Embed Size (px)

Citation preview

1

Japanese Experiences with Public and Private Sectors in

Urban Railways

September 6th 2005

Ken’ichi ShojiGraduate School of Business

Kobe University ([email protected])

9TH CONFERENCE ON COMPETITION AND OWNERSHIP IN LAND TRANSPORT

2

• Private railway companies are common and play an important role in Japanese passenger transport, especially in urban areas.

• They are financially independent and in most case their rail operation makes profits.

• Given the “self-supporting” (or “full-cost principle”) principle, the national government set up several special subsidy programmes for special cases, mainly for the new line construction projects

INTRODUCTION

3

• The subsidy programmes has been not applicable for most efficient rail operators: private railways. – to get the funds from the governments, the local

community have to employ the public (or semi-public) operator

– it becomes more difficult to thrive the rail business even for the most efficient management under the self-support principle

need to think collective interests, though market is most powerful and efficient device in guiding provision

• Lack of smart programmes which allow private railways to benefit from subsidization

Our Problems

4

• to search the smart way of subsidy programmes which is applicable for private (directly or indirectly) and dose not contaminate for the privates’ efficient management system. – A case of Kobe-Kosoku– New cases at Osaka area

• Both attempts utilize– Public-private mixed company– Infrastructure-Operation Separation

New Schemes

5

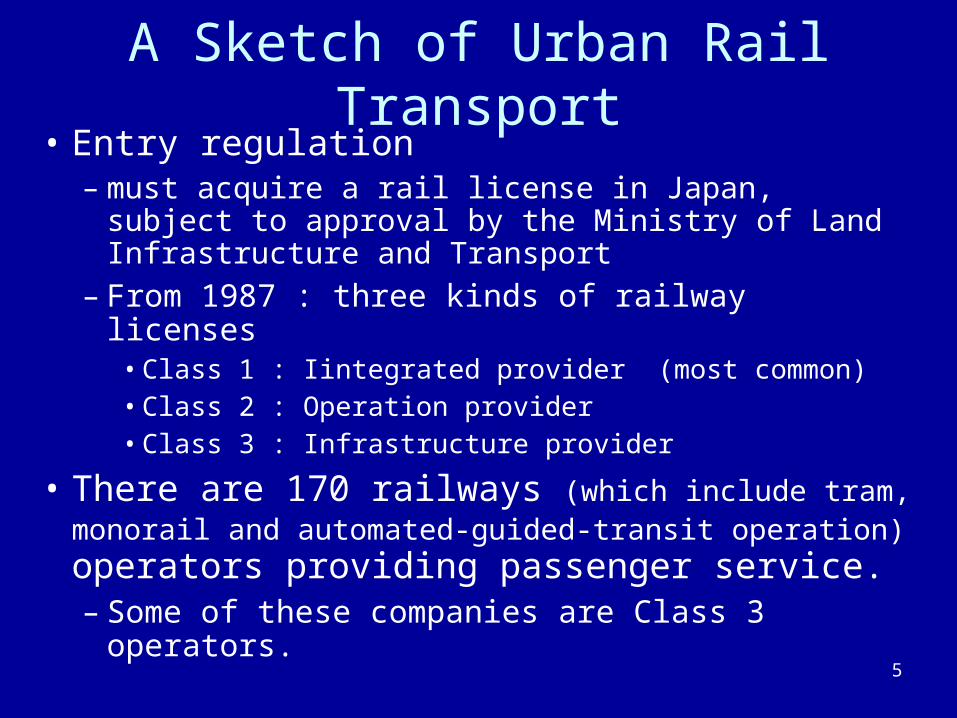

• Entry regulation – must acquire a rail license in Japan, subject to approval

by the Ministry of Land Infrastructure and Transport– From 1987 : three kinds of railway licenses

• Class 1 : Iintegrated provider (most common)• Class 2 : Operation provider • Class 3 : Infrastructure provider

• There are 170 railways (which include tram, monorail and automated-guided-transit operation) operators providing passenger service. – Some of these companies are Class 3 operators.

A Sketch of Urban Rail Transport

6

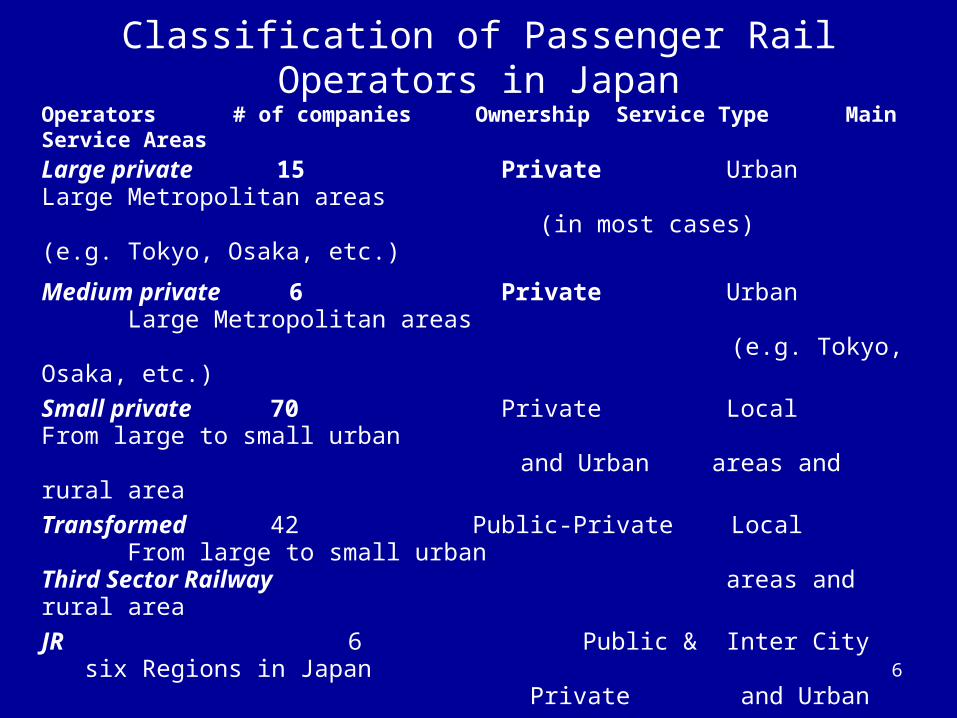

Classification of Passenger Rail Operators in JapanOperators # of companies Ownership Service Type Main Service Areas

Large private 15 Private Urban Large Metropolitan areas (in most cases) (e.g. Tokyo, Osaka, etc.)

Medium private 6 Private Urban Large Metropolitan areas (e.g. Tokyo, Osaka, etc.)

Small private 70 Private Local From large to small urbanand Urban areas and rural area

Transformed 42 Public-Private Local From large to small urbanThird Sector Railway areas and rural area

JR 6 Public & Inter City six Regions in Japan Private and Urban

TRTA 1 Public* Urban Tokyo

Municipal 12 Public Urban Tokyo, Osaka, Nagoya (local government) and 6 other large cities

Monorail 9 Public-Private Urban Large Metropolitan areas (partly private) and large urban area

AGT 9 Public-Private Urban Large Metropolitan areas

7

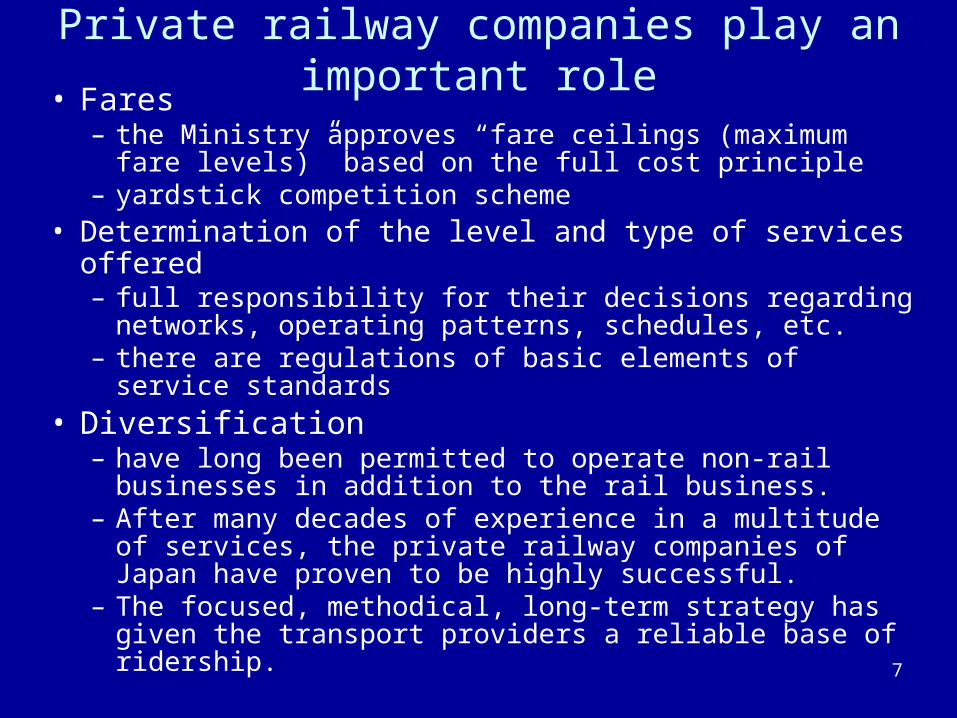

Private railway companies play an important role• Fares

– the Ministry approves “fare ceilings (maximum fare levels)” based on the full cost principle

– yardstick competition scheme • Determination of the level and type of services offered

– full responsibility for their decisions regarding networks, operating patterns, schedules, etc.

– there are regulations of basic elements of service standards • Diversification

– have long been permitted to operate non-rail businesses in addition to the rail business.

– After many decades of experience in a multitude of services, the private railway companies of Japan have proven to be highly successful.

– The focused, methodical, long-term strategy has given the transport providers a reliable base of ridership.

8

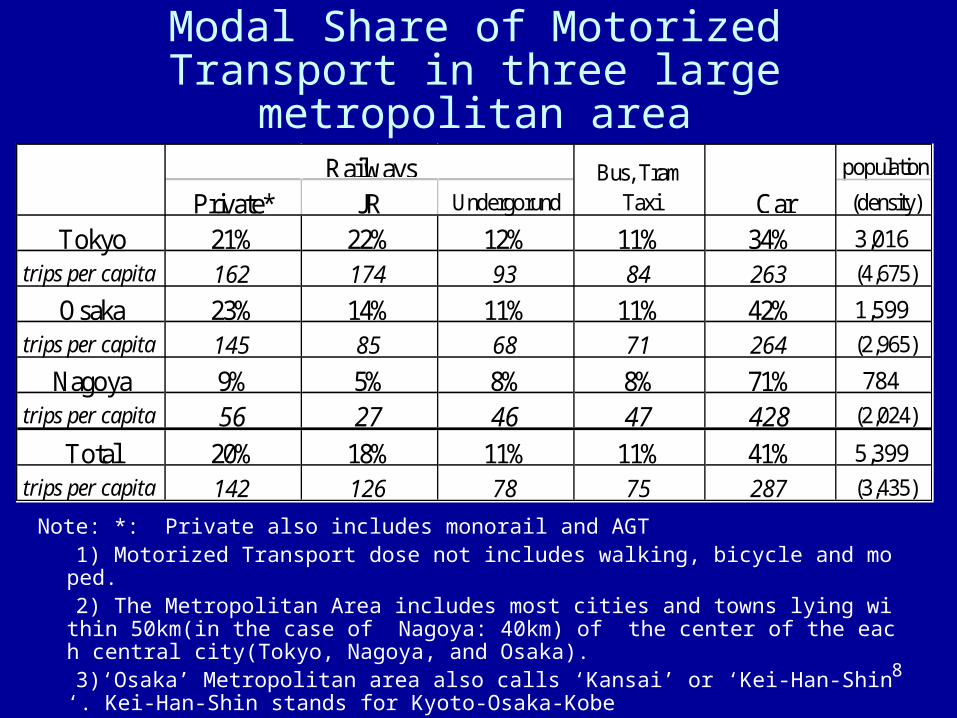

Modal Share of Motorized Transport in three large metropolitan area

population

Private* JR Undergorund (density)

Tokyo 21% 22% 12% 11% 34% 3,016

trips per capita 162 174 93 84 263 (4,675)

Osaka 23% 14% 11% 11% 42% 1,599

trips per capita 145 85 68 71 264 (2,965)

Nagoya 9% 5% 8% 8% 71% 784

trips per capita 56 27 46 47 428 (2,024)

Total 20% 18% 11% 11% 41% 5,399

trips per capita 142 126 78 75 287 (3,435)

Railways Bus, TramTaxi Car

Note: *: Private also includes monorail and AGT 1) Motorized Transport dose not includes walking, bicycle and moped. 2) The Metropolitan Area includes most cities and towns lying within 50km(in the case of Nagoya:

40km) of the center of the each central city(Tokyo, Nagoya, and Osaka). 3)‘Osaka’ Metropolitan area also calls ‘Kansai’ or ‘Kei-Han-Shin ‘. Kei-Han-Shin stands for Kyoto

-Osaka-KobeSource: Unyu Keizai Center, Toshi Kotsu Nenpo, 2002

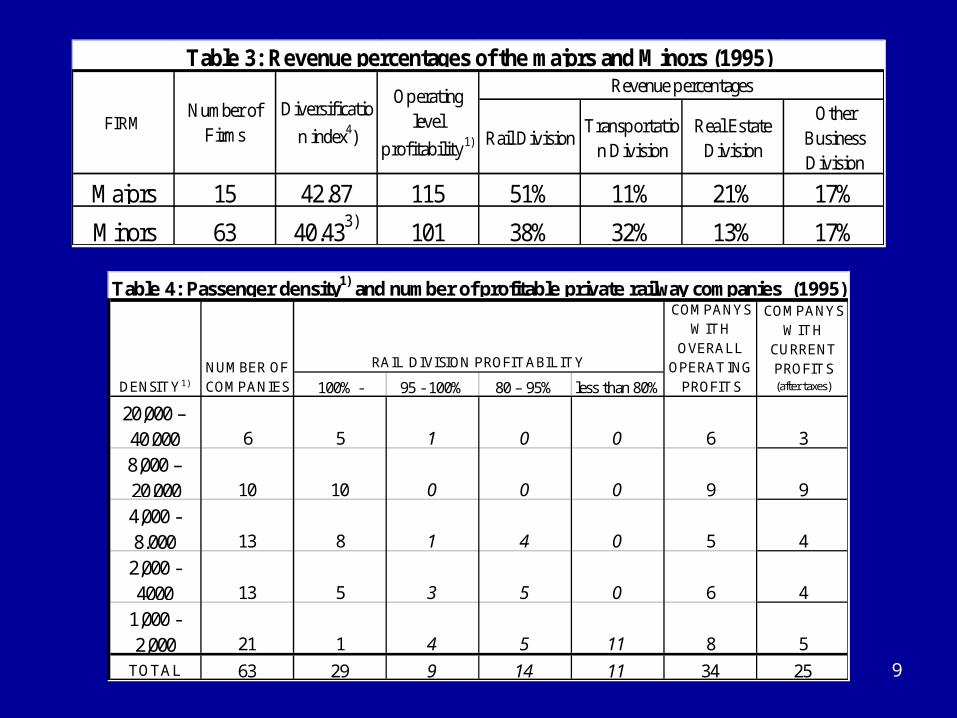

9

100% - 95 - 100% 80 – 95% less than 80%

20,000 –40,000 6 5 1 0 0 6 3

8,000 –20,000 10 10 0 0 0 9 9

4,000 -8.000 13 8 1 4 0 5 4

2,000 -4000 13 5 3 5 0 6 4

1,000 -2,000 21 1 4 5 11 8 5

TOTAL 63 29 9 14 11 34 25

Table 4: Passenger density1) and number of profitable private railway companies (1995)

DENSITY1)

NUMBER OFCOMPANIES

RAIL DIVISION PROFITABILITY

COMPANYSWITH

OVERALLOPERATING

PROFITS

COMPANYSWITH

CURRENTPROFITS(after taxes)

Rail DivisionTransportatio

n DivisionReal Estate

Division

OtherBusinessDivision

Majors 15 42.87 115 51% 11% 21% 17%

Minors 63 40.433) 101 38% 32% 13% 17%

Table 3: Revenue percentages of the majors and Minors (1995)Revenue percentages

Number ofFirms

Diversificatio

n index4)

Operatinglevel

profitability1)

FIRM

10

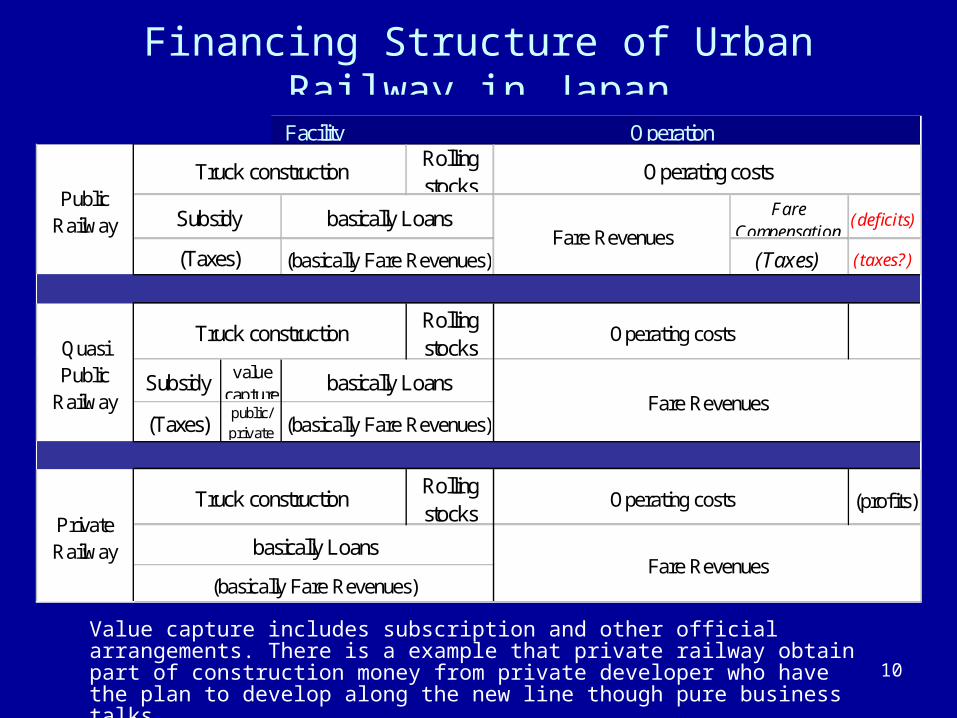

Financing Structure of Urban Railway in Japan

Rollingstocks

FareCompensation

(deficits)

(Taxes) (taxes?)

Rollingstocks

Subsidy valuecapture

(Taxes)public/private

Rollingstocks

(profits)PrivateRailway

Truck construction Operating costs

basically LoansFare Revenues

(basically Fare Revenues)

PublicRailway

Operating costs

Facility Operation

Truck construction

basically LoansSubsidy

(Taxes)Fare Revenues

(basically Fare Revenues)

QuasiPublic

Railway

Truck construction Operating costs

Fare Revenuesbasically Loans

(basically Fare Revenues)

Value capture includes subscription and other official arrangements. There is a example that private railway obtain part of construction money from private developer who have the plan to develop along the new line though pure business talks.

11

Just Remind: because Private Railways is financially independent

• In general, the Ministry itself does not generate plans for railway projects, but acts more as a director to the actors on the stage.

• the planning of a railway project is not done by the Ministry but by each individual rail enterprise. The Ministry assesses plan based on the opinions of Transport Policy Committees.

• however, there are cases in which the public sector gets involved in railway network planning. – Shinkansen (High Speed Train) network– public underground networks, which are operated by local

governments. – it is possible for the public sector to work together with the

private sector, which occurs especially in railway projects in city and/or suburbs in large metropolitan areas

12

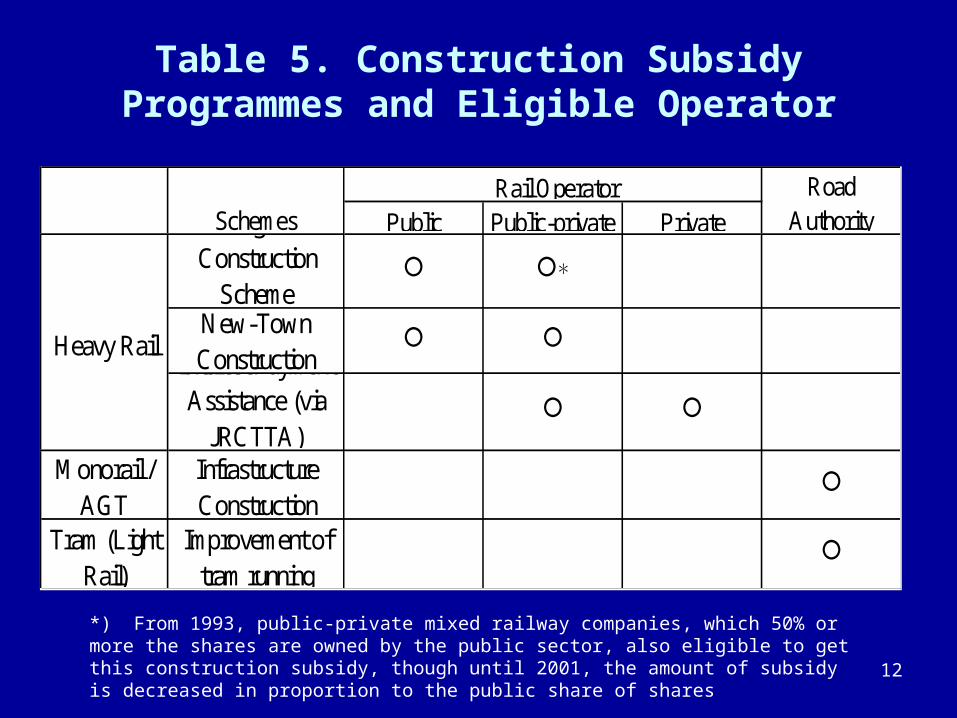

Table 5. Construction Subsidy Programmes and Eligible Operator

Public Public-private PrivateUndergroundConstruction

Scheme *

New-TownConstruction

Interest PaymentAssistance (via

JRCTTA)

Monorail /AGT

InfrastructureConstruction

Tram (LightRail)

Improvement oftram running

Heavy Rail

Schemes Rail Operator Road

Authority

*) From 1993, public-private mixed railway companies, which 50% or more the shares are owned by the public sector, also eligible to get this construction subsidy, though until 2001, the amount of subsidy is decreased in proportion to the public share of shares

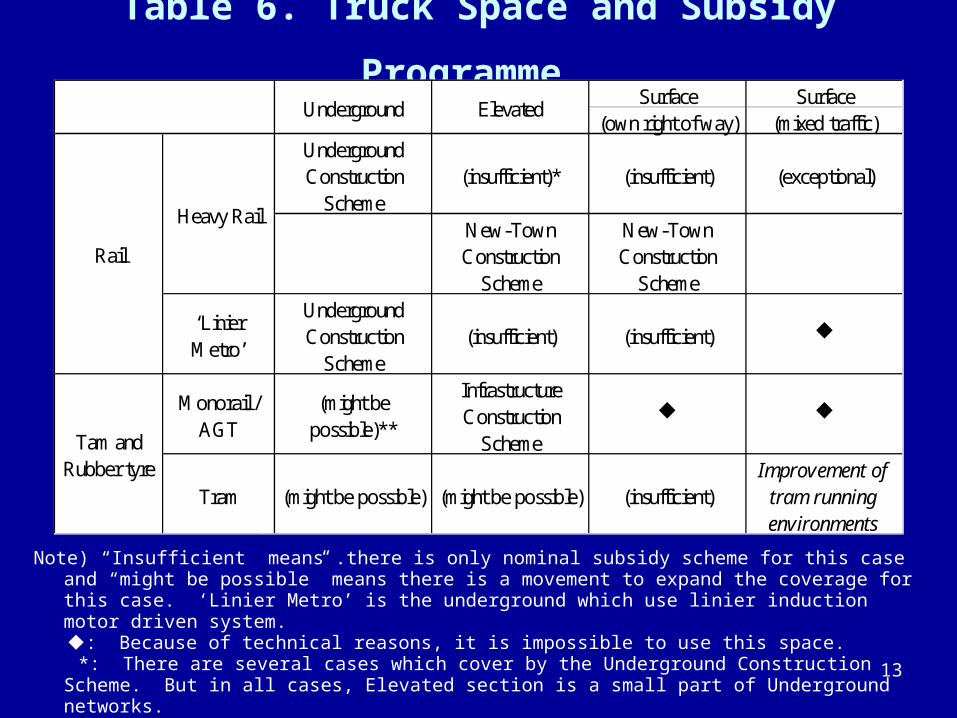

13

Table 6. Truck Space and Subsidy Programme Surface Surface

(own right of way) (mixed traffic)UndergroundConstruction

Scheme(insufficient)* (insufficient) (exceptional)

New-TownConstruction

Scheme

New-TownConstruction

Scheme

‘LinierMetro’

UndergroundConstruction

Scheme(insufficient) (insufficient)

Monorail /AGT

(might bepossible)**

InfrastructureConstruction

Scheme

Tram (might be possible) (might be possible) (insufficient)Improvement of

tram runningenvironments

Tam andRubber tyre

Underground Elevated

Rail

Heavy Rail

Note) “Insufficient” means .there is only nominal subsidy scheme for this case and “might be possible” means there is a movement to expand the coverage for this case. ‘Linier Metro’ is the underground which use linier induction motor driven system.

: Because of technical reasons, it is impossible to use this space. *: There are several cases which cover by the Underground Construction Scheme. But in all cases, Elevated

section is a small part of Underground networks. **: From 2002, Infrastructure Construction Scheme also covers this case, though there is no achievement example .

14

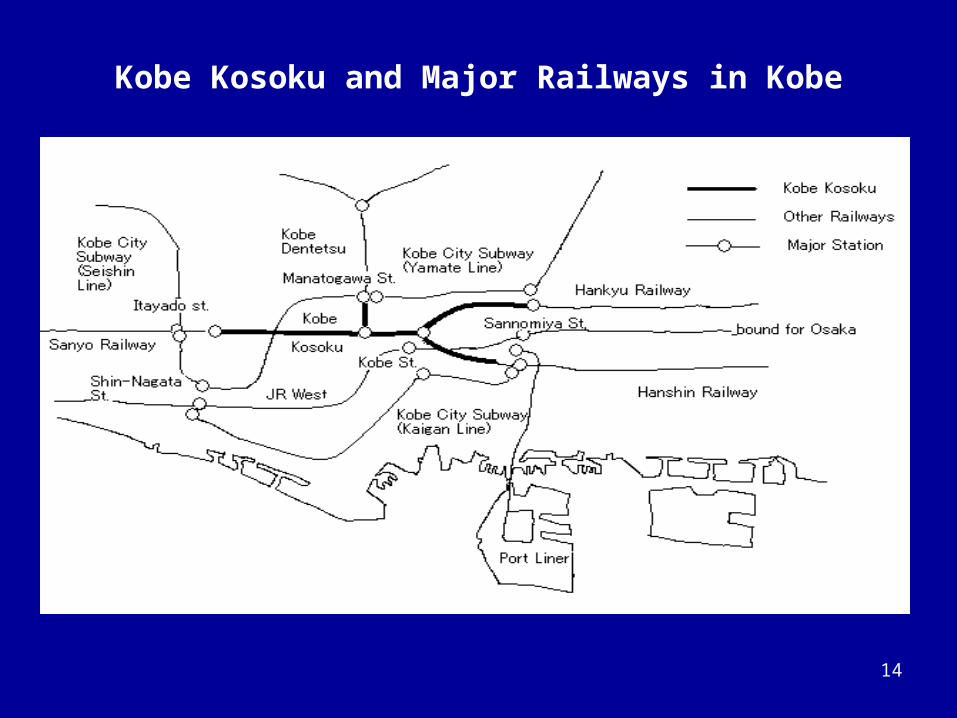

Kobe Kosoku and Major Railways in Kobe

15

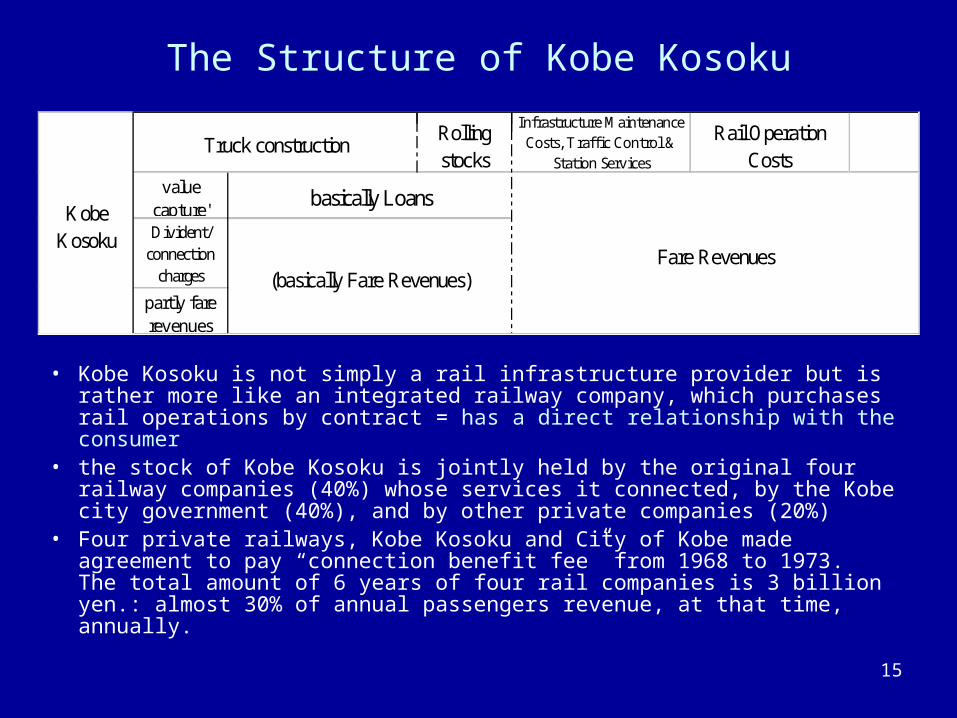

The Structure of Kobe Kosoku

• Kobe Kosoku is not simply a rail infrastructure provider but is rather more like an integrated railway company, which purchases rail operations by contract = has a direct relationship with the consumer

• the stock of Kobe Kosoku is jointly held by the original four railway companies (40%) whose services it connected, by the Kobe city government (40%), and by other private companies (20%)

• Four private railways, Kobe Kosoku and City of Kobe made agreement to pay “connection benefit fee” from 1968 to 1973. The total amount of 6 years of four rail companies is 3 billion yen.: almost 30% of annual passengers revenue, at that time, annually.

Rollingstocks

Rail OperationCosts

valuecapture'Divident/

connectioncharges

partly farerevenues

KobeKosoku

Truck constructionInfrastructure Maintenance

Costs, Traffic Control &Station Services

Fare Revenues

basically Loans

(basically Fare Revenues)

16

Nishiosaka extension line & Nakanoshima new line

• Private Rail Company benefit indirectly from subsidization – Extension plans of existing private railway line (in Osaka area)

• Establish the infrastructure company– The stock is jointly held by the private rail company (about

33.35%), which will become Class 2 operator, by the Osaka city government (33.33%), by the Osaka prefecture government (16.67%), and by other private companies (about 16.65%)

• stock is jointly held by the public and the private equally• the biggest share owned by the private railway company

– this public-private mixed company gets full subsidy as public underground (municipal)

– The costs of related investments on existing section, procurements of new rolling stocks and other related expenses are not included in the total truck construction costs

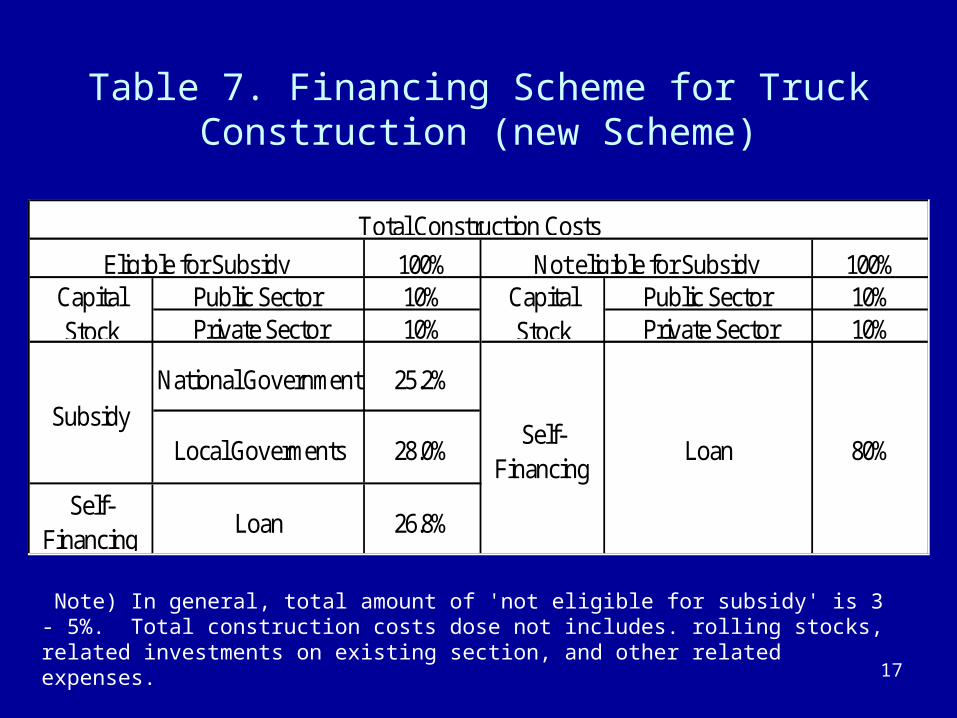

17

Table 7. Financing Scheme for Truck Construction (new Scheme)

100% 100%Public Sector 10% Public Sector 10%Private Sector 10% Private Sector 10%

National Government 25.2%

Local Goverments 28.0%

Self-Financing

Loan 26.8%

Total Construction Costs

CapitalStock

CapitalStock

Eligible for Subsidy Not eligible for Subsidy

SubsidySelf-

FinancingLoan 80%

Note) In general, total amount of 'not eligible for subsidy' is 3 - 5%. Total construction costs dose not includes. rolling stocks, related investments on existing section, and other related expenses.

18

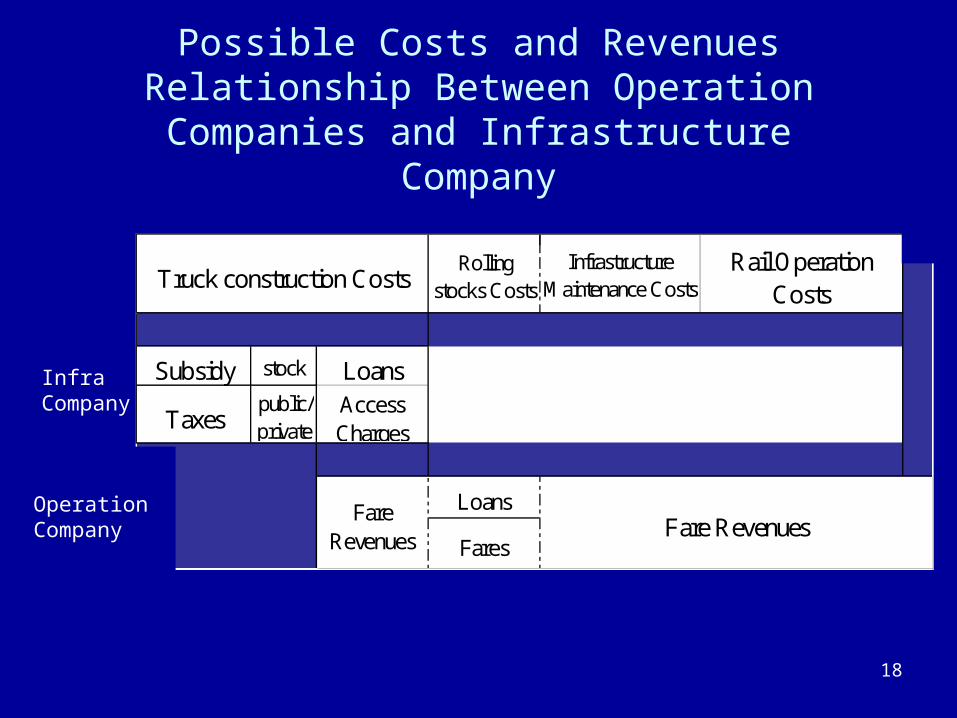

Possible Costs and Revenues Relationship Between Operation Companies and Infrastructure Company

Rollingstocks Costs

Subsidy stock Loans

Taxespublic/private

AccessCharges

Loans

Fares

FareRevenues

Fare Revenues

Truck construction CostsInfrastructure

Maintenance CostsRail Operation

Costs

Operation Company

Infra Company

19

Points or Keywords from Our Experiences• Private Railways in general

– have full responsibility for their decisions regarding networks, operating patterns, schedules and fares. In short, they are autonomous commercial entities.

– they can allow having a long-term commitment to the community it serves

– ‘self-supporting’ principle • few changes in the rules of the games• few political intervention

• Private railways have achieved a high social status by offering not only impeccable transport services but also by diversifying and bringing forth quality services in their region. – the highly reliable, punctual and comfortable rail services

without tax burden

20

Points or Keywords from Our Experiences• Kobe Kosoku Case

– to avoid the conflict between operators and infrastructure, shares are held by operation companies so that the opinions of operation companies are reflected in railway decisions, and most involved usually behave with mutual benefits in mind

– shares the revenue risk with operation companies • more like an integrated railway company, which purchases rail

operations by contract• unlike a typical infrastructure company, which charges

infrastructure fees regardless of the conditions of fare revenues – But

• besides specializing in maintaining infrastructure, maintenance cost is no different from the costs of integrated systems

• might be lack of ability to make large investments • (still) transaction costs

21

Points or Keywords from Our Experiences• Under New Scheme (for Hanshin and Keihan)

– underground construction subsidy programme is applicableabout 50% (or 60%) of truck construction costs which pre-

determined by the Ministry with local governments and private operators

– public sector involve in funding the construction phase and the construction

– establish infrastructure company just for construction• stock is jointly held by the public sector and the private sector

equally, the biggest share owned by the private railway company

• thus, private operator have last to say for the projects

• minimize the transaction costs

22

A Few Final Words• Essential keywords ?

– autonomy, entrust, mutual benefits, long time commitment, and the ‘self-supporting’ principle

• still OUR Problems– to subsidy other capital investment

• need to to integrate rather fragmental national subsidy programmes• Transfer the powers and responsibility to local governments ?

– We have experiences that the local government construct and/or adopt the plan to extend their own underground lines instead of utilising the existing private railway lines

– to subsidy operation costs ?though most Japanese still tend to think un-remunerative services might

mean that the community dose not support • Fare compensation issues• Fare levels which meet social goals

23

THANK YOU !!