Embed Size (px)

Citation preview

1

AUSTRALIA

Winning Strategies in Major project implementation

Jeremy HarrisBFA Conference, Port of Spain June 2008

Energy and Natural Resources

2

Covering today

1. Context

2. Global Survey

3. Sector Challenges

4. Trends

5. Conclusions

3

Context

Boom in the global projects market is unprecedented in world history

China and India Russia and Brazil New technologies Years of under-investment in infrastructure

4

Focus of presentation

Changing Environment“The Project”

IndustryOutlook

KPMGSurvey

Why areProject

OutcomesPoor?

5

Embracing Change?Global Construction Survey 2008

6

KPMG annual survey

KPMG’s Global Construction Survey 2005

KPMG’s Global Construction Survey 2007

KPMG’s Global Construction Survey 2008

7

KPMG survey themes

In KPMG’s 2005 Global Construction Survey, contractors expressed particular concern about managing risks in contracts, finding ways to price at a profit and recruiting and retaining the best talent.

In KPMG’s 2007 Global Construction Survey, we sought the views of buyers and owners of construction services, who saw the shortage of qualified contractors and the steep rise in costs as real barriers to completing future projects.

In KPMG’s 2008 Global Construction Survey, we focused the views of leading construction contractors around the world on four key areas impacting the industry:

Resource shortagesRisk managementEscalating costsSustainability

8

Construction Survey Findings – priorities

Owner Perspective

1. Availability of Qualified Contractors

2. Shortage of Internal Resources

3. Managing Risk

4. Rising Cost of Construction

Source: KPMG’s 2007 Global Construction Survey

5. Environmental Matters

6. Availability of Qualified Vendors

7. Delivery on Time and Budget

8. Regulatory Matters

9. Technology

10. Transferring Risk

11. Entering New Markets

1. Shortage of Qualified Resources

2. Managing Risk

3. Transferring Risk

4. Securing Forward Workload5. Entering New Markets

6. Gaining Competitive Edge

7. Succession Planning

8. Bonding Capacity

9. Reducing Overhead

10. Industrial Relations

Pri

ori

ty

Pri

ori

ty

Contractor Perspective

9

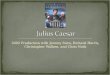

Overcoming resource shortages

84 percent of respondents say the construction industry is not doing enough to tackle

skills shortages

Over half of those responding, 55 percent, see the shortage

of good people as critical right now

The biggest single fear, 49 percent, is that a lack of good people will restrict the growth

plans of contractors

10

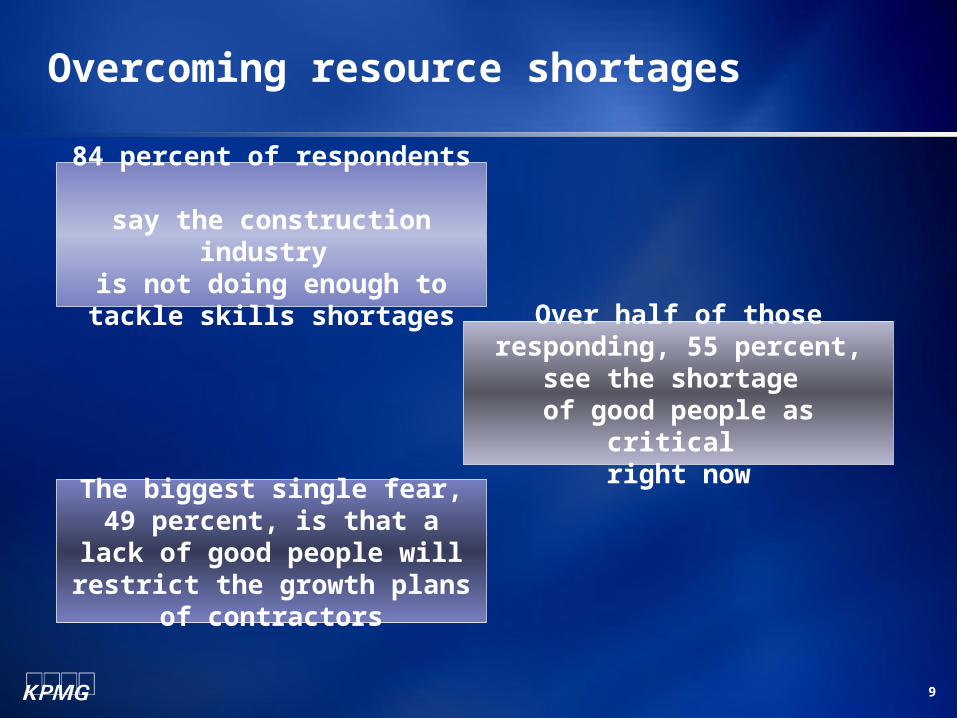

What will be the impact of this scarcity

9%

2%

19%

21%

49%

Other

We will have to beomemore specialized

Increase project costs

Increase the risk oncurrent projects

Restrain growth

How will resource issues negatively affect your business?

Source: Embracing Change? Global Construction Survey 2008, KPMG International

11

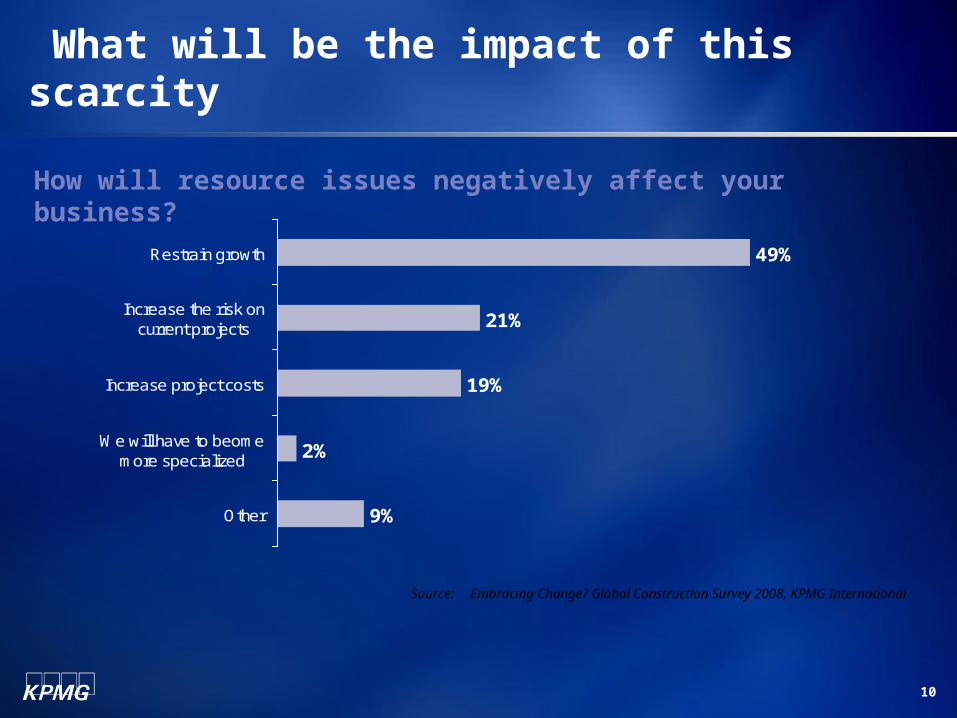

Managing risks in an uncertain environment

81 percent claim to effectivelyIdentify and assess risk

Over 70 percent feel risk assessment is effective

throughout the project life cycle

Only a third of CEOs carry direct responsibility for risk

management strategy

12

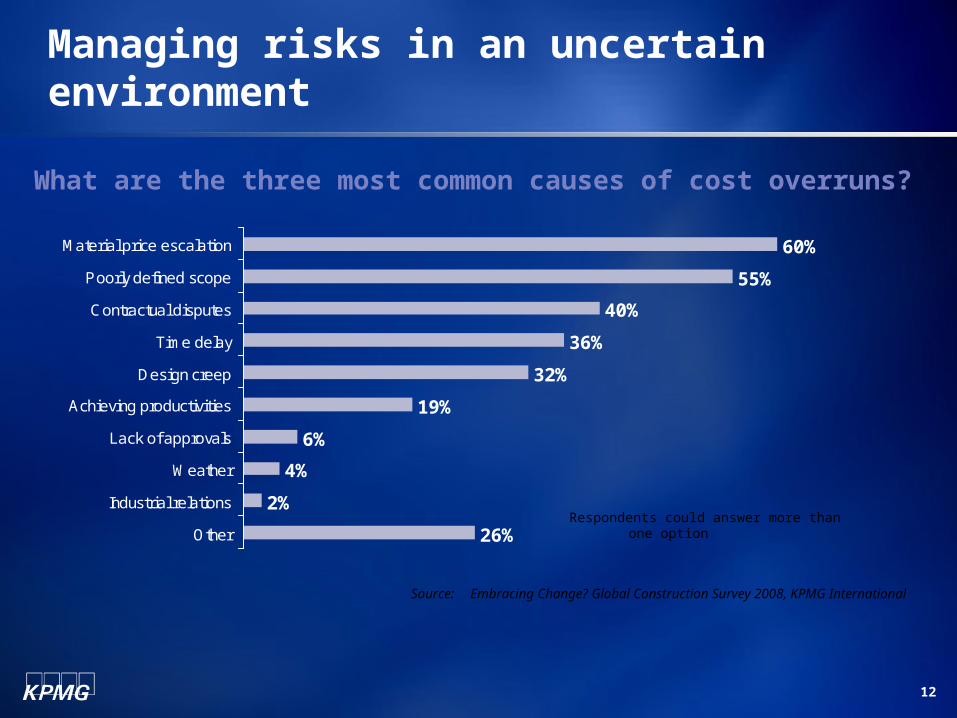

Managing risks in an uncertain environment

26%

2%

4%

6%

19%

32%

36%

40%

55%

60%

Other

Industrial relations

Weather

Lack of approvals

Achieving productivities

Design creep

Time delay

Contractual disputes

Poorly defined scope

Material price escalation

What are the three most common causes of cost overruns?

Source: Embracing Change? Global Construction Survey 2008, KPMG International

Respondents could answer more than one option

13

How well is risk integrated into the project management process?

36%

30%

13%

7%

7%

7%CFO

COO

Risk Manager / Director

Project Director

Board / Board Committees

CEO

Who is responsible for your risk management strategy?

Source: Embracing Change? Global Construction Survey 2008, KPMG International

14

Coping with escalating costs

9%

13%

13%

13%

23%

38%

45%

45%

53%

6%

2%

9%Other

Insurance

Plant

Structured elements

Manufactured equipment

Staff supervision

Copper and cement

Fuel prices

Building materials

Labor costs / trades

Sub-contractors

Steel

Where are you most susceptible to cost escalation

Source: Embracing Change? Global Construction Survey 2008, KPMG International

Respondents could answer more than one option

15

Passing on benefits – and costs

44%

7%

49%

Very detailed - down to theindividual material itemsthemselves

Detailed - based on a percentageof elements (i.e. material costs and/or labor costs)

Summary level - based on apercentage of the total project cost

When preparing your initial budget, how detailed is your cost escalation estimate?

Source: Embracing Change? Global Construction Survey 2008, KPMG International

16

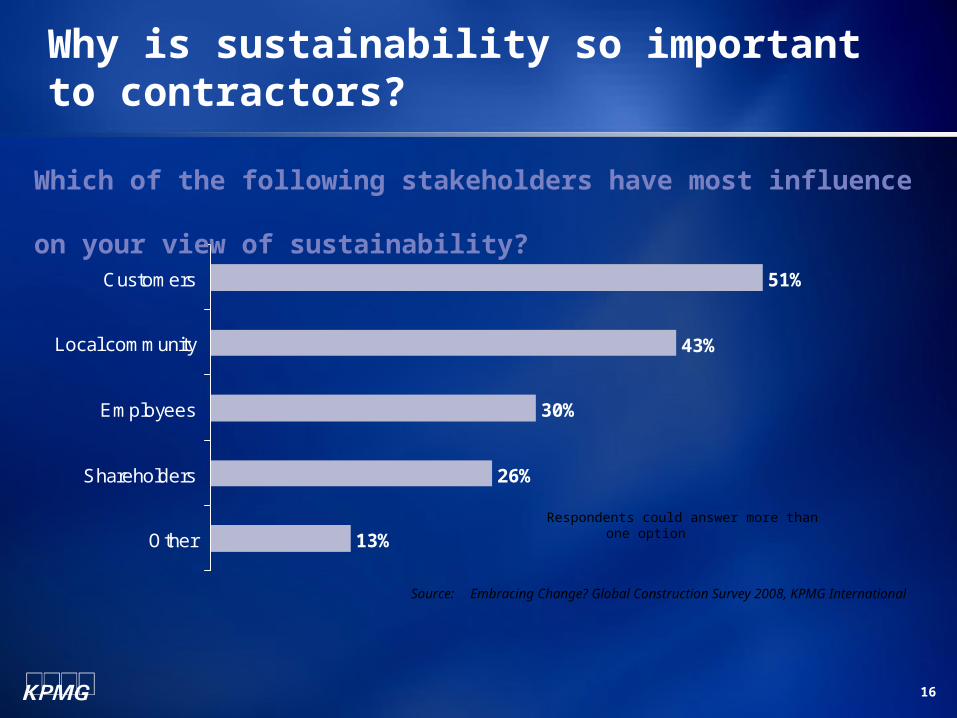

Why is sustainability so important to contractors?

13%

26%

30%

43%

51%

Other

Shareholders

Employees

Local community

Customers

Which of the following stakeholders have most influence on your view of sustainability?

Source: Embracing Change? Global Construction Survey 2008, KPMG International

Respondents could answer more than one option

17

Energy sector challenges

18

Key sector challenges

Typically projects are large (>$500m, commonly $multi-billion)Assets are frequently indivisible

Facilities are often developed in adverse physical environments, socio-political instability adding to risk and complexity

Transferring the asset to another location is generally technically unfeasible and/or commercially unviable

Asset design/development and implementation times are long, typically 2-4 years and 3-6 years, respectively

Material and labour costs escalation during the construction period Adverse regulation where authorities are transitional or unstable

Lack of available technical staff

19

Why poor performance?

20

Why Has Project Performance not Improved?

“Forecasts of cost, demand, and other impacts of planned projects have

remained constantly and remarkably inaccurate for decades”

“For the 70 year period for which cost data are available, accuracy in cost

forecasts has not improved”

Type of Project Average Inaccuracy

Rail 44.7%

Bridges and Tunnels 33.8%

Road 20.4%

21

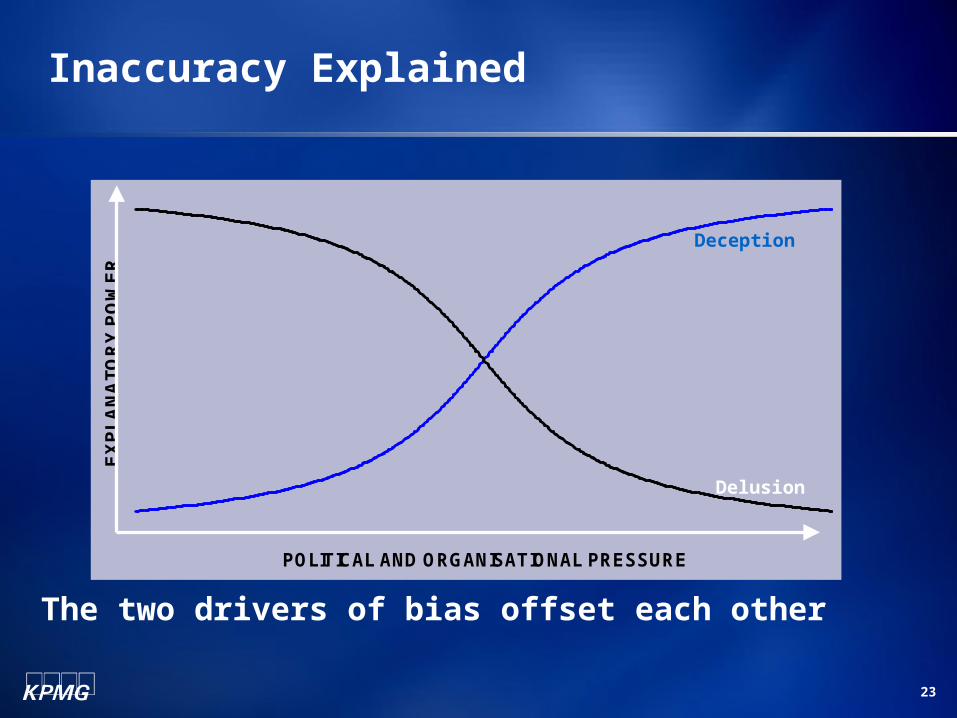

Inaccuracy Explained

Statistically inaccuracy is not due to;Unreliable or outdated dataInappropriate forecasting modelsInappropriate systems or toolsInexperience

Accuracy of estimates has not improved in 70 years in spite of:Improved data and methods after decades of studyModern systemsSpecialized trainingProfessional knowledge standards Accumulated experience

Flyvbjerg

Expected Distribution

Over BudgetUnder Budget 0

Improvement over time

22

Inaccuracy Explained

The analysis can be explained in psychological terms

Inaccuracy due to optimism bias Inaccuracy due to strategic misrepresentation

These explanations complement each other leading to a consistent inaccuracy

in forecasting

23

Inaccuracy Explained

POLITICAL AND ORGANISATIONAL PRESSURE

EX

PL

AN

ATO

RY

PO

WE

R

Deception

Delusion

The two drivers of bias offset each other

24

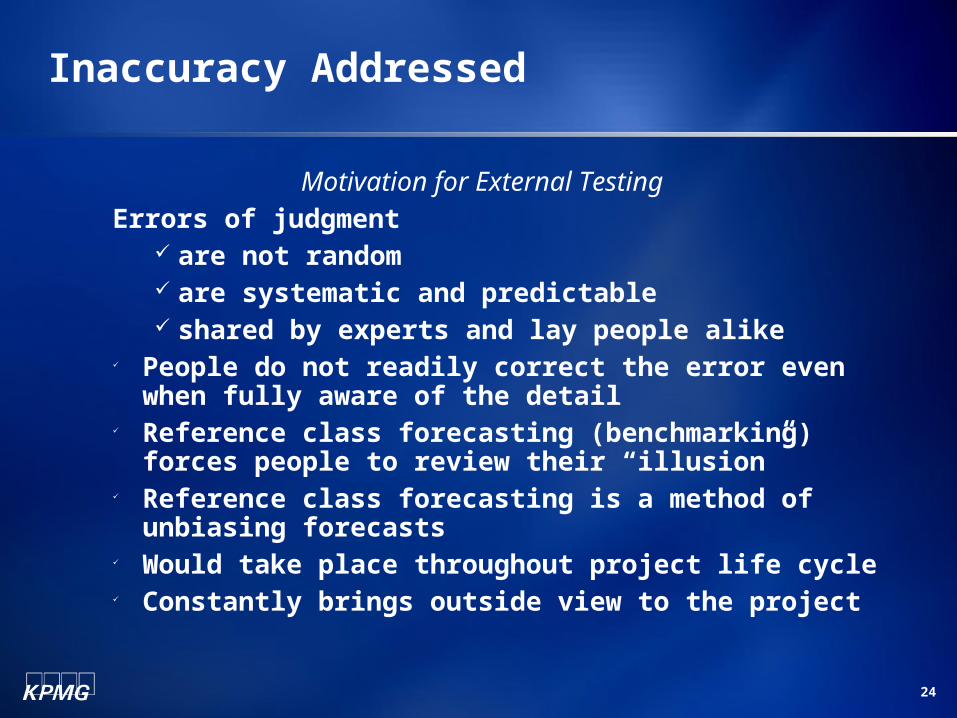

Inaccuracy Addressed

Motivation for External TestingErrors of judgment

are not random are systematic and predictable shared by experts and lay people alike

People do not readily correct the error even when fully aware of the detail

Reference class forecasting (benchmarking) forces people to review their “illusion”

Reference class forecasting is a method of unbiasing forecasts

Would take place throughout project life cycle Constantly brings outside view to the project

25

Changing Environment

Oversight of contractors activities will increase Transparency will become the norm New contracting models are appearing Owners independent oversight will extend to contractors Contractors will need to lift their own reporting quality to

level of client

26

Conclusions

Raise sector profile

Create risk-aware culture

Manage reality of costs

Sustainability

27

Jeremy Harris

Practice Leader

Major Projects Advisory

KPMG LLP (UK)

+44 (0)20 7311 8337

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2008 KPMG International. KPMG International is a Swiss cooperative. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

![BFA - Fortune Teller [2015]](https://img.pdfslide.us/doc/110x75/589f44301a28ab490c8b6b29/bfa-fortune-teller-2015.jpg)