Embed Size (px)

Citation preview

1

2

Insurance

• Is protection for individuals against possible financial losses

• Provides protection against many risks such as unexpected property loss, illness and injury

• Acts like a safety net for unforeseen events

3

Insurance Companies

• Are financial institutions agreeing to compensate for losses of individuals or businesses resulting from damages, injury, treatment or hardship

• Allow individuals to benefit from the coverage by purchasing a policy– is the scope of protection provided

under an insurance policy

4

Coverage

• Is provided by the insurance company to a policyholder to cover a risk

• Is specified in the insurance policy

5

Insurance Policy

• Is a written contract effecting insurance• Binds the insurance company to assume

the risk of the policyholder– in return, the policyholder must pay a

premium– in many cases, the policyholder is required to

pay a deductible when filing a claim

The premium is a fee the policyholder pays to the insurance company in order to be insured for

a defined period of time.

6

Deductible

• Is the portion of a claim the policyholder must pay before the insurance company provides the benefits of the policy– for example, if you have a $200 deductible

with your auto insurance, a repair covered by the policy costing $1,000 would require you pay $200, and the insurance covers the remaining $800

• Is specified in the insurance policy

7

Risk

• Is the chance of loss or injury• Refers to an accident or trouble which no

one can predict – policyholders transfer risks to insurance

companies through a policy– policyholders are required to pay a deductible,

which covers their portion of the risk

A deductible is the set amount which the policyholder must pay per loss on an insurance policy.

8

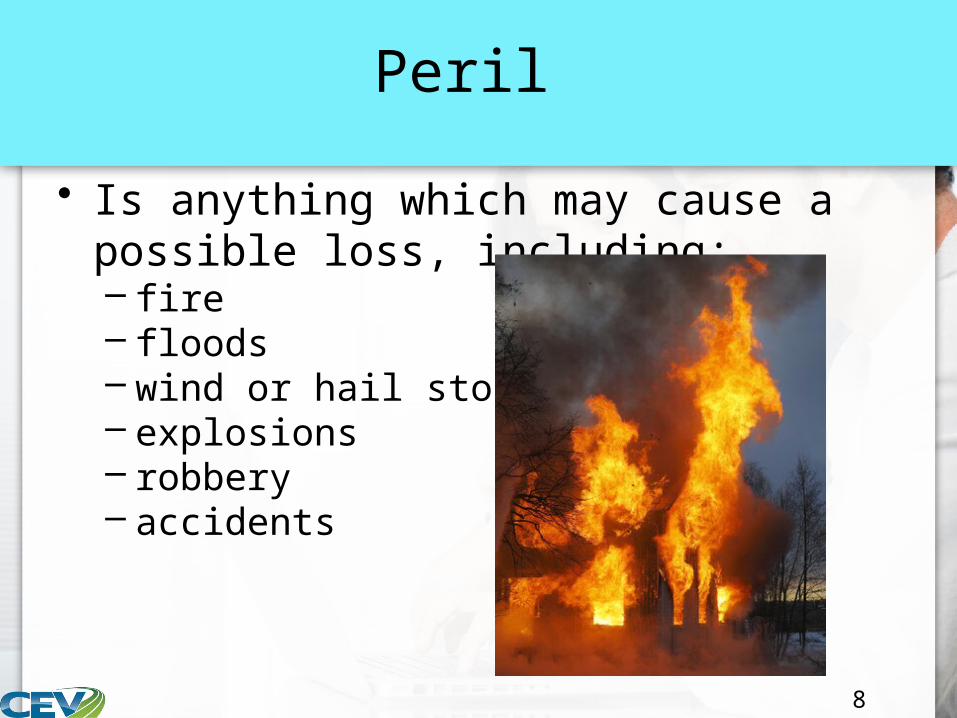

Peril

• Is anything which may cause a possible loss, including:– fire– floods– wind or hail storms– explosions– robbery– accidents

9

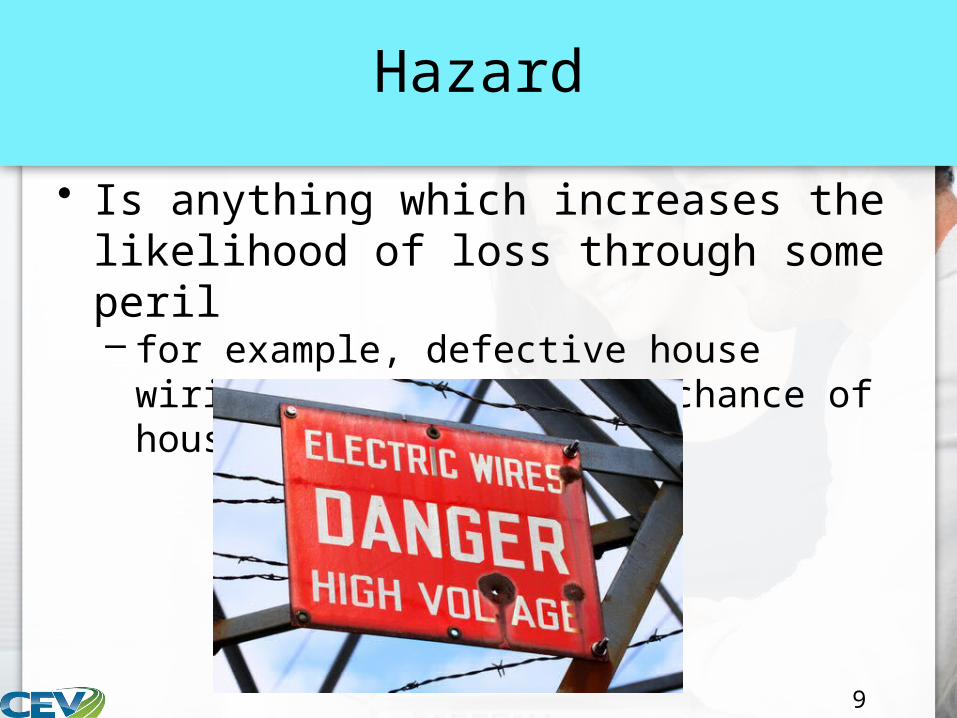

Hazard

• Is anything which increases the likelihood of loss through some peril– for example, defective house wiring can

increase the chance of house fires

10

Negligence

• Is the failure to take ordinary or reasonable care to prevent accidents from happening– for example, if a restaurant owner does not

clear the ice from the steps in front of the store, he or she creates a liability risk of customers falling

11

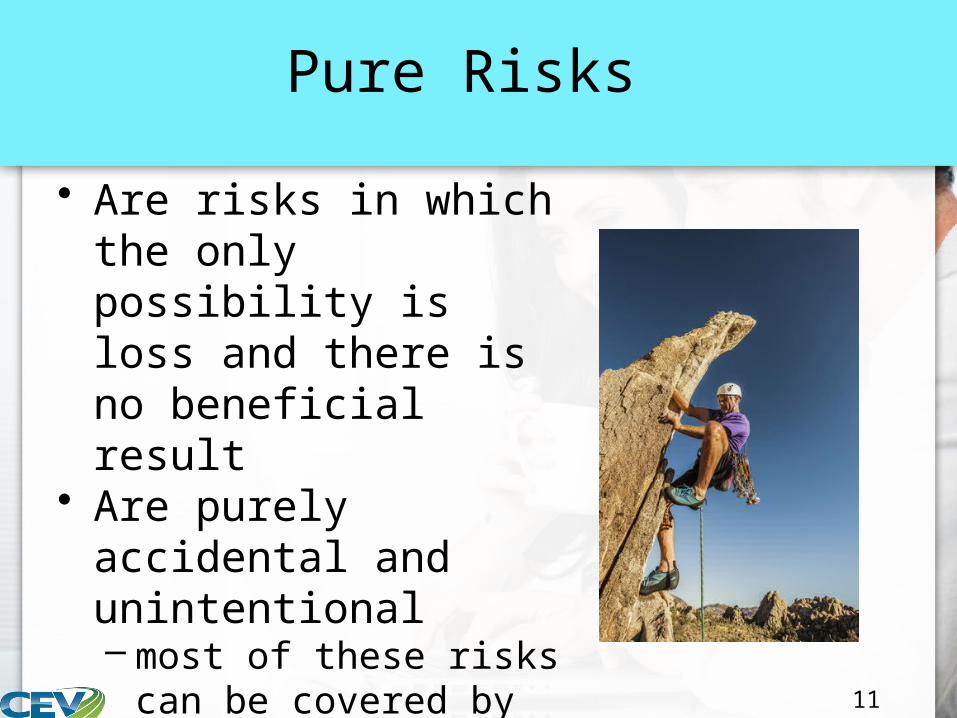

Pure Risks

• Are risks in which the only possibility is loss and there is no beneficial result

• Are purely accidental and unintentional– most of these risks can

be covered by insurance

12

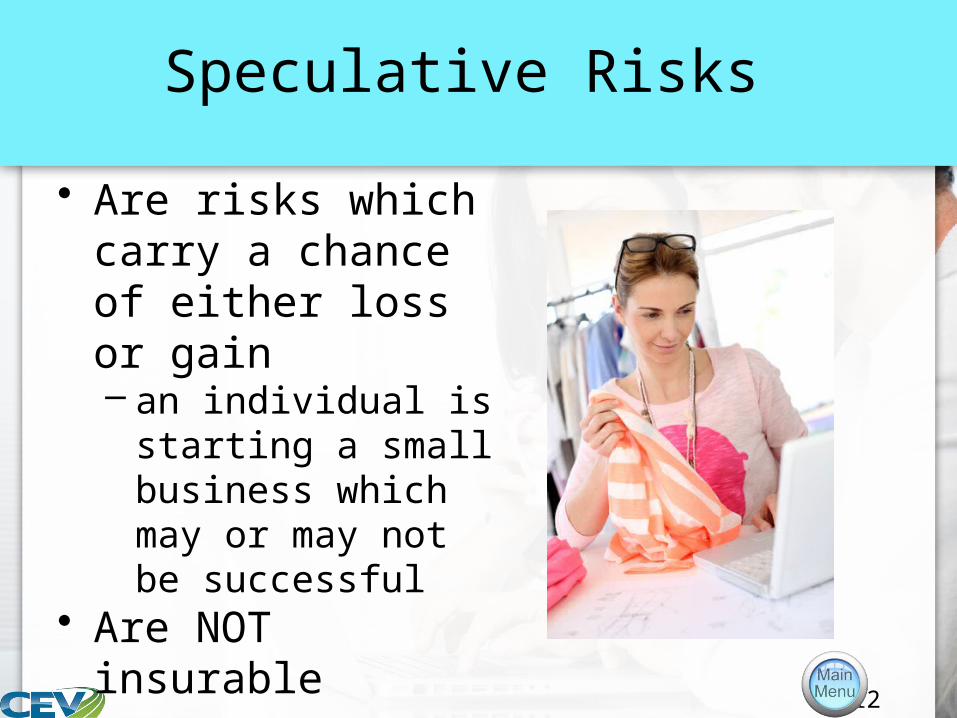

Speculative Risks

• Are risks which carry a chance of either loss or gain– an individual is

starting a small business which may or may not be successful

• Are NOT insurable

13

Automobile Insurance

• Reduces the financial impact of an automobile accident

• Is often required by Financial Responsibility Laws– these laws vary from state to state, but

require people to prove they have the financial means to pay for damage or injury caused by an accident

– some states have compulsory insurance laws requiring drivers to have liability insurance

• Typically includes a deductible

14

Types of Automobile Insurance

• Include:– bodily injury liability– property damage liability– medical payments coverage– uninsured motorist protection– collision insurance– comprehensive insurance

15

Bodily Injury Liability

• Covers physical injuries to others caused by an automobile accident for which the policyholder was responsible

• Covers costs if pedestrians, people in other cars, or passengers in the driver’s car are injured or killed

• Does not cover injuries to the policyholder

16

Property Damage Liability

• Applies when the policyholder damages the property of another person

• Covers the damage of the vehicle when an individual is driving another person’s vehicle with the owner’s permission

• Covers damage done to buildings and equipment such as telephone poles, fences or mail boxes

17

Medical Payments Coverage

• Is insurance which applies to the medical expenses of anyone who is injured in policyholder’s automobile, no matter who was at fault for the accident

• Is not available in all states

18

Uninsured Motorist Protection

• Covers costs if an individual is involved in a car accident with an uninsured driver– can include bodily injury and/or damage to the

vehicle, depending on the policy• Is relatively inexpensive to add to the

automobile policy

19

Collision Insurance

• Covers damage to the policyholder’s car when it is involved in an accident

• Allows the policyholder to collect cash value no matter who was at fault

• Only allows the policyholder to collect the cash value of the car, or of the cost of repairs, at the time of the accident

• Is required when a car is financed or leased

20

Comprehensive Insurance

• Covers physical damage to an individual’s car which occurs as a result of a non-collision incident– examples include fire, flooding, wind, damage

resulting from animals, theft, vandalism• Is required when a car is financed or

leased

21

Auto Insurance Prices

• Are affected by the following factors:– amount of coverage– vehicle type– rating territory– driver classification

22

Amount of Coverage

• Needs to protect the policyholder legally and financially– liability insurance is required

by many states to legally use the vehicle

– the policyholder can select the amount of coverage depending on his or her financial state

23

Vehicle Type

• Refers to the year, make and model of a vehicle

• Can make insurance more expensive– if the vehicle has expensive

replacement parts, requires more complicated repairs or is a type of car that is frequently stolen

• Can lower the price of insurance– if the vehicle has added safety

features or a security system

24

Rating Territory

• Is the residential location used to determine the automobile insurance premium– different locations have different costs– insurance is cheaper in rural areas due to

fewer accidents and thefts.

25

Driver Classification

• Is based on age, sex, marital status, driving record and driving habits– drivers age 21 to 24

typically represent a higher risk than other age groups

• Is also influenced by the cost and number of claims the policyholder has filed with the insurance company

26

Assigned Risk Pools

• Consist of people who cannot obtain an insurance policy from regular carriers due to poor driving record or other factors– in states where liability insurance

is required, the state assigns high-risk drivers to insurance carriers which charge them much higher rates and only allow them to buy the absolute minimum coverage

27

Tips

• To reduce auto insurance rates include:– compare companies’ rates and services– obtain premium discounts by maintaining a

good driving record– install security devices into your vehicle– increase the amount of your deductible