Embed Size (px)

Citation preview

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

1

• Business concepts: using credit cards, annual interest rate, finance charges, cost of credit• Mathematics concepts: percentage, algebraic formulas, iterative formulas.• This lesson addresses the various options and consequences in paying a revolving credit card bill.• Debit cards are rapidly growing in popularity. While this lesson won’t discuss debit cards, you should be prepared to discuss the main differences between credit cards and debit cards. A credit card is like having an instant loan that you agree to pay back in a few weeks to a few months. The price of this luxury is a high interest rate—unless you pay back the full balance each month. On the other hand a debit card is essentially an ATM card, except instead of dispensing cash from your bank account on demand, it simply transfers the funds from your account straight to the merchant’s account. Like an ATM card, if you don’t have the funds in your account, you cannot complete the transaction (or the purchase). This facet makes it somewhat more attractive to youthful users: it protects them from running up a large debt. More mature users, who may be better managers of their finances, typically find credit cards more useful.• Disclaimer: The credit card number shown in the graphic is simply a group of randomly selected digits.

2

• There are many other fees and details we could list here, but these will suffice for this one lesson. We’ll address some of the finer details (e.g., monthly interest rate), later in the lesson.• Sandy’s contract actually specifies an APR of 20.99%. (Every credit contract we’ve seen employs the “nn.99%” marketing technique.)• Although this lesson is not meant to be a “how-to” on such things, before opening a new credit card account, one should always consider the “fine print”: the annual percentage rate; grace period allowed to pay the full balance without being charged interest; annual fees, if any; the method for calculating finance charges; transaction charges, if any, for such things as balance

Page 1

Credit Card Payments March 2018

SLIDE • TEACHER NOTEStransfers, late payments, cash advances, going over your credit limit, etc.; and if offered, any bonus or “cashback” offers.

3

• For the sake of simplicity (in this first discussion), we’ve assumed that there are no cash advances or balance transfers involved here. • It really does not matter how Sandy accumulated the $869.43 worth of charges since we’re considering this the first month of usage. In the slides that follow, however, we will see how timing and amounts charged have consequences in months where finance charges are being accrued.• Ask students: How many of you have a credit card? When you get a credit card bill, what are the options for paying? In this lesson we’ll examine three options: pay the full amount, pay a portion of the full amount, and pay the minimum amount. Try to get students to volunteer some form of these three options. We’ll not seriously consider the “pay nothing” option, as that would usually (but not always) place the cardholder in violation of the cardholder agreement, with generally serious ramifications.• Many of your students will probably consider paying only part of the bill…that’s what a credit card is all about, right? (NO!) Hopefully, in this lesson we will show them how poor of a choice (financially) it is to pay anything less than the full amount.

4

• There is no “correct answer” to this question. It will be illuminating to see how your class responds. However, there are some answers that we can consider incorrect, or at least very ill-advised. Paying nothing (D) is generally a violation of the credit agreement at worst, and a sure way to incur finance charges at best. Calling the credit card company to cancel the account (E) is not a realistic option if Sandy really needs a credit account, and she will still need to pay the balance due. So choices A, B, and C all merit some discussion…

Page 2

Majestic Bank SuperCard, Inc. P.O. Box 75290 Dollar, TX 75298-5290

Account: 0521 8503 7431 4163

Sandy Spender 3657 Oleo Lane Crisco, MD 20562

Account Summary Transactions Summary Credit Limit $5,000.00 Statement Date March 31, 20XX Acct No. 0521 8503 7431 4163 Days in Billing Period 30

Previous Balance $ 0.00 Credits – $ 0.00 Purchases + $ 869.43 Finance Charges + $ 0.00 Cash Advances + $ 0.00 Fees + $ 0.00 Transactions Total = $ 869.43

Amount Due $ 869.43

Due Date April 20, 20XX Minimum Payment $10.00

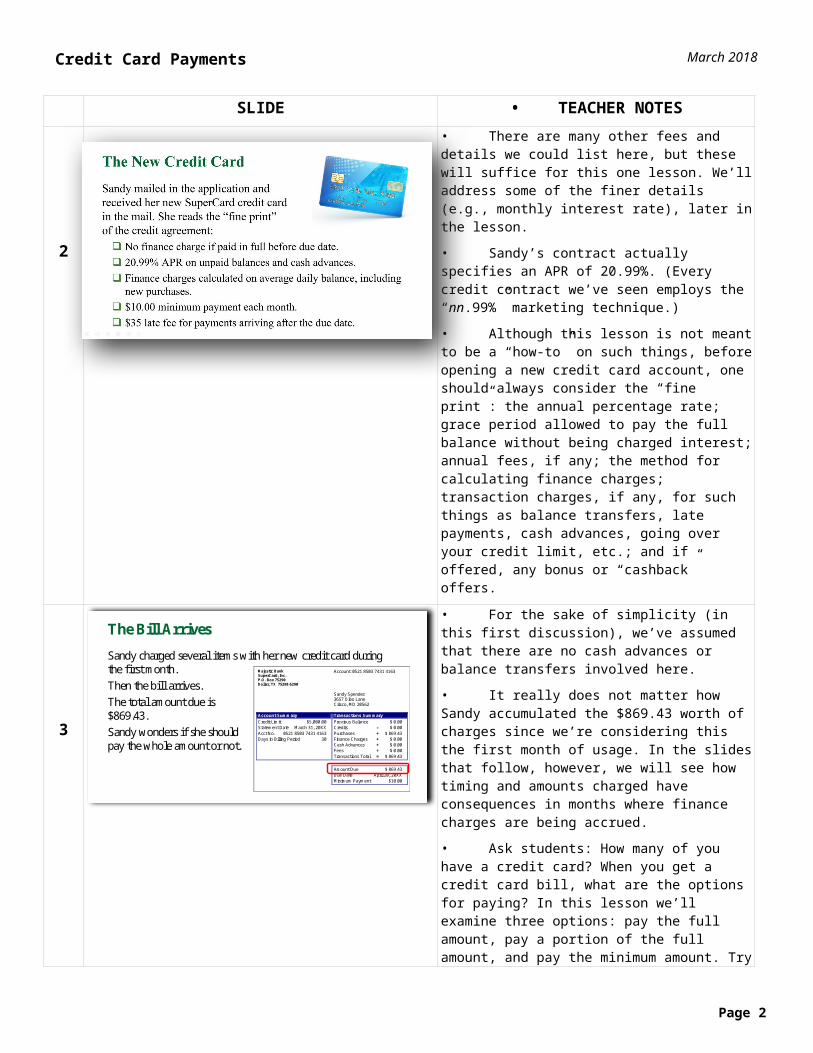

The Bill Arrives

Sandy charged several items with her new credit card during the first month. Then the bill arrives.The total amount due is $869.43.Sandy wonders if she should pay the whole amount or not.

Question 1

What’s the best way to respond to a large credit card bill like Sandy’s?A. Use your savings to pay the full balance before the due date.B. Pay about half the balance before the due date; pay the rest next

month.C. Pay the minimum balance before the due date.D. Pay nothing this month; wait until next month.E. Call the credit card company to cancel the account.

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

5

• As stated on the previous slide’s notes, there is no right answer to the CPS question. In the slides that follow we will examine the three choices which involve making a payment of some amount. The question thus becomes: “How much should Sandy pay?”

6

• The correct answer is A.• Of course, we assume that Sandy has enough in her checking account to cover the check.

7

• Most will automatically agree that paying the balance in full is the best thing to do, if possible. As stated, this action incurs no additional costs.• Some students may wish to argue that it is smarter to pay only a portion of the bill so that their savings (or checking account balance) is not depleted. Of course, as we’ll show in the coming slides, generally speaking, that is not a wise decision.• Paying the balance in full is very similar to using a debit card. Some arguable advantages for using a credit card (over a debit card) might be: the ability to make a purchase “before payday,” the flexibility to make an emergency purchase (treating the card account as an emergency loan), and cash-back or other bonus offers that are available with many credit cards. An advantage of the debit card, particularly for consumers that have a hard time controlling their debts, is that “if you don’t have it, you can’t spend it.”

Page 3

Sandy Must Pay!

There really is no “right” answer, but…“Paying nothing” (D) would be a violation of the credit agreement.“Canceling the account” (E) doesn’t change the fact that she must still pay the balance.So, since Sandy must pay for her purchases, she really has three possible choices (A, B, or C):

Option A: Pay the balance in full. Option B: Make a partial payment of the balance. Option C: Pay the minimum amount of $10.

Question 2

Suppose Sandy writes a check for the full balance $869.43. She mails the payment before the due date. Which of the following is true?A. She incurs no additional charges or fees.B. She owes an additional $15.22 for finance charge.C. She owes an additional $21 monthly usage fee.D. She will receive a $10 refund, since she paid before the due date.E. She will be charged an additional $10 fee, since she paid before

the due date.

How to Avoid Finance Charges

A. She incurs no additional charges or fees.The best thing is to pay the full balance every month.For most credit cards, this costs the user no additional interest or fees.It encourages the user to “live within one’s means.”Makes the credit card better than a “debit card” in many respects.

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

8

• It is important to respect the “grace period” (if it exists) on a new credit card account. Most credit accounts DO include a grace period, as described on this slide. The grace period implies that the credit card issuer is effectively willing to loan you the amounts of the charge interest free for a period of time (prior to the due date). The significance of an “interest-free loan” cannot be overstated in today’s financial world!• The significance of the grace period however becomes even more apparent when a payment is NOT received by the due date. In many cases, the credit card issuer will begin assessing finance charges on the charges—from the date of the purchase! (This is the virtual effect of the card issuer calculating an average daily balance.)

9

• The correct answer is D.• There is, of course, any number of reasons for not paying the full amount. Some are frivolous and others are necessary.

10

• Be absolutely certain that every student in your class appreciates the fact that the credit card company WILL assess a finance charge if they fail to pay the full balance by the due date. This is the credit card company’s means of charging the credit card user (or the business) for the use of their money (i.e., the credit). While many card agreements still offer a grace period (during which no finance charges accrue), that luxury vanishes as soon as the user fails to pay the full balance by the due date. • We assume that the card agreement includes a grace period. We also imply that there will be no finance charge if the balance is paid in full. However, a recent trend among credit card companies is to compute the balance for purchases on the two-month average daily balance. With this technique, the credit card company retroactively eliminates the grace period. The finance

Page 4

Option A: Pay in Full

In most cases, the “fine print” will reveal: A grace period: the time you make a charge until the payment

due date. Pay the full balance within the grace period, and incur no finance

charges. When paid in full, the starting balance for the following month

will be zero.The consequences next month will be:

New balance = sum of the new purchases. Grace period begins anew

Question 3

Suppose Sandy determines that she can not pay the full amount. So, she makes a partial payment: paying $400 of this month’s bill before the due date. Which of the following is true?A. Sandy will surely pay the rest of the bill next month.B. Sandy will come out ahead, earning interest on the money in her

savings account. C. If Sandy fails to pay the full amount on the bill, the credit card

company will close the account immediately.D. Next month’s bill will include finance charges.

How to Incur Finance Charges

D. Next month’s bill will include finance charges.When Sandy does not pay the full amount, it is like being granted an “instant loan.”NOTE: The credit card company WILL assess finance charges on that loan!The finance charge is the cost to Sandy for the “instant loan.”

Credit Card Payments March 2018

SLIDE • TEACHER NOTEScharge is based on the sum of the average daily balances for both the previous month (when you may very well have made a full payment) AND the current month! Yikes!

11

• It’s not especially important at this point in the lesson, but we include the fact that the payment is received on Day 2 of the billing cycle, and payments are made on certain days, because these will be important factors in the calculation of finance charges to come.• Realistically, it would be essentially impossible for the bank to receive Sandy’s payment on Day 2 of the billing cycle, because it was probably nearly Day 7 of the billing cycle before Sandy even received the bill in the mail, and it would take a few more days for the bank to actually receive her payment. Thus a more typical scenario would be that Sandy would make several purchases in the next billing period before the bank actually receives her payment. When paying the full amount before the due date, this doesn’t matter. However, if Sandy pays less than the full amount, the transaction dates become significant. Nevertheless, for the sake of simplicity, we will stick with a prompt payment scenario, as given in the slide here.• Credit card users will typically make many small charges and a few large charges. We have chosen to show Sandy making only a few charges to keep the calculations and the slides in this lesson simpler.• One use of credit cards that is growing in popularity is the ability to make online purchases.

12

• The correct answer is D.• Students are expected to be able to add and subtract the values given on this slide, and realize that the actual bill will be for MORE than just the new charges and outstanding balance—it will also include finance charges. The actual amount depends on the days on which activity occurs, as stated on the previous slide’s notes. We’ll address “how,” in the slides to come.

Page 5

Option B: Partial Payment

Alright, then. Sandy makes a partial payment of $400 towards her bill of $869.43. The bank receives the payment on Day 2 of the billing cycle. On Day 4 Sandy makes a purchase of $247.58.On Day 7, $155.71.On Day 16, $20.00.On Day 26, $51.65.

Question 4

The bank receives Sandy’s $400 payment toward her $869.43 bill. Next month, Sandy makes new purchases of $247.58, $155.71, $20.00, and $51.65. What will the bank bill Sandy for this next month?A. Less than $400B. About $475C. About $944D. About $959E. About $1344

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

13

• The most important fact for students to get from this slide is that Sandy will have finance charges added to her bill. Most students should appreciate that Sandy will still owe for the charges made and for the unpaid balance, but many will not realize that she must also pay finance charges.• Students may use the word “interest” interchangeably with “finance charges.” Here we will use the convention that interest is something earned (a benefit for the consumer), and a “finance charge” is something paid (a cost to the consumer). Of course, from the perspective of the card issuer (usually a bank), the relative value of each is exactly the opposite.• In the slides that follow we’ll address how the finance charges are calculated.

14

• There is a lot of information shown on the disclosure, but we’re going to focus on just two important items: the annual percentage rate (or APR) and the method of computing the balances for calculating the finance charges due on each month’s bill. There are other ways to incur finance charges (balance transfers and cash advances, for example), but we have chosen to not include any examples of those types here to make the calculations simpler for this first examination. • The slides that follow will address calculating the “average daily balance.” • Most people may think that all credit card agreements specify the same “method of computing the balance for purchases,” but this is not so. The most common one (currently) is the “average daily balance over one billing cycle, including new purchases” that we’ll explore in this lesson.• Other methods that might be used include:

• The “adjusted balance” method, which essentially excludes new purchases and allows you to make payments throughout the billing cycle• The “previous balance” method, which uses only the balance at the end of the previous statement. New purchases are not included.• A recent trend is a “Two-cycle average daily balance method.” This method

Page 6

Majestic Bank SuperCard, Inc. P.O. Box 75290 Dollar, TX 75298-5290

Account: 0521 8503 7431 4163

Sandy Spender 3657 Oleo Lane Crisco, MD 20562

Account Summary Transactions Summary Credit Limit $5,000.00 Statement Date April 30, 20XX Acct No. 0521 8503 7431 4163 Days in Billing Period 30

Previous Balance $ 869.43 Credits – $ 400.00 Purchases + $ 474.94 Finance Charges + $ 14.85 Cash Advances + $ 0.00 Fees + $ 0.00 Transactions Total = $ 959.22

Amount Due $ 959.22

Due Date May 20, 20XX Minimum Payment $10.00

The Credit Card Statement

D. About $959The new bill arrives!

The balance from the previous bill. Sandy’s payment of $400. New purchases totaling $474.94. A finance charge of $14.85. And the new balance.

Let’s see how the credit card company calculates the finance charges…

SUPERCARD CREDIT DISCLOSURE Annual percentage rate (APR) for purchases 20.99%

Other APRs Balance transfer APR: 18.99%. Cash advance APR: 23.99%. Default rate APR: 20.99% See explanation below.*

Variable rate information Your APRs may vary, depending on the U.S. Prime Rate. For purchases, 16.99% plus U.S. Prime Rate. For cash advances, 19.99% plus U.S. Prime Rate, but never less than 23.99%. The default rate can be as high as 20.99% plus the U.S. Prime Rate.

Grace period for repayment of balances for purchases

Not less than 20 days, if you pay your total new balance in full each billing period by the due date.

Method of computing the balance for purchases

Average daily balance (including new purchases)

Annual fees Annual Membership Fee: None Minimum finance charge $1.00 Cash Advance Fee 3% of the amount of each cash advance,

but not less than $5 Balance Transfer Fee 3% of the amount of each balance transfer, but not

less than $5 or more than $60. Late Fee $15 on balances up to $100; $25 on balances of $100

up to $1000; and $45 on balances of $1000 and above.

Calculating Finance Charges

The credit card agreement gives the important details (among other things):

Annual percentage rate (APR) for purchases: 20.99%

Method of computing the balance for purchases: Average daily balance (including new purchases)

Credit Card Payments March 2018

SLIDE • TEACHER NOTESsqueezes even more out of the customer, as it penalizes the user with at least two-months’ worth of finance charges if they fail to pay the full amount due on one month.• In rare cases, the agreement might specify that new purchases are excluded from the calculation.• Some agreements specify a minimum finance charge. For example, if your calculated finance charge for a month is $0.45, the company may charge you the minimum of $1.00.

15

• Spend a moment ensuring students understand the “formula” for the “new balance”—what we owe this month.

• We start with the balance from the last month’s statement.• If we made any payments (recall that Sandy paid $400), then we will reduce the amount we owe this month by that payment amount. If we happened to have paid the whole amount owed, then at this point in our formula, the total would be zero, right?• If we made any new purchases during this billing cycle, then we would have to add that total amount to what we owe.• And lastly, if the credit card company assessed any finance charges, that amount would also be added to what we owe.

• See if students recognize the formula for the finance charge. They should see that it is essentially the same as the familiar interest equation: Interest = Principal Rate Time.• To keep this first treatise simple, we’ve purposely excluded cash advances, balance transfers, and other adjustments and fees that would impact the new balance, if included. • Most monthly credit card statements present an equation exactly like the one shown on this slide to summarize the calculation of the new balance (and include cash advances, balance transfers, and other fees and account activities).• Students may wonder what is meant by the “average daily balance.” Good! We’re going to spend quite a bit of time on that concept in the slides to come, starting with a

Page 7

Calculating Finance ChargesThe Transaction Total is really the amount due next month:

Transaction Total = Previous balance– Payments

+ New purchases+ Finance charge

Finance charge is calculated using a formula very similar to the familiar interest formula:

Finance Charge = Average daily balanceInterest rate

Time period

Credit Card Payments March 2018

SLIDE • TEACHER NOTESCPS question on the next slide…

16

• The correct answer is B.• Here students will either know or guess what is meant by the “average daily balance.”• In this lesson we’ll address the most common method used by credit card companies today to calculate the finance charge due: the average daily balance method (including new purchases).

17

• Be sure students understand what we’re portraying here. We’re using a 30-day calendar to represent how the daily balances for a typical month might appear. Payments will reduce the daily balance (as occurs on Day 2); new purchases will increase the daily balances (see Days 4, 7, 16, and 26). Help students understand that the daily balance is the up-to-date amount owed each day. That amount may remain unchanged for several days (see days 8 through 15, for example) if there is no activity with the account. From a previous slide we recall: On Day 4 she makes a purchase of $247.58, so the daily balance increases from 469.43 to 717.01. Similarly on Day 7 she makes purchases totaling $155.71; on Day 16, $20.00; and on Day 26, $51.65. These dates are denoted with red values.• The billing cycle month for most credit cards will not run from the first of the month to the last day of the month, but, for example, from the 9th of this month to the 9th of the next month, or the 22nd to the 22nd. Thus, we’re admittedly showing a simplified case, but the principle is the same.• Note that the first day of the billing cycle (i.e., month) starts out with a non-zero balance because Sandy owed for purchases made the previous month. Ask students, “If Sandy’s bill was $869.43 and she makes a payment of $400 (received by the bank on Day 2 of the billing cycle), what will she still owe? (or, “What is her balance at the end of Day 2?)” Answer: “$469.43,” that is, $869.43 – $400.00 = $4469.43. Point to Day 2 on the calendar graphic. From that point on, her “daily balance” will be $469.43—until additional activity (payments, charges, cash

Page 8

Question 5

What is meant by a credit account’s “average daily balance”?A. Sum of each day’s charges divided by the number of days

in the monthB. Sum of each day’s balance divided by the number of days

in the month C. The average cost of each day’s purchase made

during a given month.D. Your average checking account balance for the month.

The Average Daily Balance

B. The “average daily balance” for a credit account is the sum of each day’s balance divided by the number of days in the month.Let’s see how that works. Sandy’s $400 payment is received on Day 2. Here are the daily balances for the rest of the month.

Su Mo Tu We Th Fr Sa1

869.432

469.433

469.434

717.015

717.016

717.017

872.728

872.729

872.7210

872.7211

872.7212

872.7213

872.7214

872.7215

872.7216

892.7217

892.7218

892.7219

892.7220

892.7221

892.7222

892.7223

892.7224

892.7225

892.7226

944.3727

944.3728

944.3729

944.3730

944.37

PaymentPurchases

Credit Card Payments March 2018

SLIDE • TEACHER NOTESadvances, or balance transfers) occurs in the account—as it does on Day 4.• For your own edification (probably too detailed for students), it’s also interesting to note that the Day 1 balance (for the purpose of calculating the average daily balance, as we’ll soon see) is the full amount owed because 1) a full payment was not received during the grace period, and 2) the payment was not (and usually is not) received on Day 1 of the new billing cycle. Thus, for example, if Sandy makes anything less than a full payment on Day X, the daily balances for Day 1 through Day X will all include the previous month’s balance of $869.43, plus any new purchases! This greatly inflates the average daily balance, and consequently the finance charge incurred! (Good for the bank; bad for you!) On the other hand, if Sandy were to make a full payment of the previous month’s balance before the due date, the daily balance for Day 1 through Day X would not include the $869.43 (thanks to the grace period). In fact, in that case the average daily balance would effectively remain at zero for the whole month!

18

• From a previous slide we recall: On Day 4 she makes a purchase of $247.58. On Day 7, $155.71. On Day 16, $20.00. On Day 26, $51.65. See the red values on the calendar.• Answer to the question: The balance each day increases by an amount equal to the amount of the new purchase (for example, Day 4). • Point out that the daily balance after a purchase (e.g., Day 17 through 25) remains the same until another new purchase is made (e.g., Day 26).

19

• Ask students, “How do we calculate the average? For example, if I wanted to find the average student age in this classroom…” Answer: Add up all the values and divide by the number of values. • Suggestion for teaching “average”: Make a list of the ages of students sitting in the first row (or all the male students in the class, or a similar group) on the board (they can call out their ages as you write), have everyone add up the values and agree on a sum, agree on the number of student ages in the list, and then have everyone calculate

Page 9

Sandy’s Daily Balances

Each day has a balance: an amount that Sandy owes to the credit card company. What happens to the balance on the days Sandy makes a purchase?

Su Mo Tu We Th Fr Sa1

869.432

469.433

469.434

717.015

717.016

717.017

872.728

872.729

872.7210

872.7211

872.7212

872.7213

872.7214

872.7215

872.7216

892.7217

892.7218

892.7219

892.7220

892.7221

892.7222

892.7223

892.7224

892.7225

892.7226

944.3727

944.3728

944.3729

944.3730

944.37

Purchases increase the balance

Calculating Average Daily Balance

The “average daily balance” is the sum of all these balances divided by the number of days.

$25,462.85 (rounded)30 $848.76

Sum of daily balancesAverage Daily BalanceNumber of days

MORE PRACTICE

Su Mo Tu We Th Fr Sa1

869.432

469.433

469.434

717.015

717.016

717.017

872.728

872.729

872.7210

872.7211

872.7212

872.7213

872.7214

872.7215

872.7216

892.7217

892.7218

892.7219

892.7220

892.7221

892.7222

892.7223

892.7224

892.7225

892.7226

944.3727

944.3728

944.3729

944.3730

944.37

Credit Card Payments March 2018

SLIDE • TEACHER NOTESthe average age. Compare this calculation to the formula given on this slide.• So, be sure everyone sees how the formula for “Average Daily Balance” is simply adding up the balance values for each day of the month (the billing cycle) and dividing by the number of values (or days in the billing cycle). Note that the balance for each day is part of the sum—even when the balance remains unchanged from the previous day (due to no additional purchases on that day).• If students are still confused, you can have them actually add the daily balances to confirm the sum shown in the numerator of the equation on the slide ($25,462.85). There are at least two ways to perform the calculation. The brute force way is to enter all thirty daily balances into the calculator to obtain the sum, and then divide by 30. A more efficient way is to recognize a “frequency distribution” in the chart: the value 869.43 occurs once, 469.43 occurs 2 times, 717.01 occurs 3 times, 872.72 occurs 9 times, 892.72 occurs 10 times, and 944.37 occurs 5 times. So the sum of daily balances can be calculated as:

Sum = 869.43 + (469.43 2) + (717.01 3) +

(872.72 9) + (892,72 10) + (944.37 5) = 25,462,85

The parentheses are not necessary with calculators that automatically perform multiplication before additions (scientific and financial calculators). Note that most basic four-function calculators do NOT include this feature. Hopefully, you do not allow these kinds of calculators in your classroom.• Click the “More Practice” button for another month (not at all related to the problem at hand).

Page 10

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

20

• This slide is only for extra practice. Don’t let students get confused by the different set of values. These values are NOT related in any way to the problem situation we’ve been examining.• Don’t advance the animation in the slide to reveal the answer (the equation) until everyone has a had a chance to try the calculation for themselves.• There are at least two ways to perform the calculation. The brute force way is to enter all thirty daily balances into the calculator to obtain the sum, and then divide by 30. A more efficient way is to recognize a “frequency distribution” in the chart: the value 386.44 occurs 5 times, 186.44 occurs 2 times, 374.93 occurs 5 times, 878.11 occurs 6 times, 914.24 occurs 9 times, and 980.90 occurs 3 times. So the sum of daily balances can be calculated as:

Sum = (386.44 5) + (186.44 2) + (374.93 5) + (878.11 6) + (914.24 9) + (980.90 3) =

20,646.25The parentheses are not necessary with calculators that automatically perform multiplication before additions (scientific and financial calculators).

21

• The correct answer is C.• This question will help you know whether or not your students appreciate the ramifications of how the finance charges will actually be calculated—especially as it relates to the unpaid balance.

Page 11

Extra PracticeCalculate the “average daily balance” for this month’s daily balances.

$20,646.25 (rounded)30 $688.21

Sum of daily balancesAverage Daily BalanceNumber of days

Su Mo Tu We Th Fr Sa1

386.442

386.443

386.444

386.445

386.446

186.447

186.448

374.939

374.9310

374.9311

374.9312

374.9313

878.1114

878.1115

878.1116

878.1117

878.1118

878.1119

914.2420

914.2421

914.2422

914.2423

914.2424

914.2425

914.2426

914.2427

914.2428

989.9029

989.9030

989.90

Question 6Recall Sandy made a $400 payment toward her balance, so she starts off with a $469.43 unpaid balance. When she makes additional purchases, A. She pays finance charges on the new purchases, but not on the

$469.43 unpaid balance.B. She pays finance charges only on the $469.43—not on the new

charges she makes during the month.C. She pays finance charges on the $469.43, as well as on the new

charges she makes during the month.D. She pays no finance charges since the $400 payment was more

than the minimum required payment.

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

22

• As noted earlier, the credit card issuer sets the rules for how the finance charges will actually be calculated. In this lesson we are using the most prevalent practice (at the time of this writing): that is, 1) the grace period (during which no finance charges accrue) ends when you pay less than the full amount due, and 2) paying the full amount restarts the grace period.

23

• The correct answer is C.• We’re really expecting students to simply guess here, and this will indicate to you how “credit-aware” your students are. However, we will of course show them how to actually calculate the amount in the coming slides.

24

• The correct answer is C.• We all hear about “APR,” the annual percentage rate. However, since we are getting monthly bills, and being charged monthly interest, we must use a monthly percentage rate. The monthly rate is simply 1/12 of the annual rate, but we don’t want to explain it away so flippantly, because handling it properly (mathematically speaking) here will empower us to solve more difficult problems later with relative ease. Hence, we introduce the unit ratio in the next slide.

Page 12

The Effect of New Purchases

C. She pays finance charges on the $469.43, as well as on the new charges she makes during the month.Anytime Sandy fails to pay the entire balance given on the monthly statement, finance charges will begin to accrue.In effect, Sandy pays finance charges on the unpaid balance for the whole month—even if she makes no additional purchases.Another way to say this: The grace period ends whenever Sandy pays less than the full amount due.

Question 7

How much finance charge would you guess that Sandy will pay this month on an average daily balance of $848.76? (Hint: The finance charge is 20.99% APR on the average daily balance.)A. About $1B. About $5C. About $15D. About $50E. About $100

Calculating the Finance Charge

C. About $15Let’s see how the bank calculates that. Recall the formula:

Sandy’s “principal” is her average daily balance, or $848.76, and the “time” is 1 month.But the “rate” is 20.99% APR—that is, annual percentage rate. We must convert this to a monthly rate (since our “time” is in months).

Interest Principal Rate Time

(for one month)

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

25

• Notice that we write the APR 20.99% as “20.99% per year,” or 20.99%yr.• In this example we change the units of the interest rate from “% per year” to “% per month.”• In other lessons we have developed the idea of the unit ratio. If your students did not see those lessons, we present the concept here.

• Students should be familiar with the idea that “multiplying by 1” yields the same number. That’s the identity property of multiplication. The “unit ratio” makes use of that principle: forming a ratio of two equal quantities (i.e., 1 year equals 12 months) will result in a quantity equal to “1.” Multiplying by that ratio then yields the “same number,” but since we include the units (HINT: ALWAYS include the units in your formulas!), we are able to change the result from “% per year” to “% per month,” as desired…see next slide.• Notice that we have two unit ratios…and technically we could use either one. But we chose the first because it would “conveniently” cancel the units of years and leave us with units of “per month.” Anytime we use unit ratios, we select the ratio with just such an end result in mind. With experience, it becomes easier to know which unit ratio to use.• Notice that we “cancel” the units of “yr” because they appear in both the numerator and denominator. That is, we know that yryr = 1, and “1” is the identity element for multiplication (as discussed in the above note).• You can remind students that the correct procedure for multiplying fractions is to find the numerator of the answer by multiplying all the numerators of all the factors, and find the denominator by multiplying all the denominators of all the factors.

Page 13

Using a Unit Ratio

Convert the annual rate to a monthly rate by multiplying by a unit ratio.A unit ratio is a ratio formed by two equivalent quantities, like this:

Multiply the rate by the unit ratio. The result is we “change the units.”

1 yr 12 m 1 year o12 mo 1 = 12 months yr orUnit Ratio:

20.99% 1 yryr 12 moRate (rounded)20.99% 1.75% p er m o12 mo

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

26

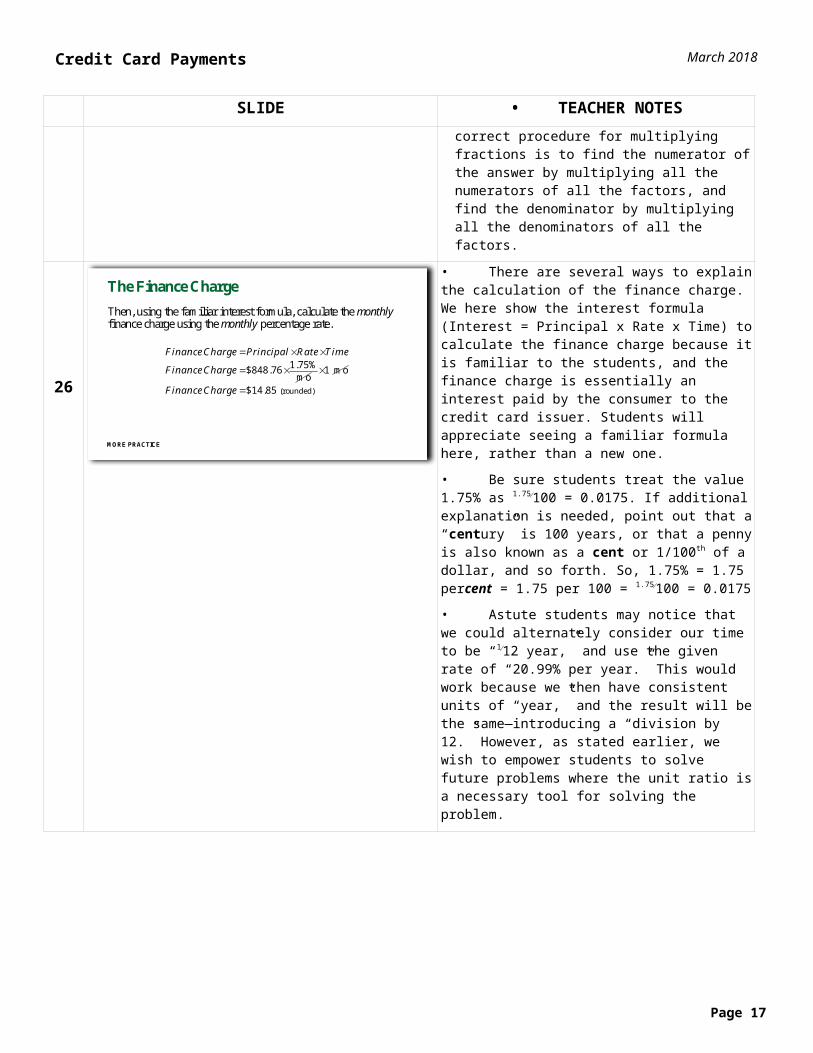

• There are several ways to explain the calculation of the finance charge. We here show the interest formula (Interest = Principal x Rate x Time) to calculate the finance charge because it is familiar to the students, and the finance charge is essentially an interest paid by the consumer to the credit card issuer. Students will appreciate seeing a familiar formula here, rather than a new one.• Be sure students treat the value 1.75% as 1.75100 = 0.0175. If additional explanation is needed, point out that a “century” is 100 years, or that a penny is also known as a cent or 1/100th of a dollar, and so forth. So, 1.75% = 1.75 percent = 1.75 per 100 = 1.75100 = 0.0175• Astute students may notice that we could alternately consider our time to be “112 year,” and use the given rate of “20.99% per year.” This would work because we then have consistent units of “year,” and the result will be the same—introducing a “division by 12.” However, as stated earlier, we wish to empower students to solve future problems where the unit ratio is a necessary tool for solving the problem.

27

• This is the first of two extra practice problems.• This is essentially the same as Sandy’s problem, but using a different average daily balance. In the answer, notice that we’ve multiplied the APR by the unit ratio within the parentheses, canceling the units of “yr” and also the units of “mo.”• Again, be sure students treat the value 20.99% as 20.99100 = 0.2099.

Page 14

The Finance ChargeThen, using the familiar interest formula, calculate the monthlyfinance charge using the monthly percentage rate.

1.75%$848.76 mo

FinanceCharge Principal Rate Time

FinanceCharge 1 mo (rounded)$14.85 FinanceCharge

MORE PRACTICE

Extra Practice

With an APR of 20.99%, what is the finance charge for an average daily balance of $777.41?Answer:

20.99%$777.41 yr

FinanceCharge Principal Rate Time

FinanceCharge 1 yr

12 mo

1 mo

$13.60 (rounded)

MORE PRACTICE BACK TO LESSON

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

28

• For this second extra practice problem, we have a different average daily balance and a different annual percentage rate.• Again, within the parentheses we multiply by a unit ratio to obtain a monthly percentage, which matches the unit of time “1 month.”• Be sure students treat the value 17.99% as 17.99100 = 0.1799.

29

• It is very tempting to accept the offer from the credit card company to make only the minimum payment. Caution students that this is probably the fastest way to get overwhelmed with debt in a very short time.

30

• The correct answer is B.• Some card agreements may, in fact, assess some penalties, but we have not specified anything like that in this lesson, so those choices are not correct—as long as the payment is greater than or equal to the minimum payment and is received before the due date.

31

• We hope students have learned from this lesson that, whenever the bill is not paid in full, finance charges begin to accrue on the very first day of the billing cycle.• Some students may argue that it’s better to keep their money in savings. Aside from the risk of having little or no savings, on the basis of interest in the savings versus finance charge on the debt, it is fairly easy to show that it is better to pay off the debt than keep the savings. The interest rates used by credit card companies will almost always be substantially greater than the interest earned

Page 15

Extra Practice

With an APR of 17.99%, what is the finance charge for an average daily balance of $1164.73?Answer:

17.99%$1164.73 yr

FinanceCharge Principal Rate Time

FinanceCharge 1 yr

12 mo

1 mo

(rounded)$17.46

Option C: Minimum PaymentSuppose Sandy is really short on cash this month.The smallest amount she is allowed to pay is known as the minimum payment.On her monthly credit card statement, she reads that the minimum amount she must pay is $10.

Majestic Bank SuperCard, Inc. P.O. Box 75290 Dollar, TX 75298-5290

Account: 0521 8503 7431 4163

Sandy Spender 3657 Oleo Lane Crisco, MD 20562

Account Summary Transactions Summary Credit Limit $5,000.00 Statement Date April 30, 20XX Acct No. 0521 8503 7431 4163 Days in Billing Period 30

Previous Balance $ 869.43 Credits – $ 400.00 Purchases + $ 474.94 Finance Charges + $ 14.85 Cash Advances + $ 0.00 Fees + $ 0.00 Transactions Total = $ 959.22

Amount Due $ 959.22

Due Date May 20, 20XX Minimum Payment $10.00

Question 8

What will be the consequence if Sandy pays only $10 towards the credit card bill of $869.43?A. Sandy will be charged a 10% penalty for paying less than $869.43.B. Sandy will begin to accrue finance charges.C. Sandy will be charged a $10 penalty for paying only the minimum

payment.D. Sandy will earn more interest by keeping her money in her savings

account, rather than withdrawing it to pay her bill.

The Cost of Paying the Minimum

B. Sandy will begin to accrue finance charges.As long as Sandy makes a payment that is greater than or equal to the minimum payment before the due date there will be no additional penalties.A payment of $10 simply reduces the balance from $869.43 to $859.43 (on the day the bank receives the payment).As in the case of a partial payment, finance charges begin to accrue, and the “grace period” ends.

Credit Card Payments March 2018

SLIDE • TEACHER NOTESin even the most robust savings account. Thus, it will always be better to pay off the credit card debts to avoid finance charges. If students challenge you on this, a simple example should be sufficient. Ask what sort of interest rate they are able to earn on a savings account? Answer: 3% APR (would be a very attractive rate at the time of this writing). So the interest earned on $859 would be 3%/12 $859.43 = $2.15, compared to the finance charges on that same $859.43 = 21%/12 $859 = $15.04, Thus, if you chose to keep that money in savings rather than pay off the credit card debt. it would cost you $12.89 (that is, $15.04 – $2.15 = $12.89) each month.

32

• The correct answer is A.• As just stated on the previous slide, the calculations of the average daily balance begin with the balance on Day 1 = $869.43 because the bank has not yet received payment.• Note that “Day 1” refers to the first day of the billing cycle, not the first day of the month. Also, students should be aware that as we calculate average daily balance in the coming slides, the date (in the billing cycle) that the payment is received is very important.

33

• Help students to understand that when they pay only a portion of the total bill (especially when they make only the minimum payment), the remaining balance is part of the daily balance for every day remaining in the month. In other words, you pay a finance charge on that remaining balance for the whole month. • Sandy will pay interest on the Day 2 balance of $859.43 for the rest of the month (i.e., 29 days). Similarly, she will pay interest on the $247.13 purchase made on Day 4 for the rest of the month (i.e., 27 days). And so on, for each charge made during the month. • It stands to reason that charges made early in the month are more costly than charges made late in the month. You can demonstrate this fact as follows: Using the example presently before students, suppose the Day 4 transaction is the only purchase made all month. Then, the average daily balance can be calculated:

Page 16

Question 9

The bank receives Sandy’s $10 minimum payment on Day 2, and on Day 4 she makes a purchase of $247.13. Which row below gives the daily balances for the first 5 days of this next billing cycle?

Day 1 Day 2 Day 3 Day 4 Day 5

A. 869.43 859.43 859.43 1106.56 1106.56B. 859.43 859.43 859.43 612.30 612.30C. 869.43 10.00 10.00 247.13 247.13D. 10.00 10.00 10.00 257.13 257.13

A Large Daily Balance

A. 869.43 859.43 859.43 1106.56 1106.56The daily balance decreases only slightly on the day when the minimum payment arrives.The new purchase increases the balance on Day 4.The large beginning balance is carried throughout the whole month, and you will pay finance charges on that amount for the whole month!If you make any additional charges during the month, you will pay finance charges on those amounts, too!

Day 1 Day 2 Day 3 Day 4 Day 5

Credit Card Payments March 2018

SLIDE • TEACHER NOTES Avg Daily Bal = (1 day*$869.43 +

2 day*$859.43 + 27 days*$1106.56)/30 days = $1082.18 (rounded)

and soFinance Charge = (20.99%/yr) *

(1 yr/12 mo)*$1082.18 = $18.93 (rounded).Then compare that to a similar month when the $247.13 charge occurs on Day 30:

Avg Daily Bal = (1 day*$869.43 + 28 day*$859.43 + 1 day*$1106.56)/30

days= $868.00 (rounded)

and soFinance Charge = (20.99%/yr) *

(1 yr/12 mo)*$868.00 = $15.18 (rounded).

34

• We specify “Day 1 of every month’s billing cycle” merely to simplify the calculations. It is only a little more cumbersome to choose another day.• Anticipating the next slide, you can help students think through this: For month 1, a payment of $25 will result in a new balance of $869.43 –$25.00 = $844.43. For month 2, a finance charge will be assessed on the average daily balance of $844.43, that is, 21%/12*$844.43 = $14.78 (rounded), and so, the new balance for month 3 will be: Starting balance ($844.43) plus the finance charge ($14.78) minus the payment ($25.00) = new balance of $834.21. And so on, for the successive months.• Done by hand (even with a calculator), this is a tedious but fruitful exercise. A spreadsheet makes this considerably easier, and it is a good application for a spreadsheet, too.

35

• Suggestion: Have students make a table showing the starting balance, the finance charge, the payment, and the resulting balance for each month—at least for the first 12 months.• Point out to students that the finance charge each month costs about $14 or $15 each month during this first year, and so the principal (the outstanding balance) is actually only being reduced by about $5 or $6 each month.

Page 17

Making Small PaymentsMaking small payments, even with no additional purchases:

Can take months or years to pay off the debt. Accumulates a significant amount of finance charge.

Suppose that Sandy simply cut up her credit card, after receiving her first statement, and faithfully paid $25 on Day 1 of every month’s billing cycle.What would be her balance after 12 months of this strategy?

Making Small Payments

Hint: If no charges are made, the average daily balance equals the balance after the payment.If Sandy faithfully pays $20 a month…

And so on, until…

After one year of payments, Sandy still owes over $787 on her original debt of $869.43!

Month 1:$869.43 $20.00 $849.43 Month 2:$849.43 1.75% $849.43 $20.00 $844.29 Month 3:$844.29 1.75% $844.29 $20.00 $839.06

Month 12:$793.76 1.75% $793.76 $20.00 $787.64

Payment New balance

Payment New balanceFinance charge

Payment New balanceFinance charge

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

36

• The correct answer is E.• We do not expect students to be able to actually know or calculate the answer to this question, but merely make an educated guess. The exact answer is 80 months, or about 6 .7 years.• This is essentially an amortization problem, which can be answered using any basic financial calculator. (Enter PV = 869.43, FV = 0, PMT = –20.00, and APR = 20.99%. Solve for N months.) However, that is not the intent here. Rather we wish for students to appreciate the impact of finance charges on revolving credit accounts like Sandy’s.• Obviously, this scenario is a little unrealistic. Most credit card users would not continue to make payments of exactly $20 every month and never make any new charges. Rather, they would continue to use the card for new purchases, and make payments of various amounts each month, based on how much cash was available each month, stretching out the original debt even longer. Unfortunately, that’s the real world for most credit card users. Hopefully this lesson will help make the point that finance charges can be a very expensive cost for quick credit.

37

• This is an excellent use of a spreadsheet, if your students have access to one. Here’s a suggested layout.

APR= 20.99%Starting balance = 869.43Payment =20.00

Month Prev Bal Payments Fin. Chg New Bal1 869.43 20.00 849.432 849.43 20.00 14.86 844.293 844.29 20.00 14.77 839.06

and so forth. If the formulas are correctly created (e.g., using named ranges for the constants), they can simply be copied down as many rows as desired. Note that there is no finance charge assessed on the first month because of the grace period. But because the payment is less than the full amount due, finance charges begin to accrue.• With the spreadsheet, students can easily verify the statements on this slide by copying the rows and formulas to represent as many months as necessary.• Spreadsheet hints:

• Use named cells for the parameters

Page 18

Question 10

Suppose Sandy continues to pay $20 every month. How long do you think it will take for Sandy to completely pay off her original credit card debt of $869.43?A. About 24 months (2 years)B. About 36 months (3 years)C. About 48 months (4 years)D. About 60 months (5 years)E. More than 72 months (6 years)

A Long Debt

E. More than 72 months (6 years)If Sandy continued her $20/month strategy, it would take her about 80 months (6.7 years) to pay off the original debt!The sum of her payments would be $1586.22.We can calculate the cost of her “quick loan” and small monthly payments:

$1,586.22 $869.43Cost of Loan Total Payments Initial Value

$716.79

Credit Card Payments March 2018

SLIDE • TEACHER NOTESvalues for APR, Starting Balance, and Monthly Payment.• Refer to the named cells in the formulas for the finance charge and the new balance. (If named cells are not used, the cell references must be made “absolute” to permit correctly copying the formulas.)• Since the finance charge formula can result in fractional amounts, a ROUND() function must be included to round to the nearest penny (i.e., two decimal places), as the credit card company will also do. Some companies may even use a ROUNDUP() function.

38

• Obviously, credit card agreements can be very complex and even confusing. In this lesson we’ve addressed only one aspect of the use of a credit card: the finance charge associated with an outstanding balance.• It would be very helpful for students to read and decipher several real agreements. Ask students to bring in some of the credit card offers they or their parents have received in the mail. Alternately, these agreements are available online from any of several banks who offer various credit opportunities. A good search term is “credit card agreement.”

39

• This is an application of the calculation of the average daily balance presented in this lesson.

Page 19

Other Charges and Fees

In addition to finance charges, credit card companies also typically charge other fees

Annual fee Balance transfer fee Cash advances finance charge (usually begins accruing

immediately) Late payment fee (if received after the due date) Over-limit fee (exceeding the card’s credit limit)

So, always read the fine print on the credit card agreement!

Practice Problem #1At the start of the billing period, Stan had a balance of $653.07.On Day 4, the bank received his payment of $200.During the rest of billing cycle, he charged:

$490.13 on the 9th day $287.05 on the 14th day $166.71 on the 17th day $64.61 on the 29th day

What is Stan’s average daily balance for this billing cycle?

SOLUTION

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

40

• Students may begin to notice that large charges made early in the month have a much greater impact on the average daily balance than those made near the end of the month.

41

• This is an application of the calculation of the finance charge presented in this lesson.

42

• Be sure students treat the value 18% as 18100 = 0.18.

43

• This is really just a problem of calculating the finance charge on the given balance. However, it couples with it an understanding that the finance charge can actually cause the debt to grow if the payment is too little.

Page 20

Solution to Problem #1

Here’s a chart of Stan’s daily balances.

(rounded)$32,711.80 $1090.39 30

Sum of daily balancesAverage Daily Balance Number of days

Su Mo Tu We Th Fr Sa1

653.072

653.073

653.074

653.075

453.076

453.077

453.078

453.079

943.2010

943.2011

943.2012

943.2013

943.2014

1230.2515

1230.2516

1230.2517

1396.9618

1396.9619

1396.9620

1396.9621

1396.9622

1396.9623

1396.9624

1396.9625

1396.9626

1461.5727

1461.5728

1461.5729

1461.5730

1461.57

Practice Problem #2

Stan’s credit card agreement states that there will be an 19.99% annual percentage rate (APR) finance charge on the average daily balance for the billing cycle.Stan’s average daily balance was $1,090.39.What finance charge will be due on Stan’s next monthly bill?

SOLUTION

Solution to Problem #2

Since the billing period is 1 month, The annual percentage rate must be converted to a monthly periodic rate by multiplying by the unit ratio .Then use the formula for calculating interest, or in this case finance charge.

1yr12mo

19.99%$1,090.39 yr

FinanceCharge Principal Rate Time

1 yr

12 mo

1 mo

(rounded)$18.16

Practice Problem #3

Bonnie uses a new credit card to purchase a $2395 cruise ticket, and nothing else. The card agreement specifies 14.99% APR on new purchases. If Bonnie makes too small a payment, the finance charges will cause the debt to grow rather than shrink each month.What is the smallest amount that Bonnie can pay each month if she hopes to ever pay off the ticket?

SOLUTION

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

44

• You can demonstrate what happens if Bonnie pays less than $30. If she pays $25, for example…After Month 1: Balance = $2395.00 – $25.00

= $2370.00 (no finance charge on first statement)After Month 2: Balance = $2370.00 + 29.61 – $25.00

= $2374.61After Month 3: Balance = $2374.61 + 29.66 – $25.00

= $2379.27After Month 4: Balance = $2379.27 + 29.72 – $25.00

= $2383.99and so on. Students should see that the balance and the monthly finance charge is growing!

45

• A challenging exercise for students as a follow-up to this problem (requires a spreadsheet or financial calculator) is to ask: How long will it take Bonnie to pay off the cost of the ticket if she makes monthly payments of $30? (Ans: 339 months, or 28.25 years!) or $40? (Ans: 109 months, or 9 years) or $50? (Ans: 73 months, or 6 years) or $75? (Ans: 41 months, or 3.4 years) or $100? (Ans: 29 months, or 2.4 years) and so on. Note that when using a financial calculator, the number of periods must be rounded up: for example, for payments of $75, the financial calculator result of N=40.34 months must be rounded up to 41 months, with the last payment (perhaps more easily found by using a spreadsheet) of $25.90.• Real-world questions like this naturally lead into a desire to understand amortization. See also the challenge problem that follows.

46

• Equipped with only the algebraic techniques of this lesson, the students will really need to use a spreadsheet or financial calculator to answer these questions.

Page 21

Solution to Problem #3

If Bonnie pays less than the amount of the finance charge each month, the balance will grow a little each month, and the finance charge will grow a little each month, and so on. Very bad news for Bonnie!If Bonnie pays exactly the amount of the finance charge each month, the balance will remain exactly the same from month to month, and so will the finance charge. This is also bad news for Bonnie.

Challenge ProblemCraig activated a new credit card having a $10,000 credit limit, offering 14.99% APR on new purchases.He used the new card to make one purchase: a new set of bedroom furniture costing $8,791. How long will it take Craig to pay off this one purchase if he

makes payments of $150 every month? What will the furniture really cost him by the time he makes

the final payment?

SOLUTION

Credit Card Payments March 2018

SLIDE • TEACHER NOTES

47

• Using a financial calculator: Enter PV = 8791, FV = 0, PMT = –150, and APR = 14.99%. Solve for N months: N = 104 months (rounded up). Or using the MS-Excel spreadsheet function: NPER(0.1499/12,–150,8791,0,1) = 104 (rounded up).• With revolving credit card accounts, payments may be applied to the daily balance at the beginning of the period or on the date the payment is received. Some calculators are able to distinguish between payments made at the start of the period or at the end of the period. To agree with the methods taught in this lesson, those calculators need to be set for the start (or beginning) of the period. Similarly, the final parameter (value = 1) in the spreadsheet NPER function specifies this “beginning” condition.• The $15,600 total cost of the television given above is approximate because the final payment will need be only $74.76 (not the full $150) to pay the final balance and finance charge. The precise total cost is $15,524.76.

Page 22

Solution to Challenge Problem

Using a spreadsheet, or a financial calculator:Initial Balance (or present value PV) = $8791,Final Value (or future value FV) = 0, Monthly Payment (or payment PMT) = –$150,Annual Interest Rate (or APR) = 14.99%.

“Financially solving” for N with a financial calculator or spread-sheet reveals it will take Craig 104 months to pay for the furniture.So, the furniture will cost Craig the total of all his payments: roughly, 104 $150 = $15,600!!