Embed Size (px)

Citation preview

11

Accounting TheoryAccounting Theory

Topic 1: Accounting HistoryTopic 1: Accounting History

22

Accounting HistoryAccounting History

Early history of accountingEarly history of accounting

Emergence of double entry Emergence of double entry bookkeepingbookkeeping

Contribution of Luca PacioliContribution of Luca Pacioli

33

Accounting HistoryAccounting History

The history of accounting is as old as The history of accounting is as old as civilization, key to important phases civilization, key to important phases of history, among the most important of history, among the most important professions in economics and professions in economics and business. business.

44

Accounting HistoryAccounting History

A.C. Littleton in his “Accounting Evolution A.C. Littleton in his “Accounting Evolution to 1900” contended that for double entry to 1900” contended that for double entry system to emerge , certain prerequisites system to emerge , certain prerequisites or antecedents had to be present. He or antecedents had to be present. He classified his antecedents into two:classified his antecedents into two:

1)1) Materials antecedents : private property, Materials antecedents : private property, capital, commerce and credit.capital, commerce and credit.

2)2) Language antecedents : writing, money Language antecedents : writing, money and arithmetic.and arithmetic.

55

Accounting HistoryAccounting History

Littleton claimed that these Littleton claimed that these antecedents , although present, did antecedents , although present, did not posses the proper intensity in the not posses the proper intensity in the ancient civilization to cause double ancient civilization to cause double entry system to emerge. The ancient entry system to emerge. The ancient civilizations referred to are; Egypt, civilizations referred to are; Egypt, Babylonia, Greece and Rome. Babylonia, Greece and Rome.

66

Alternate Explanation of Vernon Alternate Explanation of Vernon KamKam

Littleton's antecedents need to be Littleton's antecedents need to be explained further to have a fuller explained further to have a fuller understanding of the evolution of understanding of the evolution of accounting from ancient time. He accounting from ancient time. He identified three factors that create identified three factors that create and promote the growth of business and promote the growth of business entities:entities:

77

Three factorsThree factors1)1) Capitalistic spiritCapitalistic spirit2)2) Economic and political eventsEconomic and political events3)3) Technological innovationsTechnological innovations

These three factors (termed as These three factors (termed as social forces) are the reasons for social forces) are the reasons for the development of the business the development of the business organization which in turn result organization which in turn result the development of double entry the development of double entry system. system.

88

Capitalistic spiritCapitalistic spirit

Capitalistic spirit is the motivating Capitalistic spirit is the motivating force that drives people to form force that drives people to form business entity for the sake of business entity for the sake of making a profit. Of course making a profit. Of course accounting is used by both profit accounting is used by both profit and non profit organizations. The and non profit organizations. The term Capitalistic spirit is used term Capitalistic spirit is used because historically it has been because historically it has been under Capitalism that accounting under Capitalism that accounting has flourished.has flourished.

99

Capitalistic spiritCapitalistic spiritin the ancient civilizationin the ancient civilization

A class of merchants existed in all A class of merchants existed in all the ancient. Evidence support that the ancient. Evidence support that the desire for profit was present in the desire for profit was present in ancient civilizations. ancient civilizations.

But Littleton's view was that desire But Littleton's view was that desire for profit did not existed in the for profit did not existed in the ancient time. ancient time.

1010

Economic and political eventsEconomic and political eventsCommerce: an important variable to form Commerce: an important variable to form and grow business entities. Interpretation and grow business entities. Interpretation of the extent of commerce in the ancient of the extent of commerce in the ancient times is a matter of disagreement by the times is a matter of disagreement by the historians. there may have been a great historians. there may have been a great deal of trade but a complex market deal of trade but a complex market system did not existed. There was no need system did not existed. There was no need for sophisticated book keeping tool vis. a for sophisticated book keeping tool vis. a vis. double entry system. vis. double entry system.

1111

Economic and political eventsEconomic and political eventsComplex market: a complex market Complex market: a complex market consisted aa variety of separate but consisted aa variety of separate but interrelated activities. interrelated activities.

First: there is market for consumer and First: there is market for consumer and producer goods.producer goods.

Then there are markets for factors of Then there are markets for factors of productionproduction

In each of these market the forces of In each of these market the forces of demand and supply should be considered. demand and supply should be considered.

1212

Economic and political eventsEconomic and political eventsThe necessity for efficient accounting method The necessity for efficient accounting method depend on whether the supply side is depend on whether the supply side is complicated. complicated. Land was owned for the most part by govt and Land was owned for the most part by govt and wealthy people. If they were engaged in business wealthy people. If they were engaged in business activities they posed no problemactivities they posed no problemLabor was furnished by the family members and Labor was furnished by the family members and slaves, therefore keeping record of labor cost was slaves, therefore keeping record of labor cost was not a significant matter.not a significant matter.There was no capital market. Borrowing funds by There was no capital market. Borrowing funds by merchants was normally a direct transactions merchants was normally a direct transactions with specific individuals. with specific individuals.

1313

Economic and political eventsEconomic and political events

So keeping track of costs and profit So keeping track of costs and profit for the purpose of accountability to for the purpose of accountability to outside parties was not critical. Most outside parties was not critical. Most part of the business was extension of part of the business was extension of the household.the household.

1414

Technological innovationsTechnological innovationsLaggard technology: ancients resisted the Laggard technology: ancients resisted the technology. There were lack of incentive to technology. There were lack of incentive to develop the technology, because of cheap labor, develop the technology, because of cheap labor, cultural attitudes. cultural attitudes. Writing and arithmetic: Littleton mentioned Writing and arithmetic: Littleton mentioned writing, arithmetic and money as the language writing, arithmetic and money as the language antecedents of the double entry book keeping. antecedents of the double entry book keeping. Writing is verified to be existed in ancient Writing is verified to be existed in ancient civilization. With respect to arithmetic Egyptians civilization. With respect to arithmetic Egyptians used a system of counting. Babylonians were used a system of counting. Babylonians were skilled in arithmetic and astronomy. Littleton skilled in arithmetic and astronomy. Littleton concluded that arithmetic in the ancient time was concluded that arithmetic in the ancient time was difficult to employ. It depends on ability training difficult to employ. It depends on ability training and experience. and experience.

1515

Technological innovationsTechnological innovations

Money: the employment of money as Money: the employment of money as a medium of exchange in the metal a medium of exchange in the metal form of gold and silver was known to form of gold and silver was known to Egypt and Babylonia. Despite the Egypt and Babylonia. Despite the fact that money was utilized medium fact that money was utilized medium of exchange , but markets remain of exchange , but markets remain simple because of uncomplicated simple because of uncomplicated nature of demand and supply nature of demand and supply functions. functions.

1616

Emergence of double entry book Emergence of double entry book keepingkeeping

The first record of double entry The first record of double entry system is the Massari (treasurers) system is the Massari (treasurers) accounts in the city of Genoa in accounts in the city of Genoa in 1340. it is probable that double entry 1340. it is probable that double entry system made it appearance in the system made it appearance in the mid thirteenth century. why double mid thirteenth century. why double entry system emerged in this time? entry system emerged in this time? The reasons are two fold: The reasons are two fold:

1717

Emergence of double entry book Emergence of double entry book keepingkeeping

Firstly : it was the natural outcome of Firstly : it was the natural outcome of the evolutionary process in response the evolutionary process in response to the need of the time. As Littleton to the need of the time. As Littleton spoke of the evolution of the spoke of the evolution of the accounting. the notion implies that accounting. the notion implies that what took place in the preceding what took place in the preceding culture is believed to have some culture is believed to have some effect on the subsequent culture. Or effect on the subsequent culture. Or civilization. civilization.

1818

Emergence of double entry book Emergence of double entry book keepingkeeping

Second: a second reason for the Second: a second reason for the appearance of the double entry system appearance of the double entry system at this time is that the particular setting at this time is that the particular setting in the Italian city state called it forth. in the Italian city state called it forth. Thee setting is discussed in terms of Thee setting is discussed in terms of three major forces: three major forces:

a)a) Capitalistic spiritCapitalistic spirit

b)b) Economic and political eventEconomic and political event

c)c) Technological innovationTechnological innovation

1919

Emergence of double entry book Emergence of double entry book keepingkeeping

Capitalistic spirit:in the middle ages , Capitalistic spirit:in the middle ages , conduct was governed by the religious conduct was governed by the religious belief. Making a profit was almost belief. Making a profit was almost immoral. After the thirteen century, immoral. After the thirteen century, position of the business improved greatly. position of the business improved greatly. The Italian city state realized this very The Italian city state realized this very early recognizing the legitimacy of making early recognizing the legitimacy of making a profit as a means to support a family, or a profit as a means to support a family, or to have enough to give the poor or as to have enough to give the poor or as reward for public service , Italian Church reward for public service , Italian Church did not regard economic goals and did not regard economic goals and spiritual motives as necessarily conflicting.spiritual motives as necessarily conflicting.

2020

Economic and political eventEconomic and political event

1)1) Demand: By the end of the thirteen Demand: By the end of the thirteen century the complexity of the century the complexity of the market become evident. On the market become evident. On the demand side the more customer demand side the more customer goods were desired.goods were desired.

2)2) Supply: on the supply side ,labor Supply: on the supply side ,labor market had improved, banking market had improved, banking business flourished, business flourished,

2121

Economic and political eventEconomic and political event

3) Politics: power and politics in Italy 3) Politics: power and politics in Italy was also contributing factor. By the was also contributing factor. By the thirteenth century Italian cities was thirteenth century Italian cities was controlled by those who favored controlled by those who favored business interest. Therefore, business interest. Therefore, commerce and insdustry flourished. commerce and insdustry flourished.

2222

Technological innovationTechnological innovation

In contrast to the Greek and Roman In contrast to the Greek and Roman period, the middle ages saw a great period, the middle ages saw a great interest in the Technological interest in the Technological innovation. The particular innovation innovation. The particular innovation that stimulated the development of that stimulated the development of book keeping were paper making, book keeping were paper making, printing etc. printing etc.

2323

Contribution of Luca PacioliContribution of Luca Pacioli

Luca Pacioli’s bok in 1494 was the Luca Pacioli’s bok in 1494 was the first book on the double entry system first book on the double entry system . However the first person to write . However the first person to write on double entry system was probably on double entry system was probably Benedetto Cotrugli whose book was Benedetto Cotrugli whose book was completed in 1458 but published in completed in 1458 but published in 15731573

2424

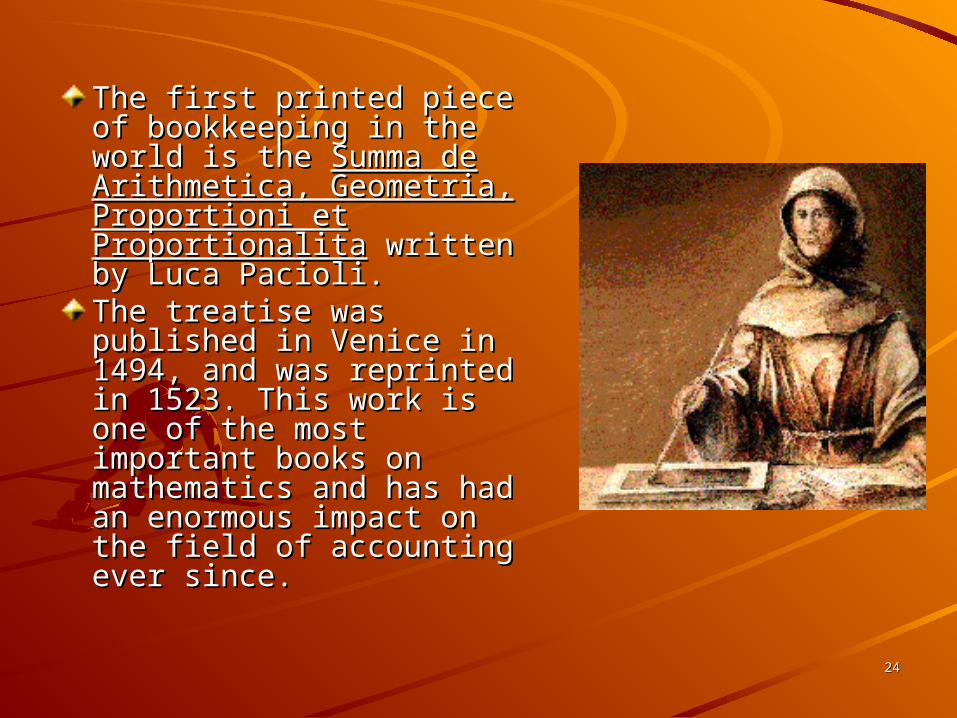

The first printed piece of The first printed piece of bookkeeping in the world bookkeeping in the world is the is the Summa de Summa de Arithmetica, Geometria, Arithmetica, Geometria, Proportioni et Proportioni et ProportionalitaProportionalita written by written by Luca Pacioli. Luca Pacioli. The treatise was published The treatise was published in Venice in 1494, and was in Venice in 1494, and was reprinted in 1523. This reprinted in 1523. This work is one of the most work is one of the most important books on important books on mathematics and has had mathematics and has had an enormous impact on an enormous impact on the field of accounting the field of accounting ever since. ever since.

2525

The first accounting book The first accounting book actually was one of five sections actually was one of five sections in Pacioli's mathematics book in Pacioli's mathematics book titled "Everything about titled "Everything about Arithmetic, Geometry, and Arithmetic, Geometry, and Proportions." This section on Proportions." This section on accounting served as the world's accounting served as the world's only accounting textbook until only accounting textbook until well into the 16th century.well into the 16th century.

2626

Contribution of Luca PacioliContribution of Luca Pacioli

The term we employ today debit and The term we employ today debit and credit were mentioned by Pacioli credit were mentioned by Pacioli debito(Owed to) and Credito(Owed debito(Owed to) and Credito(Owed by). In explaining the double entry by). In explaining the double entry system Pacioli said all entries have to system Pacioli said all entries have to be double entries ie if you make one be double entries ie if you make one creditors you must make some on a creditors you must make some on a debtor.debtor.

2727

Contribution of Luca PacioliContribution of Luca Pacioli

First activity a person must First activity a person must undertake when starting a undertake when starting a business ,V said, is to prepare an business ,V said, is to prepare an inventory. This inventory is to be inventory. This inventory is to be record in the journal at current record in the journal at current values. For sales price he values. For sales price he advised………….advised………….

2828

Contribution of Luca PacioliContribution of Luca Pacioli

Day book in his book each entry is Day book in his book each entry is stated in paragraph form. stated in paragraph form.

From the journal entries, entries are to From the journal entries, entries are to be posted ot the accounts of the be posted ot the accounts of the ledger.ledger.

But Pacioli made no mention of But Pacioli made no mention of accruing and deferring of revenue accruing and deferring of revenue and expenses. and expenses.

2929

Contribution of Luca PacioliContribution of Luca Pacioli

The determination of profit or loss The determination of profit or loss was different from eh procedure we was different from eh procedure we used today. Each venture was seen used today. Each venture was seen as a unit , when the venture closed, as a unit , when the venture closed, the account represent it was closed the account represent it was closed and profit and loss ascertained. and profit and loss ascertained. Example of the salt….Example of the salt….

3030

The bookkeeping method of Luca Pacioli has several distinct The bookkeeping method of Luca Pacioli has several distinct characteristics:characteristics:

1.1.Pacioli wrote that there are three things needed by one who wished Pacioli wrote that there are three things needed by one who wished to carry on business diligently. The most important of these is cash to carry on business diligently. The most important of these is cash or any other substantial power (altra faculta substantiale). The or any other substantial power (altra faculta substantiale). The second is a good accountant (buon ragioneri) and a sharp second is a good accountant (buon ragioneri) and a sharp bookkeeper. The third is good order in order to arrange all business bookkeeper. The third is good order in order to arrange all business to debit (debito) and credit (credito). to debit (debito) and credit (credito).

2.2.Pacioli explained the opening inventory (inventario), but he did not Pacioli explained the opening inventory (inventario), but he did not describe the closing inventory. describe the closing inventory.

3.3.Pacioli's account book system is three account books-that is, a day Pacioli's account book system is three account books-that is, a day book. The day book is the first book, the journal is the second book book. The day book is the first book, the journal is the second book and the ledger is the third book. Pacioli thought of the day book as and the ledger is the third book. Pacioli thought of the day book as the formal account book, because he wrote that the day book must the formal account book, because he wrote that the day book must be presented to a certain mercantile office (certo officio de be presented to a certain mercantile office (certo officio de mercatâti).mercatâti).

4.4.All things pertaining to a transaction must be written in the day book, All things pertaining to a transaction must be written in the day book, without omission. Pacioli wrote that no point must be omitted in the without omission. Pacioli wrote that no point must be omitted in the day book.day book.

5.5.Pacioli described debit and credit--that is, "per" and "A" in the Pacioli described debit and credit--that is, "per" and "A" in the journal, and "die dare" and "die havere" in the ledger. journal, and "die dare" and "die havere" in the ledger.