Embed Size (px)

Citation preview

1

2010Budget and Tax

Update

2

2010 BUDGET

3

Main Tax Proposals

• Personal income tax relief of R6.5 billion

• Fuel taxes to increase by 25.5 c per litre

• Voluntary disclosure programme

• Curbing of avoidance schemes

• Increased sin taxes

• Cash grant for hiring unskilled youth

4

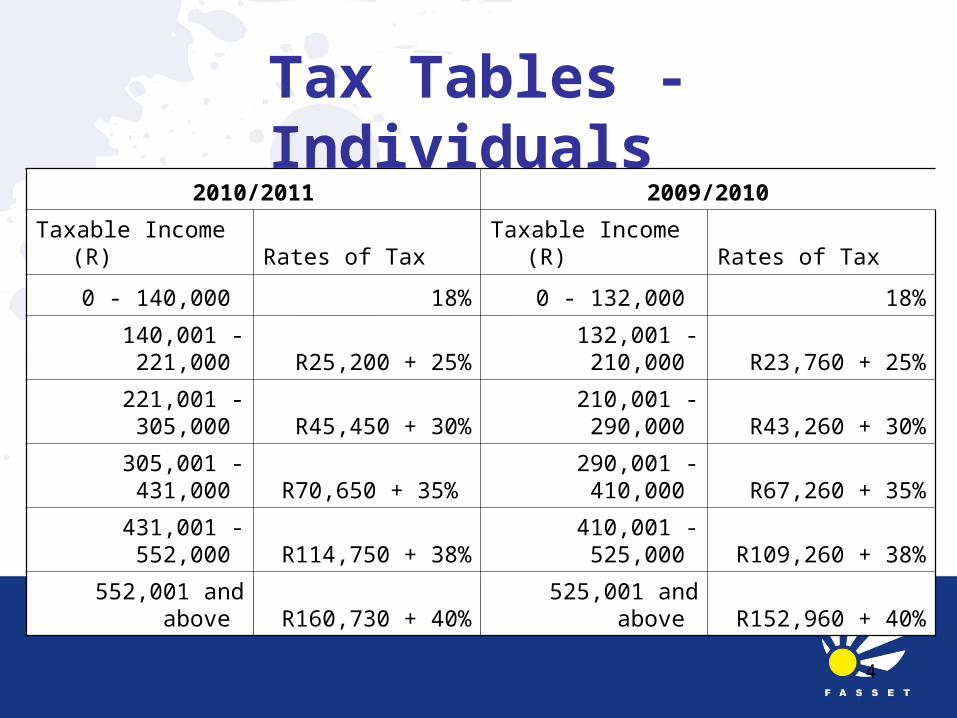

Tax Tables - Individuals 2010/2011 2009/2010

Taxable Income (R) Rates of Tax Taxable Income (R) Rates of Tax

0 - 140,000 18% 0 - 132,000 18%

140,001 - 221,000 R25,200 + 25% 132,001 - 210,000 R23,760 + 25%

221,001 - 305,000 R45,450 + 30% 210,001 - 290,000 R43,260 + 30%

305,001 - 431,000 R70,650 + 35% 290,001 - 410,000 R67,260 + 35%

431,001 - 552,000 R114,750 + 38% 410,001 - 525,000 R109,260 + 38%

552,001 and above R160,730 + 40% 525,001 and above R152,960 + 40%

5

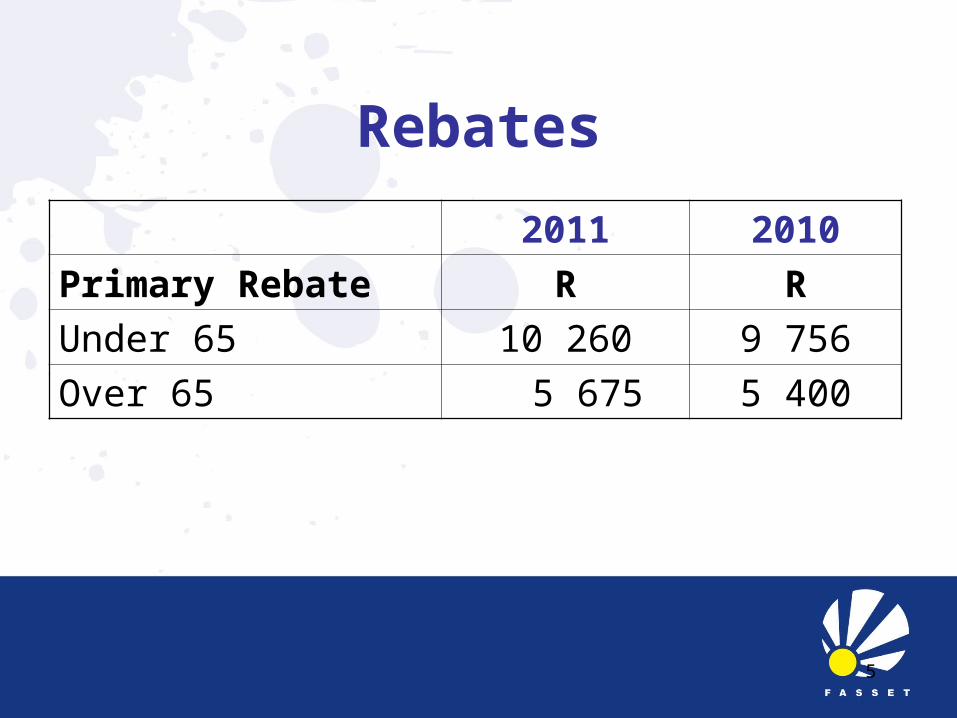

Rebates

2011 2010

Primary Rebate R R

Under 65 10 260 9 756

Over 65 5 675 5 400

6

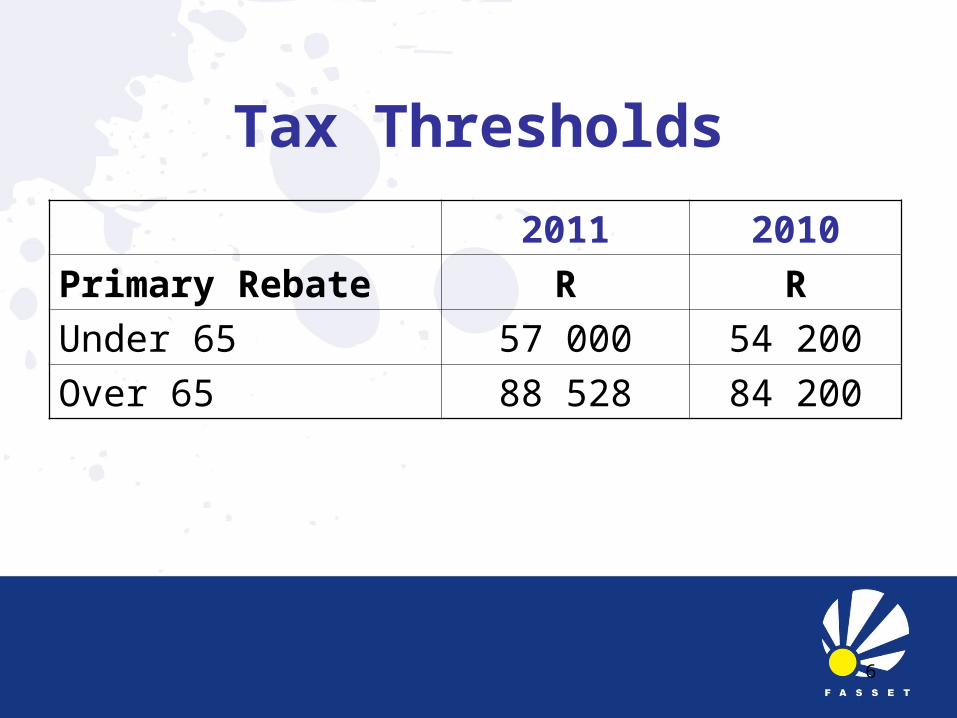

Tax Thresholds

2011 2010

Primary Rebate R R

Under 65 57 000 54 200

Over 65 88 528 84 200

7

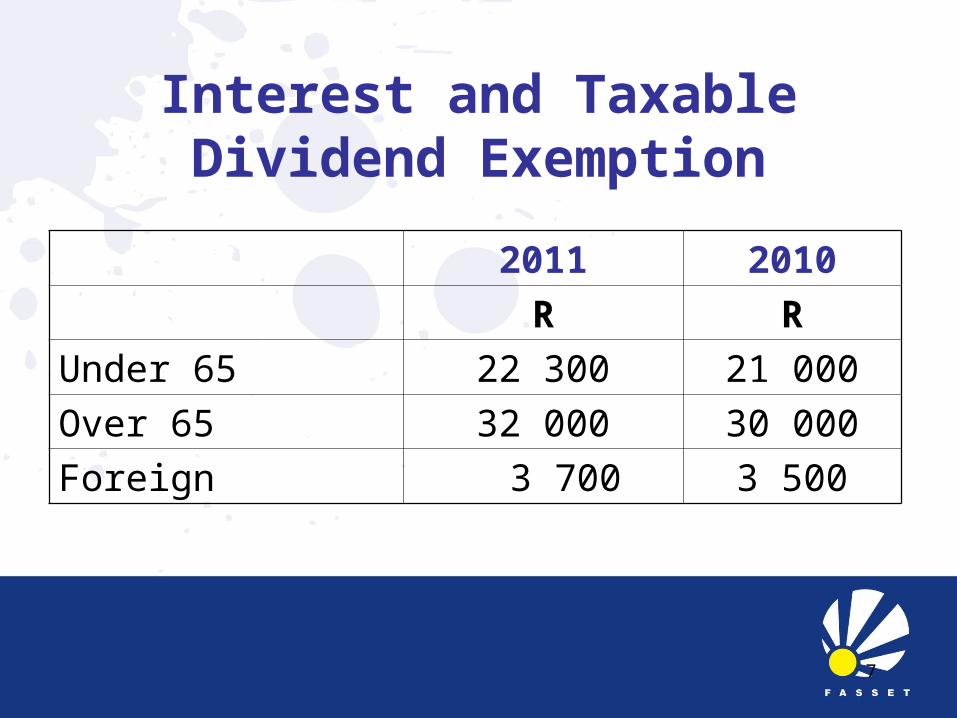

Interest and Taxable Dividend Exemption

2011 2010

R R

Under 65 22 300 21 000

Over 65 32 000 30 000

Foreign 3 700 3 500

8

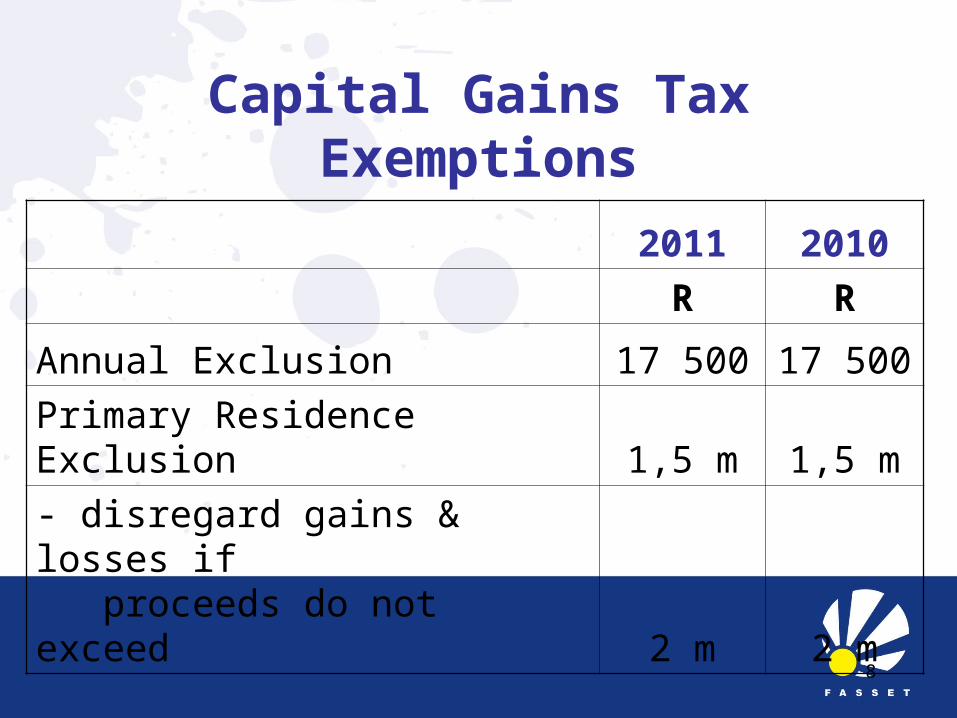

Capital Gains Tax Exemptions

2011 2010

R R

Annual Exclusion 17 500 17 500

Primary Residence Exclusion 1,5 m 1,5 m

- disregard gains & losses if proceeds do not exceed 2 m 2 m

9

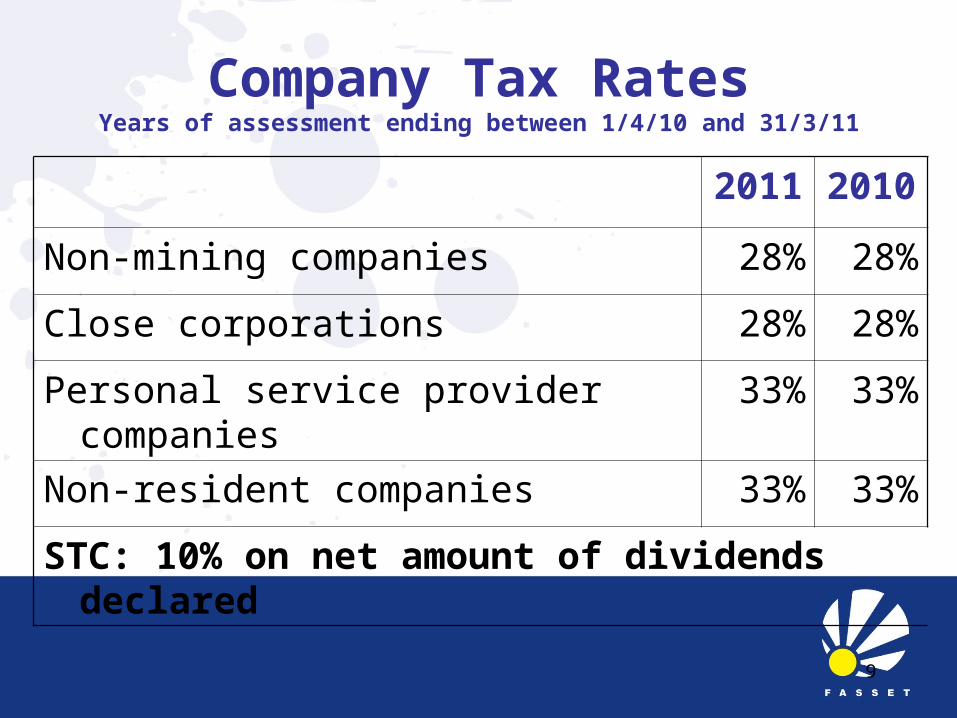

Company Tax RatesYears of assessment ending between 1/4/10 and 31/3/11

2011 2010

Non-mining companies 28% 28%

Close corporations 28% 28%

Personal service provider companies 33% 33%

Non-resident companies 33% 33%

STC: 10% on net amount of dividends declared

10

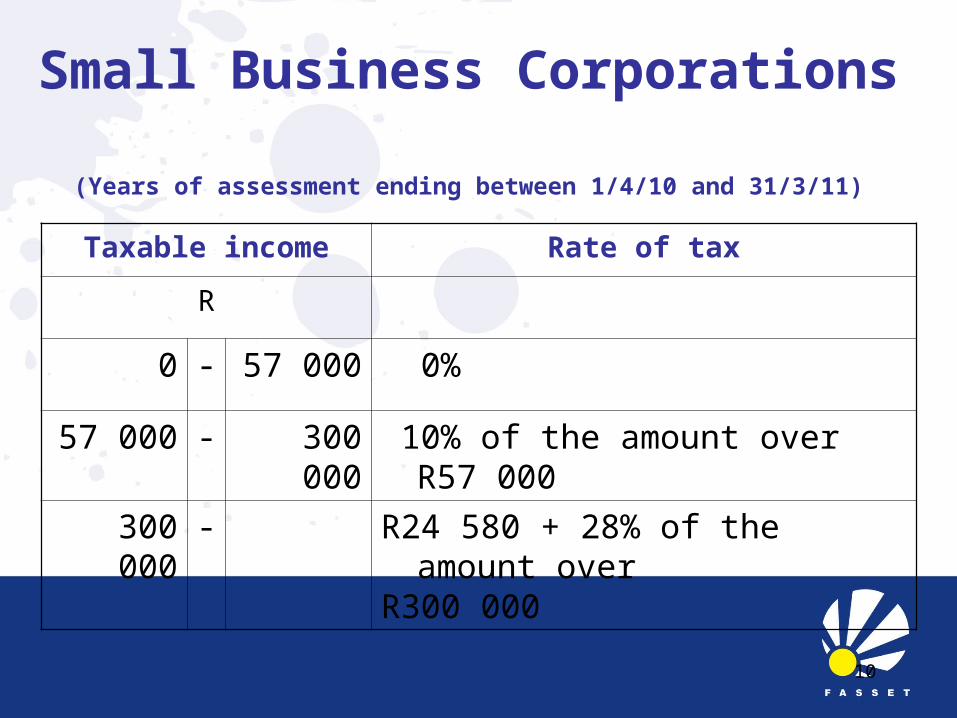

Taxable income Rate of tax

R

0 - 57 000 0%

57 000 - 300 000 10% of the amount over R57 000

300 000 - R24 580 + 28% of the amount overR300 000

Small Business Corporations (Years of assessment ending between 1/4/10 and 31/3/11)

11

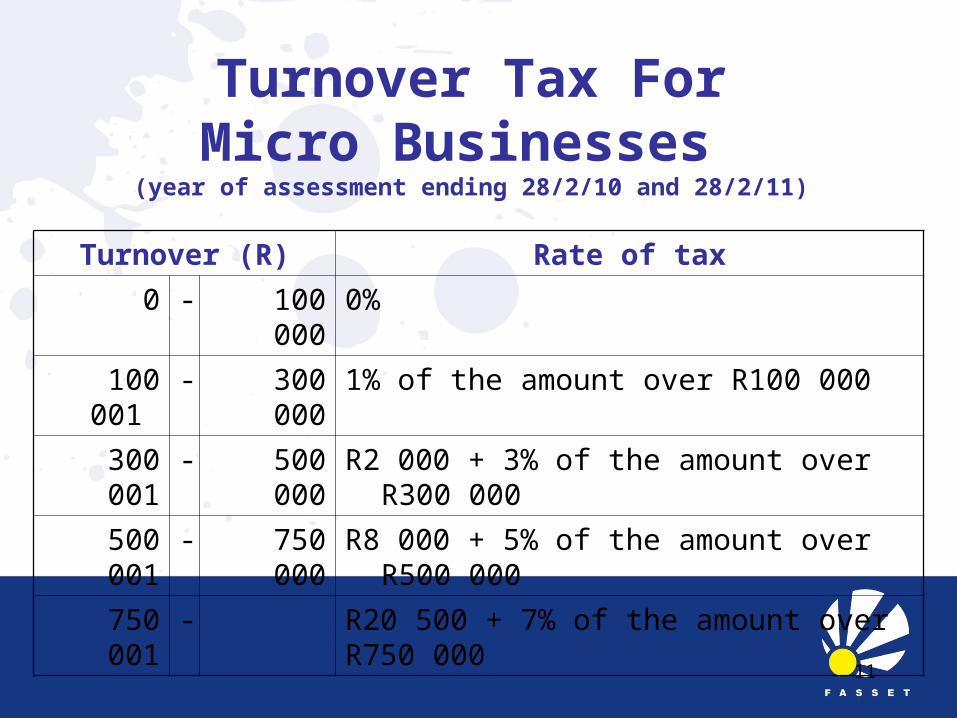

Turnover Tax ForMicro Businesses

(year of assessment ending 28/2/10 and 28/2/11)

Turnover (R) Rate of tax

0 - 100 000 0%

100 001 - 300 000 1% of the amount over R100 000

300 001 - 500 000 R2 000 + 3% of the amount over R300 000

500 001 - 750 000 R8 000 + 5% of the amount over R500 000

750 001 - R20 500 + 7% of the amount over R750 000

12

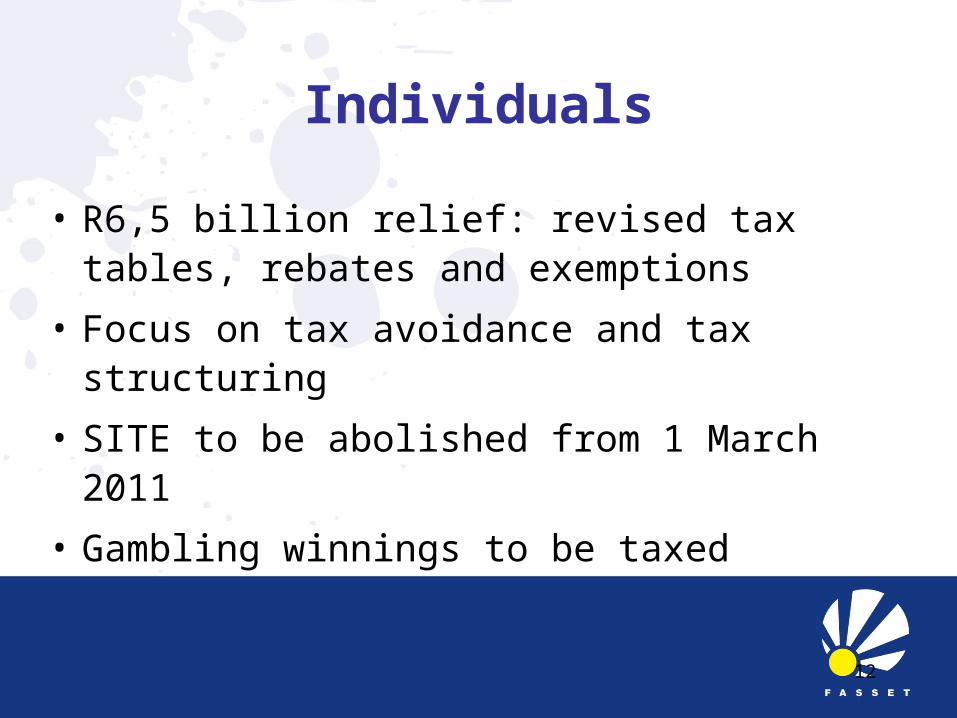

Individuals

• R6,5 billion relief: revised tax tables, rebates and exemptions

• Focus on tax avoidance and tax structuring

• SITE to be abolished from 1 March 2011

• Gambling winnings to be taxed

13

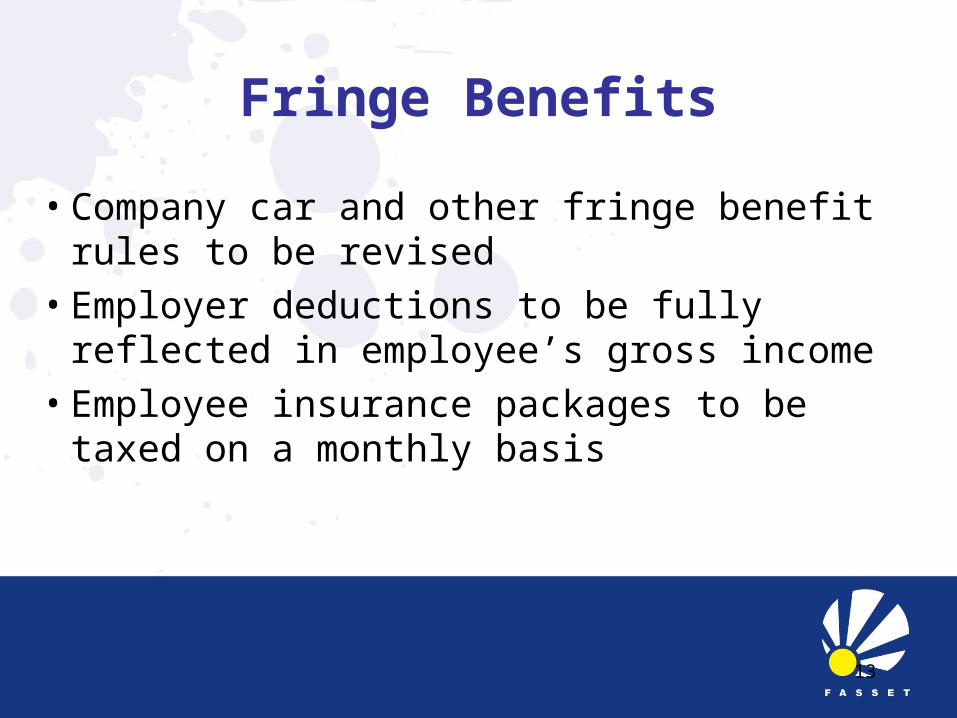

Fringe Benefits

• Company car and other fringe benefit rules to be revised

• Employer deductions to be fully reflected in employee’s gross income

• Employee insurance packages to be taxed on a monthly basis

14

Medical Aid Contributions

• Monthly caps to increase from R625 to R670 (7.2%) for each of the first

two beneficiaries and from R380 to R410 (7.9%) for each additional

beneficiary• Proposed conversion to a tax credit system

deferred until 2012/13

15

Lump Sum Gratuities

• R30 000* exemption to be merged into the retirement fund lump sum benefit system - aggregation principle will apply.

* Last adjusted in 1984

16

Subsistence Allowances • Travel in the Republic meals and incidental costs: R276 (was R260)

per day incidental costs only: R85 (was R80) per day

• Travel outside the Republic daily amount per country

17

Estate Duty

• Double tax on death: CGT and Estate Duty– Estate duty to be reviewed

18

Tax Administration

• Increased focus on enforcement and collections

• Level of tax compliance has "deteriorated”

• Third party information and "targeted lifestyle audits"

• Enhanced focus on "large taxpayers and high-net worth individuals”

19

Voluntary Disclosure Programme

• 1 Nov 2010 – 30 Oct 2011

• Some relief for Penalties Exchange control Criminal prosecution

20

VAT• Possible relief

for claw-back on temporary rentals by developers

renting of furnished residential accommodation

• 12-month claw-back rule to be relaxed on

deregistration (to avoid double-tax)

21

Youth Employment Grant

• Two-year cash grant For tax-compliant businesses, non-governmental

organisations and municipalities

22

Urban Development Zone (UDZ) Allowance

• New buildings: 20%(first year); 8% p.a. (next 10 yrs)

• Low cost housing in UDZ New buildings: 25% (first year); 13% (next 5 yrs);

10% (year 7) Improvements to existing buildings: 25% p.a.

• Enhanced allowances to be considered for private developers who improve another party's land

23

Dividends Tax• Definition of “dividend” to be refined• New definition of “foreign dividend” • Transitional issues • Practical problems relating to in specie dividends• Further refinements to the withholding system

where companies would pay dividend tax on a shareholder’s behalf

• Implementation 2011 (/2012?)

24

Corporate Tax• Attack on sophisticated tax avoidance schemes• Interest cost allocation for financial institutions• Offshore protected cell companies• Schemes channeling deductible amounts to

residents • Restricting the interest exemption for non-residents

investing in financial instruments other than South African bonds, unit trusts or publicly available interest bearing instruments

25

Headquarter Companies

• Exchange control and tax relief to be considered for various types of headquarter companies located in South Africa

26

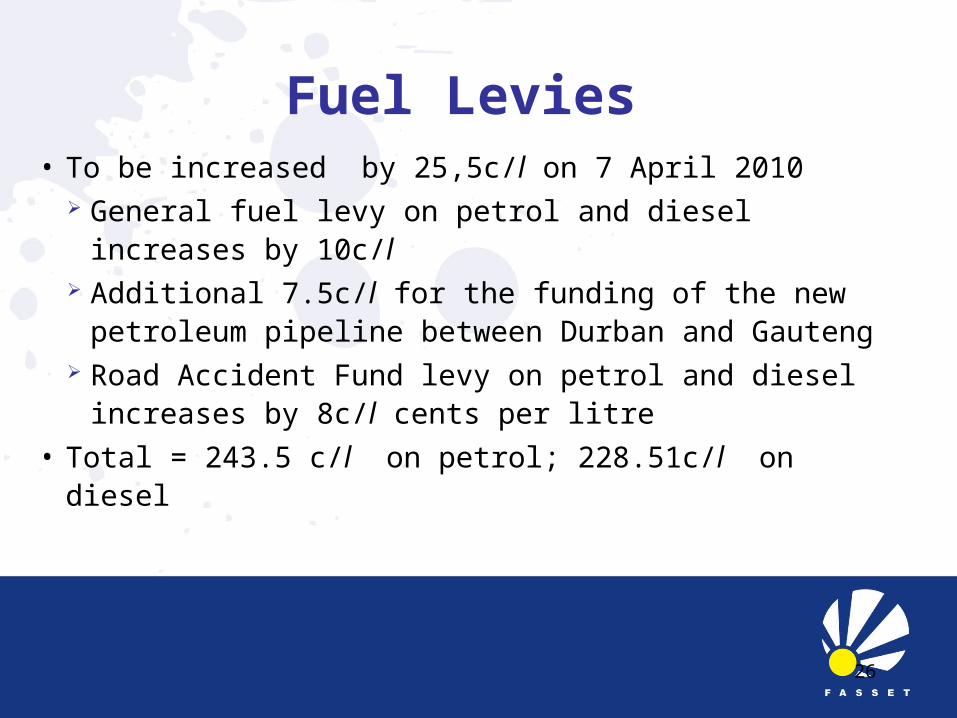

Fuel Levies • To be increased by 25,5c/l on 7 April 2010

General fuel levy on petrol and diesel increases by 10c/l

Additional 7.5c/l for the funding of the new petroleum pipeline between Durban and Gauteng

Road Accident Fund levy on petrol and diesel increases by 8c/l cents per litre

• Total = 243.5 c/l on petrol; 228.51c/l on diesel

27

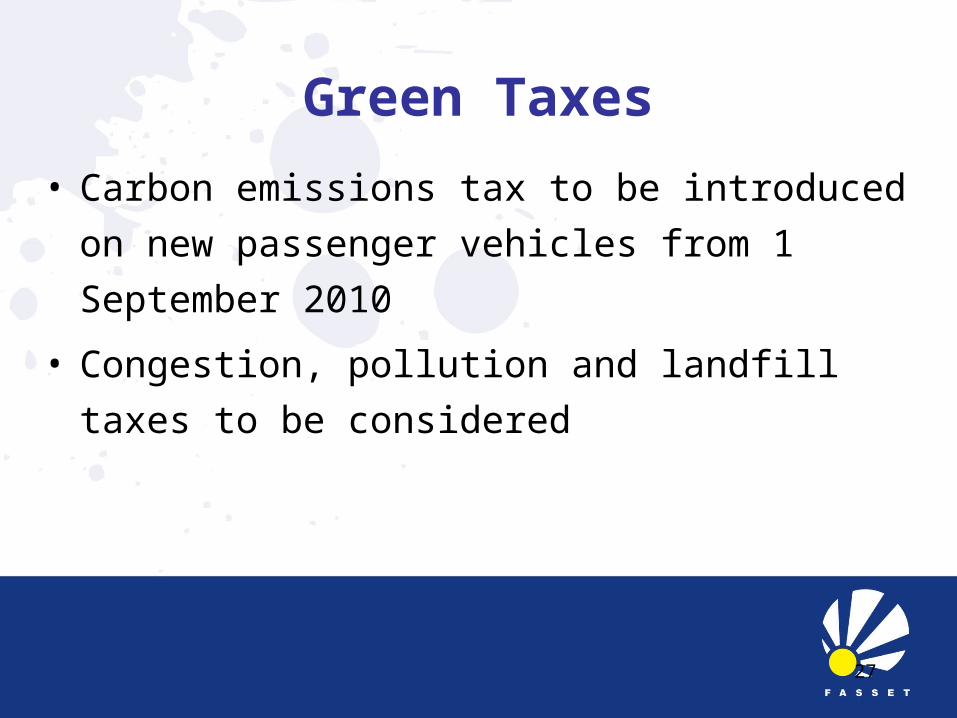

Green Taxes

• Carbon emissions tax to be introduced on new

passenger vehicles from 1 September 2010

• Congestion, pollution and landfill taxes to be

considered

28

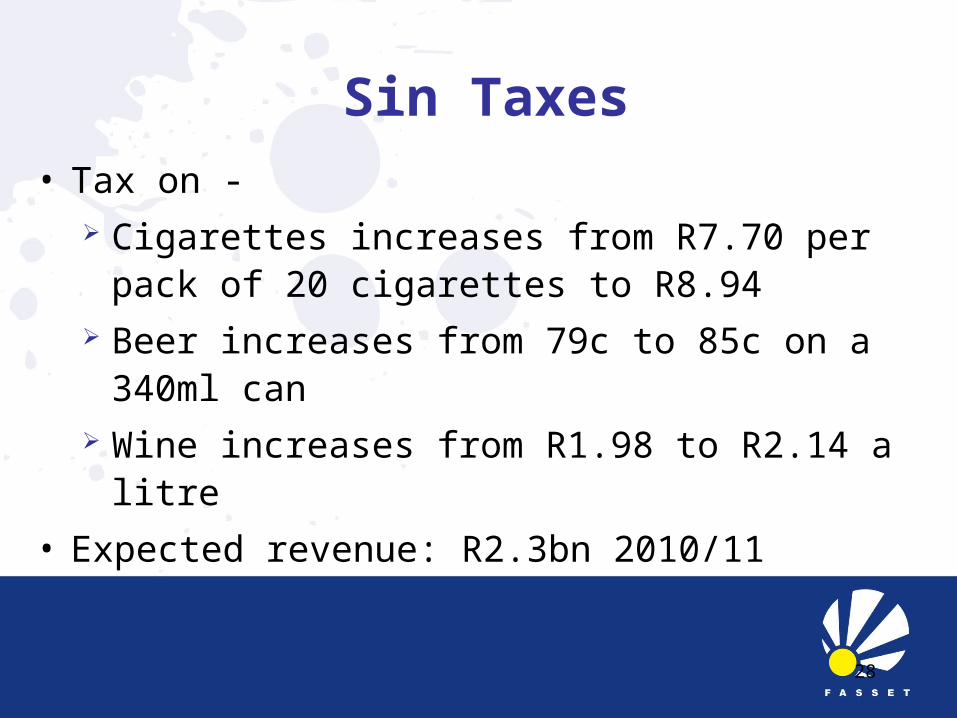

Sin Taxes

• Tax on - Cigarettes increases from R7.70 per pack of 20

cigarettes to R8.94 Beer increases from 79c to 85c on a 340ml can Wine increases from R1.98 to R2.14 a litre

• Expected revenue: R2.3bn 2010/11

29

2009 AMENDMENTS

30

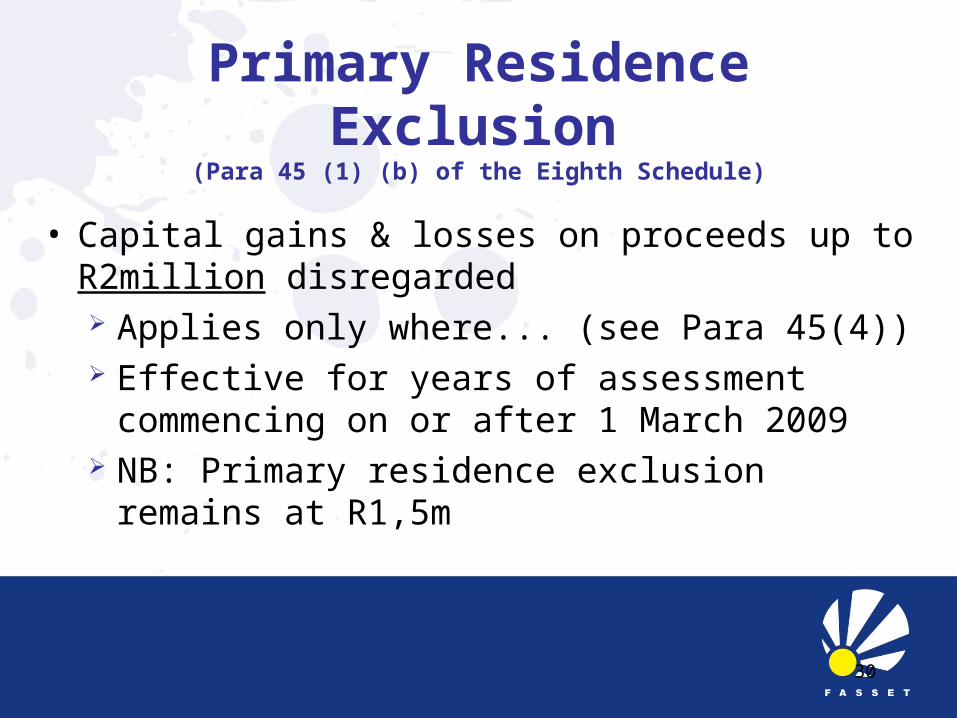

Primary Residence Exclusion

(Para 45 (1) (b) of the Eighth Schedule)

• Capital gains & losses on proceeds up to R2million disregarded Applies only where... (see Para 45(4)) Effective for years of assessment commencing

on or after 1 March 2009 NB: Primary residence exclusion remains at

R1,5m

31

Travel Allowance: Repeal of Deemed Kilometer Method

(S 8 (1)(b)(ii) & Para. 1 of the Fourth Schedule)

• The deemed kilometre method (first 18 000 km traveled per year deemed to be private travel) to be repealed from 1 March 2010

• Amount included in “remuneration” increased from 60% to 80%– from 1 March 2010

• Can still claim business travel expenses for actual kilometers recorded in a log book

32

Conversion of the STC to Dividend Withholding Tax

• 10% tax on dividends will fall on the shareholders

• A number of exemptions (e.g. pension funds; company-to-company)

• Treaty reductions (5% on re-negotiated DTAs)

33

Conversion of the STC to Dividend Withholding Tax

• Withholding obligation on the company payer (or a

regulated intermediary)

• New definition of “dividend” and “contributed tax

capital”

• Anti-avoidance rules will become effective on

implementation

34

Controlled Foreign Companies (S 9D)

“Foreign Business Establishment” definition • Fixed place• Located outside South Africa• Conducted continuously and regularly• Takes into account certain activities of CFC group

members if located in the same foreign country

35

Controlled Foreign Companies (S 9D)

“Foreign Business Establishment” definition

• Establishment located in foreign country solely or mainly for non-tax avoidance reasons

High tax jurisdictions

• CFCs will be exempt from tax in SA if subject to high foreign country taxes

36

Depreciation on Improvements (ss 11D, 12B, 12C, 12D(2), 12F, 12I and 37B)

• Amendments clarify that the depreciation allowance applies equally to improvements associated with underlying assets. Depreciation of improvements should be determined as if the improvement were a stand-alone asset.

37

Depreciation on Improvements (ss 11D, 12B, 12C, 12D(2), 12F, 12I and 37B)

• Effective for expenditure incurred in respect of years of assessment ending on or after 1 January 2010

38

Lease Improvements Allowance (s 11(g))

• The prohibition against deducting improvements where the lessor is tax-exempt will no longer apply if: – (i) the lessee is leasing land or buildings owned

directly by government (national, provincial or municipal) or indirectly by government (through institutions exempt in terms of section 10(1)(cA) and section 10(1)(t)); and

39

Lease Improvements Allowance (s 11(g))

• The prohibition against deducting improvements where the lessor is tax-exempt will no longer apply if: – (ii) the lease is of a duration of 20 years or

more. • Effective for improvements brought into use on or

after 1 January 2009

40

Pre-Trade Expenses (s 11A)

• S 24J expenditure now included

• Effective for years of assessment ending on or after 1 January 2005 (backdated)

41

Small Business Corporations (S 12E(4)(a)(ii)(hh); para 3(f)(iii) of the Sixth Schedule)

• Inactive or dormant shelf companies added to the list of permitted investments

– A shelf company is inactive or dormant until the company trades or holds assets exceeding R5 000

• Effective for years of assessment ending on or after 1 January 2010

42

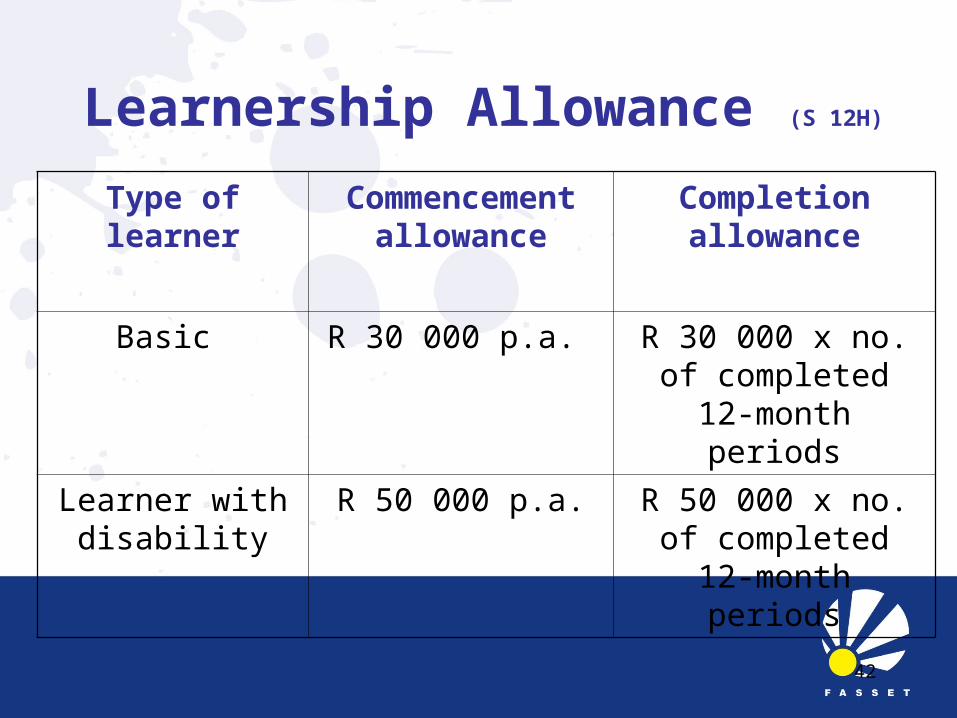

Learnership Allowance (S 12H)

Type of learner Commencement allowance

Completion allowance

Basic R 30 000 p.a. R 30 000 x no. of completed 12-month

periods

Learner with disability

R 50 000 p.a. R 50 000 x no. of completed 12-month

periods

43

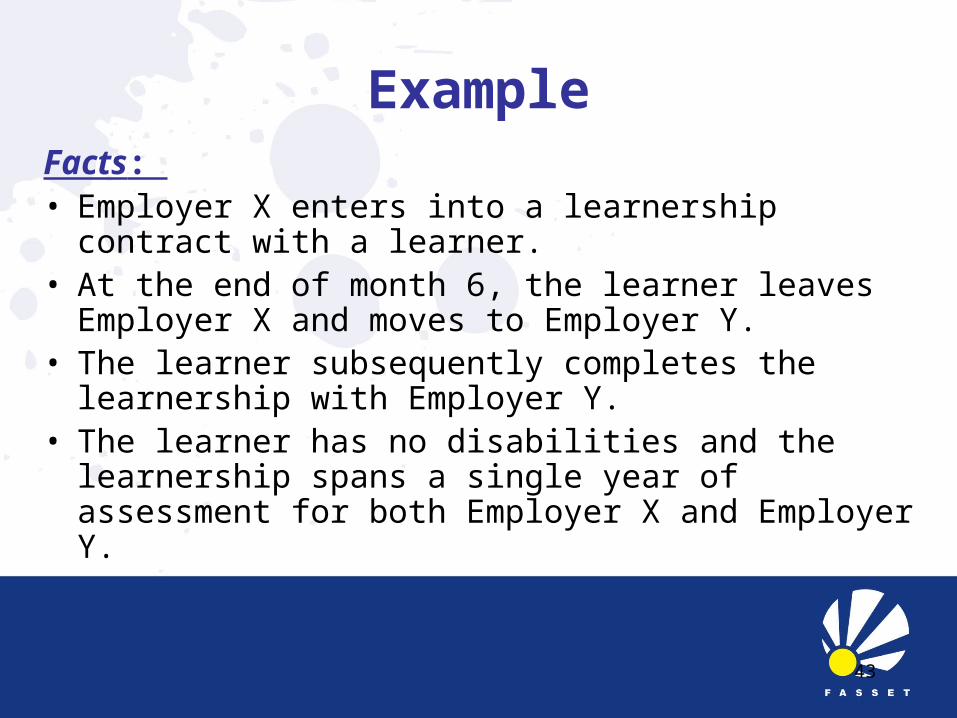

Facts: • Employer X enters into a learnership contract with a

learner. • At the end of month 6, the learner leaves Employer X

and moves to Employer Y. • The learner subsequently completes the learnership

with Employer Y. • The learner has no disabilities and the learnership

spans a single year of assessment for both Employer X and Employer Y.

Example

44

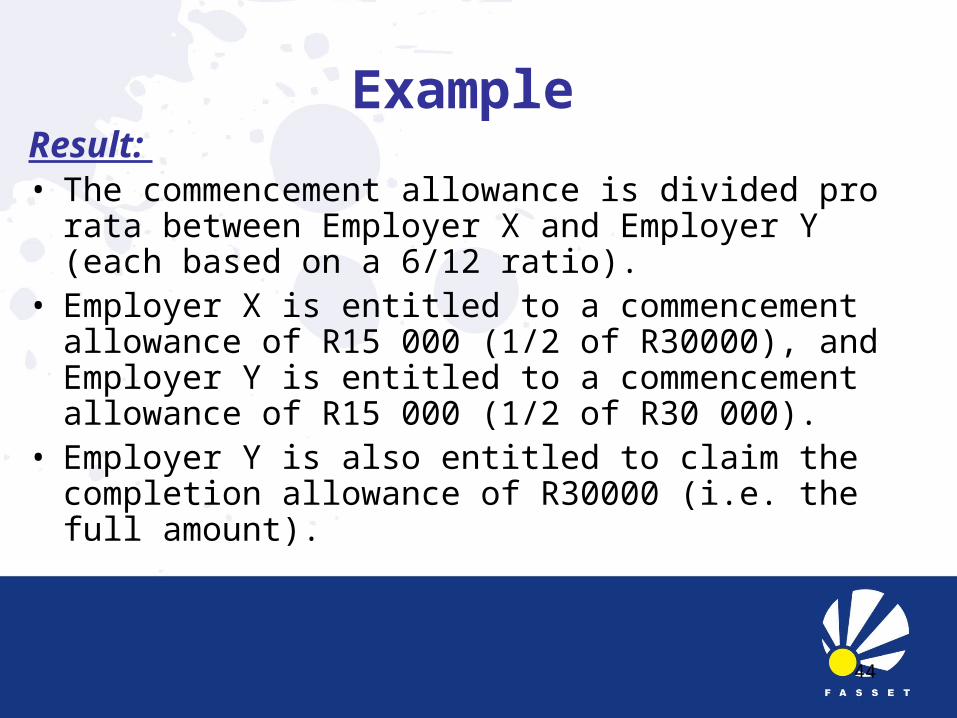

Example Result: • The commencement allowance is divided pro rata

between Employer X and Employer Y (each based on a 6/12 ratio).

• Employer X is entitled to a commencement allowance of R15 000 (1/2 of R30000), and Employer Y is entitled to a commencement allowance of R15 000 (1/2 of R30 000).

• Employer Y is also entitled to claim the completion allowance of R30000 (i.e. the full amount).

45

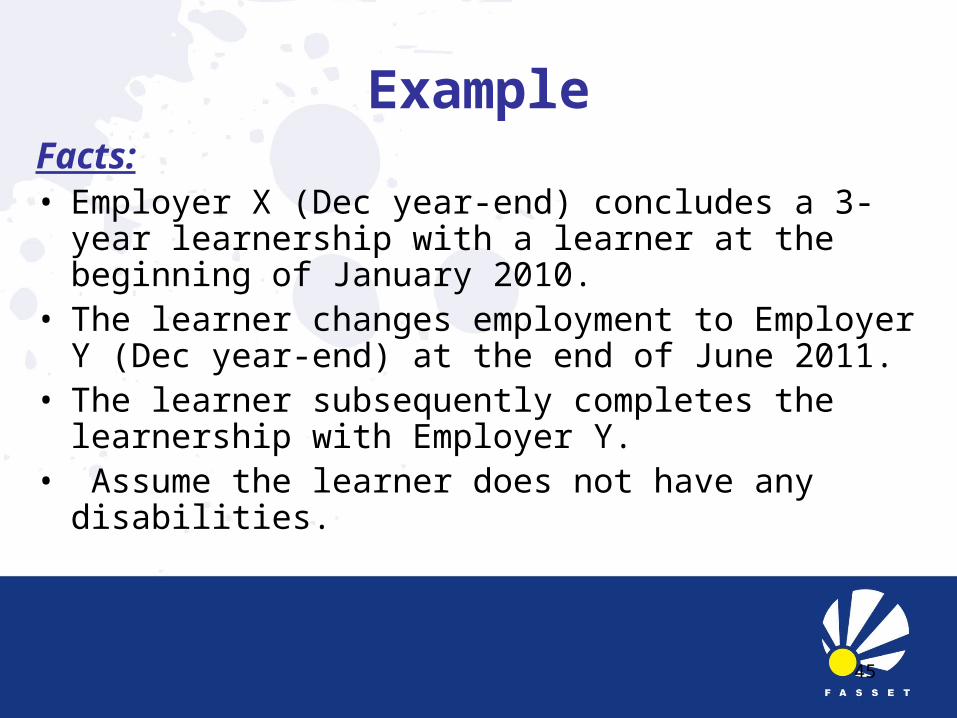

Facts: • Employer X (Dec year-end) concludes a 3-year

learnership with a learner at the beginning of January 2010.

• The learner changes employment to Employer Y (Dec year-end) at the end of June 2011.

• The learner subsequently completes the learnership with Employer Y.

• Assume the learner does not have any disabilities.

Example

46

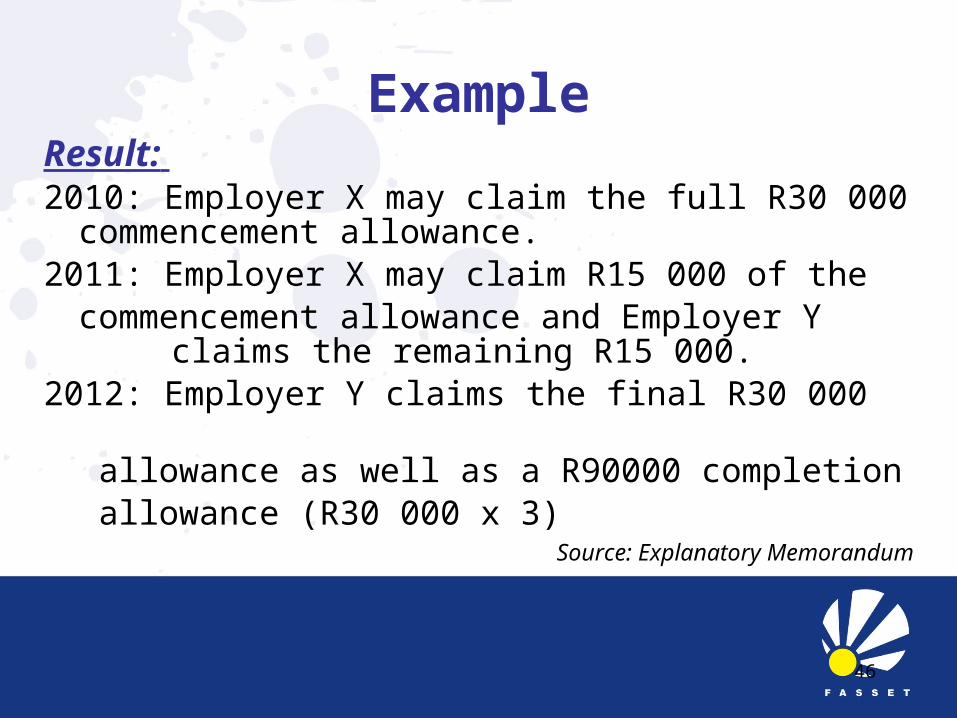

ExampleResult: 2010: Employer X may claim the full R30 000

commencement allowance. 2011: Employer X may claim R15 000 of the

commencement allowance and Employer Y claims the remaining R15 000.

2012: Employer Y claims the final R30 000 allowance as well as a R90000 completion allowance (R30 000 x 3)

Source: Explanatory Memorandum

47

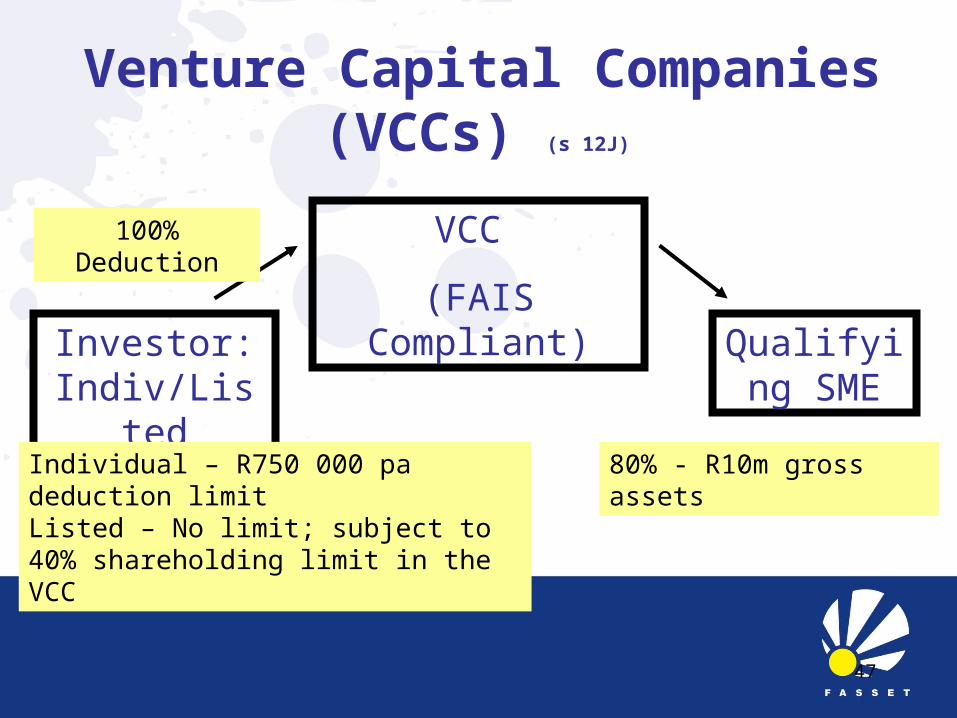

Venture Capital Companies (VCCs) (s 12J)

VCC

(FAIS Compliant)Investor:

Indiv/ListedQualifying

SME

Individual – R750 000 pa deduction limitListed – No limit; subject to 40% shareholding limit in the VCC

80% - R10m gross assets

100% Deduction

48

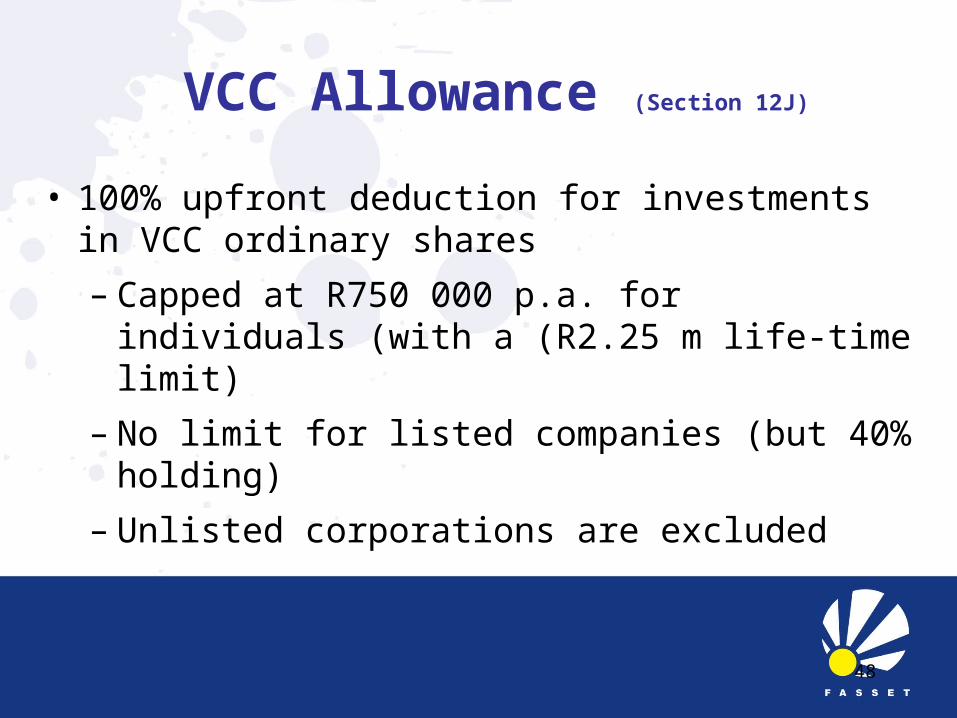

VCC Allowance (Section 12J)

• 100% upfront deduction for investments in VCC ordinary shares

– Capped at R750 000 p.a. for individuals (with a (R2.25 m life-time limit)

– No limit for listed companies (but 40% holding)

– Unlisted corporations are excluded

49

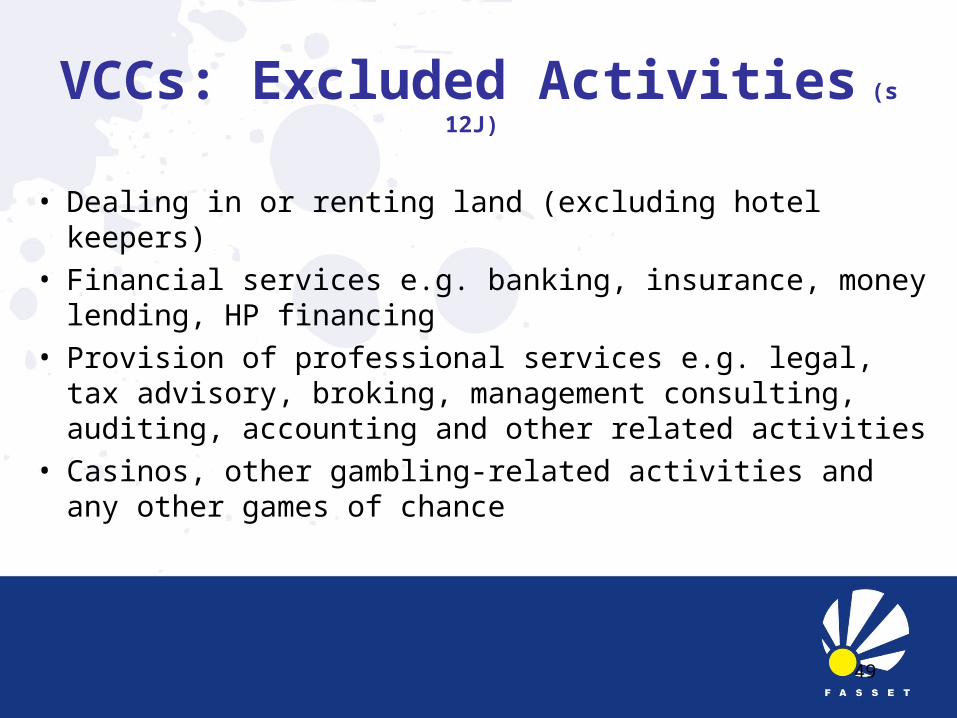

VCCs: Excluded Activities (s 12J)

• Dealing in or renting land (excluding hotel keepers)

• Financial services e.g. banking, insurance, money lending, HP financing

• Provision of professional services e.g. legal, tax advisory, broking, management consulting, auditing, accounting and other related activities

• Casinos, other gambling-related activities and any other games of chance

50

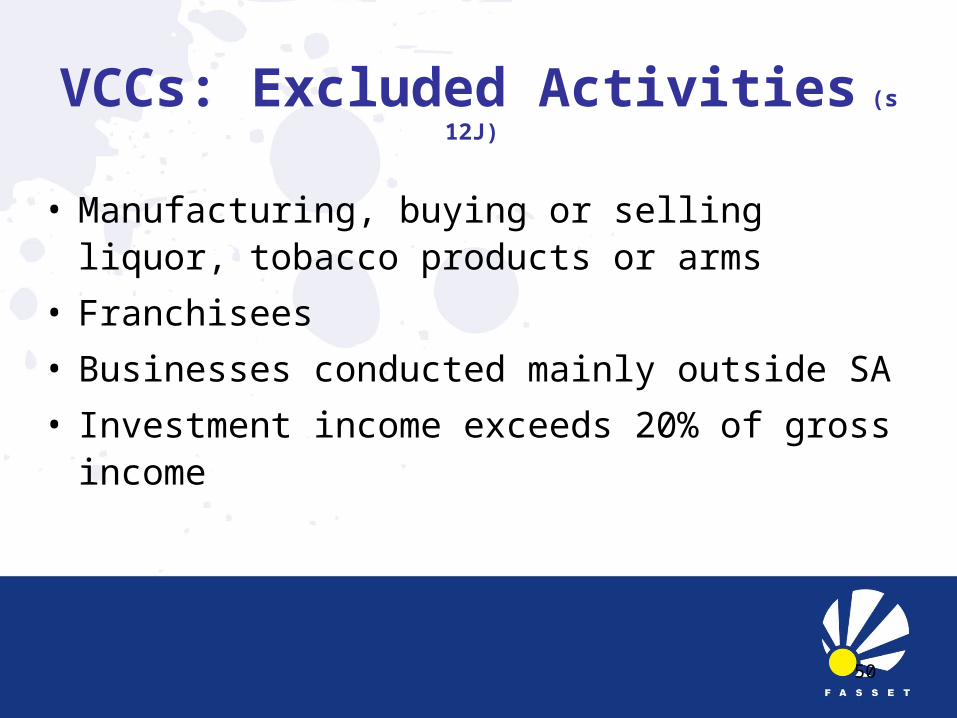

VCCs: Excluded Activities (s 12J)

• Manufacturing, buying or selling liquor, tobacco products or arms

• Franchisees

• Businesses conducted mainly outside SA

• Investment income exceeds 20% of gross income

51

Exemption of Certified Emission Reductions (S 12K)

• CERs represent emission reductions that are verified and certified by the Department of Energy

• Disposals of CERs are exempt from income tax in respect of any person that carries the Clean Development Mechanism (CDM) project registration and implements that project

• Effective from 11 February 2009 and applies in respect of disposals on or after that date

52

Energy Efficiency Allowance (S 12L)

• Annual notional allowance for energy savings achieved in the production of income

– South African National Energy Development Institute (SANEDI) energy savings certificate required

53

Energy Efficiency Allowance (S 12L)

• Basic formula - Energy efficiency

Savings in kWh (x) Applied rate2 (or a number by the Minister)

(Comes into operation on a date determined by the Minister of Finance by notice in the Gazette)

54

Employer-Provided Post-Retirement Medical Aid (S 12M)

• Lump sum payment of post-retirement medical scheme contributions to retired employees (or their spouses/dependants) or to an insurer is deductible when paid

– Applies to post-retirement medical scheme lump sums paid on or after 1 September 2009

55

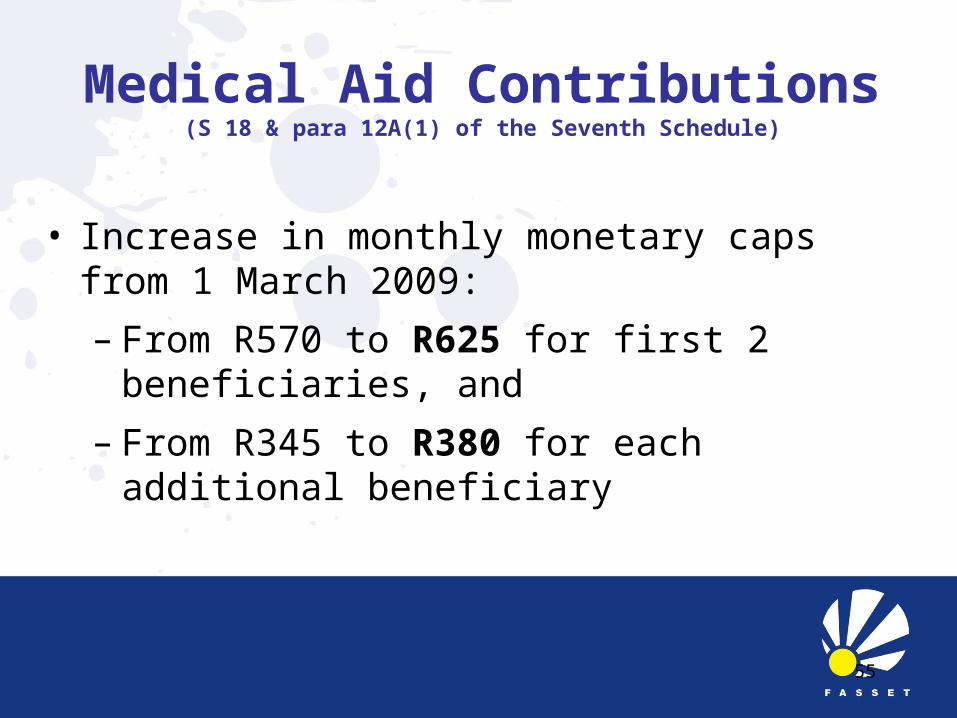

Medical Aid Contributions(S 18 & para 12A(1) of the Seventh Schedule)

• Increase in monthly monetary caps from 1 March 2009:

– From R570 to R625 for first 2 beneficiaries, and

– From R345 to R380 for each additional beneficiary

56

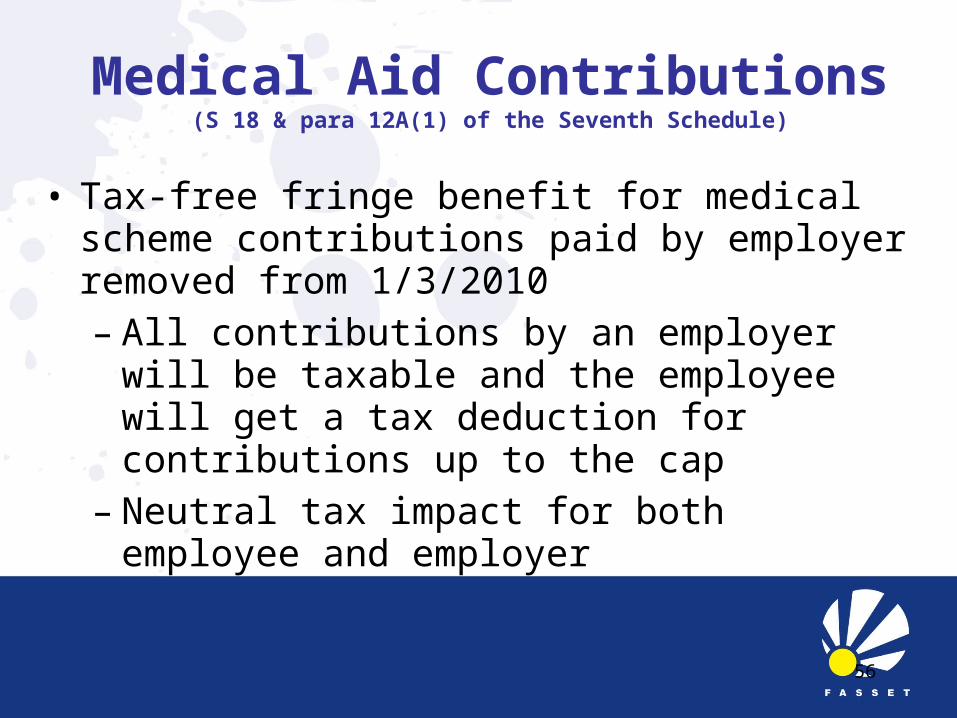

Medical Aid Contributions(S 18 & para 12A(1) of the Seventh Schedule)

• Tax-free fringe benefit for medical scheme contributions paid by employer removed from 1/3/2010– All contributions by an employer will be taxable

and the employee will get a tax deduction for contributions up to the cap

– Neutral tax impact for both employee and employer

57

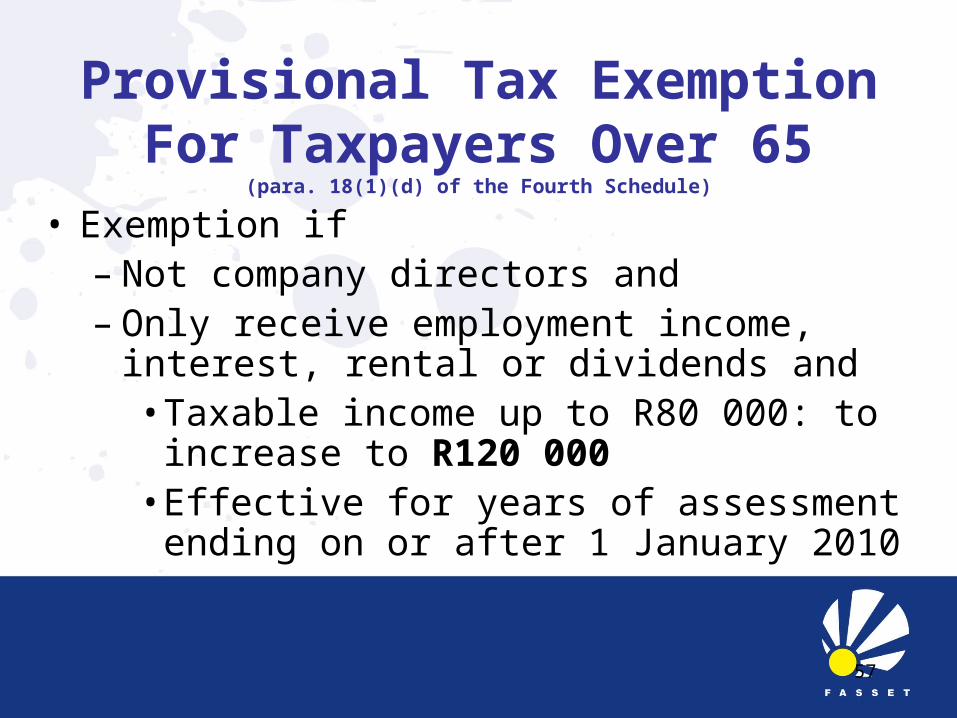

Provisional Tax Exemption For Taxpayers Over 65

(para. 18(1)(d) of the Fourth Schedule)

• Exemption if– Not company directors and – Only receive employment income, interest,

rental or dividends and• Taxable income up to R80 000: to increase

to R120 000• Effective for years of assessment ending on

or after 1 January 2010

58

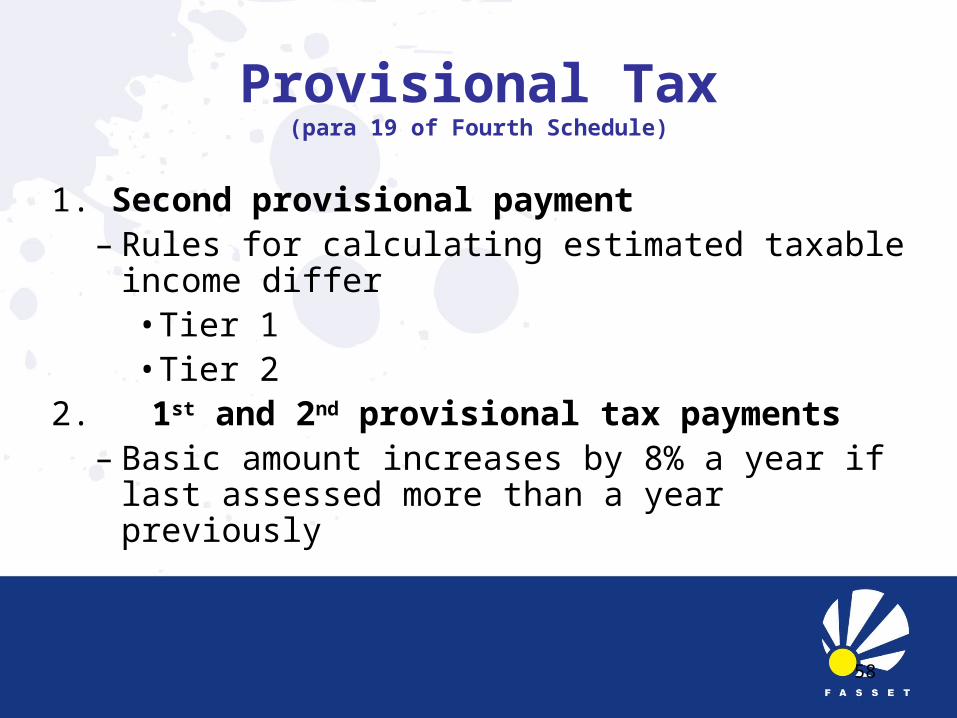

Provisional Tax(para 19 of Fourth Schedule)

1. Second provisional payment– Rules for calculating estimated taxable income

differ• Tier 1• Tier 2

2. 1st and 2nd provisional tax payments– Basic amount increases by 8% a year if last

assessed more than a year previously

59

Tier One - Smaller Taxpayers (to up to R1million ) )

• Largely reverts to previous basis

• No penalty if estimate of taxable income is at least equal to the lesser of -

- The basic amount (adjusted) or

• 90% of actual taxable income for the year

60

Tier One - Smaller Taxpayers (to up to R1million )

• Penalty of 20% of the shortfall if the estimated TI is below this level

• Unless the estimate ‘‘was seriously calculated with due regard to the factors having a bearing thereon or was not deliberately or negligently understated’’

61

Tier Two - Larger Taxpayers

• Estimated taxable income must be equal to at least 80% of actual taxable income for the year

• 20% penalty of the shortfall if the estimate does not reach this level

• Unless the estimate was ‘‘seriously calculated…(etc)”

62

Residential Accommodation Fringe Benefit

(para 9 of the Seventh Schedule)

• “B” in the formula increases from R46 000 to

R54 200

– Effective for years of assessment ending on or after

1 January 2010

63

Transfer of Properties Out of Companies and Trusts

(S 9(20) of the Transfer Duty Act, para 51 of the Eighth Schedule, s64B(5)(k))

• Until 31/12/2011 a distribution of a domestic residence from a company or trust to a sole shareholder is treated as a CGT ‘roll-over event’

• The distribution is exempt from STC and transfer duty

• Certain requirements must be met

64

Requirements to Qualify(Para 51 of the Eighth Schedule)

• Transfer of an interest in a residence from a company or trust to an individual who:

– Acquires that interest no later than 31/12/2011

– Lived (alone or with his/her spouse) in that residence and used it mainly for domestic purposes from 11/2/09 until date of transfer

– Directly held 100% of share capital or members’ interest in the company (alone or with spouse) from 11/2/09 to date of registration in his/her/spouse’s name

• OR donated or sold that residence to the trust (or financed expenditure)

65

Case Law

• Anglovaal v SARS (411/08) [2009] ZASCA 109Whether shares were acquired as a capital investment orTrading stock

• Fourie Beleggings v CSARS (168/08) [2009] ZASCA 37Payment in compensation for cancellation of a contract wasnot capital nature

• Grundlingh v CSARS [2009] SAFSHC 88Whether partnership income from Lesotho was taxable in South Africa

66

Thank-you

Fasset Call Centre

086 101 0001

www.fasset.org.za