Embed Size (px)

Citation preview

2008 2008 vs vs 20092009

!! Half year 2008 Half year 2008 vs vs half year 2009half year 2009!! WealthWealth!! Inflation / ConsumptionInflation / Consumption!! Consumer concernsConsumer concerns!! BrandingBranding!! MediaMedia!! EnvironmentEnvironment

Consumer Trends AgendaConsumer Trends Agenda

GDP growth = 8.5% - OctFDI (US Billion) = $45 B - OctInflation (CPI) = 22% - OctExports** = $48 B - SeptOverseas remittance = $8 B - DecConsumer confidence = 94%

(economy same/ better in next 12 months)Ad expenditure growth = 16%FMCG growth* = 20%Modern trade growth* = 27%Internet users growth = 23%Car sales^ = 30%

2009200920082008

Half year 2008 Half year 2008 vs vs half year 2009 Comparisonhalf year 2009 Comparison

Source: GSO /TNS * Value growth / TNS Worldpanel ^VAMA – end of August

Overall growth spend at half year is down by 25% compared to 2008While economic indices show a decline of over 50% in growth

" GDP growth = 4.5% - Oct" FDI (US Billion) = $23 B - Oct" Inflation (CPI) = 4.5% - Oct" Exports** = $42 B - Sept" Overseas remittance = 6.7 B - Dec" Consumer confidence = 86%

(economy same /better in next 12 months)" Ad expenditure growth= 23%" FMCG growth* = 8%" Modern trade growth* = 10%" Internet user Growth = 25%" Car sales^ = -19%

**Exports = End of September 09

Vietnam by the numbers - half year 2008 Vietnam by the numbers - half year 2008 vs vs 20092009Inflation down by 80%

Ad spend growth up by 23%

Internet growth up by 20%

GDP down by half

FDI down by half

Exports down by 15%

FMCG growth down 12%

Modern trade growth down by 17%

Car sales are down by 19%

As FDI & Exports accounted for US $120 Billion of the VN economy in 2008, VN will struggle moving forward, with only US $80 Billion in 2009 (est.)

Half year comparison

Wealth TrendsWealth Trends

Vietnam’s GDP has doubled in 4 years, but only by 5% in 2009

GDP per capita evolution - USDGDP per capita evolution - USD

Source: GSOVN

289

402 440

552

725

835

1,024 1,075

0

200

400

600

800

1,000

1,200

1995 2000 2002 2004 2006 2007 2008 2009 Est.

In USD

1,024

5

7

20

24

30

14

27

37

34

27

26

31

20

20

23

12

11

5

6

12

32

18

12

11

5

3

2

4

5

3

8

4

2

0% 20% 40% 60% 80% 100%

2008

2006

2004

2001

1999

SEC F SEC E SEC D SEC C SEC B SEC A SEC A+

HCMC Declared Monthly Household IncomeHCMC Declared Monthly Household Income

Source: TNS VietCycle: 1999-2008Base: N = 1,000

SEC Income Scale A1 = US $1,200 + A = US $801 -1,200 B = US $401 - 800 C = US $400 - 276 D = US $181 - 275 E = US $126 - 180 F = US $ 45 - 125

A-B-C SEC has more than doubled in the last 4 years (+59%)

1

6

26

46

40

7

26

44

36

37

35

38

20

11

14

23

10

4

3

5

31

18

5

3

3

1

0

1

1

1

2

2

0% 20% 40% 60% 80% 100%

2008

2006

2004

2001

1999

SEC F SEC E SEC D SEC C SEC B SEC A SEC A+

Hanoi Declared Monthly Household IncomeHanoi Declared Monthly Household Income

SEC Income Scale A1 = US $1,200 + A = US $801 -1,200 B = US $401 - 800 C = US $400 - 276 D = US $181 - 275 E = US $126 - 180 F = US $ 45 - 125

Source: TNS VietCycle: 1999-2008Base: N = 1,000

A-B-C SEC has almost doubled in the last 2 years

Consumer ConcernsConsumer Concerns

Quality of product and value for moneyQuality of product and value for money

The Chinese Milk scare could be felt for years &will make consumers more quality conscious

64%

48%

39%

35%

17%

Health of my family

Personal health

Unemployment

Financial stability

Global recession TNS Consumer Poll - Jan. 09

Vietnamese main fears in life - 2009Vietnamese main fears in life - 2009

Health still tops consumers main fears, followed by money matters

My personal standard of living forecastMy personal standard of living forecast

Source: TNS VietCycle 2006 / 2008 & TNS Consumer Confidence Poll – Jan. 09

Vietnamese personal standard of living forecast for the next 12 months has dropped from 70% forecasting a better living standard

in September 2008 to only 36% in January 2009

9

16

18

27

54

48

46

25

32

16

4

2

1

1

0

0

0

TNS Consumer Poll -Jan. 09

TNS VietCycle - Sept. 08

TNS VietCycle - Nov. 06

Far better A little better Same A little worse Far worse Don't know

Will you reduce spending in 2009?Will you reduce spending in 2009?

Yes

52%

No

46%

Don’t

know

2%

Source: TNS Consumer Confidence Poll – Jan. 09

Over half of consumers shall reduce their monthly spending in 2009

44

29

28

28

25

23

23

23

16

12

4

54

69

70

69

71

73

73

74

81

76

72

2

2

2

3

4

4

4

3

4

12

23

0

0

0

0

0

0

1

1

Entertainment & dining out

Home appliances (Wash machine, TV Hifi, etc)

Household utilities

Personal equipment (mobile phone, laptop ,Etc)

Communications telephone/ fax/ email

Personal care products

Transportation

House hold care products

Food & beverages products

Health care products/ services

Education

Less Same More Don't know

Consumers spending reduction in 2009?Consumers spending reduction in 2009?

Source: TNS Consumer Confidence Poll – Jan. 09

MajorDecrease

Less than25%

Stable

Base: All n = 500

Only education and healthcare seem to be unaffectedby the Global economic recession

Brand impactBrand impact

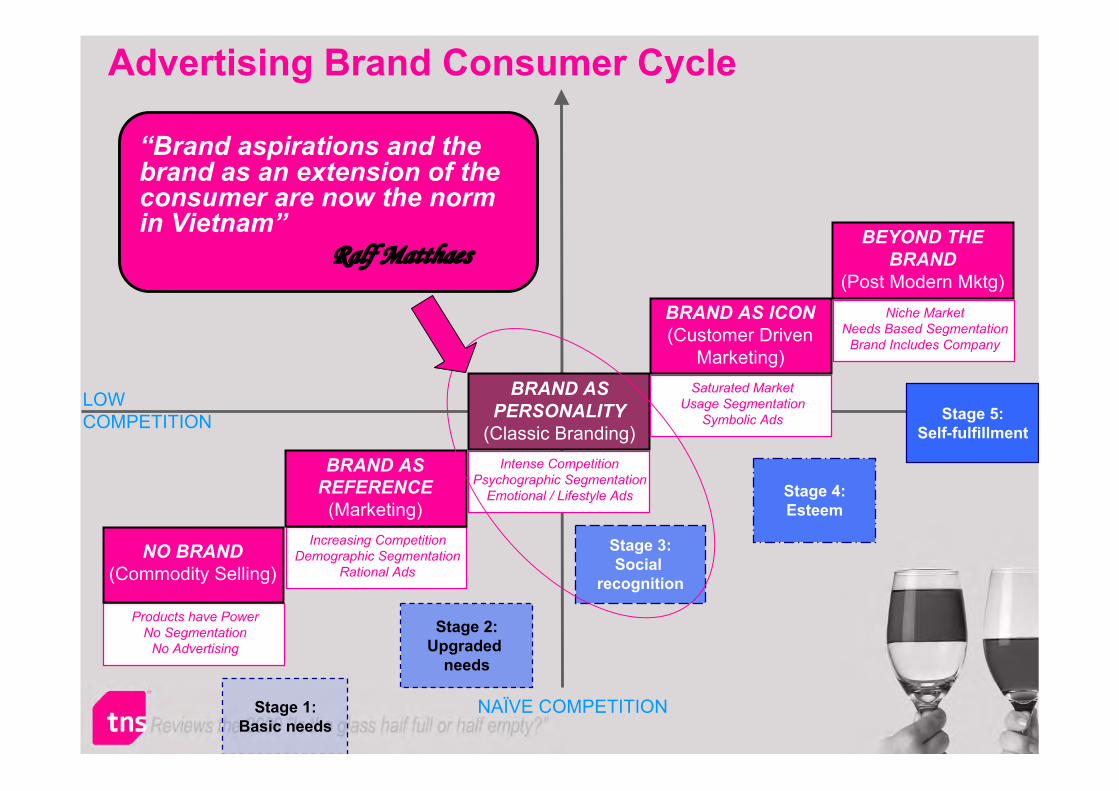

BRAND ASPERSONALITY

(Classic Branding)Intense Competition

Psychographic SegmentationEmotional / Lifestyle Ads

Saturated MarketUsage Segmentation

Symbolic Ads

BRAND AS ICON(Customer Driven

Marketing)

BEYOND THEBRAND

(Post Modern Mktg)Niche Market

Needs Based SegmentationBrand Includes Company

Increasing CompetitionDemographic Segmentation

Rational Ads

BRAND ASREFERENCE

(Marketing)

Products have PowerNo Segmentation

No Advertising

NO BRAND(Commodity Selling)

Stage 1:Basic needs

Stage 2:Upgraded

needs

Stage 3:Social

recognition

Stage 5:Self-fulfillment

Stage 4:Esteem

Advertising Brand Consumer CycleAdvertising Brand Consumer Cycle

LOWCOMPETITION

NAÏVE COMPETITION

“Brand aspirations and thebrand as an extension of theconsumer are now the normin Vietnam”

Ralf Matthaes

Vietnamese Brand PerceptionsVietnamese Brand Perceptions

International / healthy / badge value brands and brands ofhigh quality are still much more preferred by VN consumers

Source: VietCycle 2008- September 2008

32

39

50

56

56

71

73

81

0 10 20 30 40 50 60 70 80 90

There are no real differences between the brands available in the market

I prefer local Vietnamese brands

Vietnamese brands are as good as international brands

I prefer to buy well-know brands

I like to use the brand which shows my success

I’m willing to pay more for higher quality brands

I prefer brands with a health / environmental focus

I am equally concerned about Price and quality

Vietnamese brand perceptions are changingVietnamese brand perceptions are changing“My children will be veryintelligent and grow-up fasteras I feed her by a good qualitypowder milk. I feel that I am agood mother”

“I always choose the most expensivedetergent which I think it has the bestquality and good for my families clothes.I feel happy when my husband says toothers that I am a good housewife”

Source: TNS 2007-2008 FGD’s

“People say that I am a modernmother because I choose goodquality brands for my baby. It shows

my great love for my children”

RECOGNITIONRECOGNITION

SocialSocial

10 fastest growing brands 10 fastest growing brands –– Half year - 2009 Half year - 2009

Source: TNS Worldpanel

In 2007, 2 of the fastest growing brands were, Vietnamese, in 2008 = 4 and thus far in 2009 = 8 were Vietnamese Thus, meaning thatVietnamese brands and the Gov’t initiative to buy local is working

Value Share change%Market share movement

25%

22%

15%

12%

10% 10% 9% 9%8% 7%

VFRESH(Soya milk)

CHINSU(NAM NGU)

KOTEX(Pantyliner)

VFRESH(Fruit juice)

STING TRANGTIEN

TUONG AN(Margarine)

FAMI (Soyamilk)

DIELACANPHA 1

VINAMILK(UHT)

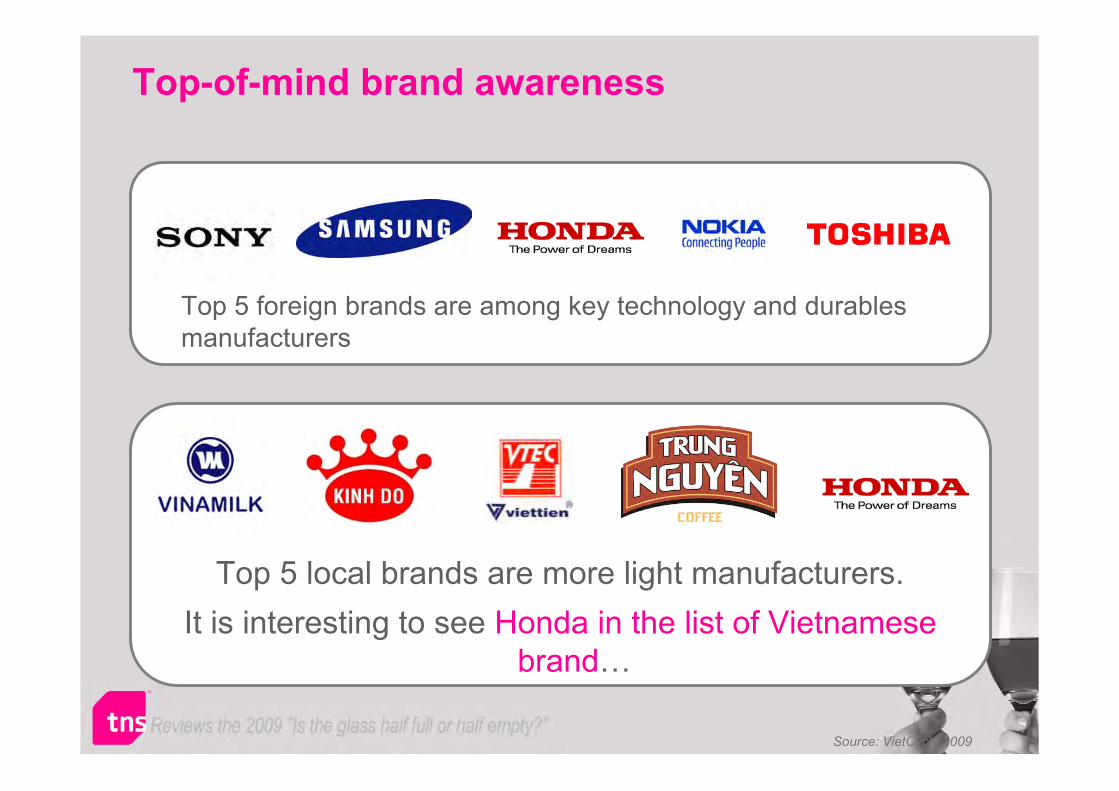

Top-of-mind brand awareness

Top 5 foreign brands are among key technology and durablesmanufacturers

Top 5 local brands are more light manufacturers.It is interesting to see Honda in the list of Vietnamese

brand…

Source: VietCycle 2009

Perception of luxury - 2009

Car Car 54%54%

Diamond Diamond 31%31%

LaptopLaptop9%9%

Home Home theatretheatre

9%9%

Overseas Overseas holidayholiday

11%11%

HouseHouse7%7%

Plasma Plasma TVTV

13%13%

Security Security 9%9%

Dish washerDish washer15%15%

Gold Gold JewelryJewelry

8%8%

Cars and Diamonds areseem as true luxury items

Source: VietCycle 2009

Internet Internet usus@@gege

Top 20 countries - internet usersTop 20 countries - internet users

Source: WorldInternetstats.com – July 2009

@

Vietnam is now the 18th most active user of the internet globally.

20

20.02

21.53

23

23.99

25

26.50

27.40

28.63

29.14

37.47

38

42.05

48.76

55.22

67.51

81

94

227.63

338

Argentina

Poland

Vietnam

Iran

Canada

Indonesia

Turkey

Mexico

Spain

Italy

Korea South

Russia

France

United Kingdom

Germany

Brazil

India

Japan

United States

China

3

8 9

21

34

0

10

20

30

40

1999 2001 2004 2006 2008

In-home Internet penetration In-home Internet penetration (Hanoi & HCMC)(Hanoi & HCMC)

Source: TNS VietCyle – 1999-2008 – HCMC & Hanoi

With 1 in 3 urban homes connected to internet, Internet based advertising will experience steady growth

Base: Past month internet users aged 15+ across all 4 major citieswho have home internet access

Source: Yahoo!-TNS Net Index 2008

174,071

191,145

155,155

133,258

115,475

Total (4 cities)

Ho Chi Minh City

Hanoi

Da Nang

Can Tho

Monthly Personal Spending on the Internet (VND)

US$36Mmonthly

Monthly Internet ExpenditureMonthly Internet Expenditure

Net users spend an average VND174,000or US $10 per month on the Internet

Online User ProfileOnline User Profile

26%14%

24%14%

12%

10%

12%

8%35%

15%

14%

18%

General Netizen*

40+

35-39

30-34

25-29

20-24

15-19

Age

56%

52% 44%

48%

General Netizen*

Female

Male

Gender

63%

64%

37%

36%

General Netizen*

Married &Others

Single

Marital Status

Skewed towards young (68% <29 years), Male (56%) and Single (63%)

A Shift in AdvertisingA Shift in Advertising

,

TV 75%

Radio0.6%

Newspapers16%

Magazines8 %

Internet (est.)0.4%

TV Radio Newspapers Magazines Internet (est.)

Advertising spend breakdown - 2008Advertising spend breakdown - 2008

Source: TNS Media Co.

TV is King and has grown to 80% in 2009, asadvertisers are returning to the tried and trusted

66%66%7%7%

4%4%7%7%

7%7%

Top 4 Daily Home activities

TV dominates followed by reading, using the computerand watching movies and listening to music

Source: VietCycle 1999-2008

99

83

73

62 62

51

11

27

99

8576

60 64

52

11

33

100

8477

6257

44

15

42

TV (Past Week) Outdoor (PastWeek)

Newspaper(Past Week)

Magazine (PastWeek)

DVD/VCD/Tape(Past Week)

Radio (PastWeek)

Cinema (Past 3Months)

Internet (PastWeek)

2006 2007 2008(%)

Base: Males and Females aged 15+ across all 4 major cities (HoChi Minh City, Hanoi, Da Nang and Can Tho)

Source: TNS Media Habits Survey (2006-2008)

Media ReachMedia Reach

TV is still King… but Internet is by far thefastest-growing medium

295

46

922 22

253

45

1024 30

233

46

8 2143

TV Newspaper Magazine Radio Internet

2006 2007 2008

Base: Males and Females aged 15+ across all 4 major cities (Ho Chi Minh City,Hanoi, Da Nang and Can Tho)

Source: TNS Media Habits Survey (2006-2008)

Time Spent Per Day (Mins)

Media Exposure Trends

Time spend watching TV has decreased by 1 hour per day since 2006,while Internet is the only medium growing (21 minutes / day)

230,000

937

42,050

828

20,500

36,980

20,429

171,000

0

50,000

100,000

150,000

200,000

250,000

TV Newspapers Magazines Radio

2008

2009

Ad spend half year 2008 Ad spend half year 2008 vsvs half year 2009 half year 2009

TV ad spend has increased by 26% andNewspaper increased by 12%, while both

Magazine & Radio have dropped.Total ad spend is up by 23% compared to 2008

(,000)

20092008

Top 6 Growth Sectors ad spend Half yr 2008 vs half yr 2009

The Beverage sector, followed byTelecoms has experienced the highestgrowth in Ad spend, followed by Foods,

Beauty Care, etc. Ironically, sectorspend does not necessarily translateinto category growth in terms of sales

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

Telecoms Food Hygiene &

beauty care

Beverages Pharmaceuticals Household

products

2008 2009

66%+

35%+

34%+

93%+

15%+42%+

Source: TNS Media - June 2008-June 2009

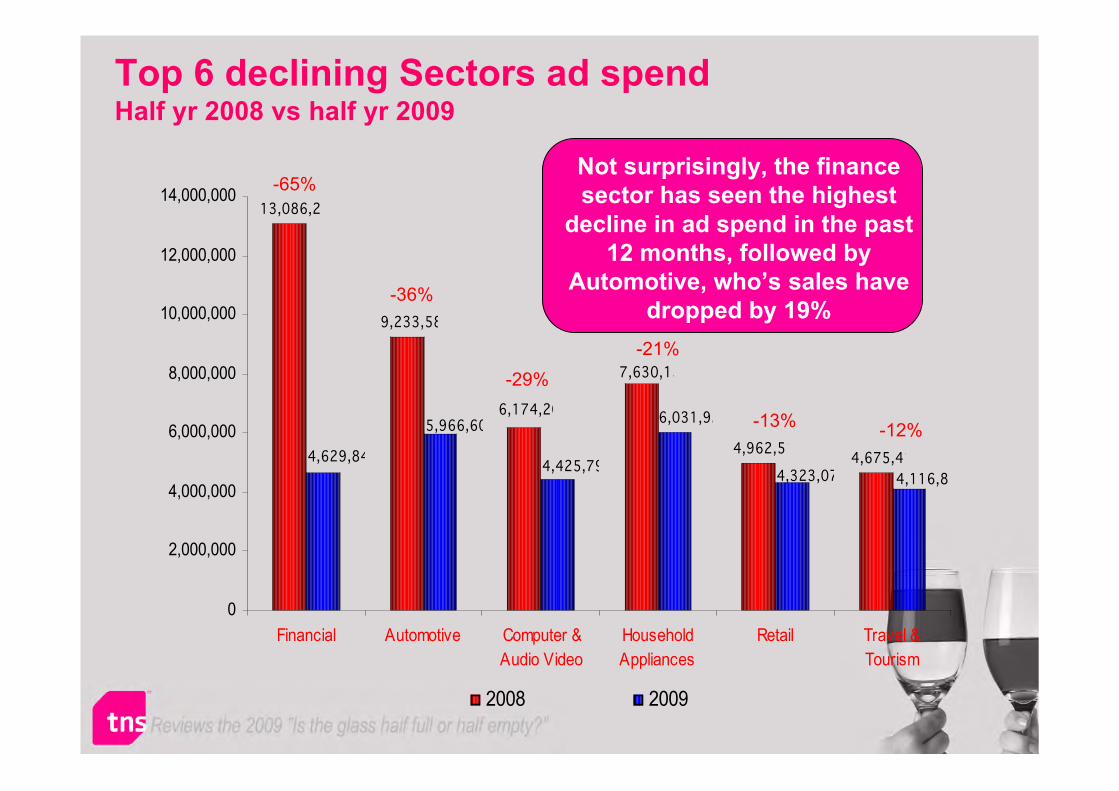

13,086,280

9,233,583

4,962,5124,675,415

7,630,154

6,174,207

4,629,849

5,966,609

4,425,797

6,031,925

4,323,077 4,116,805

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

Financial Automotive Computer &

Audio Video

Household

Appliances

Retail Travel &

Tourism

2008 2009

-65%

-36%

-29%-21%

-13% -12%

Top 6 declining Sectors ad spend Top 6 declining Sectors ad spend Half yr 2008 Half yr 2008 vsvs half yr 2009 half yr 2009

Not surprisingly, the financesector has seen the highest

decline in ad spend in the past12 months, followed by

Automotive, who’s sales havedropped by 19%

EnvironmentEnvironment

I would be willing to pay 10% more for groceries/products that are more environmentally friendly

15

10

15

15

22

26

28

41

44

38

51

38

54

54

55

58

56

55

47

46

55

42

34

33

27

27

18

17

14

11

9

6

5

13

4

3

2

1

3

1

1

1

2

3

New Zealand

Japan

Hong Kong

Singapore

South Korea

Thailand

Malaysia

Indonesia

Philippines

Chinese mainland

India

Strongly agree Somewhat agree

Somewhat disagree Strongly disagreeAve

Source: Grey Group study

3.3

3.3

3.3

3.1

3.1

3.0

2.8

2.8

2.7

2.6

3.4

Environmental awarenessEnvironmental awareness

Evidence of increasing concern across Asia…

Forecast in the next 12 monthsForecast in the next 12 monthsEnvironmental PollutionEnvironmental Pollution

5

5

7

22

17

22

9

27

23

27

40

37

36

12

9

0

0

0

TNS Consumer Poll -Jan. 09

TNS VietCycle - Sept. 08

TNS VietCycle - Nov. 06

Far better A little better Same A little worse Far worse Don't know

Source: TNS VietCycle 2006 / 2008 & TNS Consumer Confidence Poll – Jan. 09

In a short time consumer sentiment towards the worseningof Vietnam’s polluted environment has increased by 300%!

How do we rate VietnamHow do we rate Vietnam’’s environment?s environment?By SEC, age group and genderBy SEC, age group and gender

Base: All respondents

We can see the next generation of adults (teens)are quite skeptical of the environmentalsituation.

Quality of Vietnam environment

25

25

28

18

32

21

29

2624

52

57

47

60

53

54

51

5355

20

16

22

20

14

23

17

1918

3

1

2

2

1

2

2

13

AB (n=283)

CD (n=539)

EF (n=173)

Teenagers (n=195)

Young Adults (n=185)

Mature (n=296)

Older (n=324)

Male (n=503)

Female (n=497)

Very bad Fairly bad Fairly good Very good

13

17

20

26

34

39

45

51

69

45

2

3

4

13

5

7

13

4

Less use of motorbike / take more

public transport

Use more public transport

Walk or use more bicycle / electric

bicycle

Use energy saving bulbs / solar

pow er lights

Recycle / separate w aste items for

recycling

Less use plastic bags

Use less w ater

Use less energy (gas, electriccity)

Not littering

Most important Actions

What are we doing to look after the environment?Current actions vs Perceived most important action

Stopping littering isconsidered the #1 actionto fight environmentalpollution

Source: VietCycle 2009

Environmental Brand PerceptionsEnvironmental Brand Perceptions

Source: TNS VietCycle

“I can use my mobile

to show my social

status & personality”

“7 out of 10 consumers “say” theyprefer to buy environmentallyfriendly products, …but do they?

No brand in VietnamNo brand in Vietnamhas an image of beinghas an image of being

environmentally friendlyenvironmentally friendly,but lots of companies

have the opposite image!

Feeding hungry Feeding hungry mouths and buying mouths and buying aspirationalaspirational brands, brands,

rules in Vietnamrules in Vietnam

Environmentally

Environmentally

Friendly?Friendly?

So letSo let’’s smarten ups smarten up&&

start to clean up!start to clean up!

Is the glass half full or half empty - Synopsis

Overall spend has continued to increase on almost allconsumer categories, but growth has declined by 15% to 50%compared to 2008.

Not all sectors have been impacted the same…Telecoms / Food / Beverages / Pharmaceuticals / Household Products /Education have all maintained steady if not staggering growth

Electronics / Automotive / Travel-tourism, Computer-Audio video /Finance-banking, beauty-personal care and real estate have all seen amild to steep drop off

Is the glass half full or half empty - SynopsisInversely, big ticket items such as cars and computers,banking and real estate products have all been relegated to alater date, during these times of uncertainty.

Bottom-line:Glass is half empty due impact of global recession (EXORTS/ FDI/ MR)Glass is half full due to strong performance of domesticmarketGlass is full compared to the rest of Asia as Vietnam is 1 ofonly 5 Growth economies in the region