Embed Size (px)

Citation preview

11

Ch. 13: Exchange Rates and Ch. 13: Exchange Rates and the Foreign Exchange the Foreign Exchange

Market: An Asset ApproachMarket: An Asset Approach

22

Exchange RatesExchange Rates

Exchange rate is the price of one currency Exchange rate is the price of one currency in terms of another.in terms of another.

On October 18, 2002 at 15:48:14 GMT, On October 18, 2002 at 15:48:14 GMT, 1USD was worth €1.0301 or 1€ was worth 1USD was worth €1.0301 or 1€ was worth $0.9709.$0.9709.

On Jan. 1, 1999, 1€=$1.1497; on March 5, On Jan. 1, 1999, 1€=$1.1497; on March 5, 2001, 1€=$0.9358.2001, 1€=$0.9358.

You can check the exchange rates at You can check the exchange rates at http://www.economist.com/markets/currency/http://www.economist.com/markets/currency/

33

Exchange RatesExchange RatesChanges in the exchange rates affect Changes in the exchange rates affect

the prices of imports, exports, foreign the prices of imports, exports, foreign assets purchased by locals and local assets purchased by locals and local assets purchased by foreigners.assets purchased by foreigners.

When the domestic currency becomes When the domestic currency becomes more valuable (appreciates, becomes more valuable (appreciates, becomes stronger), foreign commodities and stronger), foreign commodities and assets become cheaper.assets become cheaper.

44

Exchange RatesExchange Rates If €1=$1.1497 on 01/01/99 and If €1=$1.1497 on 01/01/99 and

€1=$0.9358 on 03/05/01, then euro €1=$0.9358 on 03/05/01, then euro depreciated and USD appreciated in this depreciated and USD appreciated in this period.period.

European goods and assets would be European goods and assets would be cheaper at the recent date. cheaper at the recent date.

American goods and assets would be more American goods and assets would be more expensive at the recent date.expensive at the recent date.

In this example exchange rates are given In this example exchange rates are given per euro.per euro.

55

Price ComparisonsPrice Comparisons Suppose on 1/01/99 and 3/5/01 the price of a Suppose on 1/01/99 and 3/5/01 the price of a

Ferrari remained €100,000.Ferrari remained €100,000. Likewise, the price of a server at those dates Likewise, the price of a server at those dates

was $50,000.was $50,000. A Ferrari would have cost Americans A Ferrari would have cost Americans

$114,970 on 1/01/99 and $93,580 on 3/5/01.$114,970 on 1/01/99 and $93,580 on 3/5/01. A server would have cost Europeans A server would have cost Europeans

[($50,000)(€1/$1.1497)]=€43,489.61 on [($50,000)(€1/$1.1497)]=€43,489.61 on 1/01/99 and on 3/5/01 [($50,000)1/01/99 and on 3/5/01 [($50,000)(€1/$0.9358)]=€53,430.22.(€1/$0.9358)]=€53,430.22.

66

Price ComparisonsPrice Comparisons

If the currency appreciates (as in the previous If the currency appreciates (as in the previous example for USD) imports become cheaper example for USD) imports become cheaper and exports more expensive.and exports more expensive.

US can get more European goods for the US can get more European goods for the same amount of exports: terms of trade same amount of exports: terms of trade improvement.improvement.

If the currency depreciates (€ in the example), If the currency depreciates (€ in the example), Europe has to give up more exports for the Europe has to give up more exports for the same amount of imports: terms of trade same amount of imports: terms of trade deterioration.deterioration.

77

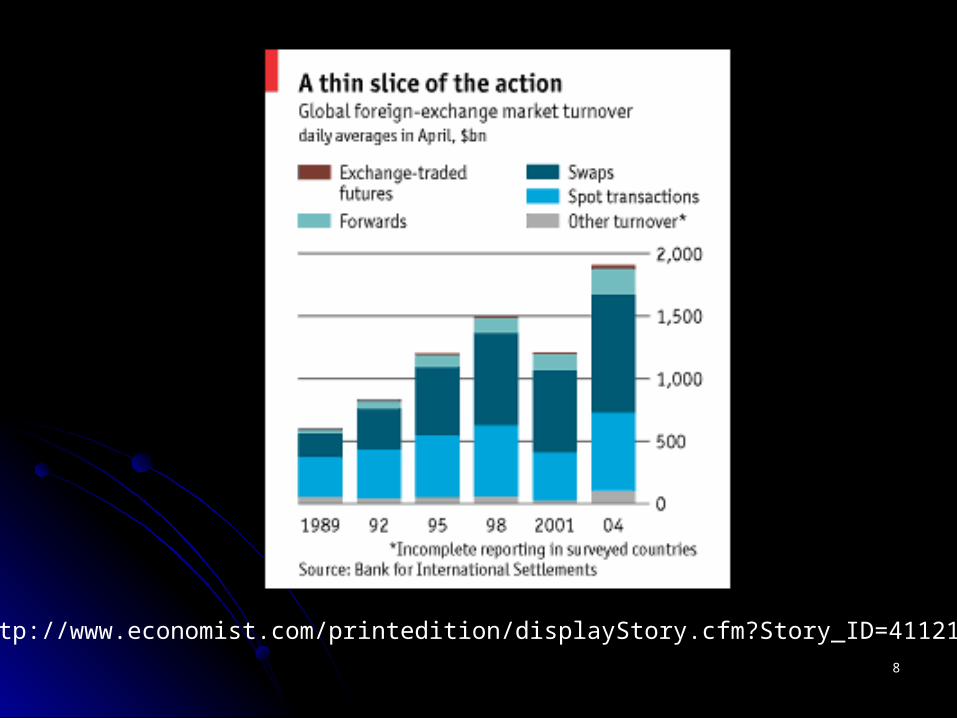

The Foreign Exchange MarketThe Foreign Exchange MarketForex market is where international Forex market is where international

currencies are traded.currencies are traded.Major participants are commercial Major participants are commercial

banks, corporations, nonbank financial banks, corporations, nonbank financial institutions and central banks.institutions and central banks.

The DAILY global trading in the FX The DAILY global trading in the FX market is about $4 trillion. market is about $4 trillion. http://online.wsj.com/article/SB10001424052748703380104576015824083855578.html?mod=igoogle_wsj_gadgv1&http://online.wsj.com/article/SB10001424052748703380104576015824083855578.html?mod=igoogle_wsj_gadgv1&

88

http://www.economist.com/printedition/displayStory.cfm?Story_ID=4112159

99

Commercial BanksCommercial BanksFor every import and export transaction For every import and export transaction

banks have to be involved for payments.banks have to be involved for payments.An importer has to instruct her bank to pay An importer has to instruct her bank to pay

the exporter in exporter’s currency.the exporter in exporter’s currency.The bank has to exchange the domestic The bank has to exchange the domestic

currency for foreign currency and transfer currency for foreign currency and transfer the funds to the exporter’s bank.the funds to the exporter’s bank.

Because they are involved with FX market, Because they are involved with FX market, banks also buy and sell for their own banks also buy and sell for their own accounts to reduce risk.accounts to reduce risk.

1010

CorporationsCorporationsBoth for importing purposes and for Both for importing purposes and for

expenses in another country, expenses in another country, corporations might need to have foreign corporations might need to have foreign currency holdings.currency holdings.

1111

Nonbank Financial InstitutionsNonbank Financial Institutions

More and more nonbank financial More and more nonbank financial institutions have been undertaking institutions have been undertaking banking functions.banking functions.

More and more mutual funds, insurance More and more mutual funds, insurance companies have been involved in companies have been involved in foreign businesses.foreign businesses.

1212

Central BanksCentral Banks

Central banks keep international Central banks keep international reserves to intervene in the FX market reserves to intervene in the FX market to keep the exchange rate at a target to keep the exchange rate at a target level.level.

1313

The Location of FX MarketThe Location of FX MarketFX is traded 24/7 around the world. FX is traded 24/7 around the world. Sunday is a work day in Israel.Sunday is a work day in Israel.Buying and selling is done with Buying and selling is done with

computers, phone lines.computers, phone lines. In short, FX market is truly global single In short, FX market is truly global single

market.market.There should not be any price There should not be any price

differentials from one place to another.differentials from one place to another.

1414

ArbitrageArbitrageSuppose $1=¥100 in New York but Suppose $1=¥100 in New York but

$1=¥101 in London.$1=¥101 in London.You work at the FX desk of Citibank.You work at the FX desk of Citibank.How would you make money for Citibank?How would you make money for Citibank?

1515

ArbitrageArbitrage

You buy USD in New York (sell ¥) and You buy USD in New York (sell ¥) and sell USD in London (buy ¥).sell USD in London (buy ¥).

You borrow yen in New York, buy USD, You borrow yen in New York, buy USD, exchange USD to yen in London and exchange USD to yen in London and pay your yen debt.pay your yen debt.

¥100 million in New York will become ¥100 million in New York will become ¥101 million in London.¥101 million in London.

http://www.marketwatch.com/tools/stockresearch/globalmarkets/default.asp?siteid=mktw&dist=10moverview&

1616

Equilibrium FXEquilibrium FXBuying USD in New York will raise the Buying USD in New York will raise the

price of $: $1 will be worth more than price of $: $1 will be worth more than ¥100 or ¥100 will be worth less than $1.¥100 or ¥100 will be worth less than $1.

Selling USD in London will lower the Selling USD in London will lower the price of $: $1 will be less than ¥101 or price of $: $1 will be less than ¥101 or ¥101 will be more than $1.¥101 will be more than $1.

Prices in New York and London will be Prices in New York and London will be $1=¥100.5.$1=¥100.5.

1717

Vehicle CurrencyVehicle Currency If there are hardly any trade and asset If there are hardly any trade and asset

purchases between two countries, they purchases between two countries, they might not have inventories of each might not have inventories of each other’s currencies.other’s currencies.

Typically, USD is the international Typically, USD is the international reserve currency that is used to reserve currency that is used to exchange from one currency to another.exchange from one currency to another.

USD acting as a vehicle currency allows USD acting as a vehicle currency allows to calculate cross rates.to calculate cross rates.

1818

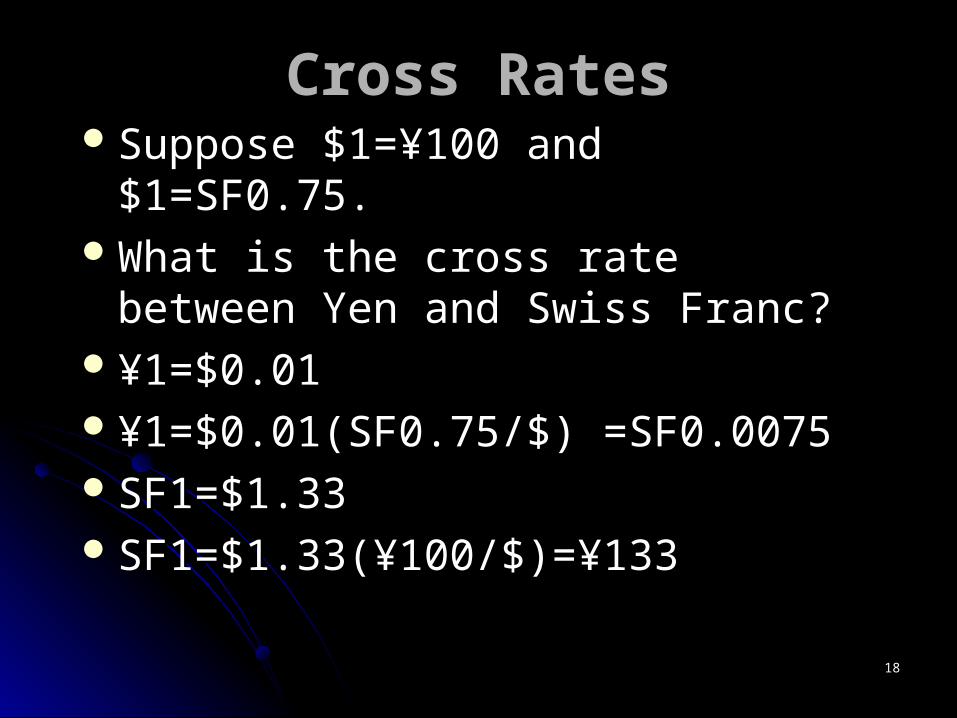

Cross RatesCross RatesSuppose $1=¥100 and $1=SF0.75.Suppose $1=¥100 and $1=SF0.75.What is the cross rate between Yen and What is the cross rate between Yen and

Swiss Franc?Swiss Franc?¥1=$0.01¥1=$0.01¥1=$0.01(SF0.75/$) =SF0.0075 ¥1=$0.01(SF0.75/$) =SF0.0075 SF1=$1.33SF1=$1.33SF1=$1.33(¥100/$)=¥133SF1=$1.33(¥100/$)=¥133

1919

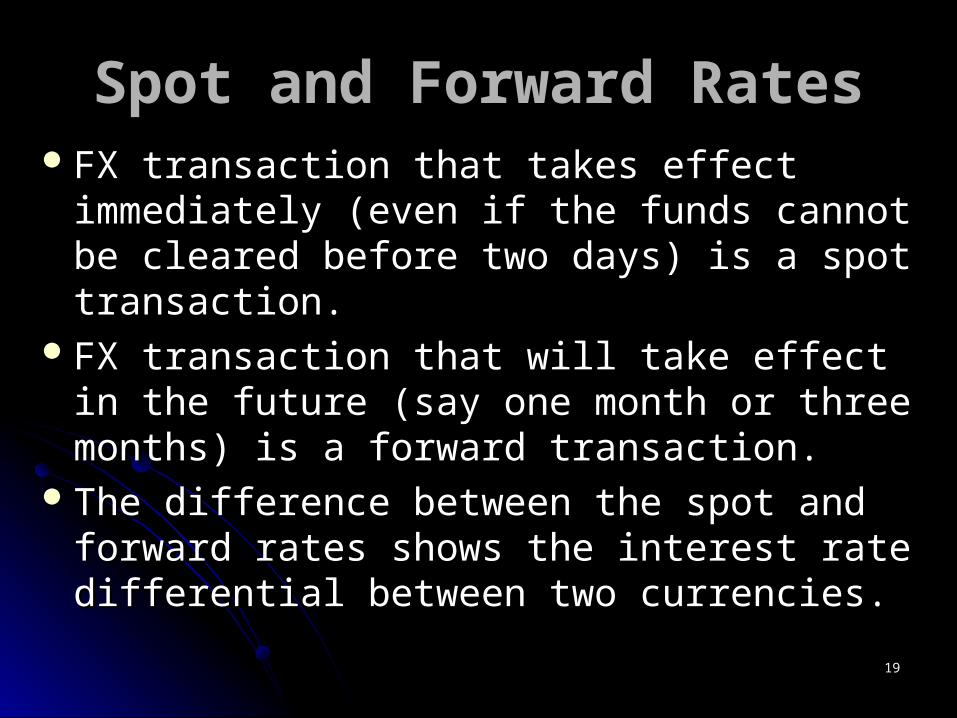

Spot and Forward RatesSpot and Forward RatesFX transaction that takes effect immediately FX transaction that takes effect immediately

(even if the funds cannot be cleared before (even if the funds cannot be cleared before two days) is a spot transaction.two days) is a spot transaction.

FX transaction that will take effect in the FX transaction that will take effect in the future (say one month or three months) is a future (say one month or three months) is a forward transaction.forward transaction.

The difference between the spot and The difference between the spot and forward rates shows the interest rate forward rates shows the interest rate differential between two currencies.differential between two currencies.

2020

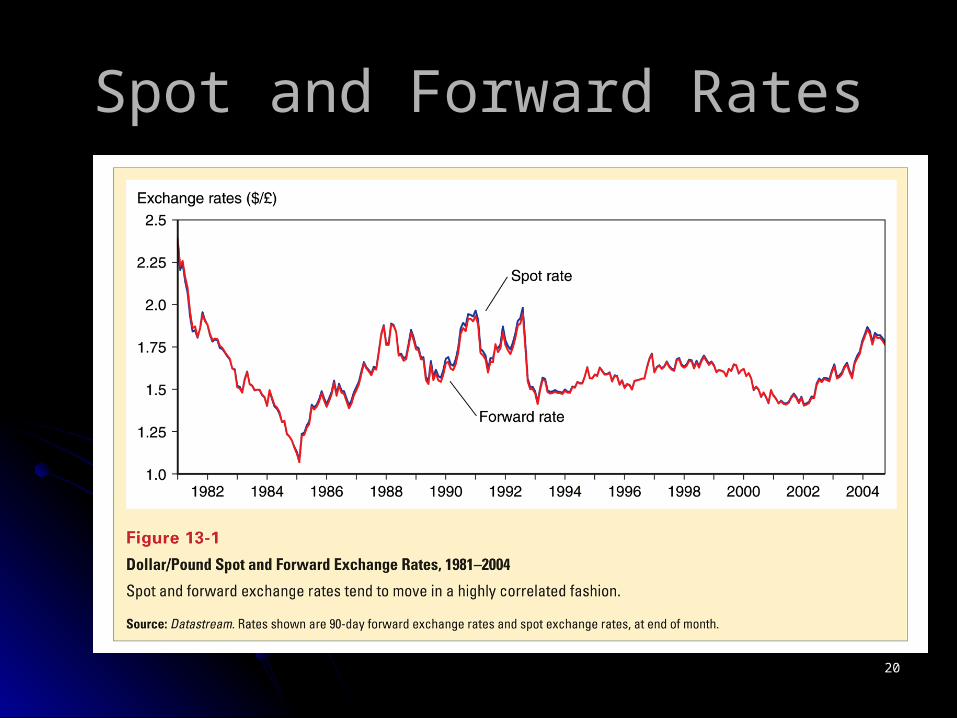

Spot and Forward RatesSpot and Forward Rates

2121

http://www.ny.frb.org/

2222

2323

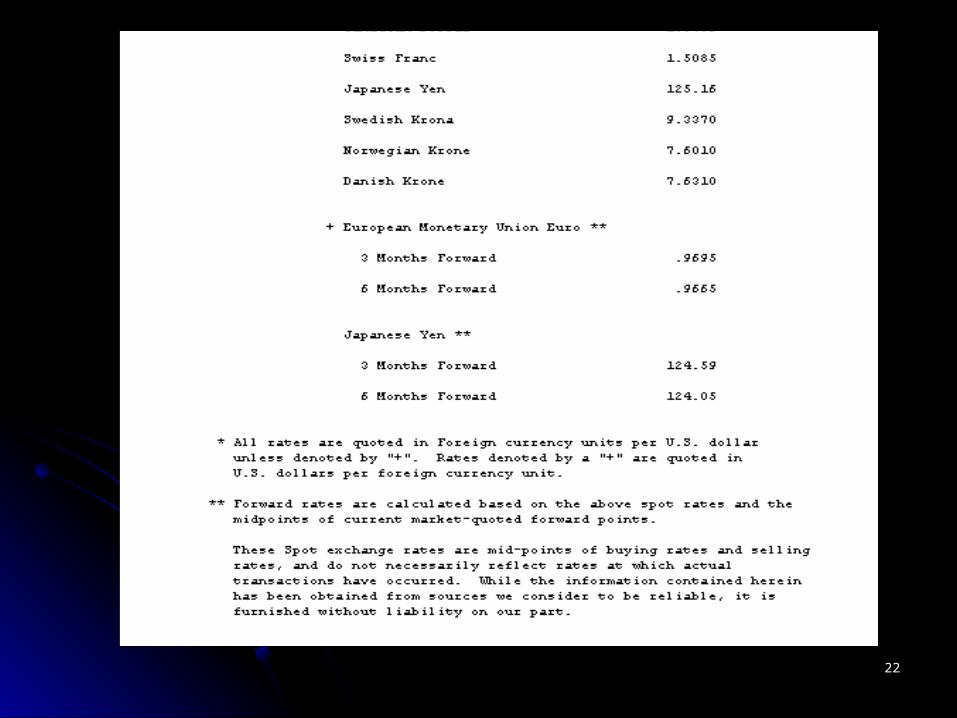

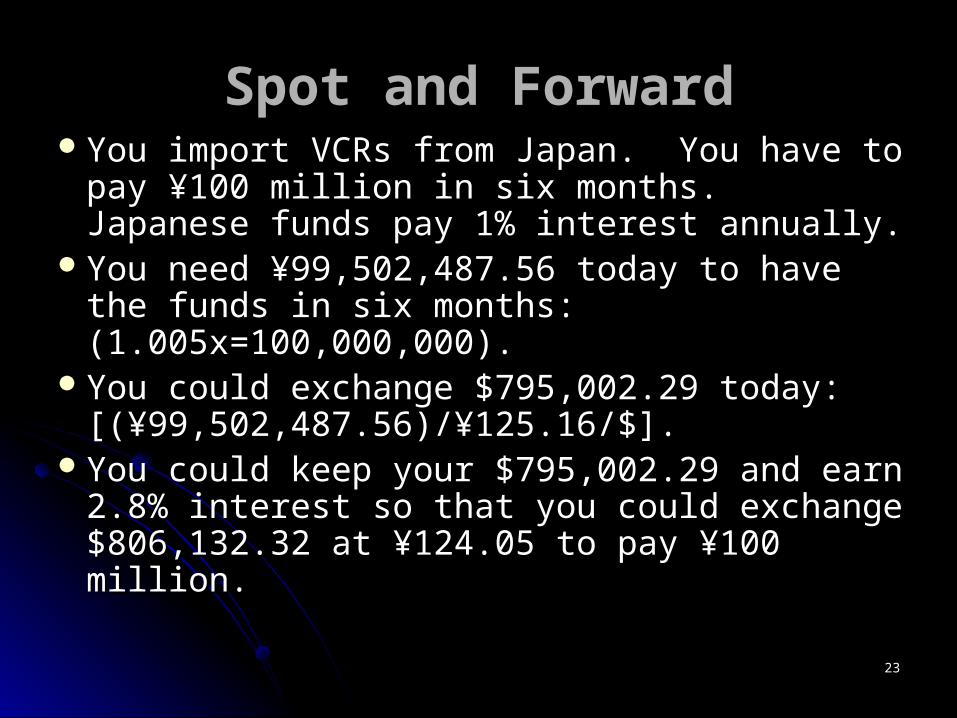

Spot and ForwardSpot and Forward You import VCRs from Japan. You have to You import VCRs from Japan. You have to

pay ¥100 million in six months. Japanese pay ¥100 million in six months. Japanese funds pay 1% interest annually.funds pay 1% interest annually.

You need ¥99,502,487.56 today to have the You need ¥99,502,487.56 today to have the funds in six months: (1.005x=100,000,000).funds in six months: (1.005x=100,000,000).

You could exchange $795,002.29 today: You could exchange $795,002.29 today: [(¥99,502,487.56)/¥125.16/$].[(¥99,502,487.56)/¥125.16/$].

You could keep your $795,002.29 and earn You could keep your $795,002.29 and earn 2.8% interest so that you could exchange 2.8% interest so that you could exchange $806,132.32 at ¥124.05 to pay ¥100 million.$806,132.32 at ¥124.05 to pay ¥100 million.

2424

Spot and ForwardSpot and Forward If it doesn’t make any difference, i.e., it costs If it doesn’t make any difference, i.e., it costs

you the same amount today, why bother?you the same amount today, why bother? Because in six months ¥/$ rate may be Because in six months ¥/$ rate may be

different.different. If ¥/$ rate in six months turns out to be ¥120, If ¥/$ rate in six months turns out to be ¥120,

you could only get ¥96,735,878.40. you could only get ¥96,735,878.40. ($806,132.32)(¥120).($806,132.32)(¥120).

By entering a forward contract with your bank By entering a forward contract with your bank you know exactly how much you are paying you know exactly how much you are paying and can price your VCRs accordingly.and can price your VCRs accordingly.

2525

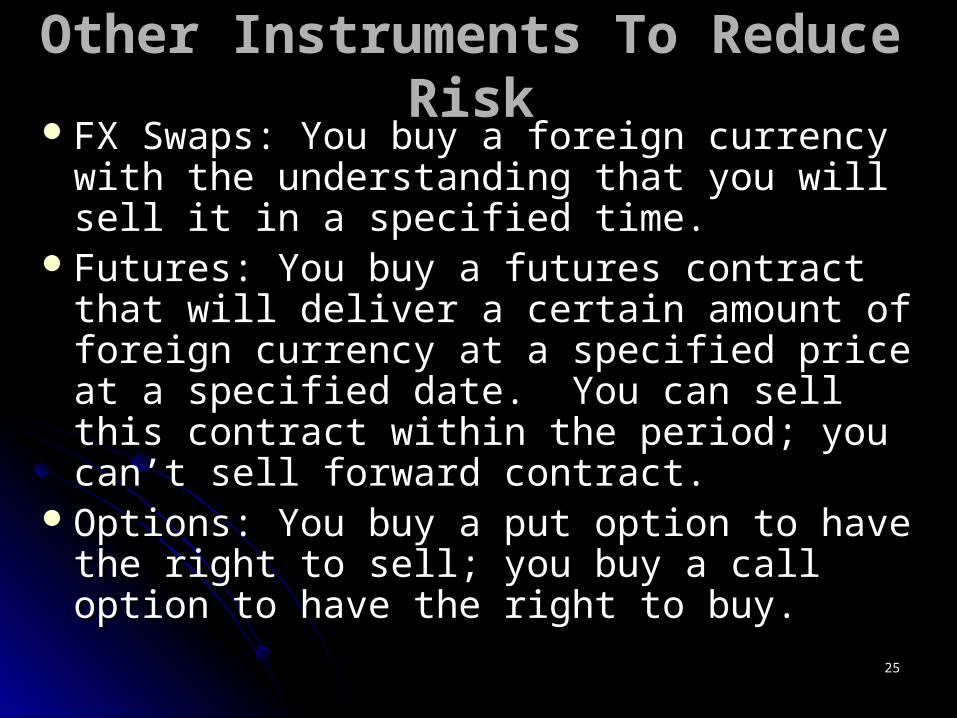

Other Instruments To Reduce RiskOther Instruments To Reduce RiskFX Swaps: You buy a foreign currency with FX Swaps: You buy a foreign currency with

the understanding that you will sell it in a the understanding that you will sell it in a specified time.specified time.

Futures: You buy a futures contract that will Futures: You buy a futures contract that will deliver a certain amount of foreign currency deliver a certain amount of foreign currency at a specified price at a specified date. You at a specified price at a specified date. You can sell this contract within the period; you can sell this contract within the period; you can’t sell forward contract.can’t sell forward contract.

Options: You buy a put option to have the Options: You buy a put option to have the right to sell; you buy a call option to have right to sell; you buy a call option to have the right to buy.the right to buy.

2626

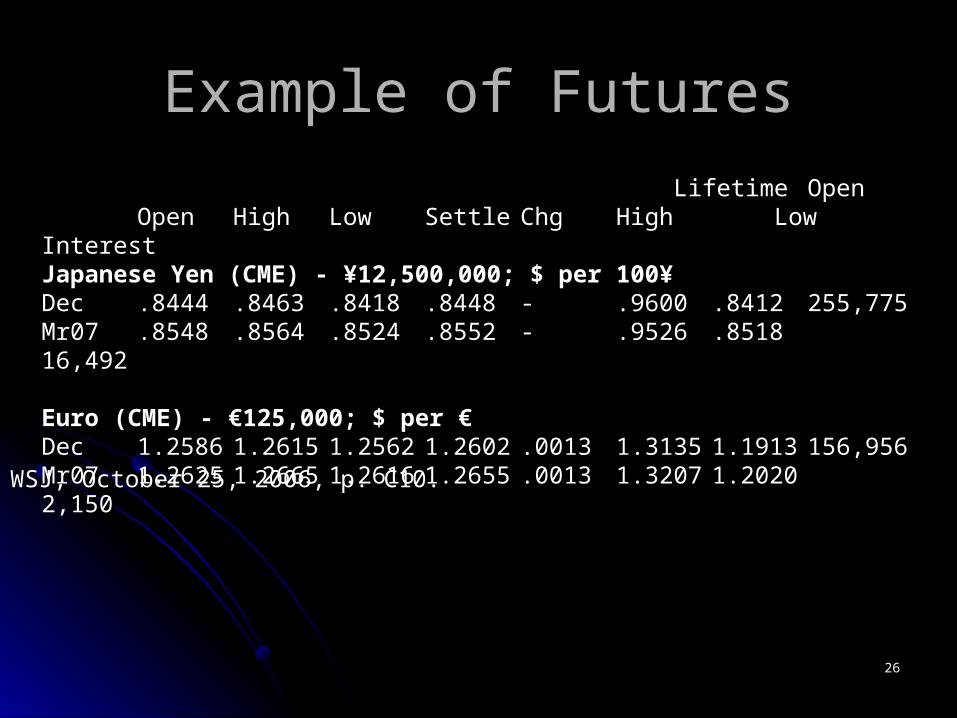

Example of FuturesExample of Futures

Lifetime OpenOpen High Low Settle Chg High Low Interest

Japanese Yen (CME) - ¥12,500,000; $ per 100¥¥12,500,000; $ per 100¥DecDec .8444.8444 .8463.8463 .8418.8418 .8448.8448 -- .9600.9600 .8412.8412 255,775255,775Mr07Mr07 .8548.8548 .8564.8564 .8524.8524 .8552.8552 -- .9526.9526 .8518.8518 16,492 16,492

Euro (CME) - €125,000; $ per €Euro (CME) - €125,000; $ per €DecDec 1.25861.2586 1.26151.2615 1.25621.2562 1.26021.2602 .0013.0013 1.31351.3135 1.19131.1913 156,956156,956Mr07Mr07 1.26251.2625 1.26651.2665 1.26161.2616 1.26551.2655 .0013.0013 1.32071.3207 1.20201.2020 2,150 2,150

WSJ, October 25, 2006, p. C10.

2727

FX: Commodity or AssetFX: Commodity or Asset

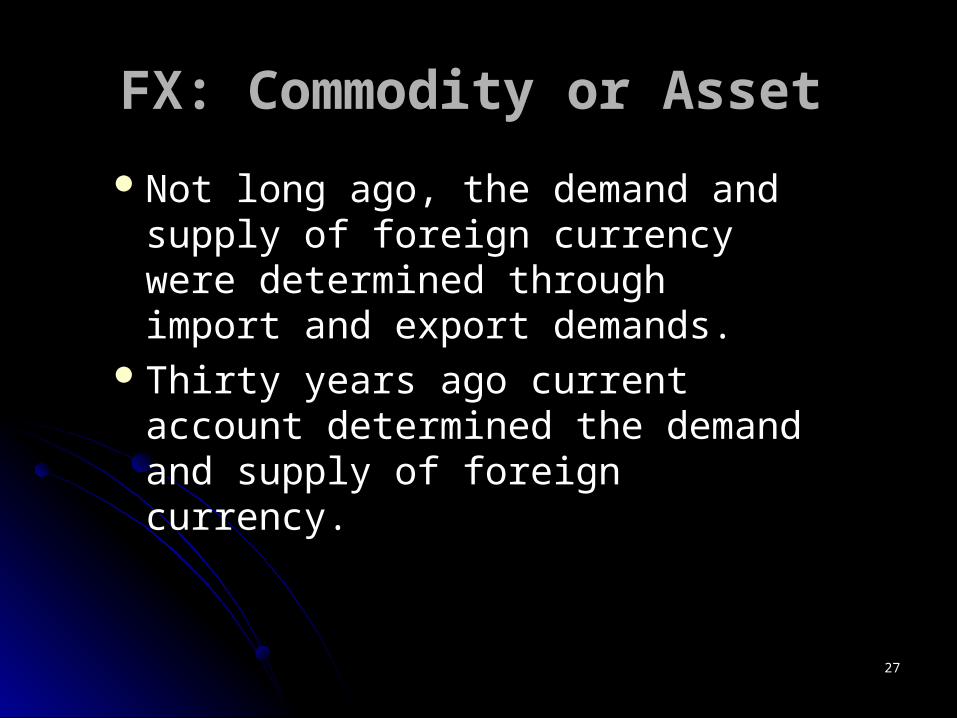

Not long ago, the demand and Not long ago, the demand and supply of foreign currency were supply of foreign currency were determined through import and determined through import and export demands.export demands.

Thirty years ago current account Thirty years ago current account determined the demand and determined the demand and supply of foreign currency.supply of foreign currency.

2828

FX: Commodity or AssetFX: Commodity or Asset

In 1980 US (not global) foreign currency In 1980 US (not global) foreign currency trading was around $18 billion per day. trading was around $18 billion per day. In Oct. 2008 this amount was $762 In Oct. 2008 this amount was $762 billion per day. billion per day. http://www.newyorkfed.org/fxc/volumesurvey/2008/octoberfxsurhttp://www.newyorkfed.org/fxc/volumesurvey/2008/octoberfxsurvey2008.pdfvey2008.pdf

It is not imports/exports but the function It is not imports/exports but the function of FX as an asset that matters.of FX as an asset that matters.

2929

The Demand for an AssetThe Demand for an Asset

Foreign currency bank deposits are Foreign currency bank deposits are assets.assets.

As with any asset, the future value is As with any asset, the future value is paramount in determining price.paramount in determining price.

Assets (wealth) allow to postpone Assets (wealth) allow to postpone purchasing power into the future.purchasing power into the future.

3030

The Demand for an AssetThe Demand for an Asset

The demand for an asset depends on The demand for an asset depends on the generated income (interest rate), the generated income (interest rate), capital gain (expected price), capital gain (expected price), riskiness, liquidity.riskiness, liquidity.

3131

Rate of ReturnRate of ReturnA $1000 bond that pays $50 provides an A $1000 bond that pays $50 provides an

interest rate of 5%.interest rate of 5%. If you sell the bond for $1100, your rate of If you sell the bond for $1100, your rate of

return is 15%.return is 15%. If you sell the bond for $900, your rate of If you sell the bond for $900, your rate of

return is -5%.return is -5%. If inflation were 5%, your real rate of If inflation were 5%, your real rate of

return would have been 10% and -10%, return would have been 10% and -10%, respectively.respectively.

3232

RiskRisk

Risk is a measure of uncertainty of Risk is a measure of uncertainty of future returns. The higher the future returns. The higher the variations in returns, the higher is the variations in returns, the higher is the risk.risk.

The higher the risk, the less desirable The higher the risk, the less desirable is the asset.is the asset.

3333

LiquidityLiquidity

Liquidity is a measure of cost and Liquidity is a measure of cost and speed to convert an asset into cash. speed to convert an asset into cash. The cheaper and speedier an asset can The cheaper and speedier an asset can be converted to cash, the more liquid it be converted to cash, the more liquid it is.is.

The more liquid an asset, the more The more liquid an asset, the more desirable it is.desirable it is.

3434

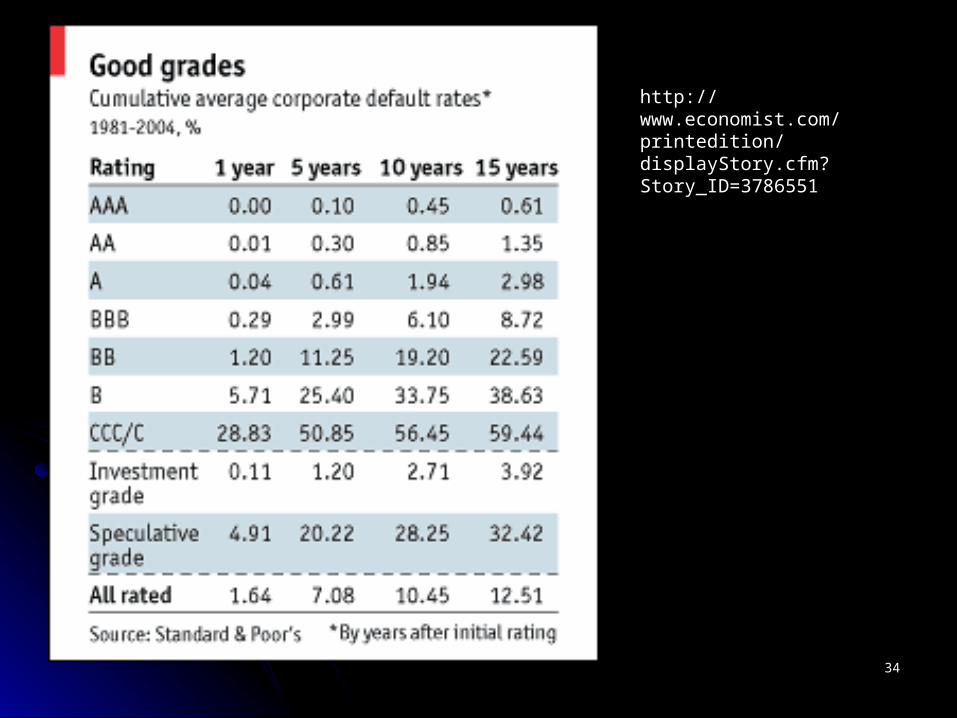

http://www.economist.com/printedition/displayStory.cfm?Story_ID=3786551

3535

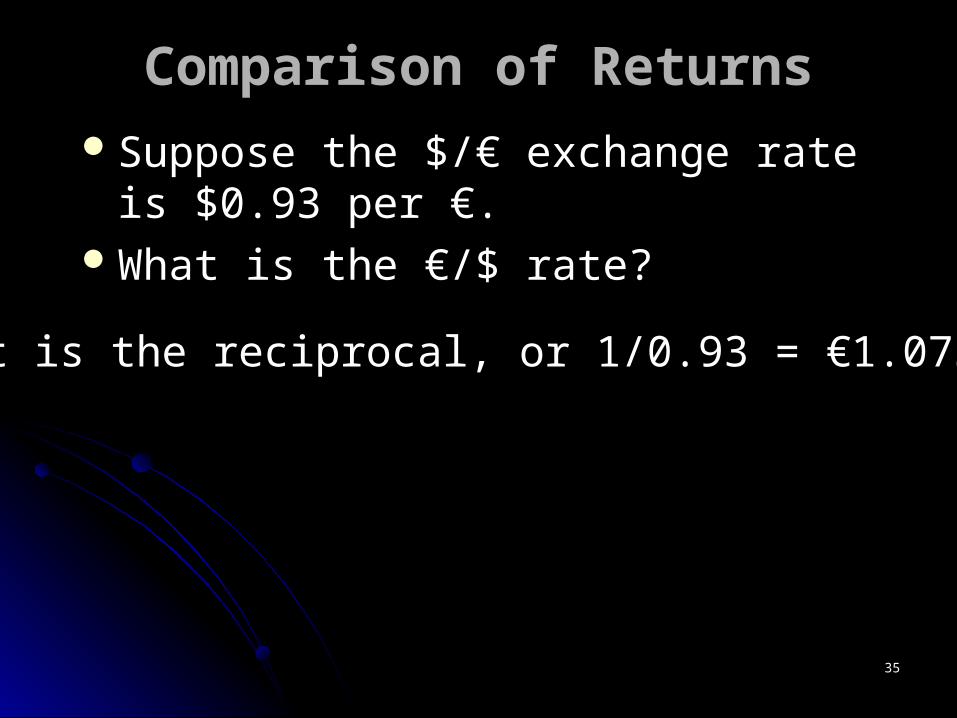

Comparison of ReturnsComparison of ReturnsSuppose the $/€ exchange rate is $0.93 Suppose the $/€ exchange rate is $0.93

per €. per €. What is the €/$ rate?What is the €/$ rate?

It is the reciprocal, or 1/0.93 = €1.075

3636

Comparison of ReturnsComparison of Returns Suppose $ deposits pay 5% interest rate.Suppose $ deposits pay 5% interest rate. Suppose € deposits pay 8% interest rate.Suppose € deposits pay 8% interest rate. Which asset ($ or €) would you rather hold?Which asset ($ or €) would you rather hold?

€ of course.

3737

Comparison of ReturnsComparison of Returns Suppose you will need your $ a year from Suppose you will need your $ a year from

now. Today the exchange rate is $0.93/€.now. Today the exchange rate is $0.93/€. You expect the $/€ rate to be $0.91.You expect the $/€ rate to be $0.91. Do you expect the $ to appreciate or Do you expect the $ to appreciate or

depreciate?depreciate? Do you expect the € to appreciate or Do you expect the € to appreciate or

depreciate?depreciate?

Your expectation is for $ to appreciate and for €to depreciate.

3838

Comparison of ReturnsComparison of ReturnsThe rate of appreciation of $ will increase The rate of appreciation of $ will increase

the percentage return on USD.the percentage return on USD.The rate of depreciation of € will decrease The rate of depreciation of € will decrease

the percentage return on €.the percentage return on €. If € is expected to move from $0.93 to If € is expected to move from $0.93 to

$0.91, its rate of depreciation is ($0.91-$0.91, its rate of depreciation is ($0.91-$0.93)/$0.93 = -0.0215 or -2.15%.$0.93)/$0.93 = -0.0215 or -2.15%.

The rate of appreciation for $ is (€1.099- The rate of appreciation for $ is (€1.099- €1.075)/ €1.075= 0.022 or 2.2%.€1.075)/ €1.075= 0.022 or 2.2%.

3939

Comparison of ReturnsComparison of Returns Since the appreciation/depreciation Since the appreciation/depreciation

calculations are approximately equal, we calculations are approximately equal, we will treat them to be equal for simplicity.will treat them to be equal for simplicity.

If we compare interest rate on $ (5%) with If we compare interest rate on $ (5%) with the returns on € (8% - 2.15%), we are still the returns on € (8% - 2.15%), we are still better off keeping our wealth in €.better off keeping our wealth in €.

If we compare interest rate on € (8%) with If we compare interest rate on € (8%) with the returns on $ (5% + 2.2%), again we are the returns on $ (5% + 2.2%), again we are still better off keeping our wealth in €.still better off keeping our wealth in €.

4040

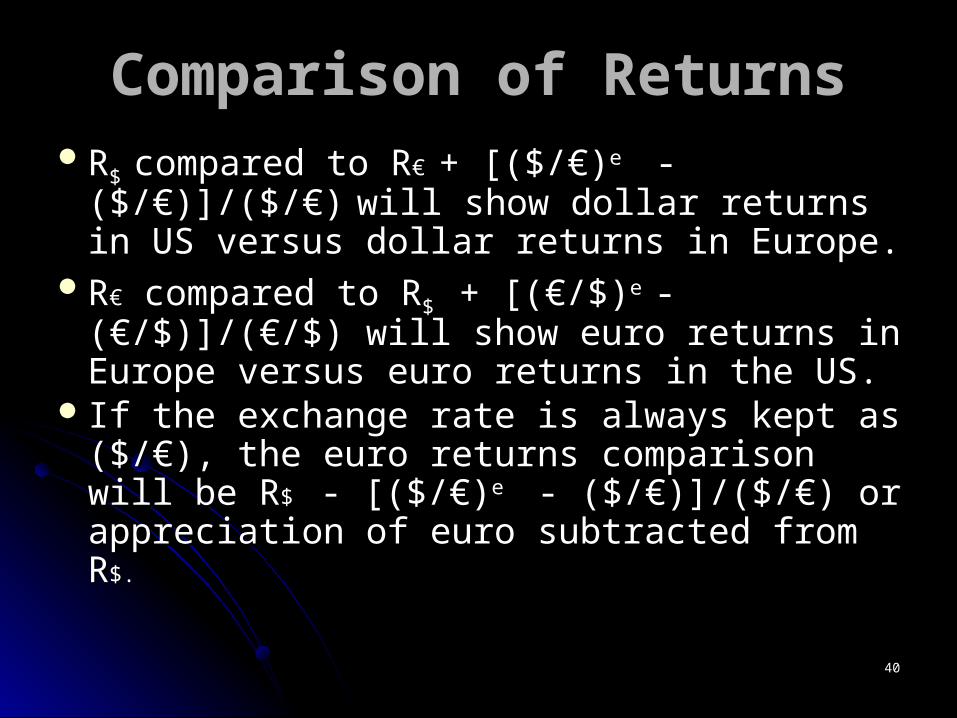

Comparison of ReturnsComparison of ReturnsRR$ $ compared to Rcompared to R€ € + [($/€)+ [($/€)e e - ($/€)]/($/€) - ($/€)]/($/€) will will

show dollar returns in US versus dollar show dollar returns in US versus dollar returns in Europe.returns in Europe.

RR€€ compared to R compared to R$ $ + [(€/$)+ [(€/$)e e - (€/$)]/(€/$) - (€/$)]/(€/$) will show euro returns in Europe versus will show euro returns in Europe versus euro returns in the US.euro returns in the US.

If the exchange rate is always kept as If the exchange rate is always kept as ($/€), the euro returns comparison will be ($/€), the euro returns comparison will be RR$ $ - [($/€)- [($/€)e e - ($/€)]/($/€) or appreciation of - ($/€)]/($/€) or appreciation of euro subtracted from Reuro subtracted from R$.$.

4141

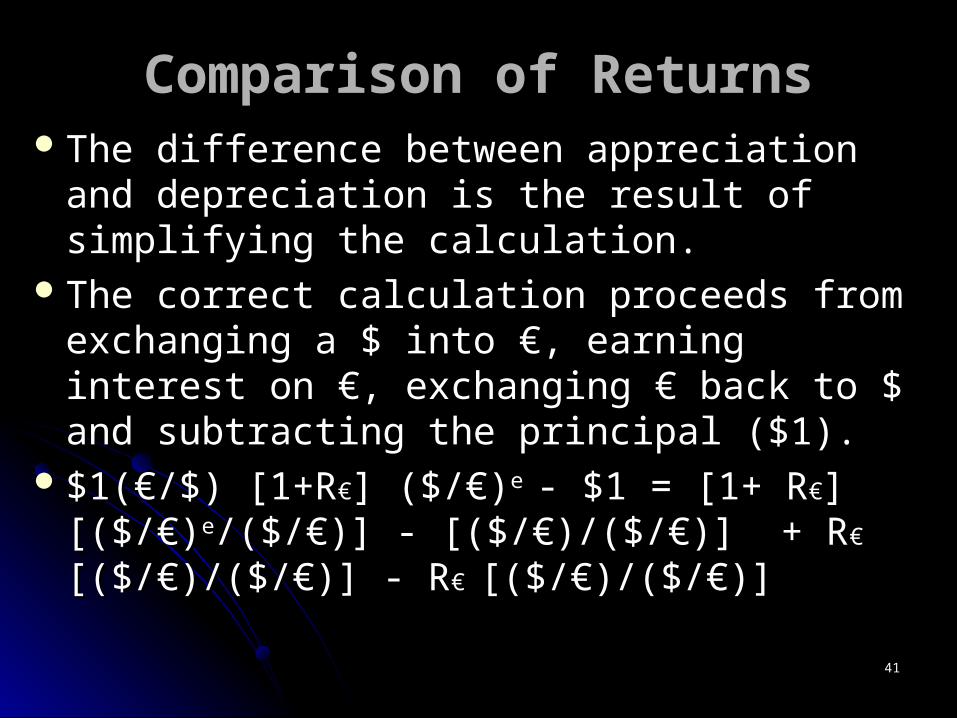

Comparison of ReturnsComparison of Returns The difference between appreciation and The difference between appreciation and

depreciation is the result of simplifying the depreciation is the result of simplifying the calculation.calculation.

The correct calculation proceeds from The correct calculation proceeds from exchanging a $ into €, earning interest on €, exchanging a $ into €, earning interest on €, exchanging € back to $ and subtracting the exchanging € back to $ and subtracting the principal ($1).principal ($1).

$1(€/$) [1+R$1(€/$) [1+R€€] ($/€)] ($/€)e e - $1 = [1+ - $1 = [1+ RR€€][($/€)][($/€)ee/($/€)] - [($/€)/($/€)] + R/($/€)] - [($/€)/($/€)] + R€€ [($/€)/($/€)] - R[($/€)/($/€)] - R€ € [($/€)/($/€)] [($/€)/($/€)]

4242

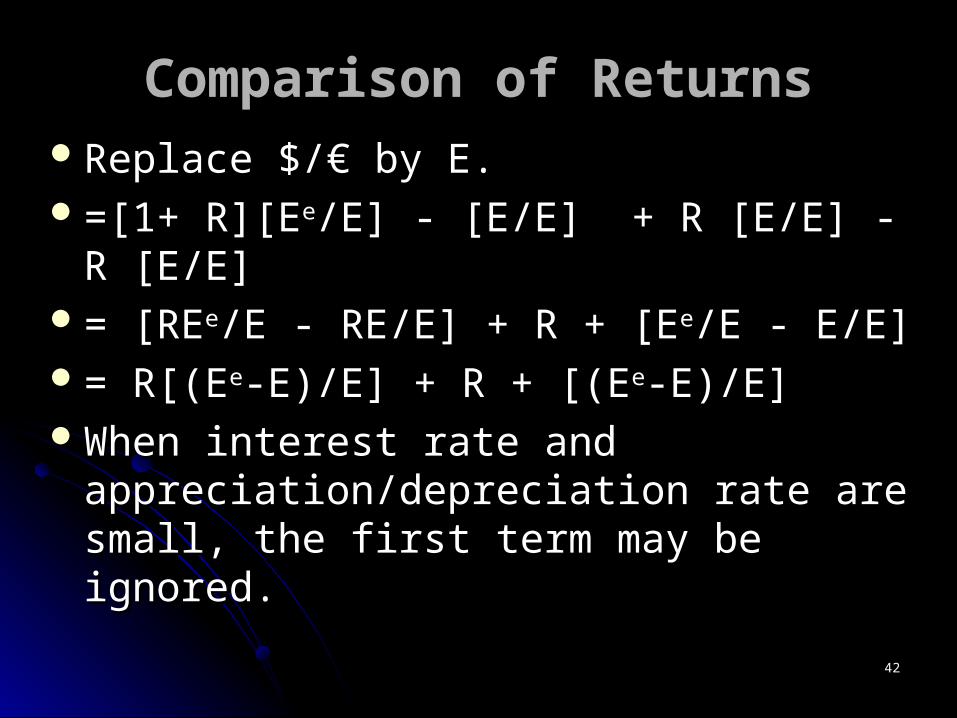

Comparison of ReturnsComparison of ReturnsReplace $/€ by E.Replace $/€ by E.=[1+ R][E=[1+ R][Eee/E] - [E/E] + R [E/E] - R [E/E]/E] - [E/E] + R [E/E] - R [E/E]= [RE= [REee/E - RE/E] + R + [E/E - RE/E] + R + [Eee/E - E/E]/E - E/E]= R[(E= R[(Eee-E)/E] + R + [(E-E)/E] + R + [(Eee-E)/E]-E)/E]When interest rate and When interest rate and

appreciation/depreciation rate are small, the appreciation/depreciation rate are small, the first term may be ignored.first term may be ignored.

4343

The Demand for Currency DepositsThe Demand for Currency Deposits

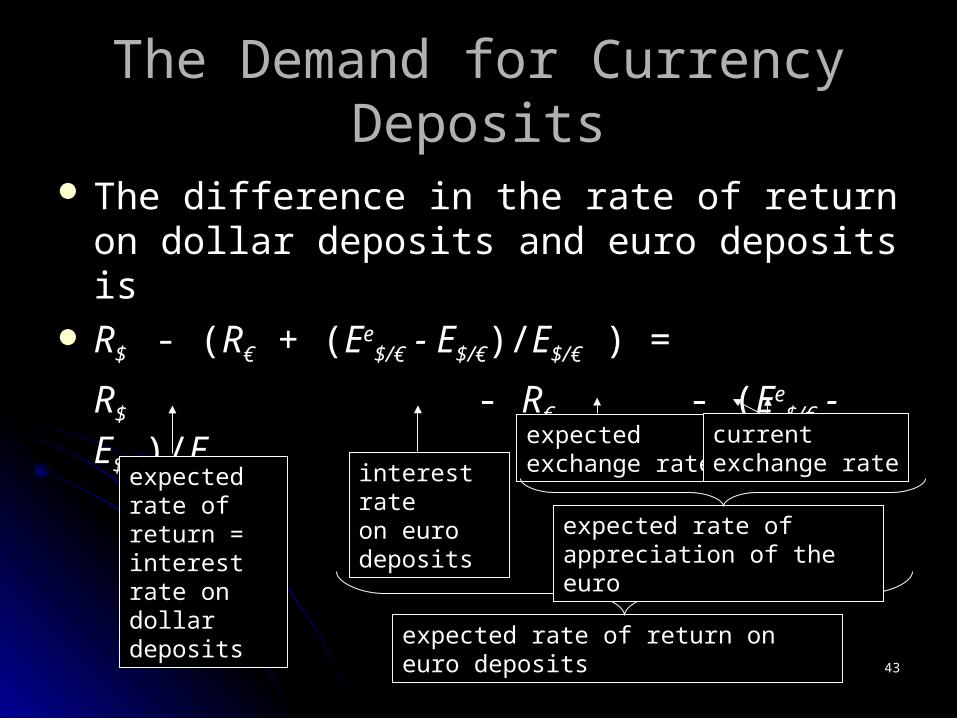

The difference in the rate of return on dollar The difference in the rate of return on dollar deposits and euro deposits is deposits and euro deposits is

RR$ $ - ( - (RR€€ + ( + (EEee$/€$/€ - E - E$/€$/€)/)/EE$/€$/€ ) = ) =

RR$$ - - RR€€ - ( - (EEee$/€$/€ - E - E$/€$/€)/)/EE$/€$/€

expected rate of return = interest rate on dollar deposits

interest rateon euro deposits

expected rate of return on euro deposits

expected exchange rate

currentexchange rate

expected rate of appreciation of the euro

4444

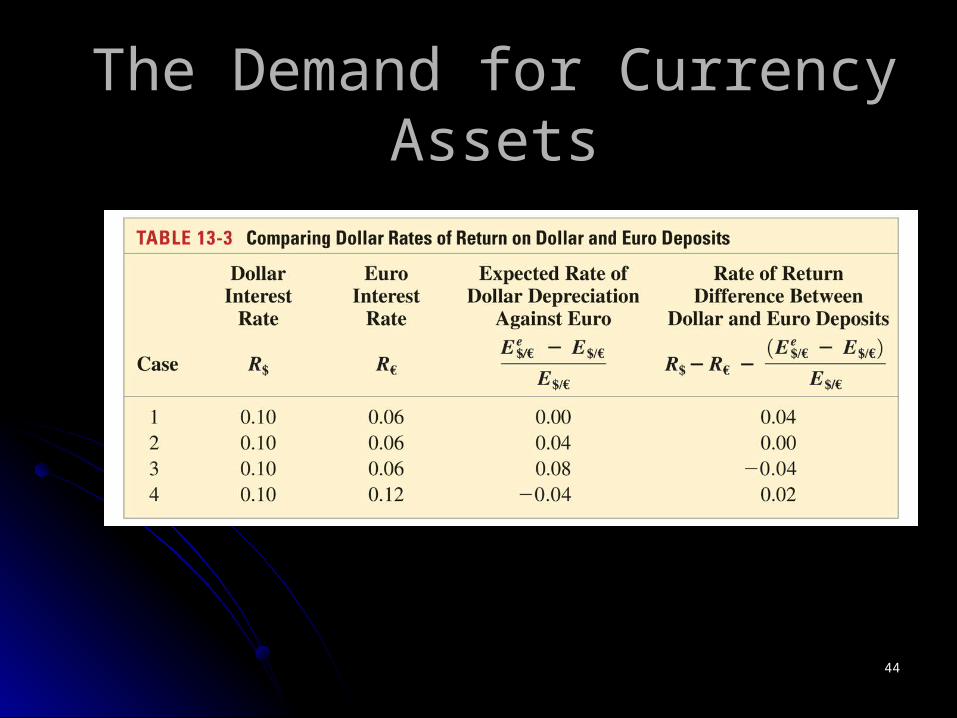

The Demand for Currency AssetsThe Demand for Currency Assets

4545

ApplicationsApplications $ interest rate is 10%; € interest rate is 8%.$ interest rate is 10%; € interest rate is 8%. Spot ($/€)Spot ($/€) rate is $0.93 per euro.rate is $0.93 per euro. If ($/€)If ($/€)e e were (a) $0.95; (b) $0.91; (c) $0.97 were (a) $0.95; (b) $0.91; (c) $0.97

where would you park your deposits?where would you park your deposits?

(a) € appreciates by (.95-.93)/.93 = 2.15%10% < 8% + 2.15%.

(b) € depreciates by (.91-.93)/.93 = - 2.15%10% > 8% - 2.15%.

(c) € appreciates by (.97-.93)/.93 = 4.3%10% < 8% + 4.3%.

4646

EquilibriumEquilibriumWhen returns from $ are the same as When returns from $ are the same as

returns from euro, there will be no returns from euro, there will be no adjustments: the foreign exchange market adjustments: the foreign exchange market between USD and euro is in equilibrium.between USD and euro is in equilibrium.

The returns are equal when the USD The returns are equal when the USD interest rate is exactly equal to euro interest interest rate is exactly equal to euro interest rate plus the rate of appreciation of euro.rate plus the rate of appreciation of euro.

Alternatively, the returns are equal when Alternatively, the returns are equal when the euro interest rate is equal to $ interest the euro interest rate is equal to $ interest rate minus the depreciation of euro.rate minus the depreciation of euro.

4747

EquilibriumEquilibrium Equilibrium in the foreign exchange market Equilibrium in the foreign exchange market

will take place when the interest parity will take place when the interest parity condition holds.condition holds.

RR$ $ = R= R€ € + [($/€)+ [($/€)e e - ($/€)]/($/€) - ($/€)]/($/€) If RIf R$ $ > R> R€ € + [($/€)+ [($/€)e e - ($/€)]/($/€), there will be - ($/€)]/($/€), there will be

an excess demand for USD (excess supply an excess demand for USD (excess supply of €) in the foreign exchange market.of €) in the foreign exchange market.

If RIf R$ $ < R< R€ € + [($/€)+ [($/€)e e - ($/€)]/($/€), there will be - ($/€)]/($/€), there will be an excess demand for euro and an excess an excess demand for euro and an excess supply of USD.supply of USD.

4848

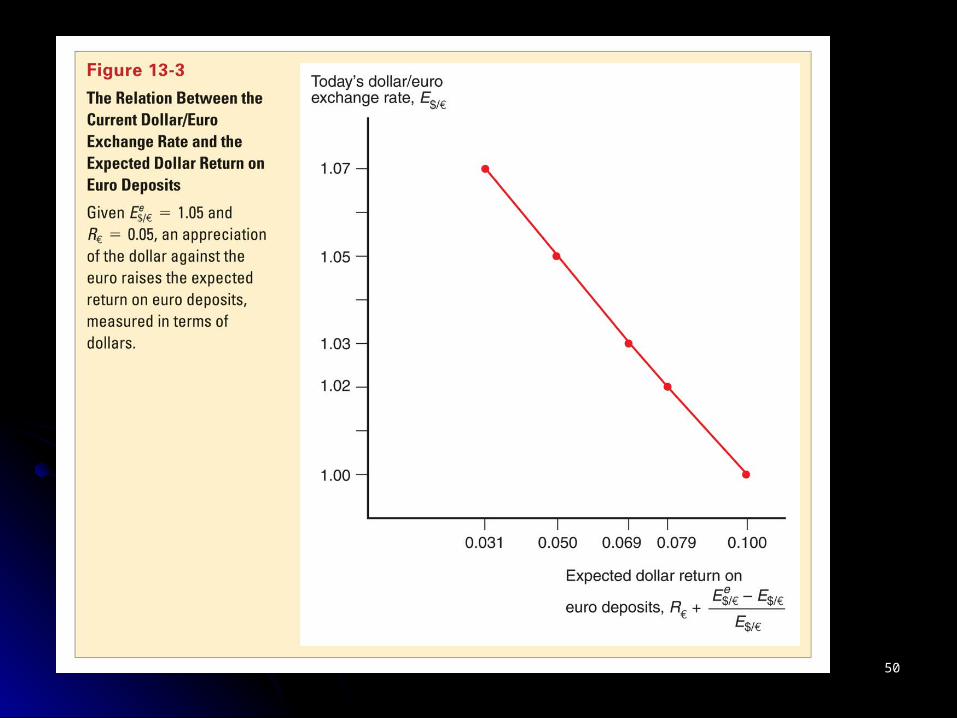

Current FX and ReturnsCurrent FX and Returns If the current FX goes up, e.g., euro If the current FX goes up, e.g., euro

appreciates today but the expected FX remains appreciates today but the expected FX remains the same, the dollar return on euro deposits the same, the dollar return on euro deposits will decrease.will decrease.

RR€ € + [($/€)+ [($/€)e e - ($/€)]/($/€) will be lower if ($/€) - ($/€)]/($/€) will be lower if ($/€) rises. rises.

RR$ $ - [($/€)- [($/€)e e - ($/€)]/($/€) will be higher if ($/€) - ($/€)]/($/€) will be higher if ($/€) rises. rises.

In other words, if USD depreciates today, the In other words, if USD depreciates today, the dollar return on euro deposits will fall.dollar return on euro deposits will fall.

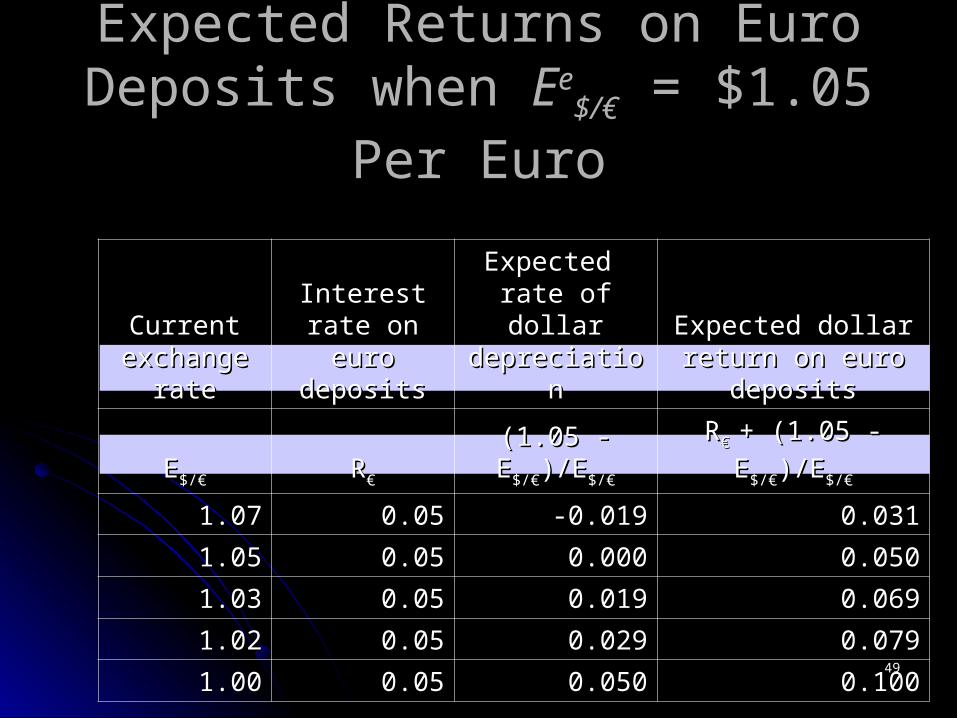

4949

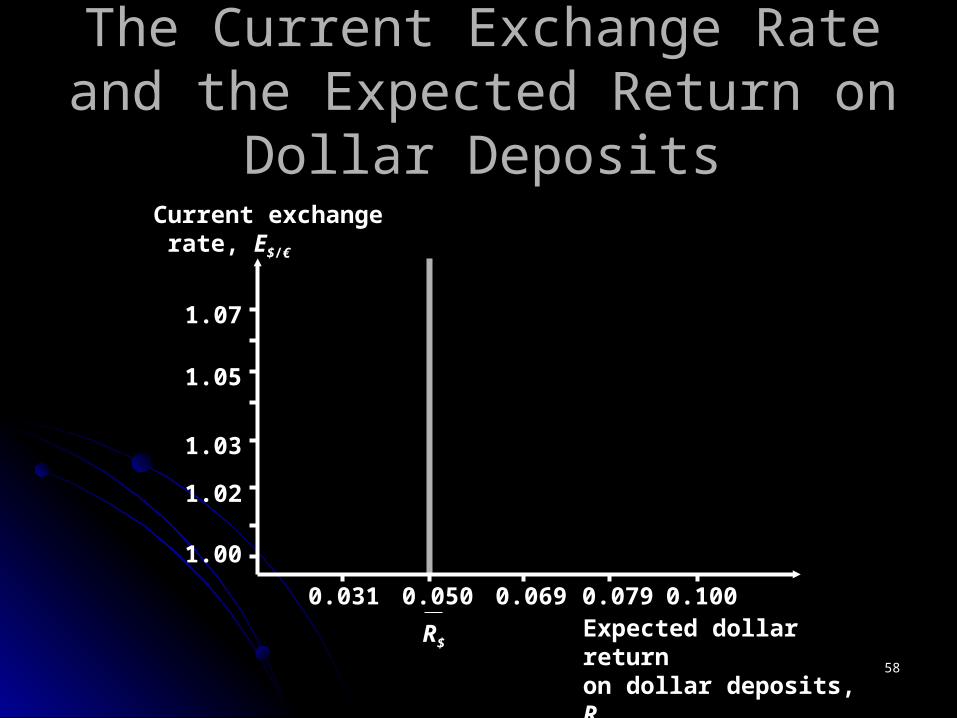

Expected Returns on Euro Deposits Expected Returns on Euro Deposits when when EEee

$/€$/€ = $1.05 Per Euro = $1.05 Per Euro

Current Current exchange rateexchange rate

Interest rate on Interest rate on euro depositseuro deposits

Expected rate of Expected rate of dollar dollar

depreciationdepreciationExpected dollar return Expected dollar return

on euro depositson euro deposits

EE$/€$/€ RR€€ (1.05 - E(1.05 - E$/€$/€)/E)/E

$/€$/€ RR€ € + (1.05 - E+ (1.05 - E$/€$/€)/E)/E

$/€$/€

1.071.07 0.050.05 -0.019-0.019 0.0310.031

1.051.05 0.050.05 0.0000.000 0.0500.050

1.031.03 0.050.05 0.0190.019 0.0690.069

1.021.02 0.050.05 0.0290.029 0.0790.079

1.001.00 0.050.05 0.0500.050 0.1000.100

5050

5151

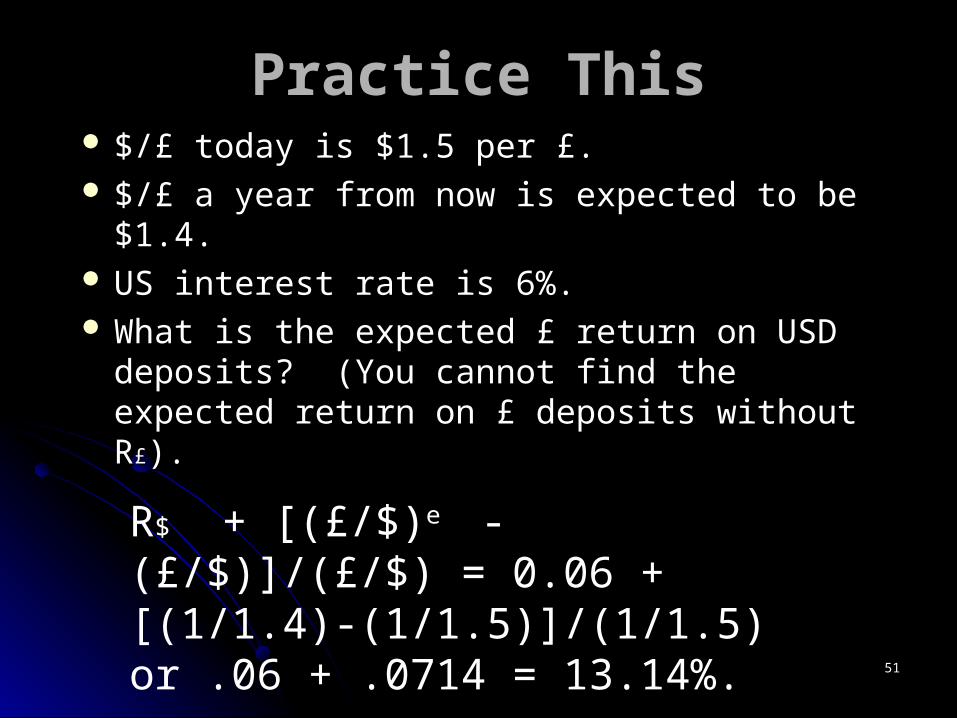

Practice ThisPractice This $/£ today is $1.5 per £.$/£ today is $1.5 per £. $/£ a year from now is expected to be $1.4.$/£ a year from now is expected to be $1.4. US interest rate is 6%.US interest rate is 6%. What is the expected £ return on USD What is the expected £ return on USD

deposits? (You cannot find the expected deposits? (You cannot find the expected return on £ deposits without Rreturn on £ deposits without R££).).

R$ + [(£/$)e - (£/$)]/(£/$) = 0.06 + [(1/1.4)-(1/1.5)]/(1/1.5) or .06 + .0714 = 13.14%.

5252

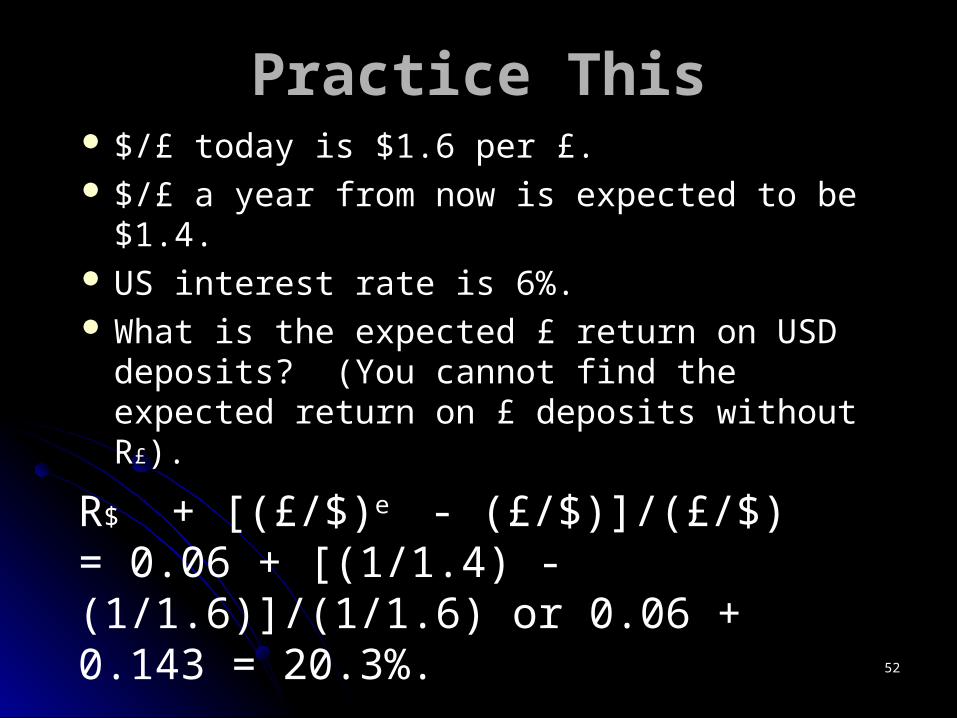

Practice ThisPractice This $/£ today is $1.6 per £.$/£ today is $1.6 per £. $/£ a year from now is expected to be $1.4.$/£ a year from now is expected to be $1.4. US interest rate is 6%.US interest rate is 6%. What is the expected £ return on USD What is the expected £ return on USD

deposits? (You cannot find the expected deposits? (You cannot find the expected return on £ deposits without Rreturn on £ deposits without R££).).

R$ + [(£/$)e - (£/$)]/(£/$) = 0.06 + [(1/1.4) - (1/1.6)]/(1/1.6) or 0.06 + 0.143 = 20.3%.

5353

Practice ThisPractice This $/£ today is $1.5 per £.$/£ today is $1.5 per £. $/£ a year from now is expected to be $1.4.$/£ a year from now is expected to be $1.4. UK interest rate is 15%.UK interest rate is 15%. What is the expected dollar return on £ What is the expected dollar return on £

deposits? deposits?

R£ + [($/£)e - ($/£)]/($/£) = 0.15 + (-0.1/1.5)or 0.15 - 0.067 = 8.3%.

5454

Practice ThisPractice This $/£ today is $1.6 per £.$/£ today is $1.6 per £. $/£ a year from now is expected to be $1.4.$/£ a year from now is expected to be $1.4. UK interest rate is 15%.UK interest rate is 15%. What is the expected dollar return on £ What is the expected dollar return on £

deposits? deposits?

R£ + [($/£)e - ($/£)]/($/£) = 0.15 + (-0.2/1.6)or 0.15 - 0.125 = 2.5%.

5555

Practice ResultPractice ResultWhen £ appreciated today, £ returns on When £ appreciated today, £ returns on

USD deposits increased.USD deposits increased.When $ depreciated today, $ returns on When $ depreciated today, $ returns on

£ deposits decreased.£ deposits decreased.

5656

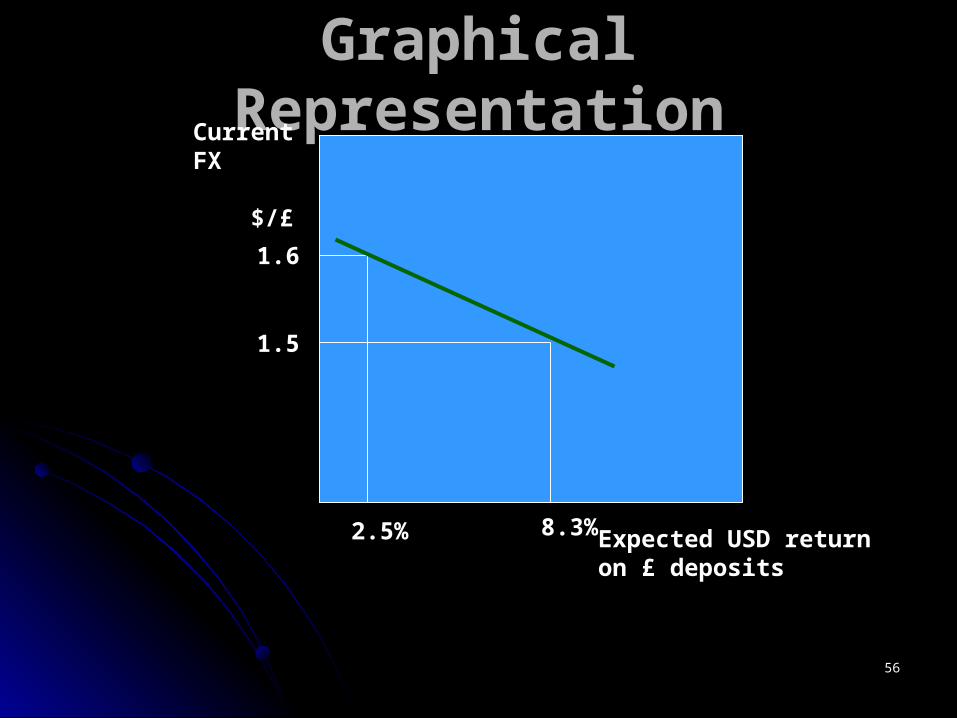

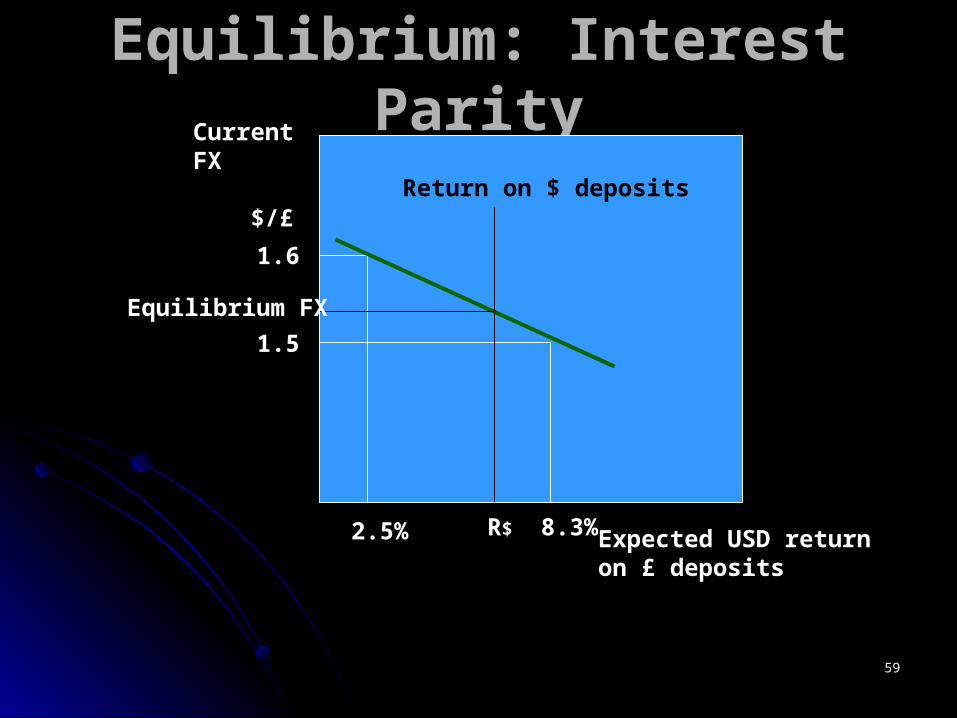

Graphical RepresentationGraphical RepresentationCurrent FX $/£

1.6

1.5

2.5% 8.3% Expected USD returnon £ deposits

5757

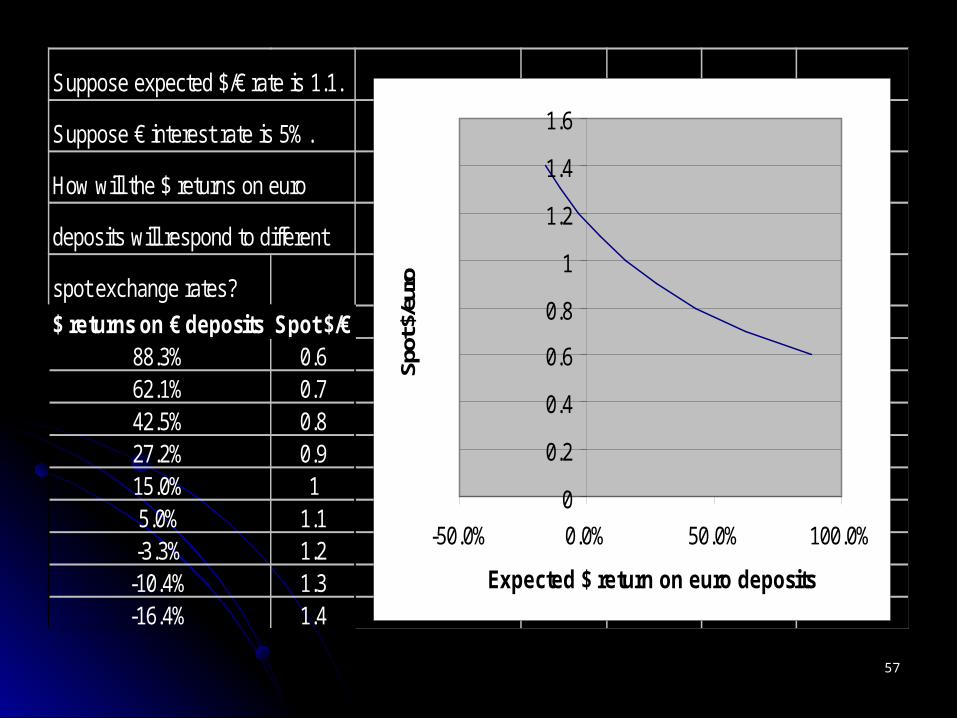

Suppose expected $/€ rate is 1.1.

Suppose € interest rate is 5%.

How will the $ returns on euro

deposits will respond to different

spot exchange rates?

$ returns on € deposits Spot $/€88.3% 0.662.1% 0.742.5% 0.827.2% 0.915.0% 15.0% 1.1-3.3% 1.2

-10.4% 1.3-16.4% 1.4

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

-50.0% 0.0% 50.0% 100.0%

Expected $ return on euro deposits

Spot

$/e

uro

5858

The Current Exchange Rate and the The Current Exchange Rate and the Expected Return on Dollar DepositsExpected Return on Dollar Deposits

Expected dollar return on dollar deposits, R$

Current exchange rate, E$/€

1.02

1.03

1.05

1.07

0.031 0.050 0.069 0.079 0.100

1.00

R$

5959

Equilibrium: Interest ParityEquilibrium: Interest ParityCurrent FX $/£

1.6

1.5

2.5% 8.3% Expected USD returnon £ deposits

R$

Return on $ deposits

Equilibrium FX

6060

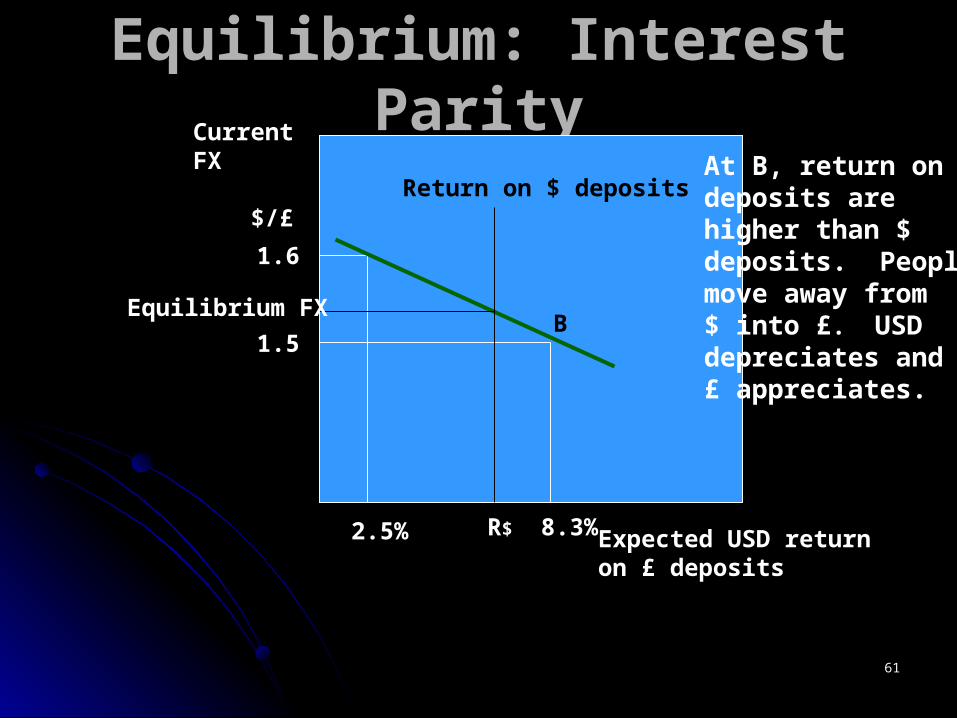

Equilibrium: Interest ParityEquilibrium: Interest ParityCurrent FX $/£

1.6

1.5

2.5% 8.3% Expected USD returnon £ deposits

R$

Return on $ deposits

Equilibrium FX

A

At A, return on $ is higher than return on £.People move away from £ into $. Demandfor $ increases,supply of £ increases. $ appreciates, £depreciates.

6161

Equilibrium: Interest ParityEquilibrium: Interest ParityCurrent FX $/£

1.6

1.5

2.5% 8.3% Expected USD returnon £ deposits

R$

Return on $ deposits

Equilibrium FXB

At B, return on £ deposits are higher than $ deposits. People move away from $ into £. USD depreciates and £ appreciates.

6262

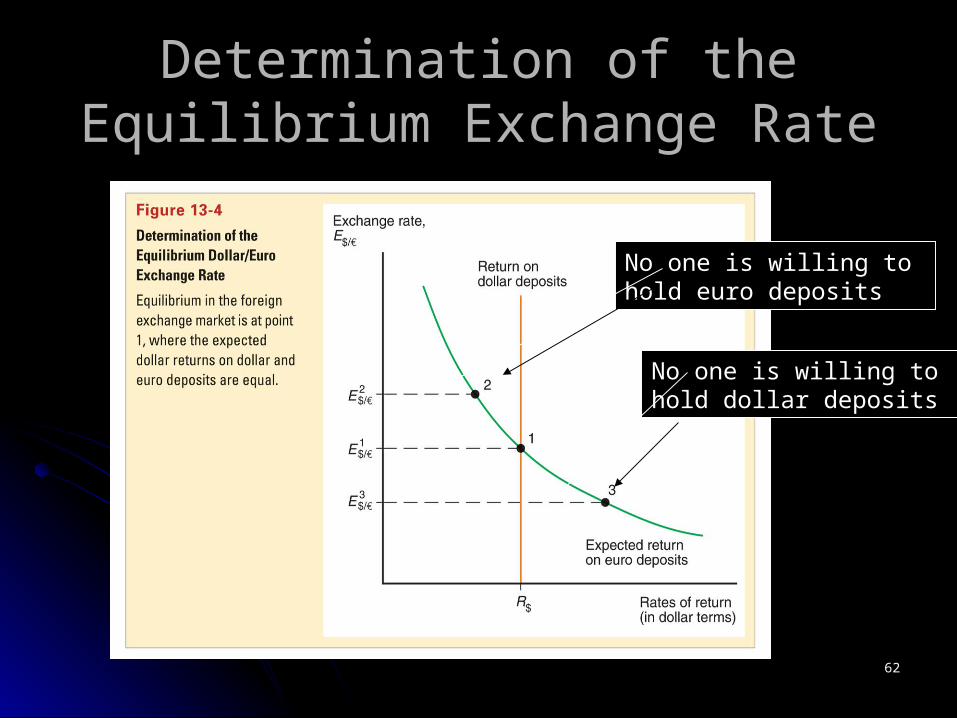

Determination of the Equilibrium Determination of the Equilibrium Exchange RateExchange Rate

No one is willing to hold euro deposits

No one is willing to hold dollar deposits

6363

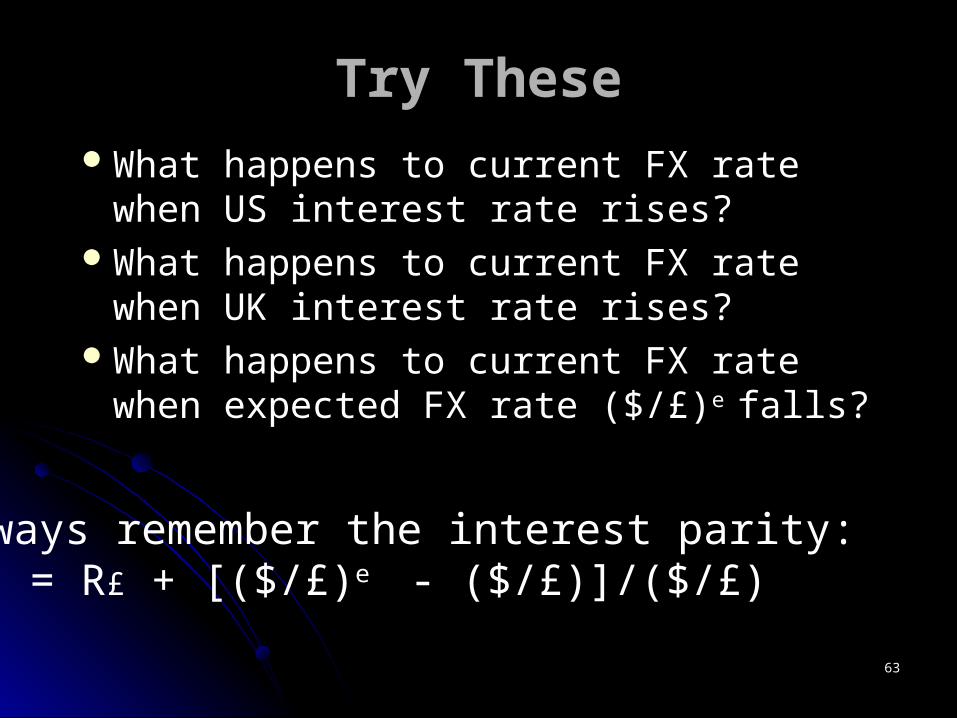

Try TheseTry These

What happens to current FX rate when What happens to current FX rate when US interest rate rises?US interest rate rises?

What happens to current FX rate when What happens to current FX rate when UK interest rate rises?UK interest rate rises?

What happens to current FX rate when What happens to current FX rate when expected FX rate ($/£)expected FX rate ($/£)e e falls?falls?

Always remember the interest parity:R$ = R£ + [($/£)e - ($/£)]/($/£)

6464

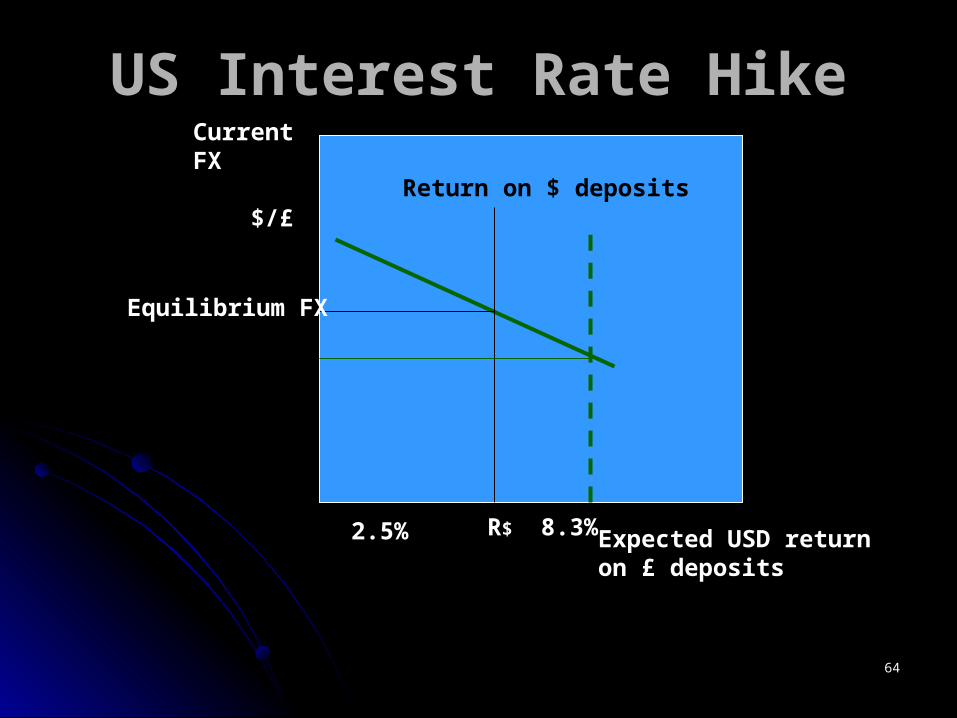

US Interest Rate HikeUS Interest Rate HikeCurrent FX $/£

2.5% 8.3% Expected USD returnon £ deposits

R$

Return on $ deposits

Equilibrium FX

6565

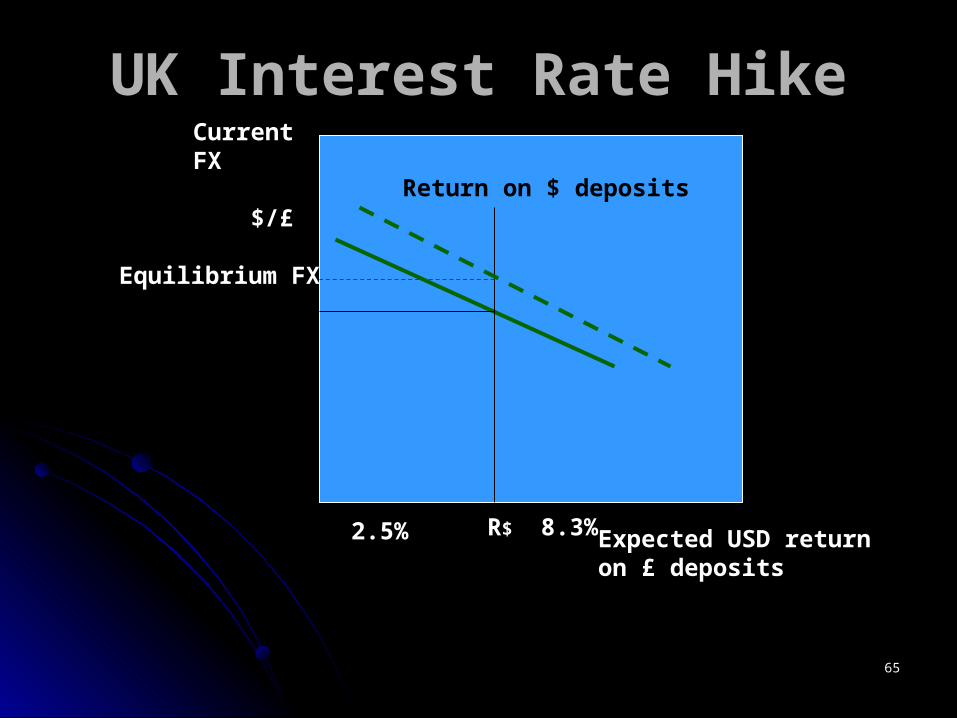

UK Interest Rate HikeUK Interest Rate HikeCurrent FX $/£

2.5% 8.3% Expected USD returnon £ deposits

R$

Return on $ deposits

Equilibrium FX

6666

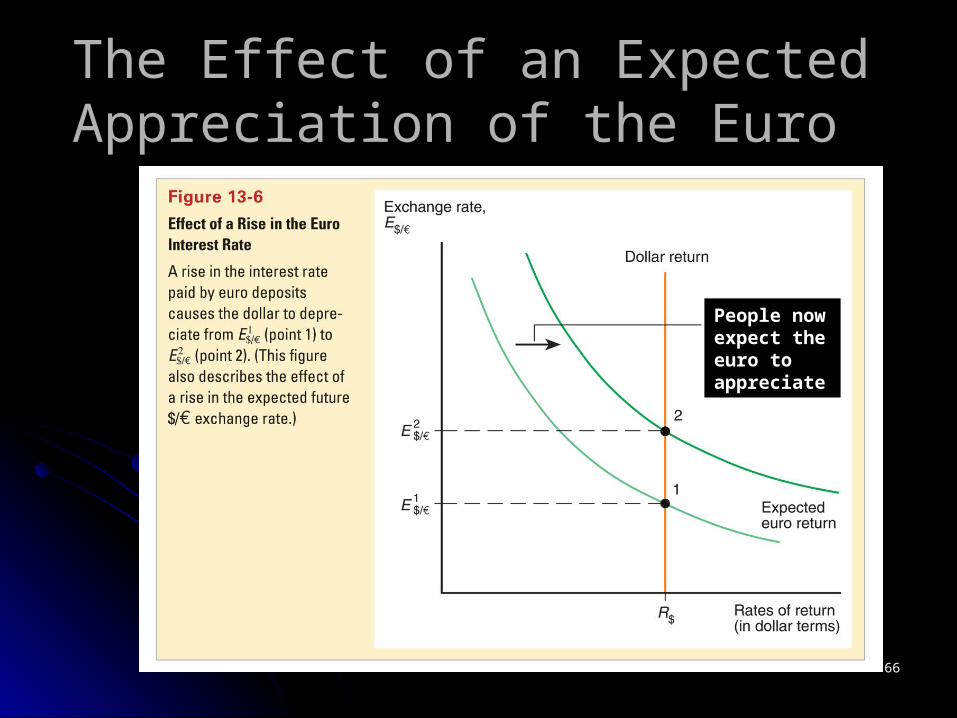

The Effect of an Expected Appreciation The Effect of an Expected Appreciation of the Euro of the Euro

People now expect the euro to appreciate

6767

The Effect of an Expected The Effect of an Expected Appreciation of the EuroAppreciation of the Euro

If people expect the euro to appreciate in the If people expect the euro to appreciate in the future, then investment will pay off in a valuable future, then investment will pay off in a valuable (“strong”) euro, so that these future euros will be (“strong”) euro, so that these future euros will be able to buy many dollars and many dollar able to buy many dollars and many dollar denominated goods.denominated goods. the expected return on euros therefore increases.the expected return on euros therefore increases. an expected appreciation of a currency leads to an an expected appreciation of a currency leads to an

actual appreciation (a self-fulfilling prophecy)actual appreciation (a self-fulfilling prophecy) an expected depreciation of a currency leads to an an expected depreciation of a currency leads to an

actual depreciation (a self-fulfilling prophecy)actual depreciation (a self-fulfilling prophecy)

6868

Covered Interest ParityCovered Interest Parity

Covered interest parity relates interest rates across Covered interest parity relates interest rates across countries and the rate of change between forward countries and the rate of change between forward exchange rates and the spot exchange rate:exchange rates and the spot exchange rate:

RR$ $ = = RR€€ + ( + (FF$/€$/€ - E - E$/€$/€)/)/EE$/€$/€

where where FF$/€$/€ is the forward exchange rate.is the forward exchange rate.

It says that rates of return on dollar deposits and It says that rates of return on dollar deposits and “covered” foreign currency deposits are the same.“covered” foreign currency deposits are the same. How could you make easy, risk-free money in the foreign How could you make easy, risk-free money in the foreign

exchange markets if covered interest parity did not hold?exchange markets if covered interest parity did not hold? Covered positions using the forward rate involve little risk.Covered positions using the forward rate involve little risk.