Embed Size (px)

Citation preview

1

A Review of the Capital Requirements for Life Insurers in

India

By Jim Thompson , Raju S, By Jim Thompson , Raju S, Richard Holloway Richard Holloway

Presented at the 5th Global Conference of Presented at the 5th Global Conference of Actuaries - Delhi, February 2003Actuaries - Delhi, February 2003

2

Content

Background Background The current situation in IndiaThe current situation in India Developments in other marketsDevelopments in other markets Conclusions and recommendations for IndiaConclusions and recommendations for India

3

Why Capital/Solvency Margin?

To give the regulator and the policyholder To give the regulator and the policyholder the peace of mind that he will be paid what the peace of mind that he will be paid what he has been promisedhe has been promised

4

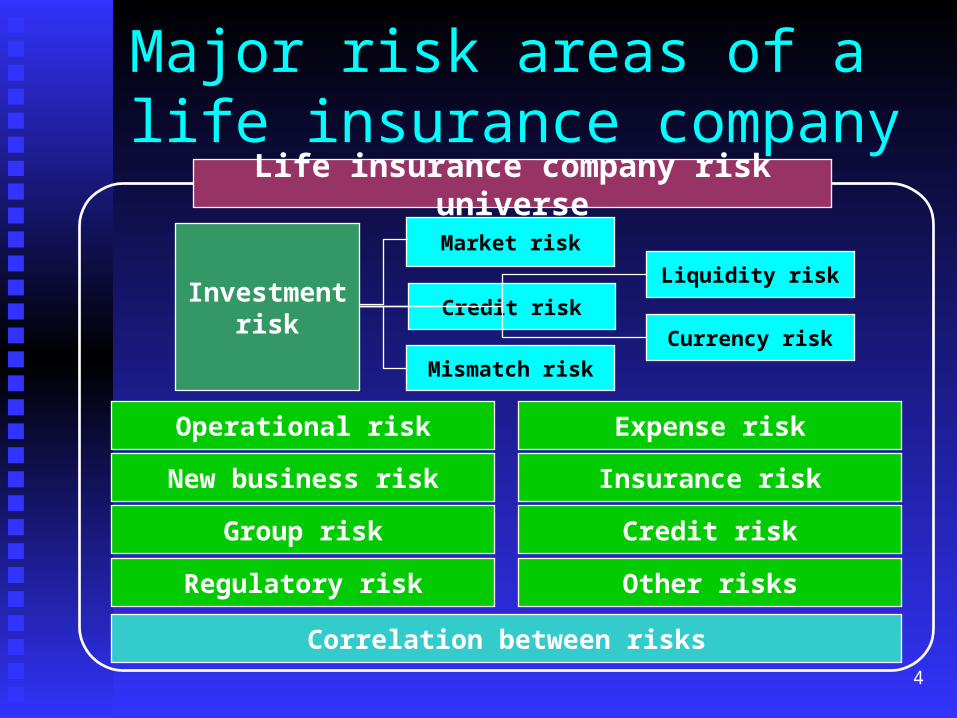

Major risk areas of a life insurance company

Investment risk

Market risk

Operational risk Expense risk

New business risk

Liquidity risk

Credit risk

Insurance risk

Mismatch risk

Currency risk

Correlation between risks

Group risk Credit risk

Life insurance company risk universe

Regulatory risk Other risks

5

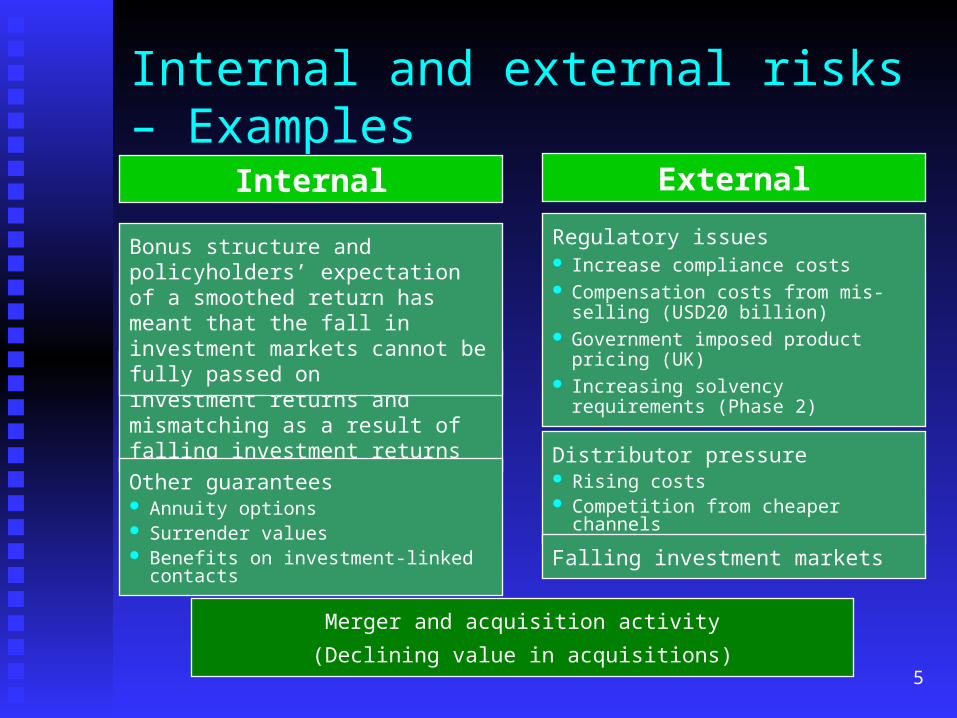

Internal and external risks – Examples

Internal External

High level of guaranteed investment returns and mismatching as a result of falling investment returns

Other guarantees Annuity options Surrender values Benefits on investment-linked contacts

Bonus structure and policyholders’ expectation of a smoothed return has meant that the fall in investment markets cannot be fully passed on

Regulatory issues Increase compliance costs Compensation costs from mis-selling

(USD20 billion) Government imposed product pricing (UK) Increasing solvency requirements (Phase 2)

Distributor pressure Rising costs Competition from cheaper channels

Merger and acquisition activity

(Declining value in acquisitions)

Falling investment markets

6

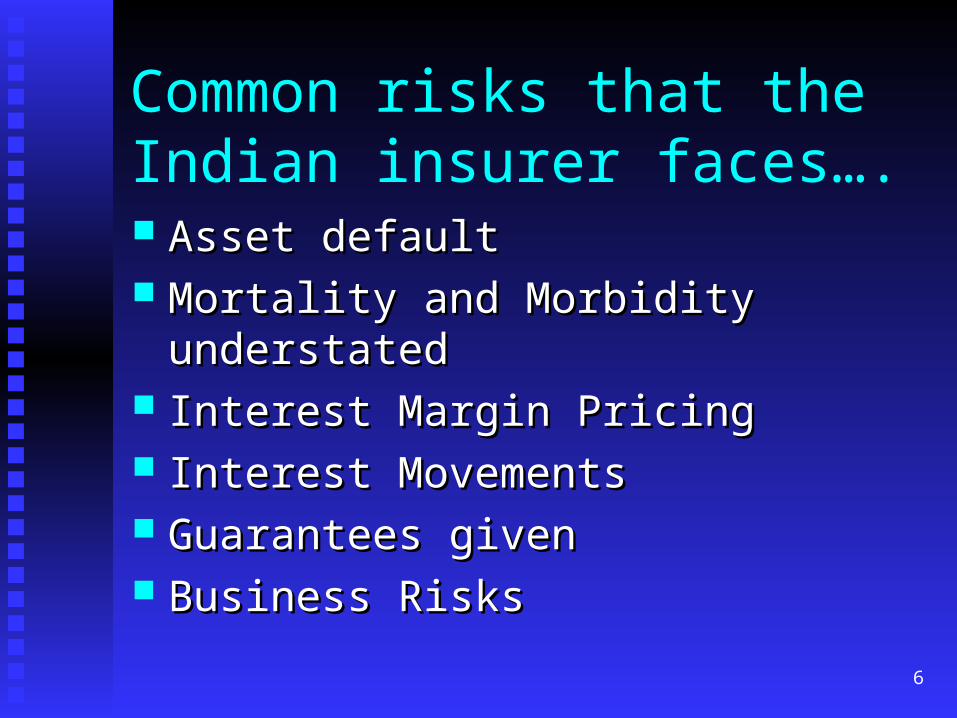

Common risks that the Indian insurer faces…. Asset defaultAsset default Mortality and Morbidity understatedMortality and Morbidity understated Interest Margin PricingInterest Margin Pricing Interest MovementsInterest Movements Guarantees givenGuarantees given Business RisksBusiness Risks

7

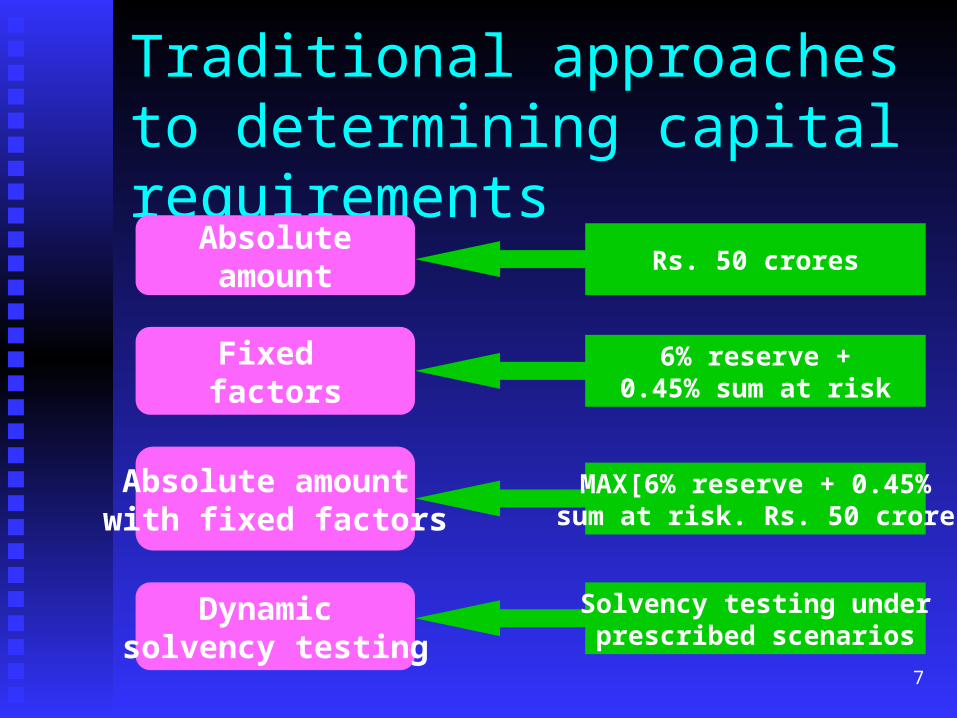

Traditional approaches to determining capital requirements

Fixed factors

Absolute amount with fixed factors

Dynamic solvency testing

Absoluteamount Rs. 50 crores

6% reserve +0.45% sum at risk

MAX[6% reserve + 0.45% sum at risk. Rs. 50 crore]

Solvency testing underprescribed scenarios

8

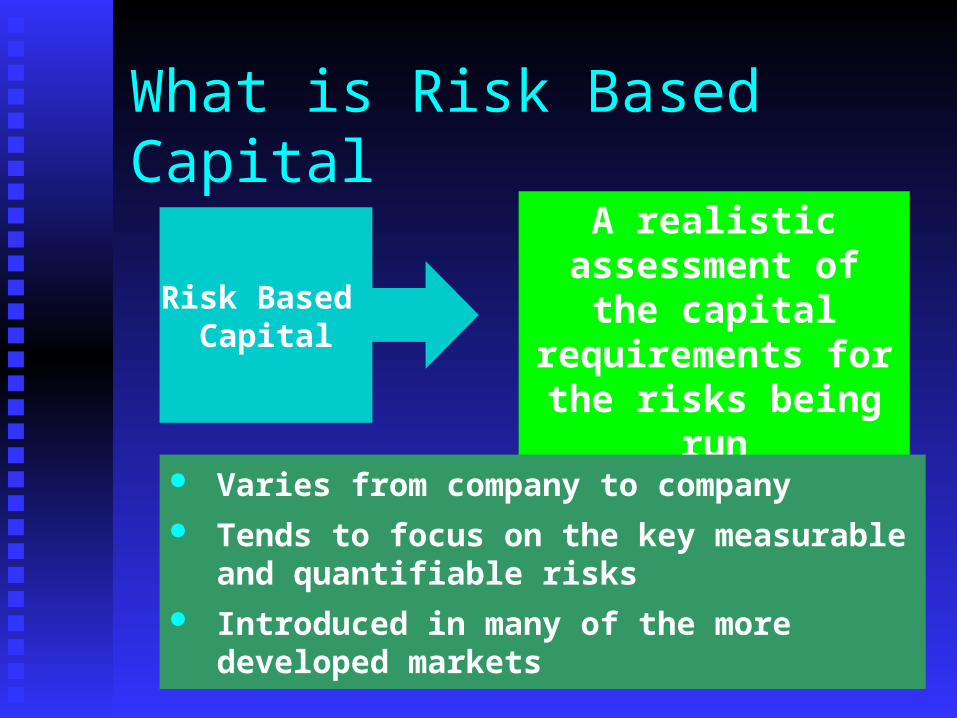

What is Risk Based Capital

A realistic assessment of the capital

requirements for the risks being run

Varies from company to company Tends to focus on the key measurable and

quantifiable risks Introduced in many of the more developed

markets

Risk Based Capital

9

Content

Background Background The current situation in IndiaThe current situation in India Developments in other marketsDevelopments in other markets Conclusions and recommendations for Conclusions and recommendations for

IndiaIndia

10

India – Overview ofsolvency requirements

Typical formula approachTypical formula approach Simplistic and easy to administerSimplistic and easy to administer Working solvency margin is 150% of the Working solvency margin is 150% of the

formulaformula Minimum solvency requirement of Rs 50 CrMinimum solvency requirement of Rs 50 Cr Solvency margin can be met by Surplus Solvency margin can be met by Surplus

from Policyholder fund and Shareholder from Policyholder fund and Shareholder fund fund

11

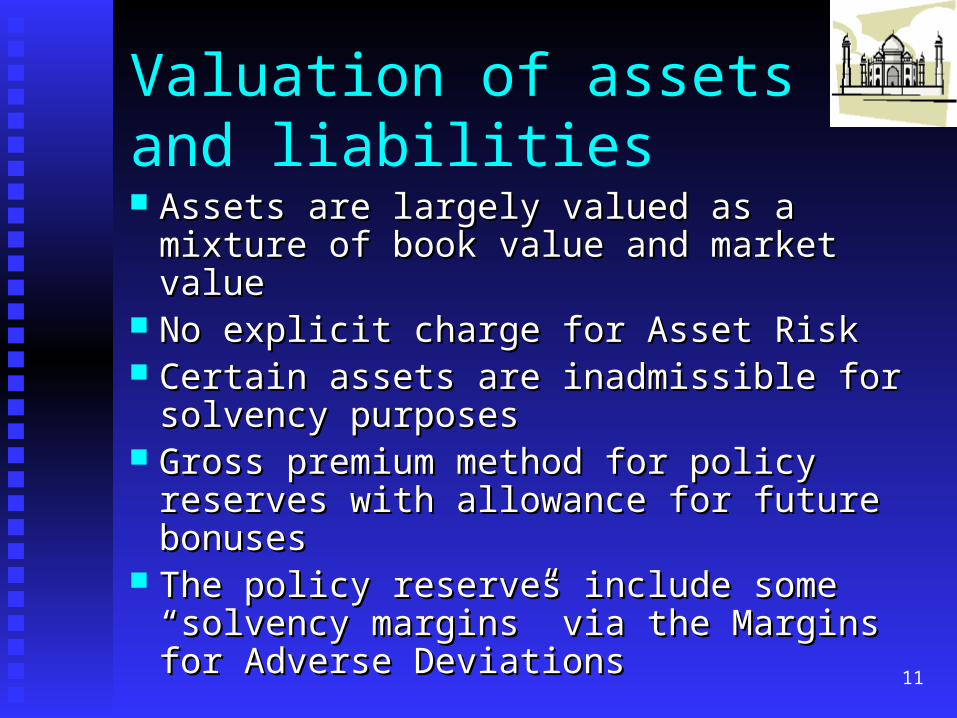

Valuation of assetsand liabilities Assets are largely valued as a mixture of Assets are largely valued as a mixture of

book value and market valuebook value and market value No explicit charge for Asset RiskNo explicit charge for Asset Risk Certain assets are inadmissible for solvency Certain assets are inadmissible for solvency

purposespurposes Gross premium method for policy reserves Gross premium method for policy reserves

with allowance for future bonuseswith allowance for future bonuses The policy reserves include some “solvency The policy reserves include some “solvency

margins” via the Margins for Adverse margins” via the Margins for Adverse Deviations Deviations

12

Solvency requirement Non-linked business: Non-linked business:

4% Reserves + 0.3% Sum at risk4% Reserves + 0.3% Sum at risk Linked Business:Linked Business:

with guarantees: 2% Reserves + 0.2% Sum at riskwith guarantees: 2% Reserves + 0.2% Sum at risk without guarantees: 1% Reserves + 0.3% Sum at without guarantees: 1% Reserves + 0.3% Sum at

risk risk Group Business:Group Business:

premiums guaranteed for not more than one year: premiums guaranteed for not more than one year: 1% Reserves + 0.2% Sum at risk1% Reserves + 0.2% Sum at risk

premiums guaranteed for more than one year:premiums guaranteed for more than one year:3% Reserves + 0.3% Sum at risk3% Reserves + 0.3% Sum at risk

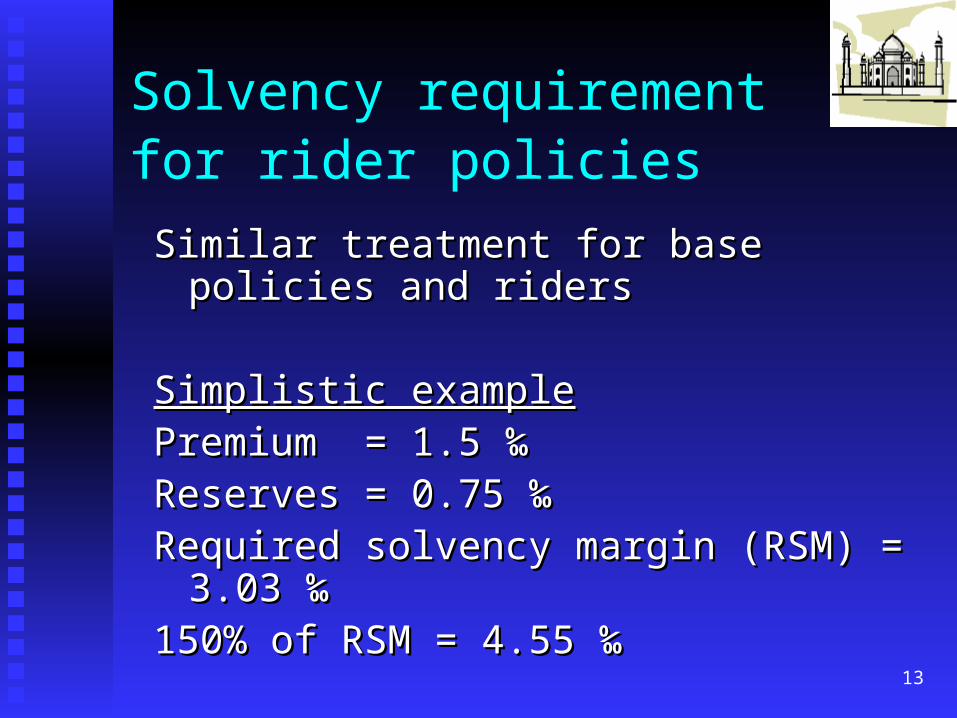

13

Solvency requirementfor rider policies

Similar treatment for base policies and ridersSimilar treatment for base policies and riders

Simplistic exampleSimplistic examplePremium = 1.5 Premium = 1.5 ‰‰Reserves = 0.75 Reserves = 0.75 ‰‰Required solvency margin (RSM) = 3.03 Required solvency margin (RSM) = 3.03 ‰‰150% of RSM = 4.55 150% of RSM = 4.55 ‰‰

14

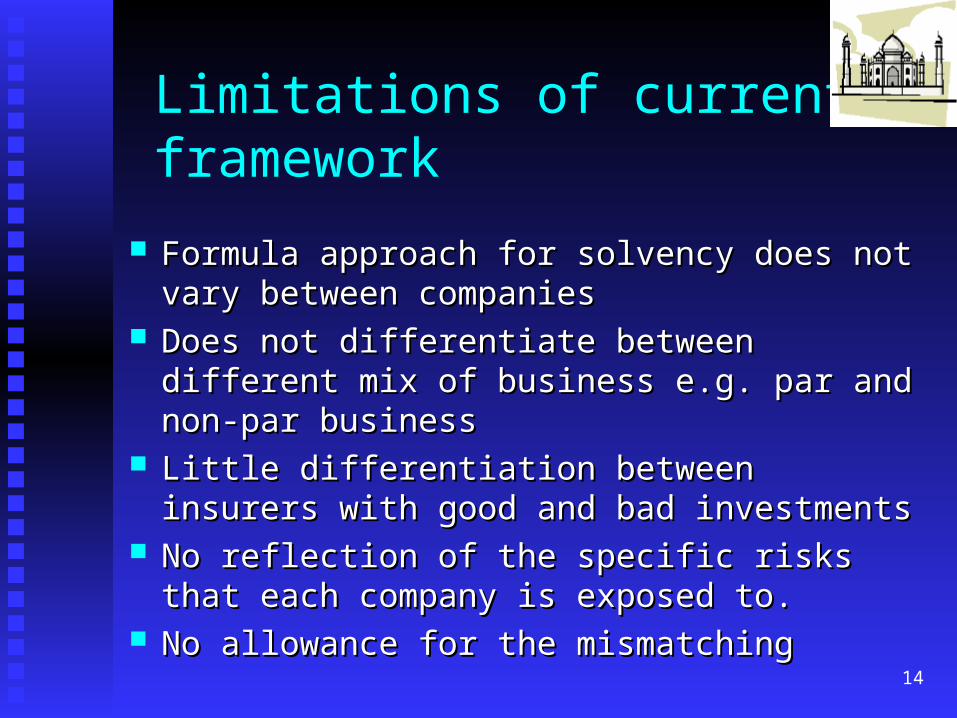

Limitations of currentframework

Formula approach for solvency does not vary Formula approach for solvency does not vary between companies between companies

Does not differentiate between different mix of Does not differentiate between different mix of business e.g. par and non-par businessbusiness e.g. par and non-par business

Little differentiation between insurers with good Little differentiation between insurers with good and bad investmentsand bad investments

No reflection of the specific risks that each No reflection of the specific risks that each company is exposed to.company is exposed to.

No allowance for the mismatchingNo allowance for the mismatching

15

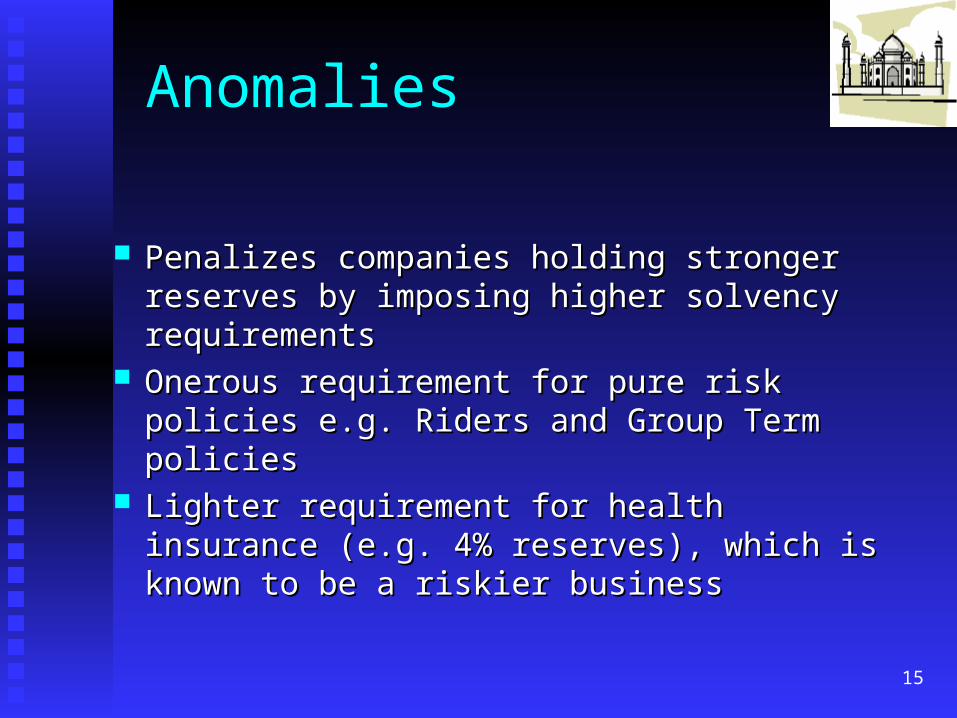

Anomalies

Penalizes companies holding stronger reserves by Penalizes companies holding stronger reserves by imposing higher solvency requirements imposing higher solvency requirements

Onerous requirement for pure risk policies e.g. Onerous requirement for pure risk policies e.g. Riders and Group Term policiesRiders and Group Term policies

Lighter requirement for health insurance (e.g. 4% Lighter requirement for health insurance (e.g. 4% reserves), which is known to be a riskier businessreserves), which is known to be a riskier business

16

Content

Background Background The current situation in IndiaThe current situation in India Developments in other marketsDevelopments in other markets Conclusions and recommendations for IndiaConclusions and recommendations for India

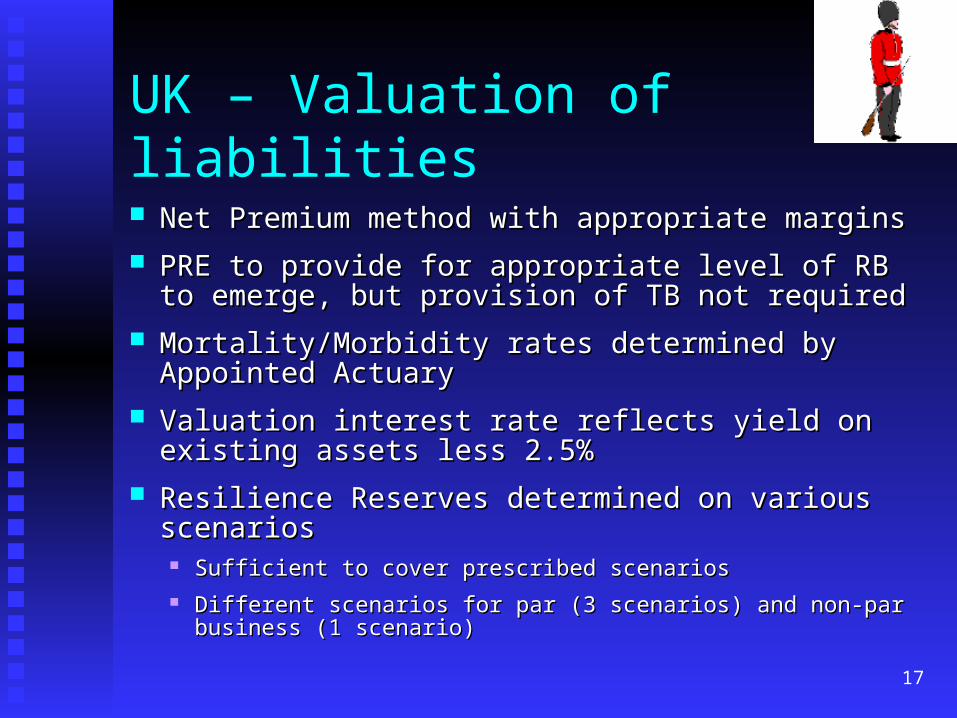

17

UK – Valuation ofliabilities Net Premium method with appropriate margins Net Premium method with appropriate margins

PRE to provide for appropriate level of RB to emerge, but PRE to provide for appropriate level of RB to emerge, but provision of TB not requiredprovision of TB not required

Mortality/Morbidity rates determined by Appointed Mortality/Morbidity rates determined by Appointed ActuaryActuary

Valuation interest rate Valuation interest rate reflects yield on existing assets less reflects yield on existing assets less 2.5%2.5%

Resilience Reserves determined on various scenariosResilience Reserves determined on various scenarios Sufficient to cover prescribed scenariosSufficient to cover prescribed scenarios

Different scenarios for par (3 scenarios) and non-par business (1 Different scenarios for par (3 scenarios) and non-par business (1 scenario)scenario)

18

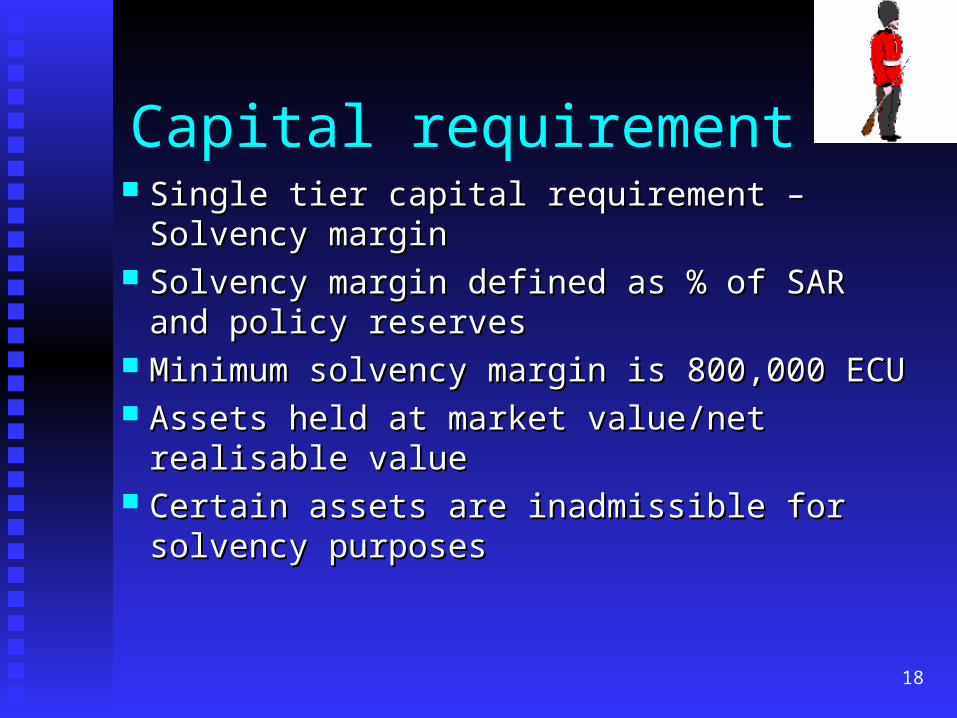

Capital requirement Single tier capital requirement – Solvency Single tier capital requirement – Solvency

marginmargin Solvency margin defined as % of SAR and Solvency margin defined as % of SAR and

policy reservespolicy reserves Minimum solvency margin is 800,000 ECUMinimum solvency margin is 800,000 ECU Assets held at market value/net realisable value Assets held at market value/net realisable value Certain assets are inadmissible for solvency Certain assets are inadmissible for solvency

purposespurposes

19

USA – Valuation ofliabilities Net Premium method with a prescribed Net Premium method with a prescribed

minimum basisminimum basis Mortality – 1980 CSOMortality – 1980 CSO Prescribed dynamic maximum valuation Prescribed dynamic maximum valuation

interest rateinterest rate Additional cash-flow testing requirementAdditional cash-flow testing requirement

Asset adequacy using cash-flow testingAsset adequacy using cash-flow testing Project asset and liability cash flows (excluding Project asset and liability cash flows (excluding

new business) under various scenariosnew business) under various scenarios

20

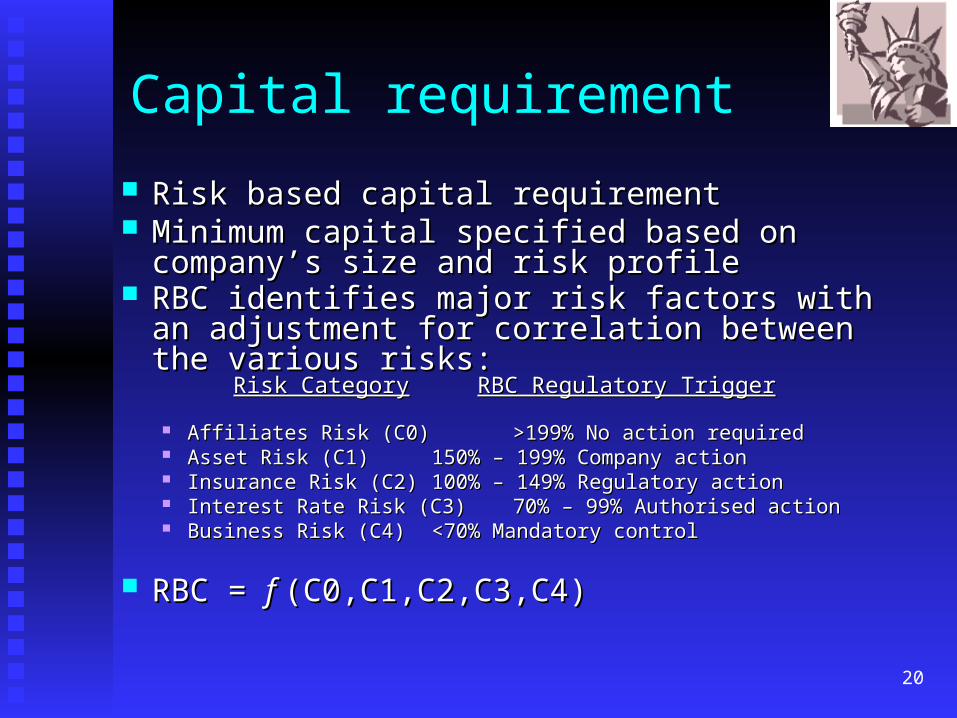

Capital requirement

Risk based capital requirementRisk based capital requirement Minimum capital specified based on company’s size Minimum capital specified based on company’s size

and risk profileand risk profile RBC identifies major risk factors with an adjustment RBC identifies major risk factors with an adjustment

for correlation between the various risks:for correlation between the various risks:Risk CategoryRisk Category RBC Regulatory TriggerRBC Regulatory Trigger

Affiliates Risk (C0) Affiliates Risk (C0) >199% No action required>199% No action required Asset Risk (C1) Asset Risk (C1) 150% – 199% Company action150% – 199% Company action Insurance Risk (C2) Insurance Risk (C2) 100% – 149% Regulatory action100% – 149% Regulatory action Interest Rate Risk (C3)Interest Rate Risk (C3) 70% – 99% Authorised action70% – 99% Authorised action Business Risk (C4) Business Risk (C4) <70% Mandatory control<70% Mandatory control

RBC = RBC = f f (C0,C1,C2,C3,C4)(C0,C1,C2,C3,C4)

21

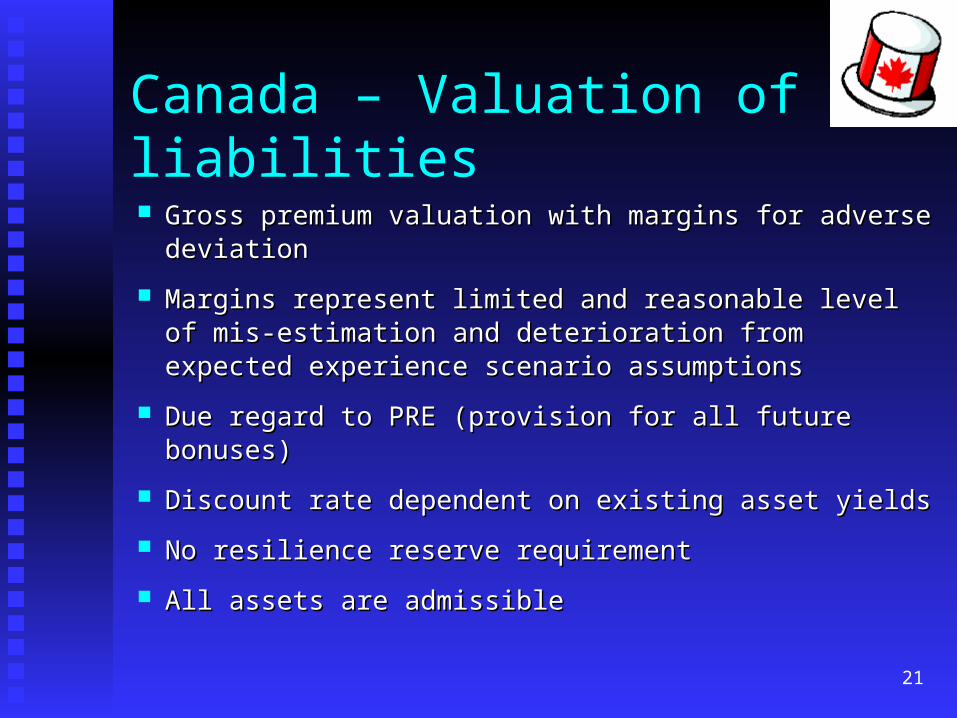

Canada – Valuation ofliabilities Gross premium valuation with margins for adverse deviationGross premium valuation with margins for adverse deviation

Margins represent Margins represent limited and reasonable level of mis-limited and reasonable level of mis-estimation and deterioration fromestimation and deterioration from expected experience expected experience scenario assumptionsscenario assumptions

Due regard to PRE (provision for all future bonuses)Due regard to PRE (provision for all future bonuses)

Discount rate dependent on existing asset yieldsDiscount rate dependent on existing asset yields

No resilience reserve requirementNo resilience reserve requirement

All assets are admissible All assets are admissible

22

Capital requirement Risk based capital requirement-Minimum Continuing Capital and Risk based capital requirement-Minimum Continuing Capital and

Surplus Requirement (MCCSR)Surplus Requirement (MCCSR)

MCCSR determined by applying factors to each of four risk MCCSR determined by applying factors to each of four risk components and adding the results components and adding the results

Risk components of MCCSR and composition of total capital Risk components of MCCSR and composition of total capital requirement (at year end 1998) were requirement (at year end 1998) were

Asset default riskAsset default risk 50%50% Mortality/morbidity/ lapse riskMortality/morbidity/ lapse risk 31%31% Interest margin pricing riskInterest margin pricing risk 4% 4% Changes in Interest Rate Environment RiskChanges in Interest Rate Environment Risk 15%15%

Target MCCSR ratio is 150% (however may vary according to Target MCCSR ratio is 150% (however may vary according to individual company risk profile)individual company risk profile)

23

Australian – Capital AdequacyStandards

1.1. Margin on Services Valuation – Gross Margin on Services Valuation – Gross Premium BasisPremium Basis

2.2. Statutory Valuation = BEL + Profit Statutory Valuation = BEL + Profit MarginMargin

3.3. All assumptions are based on the latest All assumptions are based on the latest best estimates at the time of valuation – best estimates at the time of valuation – pro active basispro active basis

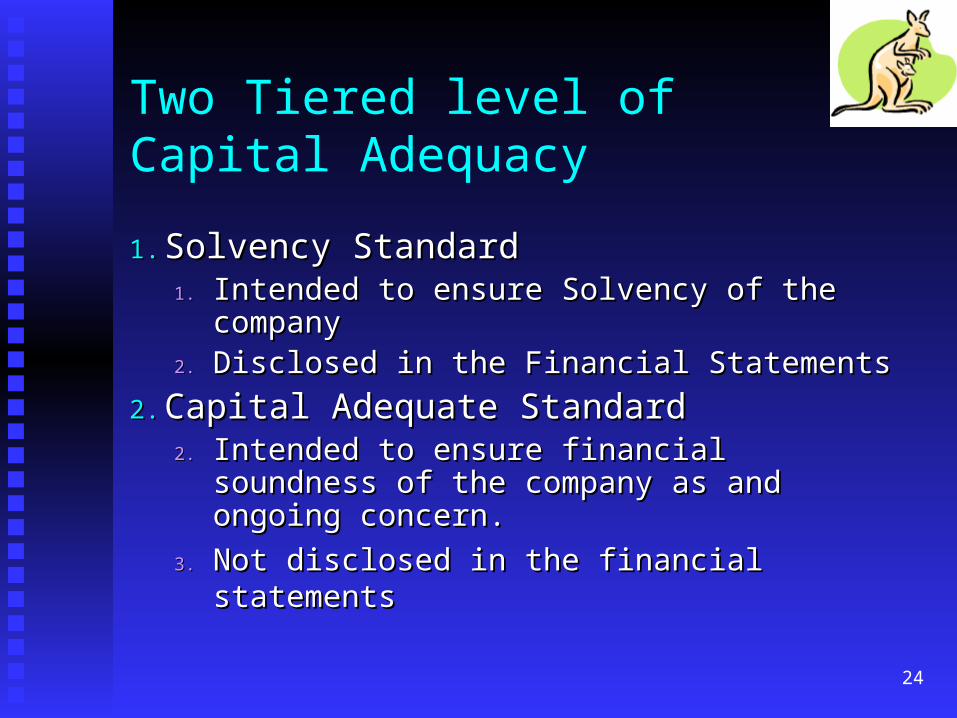

24

Two Tiered level of Capital Adequacy

1.1. Solvency StandardSolvency Standard1.1. Intended to ensure Solvency of the companyIntended to ensure Solvency of the company2.2. Disclosed in the Financial StatementsDisclosed in the Financial Statements

2.2. Capital Adequate StandardCapital Adequate Standard2.2. Intended to ensure financial soundness of Intended to ensure financial soundness of

the company as and ongoing concern.the company as and ongoing concern.

3.3. Not disclosed in the financial statementsNot disclosed in the financial statements

25

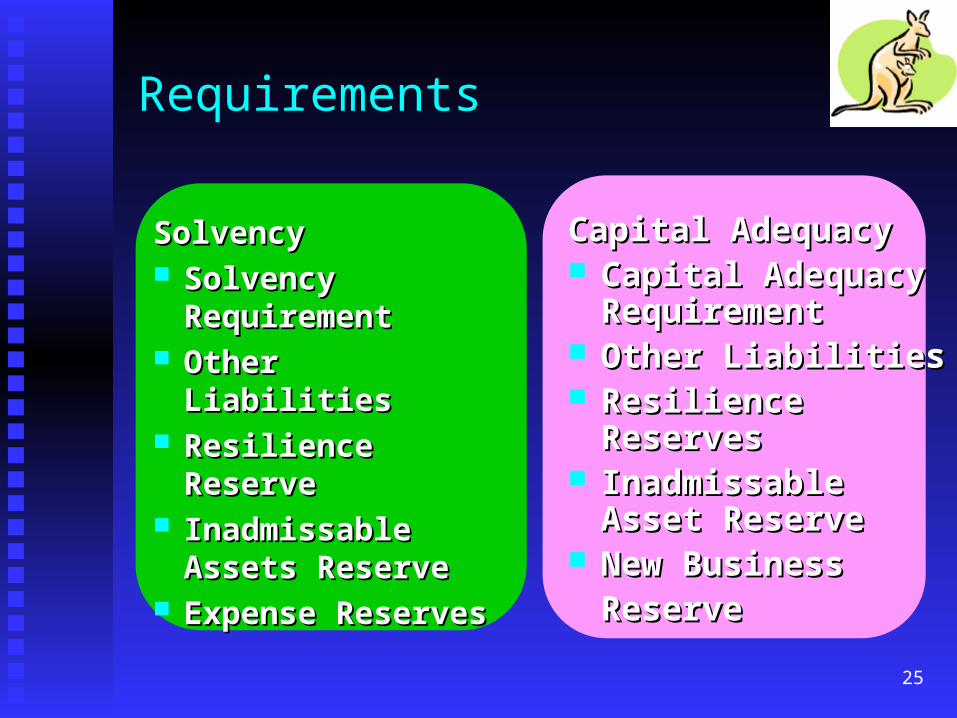

Requirements

SolvencySolvency Solvency Solvency

RequirementRequirement Other LiabilitiesOther Liabilities Resilience ReserveResilience Reserve Inadmissable Inadmissable

Assets ReserveAssets Reserve Expense ReservesExpense Reserves

Capital AdequacyCapital Adequacy Capital Adequacy Capital Adequacy

RequirementRequirement Other LiabilitiesOther Liabilities Resilience ReservesResilience Reserves Inadmissable Asset Inadmissable Asset

ReserveReserve New BusinessNew Business

ReserveReserve

26

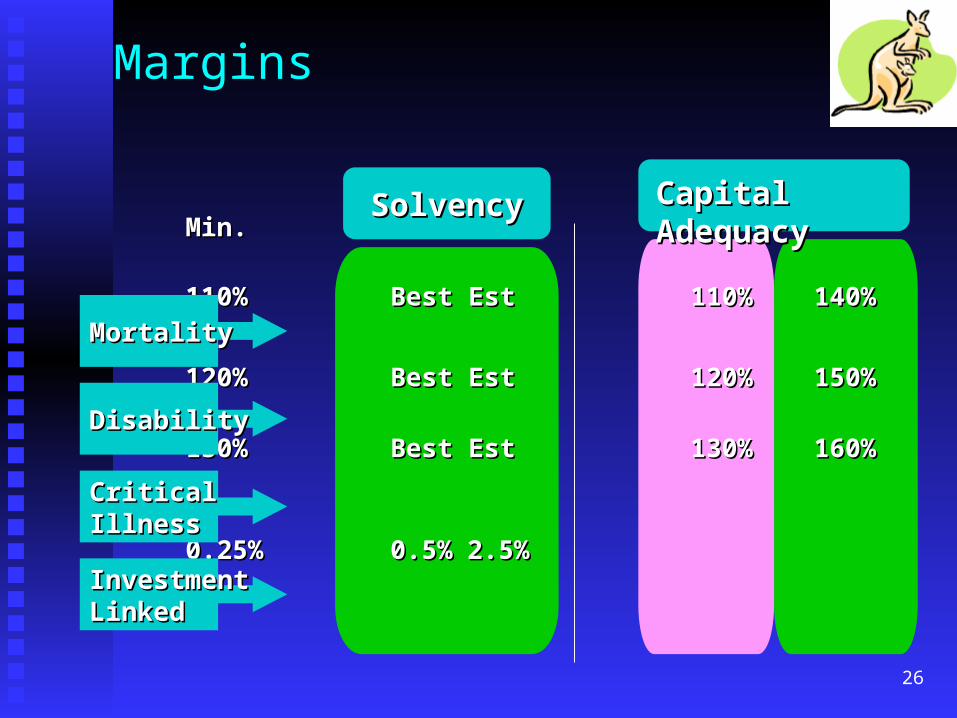

Margins

Min.Min.Max.Max.

110%110% Best EstBest Est 110%110% 140%140%

120%120% Best EstBest Est 120%120% 150%150%

130%130% Best Est Best Est 130%130% 160%160%

0.25%0.25% 0.5%0.5% 2.5%2.5%

InvestmentInvestmentLinkedLinked

CriticalCriticalIllnessIllness

DisabilityDisability

MortalityMortality

Capital AdequacyCapital AdequacySolvencySolvency

27

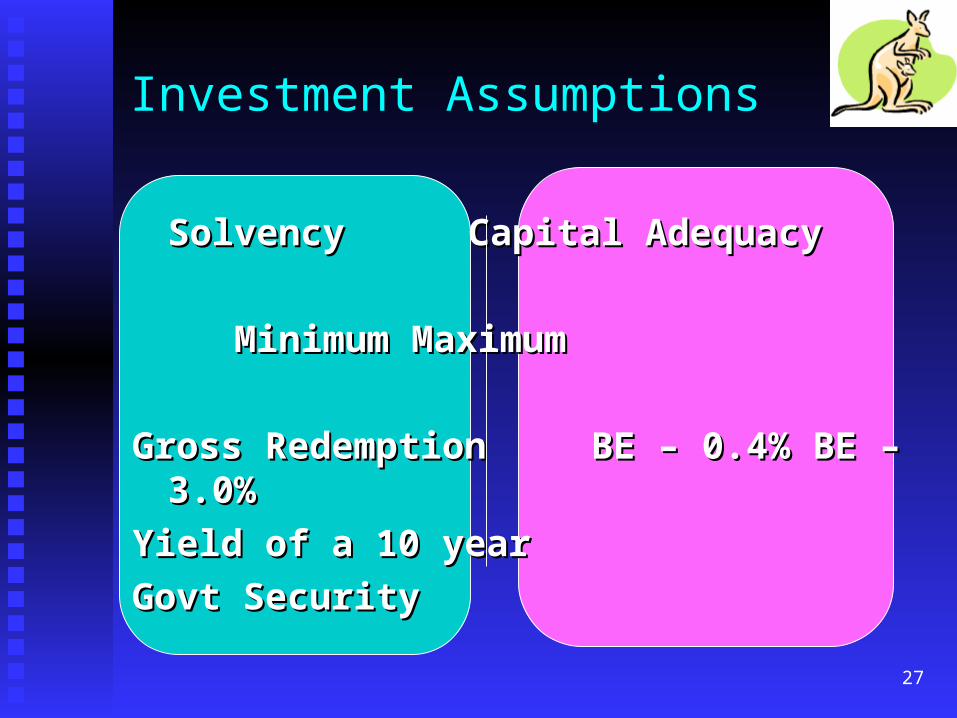

Investment Assumptions

SolvencySolvency Capital Adequacy Capital Adequacy

Minimum MaximumMinimum Maximum

Gross Redemption Gross Redemption BE – 0.4% BE – 3.0% BE – 0.4% BE – 3.0%

Yield of a 10 year Yield of a 10 year

Govt SecurityGovt Security

28

Resilience Reserves

The amount that needs to be held before the The amount that needs to be held before the happening of a prescribed set of changes in happening of a prescribed set of changes in the economic environment such that after the economic environment such that after the changes the company is able to meet the the changes the company is able to meet the liabilities of the fundliabilities of the fund

29

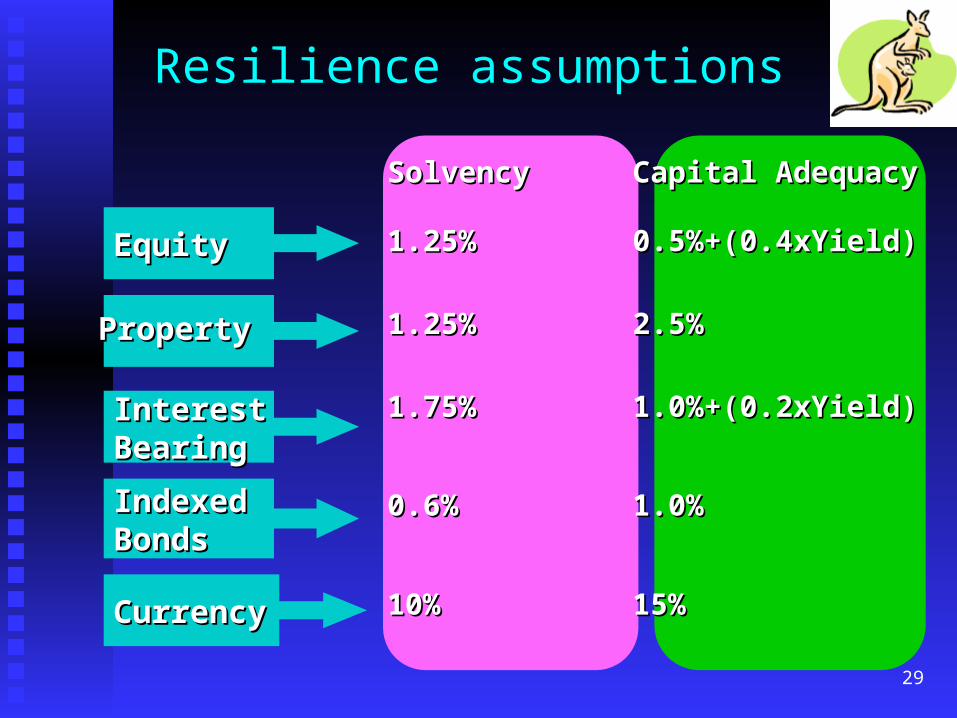

EquityEquity

Resilience assumptions

SolvencySolvency Capital AdequacyCapital Adequacy

1.25% 1.25% 0.5%+(0.4xYield)0.5%+(0.4xYield)

1.25% 1.25% 2.5%2.5%

1.75% 1.75% 1.0%+(0.2xYield)1.0%+(0.2xYield)

0.6%0.6% 1.0%1.0%

10%10% 15%15%CurrencyCurrency

IndexedIndexedBondsBonds

PropertyProperty

InterestInterestBearingBearing

30

Singapore – Valuation ofliabilities Looking to move to a gross premium basis - Looking to move to a gross premium basis -

basis selected by actuary, having regard to basis selected by actuary, having regard to professional guidance (a change from net professional guidance (a change from net premium valuation)premium valuation)

A PAD is added to the best estimate liabilities. A PAD is added to the best estimate liabilities.

Propose risk free rates are used for non-Propose risk free rates are used for non-participating business (based on government participating business (based on government bonds). bonds).

Can significantly increase liabilityCan significantly increase liability

31

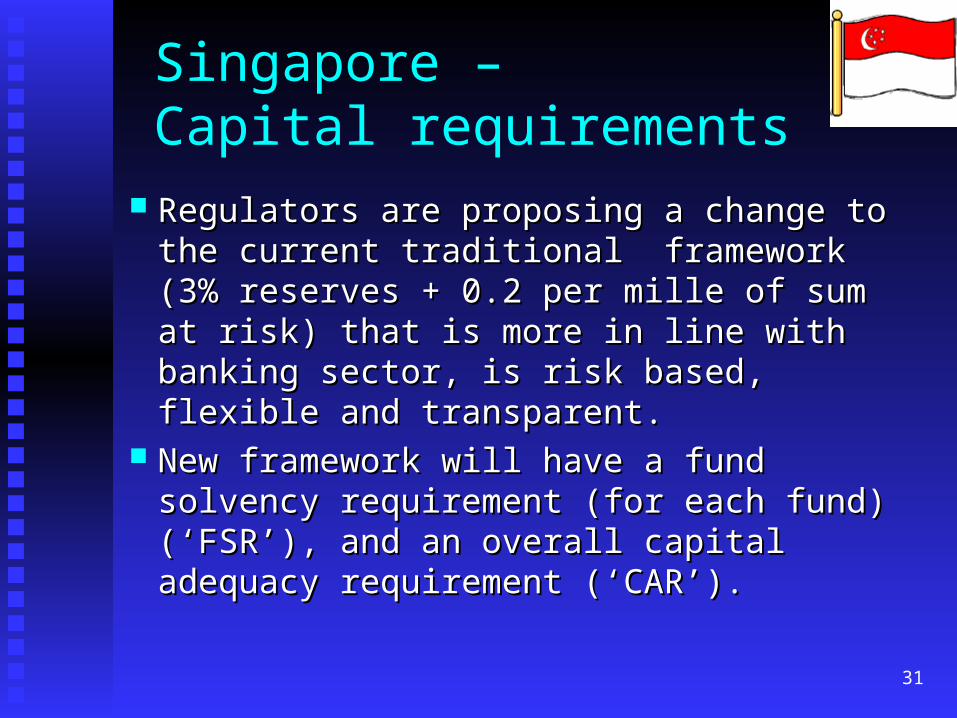

Singapore –Capital requirements

Regulators are proposing a change to the Regulators are proposing a change to the current traditional framework (3% reserves + current traditional framework (3% reserves + 0.2 per mille of sum at risk) that is more in 0.2 per mille of sum at risk) that is more in line with banking sector, is risk based, flexible line with banking sector, is risk based, flexible and transparent. and transparent.

New framework will have a fund solvency New framework will have a fund solvency requirement (for each fund) (‘FSR’), and an requirement (for each fund) (‘FSR’), and an overall capital adequacy requirement (‘CAR’).overall capital adequacy requirement (‘CAR’).

32

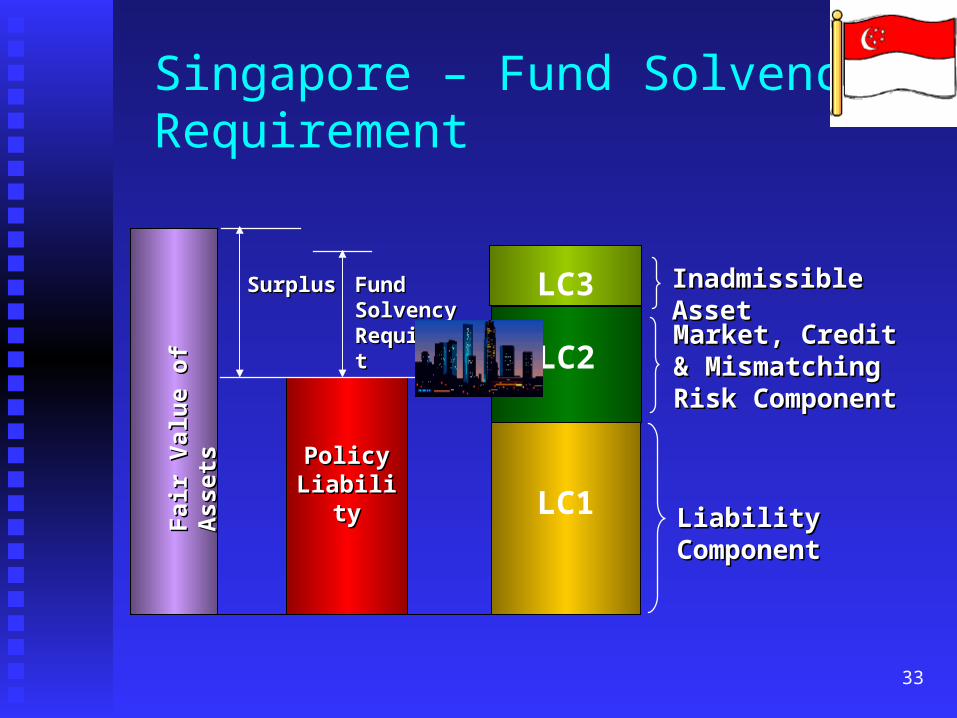

Singapore – Capital requirements

FSR takes in to account liabilities and risks in FSR takes in to account liabilities and risks in the form of three components:the form of three components: LC1 - Liability component (as per valuation with margins)LC1 - Liability component (as per valuation with margins) LC2 - Market, Credit and Mismatching RiskLC2 - Market, Credit and Mismatching Risk LC3 - Inadmissible asset risk component LC3 - Inadmissible asset risk component FSR = LC1+LC2+LC3 - Value of liabilities FSR = LC1+LC2+LC3 - Value of liabilities

Capital adequacy such that: Capital adequacy such that: Available capital/Required Capital > Specified minimum Available capital/Required Capital > Specified minimum

33

PolicyPolicy LiabilityLiability

LC1

LC2

LC3Fund Solvency Fund Solvency RequirementRequirement

SurplusSurplus

Fai

r V

alue

of

Ass

ets

Fai

r V

alue

of

Ass

ets

Liability Liability ComponentComponent

Market, Credit & Market, Credit & Mismatching Risk Mismatching Risk ComponentComponent

Inadmissible AssetInadmissible Asset

Singapore – Fund SolvencyRequirement

34

South Africa Capital Adequacy Requirements

Gross Premium Valuation BasisGross Premium Valuation Basis One level of Capital AdequacyOne level of Capital Adequacy RBC ApproachRBC Approach

35

OCAR

OCAR = OCAR = IOCAR grossed up for the effect IOCAR grossed up for the effect of of the assumed fall in fair value of the assumed fall in fair value of the the assets backing itassets backing it

OCAR =OCAR = IOCAR/0.7 if assets in equities IOCAR/0.7 if assets in equities assumed to fall 30%assumed to fall 30%

OCAR =OCAR = IOCAR if assets in cashIOCAR if assets in cash

36

IOCAR

IOCAR = IOCAR = Intermediary Ordinary Capital Intermediary Ordinary Capital Requirements before Requirements before

taking into taking into account the account the effect of the assumed effect of the assumed falls in fair falls in fair value of the assetsvalue of the assets covering it covering it – Resilience scenario– Resilience scenario

37

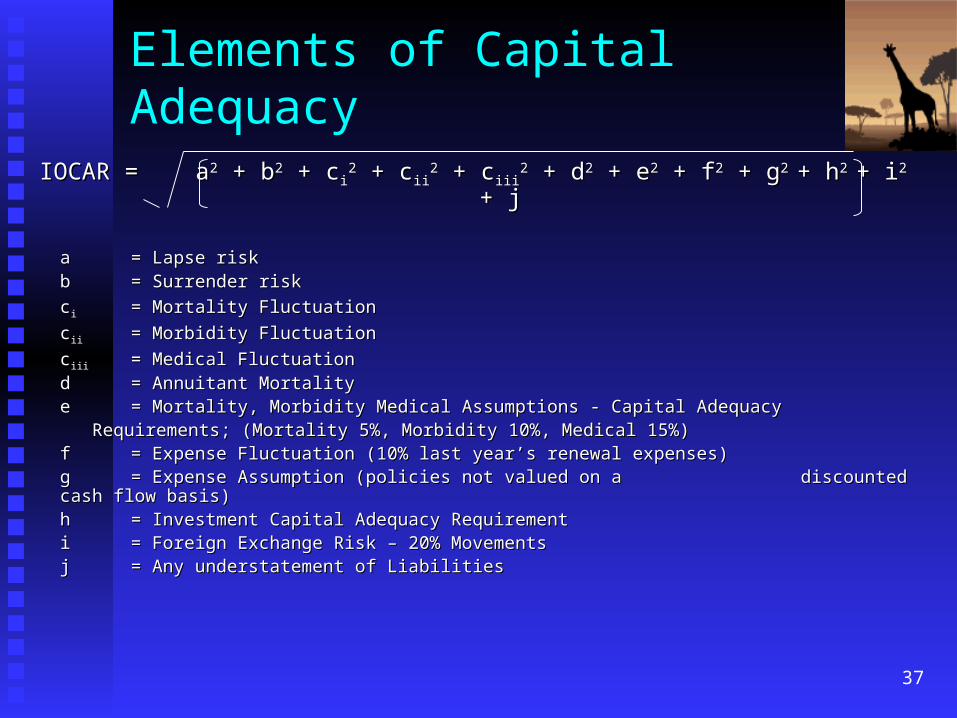

Elements of Capital Adequacy

IOCAR = aIOCAR = a22 + b + b22 + c + cii22 + c + ciiii

22 + c + ciiiiii22 + d + d22 + e + e22 + f + f22 + g + g2 2 + h+ h2 2 + i+ i22 + j + j

aa = Lapse risk= Lapse risk

bb = Surrender risk= Surrender risk

ccii = Mortality Fluctuation = Mortality Fluctuation

cciiii = Morbidity Fluctuation = Morbidity Fluctuation

cciiiiii = Medical Fluctuation = Medical Fluctuation

dd = Annuitant Mortality= Annuitant Mortalityee = Mortality, Morbidity Medical Assumptions - Capital Adequacy = Mortality, Morbidity Medical Assumptions - Capital Adequacy

Requirements; (Mortality 5%, Morbidity 10%, Medical 15%)Requirements; (Mortality 5%, Morbidity 10%, Medical 15%)ff = Expense Fluctuation (10% last year’s renewal expenses)= Expense Fluctuation (10% last year’s renewal expenses)gg = Expense Assumption (policies not valued on a = Expense Assumption (policies not valued on a

discounted cash flow basis)discounted cash flow basis)hh = Investment Capital Adequacy Requirement= Investment Capital Adequacy Requirementii = Foreign Exchange Risk – 20% Movements= Foreign Exchange Risk – 20% Movementsjj = Any understatement of Liabilities= Any understatement of Liabilities

38

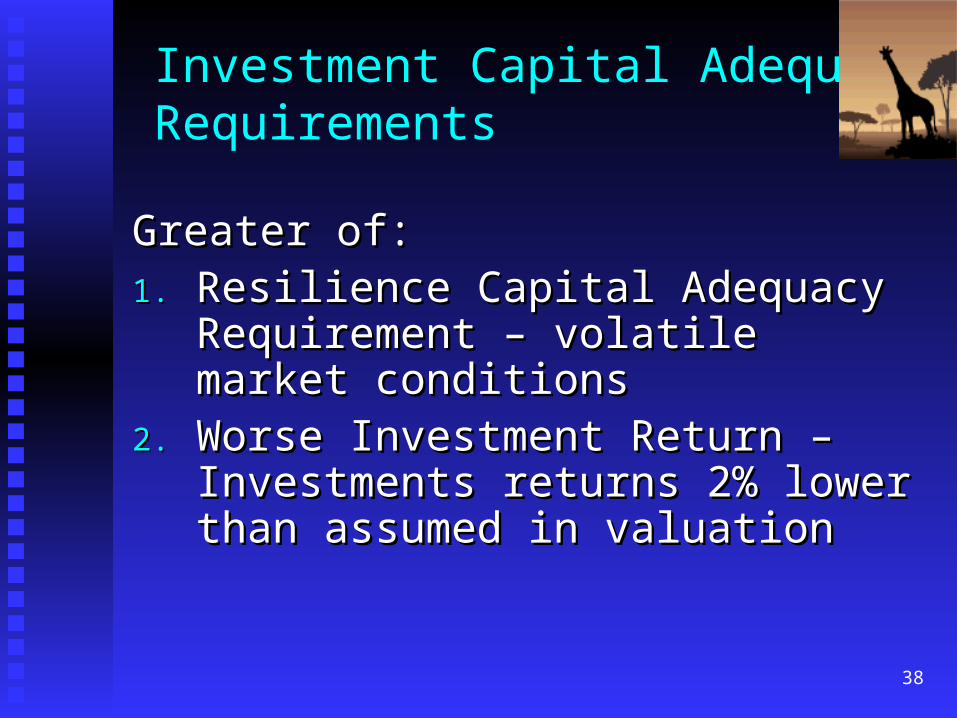

Investment Capital Adequacy Requirements

Greater of:Greater of:1.1. Resilience Capital Adequacy Requirement Resilience Capital Adequacy Requirement

– volatile market conditions– volatile market conditions2.2. Worse Investment Return – Investments Worse Investment Return – Investments

returns 2% lower than assumed in returns 2% lower than assumed in valuationvaluation

39

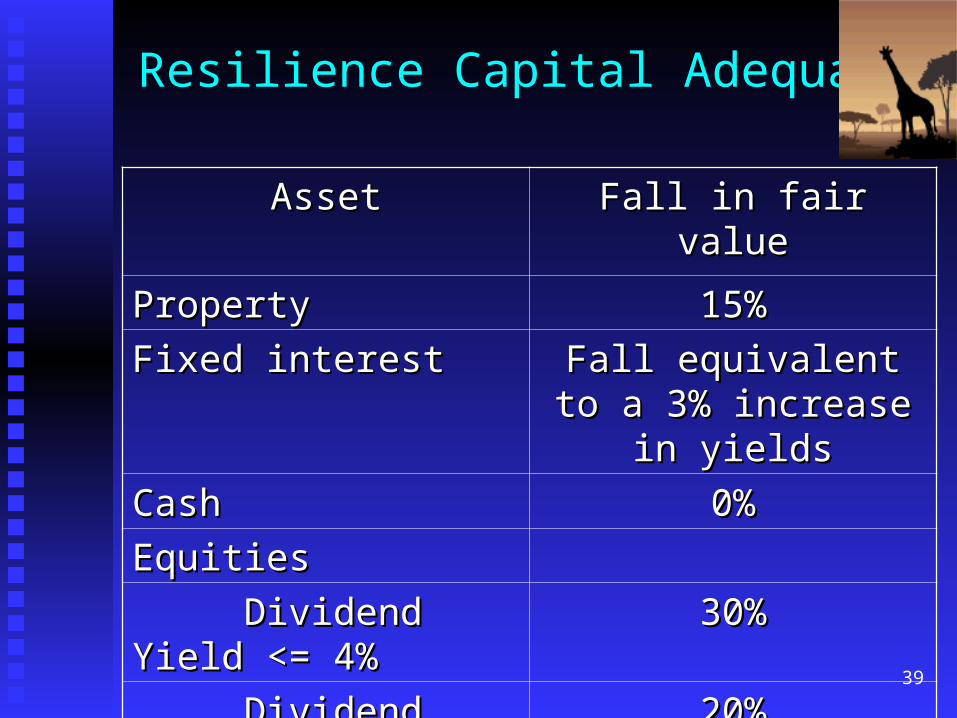

Resilience Capital Adequacy

AssetAsset Fall in fair valueFall in fair value

Property Property 15%15%

Fixed interestFixed interest Fall equivalent to a 3% Fall equivalent to a 3% increase in yieldsincrease in yields

CashCash 0%0%

EquitiesEquities

Dividend Yield <= 4%Dividend Yield <= 4% 30%30%

Dividend Yield >= 5%Dividend Yield >= 5% 20%20%

OtherOther InterpolateInterpolate

40

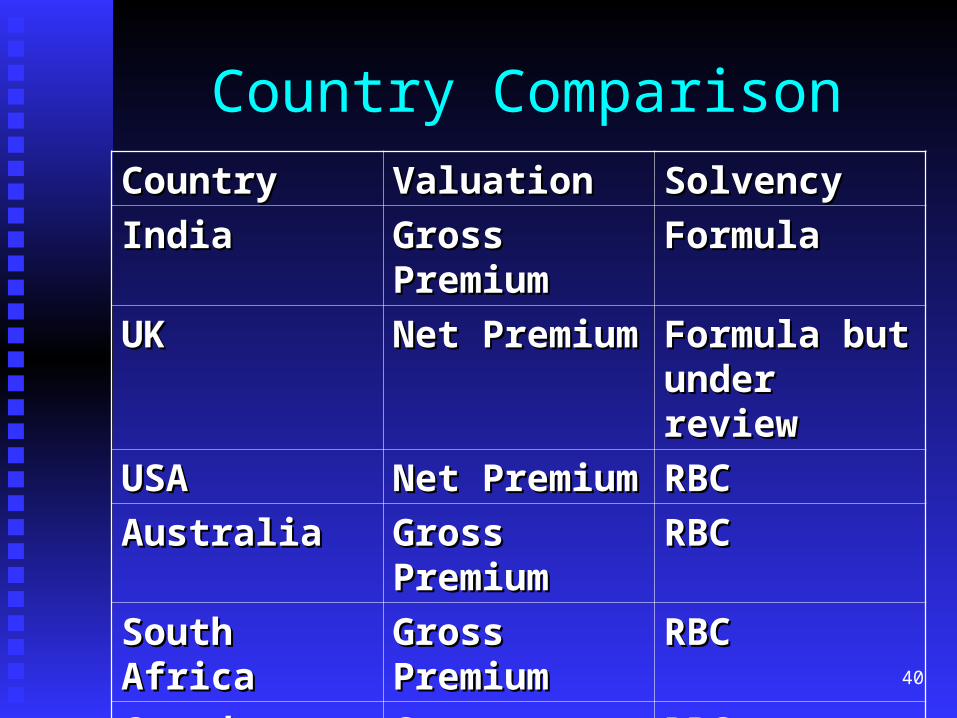

Country Comparison

CountryCountry ValuationValuation SolvencySolvency

IndiaIndia Gross PremiumGross Premium FormulaFormula

UKUK Net PremiumNet Premium Formula but Formula but under reviewunder review

USAUSA Net PremiumNet Premium RBCRBC

AustraliaAustralia Gross PremiumGross Premium RBCRBC

South AfricaSouth Africa Gross PremiumGross Premium RBCRBC

CanadaCanada Gross PremiumGross Premium RBCRBC

Singapore Singapore (Proposed)(Proposed)

Gross PremiumGross Premium RBCRBC

41

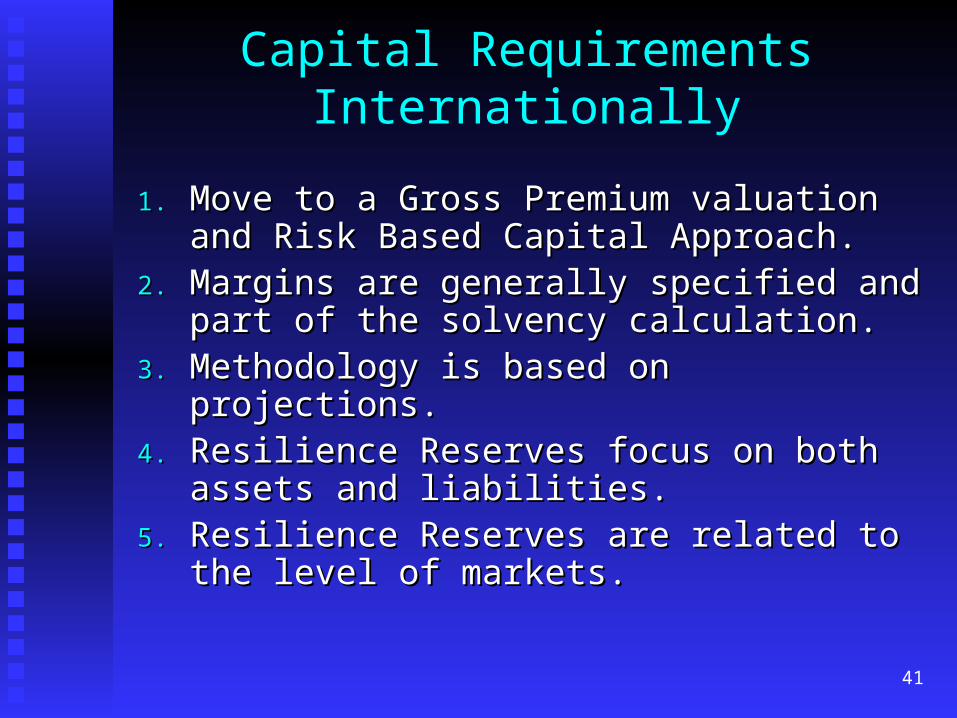

Capital Requirements Internationally

1.1. Move to a Gross Premium valuation and Move to a Gross Premium valuation and Risk Based Capital Approach.Risk Based Capital Approach.

2.2. Margins are generally specified and part of Margins are generally specified and part of the solvency calculation.the solvency calculation.

3.3. Methodology is based on projections.Methodology is based on projections.4.4. Resilience Reserves focus on both assets Resilience Reserves focus on both assets

and liabilities.and liabilities.5.5. Resilience Reserves are related to the level Resilience Reserves are related to the level

of markets.of markets.

42

Content

Background Background The current situation in IndiaThe current situation in India Developments in other marketsDevelopments in other markets Conclusions and recommendations for IndiaConclusions and recommendations for India

43

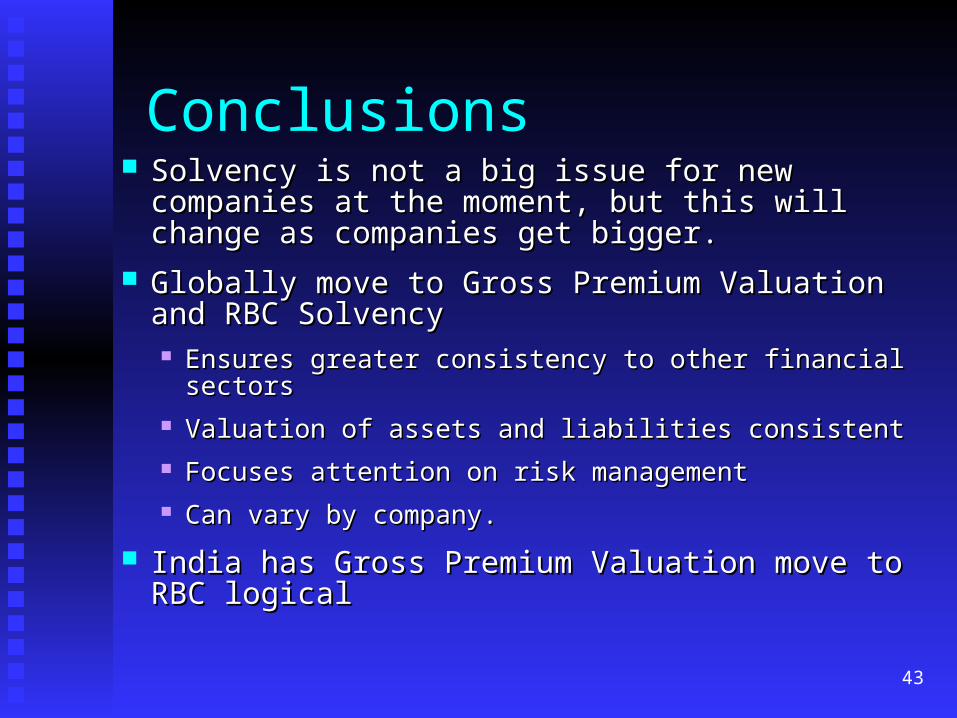

Conclusions Solvency is not a big issue for new companies at the Solvency is not a big issue for new companies at the

moment, but this will change as companies get moment, but this will change as companies get bigger. bigger.

Globally move to Gross Premium Valuation and RBC Globally move to Gross Premium Valuation and RBC SolvencySolvency Ensures greater consistency to other financial sectorsEnsures greater consistency to other financial sectors

Valuation of assets and liabilities consistentValuation of assets and liabilities consistent

Focuses attention on risk managementFocuses attention on risk management

Can vary by company.Can vary by company.

India has Gross Premium Valuation move to RBC India has Gross Premium Valuation move to RBC logicallogical

44

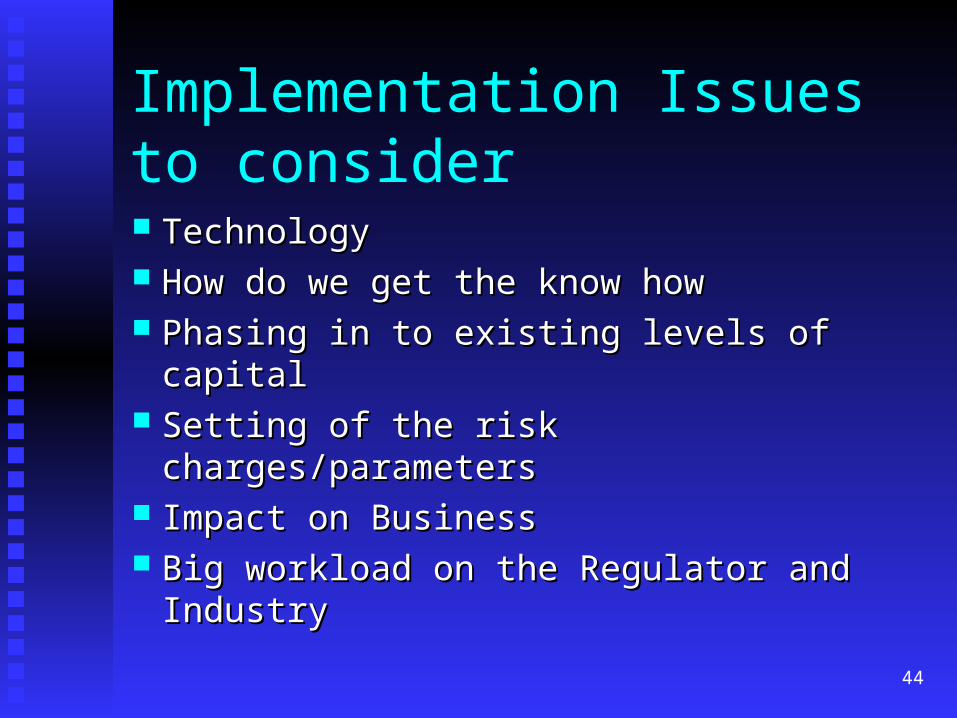

Implementation Issues to consider Technology Technology How do we get the know howHow do we get the know how Phasing in to existing levels of capitalPhasing in to existing levels of capital Setting of the risk charges/parametersSetting of the risk charges/parameters Impact on BusinessImpact on Business Big workload on the Regulator and IndustryBig workload on the Regulator and Industry

45

Recommendation

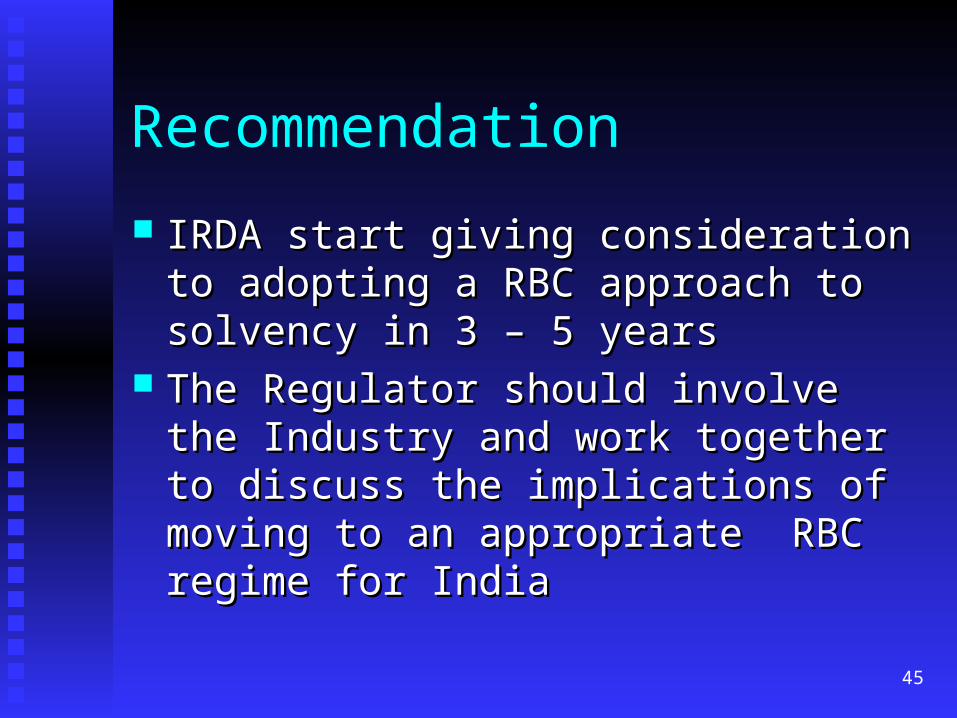

IRDA start giving consideration to adopting IRDA start giving consideration to adopting a RBC approach to solvency in 3 – 5 yearsa RBC approach to solvency in 3 – 5 years

The Regulator should involve the Industry The Regulator should involve the Industry and work together to discuss the and work together to discuss the implications of moving to an appropriate implications of moving to an appropriate RBC regime for IndiaRBC regime for India

46

Acknowledgements

We take this opportunity to thank all those We take this opportunity to thank all those actuaries and Appointed Actuaries in India actuaries and Appointed Actuaries in India who provided us with valuable inputs for who provided us with valuable inputs for this paper.this paper.

All the views expressed in this paper are the All the views expressed in this paper are the views of the authors and are not necessarily views of the authors and are not necessarily the views of our employersthe views of our employers