Embed Size (px)

Citation preview

CORE quality,prices aeasily bpaper, c ======

Quot “WhateWhatev

INDI

State Arrivals Punjab HaryanaRajasthaGujarat MaharasM. P. TelanganA. P. KarnataOrissa Other Total

PURPOSE, helping and to prevbe replacecotton bag

=========

te:

ever we rver we use

IA Arriwise

2014(Lac10.3

a 17.4an 16.5

77.4shtra 62.7

15.4na 54.0

24.5ka 24.9

3.275.06

311.8

E AND Mcotton usevent the ared as a ‘res vs. plasti

=========

receive ise is wisdo

ivals: (4-15 c bales) 39 48 53 44 75 43 08 50 95 7 6 88

MISSION: ers locate rbitrary usenewable ic/paper ba

=========

s informaom, how w

(as on d

- Ju

2015-16(Lac bale5.07 10.5 13.4 63.2 56.06 16.06 50.9 17.45 13.2 2.85 2.6 251.29

To assist regular s

e of paperresource’

ags), there

=========

ation, Whawe use it i

date: 0

st Agri

es)

cotton farsources ofr and plast

(e.g. cotteby saving

=========

atever weis our inte

COTTO

5-04-20

rmers in imf quality ctic objects ton handkthe enviro

=========

07.

e preservelligence”

ONGURU™

016)

mproving cotton at nwhere cot

kerchief vsonment.

=========

04.201

e is know”

™ Mantra

1

yield & nominal tton can s. tissue

======

16

wledge,

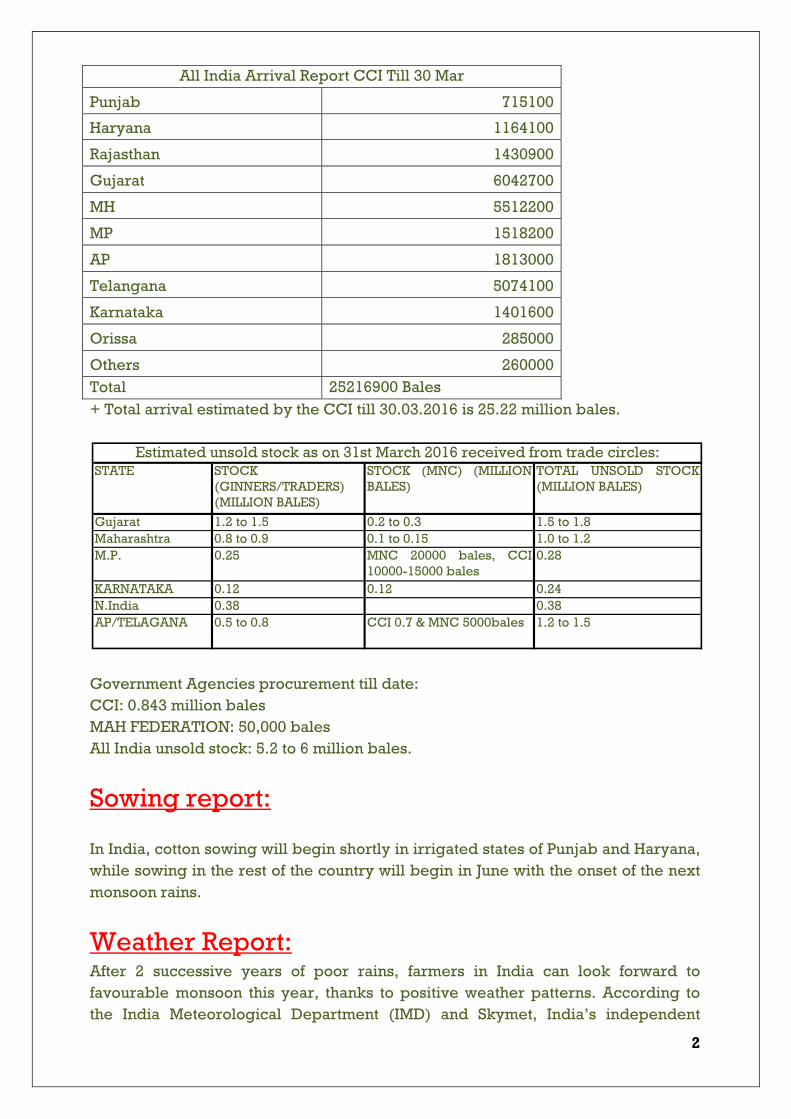

All India Arrival Report CCI Till 30 Mar

Punjab 715100

Haryana 1164100

Rajasthan 1430900

Gujarat 6042700

MH 5512200

MP 1518200

AP 1813000

Telangana 5074100

Karnataka 1401600

Orissa 285000

Others 260000 Total 25216900 Bales + Total arrival estimated by the CCI till 30.03.2016 is 25.22 million bales.

Government Agencies procurement till date: CCI: 0.843 million bales MAH FEDERATION: 50,000 bales All India unsold stock: 5.2 to 6 million bales.

Sowing report:

In India, cotton sowing will begin shortly in irrigated states of Punjab and Haryana, while sowing in the rest of the country will begin in June with the onset of the next monsoon rains.

Weather Report: After 2 successive years of poor rains, farmers in India can look forward to favourable monsoon this year, thanks to positive weather patterns. According to the India Meteorological Department (IMD) and Skymet, India’s independent

2

STATE STOCK (GINNERS/TRADERS) (MILLION BALES)

STOCK (MNC) (MILLIONBALES)

TOTAL UNSOLD STOCK(MILLION BALES)

Gujarat 1.2 to 1.5 0.2 to 0.3 1.5 to 1.8 Maharashtra 0.8 to 0.9 0.1 to 0.15 1.0 to 1.2M.P. 0.25 MNC 20000 bales, CCI

10000-15000 bales0.28

KARNATAKA 0.12 0.12 0.24N.India 0.38 0.38AP/TELAGANA 0.5 to 0.8 CCI 0.7 & MNC 5000bales 1.2 to 1.5

Estimated unsold stock as on 31st March 2016 received from trade circles:

weather forecasting service, an overall good rainfall of around 89 cm is expected between June 1 to September 30 - the monsoon period in India.

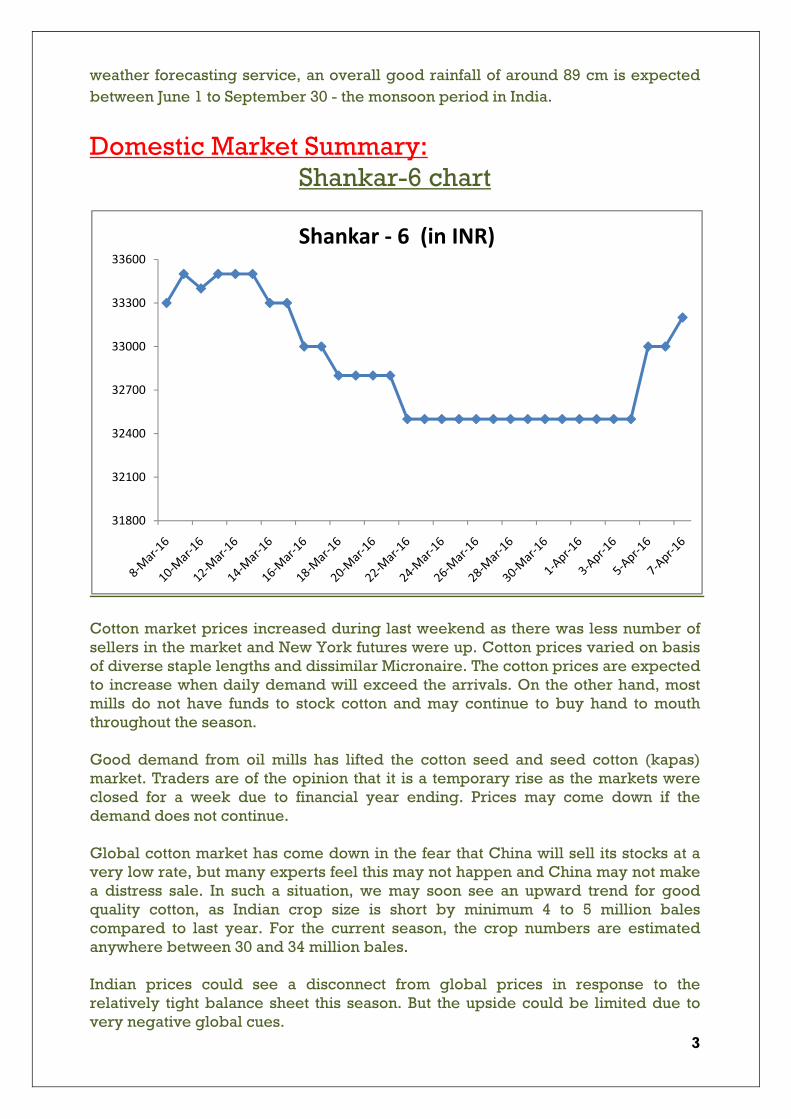

Domestic Market Summary: Shankar-6 chart

Cotton market prices increased during last weekend as there was less number of sellers in the market and New York futures were up. Cotton prices varied on basis of diverse staple lengths and dissimilar Micronaire. The cotton prices are expected to increase when daily demand will exceed the arrivals. On the other hand, most mills do not have funds to stock cotton and may continue to buy hand to mouth throughout the season.

Good demand from oil mills has lifted the cotton seed and seed cotton (kapas) market. Traders are of the opinion that it is a temporary rise as the markets were closed for a week due to financial year ending. Prices may come down if the demand does not continue.

Global cotton market has come down in the fear that China will sell its stocks at a very low rate, but many experts feel this may not happen and China may not make a distress sale. In such a situation, we may soon see an upward trend for good quality cotton, as Indian crop size is short by minimum 4 to 5 million bales compared to last year. For the current season, the crop numbers are estimated anywhere between 30 and 34 million bales.

Indian prices could see a disconnect from global prices in response to the relatively tight balance sheet this season. But the upside could be limited due to very negative global cues.

3

31800

32100

32400

32700

33000

33300

33600Shankar ‐ 6 (in INR)

4

YARN Indian yarn export to China has decreased due to rising import from Vietnam which is the second largest yarn exporting country to China. However, the fall of cotton yarn exports to China was partly offset by a rise to other destinations, like Bangladesh.

India’s spun yarn export in February 2016 was up by 22.8 % in volume terms while it declined 17.3 % in value terms. In February 2016, 87 countries imported spun yarn from India, with China accounting for 27.4 %, Bangladesh 17.8 % followed by Egypt. The top 3 importers together accounted for more than 50 % of all spun yarns exported from India in February.

Yarn prices will be under pressure until Chinese cotton stock issue becomes clear. The USD Dollar has also depreciated by over 3% vis a vis INR. Unless the is a demand and price increase possible in yarn, cotton can't run alone.

DEBATE FOR THIS MONTH:

1. Will the cotton prices rise in this season?

This is the top-of-mind question in the cotton market today.

The current year’s cotton crop is very small, especially in Top producer countries like India, China and Pakistan.

Consumption has exceeded production for the first time in many years.

Stocks outside China are very low.

There is a serious shortage of quality cotton in the market.

Then why are cotton prices not rallying?

Is China’s huge reserve stock the only reason or are we missing something?

2. Is the carry-forward stock of 5.2 million bales given by CAB justified?

The Cotton Advisory Board (CAB) assumes that the Indian cotton season opened with a carry-forward stock of 5.2 million bales (each bale is 170 kg) in October 2015.

5

The Government Agencies bought a record 8.8 million bales of cotton in the last season.

Carry-forward stock at the beginning of July 2015 was around 15.1 million bales, including 7 million bales with the CCI.

During July to September, CCI sold about 4.7 million bales.

In the same period, Indian mills consumed close to 7.6 million bales, exported around 0.9 million bales and imported 0.5 million bales, based on official numbers from government agencies.

Based on above figures, it is difficult to see how the CAB estimates the carry-forward stock as 5.2 million bales. The above 2 questions will determine the future of cotton prices in India and the world. Readers are requested to mail their views and opinions on [email protected].

COTTONGURUTM is proud to be associated as a MEDIA PARTNER with:

For Registration visit at www.worldcottonoutlook.com

6

Bangladesh-India Cotton Fest 2016

�

Bangladesh-India Cotton Festival 2016, jointly arranged by Bangladesh Cotton

Association (BCA) and Indian Cotton Association Limited (ICAL) was held in Dhaka

recently. The event was held in cooperation with the Federation of Bangladesh

Chambers of Commerce and Industry (FBCCI) and the India-Bangladesh Chamber

of Commerce and Industry (IBCCI). Commerce Minister To fail Ahmad inaugurated

the festival. High Commissioner of India Harsh Vardhan Shringla attended the

event as the guest of honour.

The event was attended by delegates from Bangladesh, India and various other

countries. It included useful sessions on cotton production and challenges; port

facilities in Bangladesh; sea ports and land ports infrastructure in Bangladesh.

Addressing the inauguration programme, High Commissioner Shringla drew

attention to the fact that India was the largest supplier of cotton and cotton yarn to

Bangladesh. Cotton and cotton yarn/thread and cotton fabric was the single largest

commodity export from India and it accounted for about 22.5% of India's total

exports to Bangladesh, he said.

Apart from the President of the Indian Cotton Association Limited, Heads of major

Industry Associations of Bangladesh, such as FBCCI, IBCCI, BGMEA, BKMEA,

BTMA were also present, according to UNB. -Source The Financial Express��

COTTONGURUTM was a Speaker during the Conference but could not attend due to unavoidable circumstances. COTTONGURUTM Media was the Media Partner for the Conference.

7

8

Conferences/Seminars: International Cotton Conference in Bremen The 33rd International Cotton Conference in Bremen was attended by over 300 delegates. In a welcoming address, Mr. Ernst Grimmelt, President of the Bremen Cotton Exchange, summarised some of the topics to be discussed during the event, including the continuing competition for market share between cotton and man-made fibres. The first session focused on sustainability in the long term. Speakers highlighted responsible working practices, international cooperation aimed at creating a more transparent textile value chain, and the challenges associated with a changing landscape, populated by end consumers increasingly concerned with environmental factors and sustainability. There were discussions regarding cotton quality and testing, new directions in cotton breeding and technology and the processes for producing cotton around the world.

Seminar by ISCI and N. India Associations for White Fly 3 major trade bodies Indian Cotton Association Limited (ICAL), Northern India Textiles Mills Association (NITMA), and Mumbai-based Indian Society for Cotton Improvement (ISCI) had jointly organized a seminar for 'Awareness of whitefly and best practices for growing cotton' at Abohar on March 21. COTTONGURUTM is a member of ISCI.

The seminar was held to discuss and find ways to avoid a repeat of the last year's pest attack on cotton crop in Punjab and Haryana. Cotton was sown over 0.45 million hectares in Punjab last year and two-third of it was damaged due to pest attack.

FTAO Cotton Forum in Paris The Fair Trade Advocacy Office (FTAO) has called on the European Union, G7 and West African governments to step up their support of fairer and more sustainable textile supply chains, including more backing for small cotton farmers.

COTTONGURUTM Sample Bank

For Registration click here: http://www.cottonguru.org/testing.php

Need of the Hour: KNOW YOUR CUSTOMER (KYC) COTTONGURUTM has been running a special package for buyers to know the complete details of the supplier (verified postal address, contact details with mobile and landline numbers, details of proprietor/partner/director, ginning and credit capacity, list of buyers, etc).This also includes a "MADE TO ORDER" sourcing plan for cotton. Similarly, there is a special package for ginners to understand the buyer (address, contact details, credit rating, credit verification, list of suppliers, etc).This also includes branding and locating suitable buyer as per ginner's quality and credit facility.

9

10

International Market: Views from experts: 1. Joe Nicosia: Nicosia, the global platform head for cotton at Louis Dreyfus Commodities, says “The volcano is ready to go; the elephant in the room is the Chinese state reserve. It was at 50 million bales, it’s down to about 45 million already. They’ve liquidated some. They own half the world’s stock.”

As an influx of cotton hits the world market, prices naturally decline. The result is that fewer acres of cotton will be planted around the globe in 2016. If there is a silver lining to suppressed prices in 2016, it is that natural laws of economics – supply and demand – will once again drive decisions. By causing significant reductions in acreage, the market, as Nicosia puts it, is doing its job.

-Source: Cotton Grower

2. Shri Sanjay Jain: Mr. Jain, MD of T.T. Ltd, an fully integrated textile company in India, is of the opinion that domestic demand has been the main spoiler, as export is maintained at old levels despite China slowly down. Most spinners are losing money today, and situation will only improve if domestic demand for garments pick up. Months of Feb & March have been very poor for the domestic trade. However, since Holi festival, there is a positive uptick. We hope there will be sustained demand which shall lead to uptick in buying of yarn and fabric. However overall don’t expect any major jump, though cotton prices have bottomed out and expect to start going up.

China:

Prices of Xinjiang Cotton have stopped falling since last week, due to reduced supply of good grade cotton in the market. Some Spinners have adopted a convenient policy of buying from the state reserves as well as supplies held at ports to meet their production requirements.

Latest reports state that Chinese reserve sales are delayed till mid/end April. China hopes to sell off some of its 11 million metric-ton stockpile, the world’s largest. China will sell about 0.3 million tons of 2011 and 4.3 million tons of 2012 cotton.

Pakistan:

Federal Minister for Commerce Engr. Khurram Dastgir Khan, while inaugurating a three day textile trade fair in Karachi has stated that from July 1, 2016 the value added tax (VAT) would become zero in order to encourage the textile sector. Textile exporters were waiting for a much-delayed Trade Policy announced by the Commerce Ministry but there are no incentives for the textile sector even though the government has announced some incentives on machines imports etc.

As per data released by Pakistan Bureau of Statistic, the textile exports declined by 5% on monthly basis to $1.02 billion, while the value added shipments declined by

11

9 % to $597 million. -Source Pakistan Today.

U.S.:

USDA estimates U.S cotton sowing area at 9.6 million acres against last year’s 8.6 million acres.

REPORTS:

USDA:

India: India’s 2016/17 cotton production forecast is 364 lakh bales of 170 kg. bales on marginally lower acreage of 11.8 million hectares. Yields are expected higher through a combination of better crop, pest, and weed management practices and assume a “normal” monsoon after two consecutive years of deficient rain. Mill consumption is forecast lower than the 2015/16 marketing year as demand remains weak. Exports are forecast at 64 lakh bales while imports are forecast at 11.5 lakh bales.

Bangladesh: Cotton and Products Annual MY 2016/17 cotton area is forecast unchanged at 43,000 hectares (HA); farmers are not projected to add cotton area due to expected higher profit margins for other short duration crops. MY 2016/17 imports are forecast at 5.8 million bales on expectations of increased export market demand for value-added products.

Egypt: Cotton and Products Annual Post forecasts total lint cotton production to increase by 23 % to 395,000 bales in MY2016/17. The expected increase in production is a result of an anticipated increase in total planted area of 20 % to 120,000 ha from MY2015/16 and an increase in yields from 3.2 bales/ha to 3.3 bales/ha. Consumption is forecast to drop by 6 % or 40,000 bales to 590,000 bales in MY2016/17. In turn, total lint cotton imports are forecast to drop by 11 % or 50,000 bales to 400,000 bales in MY2016/17 compared to 450,000 bales in the current marketing year. Exports are to increase by 33 % at 200,000 bales. At least 25 % of Egypt’s total lint cotton imports are sourced from U.S. suppliers, and since 2007, most U.S. cotton exports to Egypt have been of the Pima cotton variety.

ICAC:

From the Secretariat ICAC Press Release, April 1, 2016 Cotton Production to Recover in 2016/17 While Consumption Remains Stable Cotton planting in Northern Hemisphere countries commences this month. In 2016/17, world cotton area is expected to expand by 1% to 31.3 million hectares. From December 2015 through February 2016, international cotton prices as measured by the Cotlook A Index averaged 69 cents/lb. However, prices for competing crops during the same period have fallen, making cotton more competitive this year compared to last. World cotton production in 2016/17 is projected to increase by 4%, to just under 23 million tons, as the world average yield is anticipated to improve by 4% to 732 kg/ha. In 2016/17, India’s area is forecast up 4% to 12.4 million hectares due to improved domestic cotton prices in 2015/16. Assuming yield is similar to the 4-year average of 522 kg/ha, production could reach 6.5 million tons in 2016/17. In March, the Chinese government announced a reduced target price for Xinjiang of 18600 yuan/ton. As a result, area is likely to contract by 10% to 3.1 million hectares and production to decrease to 4.6 million tons. Cotton area in the United States is projected to increase by 2% to 3.3 million hectares and production by 9% to 3.1 million tons. After production plummeted in 2015/16, cotton production in Pakistan is expected to jump 35% to 2.1 million tons as yields recover. After declining by 2% in 2015/16, world cotton consumption is anticipated to remain stable at 23.9 million tons. Consumption in China is projected to decrease by 5% to 6.8 million tons due to increasing wages, high domestic cotton prices, and low polyester prices. In 2016/17, Vietnam’s cotton consumption is forecast to rise 16% to 1.3 million tons, making it the fifth largest consumer. Consumption in Bangladesh, the sixth largest, could increase by 10% to 1.2 million tons. After several seasons of growth, cotton mill use in India and Pakistan contracted in 2015/16 due to weaker demand. However, India’s consumption is projected to rise by 4% to 5.5 million tons, and in Pakistan by 1% to 2.2 million tons.

12

13

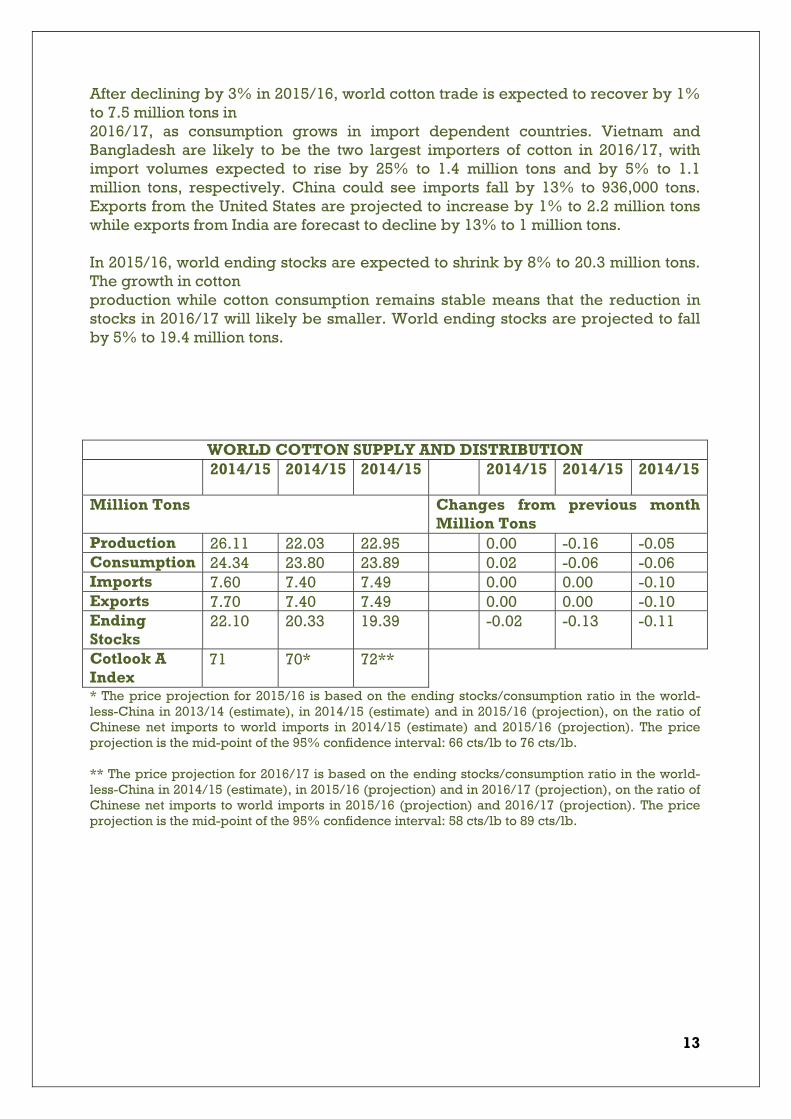

After declining by 3% in 2015/16, world cotton trade is expected to recover by 1% to 7.5 million tons in 2016/17, as consumption grows in import dependent countries. Vietnam and Bangladesh are likely to be the two largest importers of cotton in 2016/17, with import volumes expected to rise by 25% to 1.4 million tons and by 5% to 1.1 million tons, respectively. China could see imports fall by 13% to 936,000 tons. Exports from the United States are projected to increase by 1% to 2.2 million tons while exports from India are forecast to decline by 13% to 1 million tons. In 2015/16, world ending stocks are expected to shrink by 8% to 20.3 million tons. The growth in cotton production while cotton consumption remains stable means that the reduction in stocks in 2016/17 will likely be smaller. World ending stocks are projected to fall by 5% to 19.4 million tons.

WORLD COTTON SUPPLY AND DISTRIBUTION 2014/15 2014/15 2014/15 2014/15 2014/15 2014/15

Million Tons Changes from previous month Million Tons

Production 26.11 22.03 22.95 0.00 -0.16 -0.05 Consumption 24.34 23.80 23.89 0.02 -0.06 -0.06 Imports 7.60 7.40 7.49 0.00 0.00 -0.10 Exports 7.70 7.40 7.49 0.00 0.00 -0.10 Ending Stocks

22.10 20.33 19.39 -0.02 -0.13 -0.11

Cotlook A Index

71 70* 72**

* The price projection for 2015/16 is based on the ending stocks/consumption ratio in the world-less-China in 2013/14 (estimate), in 2014/15 (estimate) and in 2015/16 (projection), on the ratio of Chinese net imports to world imports in 2014/15 (estimate) and 2015/16 (projection). The price projection is the mid-point of the 95% confidence interval: 66 cts/lb to 76 cts/lb. ** The price projection for 2016/17 is based on the ending stocks/consumption ratio in the world-less-China in 2014/15 (estimate), in 2015/16 (projection) and in 2016/17 (projection), on the ratio of Chinese net imports to world imports in 2015/16 (projection) and 2016/17 (projection). The price projection is the mid-point of the 95% confidence interval: 58 cts/lb to 89 cts/lb.

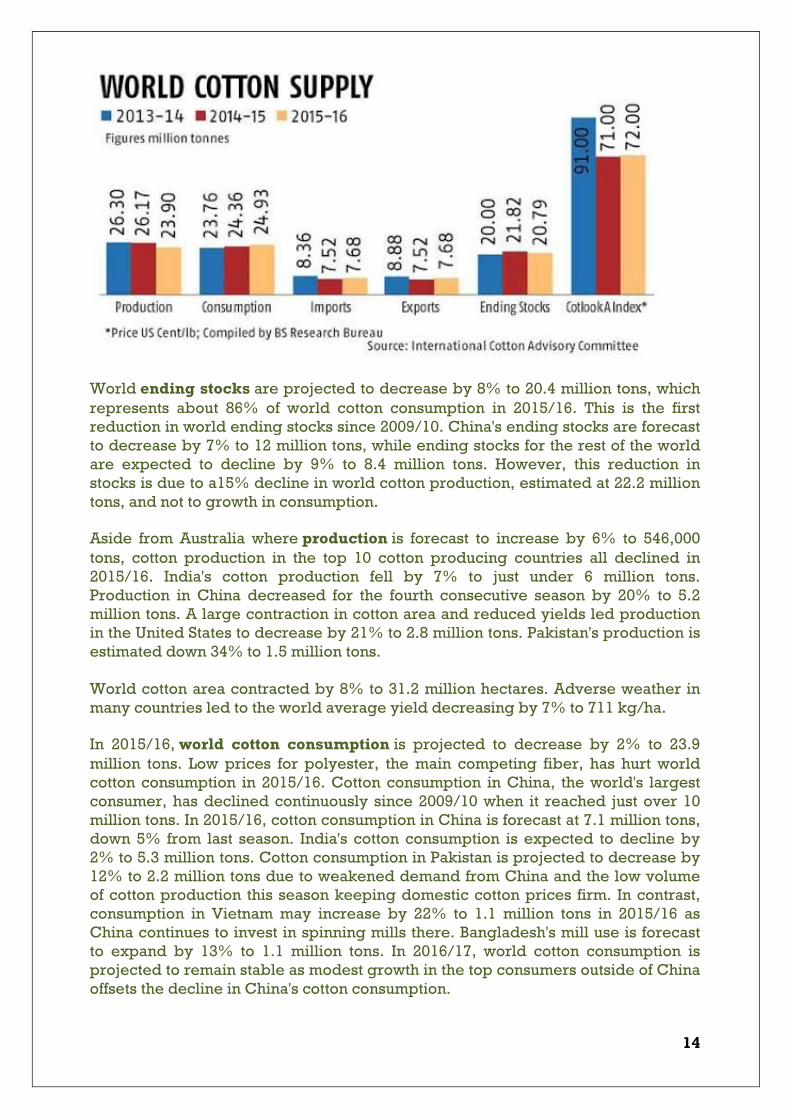

World ending stocks are projected to decrease by 8% to 20.4 million tons, which represents about 86% of world cotton consumption in 2015/16. This is the first reduction in world ending stocks since 2009/10. China's ending stocks are forecast to decrease by 7% to 12 million tons, while ending stocks for the rest of the world are expected to decline by 9% to 8.4 million tons. However, this reduction in stocks is due to a15% decline in world cotton production, estimated at 22.2 million tons, and not to growth in consumption.

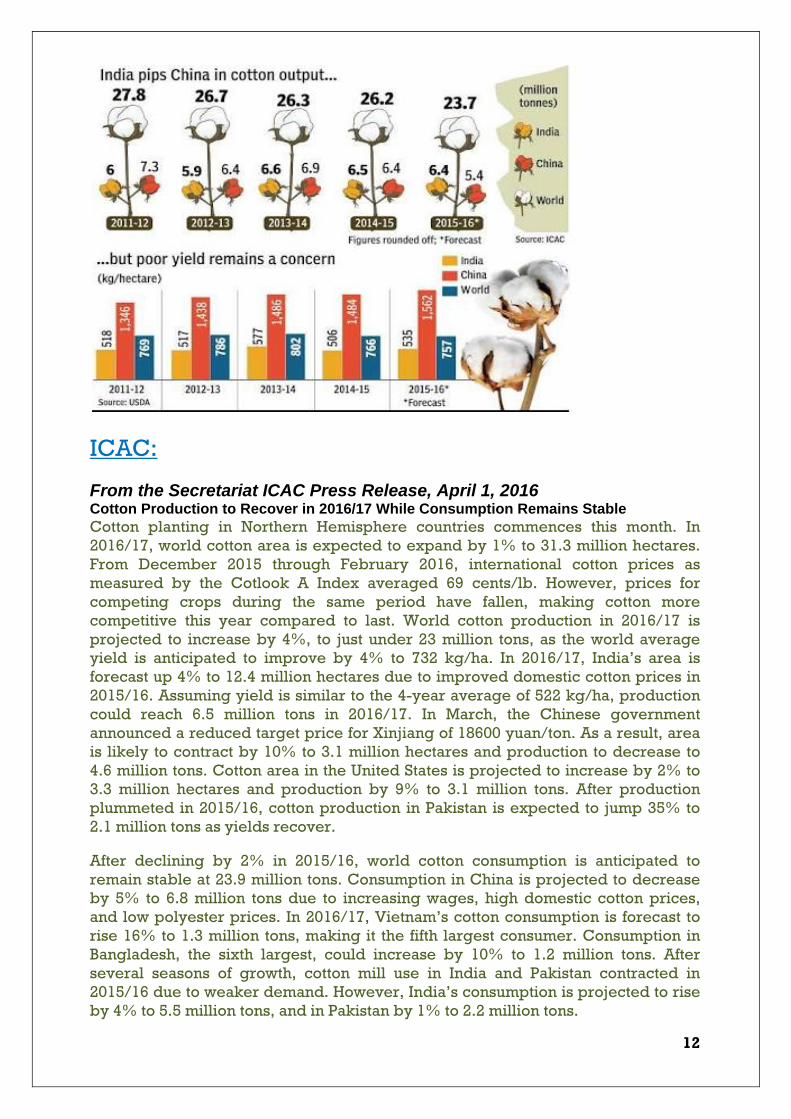

Aside from Australia where production is forecast to increase by 6% to 546,000 tons, cotton production in the top 10 cotton producing countries all declined in 2015/16. India's cotton production fell by 7% to just under 6 million tons. Production in China decreased for the fourth consecutive season by 20% to 5.2 million tons. A large contraction in cotton area and reduced yields led production in the United States to decrease by 21% to 2.8 million tons. Pakistan's production is estimated down 34% to 1.5 million tons.

World cotton area contracted by 8% to 31.2 million hectares. Adverse weather in many countries led to the world average yield decreasing by 7% to 711 kg/ha.

In 2015/16, world cotton consumption is projected to decrease by 2% to 23.9 million tons. Low prices for polyester, the main competing fiber, has hurt world cotton consumption in 2015/16. Cotton consumption in China, the world's largest consumer, has declined continuously since 2009/10 when it reached just over 10 million tons. In 2015/16, cotton consumption in China is forecast at 7.1 million tons, down 5% from last season. India's cotton consumption is expected to decline by 2% to 5.3 million tons. Cotton consumption in Pakistan is projected to decrease by 12% to 2.2 million tons due to weakened demand from China and the low volume of cotton production this season keeping domestic cotton prices firm. In contrast, consumption in Vietnam may increase by 22% to 1.1 million tons in 2015/16 as China continues to invest in spinning mills there. Bangladesh's mill use is forecast to expand by 13% to 1.1 million tons. In 2016/17, world cotton consumption is projected to remain stable as modest growth in the top consumers outside of China offsets the decline in China's cotton consumption.

14

15

In 2015/16, world cotton imports are likely to decrease by 3% to 7.4 million tons with imports by Vietnam, Bangladesh and China all projected at 1.1 million tons each. This represents 44% of world imports. The United States will lead in cotton exports despite reducing export volume by 12% to 2.1 million tons. India's exports are expected to recover by 22% to 1.1 million tons. In 2016/17, world trade may increase 3% to 7.6 million tons.

In 2016/17, poor returns for competing crops and relatively stable cotton prices may encourage farmers to plant more cotton, and cotton area may expand by 1% to 31.9 million hectares. Modest increases in cotton area in India, Pakistan and the United States are expected to offset losses in China, Brazil and Uzbekistan. World cotton production is projected to increase by 3% to 23 million tons in 2016/17.

-source: ICAC

CAI:

The Cotton Association of India (CAI) has estimated a production of 34.5 million bales (of 170 kg each) in the 2015-16 season.CAI said that during the October to February period, spot markets across the country registered an arrival of 24.5 million bales ,down 11.3 % compared to last season.

INDIA COTTON BALANCESHEET 2014-15 2015-16 Opening Stock 53.84 73.60 Crop Size 382.75 345.00 Imports 12.00 14.00 Total Supply 448.60 432.60 Mill Demand 278.00 270.00 SSI Unit Demand 27.00 24.00 Non Mill Demand 10.00 10.00 Total Consumption 315.00 304.00 Exports 60.00 -------- Total Demand 375.00 304.00 Surplus 73.60 128.60 All figures in Lac Bales of 170 Kgs. Source: Cotton Association Of India(CAI)

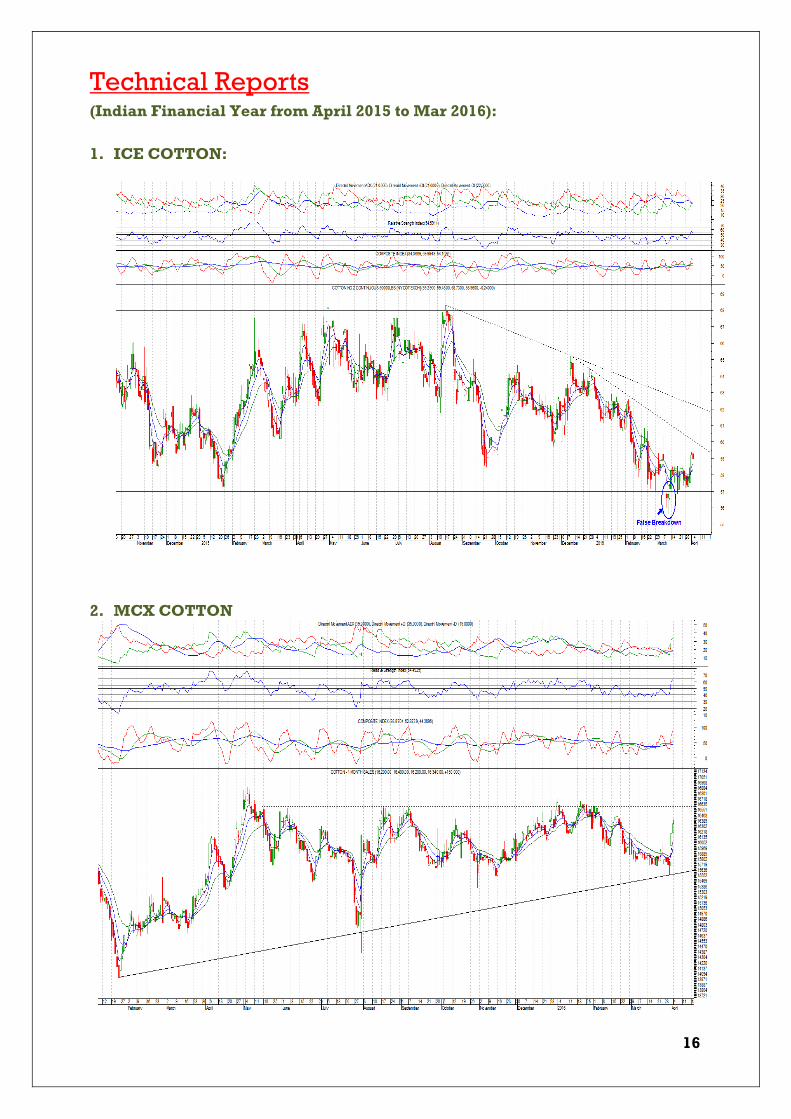

Technical Reports (Indian Financial Year from April 2015 to Mar 2016):

1. ICE COTTON:

2. MCX COTTON

16

Technical Charts Analysis: There are strong chances that Cotton may have formed medium to long term bottom. Next few weeks would give confirmations. Charts are pointing to a smart rally. On the yearly front, there is not much as there was a long consolidation from April 15 to March 16. But things look very bright for Cotton for current Fiscal, Prices could trend strongly higher, Expecting prices closer to 80 before March 2017!

Top Interviews:

Exclusive Interview with Dr. Kavita Gupta, IAS, Textile Commissioner of India.

https://www.youtube.com/watch?v=rz6BS_g9Msk

17

Exclusive Interview with Mr. B. K. Mishra, CMD, CCI

https://www.youtube.com/watch?v=_FUcljJnbFY

Exclusive interview with thought leader Mr. Suresh Kotak, Chairman of Kotak & Co.

https://www.youtube.com/watch?v=GBJL-gfzLRc

18

About the author: Mr. Manish Daga popularly referred by the cotton industry as COTTON GURU™ is a qualified textile technologist.

He is India’s only Cotton Valuer registered by the Indian Institution of Valuers, India. He is the fourth generation in cotton trade, advisory and broking services from his family. The P. R. D. Cottons Group is 112 year old in cotton business with continuity. Call or mail for any information, suggestion, feedback or to know how our Company can benefit from the knowledge and experience of COTTON GURU™. Call on +91 98200 72705 or mail to [email protected] Disclaimer: For private circulation to the addressees only and not for re-circulation. Any form of reproduction, dissemination, copying, disclosure, modification, distribution and/or publication of this Newsletter is strictly prohibited. The contents of this Newsletter are solely meant to inform and is not a substitute for professional advice.

FIRST AND ONLY REGISTERED“COTTON VALUER” IN INDIA

19

COTTON GURU™ Mr. Manish Daga