Embed Size (px)

Citation preview

1-1

Accounting Basics

Prepared/Edited

by

Nita S. Edwards, CPA

1-2

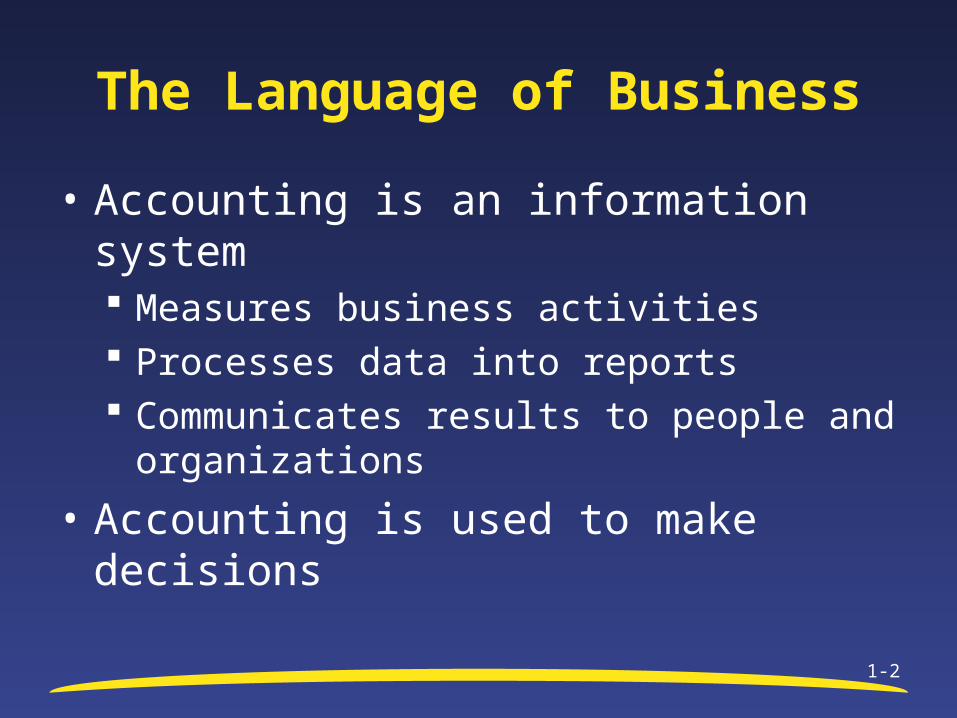

The Language of Business

• Accounting is an information system Measures business activities Processes data into reports Communicates results to people and

organizations

• Accounting is used to make decisions

1-3

Users of Accounting

IndividualsInvestors

& Creditors

Taxing Authorities

Nonprofit Organizations

1-4

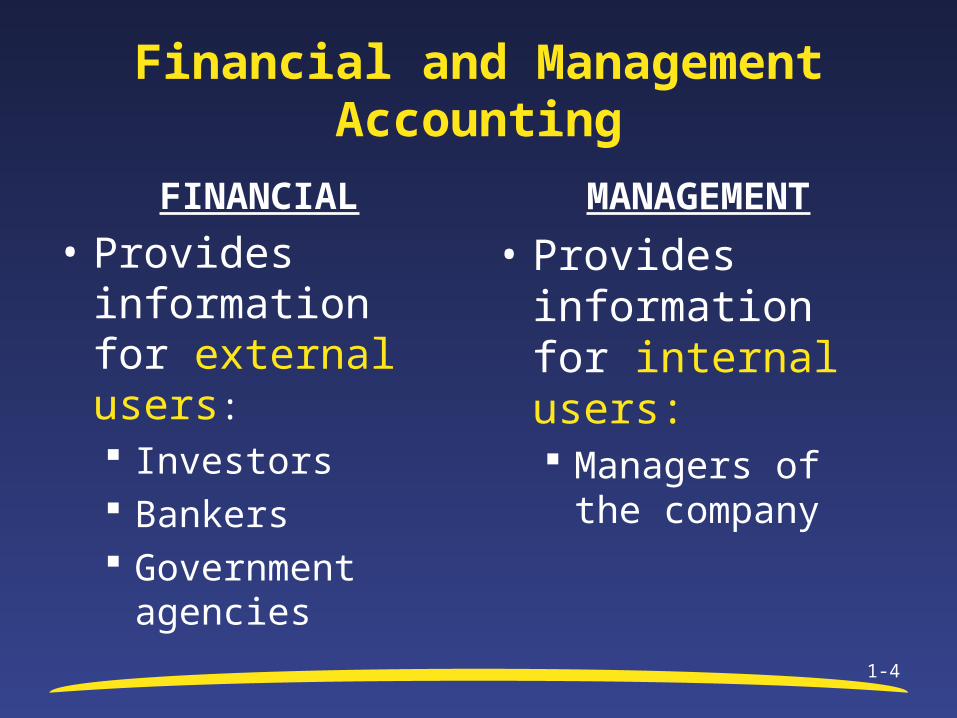

Financial and Management Accounting

FINANCIAL

• Provides information for external users: Investors Bankers Government

agencies

MANAGEMENT

• Provides information for internal users: Managers of the

company

Copyright ©2008 Pearson Prentice Hall. All rights reserved1-5

G A A P

• GAAP is an acronym for Generally Accepted Accounting Principles

• U.S. GAAP is formulated by the Financial Accounting Standards Board (FASB)

• FASB’s Conceptual Framework states that accounting should be: Relevant Reliable Comparable Consistent

1-6

Debits and Credits

• Credit – Entry on the right side of an account – Will increase an account with a Normal Credit Balance

Cash

CreditDebit

• Debit – Entry on the left side of an account – Will increase an account with a Normal Debit Balance

1-7

Assets – Balance Sheet – Permanent

• Economic resources that provide a future benefit

• Examples: Cash Inventory Equipment Land Buildings

1-8

Liabilities – Balance Sheet - Permanent

• Outsiders claims to assets Include debts payable to creditors

• Examples: Accounts payable – liability for goods or

services purchased on credit Notes payable – written promise to pay on a

certain date (bank loan)

1-9

Owners’ Equity – Balance Sheet - Permanent

• Owners’ claim on a business

• Includes Initial Investments less Withdrawals/Dividends and Retained Earnings

• Retained Earnings is the accumulation of Net Income/Losses.

• A corporation’s equity is called Stockholders’ Equity

1-10

Revenue – Income Statement - Nominal

• Sales from Merchandise or Services

• Presented on the Income Statement

• Closed at the end of the Period

• Normal Balance is a Credit

• Examples: Rent Revenue Service Revenue Sales Revenue

1-11

Expenses – Income Statement - Nominal

• Costs of doing business

• Presented on the Income Statement

• Closed at the end of the Period

• Normal Balance is a Debit

• Examples: Salaries Expense Utilities Expense Insurance Expense

1-12

Net Income

• Revenue – Expenses = Net Income or Net Loss

• Net Income/Loss Reported on Income Statement

• Net Income/Loss is included in Retained Earnings

1-13

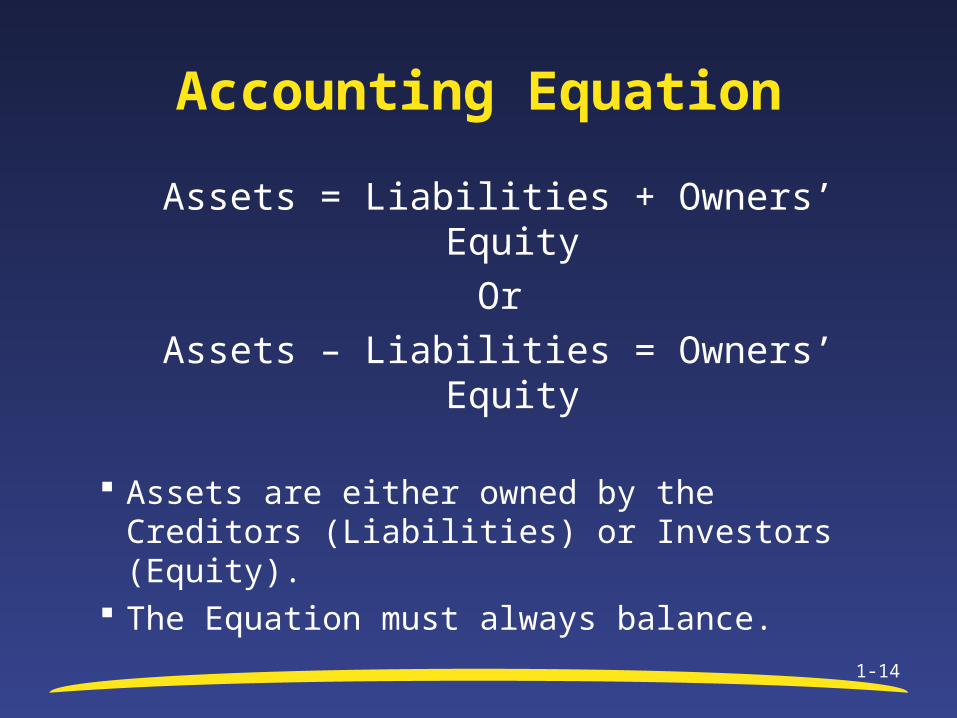

The Accounting Equation

=

Liabilities

Owners’ Equity

+

1-14

Accounting Equation

Assets = Liabilities + Owners’ Equity

Or

Assets – Liabilities = Owners’ Equity

Assets are either owned by the Creditors (Liabilities) or Investors (Equity).

The Equation must always balance.

1-15

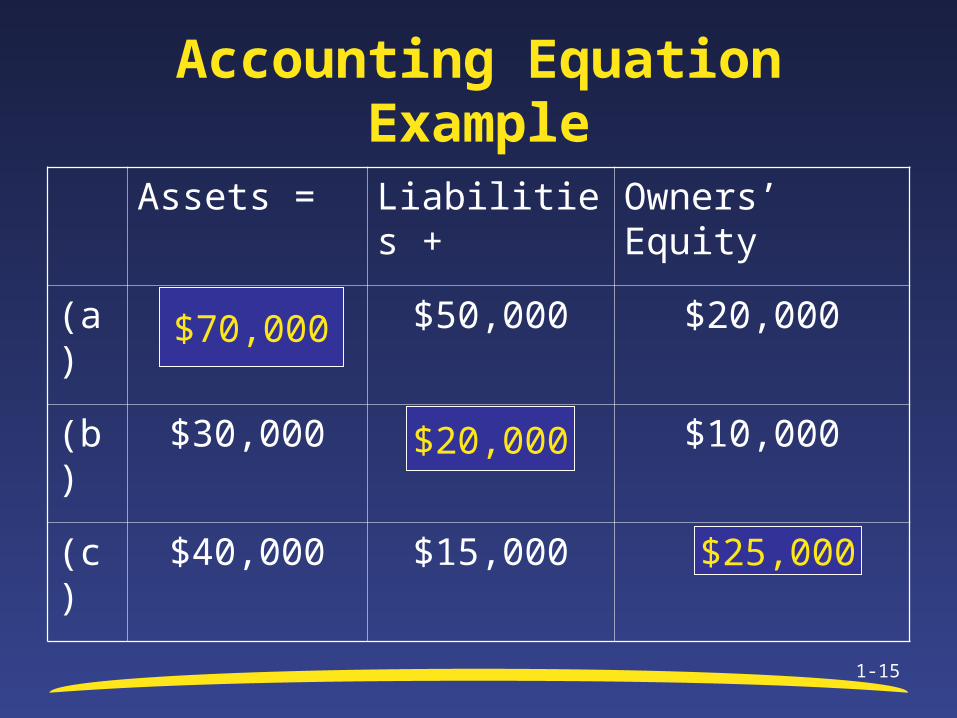

Accounting Equation Example

Assets = Liabilities + Owners’ Equity

(a) $50,000 $20,000

(b) $30,000 $10,000

(c) $40,000 $15,000

$70,000

$20,000

$25,000

The Accounting Cycle

• Journalize Transactions• Post to General Ledger• Prepare Trial Balance• Complete Adjusting Entries• Prepare Adjusted Trial Balance• Prepare Financial Statements• Close Permanent Accounts• Post Closing Trial Balance

1-16

The Financial Statements

• Report company’s results to the public

• Four Statements Income Statement Statement of Retained Earnings Balance Sheet Statement of Cash Flows

1-17

The Income Statement

• Measures operating performance for the period

• Reports revenue and expenses and resulting net income (or loss)

• Also includes gains and losses

1-18

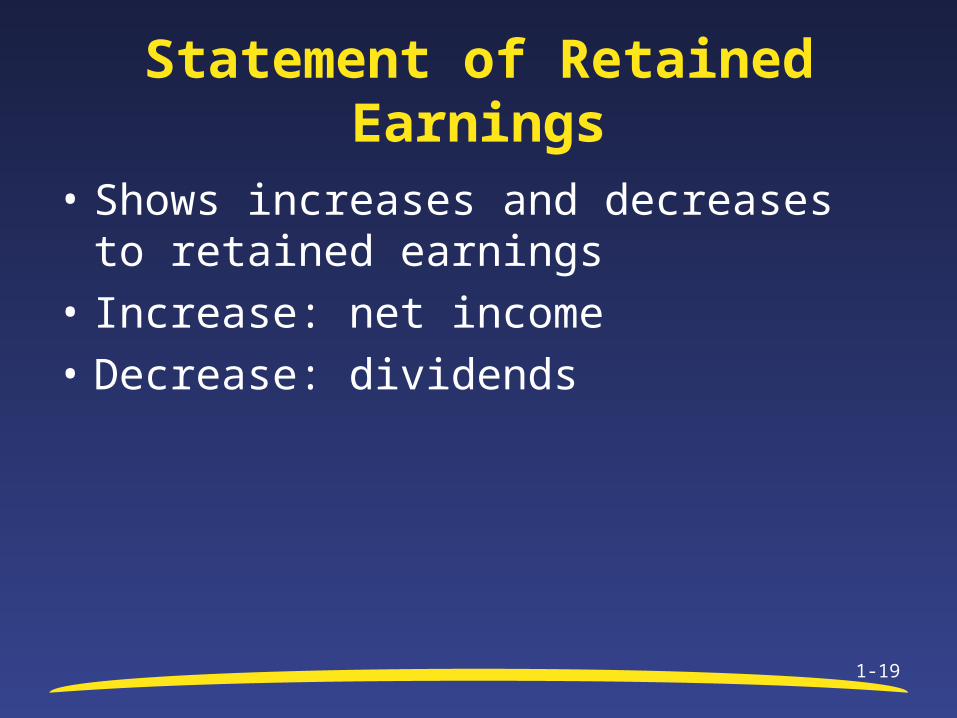

Statement of Retained Earnings

• Shows increases and decreases to retained earnings

• Increase: net income

• Decrease: dividends

1-19

Balance Sheet

• Measures financial position

• Reports assets, liabilities and shareholders’ equity

• Assets and liabilities are categorized Current and Long-term

1-20

Balance Sheet Categories

• Current assets Converted to cash or used within one year Cash, Short-term Investments, Accounts

Receivable, Inventory

• Long-term Property, plant, and equipment Intangible assets Investments Other

1-21

Balance Sheet Categories

• Current liabilities Due within one year of balance sheet date Accounts payable, salaries payable, taxes

payable, short-term borrowings

• Long-term liabilities Long-term notes payable, mortgage payable

1-22

Balance Sheet Categories

• Stockholders’ Equity Paid-in capital

• Common stock

Retained Earnings

1-23

Statement of Cash Flows

• Shows inflows and outflows of cash by category: Operating activities Investing activities Financing activities

1-24

Cash Flow Categories

• Operating Cash generated from day-to-day business

activities Related to selling goods and services to

customers

• Investing Cash invested in long-term assets Related to purchasing and selling plant assets

and investments1-25

Cash Flow Categories

• Financing How a company obtains resources to finance

business Related to long-term debt and equity (issuing

stock)

1-26

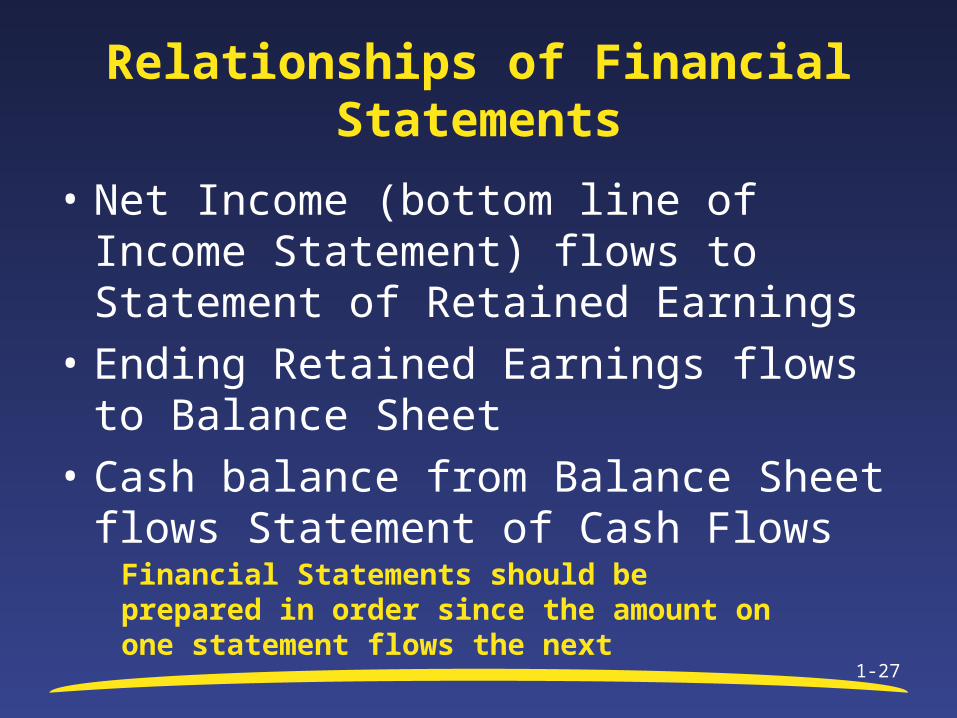

Relationships of Financial Statements

• Net Income (bottom line of Income Statement) flows to Statement of Retained Earnings

• Ending Retained Earnings flows to Balance Sheet

• Cash balance from Balance Sheet flows Statement of Cash Flows

1-27

Financial Statements should be prepared in order since the amount on one statement flows the next

INCOME STATEMENT

RETAINED EARNINGS STATEMENT

BALANCE SHEET

STATEMENT OF CASH FLOWS

NET INCOME

ENDING RETAINED EARNINGS

ENDING CASH

1-28

Reference

1-29

Harrison, W.T., Horngren, C.T. and Thomas, B. (2009). Financial accounting, 8th edition. Boston, MA: Pearson Prentice-Hall.

Questions?

1-30