Embed Size (px)

Citation preview

1

Access:From Interconnection to

Convergence

Yale M. BraunsteinSchool of Information

University of CaliforniaBerkeley, CA 94720 (U.S.A.)

March 2008

2

Access has several dimensions

(Physical or geographic) proximity

Possession of needed skills

Economics

For free or fee-based

Connection to (the) network

3

History (U.S. Telephony) Competing networks

Bell & Edison in the U.S. Resolved by patent decisions

“The fundamental principle, formulated by AT&T president Theodore Vail in 1907, was that the telephone by the nature of its technology would operate most efficiently as a monopoly providing universal service.”

New technologies & business plans lead to bypass (MCI) and interconnection (role of SS7)

UNEs (unbundled network elements)

More new technologies (now digital)

4

Issues are inter-related As new entrants enter a telecommunications

market the problem of interconnection has two dimensions: technical and economic. My focus is on the latter.

Often there is the view that it is in the national interest to encourage the widespread diffusion of the telecom network and to promote access by users who might not be considered economically viable by operators.

Interconnection and universal service are often linked.

Presentation of some of the issues Optional “mini case studies”

5

Outline

Interconnection

Interconnection & universal service

Convergence (which has many meetings)

Competition (?)

6

The dimensions of interconnection

B.C. (before competition) it was common to see some or all of the following:• Local tariffs were averaged across

customers. In addition, the non-traffic-sensitive portion of the tariff was often kept artificially low.

• The tariffs for trunk calls were sufficiently higher than costs so as to enable the costs of local service to be kept low.

• International rates were many times the cost of service.

7

Typical interconnection pricing philosophies

Cost-based

Price-based

“Bill and keep”

Private negotiation

8

Additional concerns

Equal treatment and symmetry requirements Whose costs? Possible difference in technologies Legacy customers

Preferences for corporate relatives

9

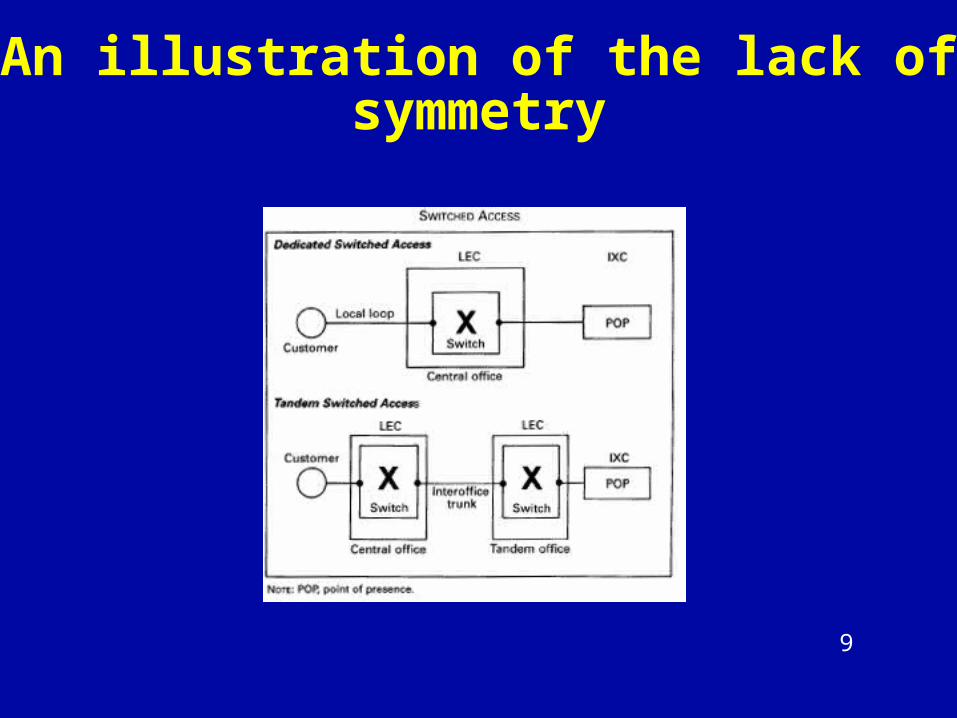

An illustration of the lack of symmetry

10

Universal service

Among the possible “definitions” are the following loosely-stated concepts: Basic residential telephone service should be

available to all regions of a country for a common, reasonable monthly fee.

Income and wealth levels should not be significant barriers.

Every village of a certain size should have at least one public telephone.

All local telephone providers should be able to interconnect to the national telephone network at reasonable rates.

11

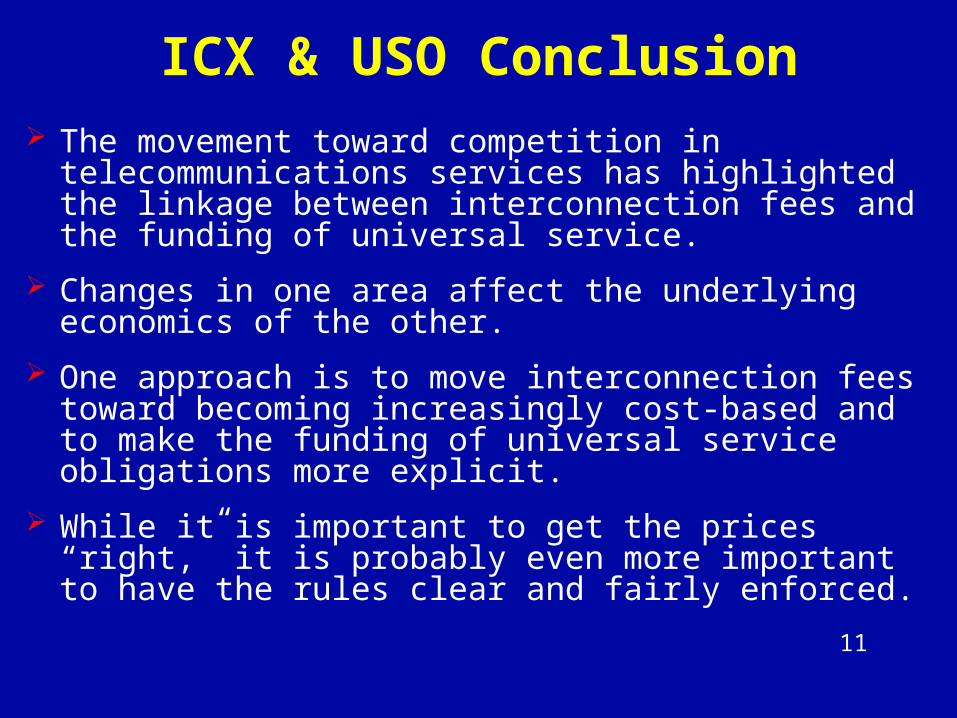

ICX & USO Conclusion The movement toward competition in

telecommunications services has highlighted the linkage between interconnection fees and the funding of universal service.

Changes in one area affect the underlying economics of the other.

One approach is to move interconnection fees toward becoming increasingly cost-based and to make the funding of universal service obligations more explicit.

While it is important to get the prices “right,” it is probably even more important to have the rules clear and fairly enforced.

12

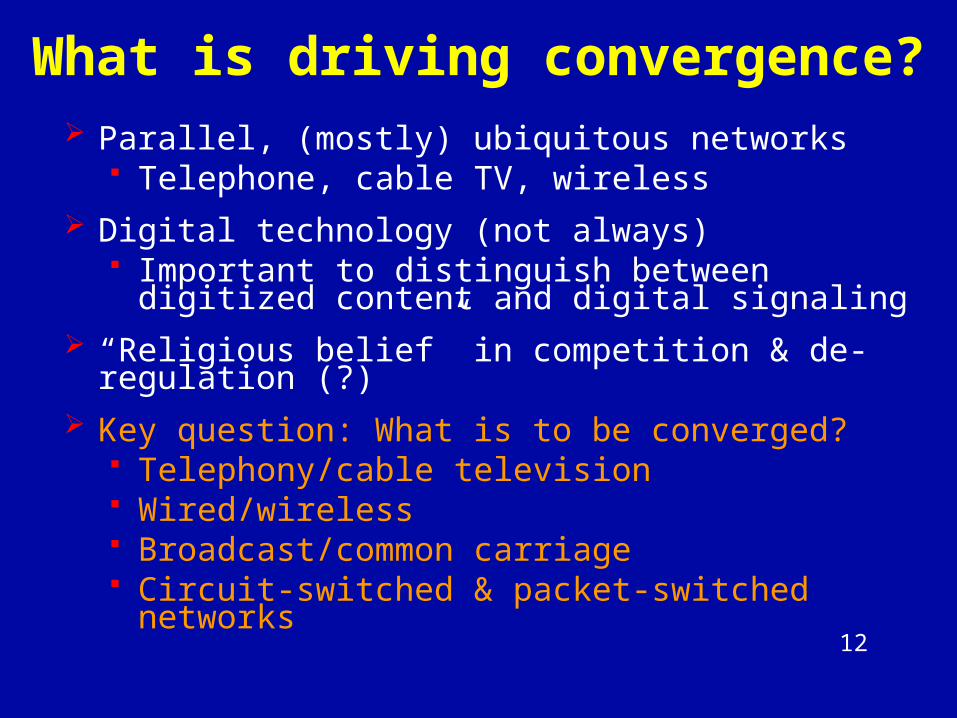

What is driving convergence? Parallel, (mostly) ubiquitous networks

Telephone, cable TV, wireless Digital technology (not always)

Important to distinguish between digitized content and digital signaling

“Religious belief” in competition & de-regulation (?)

Key question: What is to be converged? Telephony/cable television Wired/wireless Broadcast/common carriage Circuit-switched & packet-switched networks

13

Alternate regulatory approaches

Wait until competition, however defined, is well established

Get out of the way early (leaving things to the anti-monopoly authorities)

“Bright-line” tests of market share How is the market define?

Rely on case-by-case judgment of regulators

14

Case studies

15

Mobile-to-fixed, fixed-to-mobile, and mobile-to-mobile in

IsraelTable 1: Average Number of Monthly Usage Minutes, Israeli Mobile Operators

Operator 1995 1996 1997 1998 1999

Pelephone 530 430 320 300 295

Partner 427 (Q4)

Table 2: Current & Proposed Incoming Interconnection Rates, Israeli Mobile Operators

Proposed

Operator Current 2000 2001 2002 2003

Pelephone 0.17 0.13 0.12 0.11 0.10

Cellcom 0.12 “ “ “

Partner 0.13 “ “ “ “

Note: All rates are per-minute, given in U.S. dollars at US $ 1 = NIS 4.16

16

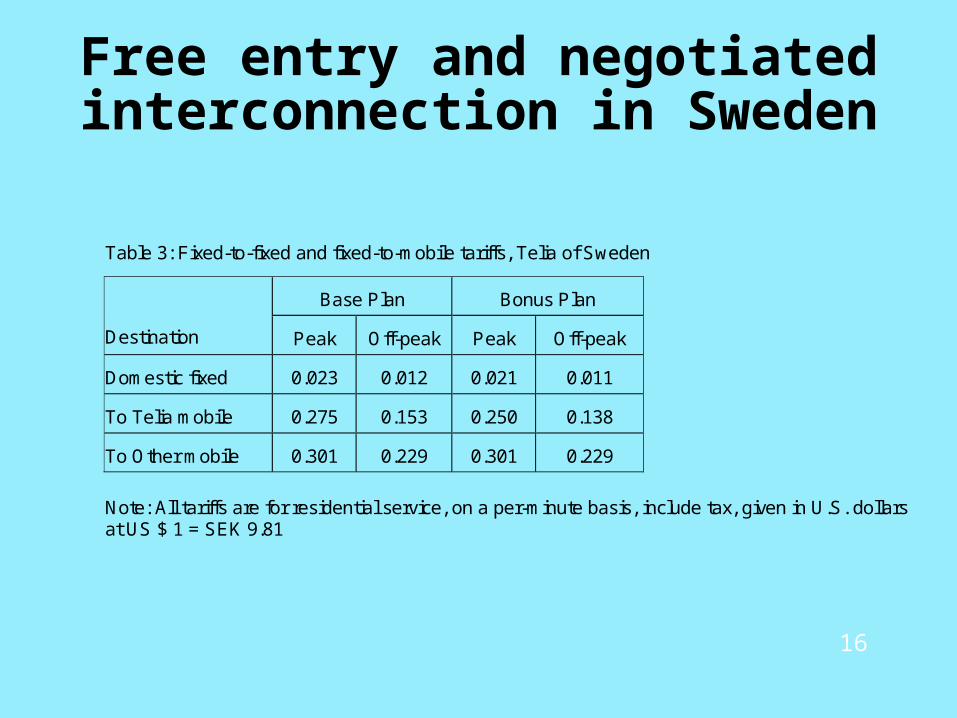

Free entry and negotiated interconnection in Sweden

Table 3: Fixed-to-fixed and fixed-to-mobile tariffs, Telia of Sweden

Base Plan Bonus Plan

Destination Peak Off-peak Peak Off-peak

Domestic fixed 0.023 0.012 0.021 0.011

To Telia mobile 0.275 0.153 0.250 0.138

To Other mobile 0.301 0.229 0.301 0.229

Note: All tariffs are for residential service, on a per-minute basis, include tax, given in U.S. dollars at US $ 1 = SEK 9.81

17

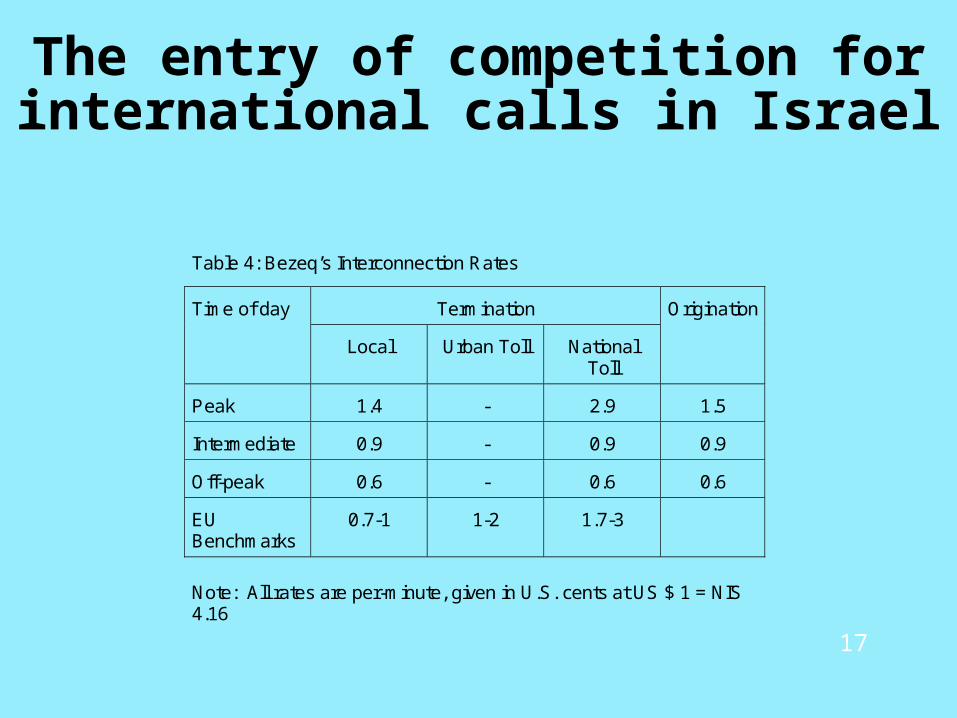

The entry of competition for international calls in Israel

Table 4: Bezeq’s Interconnection Rates

Termination Time of day

Local Urban Toll National Toll

Origination

Peak 1.4 - 2.9 1.5

Intermediate 0.9 - 0.9 0.9

Off-peak 0.6 - 0.6 0.6

EU Benchmarks

0.7-1 1-2 1.7-3

Note: All rates are per-minute, given in U.S. cents at US $ 1 = NIS 4.16

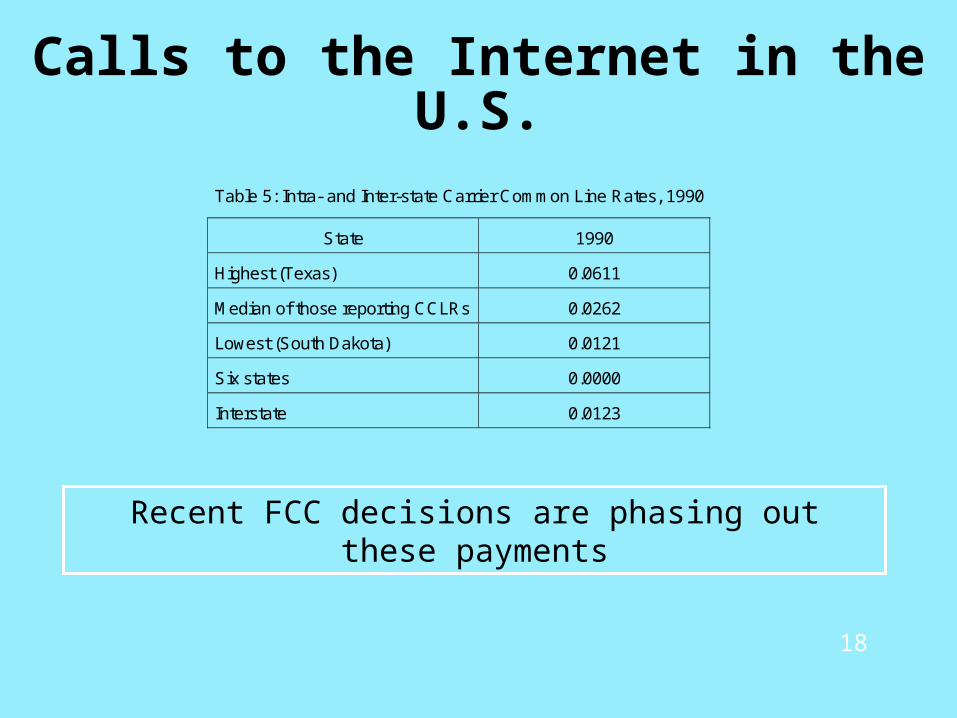

18

Calls to the Internet in the U.S.

Table 5: Intra- and Inter-state Carrier Common Line Rates, 1990

State 1990

Highest (Texas) 0.0611

Median of those reporting CCLRs 0.0262

Lowest (South Dakota) 0.0121

Six states 0.0000

Interstate 0.0123

Recent FCC decisions are phasing out these payments

19

Financing the USO and current tariffs in India

The Government is committed to provide access to all people for basic telecom services at affordable and reasonable prices. The Government seeks to achieve the following universal service objectives:

• Provide voice and low speed data service to the balance 2.9 lakh [290,000] uncovered villages in the country by the year 2002

• Achieve Internet access to all district head quarters by the year 2000

• Achieve telephone on demand in urban and rural areas by 2002

The resources for meeting the USO would be raised through a ‘universal access levy’ which would be a percentage of the revenue earned by all the operators under various licenses.

--New Telecom Policy of 1999

20

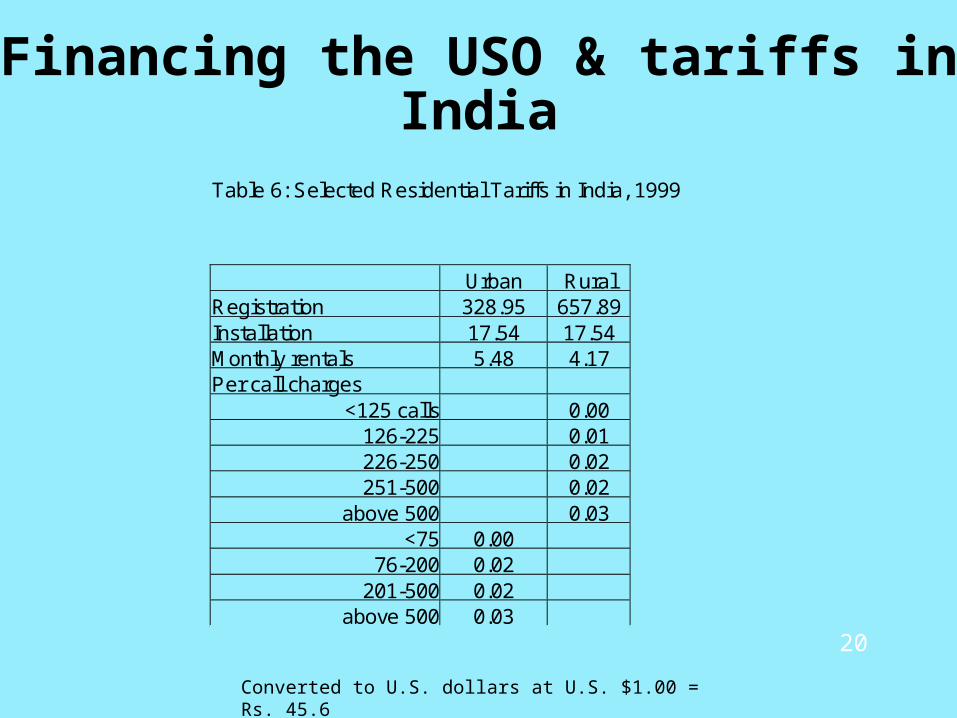

Financing the USO & tariffs in India

Table 6: Selected Residential Tariffs in India, 1999

Urban Rural Registration 328.95 657.89 Installation 17.54 17.54 Monthly rentals 5.48 4.17 Per call charges

<125 calls 0.00 126-225 0.01 226-250 0.02 251-500 0.02

above 500 0.03 <75 0.00

76-200 0.02 201-500 0.02

above 500 0.03

Converted to U.S. dollars at U.S. $1.00 = Rs. 45.6

21

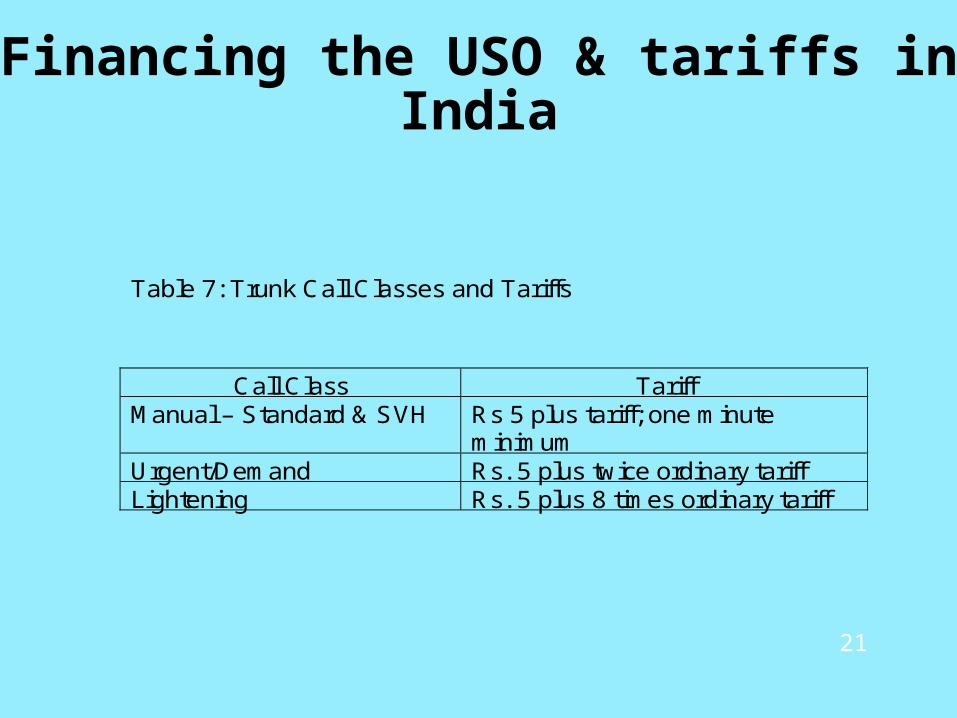

Financing the USO & tariffs in India

Table 7: Trunk Call Classes and Tariffs

Call Class Tariff Manual – Standard & SVH Rs 5 plus tariff; one minute

minimum Urgent/Demand Rs. 5 plus twice ordinary tariff Lightening Rs. 5 plus 8 times ordinary tariff

22

Interconnection Policy in EU States

Local Access Pricing and E-Commerce DSTI/ICCP/TISP(2000)1/FINAL July 2000

23

Conclusion The movement toward competition in

telecommunications services has highlighted the linkage between interconnection fees and the funding of universal service.

Changes in one area affect the underlying economics of the other.

One approach is to move interconnection fees toward becoming increasingly cost-based and to make the funding of universal service obligations more explicit.

While it is important to get the prices “right,” it is probably even more important to have the rules clear and fairly enforced.