Embed Size (px)

Citation preview

1 1

Investment Update

December 2011 Quarter

2 2

General advice warning and disclaimer

This information has been provided by MLC Limited (ABN 90 000 000 402) a member of the National Group, 105–153 Miller Street, North Sydney 2060.

Any opinions expressed in this communication constitute our judgement at the time of issue and are subject to change. We believe that the information contained in this communication is correct and that any estimates, opinions, conclusions or recommendations are reasonably held or made as at the time of compilation. However, no warranty is made as to their accuracy or reliability (which may change without notice) or other information contained in this communication.

Past performance is not indicative of future performance. The value of an investment may rise or fall with the changes in the market. Please note that all performance reported is before management fees and taxes, unless otherwise stated.

The specialist investment managers are current as at the date this communication was prepared. Investment managers are regularly reviewed and may be appointed or removed at any time without prior notice to you.

This communication contains general information and may constitute general advice. Any advice in this communication has been prepared without taking account of individual objectives, financial situation or needs. It should not be relied upon as a substitute for financial or other specialist advice.

Before making any decisions on the basis of this communication, you should consider the appropriateness of its content having regard to your particular investment objectives, financial situation or individual needs. You should obtain a Product Disclosure Statement or other disclosure document relating to any financial product issued by MLC Investments Limited (ABN 30 002 641 661 [include AFSL for PDSs/FSGs/Annual Reports]) and consider it before making any decision about whether to acquire or continue to hold the product. A copy of the Product Disclosure Statement or other disclosure document is available upon request by phoning the MLC call centre on 132 652 or on our website at mlc.com.au.

3 3

Agenda

Time* Activity Speaker

11:00am Welcome & Introduction Mark Montaldi

11:05am Investment Update Michael Karagianis & Andrew Connors

11:50am “Q & A”

Midday Close

* All times shown as Eastern Daylight Savings Time

4 4

Review of 2011 Performance

5

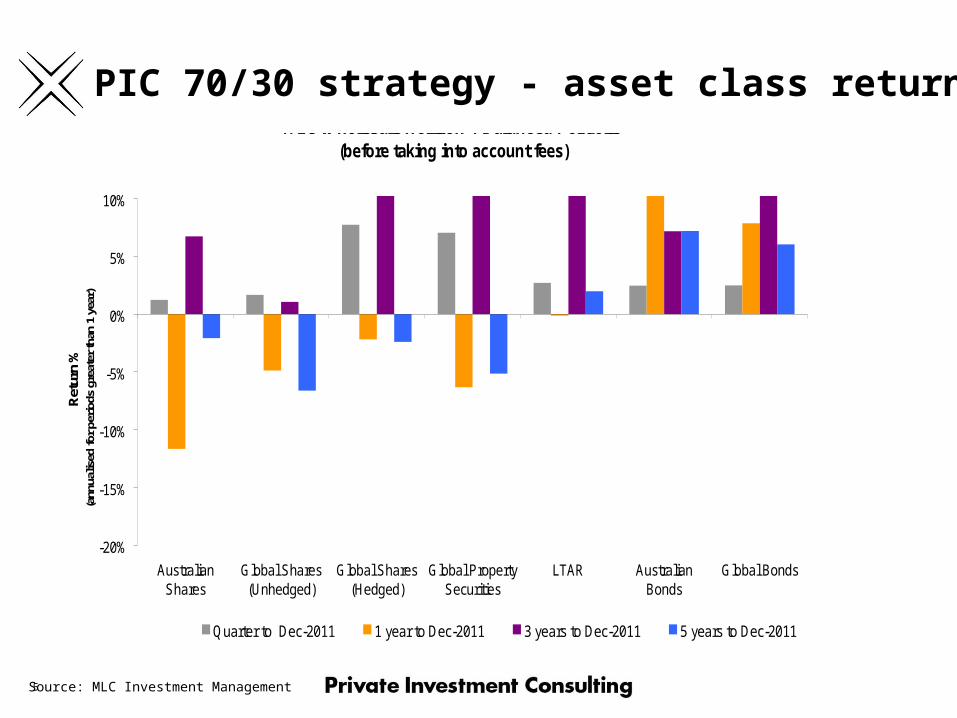

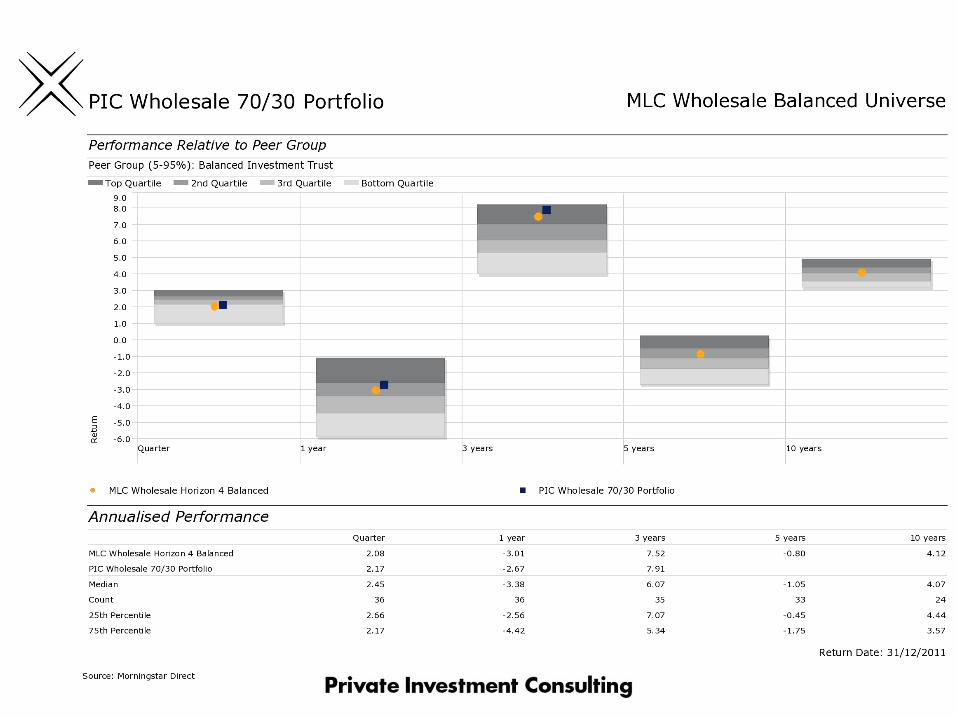

PIC 70/30 strategy - asset class returns

Source: MLC Investment Management

Total Return by Asset ClassMLC Wholesale Horizon 4 Balanced Portfolio

(before taking into account fees)

-20%

-15%

-10%

-5%

0%

5%

10%

AustralianShares

Global Shares(Unhedged)

Global Shares(Hedged)

Global PropertySecurities

LTAR AustralianBonds

Global Bonds

Ret

urn

%(a

nnua

lised

for p

erio

ds g

reat

er th

an 1

yea

r)

Quarter to Dec-2011 1 year to Dec-2011 3 years to Dec-2011 5 years to Dec-2011

7

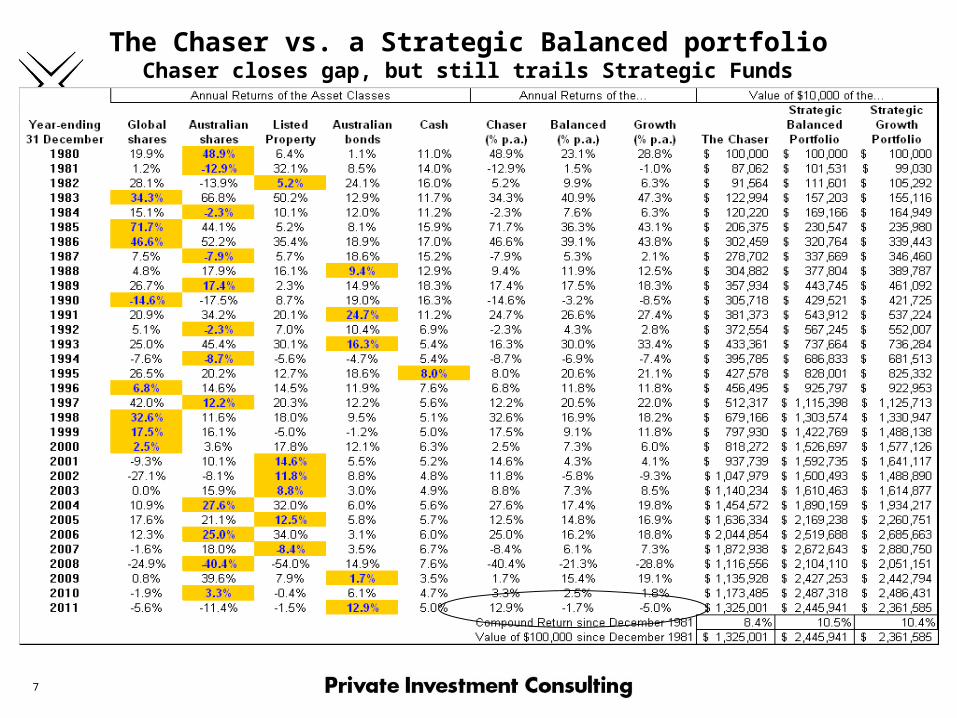

The Chaser vs. a Strategic Balanced portfolioChaser closes gap, but still trails Strategic Funds

8 8

Key Investment Themes for 2012

9

Key Investment Themes for 2012

1. Economic prospects for 2012

2. China - key issues for 2012

3. The role of alternatives in a post-GFC portfolio

4. Income investing – Investment fad or trend?

5. Where to next? Australian housing market update

6. Investment outlook and strategies for 2012

10

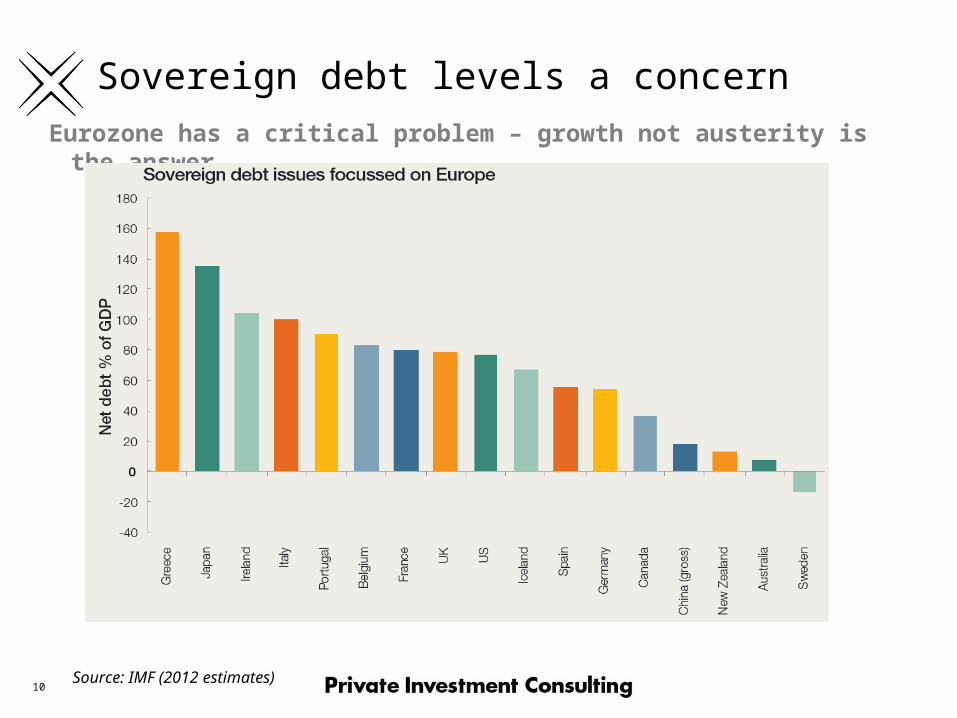

Sovereign debt levels a concern

Source: IMF (2012 estimates)

Eurozone has a critical problem – growth not austerity is the answer

11

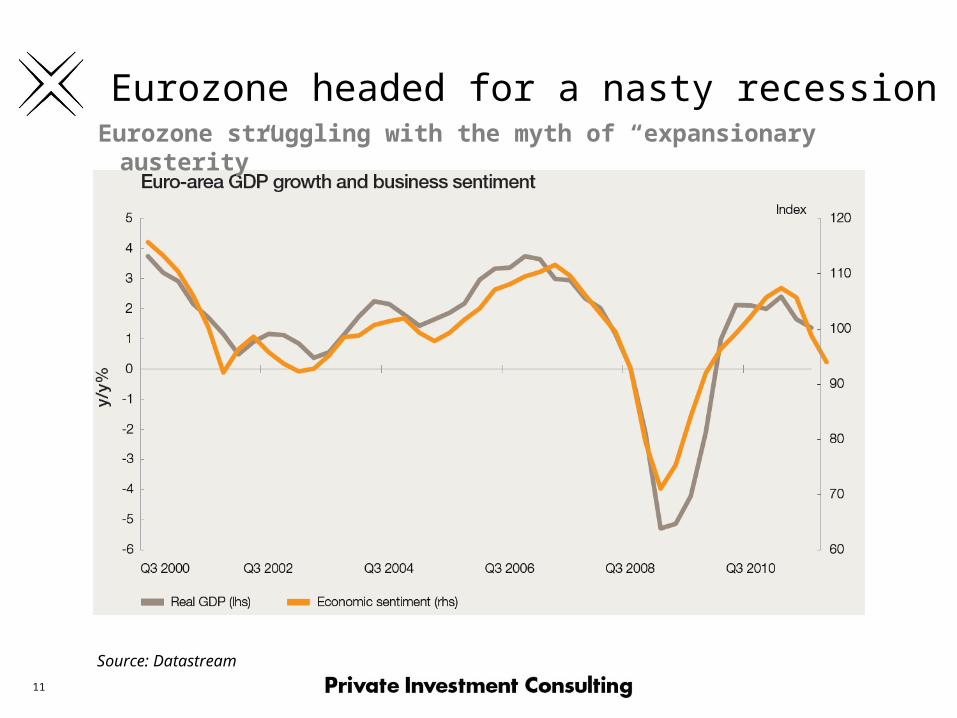

Eurozone headed for a nasty recession

Source: Datastream

Eurozone struggling with the myth of “expansionary austerity”

12

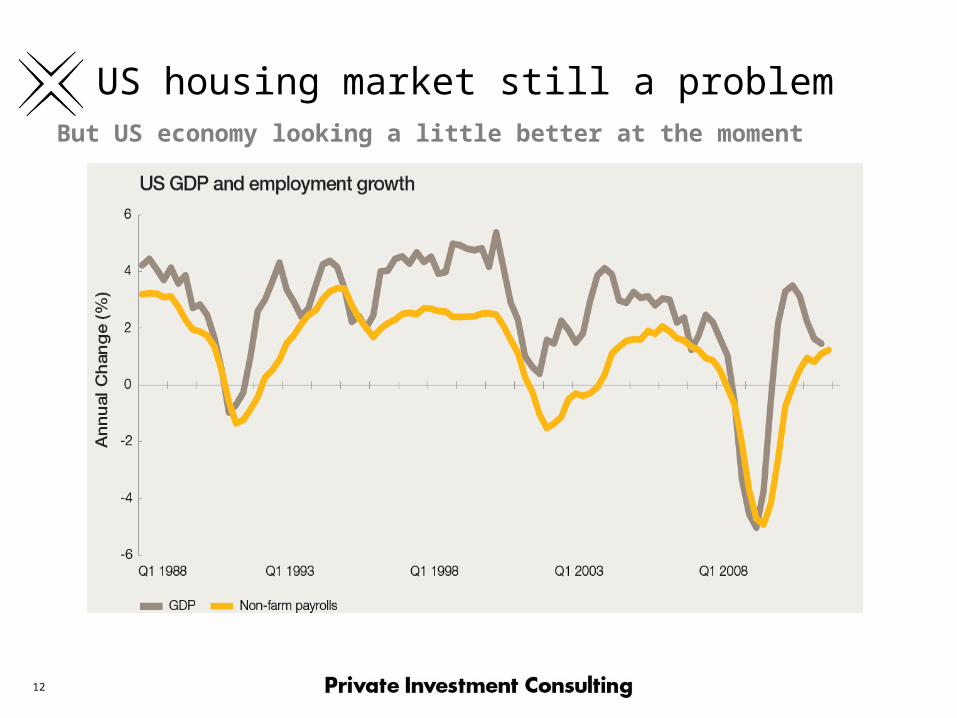

US housing market still a problem But US economy looking a little better at the moment

13

Source: Datastream

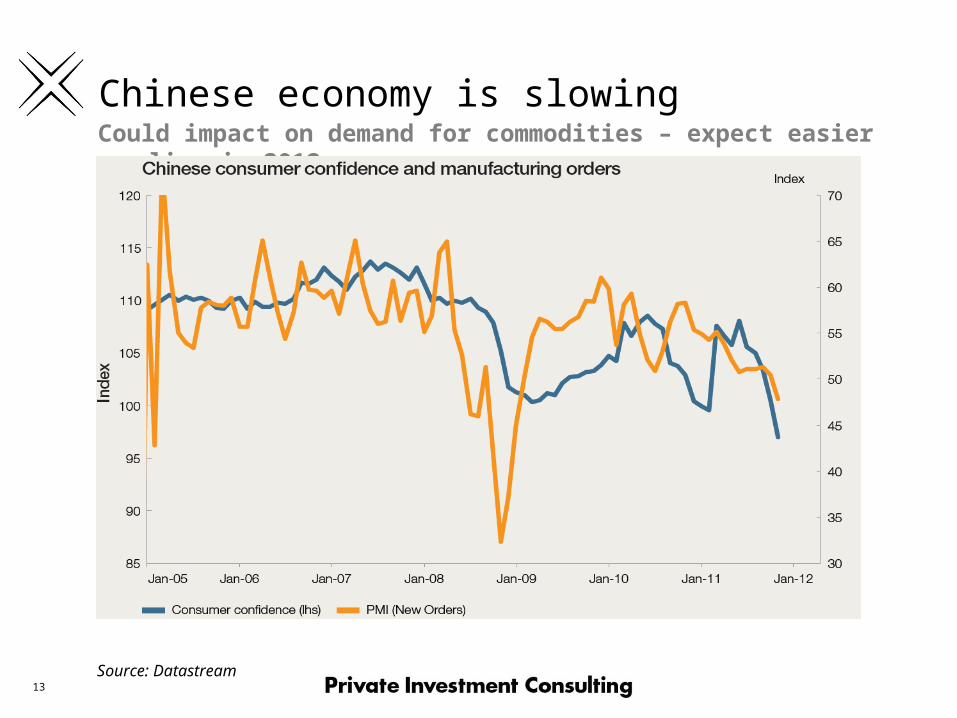

Chinese economy is slowing Could impact on demand for commodities – expect easier

policy in 2012

14

Source: Datastream

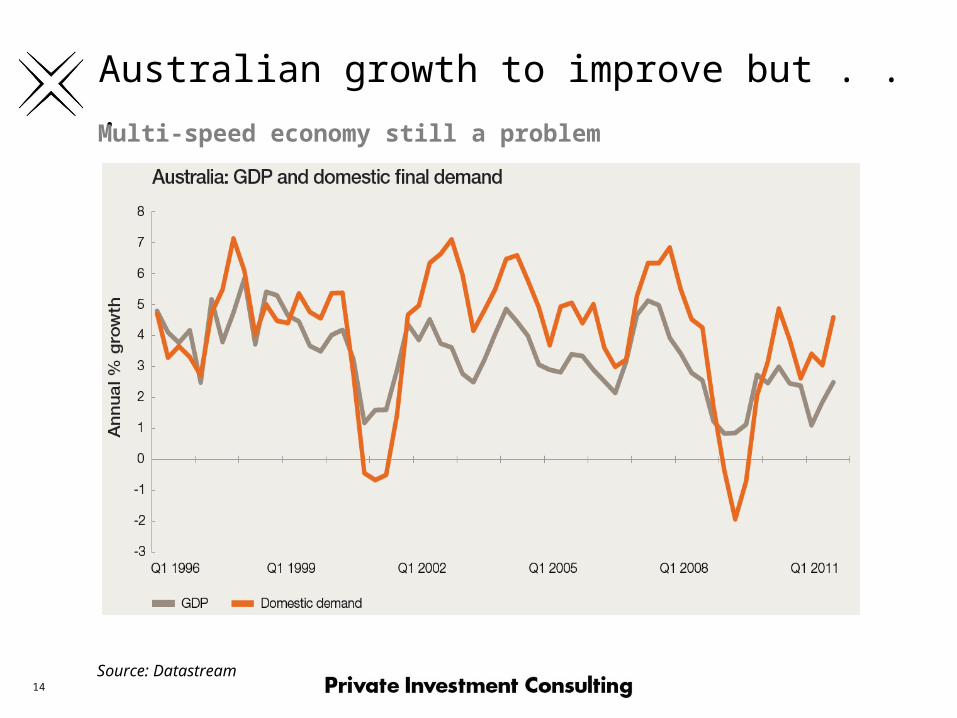

Australian growth to improve but . . . Multi-speed economy still a problem

15

Source: Reserve Bank of Australia

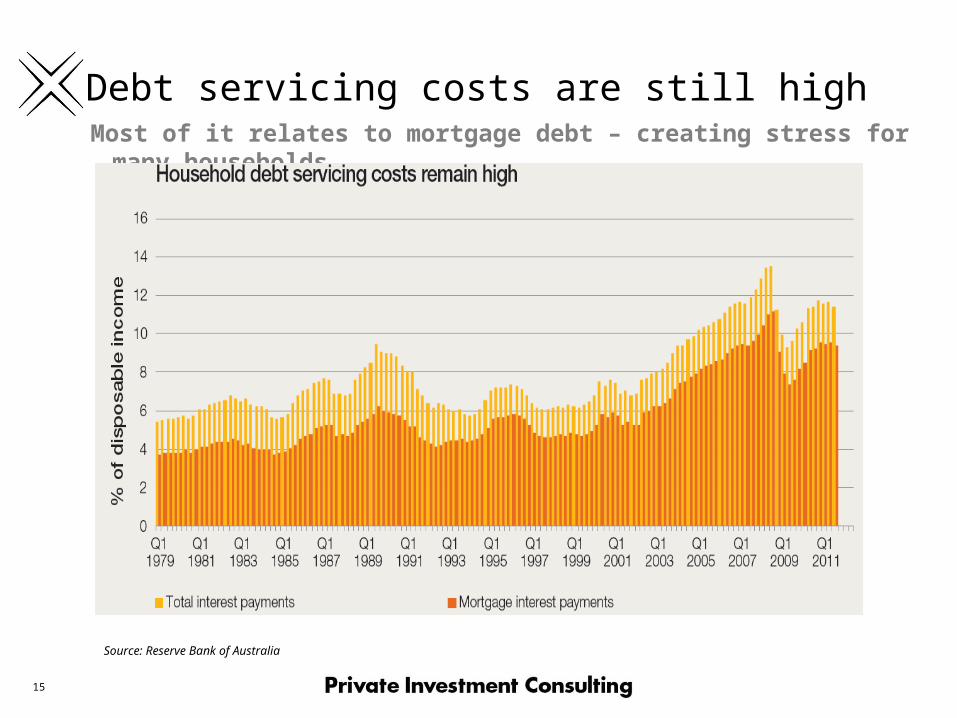

Debt servicing costs are still highMost of it relates to mortgage debt – creating stress for many

households

16

Source: Reserve Bank of Australia

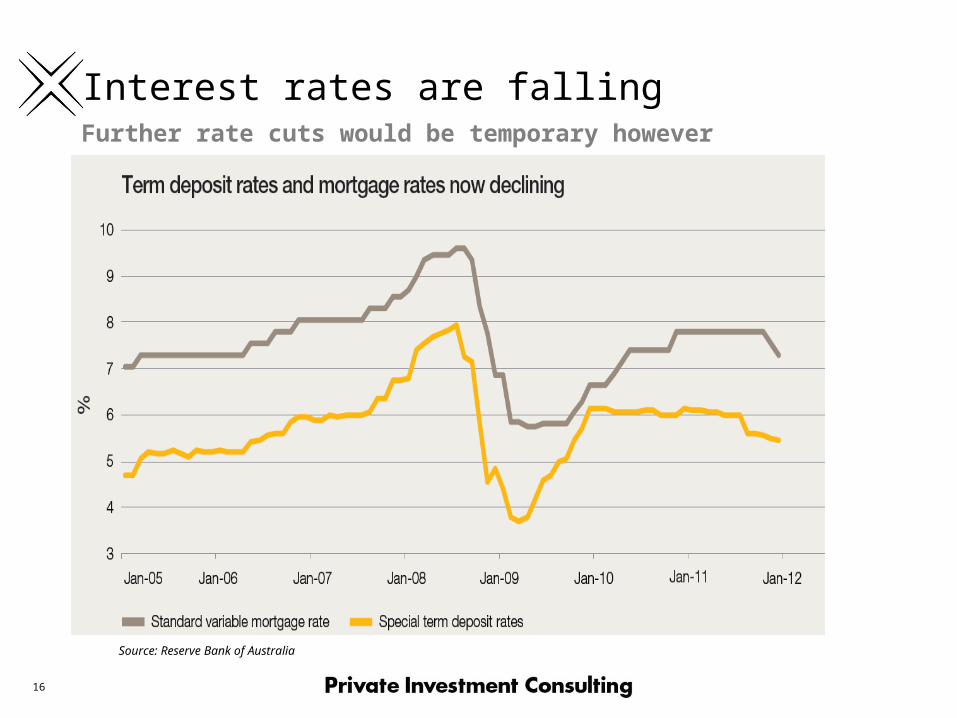

Interest rates are fallingFurther rate cuts would be temporary however

17

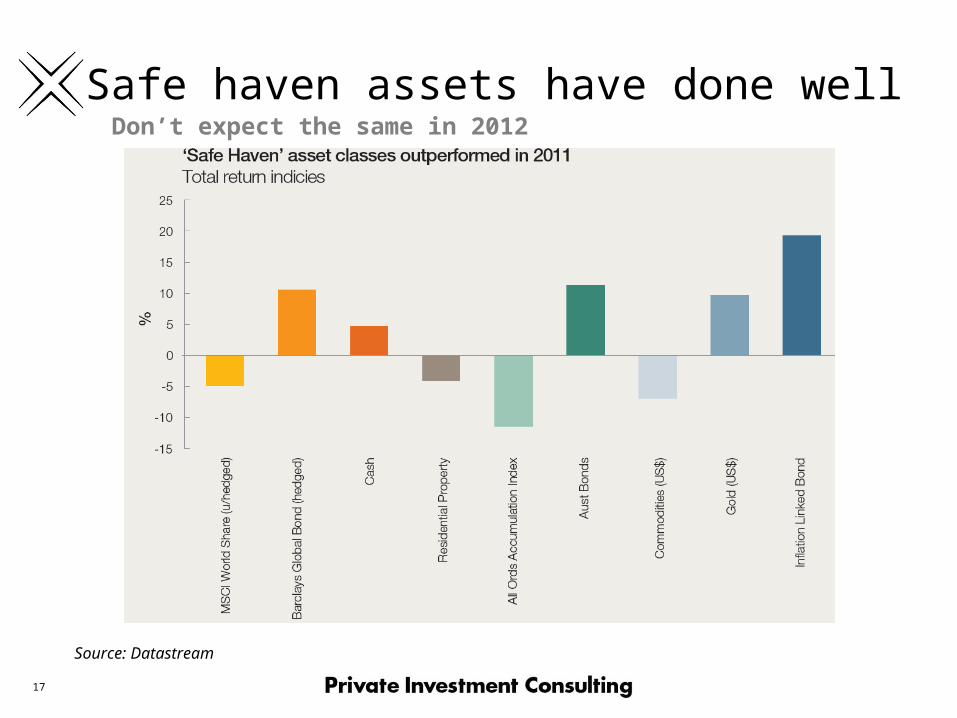

Safe haven assets have done well

Source: Datastream

Don’t expect the same in 2012

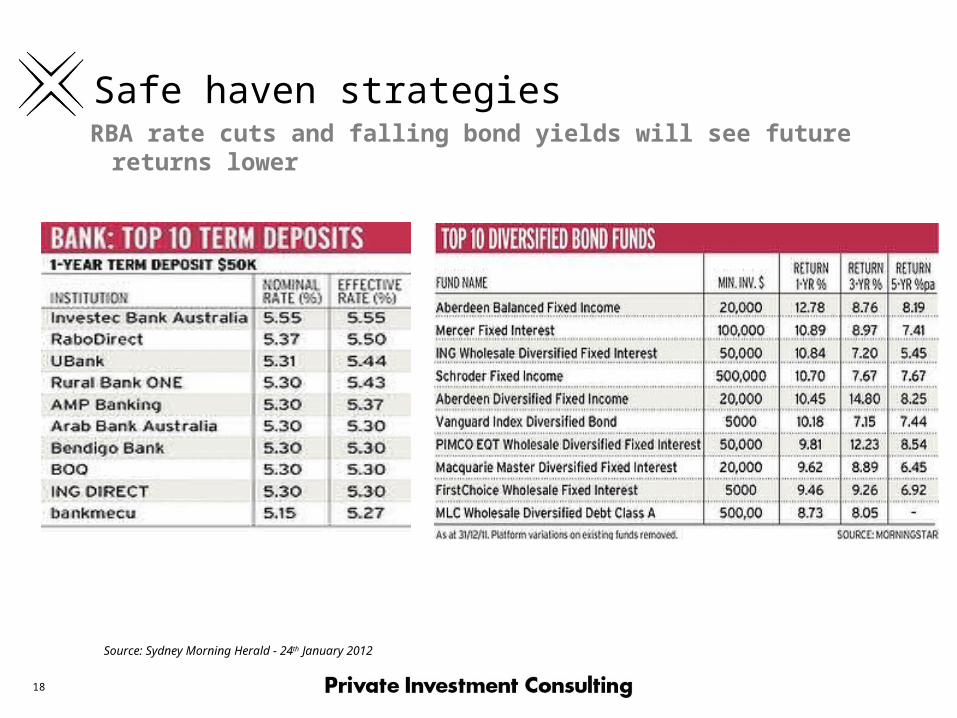

18

Source: Sydney Morning Herald - 24th January 2012

Safe haven strategies RBA rate cuts and falling bond yields will see future

returns lower

19

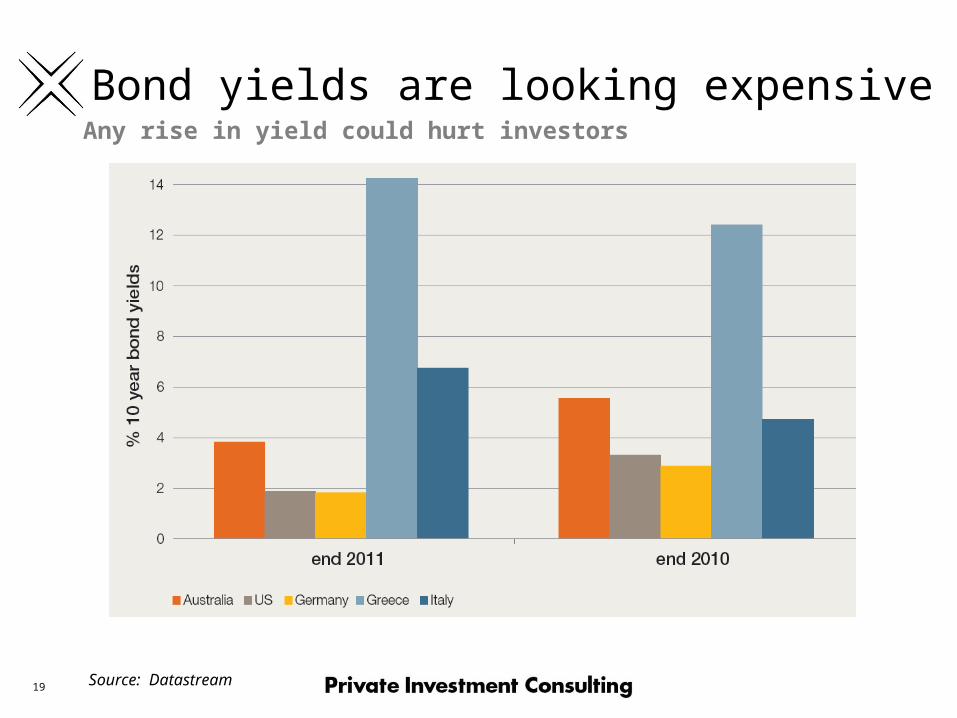

Bond yields are looking expensive

Source: Datastream

Any rise in yield could hurt investors

20

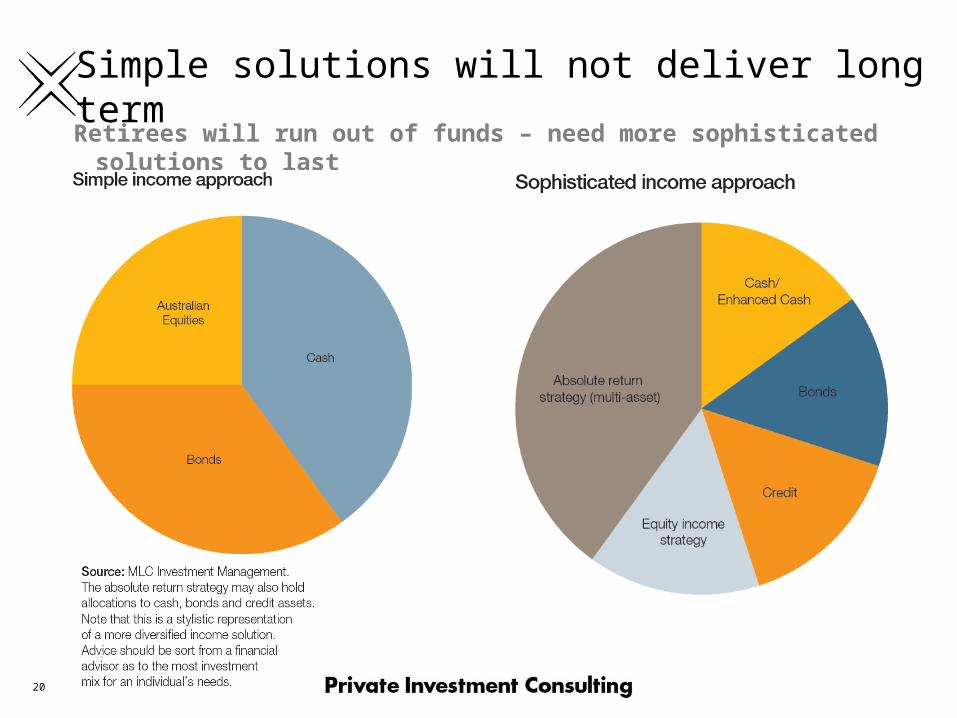

Simple solutions will not deliver long termRetirees will run out of funds – need more sophisticated

solutions to last

21

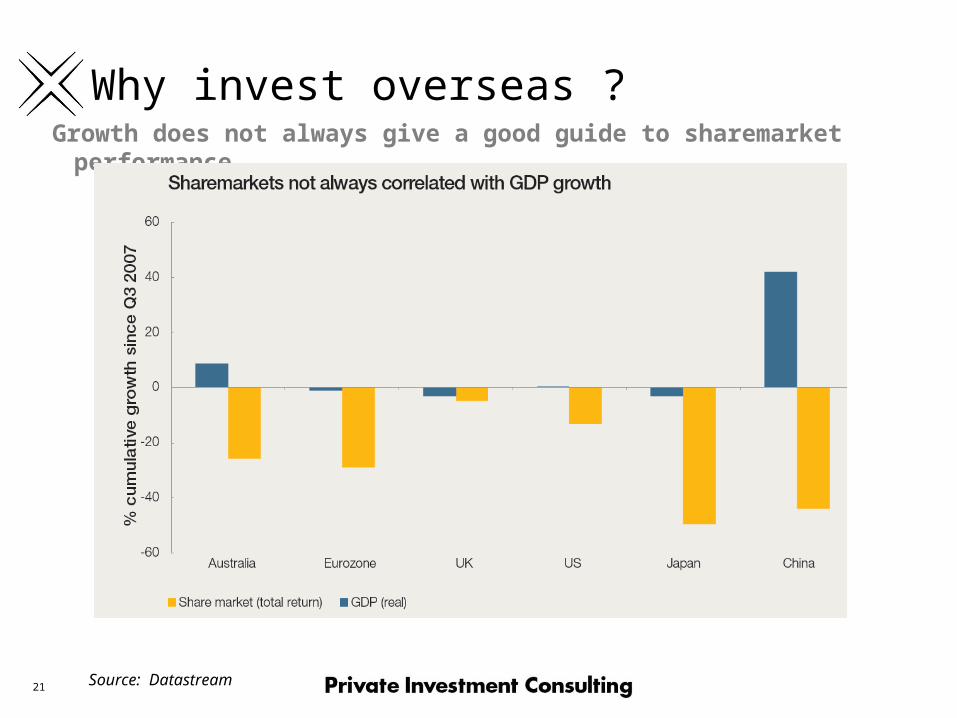

Why invest overseas ?

Source: Datastream

Growth does not always give a good guide to sharemarket performance

22

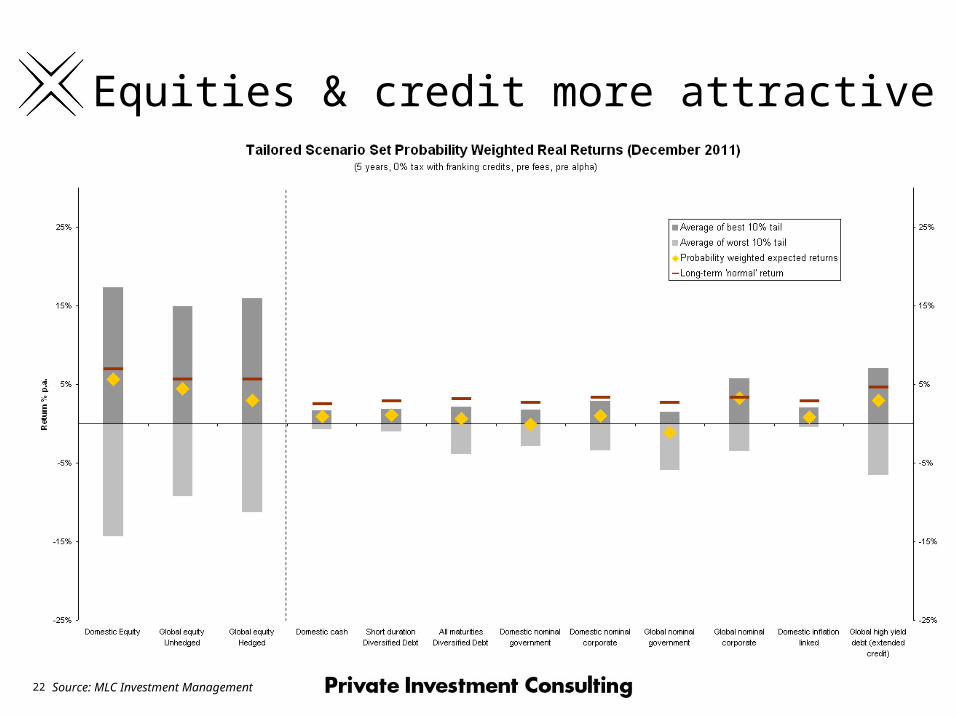

Equities & credit more attractive

Source: MLC Investment Management

Expected to outperform cash and bonds but with tail risks & continuing volatility

23 23

Snapshot of Innovation

The Long Term Absolute Return Portfolio (LTAR)

24

What is LTAR?

The Challenge: • Volatility has wreaked havoc to investor plans over the past few years• Many investments and asset classes did not perform how they were

expected to, meaning many people are now seeking new places to invest

MLC Response: • LTAR is different to traditional funds. It has flexibility to invest

anywhere, at any time, even in none traditional asset classes. And as well as providing additional sources of returns, this also provides additional sources of diversification – to help buffer when markets are volatile.

25

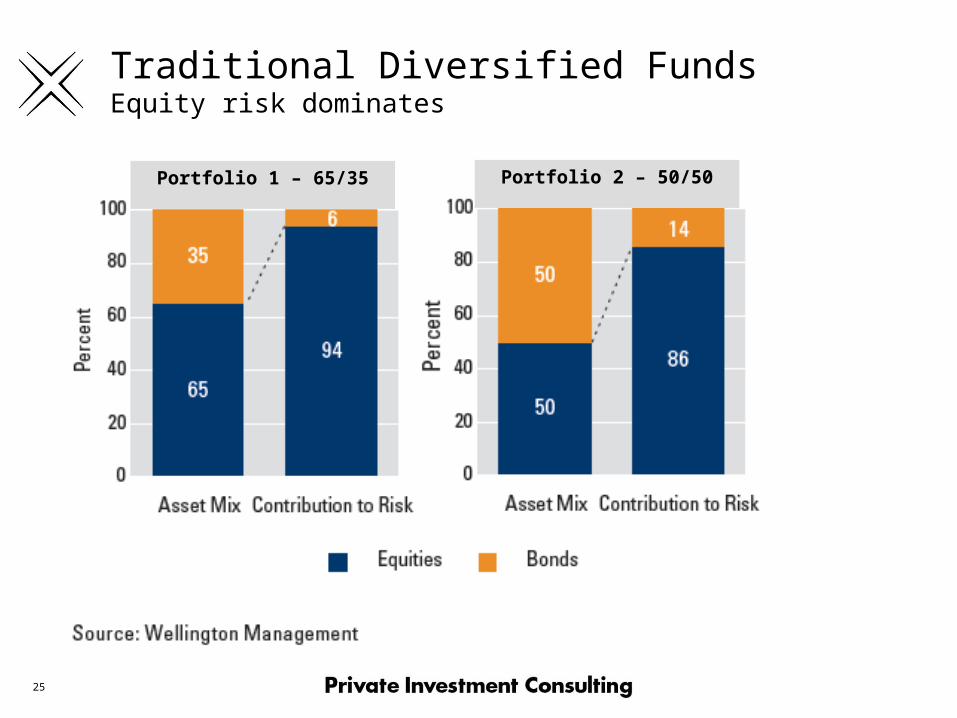

Traditional Diversified FundsEquity risk dominates

Portfolio 1 – 65/35 Portfolio 2 – 50/50

26

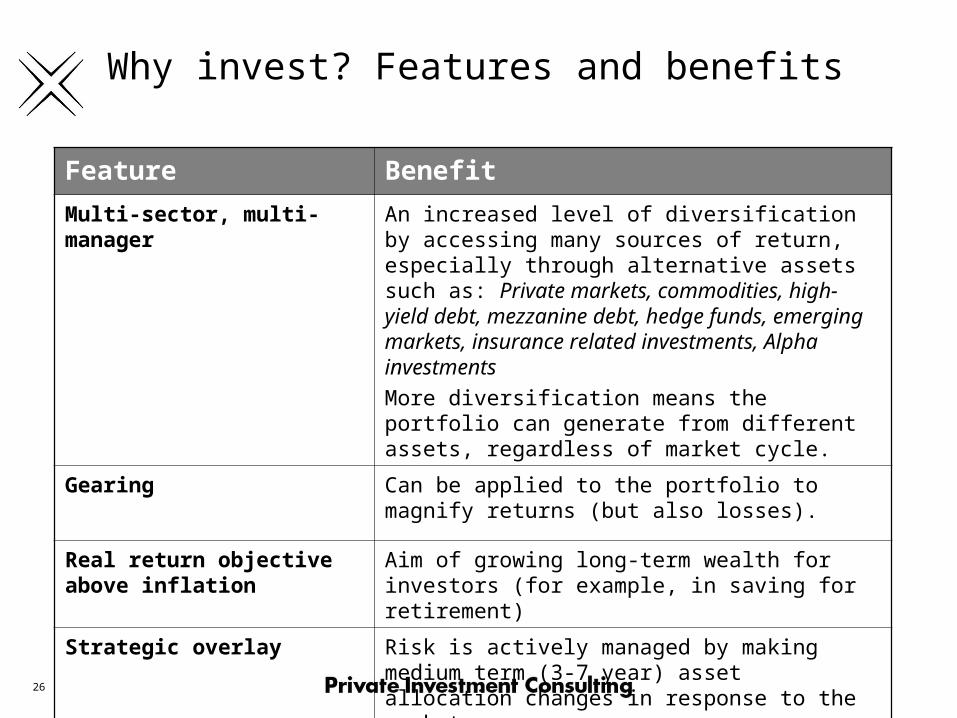

Why invest? Features and benefits

Feature Benefit

Multi-sector, multi-manager An increased level of diversification by accessing many sources of return, especially through alternative assets such as: Private markets, commodities, high-yield debt, mezzanine debt, hedge funds, emerging markets, insurance related investments, Alpha investments

More diversification means the portfolio can generate from different assets, regardless of market cycle.

Gearing Can be applied to the portfolio to magnify returns (but also losses).

Real return objective above inflation

Aim of growing long-term wealth for investors (for example, in saving for retirement)

Strategic overlay Risk is actively managed by making medium term (3-7 year) asset allocation changes in response to the market

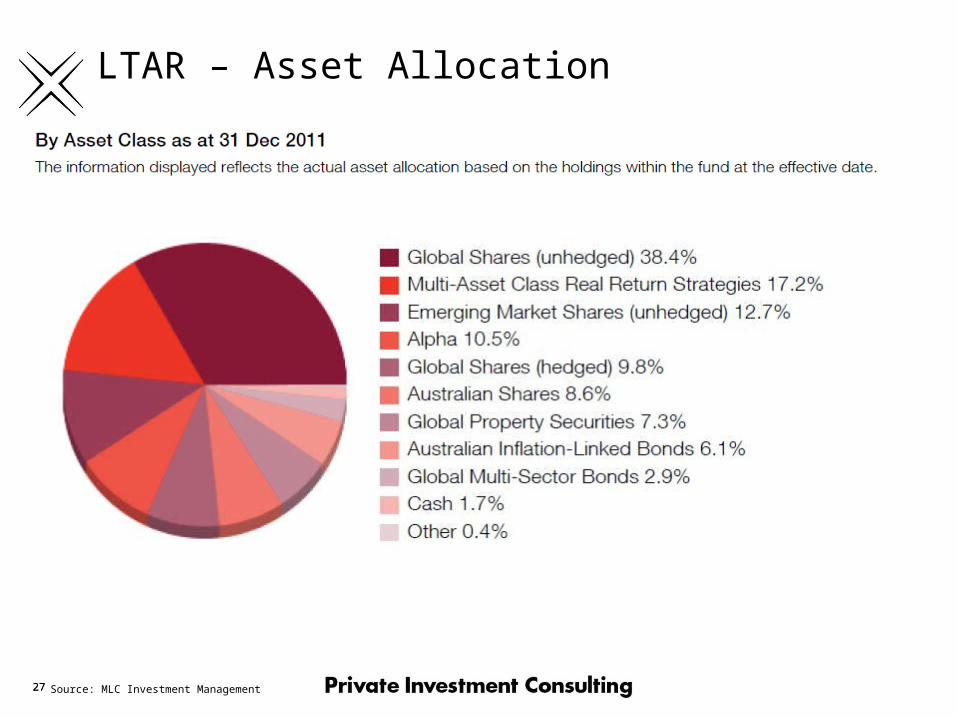

27 27

LTAR – Asset Allocation

Source: MLC Investment Management

28

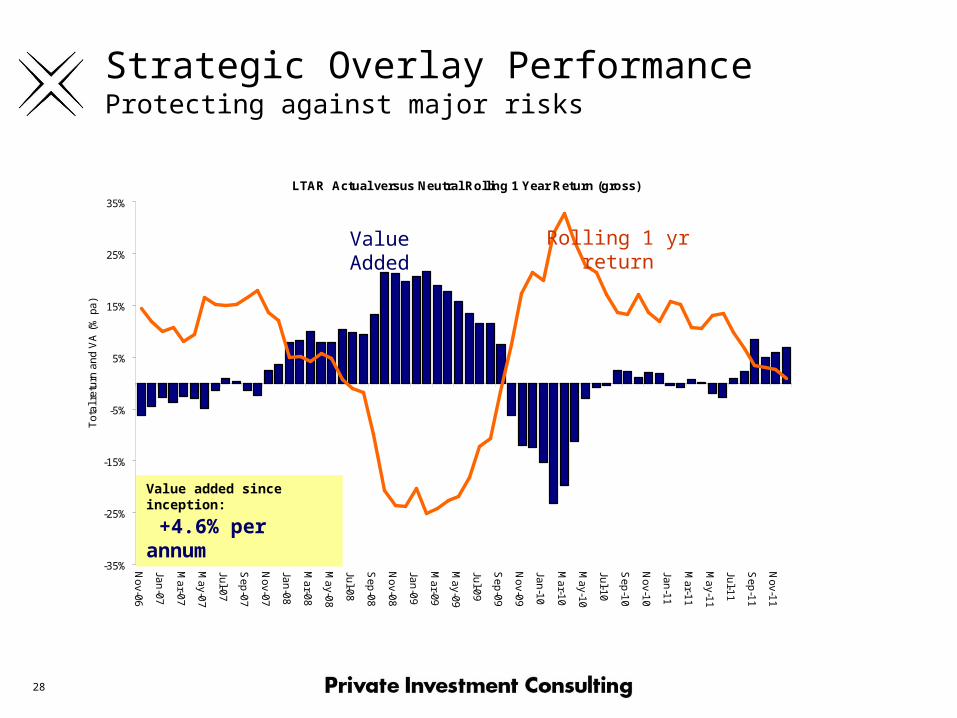

LTAR Actual versus Neutral Rolling 1 Year Return (gross)

-35%

-25%

-15%

-5%

5%

15%

25%

35%

No

v-06

Jan

-07

Ma

r-07

Ma

y-07

Jul-0

7

Se

p-0

7

No

v-07

Jan

-08

Ma

r-08

Ma

y-08

Jul-0

8

Se

p-0

8

No

v-08

Jan

-09

Ma

r-09

Ma

y-09

Jul-0

9

Se

p-0

9

No

v-09

Jan

-10

Ma

r-10

Ma

y-10

Jul-10

Se

p-1

0

No

v-10

Jan

-11

Mar-1

1

Ma

y-11

Jul-1

1

Se

p-1

1

Nov-1

1

To

tal r

etu

rn a

nd

VA

(%

pa

)

Strategic Overlay Performance Protecting against major risks

Value added since inception:

+4.6% per annum

Value AddedRolling 1 yr

return

29

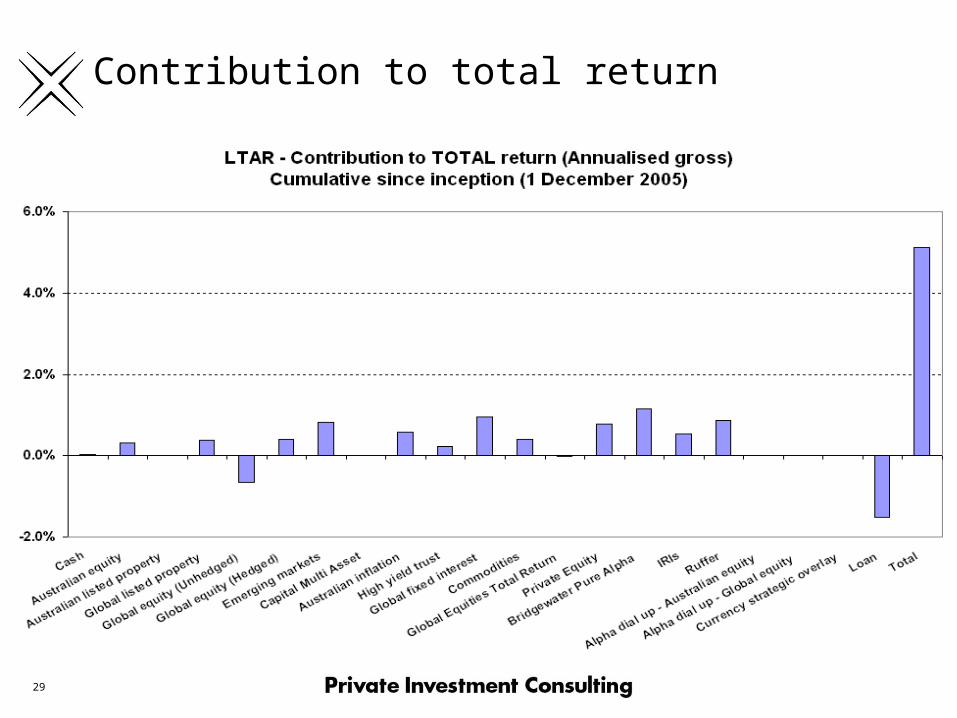

Contribution to total return

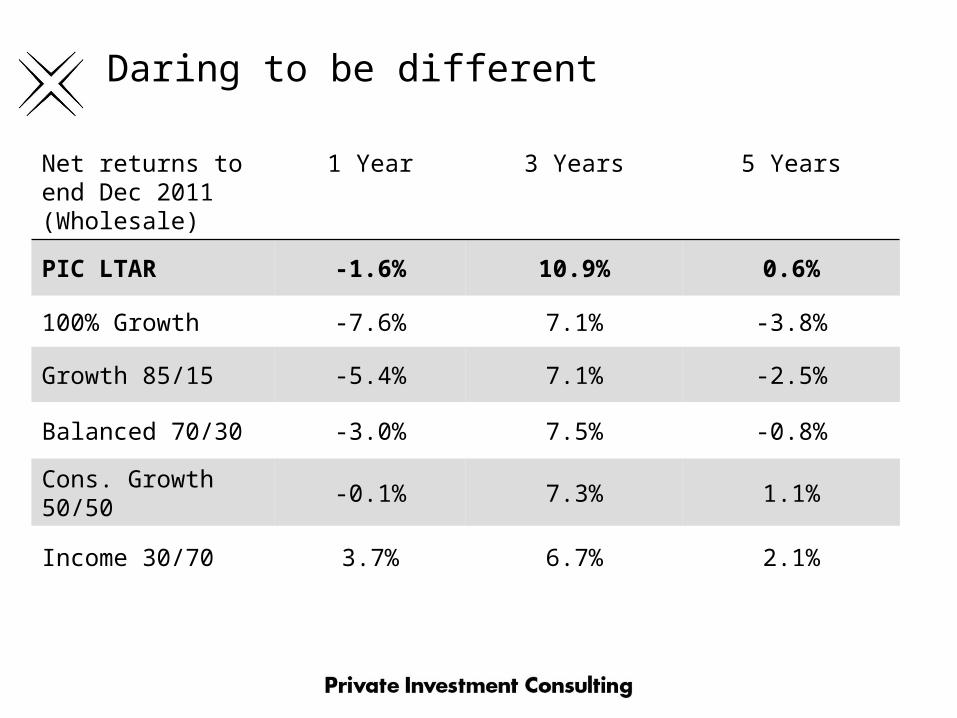

Daring to be different

Net returns to end Dec 2011 (Wholesale)

1 Year 3 Years 5 Years

PIC LTAR -1.6% 10.9% 0.6%

100% Growth -7.6% 7.1% -3.8%

Growth 85/15 -5.4% 7.1% -2.5%

Balanced 70/30 -3.0% 7.5% -0.8%

Cons. Growth 50/50 -0.1% 7.3% 1.1%

Income 30/70 3.7% 6.7% 2.1%

31 31

“Q&A”

MLC Investment Management speakers today:

•Michael Karagianis – Snr Investment Strategist

•Andrew Connors – Portfolio Specialist