Embed Size (px)

Citation preview

1

2004 Half Year Results Wednesday, 26 May 2004

2004 Half Year Results Wednesday, 26 May 2004

2

Andrew Lindberg

Managing Director, AWB Limited

3

Content

• Result highlights

• Financial performance (CFO)

• Business operations

• Landmark integration

• Strategy

• Outlook

4

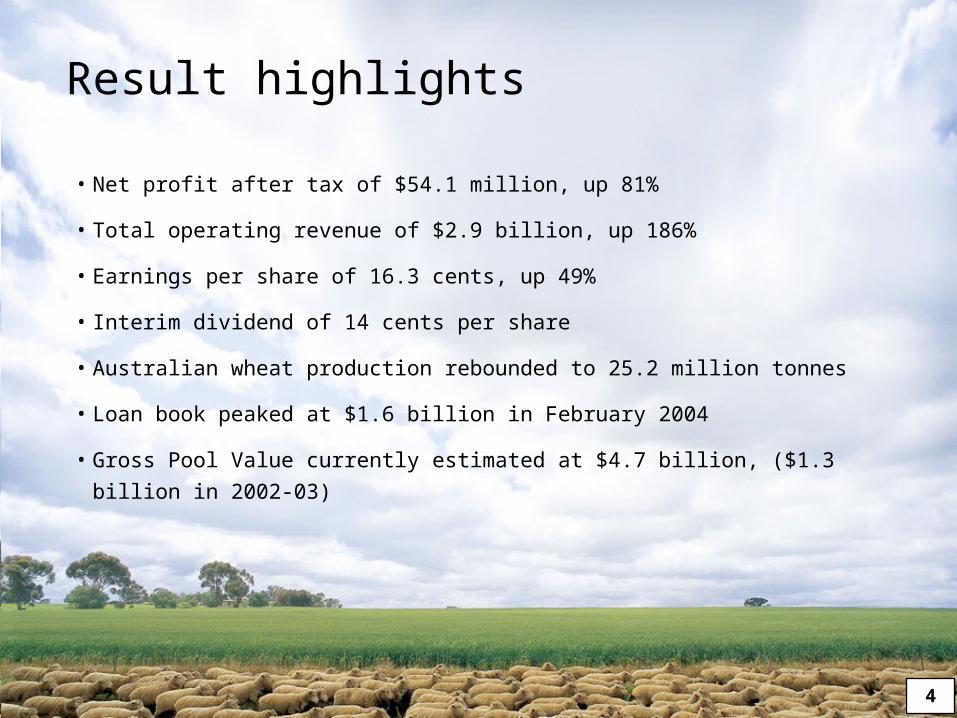

• Net profit after tax of $54.1 million, up 81%

• Total operating revenue of $2.9 billion, up 186%

• Earnings per share of 16.3 cents, up 49%

• Interim dividend of 14 cents per share

• Australian wheat production rebounded to 25.2 million tonnes

• Loan book peaked at $1.6 billion in February 2004

• Gross Pool Value currently estimated at $4.7 billion, ($1.3 billion in 2002-03)

Result highlights

5

Paul Ingleby

Chief Financial Officer

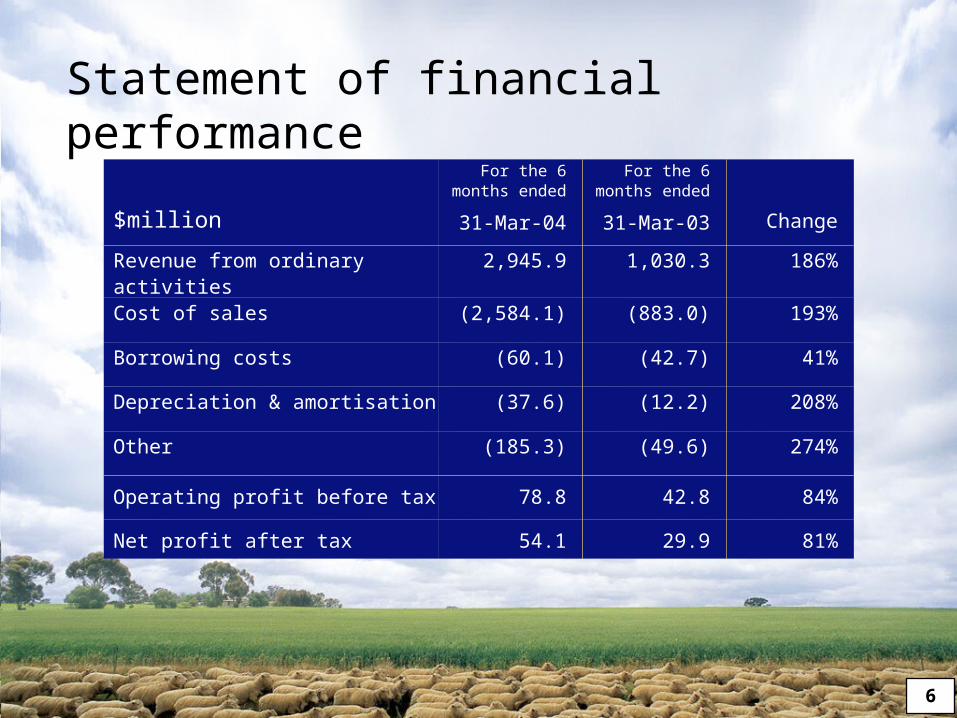

6

$million

For the 6 months ended

31-Mar-04

For the 6 months ended

31-Mar-03 Change

Revenue from ordinary activities 2,945.9 1,030.3 186%

Cost of sales (2,584.1) (883.0) 193%

Borrowing costs (60.1) (42.7) 41%

Depreciation & amortisation (37.6) (12.2) 208%

Other (185.3) (49.6) 274%

Operating profit before tax 78.8 42.8 84%

Net profit after tax 54.1 29.9 81%

Statement of financial performance

7

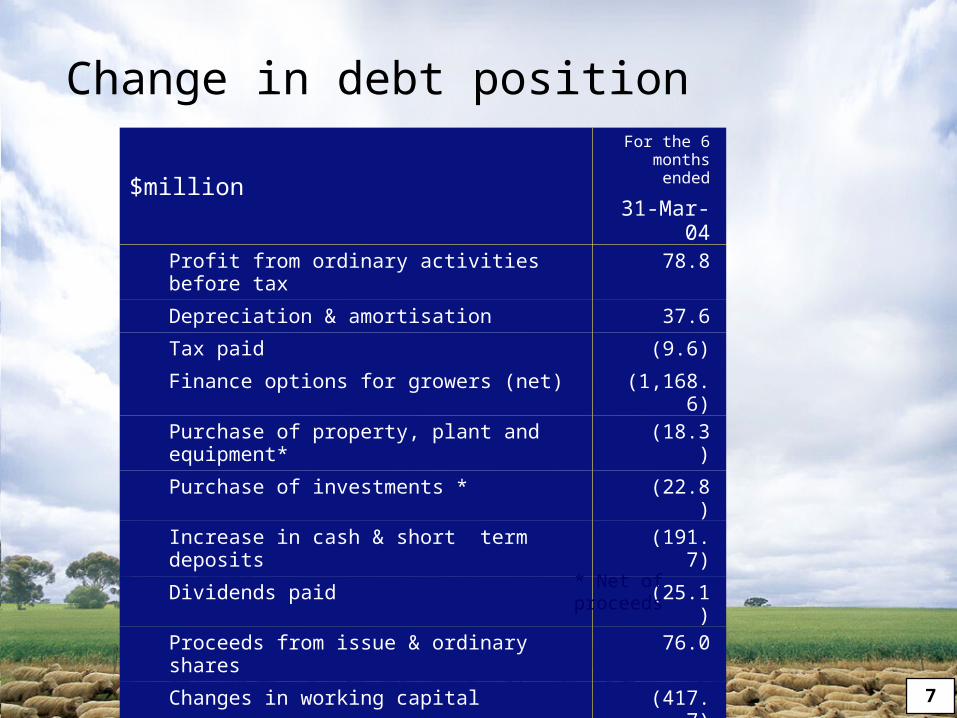

$million

For the 6 months ended

31-Mar-04

Profit from ordinary activities before tax 78.8

Depreciation & amortisation 37.6

Tax paid (9.6)

Finance options for growers (net) (1,168.6)

Purchase of property, plant and equipment* (18.3)

Purchase of investments * (22.8)

Increase in cash & short term deposits (191.7)

Dividends paid (25.1)

Proceeds from issue & ordinary shares 76.0

Changes in working capital (417.7)

Change in debt – (increase) / decrease (1,661.3)

* Net of proceeds

Change in debt position

8

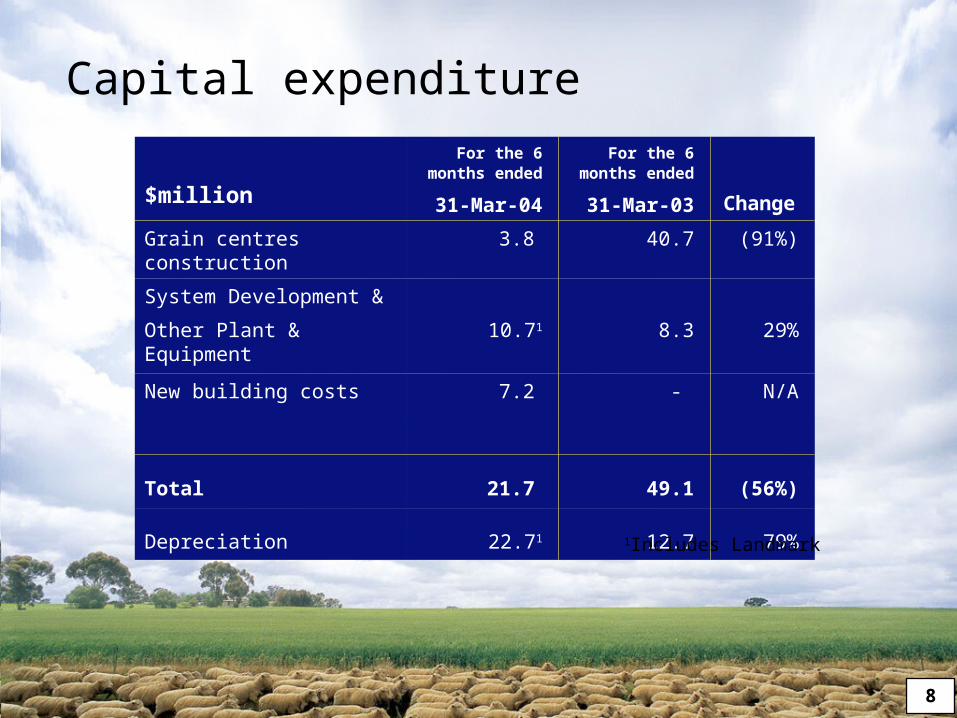

$million

For the 6 months ended

31-Mar-04

For the 6 months ended

31-Mar-03 Change

Grain centres construction 3.8 40.7 (91%)

System Development &

Other Plant & Equipment 10.71 8.3 29%

New building costs

7.2 - N/A

Total 21.7 49.1 (56%)

Depreciation 22.71 12.7 79%

1Includes Landmark

Capital expenditure

9

$million As at 31-Mar-04

As at 30-Sep-03

Assets

Cash 28.8 54.8

Receivables 2,523.4 1,012.6

Intangibles 576.9 583.6

Investments 16.2 12.9

Inventories 332.9 185.4

Property, plant & equipment 296.9 300.4

Other 520.0 266.2

4,295.1 2,415.9

Liabilities

Payables 444.2 336.0

Interest bearing liabilities 2,740.0 1,062.9

Provisions 49.0 52.4

Other 28.2 32.6

3,261.4 1,483.9

Net Assets 1,033.7 932.0

Statement of financial position

10

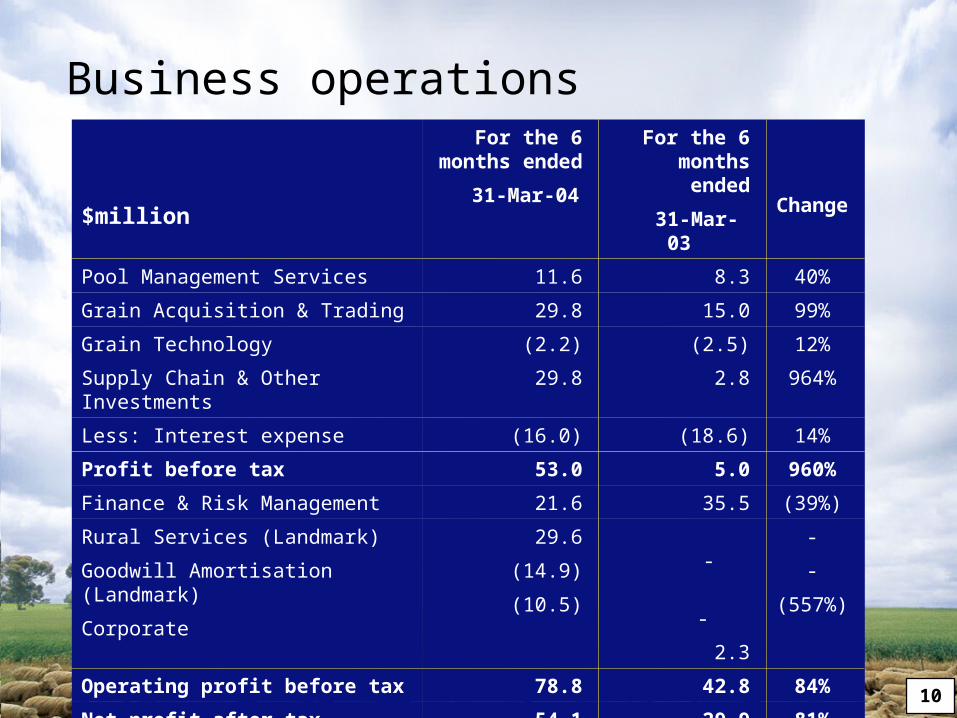

$million

For the 6 months ended

31-Mar-04

For the 6 months ended

31-Mar-03 Change

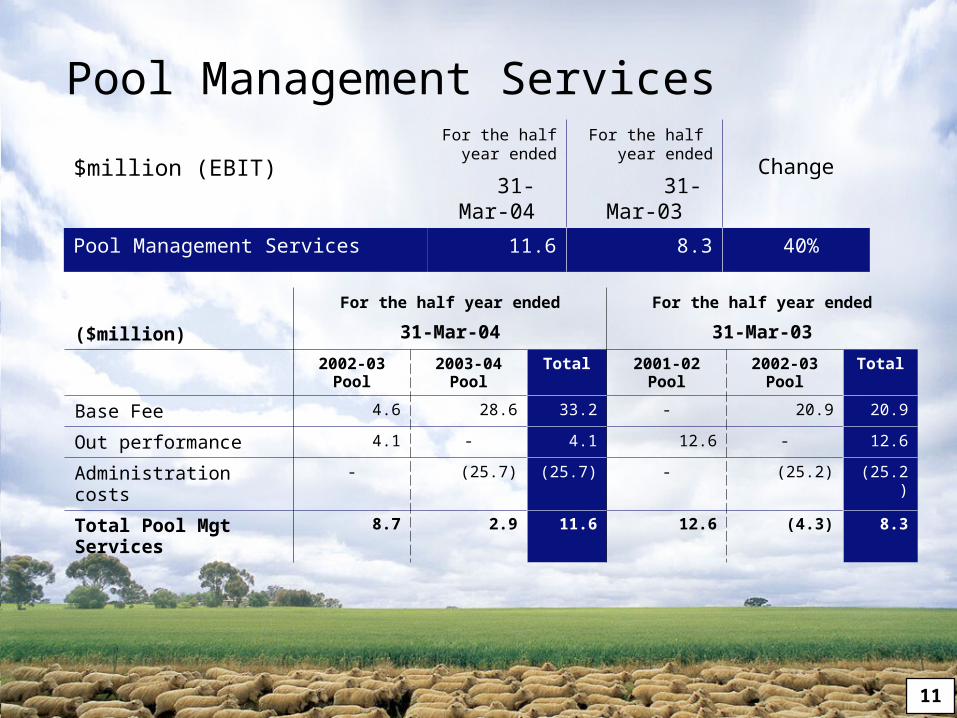

Pool Management Services 11.6 8.3 40%

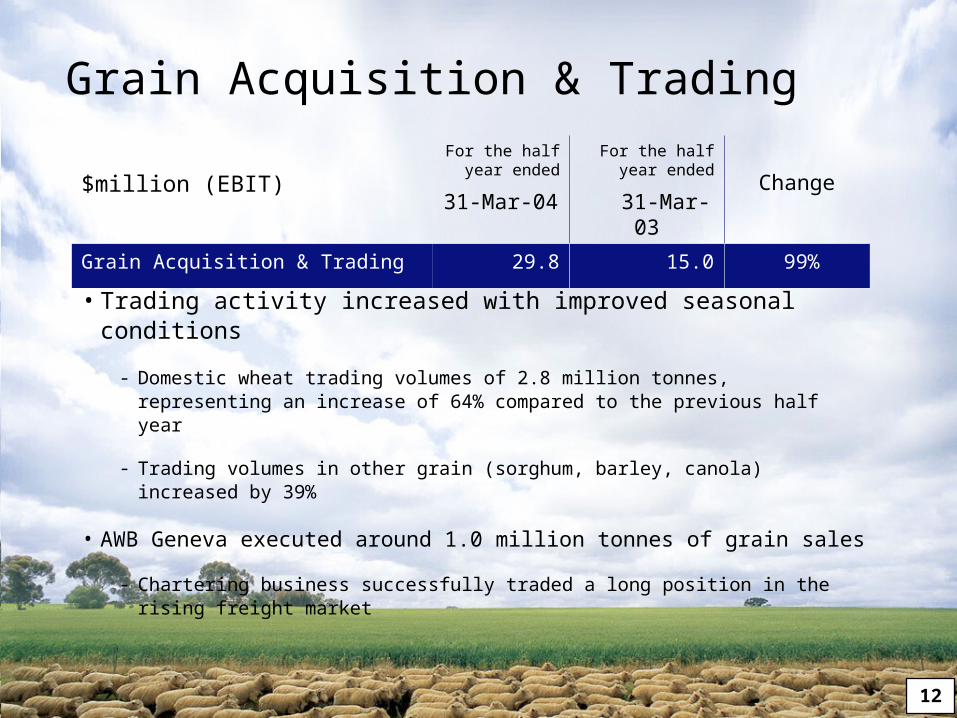

Grain Acquisition & Trading 29.8 15.0 99%

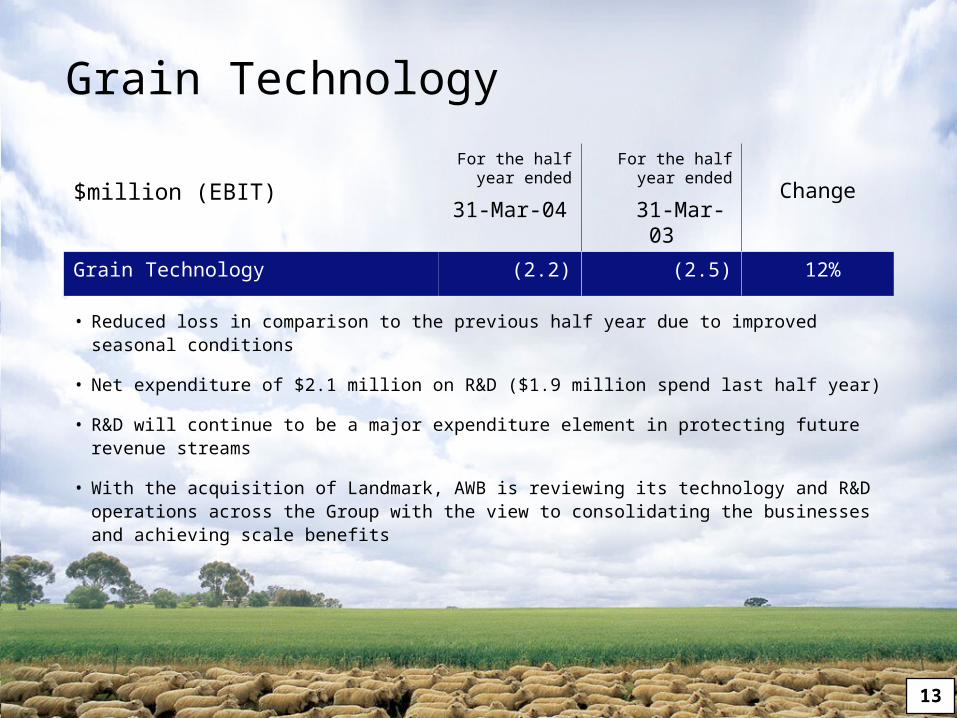

Grain Technology (2.2) (2.5) 12%

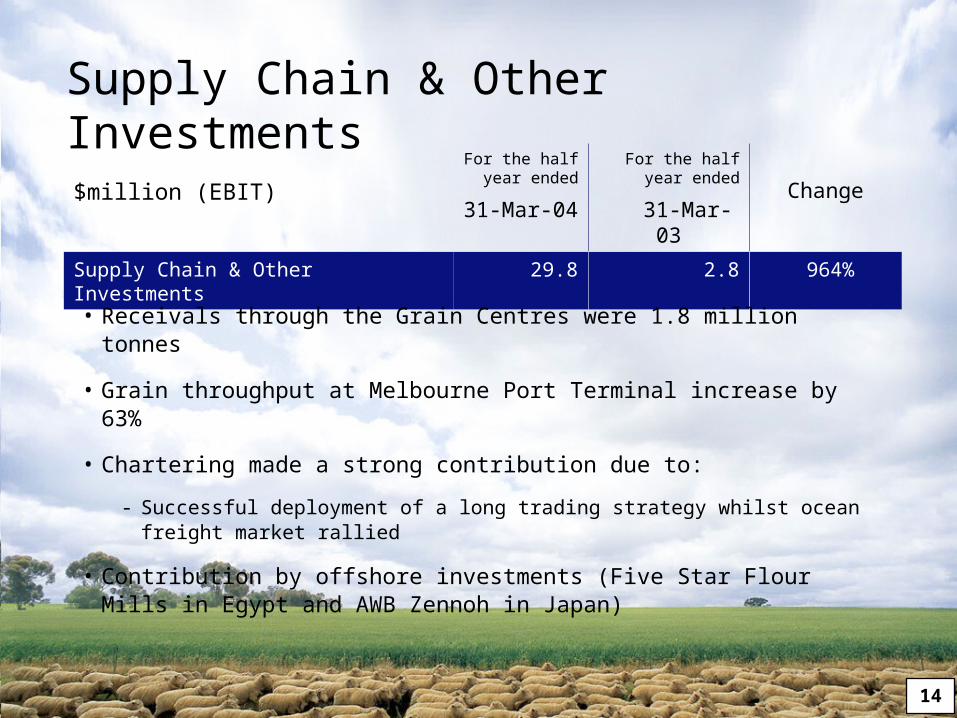

Supply Chain & Other Investments 29.8 2.8 964%

Less: Interest expense (16.0) (18.6) 14%

Profit before tax 53.0 5.0 960%

Finance & Risk Management 21.6 35.5 (39%)

Rural Services (Landmark)

Goodwill Amortisation (Landmark)

Corporate

29.6

(14.9)

(10.5)

-

-

2.3

-

-

(557%)

Operating profit before tax 78.8 42.8 84%

Net profit after tax 54.1 29.9 81%

Business operations

11

$million (EBIT)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03Change

Pool Management Services 11.6 8.3 40%

($million)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03

2002-03 Pool

2003-04 Pool

Total 2001-02 Pool 2002-03 Pool

Total

Base Fee 4.6 28.6 33.2 - 20.9 20.9

Out performance 4.1 - 4.1 12.6 - 12.6

Administration costs - (25.7) (25.7) - (25.2) (25.2)

Total Pool Mgt Services

8.7 2.9 11.6 12.6 (4.3) 8.3

Pool Management Services

12

$million (EBIT)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03Change

Grain Acquisition & Trading 29.8 15.0 99%

• Trading activity increased with improved seasonal conditions

- Domestic wheat trading volumes of 2.8 million tonnes, representing an increase of 64% compared to the previous half year

- Trading volumes in other grain (sorghum, barley, canola) increased by 39%

• AWB Geneva executed around 1.0 million tonnes of grain sales

- Chartering business successfully traded a long position in the rising freight market

Grain Acquisition & Trading

13

$million (EBIT)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03Change

Grain Technology (2.2) (2.5) 12%

Grain Technology

• Reduced loss in comparison to the previous half year due to improved seasonal conditions

• Net expenditure of $2.1 million on R&D ($1.9 million spend last half year)

• R&D will continue to be a major expenditure element in protecting future revenue streams

• With the acquisition of Landmark, AWB is reviewing its technology and R&D operations across the Group with the view to consolidating the businesses and achieving scale benefits

14

$million (EBIT)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03Change

Supply Chain & Other Investments 29.8 2.8 964%

• Receivals through the Grain Centres were 1.8 million tonnes

• Grain throughput at Melbourne Port Terminal increase by 63%

• Chartering made a strong contribution due to:

- Successful deployment of a long trading strategy whilst ocean freight market rallied

• Contribution by offshore investments (Five Star Flour Mills in Egypt and AWB Zennoh in Japan)

Supply Chain & Other Investments

15

$million (PBT)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03Change

Finance & Risk Management 21.6 35.5 (39%)

• Impacted by reduced contribution from Group funding due to surplus capital utilised for the acquisition of Landmark

• Contribution by Financial Services increased 50% to an EBIT of $14.8 million mainly due to seasonal conditions

• The level of underwriting revenue and take up of products increased significantly

Finance & Risk Management

16

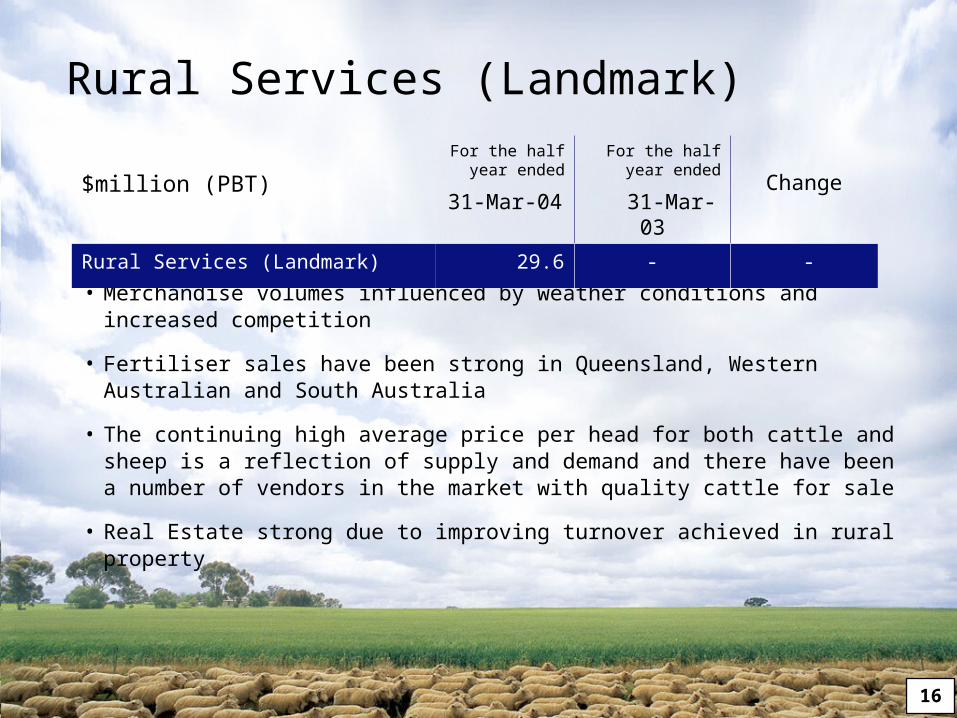

• Merchandise volumes influenced by weather conditions and increased competition

• Fertiliser sales have been strong in Queensland, Western Australian and South Australia

• The continuing high average price per head for both cattle and sheep is a reflection of supply and demand and there have been a number of vendors in the market with quality cattle for sale

• Real Estate strong due to improving turnover achieved in rural property

$million (PBT)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03Change

Rural Services (Landmark) 29.6 - -

Rural Services (Landmark)

17

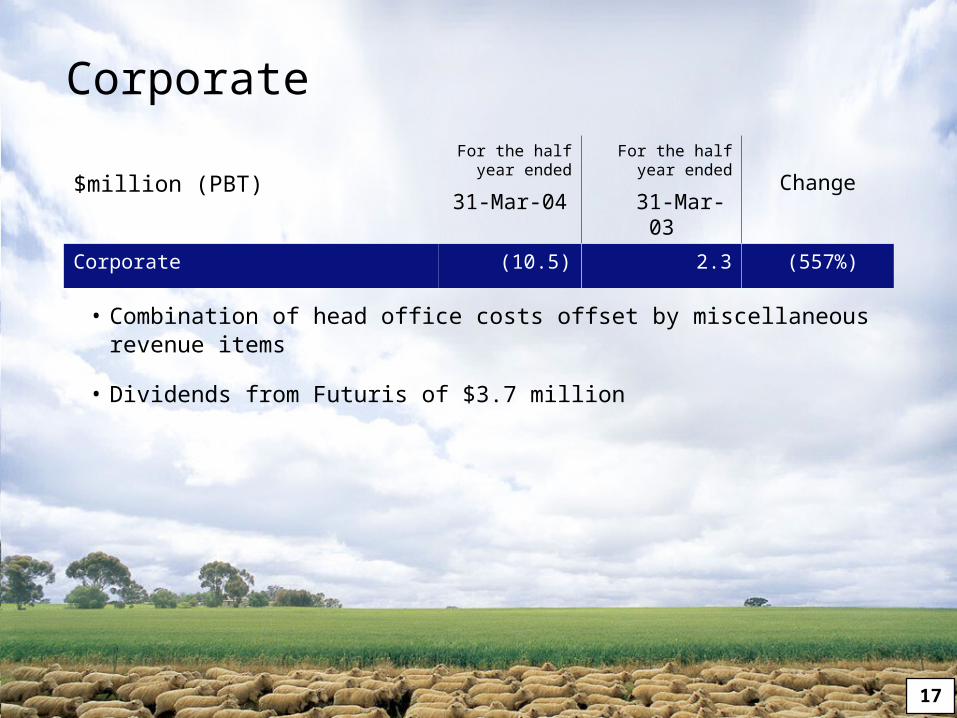

• Combination of head office costs offset by miscellaneous revenue items

• Dividends from Futuris of $3.7 million

$million (PBT)

For the half year ended

31-Mar-04

For the half year ended

31-Mar-03Change

Corporate (10.5) 2.3 (557%)

Corporate

18

Overall Status

Sale and Purchase process

Transition

Integration

Growth

Overall we are making good progress on ensuring a successful integration

Estimated % complete

50%

100%

95%

80%

5%

19

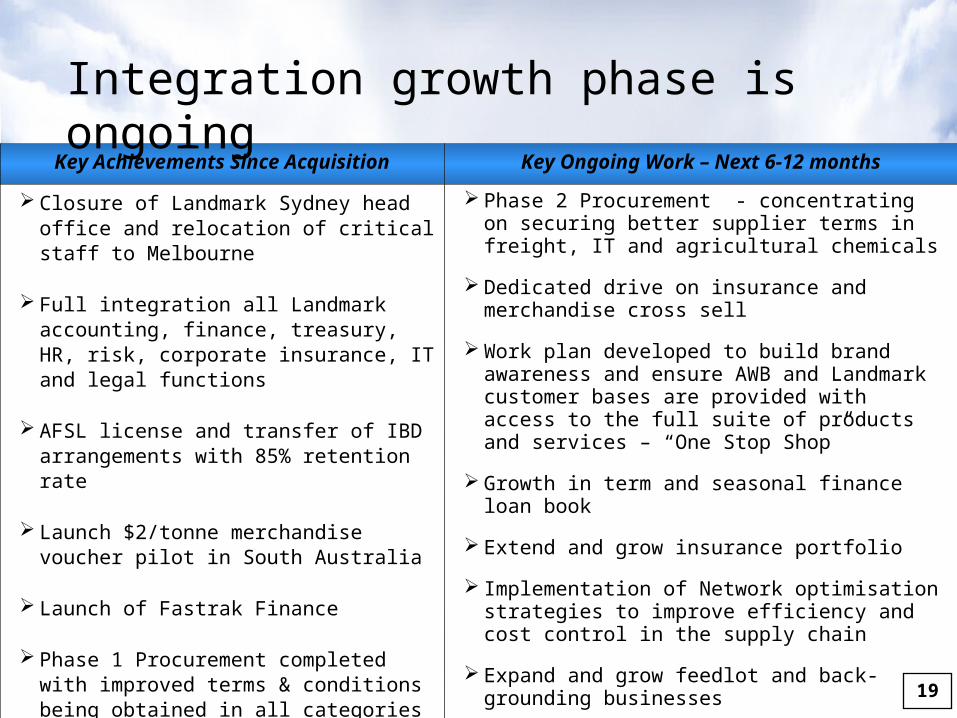

Key Achievements Since Acquisition

Closure of Landmark Sydney head office and relocation of critical staff to Melbourne

Full integration all Landmark accounting, finance, treasury, HR, risk, corporate insurance, IT and legal functions

AFSL license and transfer of IBD arrangements with 85% retention rate

Launch $2/tonne merchandise voucher pilot in South Australia

Launch of Fastrak Finance

Phase 1 Procurement completed with improved terms & conditions being obtained in all categories

Consolidation of 8 network offices.

Integration growth phase is ongoing

Key Ongoing Work – Next 6-12 months

Phase 2 Procurement - concentrating on securing better supplier terms in freight, IT and agricultural chemicals

Dedicated drive on insurance and merchandise cross sell

Work plan developed to build brand awareness and ensure AWB and Landmark customer bases are provided with access to the full suite of products and services – “One Stop Shop”

Growth in term and seasonal finance loan book

Extend and grow insurance portfolio

Implementation of Network optimisation strategies to improve efficiency and cost control in the supply chain

Expand and grow feedlot and back-grounding businesses

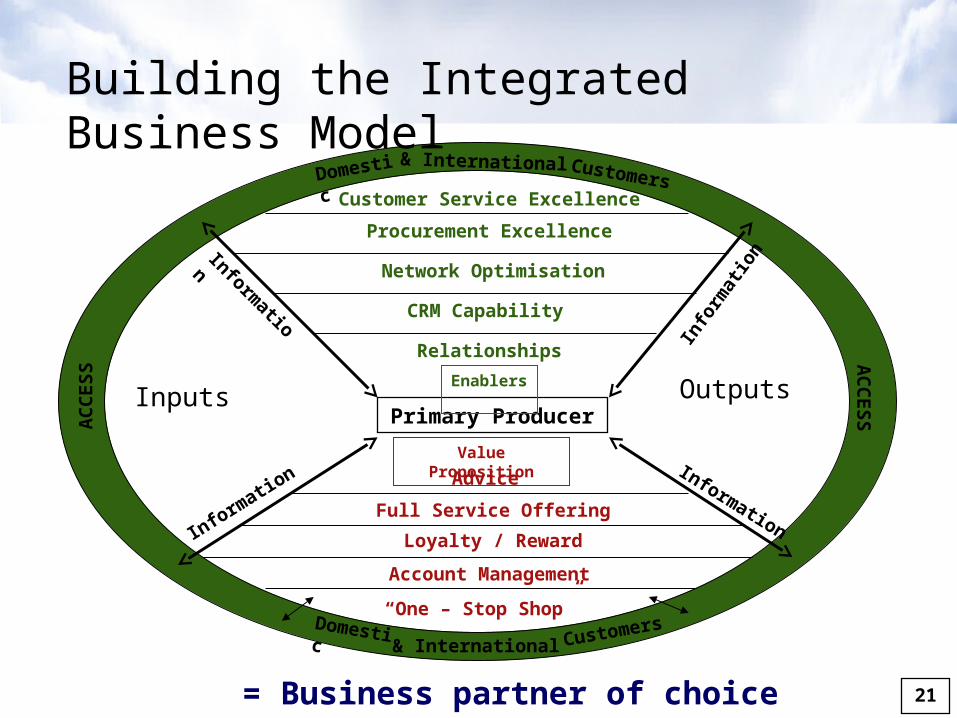

BUILD THE INTEGRATED BUSINESS MODEL 19

20

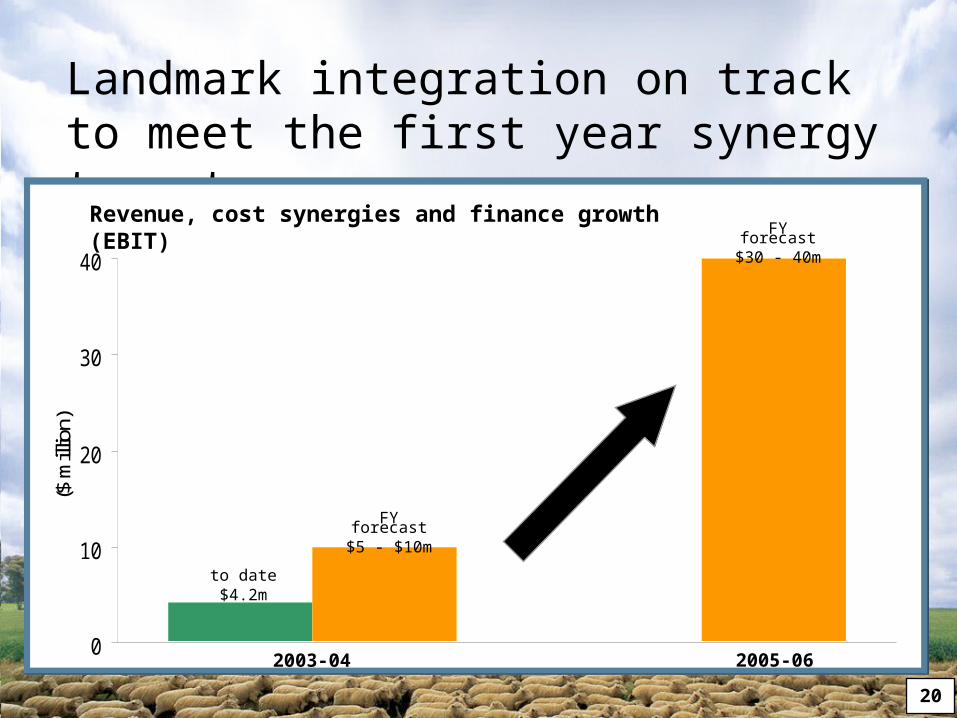

Landmark integration on track to meet the first year synergy targets

0

10

20

30

40

($ m

illio

n)

0

10

20

30

40

($ m

illio

n)

Revenue, cost synergies and finance growth (EBIT)

to date$4.2m

FY forecast$5 - $10m

FY forecast$30 - 40m

2003-04 2005-06

21

Primary Producer

Enablers

Value Proposition

Inputs Outputs

& InternationalDomestic Customers

Advice

Full Service Offering

Loyalty / Reward

Account Management

“One – Stop Shop”

Relationships

CRM Capability

Network Optimisation

Procurement Excellence

Customer Service ExcellenceDomestic & International Customers

Information

InformationInform

ation

Info

rmat

ion

AC

CE

SSA

CC

ES

S

= Business partner of choice

Building the Integrated Business Model

21

22

Iraq • Successful in the first Iraqi Grains Board tender – 50% of tender, ie, 100,000 tonnes

• 560,000 tonnes for period

China – 1 million tonne contract signed in December 2003 • First significant sale since 1996

• Strong position to meet Chinese quality and shipping requirements

Egypt – heads of agreement signed• Will build on the successful trade relationship with Egypt for over 50 years

• Establishes a framework to pursue the opportunity for a long- term supply contract of wheat

• Positioned to export in excess of 2.3 million tonnes to Egypt

Opportunities – global wheat market

23

VISION: To be Australia’s leading Agribusiness

Corporate strategy

Australia’s leading Agribusiness

Primary producer Business partner of choice End use customer

Our vision

delivered by..

Comprehensive product / service offering

managedthrough an...

Grain Marketing

andHandling

CharteringRisk

Manage-ment

FinancialServices

InsuranceMerchan-

diseAgronomy Wool Real EstateLivestock

IntegratedValue Chain

to ensure thatAWB is the…

BusinessPartnerof choice

Seedsand R&D

Farminputs

DomesticSupplyChain

Acquisitionand

TradingFreight

OffshoreSupplyChain

End usedemand

Millingand

Processing

23

24

Outlook

• 2003-04 NPAT forecast $110-$120 million(pre goodwill amortisation including one off costs)

• Wheat production forecast between 21 – 24 million tonnes for 2004-05

• Focus remains on AWB’s core wheat business

• Integrate and expand the Landmark business to deliver the integrated business model

25

QUESTIONS

26

For more information contact:

Delphine Cassidy

Head of Investor Relations

Ph: +61 3 9209 2404

Email: [email protected]

www.awb.com.au