Embed Size (px)

Citation preview

02.11.07 Michael PirsonHarvard University

Bridging the organizational trust gap –

relevant antecedents of stakeholder trust

Michael PirsonHarvard University

02.11.07 Michael PirsonHarvard University

Agenda

1 Introduction2 Research problem 3 Concept of trust4 Stakeholder trust measurement5 Quantitative Study: Antecedents of

stakeholder trust6 Qualitative Study: more findings on trust

antecedents7 Managerial Implications8 Discussion

02.11.07 Michael PirsonHarvard University

1 Introduction

• Which organizations do you trust most, which least?– UN– Police– Church– Government– Business– NGO’s– Military– Hospitals

02.11.07 Michael PirsonHarvard University

1 Introduction

“Trust is like air, we notice its importance only when it is polluted or gone.”

(Baier, 1998)

Trust has been widely recognized to be• a key enabler of organizational success (Shaw 1997)• facilitate efficient business transactions (Williamson 1993; Noteboom

1996) • increase customer/employee satisfaction ( Doney and Cannon 1997). • reduce the risks associated with opportunism (Pavlou 2002) and is seen as a source of competitive advantage (Barney and Hansen

1994).

Overall trust is seen as the basis for• successful cooperation, • motivation, • innovation, and • transformation

02.11.07 Michael PirsonHarvard University

1 IntroductionThe overall demand for trust is increasing…

Quality and intensity of relationship increase

Demand for Trust

increases

DemocratizationGlobalizationLiberalization

MediatizationInformation technology

Organizational shiftsLess Hierarchy-More Teamwork

Possibilities for interaction increase

– more strangers meet

CooperationMotivation

InnovationTransformation

Complexity is increasing

02.11.07 Michael PirsonHarvard University

1 Introduction…but trust in organizations is actually decreasing…

Trust level in organizations is low

Unethical Behavior

Discrepancy between external and

internal demands(Value Shift)

System criticism, lack of solutions to social problems

Based on WEF (2006) data

02.11.07 Michael PirsonHarvard University

A trust gap evolved, hampering organizational effectiveness.

Problem: How can organizations, and management boards deal

with the trust gap effectively, counter the trend of declining trust, and sustain competitive advantage?

1. Know what trust is2. Be able to measure it3. And find out which antecedents of trust are most

relevant to trust 4. Find ways to influence them

2 Research Problem

02.11.07 Michael PirsonHarvard University

3 Concept of Trust

What is trust?

Trust in general is the willingness to be vulnerable to the actions of another party based on positive expectations regarding the motivation and behavior of the other (Mayer et al. 1995; Rousseau et al., 1998).

Expectations are often based on attributions of the other party along relevant characteristics:

Competence (Jarvenpaa and Tractinsky, 1999; Shockley-Zalabak, Ellis et al., 1999)Integrity (McAllister, 1995; Mishra, 1996); Benevolence (Mayer, Davis et al., 1995; Hoy and Tschannen - Moran, 1999);Transparency (Rotter, 1971; Morgan and Hunt, 1994; Pavlou, 2002), Identification ( Lewicki and Bunker, 1995; Shockley-Zalabak, Ellis et al., 1999)

Stakeholder trust can be defined as a behavioral attitude by a stakeholder towards an organization based on the perception of the organizations trustworthiness evaluated along the dimensions of transparency, integrity, competence, benevolence, and identification (Mishra, 1996; Tschannen-Moran, 2000; Shockley Zalabak, 2004).

02.11.07 Michael PirsonHarvard University

3 Concept of Trust

Antecedents of trust

Competence-based trust is relevant to stakeholders that must rely on the organization’s ability to perform in the manner that is expected or promised. (Jarvenpaa & Tractinsky, 1999; Shockley-Zalabak et al., 1999; McKnight & Chervany 2002).

Integrity-based trust is based on perceptions of the organization as honest and forthcoming, such that they not act immorally or unfairly (Whitener et al., 1998; Hoy & Tschannen-Moran, 1999; Pavlou, 2002). Mishra and Spreitzer (1998)

Benevolence-based trust stems from the belief that the organization cares about the particular stakeholder and will thus act in ways that are in the stakeholder’s best interest. (Edmondson, 1999).

Transparency-based trust is based on openness of an organization and the commitment to communicate relevant issues with stakeholders. (Turnbull, 2002; Dervitsiotis, 2003).

Identification-based trust stems from value congruence, and the perception of shared identity. (Schein, 1985; Shockley-Zalabak & Morley, 1994; Shockley-Zalabak et al., 1997; Ellis & Shockley-Zalabak 1999).

02.11.07 Michael PirsonHarvard University

• Trust here is viewed as a behavioral attitude (Schweer and Thies 2003), which according to Thurstone (1928), can be measured.

• Developing survey measures – Panel of experts– Pretests– Field test– Large scale study

• 2,053 respondents • 4 different organizations and • 8 different stakeholder groups

• Reliability and validity of the items, and constructs were confirmed (correlation analyses, discriminatory analyses, exploratory and confirmatory factor analyses).

• However, competence seems to be a two factor concept (managerial and technical aspects)

4 Trust Measurement

02.11.07 Michael PirsonHarvard University

5 Quantitative Study Stakeholder trust – what antecedents matter to whom?

Currently trust is seen as a general construct (Mayer & Davis, 1999; Lusch et al., 2003; Mayer & Gavin, 2005)

• trust is situation and context-specific (Coleman 1990; Zey 1998)

• What are the contexts for organizational trust?

Research question: Is stakeholder trust context specific or not, and are some antecedents more relevant than others?

02.11.07 Michael PirsonHarvard University

5 Quantitative Study

Conceptualization of Stakeholder trust2 Dimensions

• Locus: relates to the position that the stakeholder has towards the organization, which translates into different expectations.

(internal/external)• Depth: relates to the type and degree of vulnerability that the stakeholder

faces.( measured by interaction frequency and relationship duration)

external

internal

high lowDEPTH

LOCUS

H5

H7 H8

H1H2H3H4

H6

02.11.07 Michael PirsonHarvard University

DepthLow-depth relationships• Hypothesis 1: Stakeholder trust in low-depth relationships will

be based on perceptions of transparency and integrity.

High-depth relationships• Hypothesis 2: Stakeholder trust in high-depth relationships will

be based on perceptions of integrity and benevolence while perceptions of transparency do not play a role.

• Hypothesis 3: Perceived benevolence will be significantly more relevant to stakeholder trust in high-depth relationships than in low-depth relationships.

• Hypothesis 4: Perceived integrity and transparency will be significantly less relevant to stakeholder trust in high-depth relationships than in low-depth relationships.

5 Quantitative Study-Hypotheses

02.11.07 Michael PirsonHarvard University

LocusCompetence• Hypothesis 5: Perceived managerial competence will be more

relevant to trust among internal stakeholders than among external stakeholders.

• Hypothesis 6: Perceived technical competence will be more relevant to trust among external stakeholders than among internal stakeholders.

Identification• Hypothesis 7: Identification will be relevant to stakeholder trust

in internal relationships only.• Hypothesis 8: Identification will be more relevant to

stakeholder trust for internal, high-depth stakeholders, than for any other type of stakeholder.

5 Quantitative Study-Hypotheses

02.11.07 Michael PirsonHarvard University

5 Quantitative Study-Hypotheses

external

internal

high lowDEPTH

Managerial Competence +

Technical Competence -

Benevolence

Integrity -

Identification

LOCUSManagerial Competence +

Technical Competence -

Integrity +

Transparency

Managerial Competence -

Technical Competence +

Benevolence

Integrity -

Managerial Competence -

Technical Competence +

Integrity +

Transparency

02.11.07 Michael PirsonHarvard University

• Internet-based questionnaire

• Sample: Clients, Employees, Investors, Suppliers– from four different organizations in Western Europe.

• Organization 1 is a small to medium-sized firm in the manufacturing industry in Switzerland;

• Organization 2 is a large logistical company based in Germany;

• Organization 3 is a Western European branch of an international consulting firm;

• Organization 4 is a public university in Switzerland.

5 Quantitative Study - Method and Sample

02.11.07 Michael PirsonHarvard University

Organization

Stakeholder 1 2 3 4 Total

Customers 23 512 66 0 601

Employees 43 153 117 110 423

Suppliers 22 115 4 0 141

Investors 4 40 89 0 133

Total 93 876 404 110 1298

5 Quantitative Study - Method and Sample

02.11.07 Michael PirsonHarvard University

Independent Measures• established based on works of Mishra (1996), Hoy and

Tschannen-Moran (1999) and Shockley-Zalabak and Ellis (2004)

• 3 to 4 items per antecedent of trust that demonstrate high convergent and discriminatory validity. (alphas ranging from .8-.9)

Dependent Measure• based on Shockley-Zalabak and Ellis (2004) and Globalscan

(2003)• combination of two items measure the stakeholder’s level of

trust in the organization: “The organization is trustworthy”, and “I trust the organization” (alpha= .8)

Control MeasuresAge, Gender, Organization, Stakeholder type, Multiple Stakeholdership

5 Quantitative Study-Measures

02.11.07 Michael PirsonHarvard University

5 Quantitative Study

General analysis: (multiple regression models)

1) Test significance of the elements of trust across all stakeholders. • all dimensions relevant • except for transparency

2) we included controls and also tested the significance of our categorization. • both dimensions are significant (depth: p=.02; locus: p=.056) • even though the locus dimension only remains within a 90%

confidence interval

02.11.07 Michael PirsonHarvard University

5 Quantitative StudyDepth: The Relevance of Integrity, Benevolence, and

Transparency

Absolute significance: In low depth relationships• integrity is a highly significant (b=.407; p<.001), • while benevolence is not (b=.058; p=.147). However, contrary to Hypothesis 1 we find that transparency is not a significant element of organizational trust in low-depth relationships (b=.011; p=.755).

In high-depth relationships• integrity (b=.239; p<.001) and • benevolence (b=.219; p<.001) are crucial • while transparency is not (b=-.02; p=.596).

02.11.07 Michael PirsonHarvard University

Relative significance• Benevolence is significantly more salient in high-depth

relationships than low-depth relationships, interaction term for benevolence and depth ( b=0.164; p=. 004).

• Integrity is significantly more relevant for stakeholders in low-depth relationships than in high-depth relationships interaction term for integrity and depth (b=-.167; p=.001)

• Transparency, however, displays no significant change.

Overall

considerable support for the model

Exception: the role of transparency

Test of the very low-depth relationships: no significance.

5 Quantitative StudyDepth: The Relevance of Integrity, Benevolence, and

Transparency

02.11.07 Michael PirsonHarvard University

Relevance of Managerial and Technical Competence• The model predicted that internal stakeholders value managerial

competence more than external stakeholders (Hypothesis 5) and external stakeholders value technical competence more than internal stakeholders (Hypothesis 6).

• Using the categorization of employees and investors as internal stakeholders and customers and suppliers as external stakeholders we find indeed that internal stakeholders rely significantly more on managerial competence attributions when trusting the organization than external stakeholders. The interaction effect of managerial competence and locus is significant at p<.05 (b=-.103, p=.022).

• We also find that external stakeholders value technical competence significantly more than internal stakeholders. The interaction effect of technical competence and locus is also significant at p<.05 (b=.097, p=.031).

• These results strongly support hypotheses 5 and 6.

5 Quantitative StudyStakeholder Locus

02.11.07 Michael PirsonHarvard University

• Identification and Trust• We predicted that identification would only be a significant predictor for trust

among internal stakeholders in high-depth relationships with the organization (Hypothesis 7). Results show (Table 5) that identification plays a significant role in all stakeholder relationships: low-depth stakeholders (b=.202; p<.001), high-depth stakeholders (b= .274; p<.001), internal (b=.314; p<.001) and external stakeholders (.b=.199; p<.001)

• This intriguing result contradicts prior research (Lewicki et al., 1996) which suggests that identification is a relevant factor in very few relationships.

• We also suggested that identification would be significantly more relevant to internal high-depth stakeholders than any other group (Hypothesis 8). In Model 4 (Table 6) the base case represents all stakeholders that are external and high depth as well as internal and external stakeholder with low-depth relations. The interaction effects demonstrate the changes for internal and high-depth relationship stakeholders. The results of Model 4 (Table 6) thus show strong support for our hypothesis as the interaction effect for identification and internal and high-depth relationship stakeholders is highly significant (b=.171, p=.002).[i]

•[i] We also find a significant interaction effect for integrity. We attribute this finding to the above mentioned effects of relationship depth also expressed in Model 4.

5 Quantitative Study-Results

02.11.07 Michael PirsonHarvard University

H4: Internal Stakeholder relationships (Managerial Competence and Identification)

5 Quantitative Study-Results

02.11.07 Michael PirsonHarvard University

5 Quantitative Study-Results

external

internal

high lowDEPTH

Managerial Competence +

Technical Competence -

Benevolence

Integrity -

Identification+

LOCUSManagerial Competence +

Technical Competence -

Integrity +

Identification

Managerial Competence -

Technical Competence +

Benevolence

Integrity –

Identification

Managerial Competence -

Technical Competence +

Integrity +

Identification

02.11.07 Michael PirsonHarvard University

• Prior research states one size fits all (e.g. Morgan & Hunt, 1994; Mayer & Davis, 1999; Lusch et al., 2003; Mayer & Gavin, 2005).

• We find there are stakeholder specificities• Intensity categorization can be helpful

– Those stakeholders that have low intensity relationships base their trust largely on perceptions of integrity. Trust among stakeholders that have high intensity relationships (e.g., employees and clients), on the other hand, is also affected by perceptions of benevolence and reliability.

• Locus categorization results are mixed

Surprises: – no role of transparency (=>Sarbanes Oxley, CG codes etc.)

The organization...• explains its decisions.• says, if something goes wrong.• is transparent.• openly shares all relevant information.

– role of identification (value congruence) across all stakeholders

Limitations: • Cross sectional view,• four different organizations, • skewed sample

5 Quantitative Study-Discussion

02.11.07 Michael PirsonHarvard University

Method and sampleMethod• semi-structured interviews (interviews spanned

from 20 to 90 minutes, averaging about 40 minutes)

Sample• 32 semi-structured interviews, with different

stakeholder groups across different organizations.

6 Qualitative Study-Method and Sample

Organization 1 2 3 4 othersNo. of respondents 4 6 3 4 21Stakeholder Employee Client Investor Supplier Competitor Student

16 18 5 3 2 4

Interview distribution (N=32)*

02.11.07 Michael PirsonHarvard University

1 INTERVIEWER: So can you tell me why you don’t trust any bank? CLIENT: that’s a difficult question. I think they only care about the money which is on the account and how they can use the last dollar of every customer. But, it’s not really about your money, ‘cause you don’t get really a lot of interest on your savings account either. And, you actually pay more interest if you overcharge your account, … I don’t think this is the way it should be.

2 FORMER EMPLOYEE: …I trust [organization 3] less, because what I don’t like about the organization is that they are basically profit motivated.

3 INTERVIEWER: Which societal organizations do you trust the most and which the least?

• RESPONDENT: … trust in the church and NGO’s is high, business I trust much less, for example the pharma industry is only interested in making profit. They are aligned in a way that they have to screw you over…

4 INTERVIEWER: So, would you say you trust businesses in general? • RESPONDENT:… for businesses in general [my trust] would be quite low. • INTERVIEWER: Because? • RESPONDENT: Because, well they’re profit motivated.. .

6 Qualitative Study-Results

02.11.07 Michael PirsonHarvard University

5 INTERVIEWER: But is there one organization that you can come up with that you trust the most?.. or which one would you consider specifically trustworthy?

• RESPONDENT: For me, family businesses are often much more trustworthy because the reputation of the owner’s family is at stake. They’re much more attached to their local environment because they often live in that area and, therefore, have an expectation to live up to.

6 INTERVIEWER: So, can you tell me why you trust churches..? • RESPONDENT: Yeah, … you know where they come from, you trust them

because they have… an altruistic view of what life is about, [they are] … concerned with serving others than themselves.

7 INTERVIEWER: So why do you trust the police? • RESPONDENT: …the Swiss police. I have the impression that… in Europe,

or in countries I’ve been to, I can really trust the police. And …when you have a problem, you can go to them and they will somehow help you. Not … when you…pay them money, then they will help you, or that they just send you right away, but they will somehow help you. Whether it’s successful or not, I don’t know. … the police … helps.

6 Qualitative Study-Results

02.11.07 Michael PirsonHarvard University

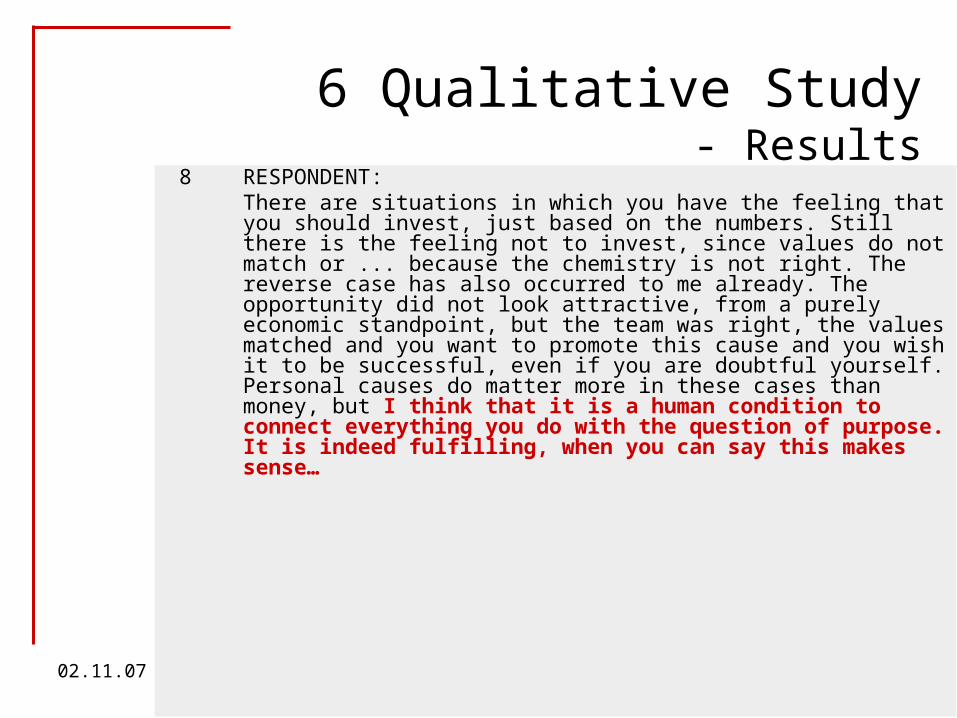

8 RESPONDENT: There are situations in which you have the feeling that you should invest, just based on the numbers. Still there is the feeling not to invest, since values do not match or ... because the chemistry is not right. The reverse case has also occurred to me already. The opportunity did not look attractive, from a purely economic standpoint, but the team was right, the values matched and you want to promote this cause and you wish it to be successful, even if you are doubtful yourself. Personal causes do matter more in these cases than money, but I think that it is a human condition to connect everything you do with the question of purpose. It is indeed fulfilling, when you can say this makes sense…

6 Qualitative Study- Results

02.11.07 Michael PirsonHarvard University

7 Managerial Implications and Limitations

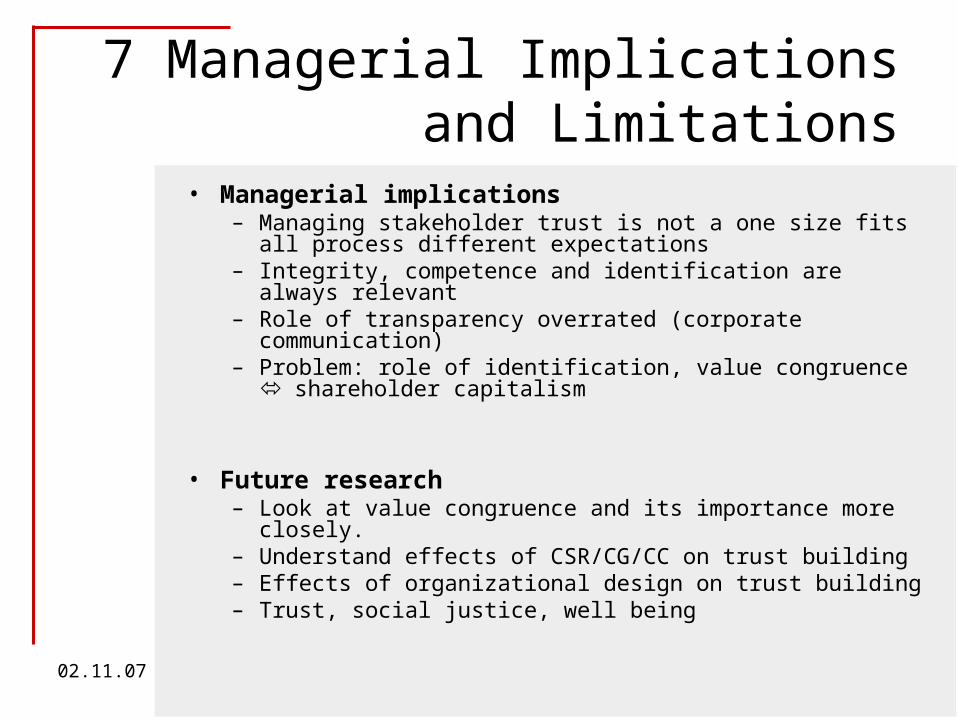

• Managerial implications– Managing stakeholder trust is not a one size fits all process

different expectations – Integrity, competence and identification are always relevant– Role of transparency overrated (corporate communication)– Problem: role of identification, value congruence

shareholder capitalism

• Future research– Look at value congruence and its importance more closely.– Understand effects of CSR/CG/CC on trust building– Effects of organizational design on trust building– Trust, social justice, well being

02.11.07 Michael PirsonHarvard University

8 Discussion

• Questions

• Suggestions

• Comments

02.11.07 Michael PirsonHarvard University

Regression resultsRelevance of Trust Antecedents for different stakeholder groups

Stakeholder TypeVariable B S.E. B S.E. B S.E. B S.E.

Intercept 0.063 0.125 0.375 0.118 -0.007 0.158 0.083 0.150Managerial Competence 0.167*** 0.033 0.079* 0.037 0.202*** 0.036 0.102** 0.033Technical Competence 0.209*** 0.030 0.181*** 0.032 0.130*** 0.033 0.218*** 0.030Integrity 0.407*** 0.035 0.239*** 0.037 0.274*** 0.037 0.344*** 0.035Transparency 0.011 0.037 -0.020 0.038 0.022 0.038 -0.012 0.036Benevolence 0.058 0.040 0.219*** 0.041 0.108** 0.039 0.141** 0.041Identification 0.202*** 0.030 0.274*** 0.031 0.314*** 0.031 0.199*** 0.029

Gender 0.027 0.048 0.022 0.052 0.065 0.049 -0.024 0.050Age -0.042 0.029 -0.025 0.028 -0.050 0.032 -0.011 0.027Multiple Stakeholdership -0.081 0.051 -0.102 0.051 -0.075 0.043 -0.116 0.060

Organization 1 -0.074 0.086 0.038 0.111 0.028 0.091 0.104 0.115Organization 2 0.087 0.066 0.143 0.081Organization 3 -0.086 0.065 0.007 0.080Organization 4 0.071 0.097 0.149 0.092 0.169* 0.066

Employee -0.081 0.064 -0.065 0.068CustomerInvestor -0.189* 0.077 -0.158 0.078 -0.046 0.055Supplier -0.065 0.071 -0.035* 0.093 -0.115* 0.058

Adjusted R Square 0.721 0.758 0.730 0.662N 665 633 556 742* p < .05** p < .01*** p < .001

Low-Depth High-Depth Internal External

02.11.07 Michael PirsonHarvard University

Regression resultsTable 5

B S.E. B S.E. B S.E. B S.E. B S.E.

(Constant) 2.969*** (0.104) 0.172 (0.06) 0.116 (0.098) 0.071 (0.116) 0.144 (0.095)

Managerial Competence 0.108*** (0.021) 0.133*** (0.025) 0.225*** (0.044) 0.137*** (0.026)

Technical Competence 0.182*** (0.022) 0.19*** (0.022) 0.135** (0.041) 0.209*** (0.024)

Integrity 0.332*** (0.025) 0.331*** (0.025) 0.36*** (0.047) 0.359*** (0.028)

Transparency 0.002 (0.026) -0.007 (0.026) 0.043 (0.05) -0.004 (0.03)

Benevolence 0.128*** (0.028) 0.126*** (0.028) 0.026 (0.053) 0.105** (0.032)

Identification 0.227*** (0.02) 0.236*** (0.021) 0.279*** (0.04) 0.21*** (0.024)

Age -0.059† (0.035) -0.034† (0.02) -0.029 (0.02) -0.032 (0.02)

Gender -0.057 (0.06) 0.02 (0.035) 0.031 (0.035) 0.019 (0.035)

Multiple Stakeholdership -0.04 (0.061) -0.108** (0.035) -0.087* (0.036) -0.096** (0.036)

Organization 1 ‡ 0.789*** (0.107) -0.032 (0.067) -0.057 (0.067) -0.037 (0.068)

Organization 3 0.509*** (0.074) -0.063 (0.05) -0.079 (0.051) -0.035 (0.052)

Organization 4 0.588*** (0.108) 0.133* (0.065) 0.07 (0.067) 0.11† (0.067)

Employees‡‡ 0.717*** (0.071) -0.144 (0.147) -0.085 (0.056)

Suppliers 0.245** (0.089) -0.095† (0.053) -0.099† (0.053)

Investors 0.369*** (0.1) -0.192 (0.148) -0.133* (0.065)

Locus 0.078† (0.041) -0.063 (0.042)

Depth 0.073* (0.031) 0.294* (0.12) 0.082* (0.041)

Deep/ Internal 0.224 (0.201)

Managerial Competence * Depth -0.063 (0.042)

Technical Competence * Depth -0.016 (0.043)

Integrity * Depth -0.167** (0.051)

Transparency * Depth -0.041 (0.052)

Benevolence * Depth 0.164** (0.057)

Identification * Depth 0.068 (0.041)

Managerial Competence * Locus -0.103* (0.045)

Technical Competence * Locus 0.097* (0.045)

Integrity * Locus 0.065 (0.052)

Transparency * Locus -0.038 (0.054)

Benevolence * Locus 0.056 (0.057)

Identification * Locus -0.12** (0.044)

Managerial Competence * Deep/Internal -0.041 (0.052)

Technical Competence * Deep/Internal -0.094 (0.058)

Integrity* Deep/Internal -0.176** (0.065)

Transparency * Deep/Internal 0.018 (0.065)

Benevolence* Deep/Internal 0.087 (0.064)

Identification * Deep/Internal 0.171** (0.054)

Adjusted R20.229 0.732 0.737 0.743 .741

† p < .10; * p < .05; ** p < .01; *** p < .001‡ Organization 2 is base case.‡‡ Customers are base case. Stakeholder controls are only introduced in Model 3 because locus dimensions effects would be skewed.

Model 4Model 0 Model 1 Model 2 Model 3

02.11.07 Michael PirsonHarvard University

Descriptives and Correlations

Table 3Means, Standard Deviations, Correlations and Scale Reliabilities for Study VariablesVariable Mean S.D. 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 161. Managerial Competence 3.16 1.14 (0.87)2. Technical Competence 3.54 1.05 0.68 ** (0.85)3. Reliability 3.07 0.98 0.74** 0.73** (0.86)4. Integrity 3.25 1.02 0.61** 0.63** 0.77** (0.85)5. Transparency 2.87 0.91 0.64** 0.57** 0.74** 0.69** (0.87)6. Benevolence 2.97 0.96 0.60** 0.61** 0.76** 0.76** 0.71** (0.88)7. Identification 2.96 1.20 0.65** 0.64** 0.70** 0.67** 0.63** 0.70** (0.93)8. Trust 3.29 1.05 0.68** 0.70** 0.77** 0.77** 0.65** 0.72** 0.75** (0.8)9. Recommendation 3.17 1.08 0.69** 0.69** 0.71** 0.68** 0.63** 0.70** 0.84** 0.76** (0.9)10. Gender 0.26 0.44 -0.05** -0.06 -0.04 -0.03 -0.01 -0.05 -0.09 -0.04** -0.08**11. Age 2.72 0.76 0.05 0.04 0.01 -0.02 -0.02 -0.03 0.01 -0.01 0.03 -0.14**12. Contact Duration 3.19 0.97 -0.24** -0.18** -0.26** -0.20** -0.19** -0.23** -0.19** -0.15** -0.18** -0.03 0.19**13. Multiple Stakeholder 0.29 0.45 0.18** 0.18** 0.15** 0.12** 0.10** 0.14** 0.22** 0.12** 0.20** -0.07** 0.02 -0.11**14. Organization 1 0.07 0.26 0.23** 0.14** 0.22** 0.18** 0.22** 0.26** 0.17** 0.18** 0.18** -0.12** 0.18** -0.04 -0.06*15. Organization 2 0.63 0.48 -0.65** -0.42** -0.49** -0.36** -0.36** -0.35** -0.41** -0.40** -0.44** 0.05 -0.05 0.36** -0.18** -0.36**16. Organization 3 0.21 0.41 0.46** 0.29** 0.30** 0.20** 0.19** 0.13** 0.22** 0.21** 0.26** -0.03 -0.07* -0.36** 0.16** -0.14** -0.71**17. Organization 4 0.08 0.28 0.24** 0.18** 0.21** 0.17** 0.14** 0.18** 0.22** 0.22** 0.22** 0.07* 0.03 -0.06* 0.14** -0.08** -0.4** -0.16**N=1298 Alpha Coefficients on the diagonal in parentheses. ** correlations significant at 0.01 level, * correlations significant at 0.05 level.

02.11.07 Michael PirsonHarvard University

Scale Items Measuring Each Construct

Managerial Competence The organization...• can successfully adapt to changing demands.• is able to reach set goals.Technical Competence The organization...• is very competent in its area.• generally has high standards.Reliability The organization...• is consistent when dealing with stakeholders.• communicates regularly important events and

decisions.• does what it says.• is reliable.Transparency The organization...• explains its decisions.• says, if something goes wrong.• is transparent.• openly shares all relevant information.

Integrity The organization…• does not try to deceive.• has high moral standards.• treats its stakeholder with respect.Benevolence The organization...• is caring.• listens to my needs.• is fair.• does not abuse stakeholder.Reputation • The organization enjoys a high reputation.• People I know speak highly of the organization.• Stakeholders are positive towards the organization.

02.11.07 Michael PirsonHarvard University

3 Concept of Trust

(Lewicki and Bunker 1995)

Development of trust