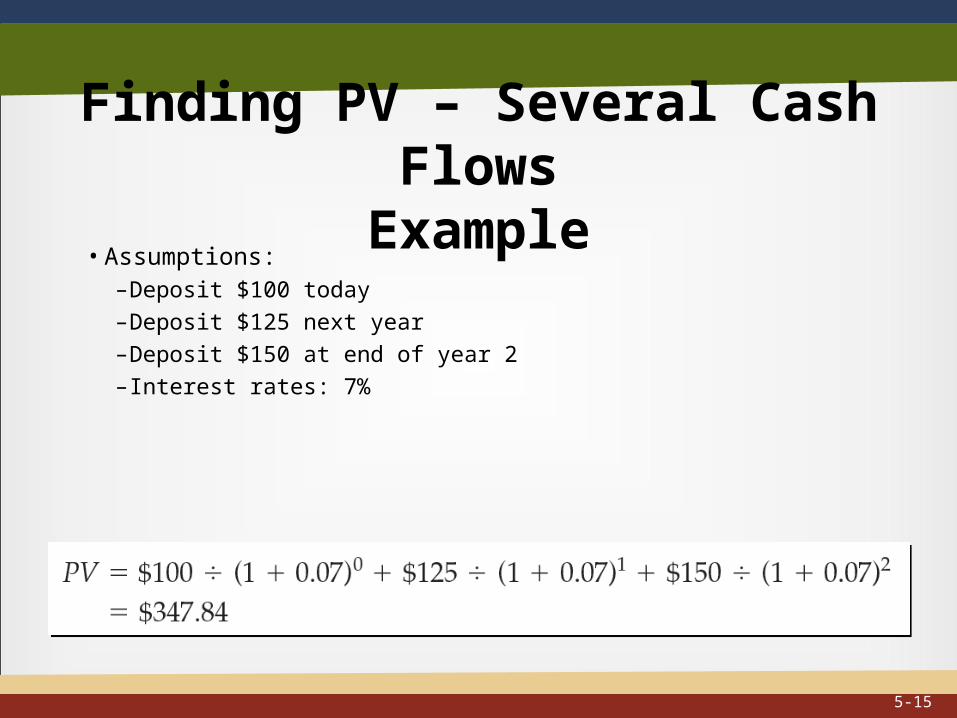

Finding PV – Several Cash FlowsExample

...

• Assumptions:– Deposit $100 today – Deposit $125 next year – Deposit $150 at end of year 2 – Interest rates: 7%

5-15

PV Several Cash Flows Time Line Example

...

5-16

PV Several Cash Flows

$150/ (1.07)2

$0 / (1.07)3

0 1 2 3

$100 $125 $150 $0

$116.82

$131.02

$0.00

$125/(1.07)

$347.84

5-17

Present Value – Level Cash Flows• Concept: Discounting

– Value of future sum today– Level cash flows paid in at different times

• Most loans set up with even payments throughout life of loan

...

5-18

Finding PV – Level Cash FlowsExample

...

• Assumptions:– $100 payments at end of each year for 5 years– Interest rates: 8% per year

5-19

PV Level Cash Flows Time Line Example

...

5-20

Present Value – Multiple Annuities• Concept: Discounting

– Changing level cash flows– Ex: Alex Rodriguez’s baseball contract

...

5-21

PV – Multiple Annuities Example

...

• Assumptions (Alex Rodriguez’s Contract):– $10 million signing bonus– $21 million per year from 2001 – 2004– $25 million per year in 2005 and 2006– $27 million per year in 2007 - 2010– Interest rates: 8% per year

5-22

PV Multiple Annuities Example (cont.)

5-23

Perpetuity – Special Annuity• Concept: Discounting

– Stream of level cash flows paid forever– Preferred stocks are an example– Value of investment is present value of all

future annuity payments

...

5-24

Ordinary Annuities vs. Annuities Due

• Ordinary Annuity– Payment occurs at the end of each period

• Annuity Due– Payment occurs at the beginning of each period

5-25

Annuity Due Time Line Example

• Cash flows at beginning, not at end of period• Five annuity-due cash flows basically same as

payment today plus 4-year ordinary annuity• Payments occur one period sooner than

ordinary annuity -- earn extra period of interest

...

5-26

Future Value of Annuity Due

• Concept: Compounding– Value of future sum today– Cash flows at beginning of each period

...

5-27

Future Value of Annuity Due

...

– Assumptions:• Assumes cash flows at the beginning of each period • 5 annuity-due cash flows of $100 each

– First cash flow compounds for 5 years– Last cash flow compounds for 1 year

• Interest rates: 8%

5-28

Present Value of Annuity Due• Concept: Discounting

– Today’s value of future sum– Cash flows at beginning of each period

...

5-29

Present Value of Annuity Due

...

• Assumptions:– Cash flows at beginning of period – 5 annuity-due cash flows of $100

• First cash flow paid today – not discounted • Last cash flow discounted 4 years• All cash flows discounted for one year less than ordinary annuity

• Interest rates: 8%

5-30

Compounding Frequency

• Used in situations that do not use yearly time periods– Semiannual bond payments– Quarterly stock dividends– Consumer loans – monthly payments

5-31

Effect of Compounding Frequency

...

• Assumptions:– $100 deposit today– 12% annual interest rate– Bank compounds interest at six months instead of end of year– Interest is earned on interest

5-32

EARS and APRS

...

• Quoted, or nominal rate called annual percentage rate (APR)• Rate that incorporates compounding called effective annual rate (EAR)• Relationship between APR and EAR:

5-33

EARS vs. APR Example

...

– Assumptions:• Borrow $100 today• 12% annual interest rate• APR: Loan compounds annually -- you pay 12.00% • EARS: Loan compounds monthly -- you pay 12.68%

– Formula to convert APR to EAR:

11212.0

112

EAR

5-34

Annuity Loans

• Compares payments

• Compares implied interest rate

5-35

Finding Payments on Amortized Loan

• Concept:– Rearrange PV of annuity formula to solve for payment

...

5-36

Payments on Amortized LoanExample

...

• Assumptions:– Need $10,000 to buy car– Loan term: 4 years– Interest rate: 9%

• Use interest rate of 0.75 % (=9%/12) and 48 periods (=4 X 12)

5-37