Embed Size (px)

Citation preview

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 1/37

MSC MARKETING AND STRATEGY

IB9W90: THE DIFFUSION OF NEW PRODUCTS AND TECHNOLOGIES

FACTORS INFLUENCING THE ADOPTION AND USAGE OF INTERNET

BANKING IN NIGERIA

11TH APRIL 2010

UNIVERSITY NO: 0954927

WORD COUNT: 3803

All the work contained in this assignment is my own, original

unaided effort and conforms to the University’s guidelines on

plagiarism

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 2/37

Abstract

This study applies the Perceived Characteristics of Innovation (PCI)

framework, Moore and Benbasat (1991) which takes into

consideration, the Diffusion of Innovation (DoI) theory, Rogers

(1962) and the Technology Acceptance model, Davis (1989) to

identify possible factors that influence consumer adoption and

usage behaviour of Internet Banking (IB) in Nigeria. Individuals were

surveyed to reveal the actual influencers.

The results revealed that attitudinal factors mainly influenced

consumer acceptance of the technology. Other concerns that

included security gaps and basic operational challenges also

impacted on the tendency to adopt the innovation.

The paper further offers recommendations to ease consumers’

uncertainty with IB and by this;(delete the semi-colon) influence the

rate of diffusion of the innovation.

Keyword(s):

Internet banking; Nigeria; Adoption; Innovation

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 3/37

Table of Contents

Introduction (250) 235

The Nigerian Banking Industry in Recent Times (250) 229

An Overview of Internet banking: A Nigerian Perspective (250) 225

The Diffusion Profile of Internet banking in Nigeria (500)

Theoretical Background of Adoption and Usage of Innovations (250)

Factors Influencing Consumer Adoption of Internet banking

Technologies (750)

Research Methodology (250) 221

Data Findings and Analysis (250)

Recommendations for Nigerian Banks (250)

Conclusion (250)

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 4/37

List of Tables:

Table 1: Demographic Profile of Respondents

Table 2: Innovation Access and Usage

List of Figures:

Figure 1: User’s perception of Relative Advantage of Internet

Banking

Figure 2: User’s perception of Ease of Use of Internet Banking

Figure 3: User’s perception of Compatibility of Internet Banking

Figure 4: User’s perception of Visibility of Internet Banking

Appendices:

Appendix 1: Diffusion of Internet Banking Services Questionnaire

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 5/37

Introduction

Since the 1980’s, the global banking system has evolved quite

steadily with the adoption of Information Technology (IT) systems to

support their operations. The need for this form of home banking

was driven by a new competitive landscape in the banking industry

(Chou and Chou 2000). For banks to survive and compete

effectively, it became imperative that they adopted this technology

that increased convenience for the customers while also increasing

their efficiency.

While this technology has since advanced world-wide, particularly in

developed countries, the opposite seems to be the case in many

developing nations like Nigeria. In a region characterised by slow

technology response and adoption, IB was slow to be offered by the

banks and has had an even slower user response. Although all

existing Nigerian banks now offer IB features, consumers are yet to

accept the technology.

Scholars have made contributions that explain the diffusion of

innovation and identify typical consumer reactions to new products

and technologies. However, previous researches that have studied

IB diffusion mainly focus on North American and European

countries, (Mols 2000) failing to identify adoption factors that may

be unique in a different context. This study therefore seeks to

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 6/37

identify the factors that hinder or accelerate the adoption of IB in

Nigeria. Additionally, it seeks to offer recommendations on

strategies these banks could employ to accelerate consumer

acceptance of this self-service innovation.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 7/37

The Nigerian Banking Industry in Recent Times

Regulations guiding the Nigerian banking industry were only

developed in 1952 although some banking institutions were already

in operation. At its peak, there were about 90 banks in operation in

the county, (Ezoha 2005). These banks constituted of a few foreign

and many indigenous banks who invariable dominated the market.

Although the local banks were the clear leaders, they lacked public

confidence and were characterised as corrupt and unstable.

Thankfully (take it out as you no longer sound neutral), the

governing body for financial institutions, the Central Bank of Nigeria

(CBN) with the advent of democracy in the country, began able to

fulfil the duties to which they are mandated by law. Since 2004,

they have embarked on a series of reconstructive efforts to salvage

the reputation of the banking industry in the country whilst enabling

the institutions provide better services for their customers. These

reforms included creating a minimum capital base and a

standardised reporting period for all banks. This resulted in the

reduction of the number of banks to 24, through mergers,

acquisitions and dissolutions, and the creation of stronger banks

that are stronger and better positioned to serve customers in the

most efficient manner. More recently, the CBN completed audits of

the remainder banks to ascertain their financial health – it was

discovered that 11 banks were hit by liquidity inadequacies and

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 8/37

undercapitalisation. To resolve this, the governing bank replaced

the management of the affected banks and injected funds into the

sector while also making efforts to ensure loan defaulters were

accountable for their debts.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 9/37

Overview of Internet banking: A Nigerian Perspective

IB features the use of computers and other devices that are

connected to the Internet to conduct various banking transactions

such as viewing of bank balance, facilitating funds transfers and

payment of bills. The growth of IB has generally been quite rapid as

it has been identified as pertinent to the long-term survival of

banking institutions (Ovia 2001). This growth can be attributed to

the advantages it offers both consumers and the user bank itself. IB

helps the bank develop a direct relationship with its customers

without having to go through software companies, while from a

consumer perspective; it offers flexibility of connecting to their bank

from anywhere provided they have access to any Web-enabled

computer.

While this technology has since advanced world-wide, particularly in

developed countries, the opposite seems to be the case in many

developing nations like Nigeria. Although the major banks in the

country now offer IB services, this innovation has not achieved

expected adoption levels as the infrastructure in the country that

supports the technology is grossly inadequate. With issues such as

telecommunication problems and electricity outages, sensitive

banking transactions are usually done face-to face. Also with

Internet crime being very popular in the country, concerns about

security of transactions also hinder the use of this service channel.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 10/37

The Diffusion Profile of Internet banking in Nigeria

Unlike what would be expected, IB was not launched by a foreign

bank in Nigeria. Rather, it was introduced in Nigeria by the

technology focused First Atlantic Bank (now part of the First Inland

Bank Group) in 2000. As at the time, in order to make their services

more accessible to customers, most local banks had many

branches. With a total of 89 banks accounting for about 3017

branches nationwide (Ezoha 2005), these multiple branch systems

poised management challenges for the banks.

In a 2002 survey carried by the CBN, of the 89 banks in operation,

only 17 were offering IB. Although the technology had been

launched, a large majority of the banks either had not adopted the

innovation probably because they did not see the advantage the

service provided their businesses and customers or they could not

afford the necessary platforms to support the technology. Ezoha

(2005) observed that by 2005, there had still been no significant

improvements in the numbers of Nigerian banks that offered these

services rather their focus remained on other forms of electronic

banking. Furthermore, he attributed the slow rate of adoption by the

banks to the lack of operational infrastructure to support the

technology.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 11/37

Today, all Nigerian banks offer IB services, although at the very

basic level of interactivity with only a few of them providing

transaction services (Chiemeke 2006). He identifies security and

lack of adequate operational facilities as the major inhibitors to the

diffusion of the technology. It is believed nevertheless that IB will

spread more rapidly once issues relating to Internet fraud are

decidedly dealt with in the country.

Factors Impacting on the Diffusion Process

It has been established that the motivators for banks to begin to

offer IB services include increased globalisation, increased customer

sophistication and demands and recent regulatory inducements

(Bradley and Stewart 2002). However, certain factors either drive

the adoption by the banks or inhibit the diffusion of this process.

This chapter seeks to analyse the operating landscape of IB in

Nigeria.

Political Factors

The advent of democracy in 1999 and subsequent stability in the

political environment culminated in thriving business operations

nationwide that in turn encouraged local banks increase their

investments in ensuring efficient service delivery. Prior to this, the

volatility in the political arena and government left banks wary of

making huge infrastructural investments. Additionally, because the

democratised regulatory bodies introduced regulatory inducements

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 12/37

to ensure local banks met global operating standards the banks

were also driven to adopt IB.

Economic Factors

The recapitalisation of Nigerian banks at the turn of the decade

resulted in a healthier financial state for these institutions and

motivated efforts to operate at global standards. However, the

country remains ‘underbanked’ and majority of its population live on

less than a dollar a day. This high prevalence of poverty and lack of

utilisation of banking services has resulted in a largely

unsophisticated consumer base nationwide thus stifling the growth

of IB.

Social Factors

The proliferation of bank branches, through the ‘brick and mortar’

approach, has limited the need for IB – this explosive growth of

banks branches (with Automated Teller Machines) has promoted the

cash driven culture that continues to hamper the need for virtual

banking. In contrast to developed countries, the IB phenomenon is

still at its infancy largely due to the general notion the transactions

conducted over the internet remain susceptible to fraudulent

activities.

Technological Factors

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 13/37

The improvement in the financial state of banks has led to their

ability to invest tremendously in IT infrastructure capable of

supporting a wide array of capabilities. Up until recently, the

Internet access in the country was very slow because of obsolete

technology. However, the recent developments in the technology

sector that support high speed Internet needed for efficient

completion of online transactions have provided the banks an

opportunity to enhance their IB offerings.

Legal Factors

Although there are minimal legal requirements governing IB in

Nigeria, the industry remains confident in the ability of the

regulatory bodies’ protection and support – thus banks are willing to

offer these services to their consumers. On the other hand, the near

absence of legal requirements results in the slow pace of judicial

adjudication in financial related matters – such experiences remain

unpalatable to the banking public hence heightening their

scepticism about IB.

Environmental Factors

The dire state of infrastructure, particularly power, in Nigeria has

impeded the growth of IB. The instability of electricity nationwide

has reduced the effectiveness and negatively impacted on the

service experience. Adopting the innovation in a Nigerian bank will

automatically translate into huge investments in supporting

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 14/37

electricity generators; the same applies for the customers who

because of the epileptic nature of electricity are not guaranteed

access to the convenience IB offers.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 15/37

Theoretical Background of Adoption and Usage of Innovations

This chapter seeks to construct the theoretical framework for the

empirical study by analysing previous diffusion of innovation studies

and later linking it to the adoption of IB technologies in Nigerian

banks.

There have been many contributions to the knowledge on diffusion

of innovations. Rogers (1962) proposed a theory which suggested

that the decision to adopt an innovation was dependent on certain

factors that included the consumer perception of specific attributes

of the new product or technology. He listed this attributes as (1)

relative advantage, (2) compatibility, (3) complexity, (4) trialability,

and (5) observability. He believed that all adoption decisions were

based on the degrees of favourability of these attributes to the

consumer, i.e. a new innovation that is perceived to provide better

services than what is currently in use has a greater chance of being

adopted by users. Further expanding on the Diffusion of Innovation

(DoI) model, Davis (1989) proposed a model that suggested factors

that influenced consumer attitudes towards adoption of innovations

which included perceived usefulness and perceived ease of use of

the new product. Venkatesh and Davis (2000) further explained the

1989 model to include new influencers such as the degree to which

adoption was compulsory, the image of the producer(s) of the

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 16/37

innovation and the extent to which the results/advantages of the

new product could be demonstrated.

Moore and Benbasat (1991) however argued that although many of

these contributions were insightful, some factors in their models

were sometimes interrelated, e.g. relative advantage and

complexity which are conceptually similar to perceived usefulness

and ease of use. As past research has generally revealed a positive

correlation between adoption and characteristics of innovation, they

proposed the Perceived Characteristics of Innovation (PCI)

framework that provides a balanced opinion of all economic, social

and psychological drivers that could drive user adoption of a new

technology.

Research Objectives

This study aims to explore the factors that influence consumer

adoption of IB in Nigeria. It considers the dimensions of the PCI

framework in guiding the investigation, based on its robustness and

its incorporation of both the DoI and TAM models (Moore and

Benbasat 1991).

Research Methodology

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 17/37

The study employs primary and secondary data. The secondary data

was retrieved using information from various published sources. The

primary data was collected by a structured survey. The survey was

drafted in an electronic format that was conducted to meet the

research objectives. As the study sought to explore consumer

adoption of IB in Nigeria, it was appropriate to survey a sample of

bank account owners in the country to test the hypothesis.

Company employees were chosen for this survey as it is customary

in the country to pay salaries into workers accounts, as such, this

sample group are expected to not only own bank accounts, but also

have regular access to the Internet.

The questionnaires were sent via email to 400 people living in

Lagos, mainly because as the central business district of the

country, it has all the social amenities needed to support IB

technologies. A total of 127 responses (response rate of 31.75%)

were received with 121 suitable for the data analysis.

The questionnaire consists of 30 questions that include three

sections. The first section collects general information about the

user’s Internet access and usage, banking habits and seeks to

determine whether or not the respondent has embraced the

innovation, while the second section makes inquiries about the

respondent’s perceptions of the characteristics of IB using factors

from Moore and Benbasat (1991) revision of the DoI and TAM

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 18/37

models. Finally, the third section goes further to enquire about

actual experiences with IB and further explores reasons for adoption

or non-adoption.

A copy of the questionnaire is attached in Appendix 1.

Data Findings and Analysis

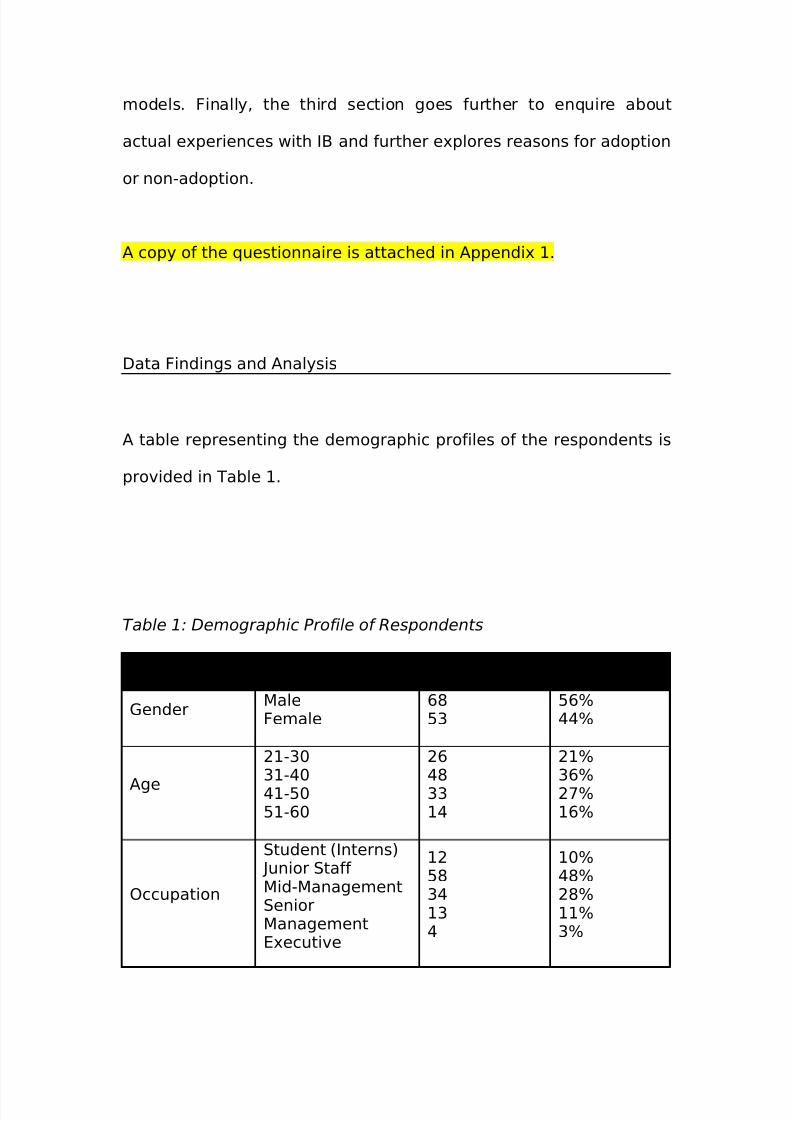

A table representing the demographic profiles of the respondents is

provided in Table 1.

Table 1: Demographic Profile of Respondents

Variable Frequency Percentage

GenderMaleFemale

6853

56%44%

Age

21-3031-4041-5051-60

26483314

21%36%27%16%

Occupation

Student (Interns)Junior Staff Mid-ManagementSeniorManagementExecutive

125834134

10%48%28%11%3%

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 19/37

Research has found that demographics could influence user

acceptance of technological innovations (Harrison et al 1992). For

instance, the findings of these studies revealed that respondents

within the higher age bracket tended to reject IB- they seemed

averse to accepting anything unfamiliar.

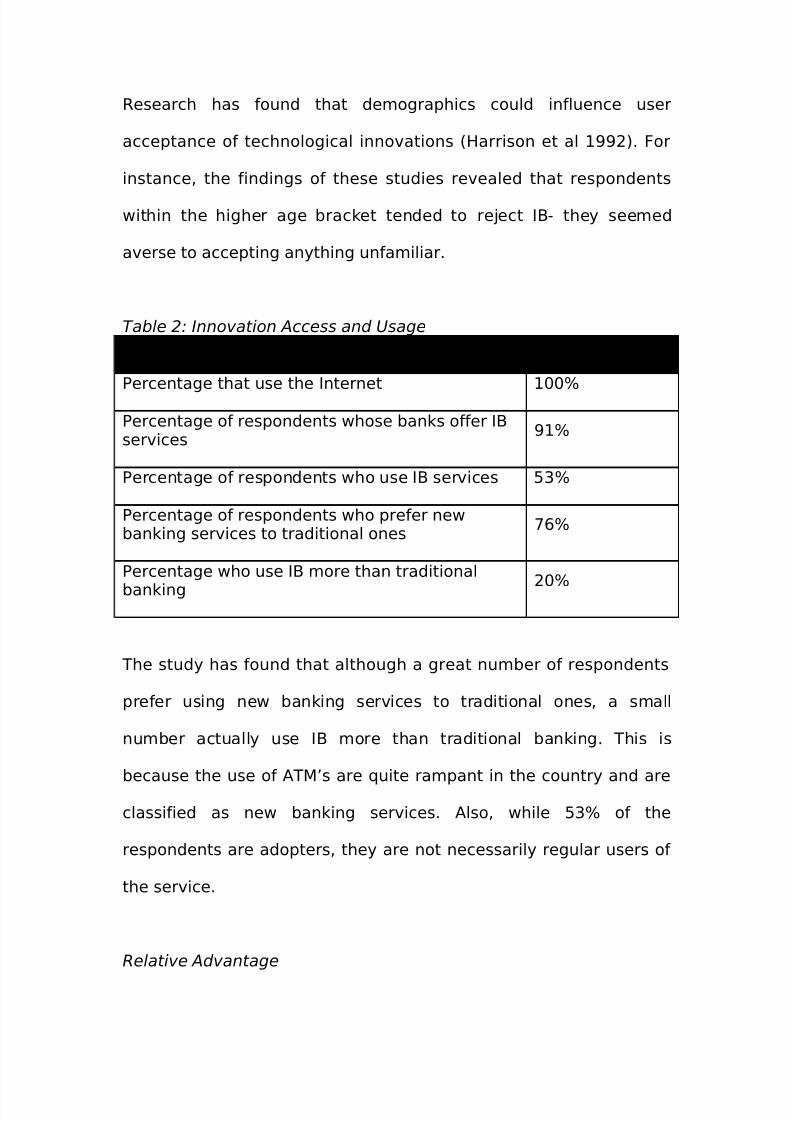

Table 2: Innovation Access and Usage

PercentagePercentage that use the Internet 100%

Percentage of respondents whose banks offer IBservices

91%

Percentage of respondents who use IB services 53%

Percentage of respondents who prefer newbanking services to traditional ones

76%

Percentage who use IB more than traditional

banking 20%

The study has found that although a great number of respondents

prefer using new banking services to traditional ones, a small

number actually use IB more than traditional banking. This is

because the use of ATM’s are quite rampant in the country and are

classified as new banking services. Also, while 53% of the

respondents are adopters, they are not necessarily regular users of

the service.

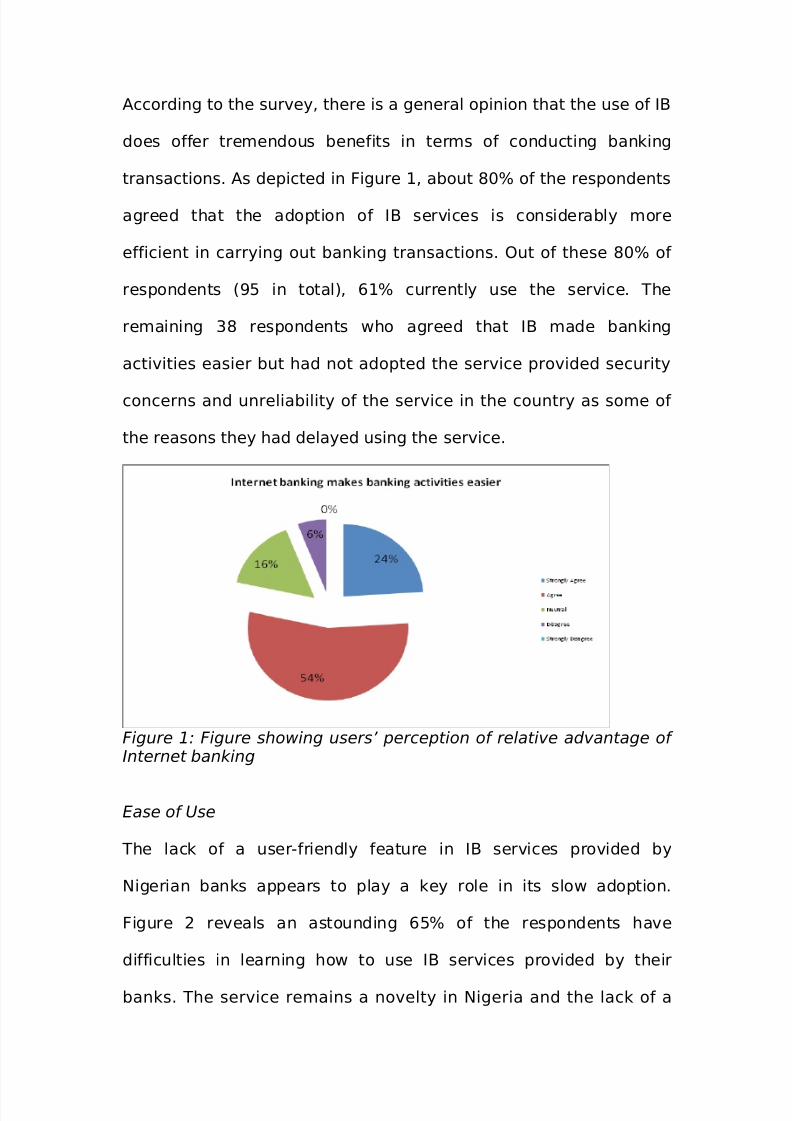

Relative Advantage

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 20/37

According to the survey, there is a general opinion that the use of IB

does offer tremendous benefits in terms of conducting banking

transactions. As depicted in Figure 1, about 80% of the respondents

agreed that the adoption of IB services is considerably more

efficient in carrying out banking transactions. Out of these 80% of

respondents (95 in total), 61% currently use the service. The

remaining 38 respondents who agreed that IB made banking

activities easier but had not adopted the service provided security

concerns and unreliability of the service in the country as some of

the reasons they had delayed using the service.

Figure 1: Figure showing users’ perception of relative advantage of Internet banking

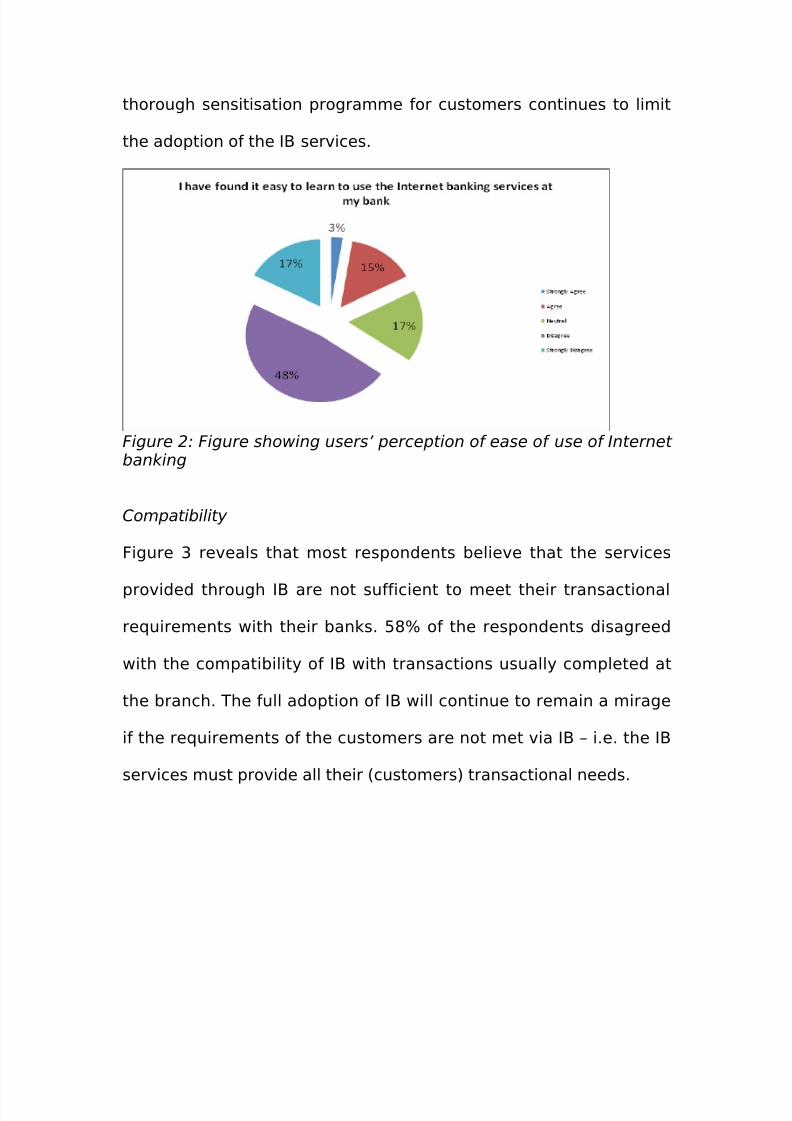

Ease of Use

The lack of a user-friendly feature in IB services provided by

Nigerian banks appears to play a key role in its slow adoption.

Figure 2 reveals an astounding 65% of the respondents have

difficulties in learning how to use IB services provided by their

banks. The service remains a novelty in Nigeria and the lack of a

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 21/37

thorough sensitisation programme for customers continues to limit

the adoption of the IB services.

Figure 2: Figure showing users’ perception of ease of use of Internet banking

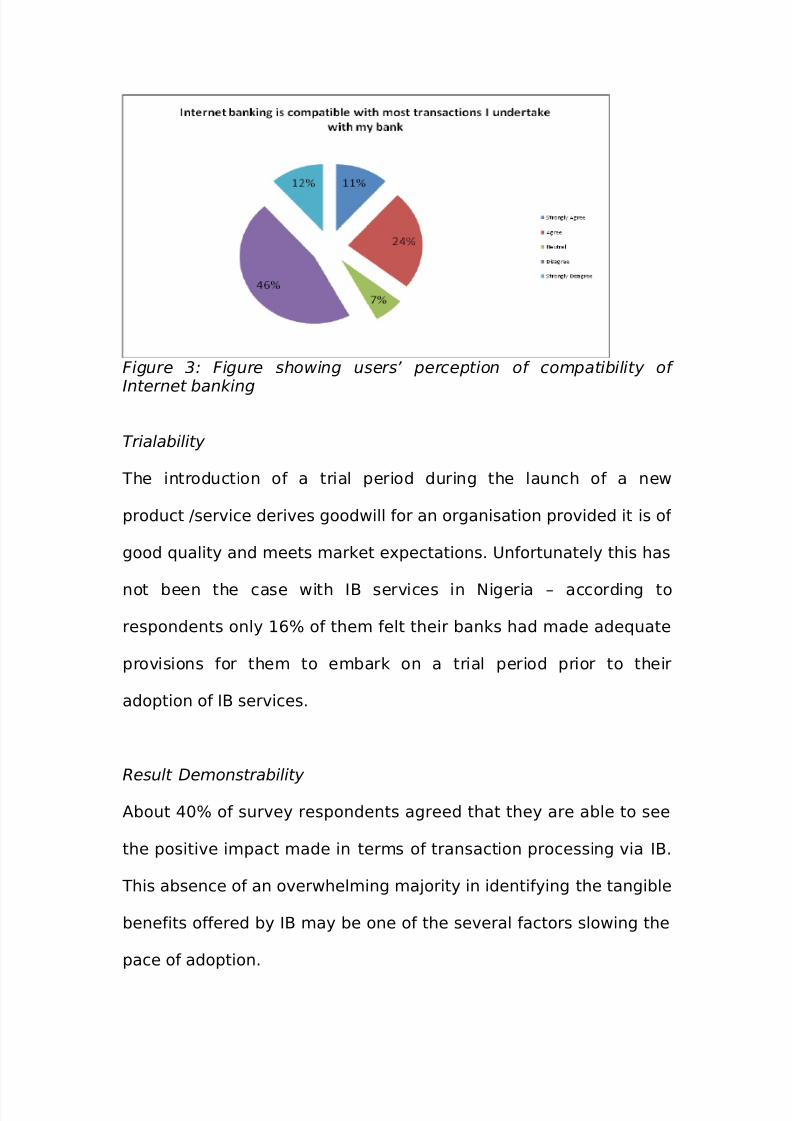

Compatibility

Figure 3 reveals that most respondents believe that the services

provided through IB are not sufficient to meet their transactional

requirements with their banks. 58% of the respondents disagreed

with the compatibility of IB with transactions usually completed at

the branch. The full adoption of IB will continue to remain a mirage

if the requirements of the customers are not met via IB – i.e. the IB

services must provide all their (customers) transactional needs.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 22/37

Figure 3: Figure showing users’ perception of compatibility of

Internet banking

Trialability

The introduction of a trial period during the launch of a new

product /service derives goodwill for an organisation provided it is of

good quality and meets market expectations. Unfortunately this has

not been the case with IB services in Nigeria – according to

respondents only 16% of them felt their banks had made adequate

provisions for them to embark on a trial period prior to their

adoption of IB services.

Result Demonstrability

About 40% of survey respondents agreed that they are able to see

the positive impact made in terms of transaction processing via IB.

This absence of an overwhelming majority in identifying the tangible

benefits offered by IB may be one of the several factors slowing the

pace of adoption.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 23/37

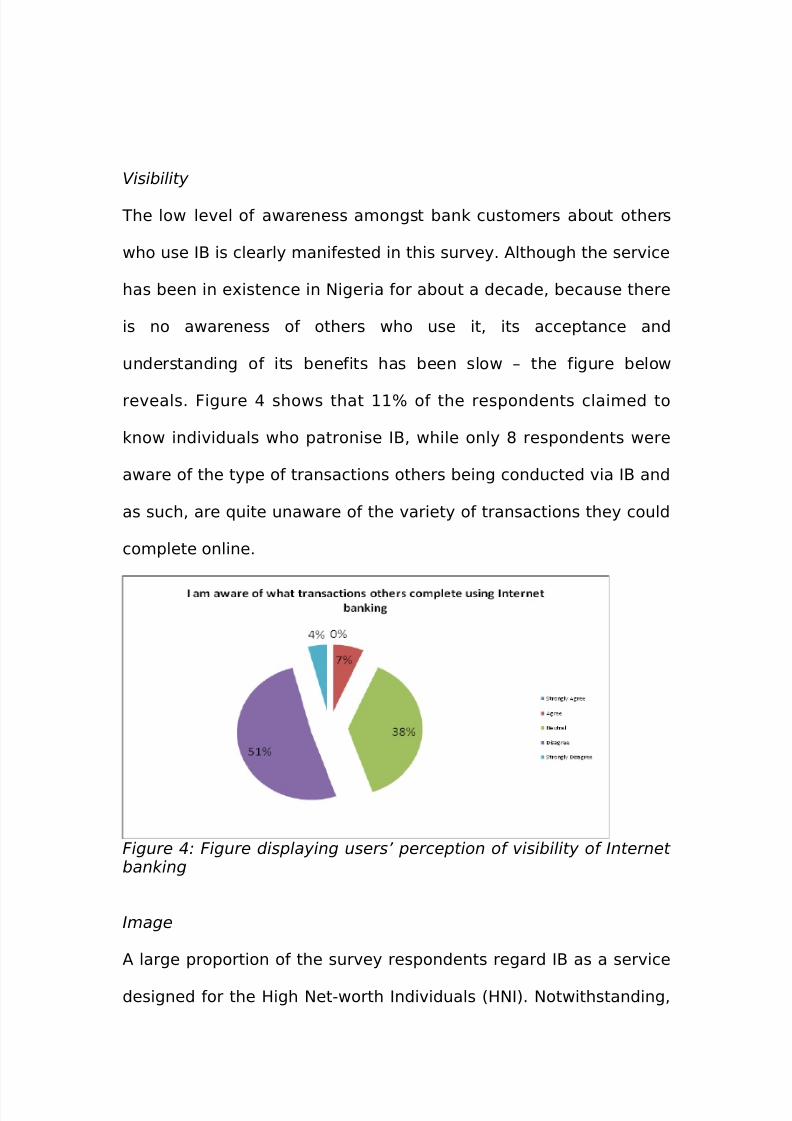

Visibility

The low level of awareness amongst bank customers about others

who use IB is clearly manifested in this survey. Although the service

has been in existence in Nigeria for about a decade, because there

is no awareness of others who use it, its acceptance and

understanding of its benefits has been slow – the figure below

reveals. Figure 4 shows that 11% of the respondents claimed to

know individuals who patronise IB, while only 8 respondents were

aware of the type of transactions others being conducted via IB and

as such, are quite unaware of the variety of transactions they could

complete online.

Figure 4: Figure displaying users’ perception of visibility of Internet banking

Image

A large proportion of the survey respondents regard IB as a service

designed for the High Net-worth Individuals (HNI). Notwithstanding,

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 24/37

utilisation of this service is not believed to result in any form of

preferential treatment by the bank – with over 60% of the

respondents supporting the former notion only 24% of respondents

supported the latter. A key insight from this is the bank’s passive

approach in ensuring a wider reach for IB services – the banks

appear to be targeting a certain class of customers to utilise IB

services.

Voluntariness

Nigerian banks have not seen any urgency in ensuring that majority

of their customers use IB. Only 3% of survey respondents stated

that their banks have begun taking steps to ensure that the usage

of IB is mandatory for all customers. This is further buttressed by

66% of respondents being of the opinion that their bank does not

require them to use IB. It may be argued that to drive the adoption

of IB in Nigeria, banks may need to compel their customers to utilise

the service in conducting their transactions. Such measures may be

viewed as draconian but if they are applied with suitable incentives

the adoption of IB in Nigeria may witness unprecedented growth.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 25/37

Factors Influencing the Adoption of Internet banking Technologies in

Nigeria

The survey was able to highlight certain factors outside of the PCI

framework that were unique to the Nigerian context and affecting

adoption and usage of the service. The study found that Nigerian

consumers face certain potential sources of uncertainty in the

process of adopting a new technology that include:

i. Risk of Fraud: Many consumers hesitate to adopt IB in the

country because they are uncomfortable with the levels of

security that are offered. Since internet fraud is quite rampant

in the country, it is difficult to convince them that operating

their accounts online will not attract cyber hackers.

ii. Operational Failures: Issues such as epileptic power failure

and inaccessibility of high speed internet access in many parts

of the country also cause consumers to delay adopting the

technology.

iii. Lack of Technical Support: Some users complain about the

unreliability of the IB service offerings in the country

protesting that the sites usually experience downtimes that

are not quickly resolved. As a result of the instances of poor

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 26/37

support once an error was made when using IB, one adopter

has since stopped using the service.

iv. Incompatibility with lifestyles: Another major factor that

hinders the spread of IB in the country is the lack of

compatibility with the Nigerian lifestyle which is essentially a

cash driven nation. As such, the functions of the service are

often limited to monitoring and transfer activities alone.

v. Lack of Awareness: Although all banks in Nigeria now offer

some form of IB, some respondents were unaware that their

banks were offering the service. Some users are also unaware

of the many uses and benefits of IB, and as such have not

adopted the service.

It is the responsibility of the banks to address these uncertainties

that are experienced by the consumers so as to increase the rate

at which they accept the service.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 27/37

Recommendations for Nigerian Banks

At present, most Nigerian customers have not gone beyond using

their bank’s website solely to retrieve general information especially

as their banks are yet to fully offer and promote transaction support

on their websites. With the risk of fraud complicating the IB

environment, lack of public trust in the sector, and poor access to

requisite amenities (Ezoha 2005), it may take an age for the country

to enjoy the same level of acceptance and use as other developed

nations. Banks need to make more accurate conclusions regarding

how their technology driven channels will be received (Gounaris and

Koritos 2008) before making investments in deploying them as in

the case of Nigeria.

However, banks can take actions to ease common IB user

uncertainties. Some of these actions include:

i. Ensure security of their sites by regularly purchasing

software that prevents and detects intrusion.

ii. Engage good public relations teams to spread the word of

the services they offer and emphasize its safety and other

benefits.

iii. Ensure their marketing communications is targeted at the

right demographics.

iv. Provide training and testing scenarios at branches for bank

customers who seem interested in using the service

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 28/37

v. Ensure their websites are user friendly to ensure the

customer is able to navigate easily

vi. Train world-class support teams that are able to guide

users through when they come across glitches

vii. Offer incentives for service users, e.g. free internet service

for one month to regular users.

viii. Provide free access in public locations and bank branches

(Jaruwachirathanakul and Fink 2005).

ix. Attempt to increase service uses and value by

collaborating with other banks and e-commerce merchants.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 29/37

Bibliography

• Agboola, A.A. (2006). Electronic Payment Systems and Tele-

Banking Services in Nigeria. Journal of Internet banking and

Commerce, 11(3).

• Bradley, L. and Stewart, K. (2002). A Delphi study of the

drivers and inhibitors of Internet banking. International Journal

of Bank Marketing, 20(6), pp. 250-260.

• Chan, S. C. and Lu. T. M. (2004). Understanding Internet

banking adoption and use behaviour: a Hong Kong

perspective. Journal of Global Information Management , 12

(3), pp. 12-43.

• Chiemeke, S.C. (2006). The Adoption of Internet banking in

Nigeria: An Empirical Investigation. Journal of Internet banking

and Commerce, 11(3).

• Chou, D. C. and Chou, Amy Y.(2000). A Guide to the Internet

Revolution in Banking. Information Systems Management ,

17(2), pp. 1 — 7.

•Davis, F. D. (1989). Perceived usefulness, Perceived Ease of

use and user acceptance of information technology. MIS

Quarterly , 16(2), pp. 319-340.

• Ezeoha, A. E (2005). Regulating Internet banking in Nigeria,

Problem and Challenges-Part1. Journal of Internet banking

and Commerce, 10(3). Retrieved 16th April, 2010 from

http://www.arraydev.com/commerce/jibc/.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 30/37

• Gerrard, P. and Cunningham, J.B. (2003). The diffusion of

Internet banking among Singapore consumers. International

Journal of Bank Marketing, 21(1), pp. 16-28.

• Gounaris, S. and Koritos, C. (2008). Investigating the drivers of

Internet banking adoption decision: A comparison of three

alternative frameworks. International Journal of Bank

Marketing, 26(5), pp. 282-304.

• Harrison, A.W. and Rainer, R.K. (1992). The influence of

individual differences on skill in end-user computing. Journal

of Management Information Systems, 9(1), pp. 93-111.

• Jaruwachirathanakul, B. and Fink, D. (2005). Internet banking

adoption strategies for a developing country: the case of

Thailand. Internet Research, 15(3), pp. 295-311.

• Jayawardhena, C. and Foley, P. (2000). Changes in the

banking sector – the case of Internet banking in the

UK. Internet Research: Electronic Networking Applications and

Policy , 10(1), pp.19-31.

• Mols, N. P. (2000). The Internet and Services marketing – the

case of Danish retail banking. Internet Research: Electronic

Networking Applications and Policy , 10 (1), pp. 7-18.

• Moore, C. G. and Benbasat, I. (1991). Development of an

instrument to measure the perceptions of adopting an

information technology innovation. Information Systems

Research, 2(3), pp. 192-222.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 31/37

• Ovia, J. (2001). Internet banking: Practices and Potentials in

Nigeria. A paper at the conference organized by the Institute

of Chartered Accountants of Nigeria (ICAN), Lagos, September

5, 2001.

• Rogers, E.M. (1962). Diffusion of Innovations. The Free Press:

New York.

• Rogers, E.M. (1983). Diffusion of Innovations. 3rd Edition. The

Free Press: New York.

• Rogers, E.M. (1995). Diffusion of Innovations. 4th Edition. The

Free Press: New York, NY.

• Salawu, R.O. and Salawu, M.K. (2007). The Emergence of

Internet banking in Nigeria: An Appraisal. Information

Technology Journal, 6(4), pp. 490-496.

• Singhal, D. and Padhmanabhan, V. (2008). A Study on

Customer Perception Towards Internet Banking: Identifying

Major Contributing Factors. The Journal of Nepalese Business

Studies, 5(1), pp. 101-111.

• Tan, M. and Teo, T., S., H. (2000). Factors influencing the

adoption of Internet banking. Journal of the Association for

Information Systems, 1(5), pp. 1-42.

• Venkatesh, V. and Davis, F. (2000). A theoretical extension of

the technology acceptance model: Four longitudinal field

studies. Management Science, 46(2), pp. 186-204.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 32/37

• Venkatesh, V., Morris, M.G., Davis, G.B., Davis, F.D. (2003).

User acceptance of information technology: toward a unified

view. MIS Quarterly , 27(3), pp.425-78.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 33/37

Appendix 1_____________________________________________________________________

THE DIFFUSION OF INTERNET BANKING SERVICES QUESTIONNAIRE_____________________________________________________________________ _________________

This survey is designed to study the rate of diffusion of Internetbanking services in Nigeria. Data collected will be used to determinethe factors that influence user adoption of the innovation.

PERSONAL DETAILS(These details are only for statistical purposes and will remainconfidential)Name:

_____________________________________________________________________ _________ Gender

_____________________________________________________________________ Age

_____________________________________________________________________ _______ Occupation:

_____________________________________________________________________ __ Telephone No:

_______________________________________________________________ Email Address:

_______________________________________________________________

INSTRUCTIONS FOR COMPLETING THE QUESTIONNAIREThis questionnaire is in electronic format to facilitate its completionand enable the responses be automatically prepared for analysis.Questions 1 to 23 - Please respond by ticking or highlighting therelevant boxQuestion 24 to 25 – Please respond by filling out the space provided.

Thank you for completing this survey, if you have any questionsregarding its completion please, kindly contact Toni Dada by phoneon (234) 8022951621. Please return responses [email protected] or [email protected]

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 34/37

SECTION 1

1. Are you computer literate?

Yes No

2. How often do you use the internet?

Daily 2 or 3 times a Week Less that 3 times a

week

At least once a month Never

3. Do you currently own a bank account in Nigeria?

Yes No

4. How long have you had this bank account?

Less than a year Between 1-5 years Between6-10 years

More than 10 years Not Applicable 5. How frequently do you visit your bank for transactions?

Daily 2 or 3 times a Week Less that 3 times a

week

At least once a month Never

6. What transactions do you most frequently carry out in yourbank?

Depositing into my account Transfers into others’accounts

Check bank balance Make bill payments Withdraw

cash

Make enquiries Others (please specify) -____________________________

7. My bank is in close proximity to my home, office or school?

Yes No

8. My bank offers Internet banking services.Yes No Not Sure

9. My bank has done an excellent job in promoting its Internetbanking services and its advantages.

Strongly Agree Agree Neutral Disagree

Strongly Disagree

10. I prefer to use new banking services rather thantraditional ones.

Strongly Agree Agree Neutral Disagree

Strongly Disagree

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 35/37

11. I use the Internet banking services that my bank offers.

Strongly Agree Agree Neutral Disagree

Strongly Disagree

12. I use Internet banking services more than I visit the bank.

Strongly Agree Agree Neutral Disagree Strongly Disagree

SECTION 2

13. Internet banking makes banking activities easier

Strongly Agree Agree Neutral Disagree

Strongly Disagree

14. The experience with Internet banking is considerably betterthan that of traditional banking

Strongly Agree Agree Neutral Disagree

Strongly Disagree

15. I have found it easy to learn to use the Internet bankingservices at my bank

Strongly Agree Agree Neutral Disagree

Strongly Disagree

16. I am able to use Internet banking to perform the transactions Iwant to

Strongly Agree Agree Neutral Disagree

Strongly Disagree

17. Internet banking is compatible with my lifestyle as I haveaccess to my account on the go

Strongly Agree Agree Neutral Disagree

Strongly Disagree

18. Internet banking is compatible with most transactions Iundertake with my bank

Strongly Agree Agree Neutral Disagree

Strongly Disagree

19. Internet banking users are regarded highly in my bank

Strongly Agree Agree Neutral Disagree

Strongly Disagree

20. Internet banking users are generally prestigious or high net-

worth individualsStrongly Agree Agree Neutral Disagree

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 36/37

Strongly Disagree

21. I would find it easy relating the benefits or demerits of Internet banking to others

Strongly Agree Agree Neutral Disagree

Strongly Disagree

22. I have found it easy to evaluate the results of using Internetbanking

Strongly Agree Agree Neutral Disagree

Strongly Disagree

23. I know others who use Internet banking

Strongly Agree Agree Neutral Disagree

Strongly Disagree

24. I am aware of what transactions others complete usingInternet banking

Strongly Agree Agree Neutral Disagree

Strongly Disagree

25. I can try out using Internet banking before deciding to use it

Strongly Agree Agree Neutral Disagree

Strongly Disagree

26. My bank has made adequate provisions to guide my trial of Internet banking

Strongly Agree Agree Neutral Disagree

Strongly Disagree 27. My bank does not need me to use Internet banking

Strongly Agree Agree Neutral Disagree

Strongly Disagree

28. My bank has made the use of Internet banking compulsory for

all customersStrongly Agree Agree Neutral Disagree

Strongly Disagree

SECTION THREE

29. Have you had a particularly bad or good experience withInternet banking services in Nigeria? Please discuss.

8/7/2019 0954927_Diffusion of Innovation Coursework_v7

http://slidepdf.com/reader/full/0954927diffusion-of-innovation-courseworkv7 37/37

__________________________________________________________________

__________________________________________________________________

________________________________

30. Are there any additional comments you will like to include toexplain why you have, (or haven’t) embraced the Internetbanking services offered by your bank, e.g. you don’t possesssufficient computer skills or secure internet access?

__________________________________________________________________

__________________________________________________________________

________________________________