Embed Size (px)

Citation preview

1

Anne ter Braak

Barbara Deleersnyder

Inge Geyskens

Marnik G. Dekimpe

SLEEPING WITH THE ENEMY: Does Private-Label Production by

National-Brand Manufacturers Create Discounter Goodwill?

2

Current situation Private labels are becoming more and more

important in retailing

>40%

Switzerla

nd

U.K.

Prior empirical research

Determinants of private-label success (Hoch and Banerji, 1993; Dhar and Hoch, 1997; Steenkamp and Dekimpe, 1997; Lamey et al. 2011).

Demographic and psychographic characteristics of PL buyers

(Richardson et al.,1996; Ailawadi et al., 2001; Ailawadi and Keller, 2004).

Prior empirical research

Determinants of private-label success

Demographic and psychographic characteristics of PL buyers

Private-label production: largely ignored

5

Some absolute numbers

European PL market (2010): €431 billion

Wal-Mart PL sales (2009): $132 billion

6

Retailers hardly ever occurs (Mills 1995)

Who produces private labels?

7

Retailers hardly ever occurs (Mills 1995)

Dedicated private label manufacturers

Who produces private labels?

8

Retailers hardly ever occurs (Mills 1995)

Dedicated private label manufacturers: Mostly for commoditized products

National-brand (NB) manufacturers

Who produces private labels?

9

Mixed choices

(Kumar & Steenkamp 2007)

PL production: YES!

PL production: NO!

NB manufacturers are struggling… “Whether to produce PLs or not, is certainly one of

the central dilemmas that preoccupy NB manufacturers.”

(Business Strategy Review 2006, p.42)

Despite the “high level of managerial interest” surprisingly little research has studied this phenomenon. (Sethuraman, Marketing Science 2009, p. 771)

10

Prior research on PL production Game-theoretical models

see e.g.,Gomez-Arias and Bello-Acebron 2008; Kumar, Radhakrishnan, and Rao 2010

Structural Model (1 product category) Chen et al. 2010

Very limited empirical research

11

12

Why still an issue?

Hard to get the data “a true CIA job” (Alfred Dijs, Director Knowledge Management and Transfer, GfK, April 2008)

managers very secretive about it

invalidates survey methodology

13

Major motivation to NOT produce Implications for own brand image, brand

equity

14

Excess capacity

Ability to influence PL quality

To cultivate a better relation with retailers, i.e. to create retailer goodwill

Major motivations to produce PLs

15

Underlying arguments

PL production is cooperative behavior of NB manufacturer

is perceived as a pledge by the retailer(Anderson & Weitz 1992)

may increase relational embeddedness (Kaufman, Jayachandran, and Rose 2006)

16

Mixed support for “goodwill” argument

}o

}-

Dunne & Narasimhan (HBR, 1999)

“For manufacturers who seek closer ties with retailers, private labels may represent a neglected opportunity […]”

Quelch & Harding (HBR, 1996)“[….] no evidence that making PL products enhances a brand

manufacturer’s trade relationships […]”

Kumar & Steenkamp (2007)

“[…] we were never able to uncover hard evidence that making private label products […] leads to preferential merchandising support”

Glemet & Mira (The McKinsey Quarterly, 1993)

“ […] result in a long-term deterioration of overall relationship […] once the honeymoon is over.”

}+

17

Goodwill can manifest itself in:Product (Dunne & Narasimhan 1999; Quelch & Harding 1996)

• Shelf access• Shelf breadth Shelf presence• Shelf length

Selection as category captain

Promotion• Extent of pass-through (Ailawadi & Harlam 2008)

• Promotional calendar (Dunne & Narasimhan 1999; Quelch & Harding 1996)

18

Our setting: PL Production for Discounters Increasingly important channel (30+ market

share in Germany, 2007)

19

KEY CHARACTERISTICS DISCOUNT KEY CHARACTERISTICS DISCOUNT STORESSTORES

Simple, no-frills, store format

Compete on price

More limited assortment depth

Emphasize PL

Recent development

Started to add a few NBs in their assortment

Why? (Deleersnyder et al. 2007)

- Way of differentiation relative to other discounters

- Way to expand customer base

21

Added benefits of discount setting Centralized approach to assortment

management

No (very limited) use of slotting allowances

EDLP setting

22

23

As such:

Discounter goodwill can manifest itself in: NB Shelf presence

Hence:

H1: PL production by a NB manufacturer increases the likelihood of shelf presence

Manufacturer market power

Powerful firms secure high levels of influence on channel members (e.g., Anderson, Lodish, and Weitz 1987; Rao and McLaughlin 1989; Shervani, Frazier, and Challagalla 2007).

H2: NB manufacturer market power increases the likelihood of shelf presence

24

Interaction effect

H3a: PL production enhances (amplifies) the effect of manufacturer market power in increasing the likelihood of shelf presence for a NB manufacturer.

H3b: PL production diminishes the effect of manufacturer market power in increasing the likelihood of shelf presence for a NB manufacturer.

25

26

Moreover….

Not all NB manufacturers are equally willing to participate in PL production.

Not all NB manufacturers are equally appealing to the retailer as PL producer

Both retailer and manufacturer considerations

Observable drivers of PL production by a given manufact.

Unobservable drivers: self-selection model

27

Observable drivers Manufacturer sales growth (H4)

Ease of producing high-quality products (H5)

Manufacturer marketing tools Innovativeness of manufacturer (H6) Extent of advertising support of manufacturer (H7) Price premium manufacturer can charge (H8)

Manufacturer market power (H9)

28

+H2 +/-

H9

-H4

+H1

+H5

+/-H6, H7, H8

Ease of Producing High-Quality Products

Manufacturer Marketing Tools: - Innovations - Advertising - Price Premium over PLs

PL Production

Manufacturer Market Power

Manufacturer Sales Growth

Shelf Presence

+/- H3

Conceptual Framework

CONSEQUENCEANTECEDENTS

Data

Europe’s leading hard discounter:

Europe’s leading soft discounter:

29

30

Data Aldi: 37 categories Mercadona: 53 categories

That contained at least one NBProduct Group ExamplesAssorted foods noodles, jam, riceBeverages beer, mineral water, juiceCandy candy bars, chocolate, bonbonsCanned/bottled foods fish, beans, tomatoCare products shampoo, diapers, toilet tissueCooking fats butter, olive oil, margarineCleaning products bleach, detergent, fabric conditionerDairy products milk, yoghurt, ice creamHousehold supplies basket bin bags, toilet tablets, cellulosesInstant meals ready desserts, ready meals, saladPastry cakes, sweet biscuitsPet products wet dog food, dry dog foodTaste enhancers ketchup, salad dressing, mayonnaise

31

Data collection procedure (1)

1. Derive top 5 NB manufacturers per category

Source: GfK panel data (for Aldi) and Kantar Worldpanel data (for Mercadona)

32

Data collection procedure (2)

2. Collect info on focal variables for 450 observations

(37 * 5)+(53 * 5):

(i) NB shelf presence

Source: GfK panel data (for Aldi) and Kantar Worldpanel data (for Mercadona)

33

Data collection procedure (2)

Source for Mercadona: Kantar Worldpanel data

2. (ii) Private-label production

Sources for Aldi: - address matching (Bell & Zabriskie 1978) - books (Bertram 2006; Schaab & Eschenbek 2008; Schneider 2005, 2006) - websites (e.g. www.ciao.de,.... )- store visits

33

34

Data collection procedure (3)3. Then, combine both:

National brand present?

Private-label Production? Yes No Total

Yes 52 40 92

No 133 225 358

Total 185 265 450

52PL production & NB presence combinations!

)01.(34.11)1(2 p

35

Data collection procedure (4)

4. Collect data on other variables …

Manufacturer sales growth (H4)

Source: GfK panel data (for Aldi) and Kantar Worldpanel data (for Mercadona)

36

Data collection procedure (4)

4. Collect data on other variables …

Ease of producing high-quality products (H5)

Source: consumer survey data (Steenkamp et al., 2010)

37

Data collection procedure (4)

4. Collect data on other variables …

Manufacturer marketing tools

Innovativeness of manufacturer (H6)

Extent of advertising support of manufacturer (H7)

Price premium manufacturer charges (H8)

Source: Product Launch Analytics (formerly Productscan)

Source: Thomson Media Control (for Aldi) and InfoAdex S.A. (for Mercadona)

Source: GfK panel data (for Aldi) and Kantar Worldpanel data (for Mercadona)

38

Data collection procedure (4)

4. Collect data on other variables …

Manufacturer market power

Source: GfK panel data (for Aldi) and Kantar Worldpanel data (for Mercadona)

39

+H2 +/-

H9

-H4

+H1

+H5

-H6, H7, H8

Ease of Producing High-Quality Products

Manufacturer Marketing Tools: - Innovations - Advertising - Price Premium over PLs

PL Production

Manufacturer Market Power

Manufacturer Sales Growth

Shelf Presence

+/- H3

Conceptual Framework

40

Method

Bivariate probit selection model (Heckman 1979)

Two discounters: prior pooling tests

41

Method

Bivariate probit selection model (Heckman 1979)

Two discounters: prior pooling tests

Pooling allowed, three exceptions

Manufacturer power in outcome equation

Role of price premium and innovation in selection equation

Outcome equation:

Strategy-selection equation:

42

Method (2)

PRESENCEijd = β0 + '0 D_MERCd + β1 PLPRODijd

+ β2 (M_POWERijd * D_ALDId) + '2 (M_POWERijd * D_MERCd)

+ β3 (PLPRODijd * M_POWERijd * D_ALDId) + '3 (PLPRODijd * M_POWERijd * D_MERCd)

+ γ1 VALGAPjd + γ2 DISC_SHAREjd + εijd

PLPRODijd = δ0 + '0 D_MERCd + δ1 GROWTHijd + δ2 EASEjd + δ3 ADVijd

+ δ4 (PPREMijd * D_ALDId) + '4 (PPREMijd * D_MERCd)

+ δ5 (INNOVijd * D_ALDId) + '5 (INNOVijd * D_MERCd)

+ δ6 M_POWERijd + η1 VALGAPjd + η2 DISC_SHAREjd + 'ijd

Cd )

Bivariate probit

][ 'ijdijdcorr

43

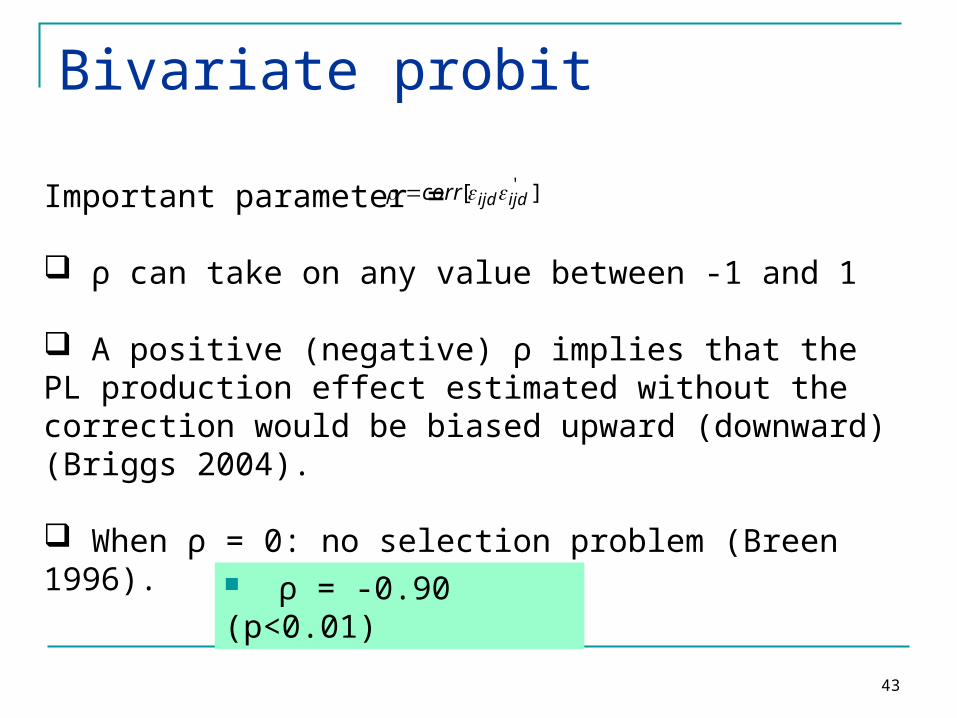

Important parameter =

ρ can take on any value between -1 and 1

A positive (negative) ρ implies that the PL production effect estimated without the correction would be biased upward (downward) (Briggs 2004).

When ρ = 0: no selection problem (Breen 1996).

ρ = -0.90 (p<0.01)

Results

Variable Coefficient (t-value)Outcome Equation (Shelf Presence)

Intercept (β0) -1.46 ††† (-11.46)

PL production (β1) 2.21 *** (11.56)

Manufacturer market power Aldi (β2) -.10 (-1.31)

Manufacturer market power Mercadona (β’2) .48 *** (6.72)

PL production * Manufacturer market power Aldi (β3) .06 (.35)

PL production * Manufacturer market power Mercadona (β’3) -.62 † (-1.67)

Control variables

Value gap (γ1) .03 (.12)

Discounter category share (γ2) .03 (.15)

Discounter dummy (0 = Aldi, 1 = Mercadona) (β’0) 1.35 ††† (8.99)

44

PRESENCEijd = β0 + '0 D_MERCd + β1 PLPRODijd

+ β2 (M_POWERijd * D_ALDId) + '2 (M_POWERijd * D_MERCd)

+ β3 (PLPRODijd * M_POWERijd * D_ALDId) + '3 (PLPRODijd * M_POWERijd *

D_MERCd) + γ1 VALGAPjd + γ2 DISC_SHAREjd + εijd

Results

45

PRESENCEijd = β0 + '0 D_MERCd + β1 PLPRODijd

+ β2 (M_POWERijd * D_ALDId) + '2 (M_POWERijd * D_MERCd)

+ β3 (PLPRODijd * M_POWERijd * D_ALDId) + '3 (PLPRODijd * M_POWERijd *

D_MERCd) + γ1 VALGAPjd + γ2 DISC_SHAREjd + εijd

Variable Coefficient (t-value)Outcome Equation (Shelf Presence)

Intercept (β0) -1.46 ††† (-11.46)

PL production (β1) 2.21 *** (11.56)

Manufacturer market power Aldi (β2) -.10 (-1.31)

Manufacturer market power Mercadona (β’2) .48 *** (6.72)

PL production * Manufacturer market power Aldi (β3) .06 (.35)

PL production * Manufacturer market power Mercadona (β’3) -.62 † (-1.67)

Control variables

Value gap (γ1) .03 (.12)

Discounter category share (γ2) .03 (.15)

Discounter dummy (0 = Aldi, 1 = Mercadona) (β’0) 1.35 ††† (8.99)

Results

46

PRESENCEijd = β0 + '0 D_MERCd + β1 PLPRODijd

+ β2 (M_POWERijd * D_ALDId) + '2 (M_POWERijd * D_MERCd)

+ β3 (PLPRODijd * M_POWERijd * D_ALDId) + '3 (PLPRODijd * M_POWERijd *

D_MERCd) + γ1 VALGAPjd + γ2 DISC_SHAREjd + εijd

Variable Coefficient (t-value)Outcome Equation (Shelf Presence)

Intercept (β0) -1.46 ††† (-11.46)

PL production (β1) 2.21 *** (11.56)

Manufacturer market power Aldi (β2) -.10 (-1.31)

Manufacturer market power Mercadona (β’2) .48 *** (6.72)

PL production * Manufacturer market power Aldi (β3) .06 (.35)

PL production * Manufacturer market power Mercadona (β’3) -.62 † (-1.67)

Control variables

Value gap (γ1) .03 (.12)

Discounter category share (γ2) .03 (.15)

Discounter dummy (0 = Aldi, 1 = Mercadona) (β’0) 1.35 ††† (8.99)

Results

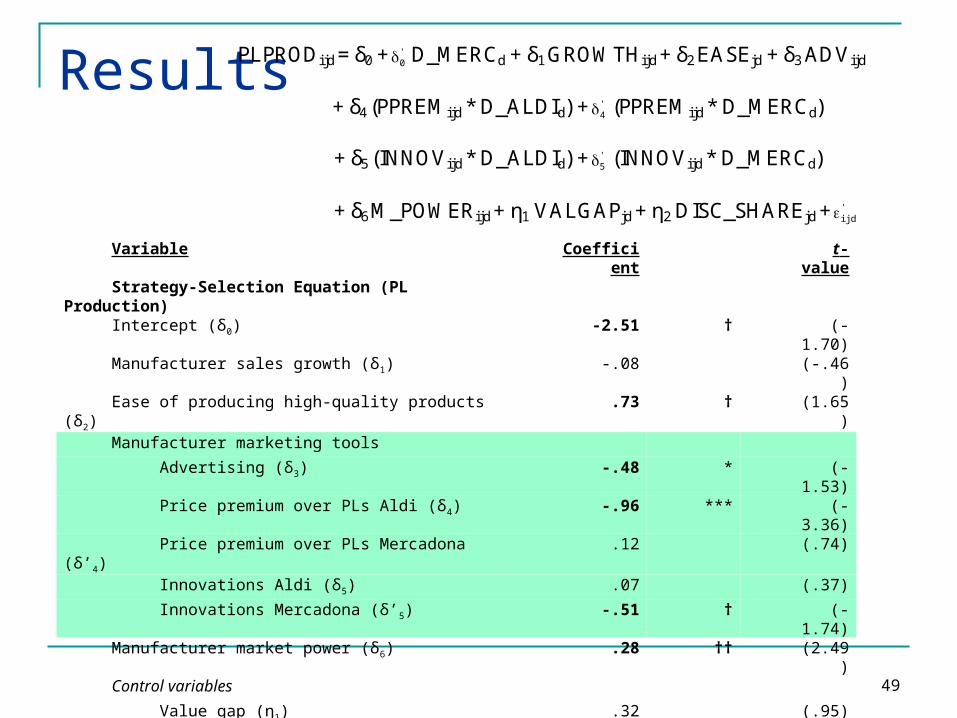

Variable Coefficient t-value

Strategy-Selection Equation (PL Production)

Intercept (δ0) -2.51 † (-1.70)

Manufacturer sales growth (δ1) -.08 (-.46)

Ease of producing high-quality products (δ2) .73 † (1.65)

Manufacturer marketing tools

Advertising (δ3) -.48 * (-1.53)

Price premium over PLs Aldi (δ4) -.96 *** (-3.36)

Price premium over PLs Mercadona (δ’4) .12 (.74)

Innovations Aldi (δ5) .07 (.37)

Innovations Mercadona (δ’5) -.51 † (-1.74)

Manufacturer market power (δ6) .28 †† (2.49)

Control variables

Value gap (η1) .32 (.95)

Discounter category share (η2) .60 †† (2.01)

Discounter dummy (0 = Aldi, 1 = Mercadona) (δ’0) -1.09 ††† (-5.15)

47

PLPRODijd = δ0 + '0 D_MERCd + δ1 GROWTHijd + δ2 EASEjd + δ3 ADVijd

+ δ4 (PPREMijd * D_ALDId) + '4 (PPREMijd * D_MERCd)

+ δ5 (INNOVijd * D_ALDId) + '5 (INNOVijd * D_MERCd)

+ δ6 M_POWERijd + η1 VALGAPjd + η2 DISC_SHAREjd + 'ijd

Results

48

Variable Coefficient t-value

Strategy-Selection Equation (PL Production)

Intercept (δ0) -2.51 † (-1.70)

Manufacturer sales growth (δ1) -.08 (-.46)

Ease of producing high-quality products (δ2) .73 † (1.65)

Manufacturer marketing tools

Advertising (δ3) -.48 * (-1.53)

Price premium over PLs Aldi (δ4) -.96 *** (-3.36)

Price premium over PLs Mercadona (δ’4) .12 (.74)

Innovations Aldi (δ5) .07 (.37)

Innovations Mercadona (δ’5) -.51 † (-1.74)

Manufacturer market power (δ6) .28 †† (2.49)

Control variables

Value gap (η1) .32 (.95)

Discounter category share (η2) .60 †† (2.01)

Discounter dummy (0 = Aldi, 1 = Mercadona) (δ’0) -1.09 ††† (-5.15)

PLPRODijd = δ0 + '0 D_MERCd + δ1 GROWTHijd + δ2 EASEjd + δ3 ADVijd

+ δ4 (PPREMijd * D_ALDId) + '4 (PPREMijd * D_MERCd)

+ δ5 (INNOVijd * D_ALDId) + '5 (INNOVijd * D_MERCd)

+ δ6 M_POWERijd + η1 VALGAPjd + η2 DISC_SHAREjd + 'ijd

Results

49

Variable Coefficient t-value

Strategy-Selection Equation (PL Production)

Intercept (δ0) -2.51 † (-1.70)

Manufacturer sales growth (δ1) -.08 (-.46)

Ease of producing high-quality products (δ2) .73 † (1.65)

Manufacturer marketing tools

Advertising (δ3) -.48 * (-1.53)

Price premium over PLs Aldi (δ4) -.96 *** (-3.36)

Price premium over PLs Mercadona (δ’4) .12 (.74)

Innovations Aldi (δ5) .07 (.37)

Innovations Mercadona (δ’5) -.51 † (-1.74)

Manufacturer market power (δ6) .28 †† (2.49)

Control variables

Value gap (η1) .32 (.95)

Discounter category share (η2) .60 †† (2.01)

Discounter dummy (0 = Aldi, 1 = Mercadona) (δ’0) -1.09 ††† (-5.15)

PLPRODijd = δ0 + '0 D_MERCd + δ1 GROWTHijd + δ2 EASEjd + δ3 ADVijd

+ δ4 (PPREMijd * D_ALDId) + '4 (PPREMijd * D_MERCd)

+ δ5 (INNOVijd * D_ALDId) + '5 (INNOVijd * D_MERCd)

+ δ6 M_POWERijd + η1 VALGAPjd + η2 DISC_SHAREjd + 'ijd

Results

50

Variable Coefficient t-value

Strategy-Selection Equation (PL Production)

Intercept (δ0) -2.51 † (-1.70)

Manufacturer sales growth (δ1) -.08 (-.46)

Ease of producing high-quality products (δ2) .73 † (1.65)

Manufacturer marketing tools

Advertising (δ3) -.48 * (-1.53)

Price premium over PLs Aldi (δ4) -.96 *** (-3.36)

Price premium over PLs Mercadona (δ’4) .12 (.74)

Innovations Aldi (δ5) .07 (.37)

Innovations Mercadona (δ’5) -.51 † (-1.74)

Manufacturer market power (δ6) .28 †† (2.49)

Control variables

Value gap (η1) .32 (.95)

Discounter category share (η2) .60 †† (2.01)

Discounter dummy (0 = Aldi, 1 = Mercadona) (δ’0) -1.09 ††† (-5.15)

PLPRODijd = δ0 + '0 D_MERCd + δ1 GROWTHijd + δ2 EASEjd + δ3 ADVijd

+ δ4 (PPREMijd * D_ALDId) + '4 (PPREMijd * D_MERCd)

+ δ5 (INNOVijd * D_ALDId) + '5 (INNOVijd * D_MERCd)

+ δ6 M_POWERijd + η1 VALGAPjd + η2 DISC_SHAREjd + 'ijd

51

Robustness check: Timing Issue

PL Production NB presence

Therefore, > for all 52 PL production & NB presence

combinations!

For 30 Aldi observations:

Personal communication to determine temporal ordering

2 cases disconfirmed deleted from sample stable results

)( producept )(listinglt

lt pt

51

52

Conclusion

Benefits for the NB manufacturer?

Evidence of discounter goodwill creation!

SLEEPING WITH THE ENEMY: PRIVATE-LABEL PRODUCTION BY NATIONAL-BRAND MANUFACTURERS

PREVIOUS SETTING

DISCOUNTER SETTING

GOODWILL MEASURE: SHELF PRESENCE

HOW ABOUT

CONVENTIONAL SUPERMARKETS

OTHER GOODWILL METRIC: MARGIN

Prior research on PL margins(Ailawadi & Harlam 2004; Kumar & Steenkamp 2007)

Insight 1: PL margins for the retailer are high

PL suppliers face unfavorable channel relationships Lack of product differentiation

Insight 2: PL margins vary across categories

55

How about within category differences?

1. Multiple PL tiers

2. Heterogeneity in supplier-retailer relationships

3. Different supplier types

56

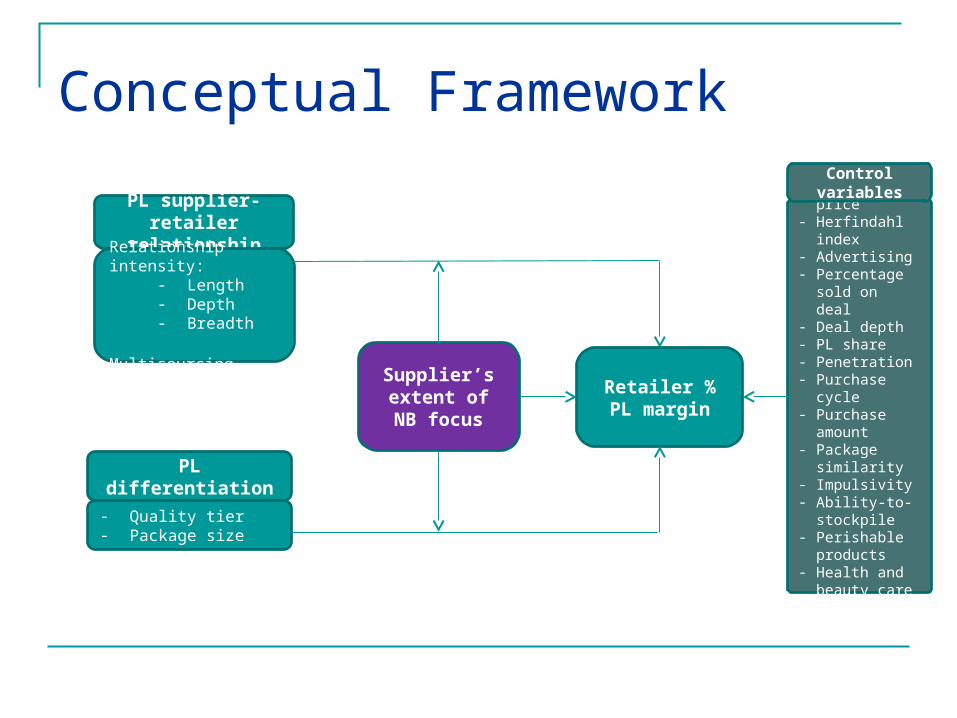

Conceptual Framework

PL differentiation

PL supplier-retailer relationship

Retailer % PL margin

- Retail price- Herfindahl

index- Advertising- Percentage

sold on deal- Deal depth- PL share- Penetration- Purchase cycle- Purchase

amount- Package

similarity- Impulsivity- Ability-to-

stockpile- Perishable

products- Health and

beauty care- Food

Supplier’s extent of NB

focus

- Quality tier- Package size

Relationship intensity:- Length- Depth- Breadth

Multisourcing

Control variables

Supplier NB focus More NB oriented PL suppliers :

Offer more PL quality assurance (Sethuraman 2009) Have more innovative capacity (Kumar & Steenkamp 2007) Have more contact points across the retailer’s business

(IGD 2006) Are valuable for a retailer in terms of their NBs (Dhar &

Hoch 1996)

H5: The more NB oriented a PL supplier is, the lower a retailer’s PL margins

58

Some summary statistics

Average PL margin = 36.6% 38.4% premium 37.5% standard 17.9% economy

189 PL suppliers 562 PL skus are produced by dedicated PL

suppliers 983 PL skus are produced by dual branders

1 – 16 suppliers within a category

59

p <.01

p =.68

Distribution of NB focus

Some empirical results

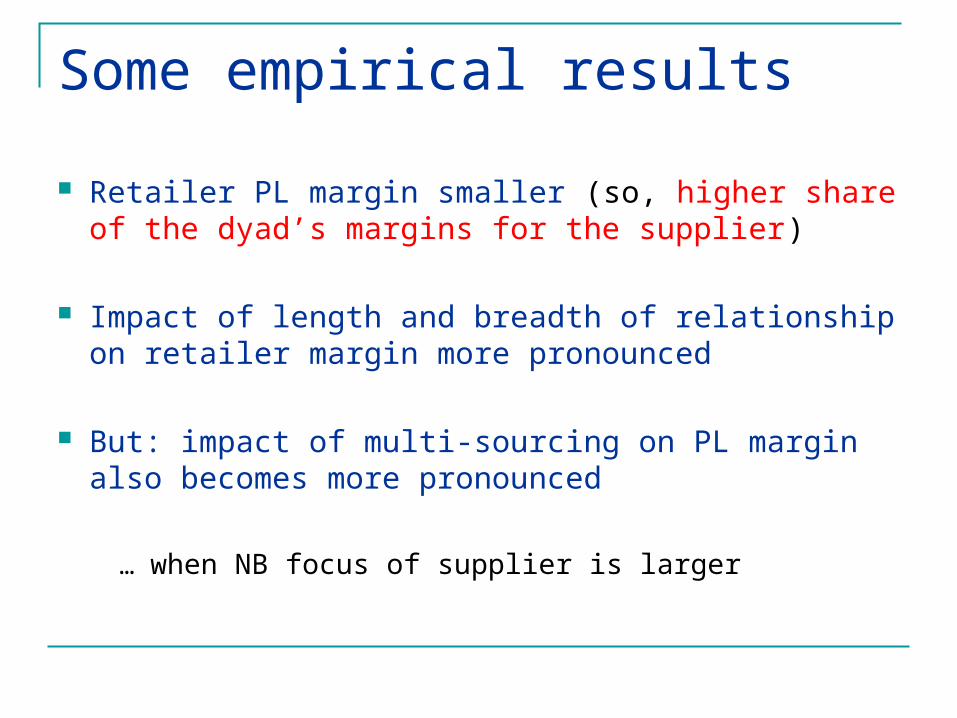

Retailer PL margin smaller (so, higher share of the dyad’s margins for the supplier)

Impact of length and breadth of relationship on retailer margin more pronounced

But: impact of multi-sourcing on PL margin also becomes more pronounced

… when NB focus of supplier is larger

TO CONCLUDE:

PL production pays off;

With discounters: easier shelf access.

With supermarkets: higher share of the dyad’s margin + relationship quality rewarded more.

BUT:

HOW ABOUT CROSS-CATEGORY IMPLICATIONS?

HOW ABOUT CROSS-RETAILER IMPLICATIONS?

64