Embed Size (px)

Citation preview

1

Business Information TechnologyData Centers Presentation

RTF Data Center Working Group

Geoff Wickes

Emerging Technologies

NEEA May 7th, 2013

Updated May 8th, 2012

2

Emerging Technology

Goal: Fill the pipeline with energy

efficiency opportunities

Key Objective: Project portfolio with 20

year potential of 300 aMW

Activities: Identification Confirmation Market Readiness

3

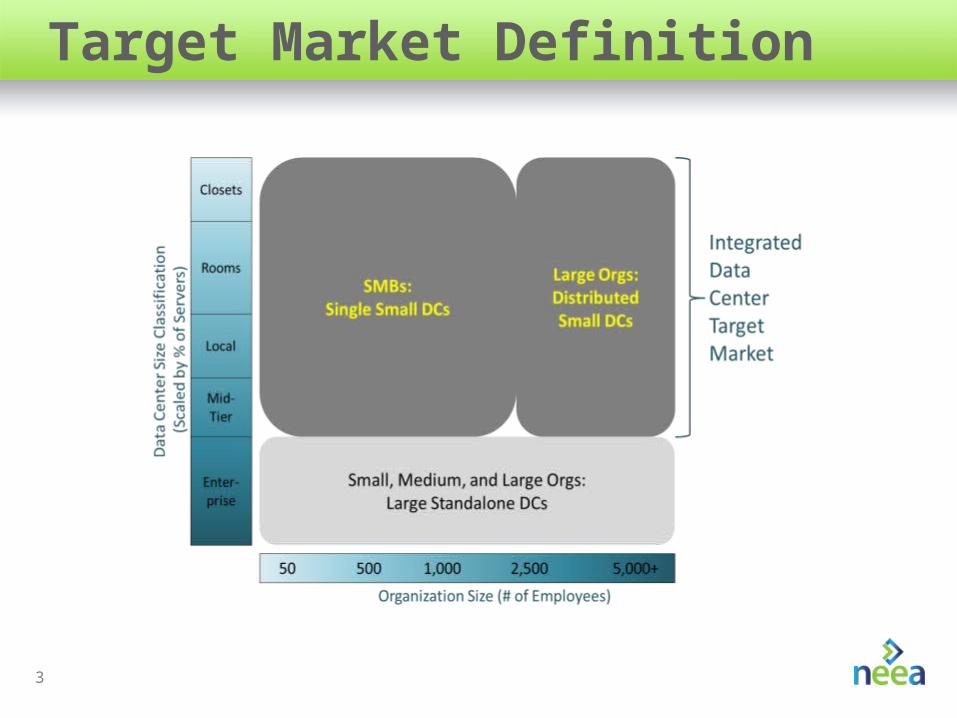

Target Market Definition

4

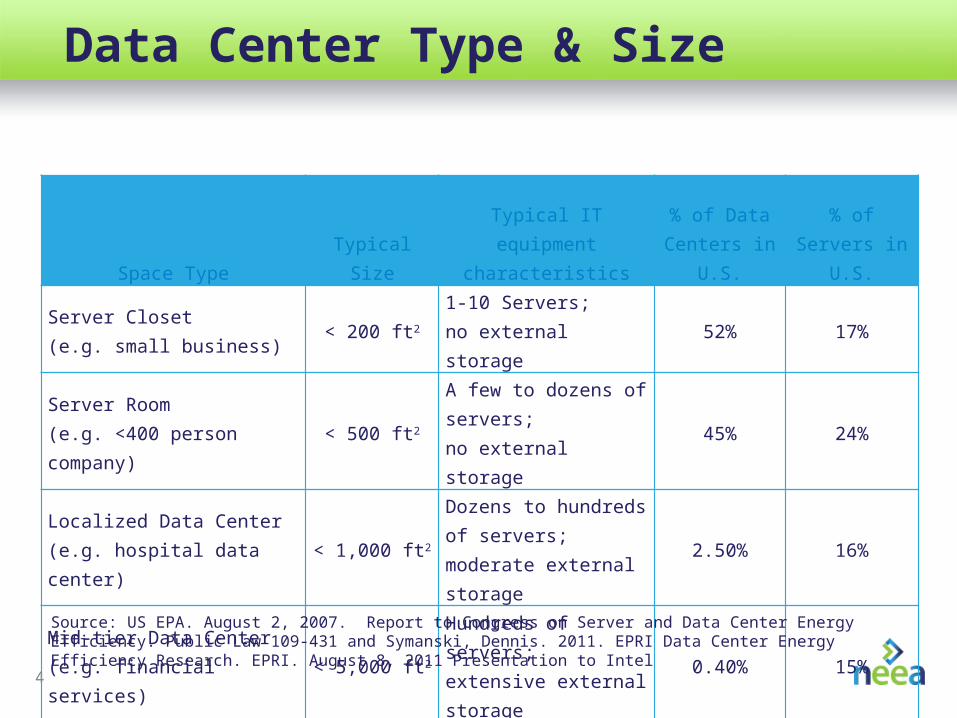

Data Center Type & Size

Space Type Typical SizeTypical IT equipment

characteristics

% of Data Centers in

U.S.% of Servers

in U.S.

Server Closet (e.g. small business)

< 200 ft21-10 Servers; no external storage

52% 17%

Server Room (e.g. <400 person company)

< 500 ft2

A few to dozens of servers; no external storage

45% 24%

Localized Data Center (e.g. hospital data center)

< 1,000 ft2

Dozens to hundreds of servers; moderate external storage

2.50% 16%

Mid-tier Data Center (e.g. financial services)

< 5,000 ft2

Hundreds of servers; extensive external storage

0.40% 15%

Source: US EPA. August 2, 2007. Report to Congress on Server and Data Center Energy Efficiency. Public Law 109-431 and Symanski, Dennis. 2011. EPRI Data Center Energy Efficiency Research. EPRI. August 8, 2011 Presentation to Intel

5

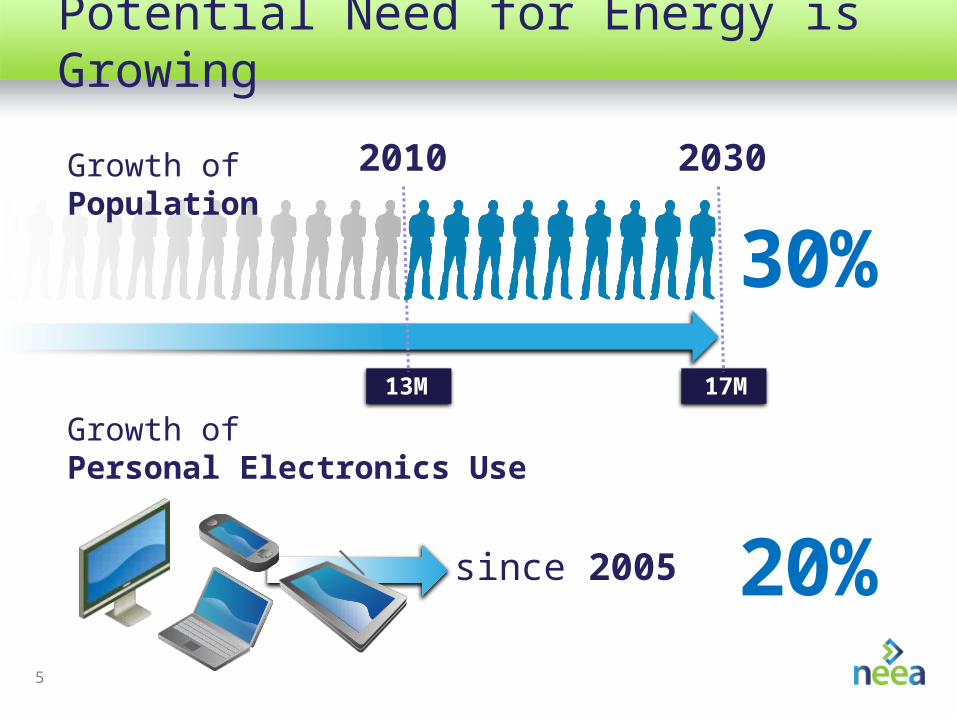

Potential Need for Energy is Growing

17M

2010

30%

2030

13M

Growth of Personal Electronics Use

Growth of Population

since 2005 20%

6

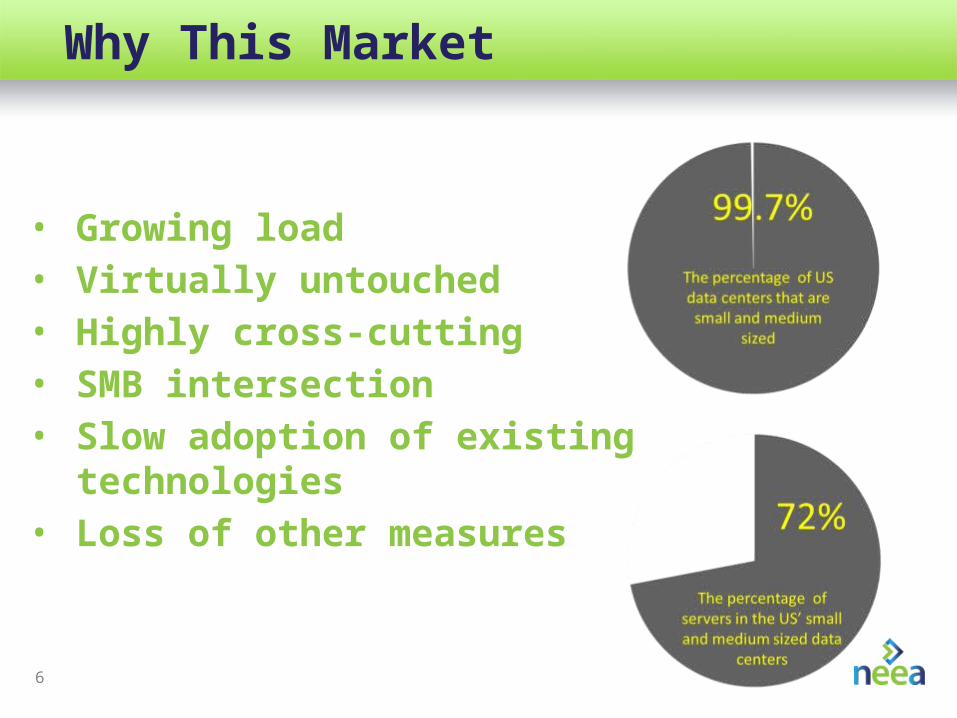

Why This Market

• Growing load• Virtually untouched• Highly cross-cutting• SMB intersection• Slow adoption of existing

technologies• Loss of other measures

7

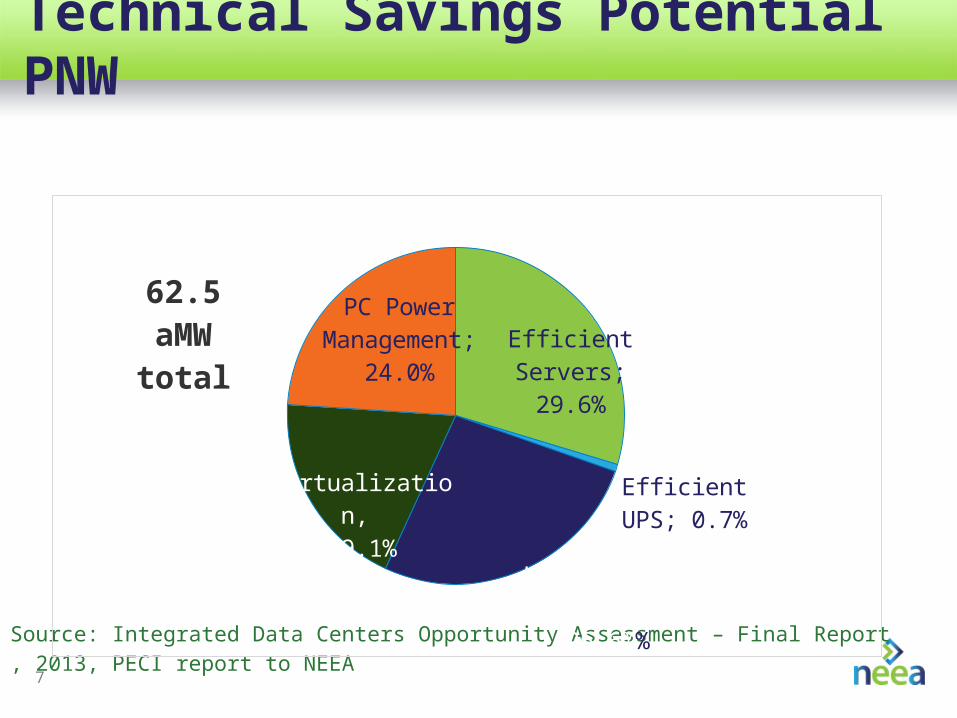

Technical Savings Potential PNW

Source: Integrated Data Centers Opportunity Assessment – Final Report , 2013, PECI report to NEEA

Efficient Servers; 29.6%

Efficient UPS; 0.7%

HVAC and Air Handling,

26.6%%

Virtualization, 19.1%

PC Power Man-agement; 24.0%

62.5 aMW total

8

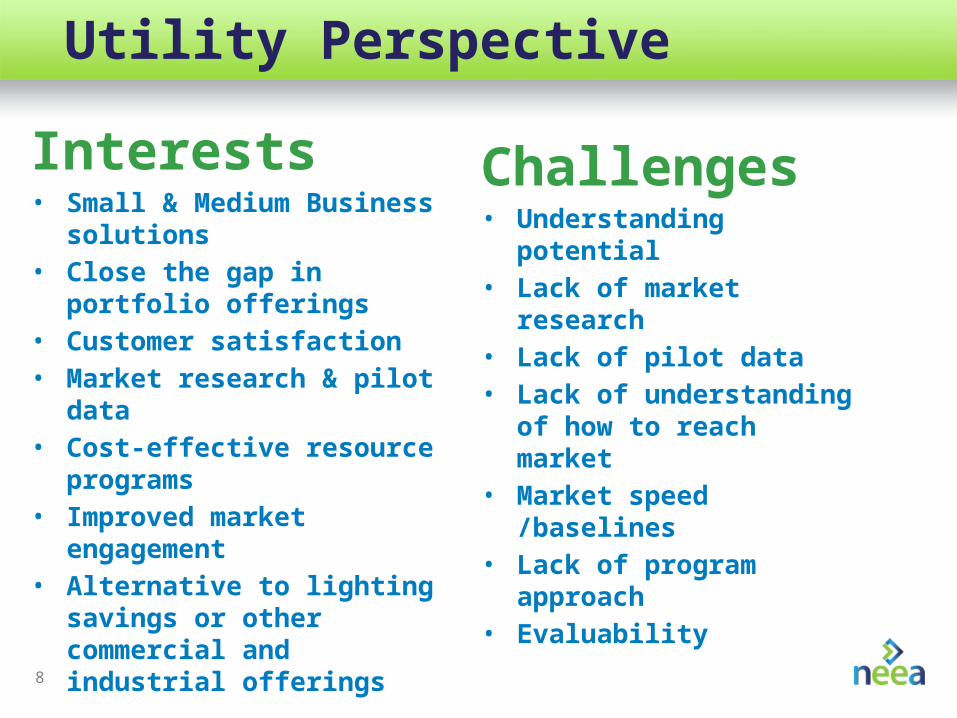

Utility Perspective

Interests• Small & Medium Business

solutions• Close the gap in portfolio

offerings• Customer satisfaction• Market research & pilot data• Cost-effective resource

programs• Improved market engagement• Alternative to lighting savings

or other commercial and industrial offerings

Challenges• Understanding potential• Lack of market research • Lack of pilot data• Lack of understanding of

how to reach market• Market speed /baselines• Lack of program approach• Evaluability

9

Opportunity

Coordinated Intervention

Combined Resources

Leverage

Market Reach

Market Engagement

Unlock Savings

Support Utilities

Market Transformation

10

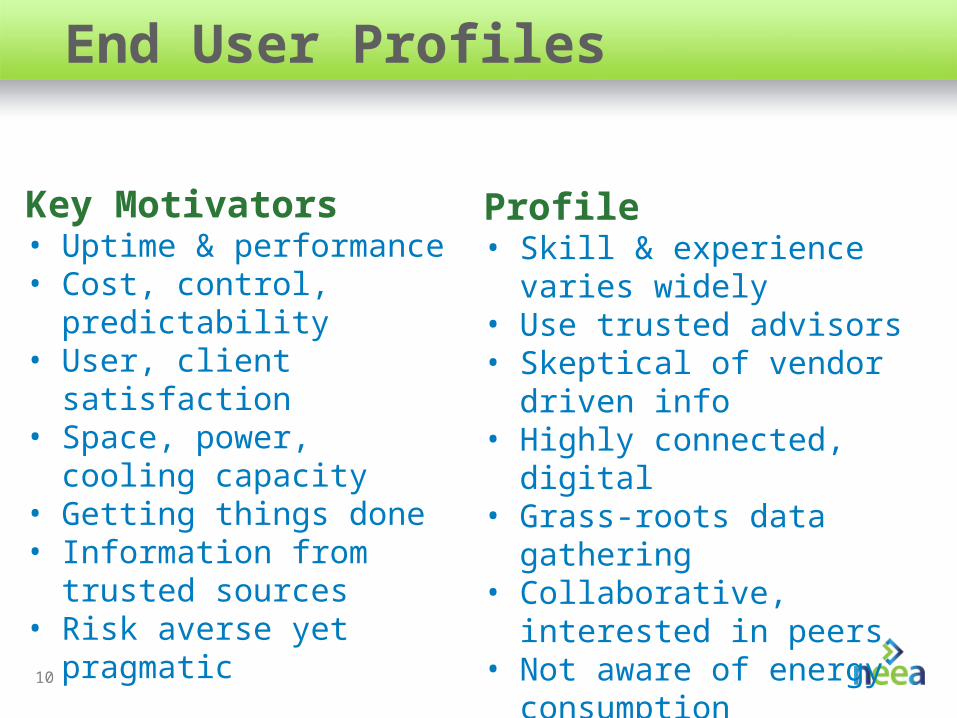

End User Profiles

Key Motivators• Uptime & performance• Cost, control, predictability• User, client satisfaction• Space, power, cooling

capacity• Getting things done• Information from trusted

sources• Risk averse yet pragmatic

Profile• Skill & experience varies

widely• Use trusted advisors• Skeptical of vendor driven

info• Highly connected, digital • Grass-roots data gathering• Collaborative, interested in

peers• Not aware of energy

consumption

11

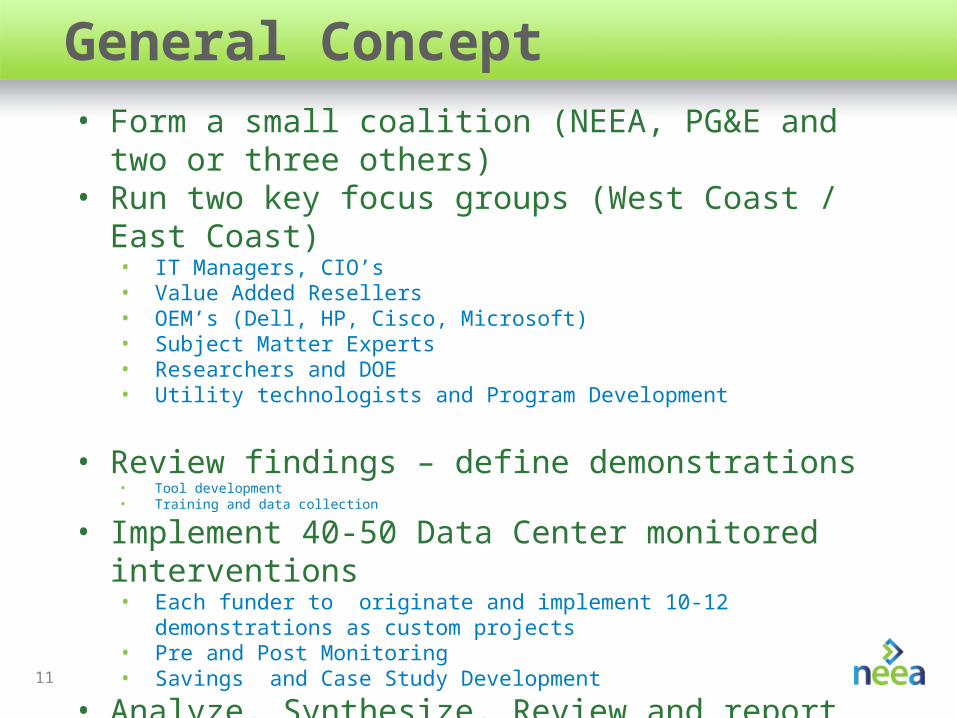

General Concept • Form a small coalition (NEEA, PG&E and two or three

others) • Run two key focus groups (West Coast / East Coast)

• IT Managers, CIO’s • Value Added Resellers• OEM’s (Dell, HP, Cisco, Microsoft)• Subject Matter Experts• Researchers and DOE • Utility technologists and Program Development

• Review findings – define demonstrations• Tool development• Training and data collection

• Implement 40-50 Data Center monitored interventions• Each funder to originate and implement 10-12 demonstrations as custom

projects• Pre and Post Monitoring• Savings and Case Study Development

• Analyze, Synthesize, Review and report results – Make recommendations

12

Proposed Approach

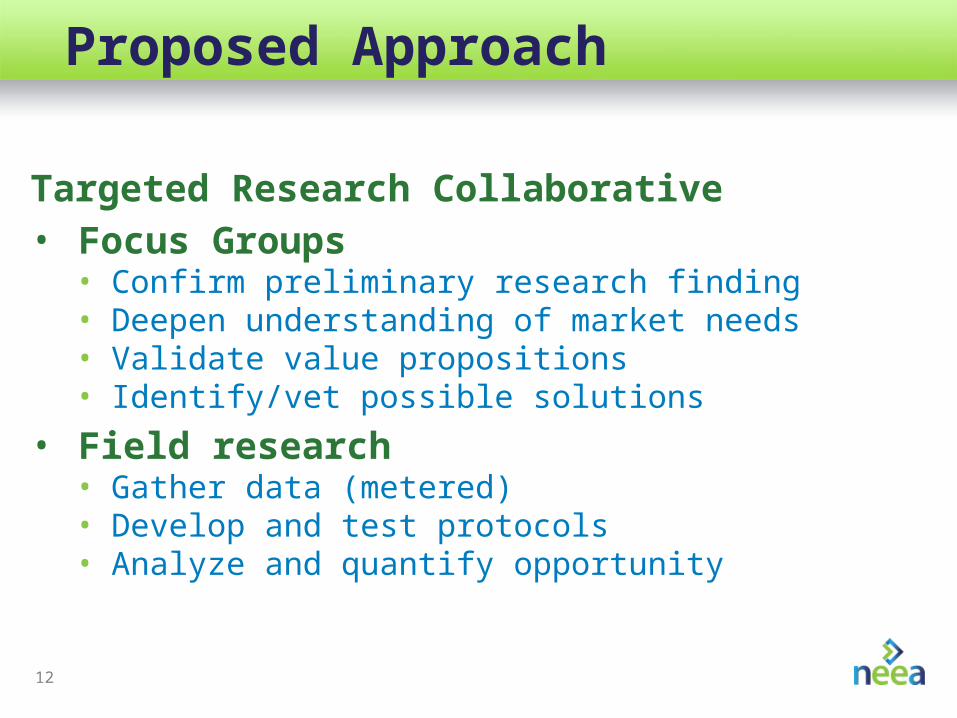

Targeted Research Collaborative • Focus Groups

• Confirm preliminary research finding• Deepen understanding of market needs• Validate value propositions • Identify/vet possible solutions

• Field research • Gather data (metered)• Develop and test protocols• Analyze and quantify opportunity

13

Optimal Solution

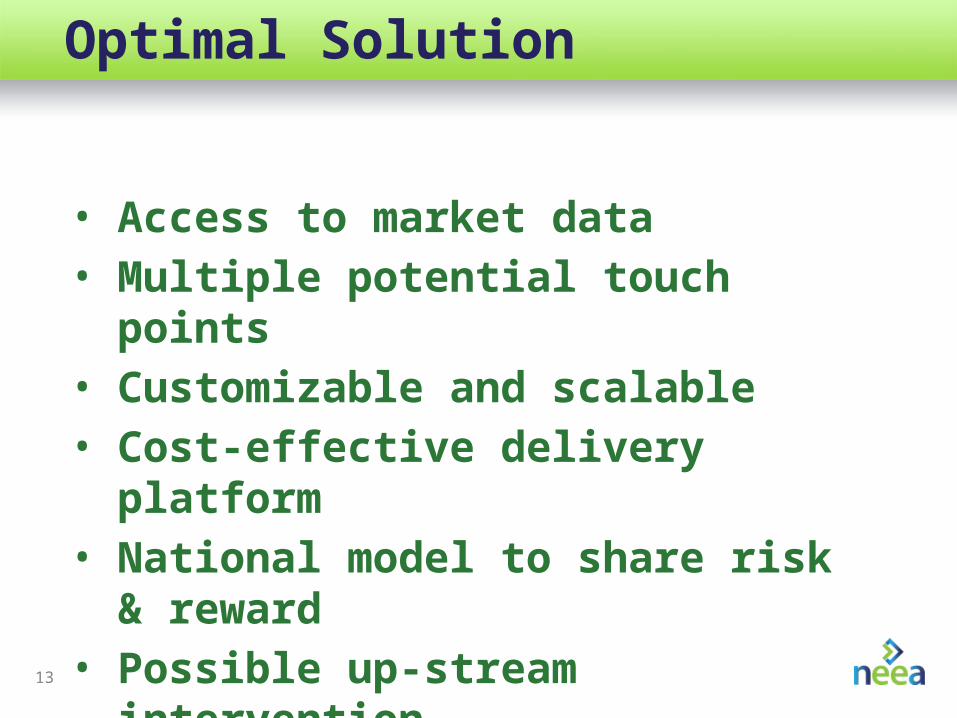

• Access to market data• Multiple potential touch points • Customizable and scalable• Cost-effective delivery platform• National model to share risk &

reward• Possible up-stream intervention

14

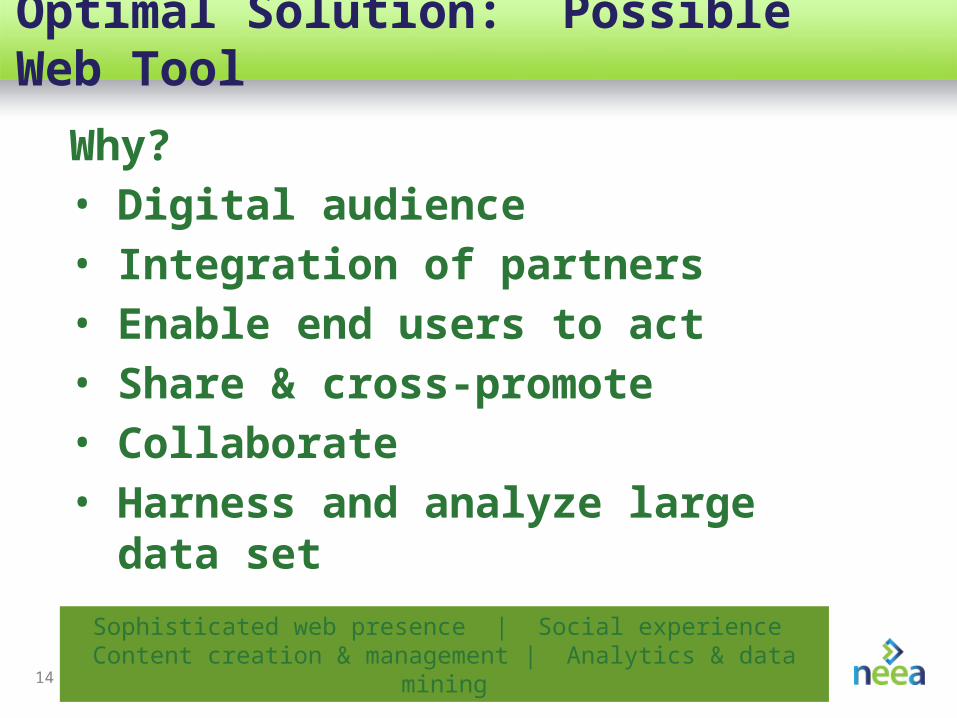

Optimal Solution: Possible Web Tool

Why?• Digital audience• Integration of partners• Enable end users to act• Share & cross-promote• Collaborate• Harness and analyze large data set

Sophisticated web presence | Social experience Content creation & management | Analytics & data mining

15

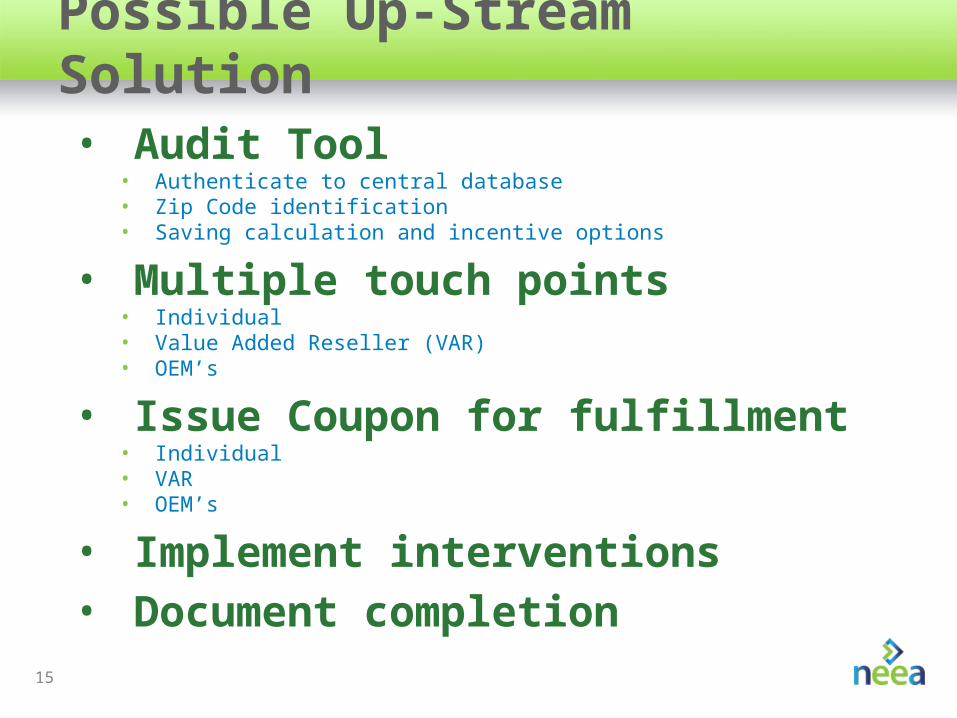

Possible Up-Stream Solution

• Audit Tool• Authenticate to central database• Zip Code identification• Saving calculation and incentive options

• Multiple touch points• Individual• Value Added Reseller (VAR)• OEM’s

• Issue Coupon for fulfillment• Individual• VAR• OEM’s

• Implement interventions• Document completion

16

1. Recruit RC Members & Launch

Research Scope

17

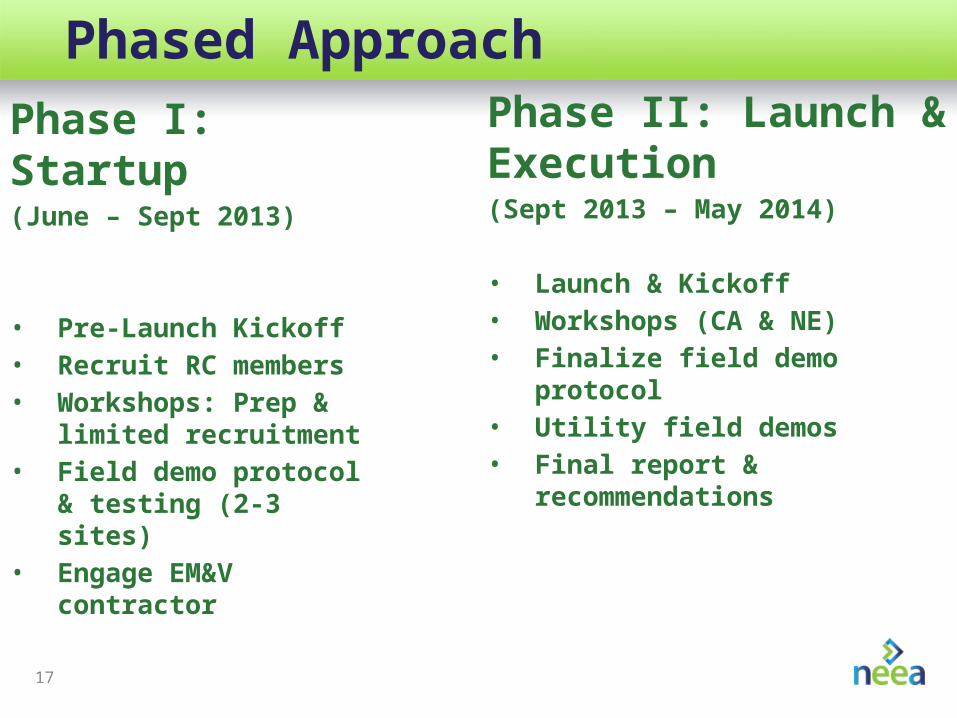

Phased Approach

Phase I: Startup (June – Sept 2013)

• Pre-Launch Kickoff• Recruit RC members• Workshops: Prep &

limited recruitment• Field demo protocol &

testing (2-3 sites)• Engage EM&V contractor

Phase II: Launch & Execution(Sept 2013 – May 2014)

• Launch & Kickoff• Workshops (CA & NE)• Finalize field demo protocol• Utility field demos• Final report & recommendations

18

Budget Overview

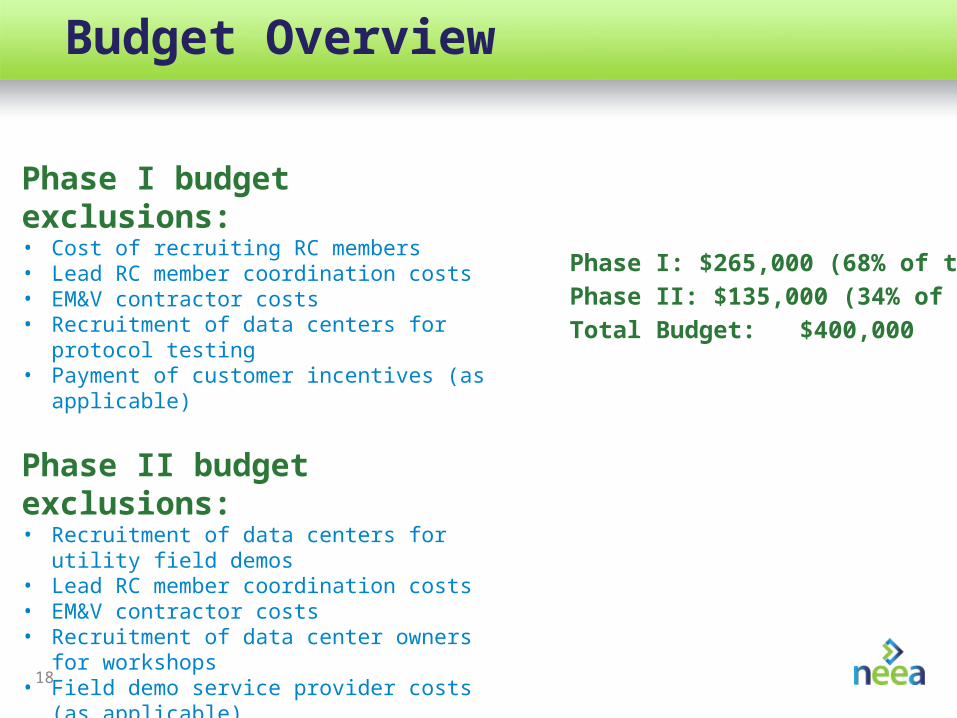

Phase I budget exclusions:• Cost of recruiting RC members• Lead RC member coordination costs• EM&V contractor costs• Recruitment of data centers for protocol testing• Payment of customer incentives (as applicable)

Phase II budget exclusions:• Recruitment of data centers for utility field demos• Lead RC member coordination costs• EM&V contractor costs• Recruitment of data center owners for workshops• Field demo service provider costs (as applicable)• Payment of customer incentives (as applicable)

Phase I: $265,000 (68% of total)

Phase II: $135,000 (34% of total)

Total Budget: $400,000

19

Additional Content

![[MS-OXRTFCP]: Rich Text Format (RTF) Compression Algorithm · The Rich Text Format (RTF) Compression Algorithm is used to compress and decompress RTF data, as described in [MSFT-RTF],](https://img.pdfslide.us/doc/110x75/5e9e1be31138b067ae753825/ms-oxrtfcp-rich-text-format-rtf-compression-algorithm-the-rich-text-format.jpg)