Embed Size (px)

Citation preview

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 1/41

McGraw-Hill/Irwin Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved

CHAPTER

4Discounted Cash Flow

Valuation

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 2/41

Slide 2

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Key Concepts and Skills

• Be able to compute the future value and/orpresent value of a single cash flow orseries of cash flows

• Be able to compute the return on aninvestment

• Be able to use a financial calculator and/orspreadsheet to solve time value problems

• Understand perpetuities and annuities

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 3/41

Slide 3

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Chapter Outline

4.1 Valuation: The One-Period Case

4.2 The Multiperiod Case

4.3 Compounding Periods4.4 Simplifications

4.5 What Is a Firm Worth?

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 4/41

Slide 4

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

4.1 The One-Period Case

If you were to invest $10,000 at 5-percentinterest for one year, your investment wouldgrow to $10,500.

$500 would be interest ($10,000 × .05)$10,000 is the principal repayment ($10,000 × 1)

$10,500 is the total due. It can be calculated as:

$10,500 = $10,000×(1.05)

The total amount due at the end of theinvestment is call the Future Value (FV ).

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 5/41

Slide 5

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Future Value

• In the one-period case, the formula for FV can be written as:

FV = C 0×(1 + r )

Where C 0 is cash flow today (time zero), and

r is the appropriate interest rate.

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 6/41

Slide 6

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

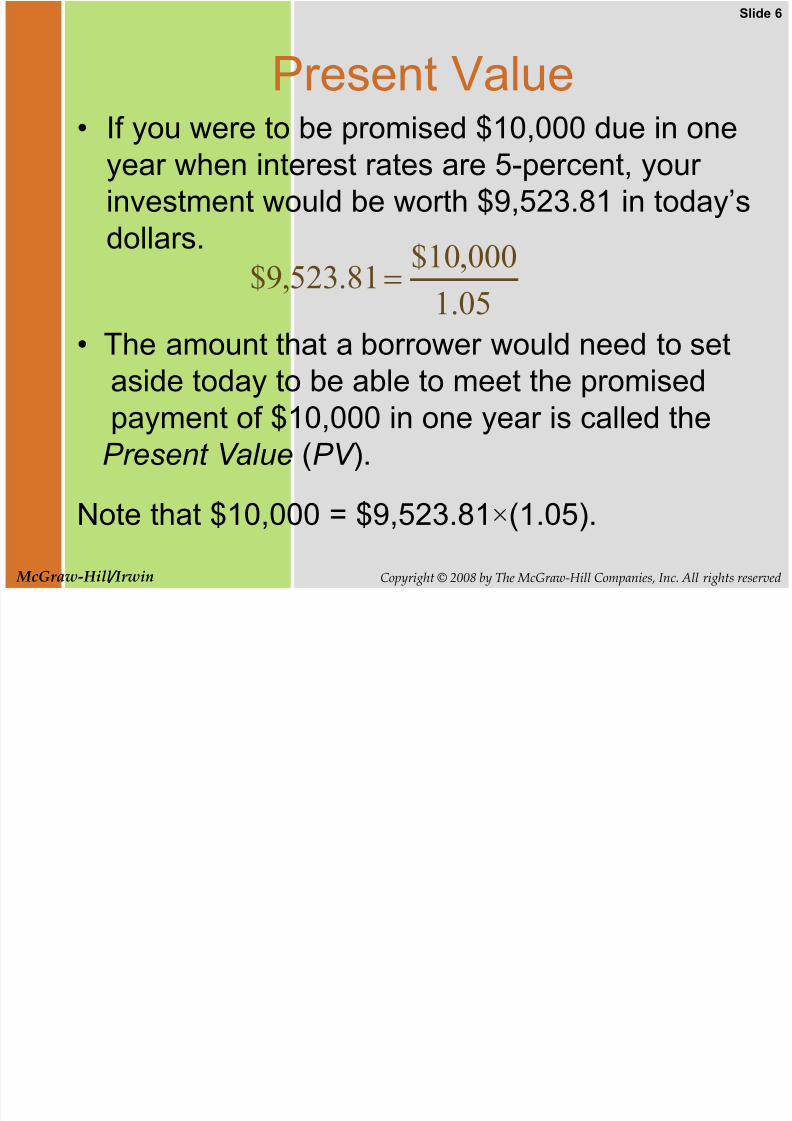

Present Value

• If you were to be promised $10,000 due in oneyear when interest rates are 5-percent, yourinvestment would be worth $9,523.81 in today’sdollars.

05.1

000,10$81.523,9$

• The amount that a borrower would need to setaside today to be able to meet the promised

payment of $10,000 in one year is called thePresent Value (PV ).

Note that $10,000 = $9,523.81×(1.05).

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 7/41

Slide 7

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Present Value

• In the one-period case, the formula for PV can be written as:

r

C PV

1

1

Where C 1 is cash flow at date 1, and

r is the appropriate interest rate.

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 8/41

Slide 8

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Net Present Value

• The Net Present Value (NPV ) of aninvestment is the present value of the

expected cash flows, less the cost of theinvestment.

• Suppose an investment that promises to

pay $10,000 in one year is offered for salefor $9,500. Your interest rate is 5%.Should you buy?

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 9/41

Slide 9

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Net Present Value

81.23$81.523,9$500,9$

05.1

000,10$500,9$

NPV

NPV

NPV

The present value of the cash inflow is greaterthan the cost. In other words, the Net PresentValue is positive, so the investment should bepurchased.

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 10/41

Slide 10

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

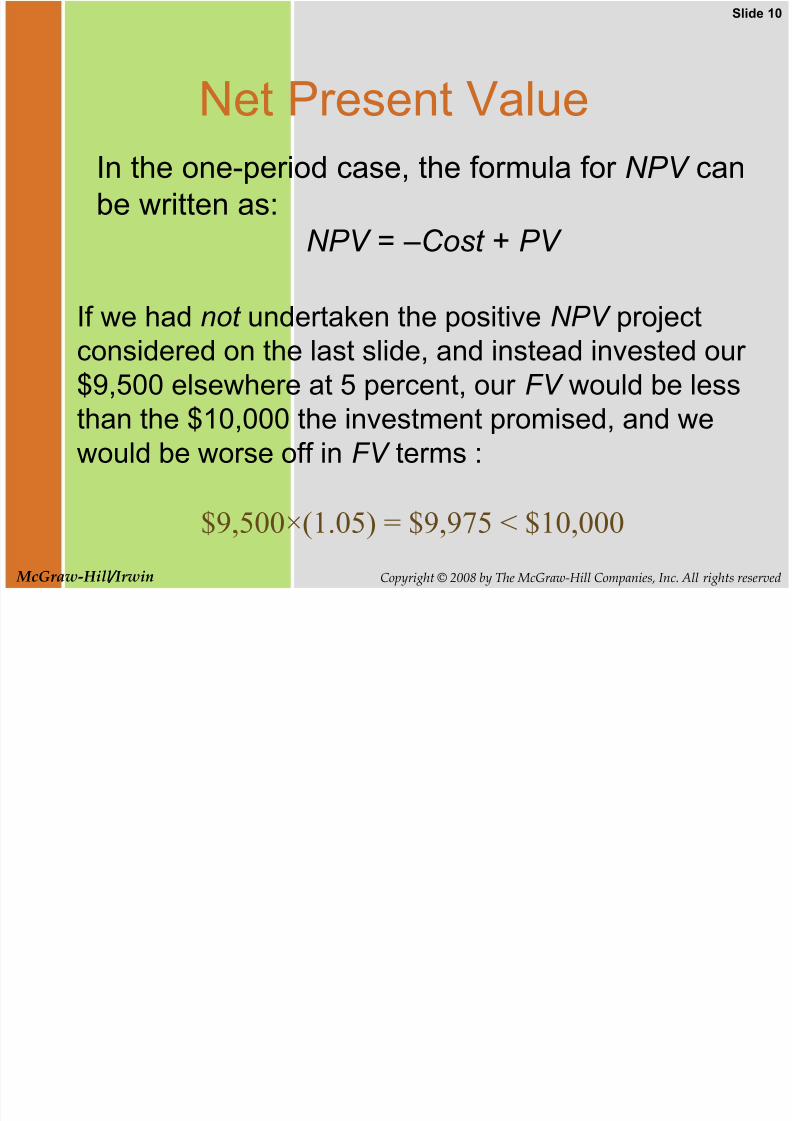

Net Present Value

In the one-period case, the formula for NPV canbe written as:

NPV = –Cost + PV

If we had not undertaken the positive NPV projectconsidered on the last slide, and instead invested our$9,500 elsewhere at 5 percent, our FV would be less

than the $10,000 the investment promised, and wewould be worse off in FV terms :

$9,500×(1.05) = $9,975 < $10,000

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 11/41

Slide 11

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

4.2 The Multiperiod Case

• The general formula for the future value ofan investment over many periods can bewritten as:

FV = C 0×(1 + r )T

Where

C 0 is cash flow at date 0,

r is the appropriate interest rate, andT is the number of periods over which the cashis invested.

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 12/41

Slide 12

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

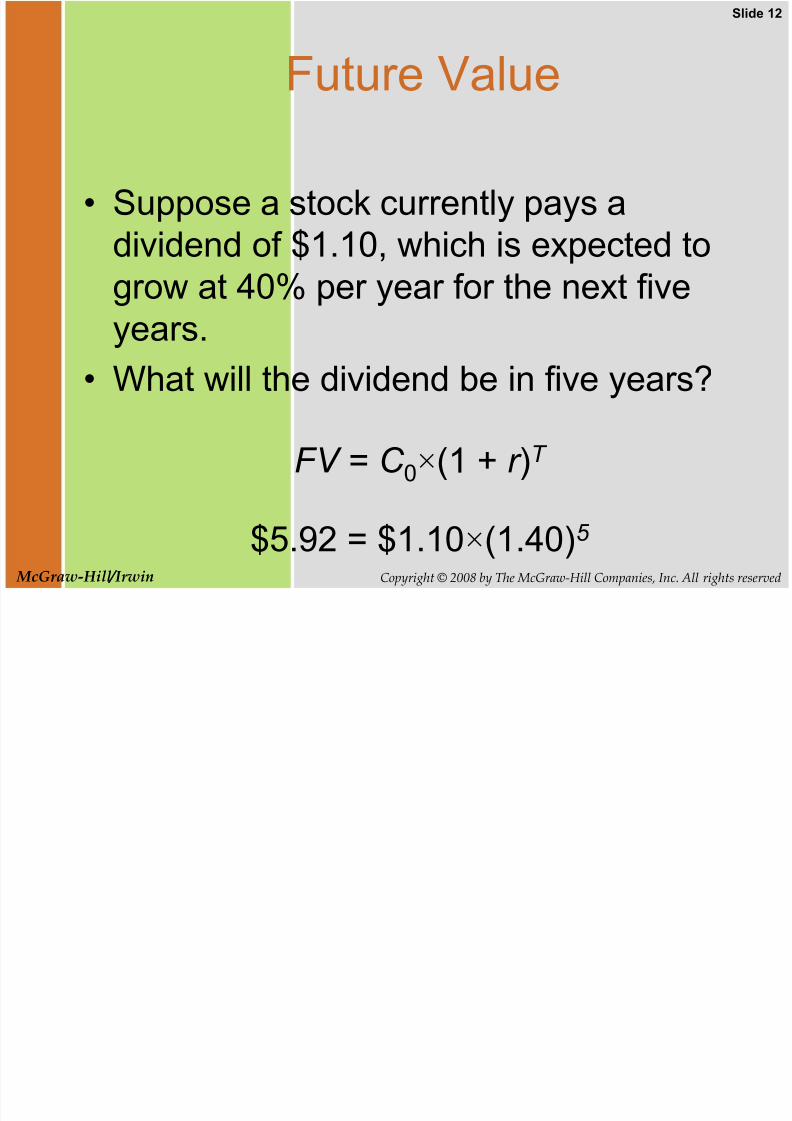

Future Value

• Suppose a stock currently pays adividend of $1.10, which is expected to

grow at 40% per year for the next fiveyears.

• What will the dividend be in five years?

FV = C 0×(1 + r )T

$5.92 = $1.10×(1.40)5

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 13/41

Slide 13

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Future Value and Compounding

• Notice that the dividend in year five,$5.92, is considerably higher than the

sum of the original dividend plus fiveincreases of 40-percent on the original$1.10 dividend:

$5.92 > $1.10 + 5×[$1.10×.40] = $3.30

This is due to compounding .

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 14/41

Slide 14

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Future Value and Compounding

0 1 2 3 4 5

10.1$

3)40.1(10.1$

02.3$

)40.1(10.1$

54.1$

2)40.1(10.1$

16.2$

5)40.1(10.1$

92.5$

4)40.1(10.1$

23.4$

Slid 15

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 15/41

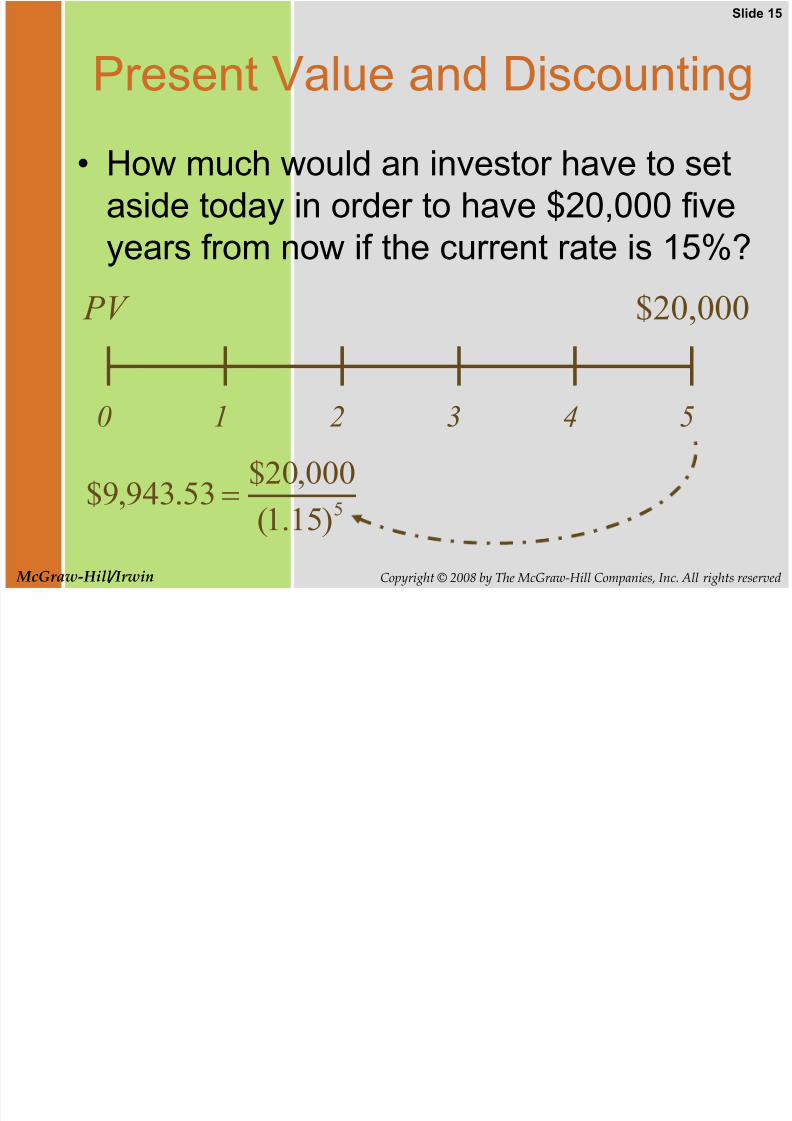

Slide 15

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Present Value and Discounting

• How much would an investor have to setaside today in order to have $20,000 fiveyears from now if the current rate is 15%?

0 1 2 3 4 5

$20,000 PV

5)15.1(

000,20$53.943,9$

Slid 16

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 16/41

Slide 16

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

How Long is the Wait?

If we deposit $5,000 today in an account paying10%, how long does it take to grow to $10,000?

T r C FV

)1(0 T

)10.1(000,5$000,10$

2000,5$

000,10$)10.1( T

)2ln()10.1ln( T

years27.7

0953.0

6931.0

)10.1ln(

)2ln(T

Slid 17

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 17/41

Slide 17

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Assume the total cost of a college education will be$50,000 when your child enters college in 12 years.You have $5,000 to invest today. What rate ofinterest must you earn on your investment to coverthe cost of your child’s education?

What Rate Is Enough?

T r C FV )1(0 12)1(000,5$000,50$ r

10000,5$

000,50$)1( 12 r 12110)1( r

2115.12115.1110 121

r

About 21.15%.

Slide 18

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 18/41

Slide 18

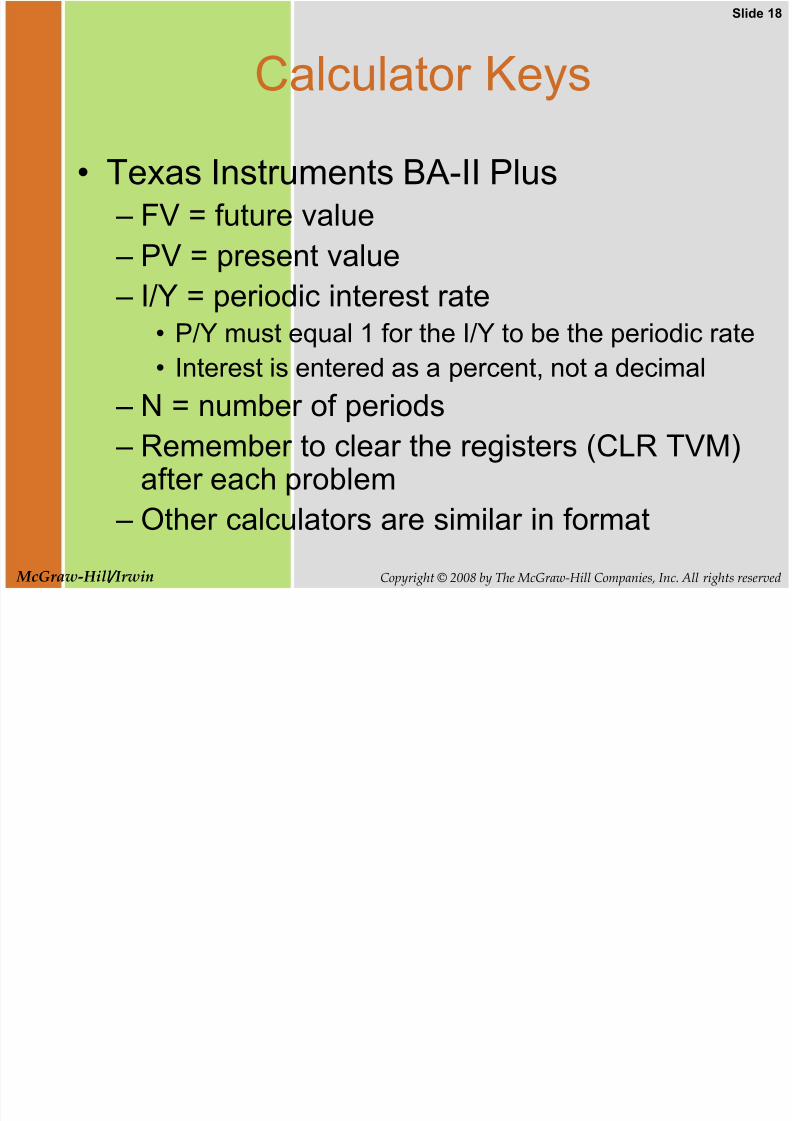

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Calculator Keys

• Texas Instruments BA-II Plus – FV = future value

– PV = present value

– I/Y = periodic interest rate• P/Y must equal 1 for the I/Y to be the periodic rate

• Interest is entered as a percent, not a decimal

– N = number of periods – Remember to clear the registers (CLR TVM)

after each problem

– Other calculators are similar in format

Slide 19

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 19/41

Slide 19

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Multiple Cash Flows

• Consider an investment that pays $200one year from now, with cash flowsincreasing by $200 per year through year

4. If the interest rate is 12%, what is thepresent value of this stream of cash flows?

• If the issuer offers this investment for

$1,500, should you purchase it?

Slide 20

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 20/41

Slide 20

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Multiple Cash Flows

0 1 2 3 4

200 400 600 800178.57

318.88

427.07

508.41

1,432.93

Present Value < Cost → Do Not Purchase

Slide 21

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 21/41

Slide 21

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Valuing “Lumpy” Cash Flows

First, set your calculator to 1 payment per year.Then, use the cash flow menu:

CF2

CF1

F2

F1

CF0

1

200

1

1,432.93

0

400

I

NPV

12

CF4

CF3

F4

F3 1

600

1

800

Slide 22

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 22/41

Slide 22

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

4.3 Compounding Periods

Compounding an investment m times ayear for T years provides for future value ofwealth:

T m

m

r C FV

10

Slide 23

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 23/41

Slide 23

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Compounding Periods

For example, if you invest $50 for 3years at 12% compounded semi-annually, your investment will grow to

93.70$)06.1(50$

2

12.150$ 6

32

FV

Slide 24

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 24/41

Slide 24

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

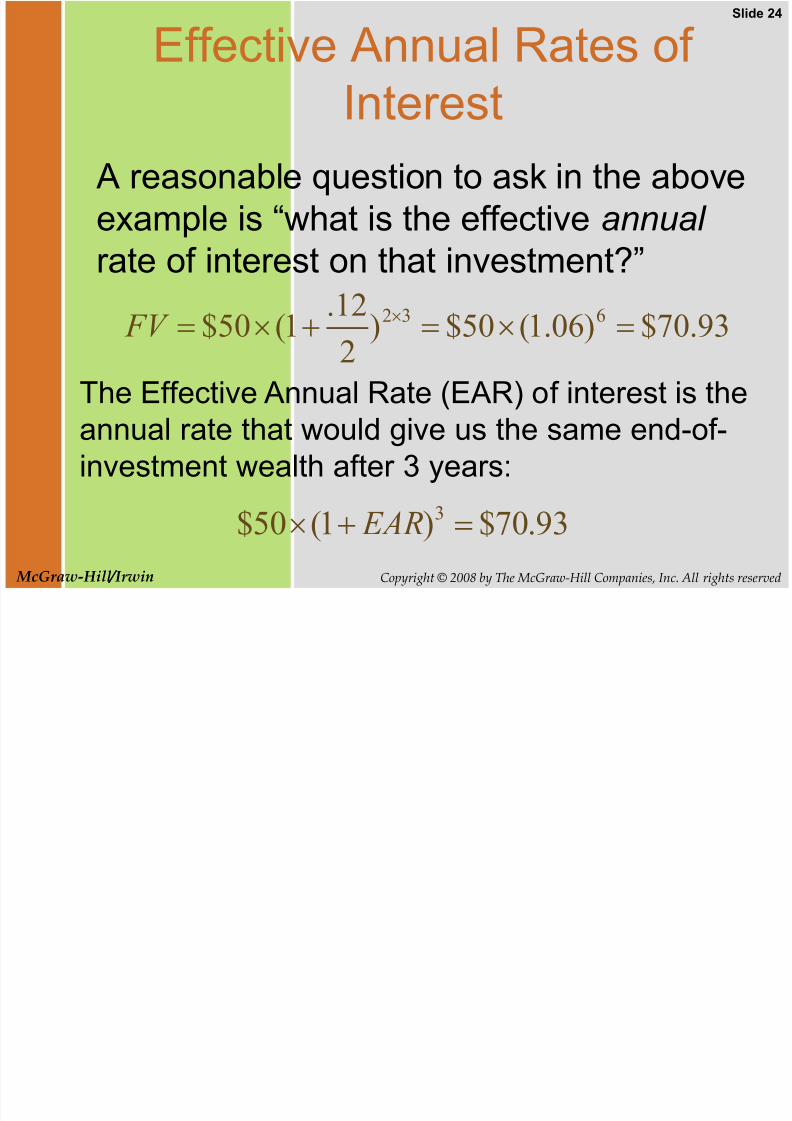

Effective Annual Rates ofInterest

A reasonable question to ask in the aboveexample is “what is the effective annual

rate of interest on that investment?”

The Effective Annual Rate (EAR) of interest is the

annual rate that would give us the same end-of-investment wealth after 3 years:

93.70$)06.1(50$)2

12.1(50$ 632

FV

93.70$)1(50$ 3 EAR

Slide 25

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 25/41

Slide 25

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Effective Annual Rates ofInterest

So, investing at 12.36% compoundedannually is the same as investing at 12%compounded semi-annually.

93.70$)1(50$ 3 EAR FV

50$

93.70$

)1( 3

EAR

1236.150$

93.70$ 31

EAR

Slide 26

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 26/41

Slide 26

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Effective Annual Rates of Interest

• Find the Effective Annual Rate (EAR) ofan 18% APR loan that is compoundedmonthly.

• What we have is a loan with a monthlyinterest rate rate of 1½%.

• This is equivalent to a loan with an annual

interest rate of 19.56%.

1956.1)015.1(12

18.11 12

12

mn

m

r

Slide 27

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 27/41

Slide 27

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

EAR on a Financial Calculator

keys: description:

[2nd] [ICONV] Opens interest rate conversion menu

[↓] [EFF=] [CPT] 19.56

Texas Instruments BAII Plus

[↓][NOM=] 18 [ENTER] Sets 18 APR .

[↑] [C/Y=] 12 [ENTER] Sets 12 payments per year

Slide 28

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 28/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Continuous Compounding

• The general formula for the future value of aninvestment compounded continuously overmany periods can be written as:

FV = C 0×erT

WhereC 0 is cash flow at date 0,

r is the stated annual interest rate,

T is the number of years, ande is a transcendental number approximately

equal to 2.718. e x is a key on yourcalculator.

Slide 29

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 29/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

4.4 Simplifications

• Perpetuity – A constant stream of cash flows that lasts forever

• Growing perpetuity

– A stream of cash flows that grows at a constant rateforever

• Annuity

– A stream of constant cash flows that lasts for a fixed

number of periods

• Growing annuity

– A stream of cash flows that grows at a constant ratefor a fixed number of periods

Slide 30

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 30/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Perpetuity

A constant stream of cash flows that lasts forever

0…

1

C

2

C

3

C

32 )1()1()1( r

C

r

C

r

C

PV

r

C PV

Slide 31

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 31/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Perpetuity: Example

What is the value of a British consol thatpromises to pay £15 every year forever?

The interest rate is 10-percent.

0

…

1

£15

2

£15

3

£15

£150

10.

£15 PV

Slide 32

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 32/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Growing Perpetuity

A growing stream of cash flows that lasts forever

0…

1

C

2

C ×(1+ g )

3

C ×(1+ g )2

3

2

2 )1(

)1(

)1(

)1(

)1( r

g C

r

g C

r

C

PV

g r

C PV

Slide 33

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 33/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Growing Perpetuity: Example

The expected dividend next year is $1.30, anddividends are expected to grow at 5% forever.

If the discount rate is 10%, what is the value ofthis promised dividend stream?

0

…

1

$1.30

2

$1.30×(1.05)

3

$1.30 ×(1.05)2

00.26$

05.10.

30.1$

PV

Slide 34

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 34/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Annuity A constant stream of cash flows with a fixed

maturity

0 1

C

2

C

3

C

T

r

C

r

C

r

C

r

C PV

)1()1()1()1( 32

T r r

C PV

)1(

11

T

C

Slide 35

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 35/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Annuity: Example

If you can afford a $400 monthly car payment,how much car can you afford if interest rates are7% on 36-month loans?

0 1

$400

2

$400

3

$400

59.954,12$)1207.1(

11

12/07.

400$36

PV

36

$400

Slide 36

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 36/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

What is the present value of a four-year annuity of$100 per year that makes its first payment two years fromtoday if the discount rate is 9%?

22.297$09.1

97.327$

0 PV

0 1 2 3 4 5

$100 $100 $100 $100$323.97$297.22

97.323$)09.1(

100$

)09.1(

100$

)09.1(

100$

)09.1(

100$

)09.1(

100$4321

4

1

1 t

t PV

Slide 37

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 37/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Growing Annuity

A growing stream of cash flows with a fixedmaturity

0 1

C

T

T

r

g C

r

g C

r

C PV

)1(

)1(

)1(

)1(

)1(

1

2

T

r

g

g r

C PV

)1(

11

2

C ×(1+ g )

3

C ×(1+ g )2

T

C×(1+ g )T -1

Slide 38

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 38/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Growing Annuity: Example A defined-benefit retirement plan offers to pay $20,000

per year for 40 years and increase the annual payment by3% each year. What is the present value at retirement ifthe discount rate is 10%?

0 1

$20,000

57.121,265$10.1

03.11

03.10.

000,20$ 40

PV

2

$20,000×(1.03)

40

$20,000×(1.03)39

Slide 39

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 39/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

Growing Annuity: Example

You are evaluating an income generating property. Net rent isreceived at the end of each year. The first year's rent is

expected to be $8,500, and rent is expected to increase 7%

each year. What is the present value of the estimated income

stream over the first 5 years if the discount rate is 12%?

0 1 2 3 4 5

500,8$

)07.1(500,8$

2)07.1(500,8$

095,9$ 65.731,9$

3)07.1(500,8$

87.412,10$

4)07.1(500,8$

77.141,11$

$34,706.26

Slide 40

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 40/41

Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved McGraw-Hill/Irwin

4.5 What Is a Firm Worth?

• Conceptually, a firm should be worth thepresent value of the firm’s cash flows.

• The tricky part is determining the size,timing, and risk of those cash flows.

Slide 41

8/14/2019 04120802 Chap 004

http://slidepdf.com/reader/full/04120802-chap-004 41/41

Quick Quiz

• How is the future value of a single cash flowcomputed?

• How is the present value of a series of cash

flows computed.• What is the Net Present Value of an

investment?

• What is an EAR, and how is it computed?• What is a perpetuity? An annuity?