Embed Size (px)

Citation preview

ANNEXES

Page 1

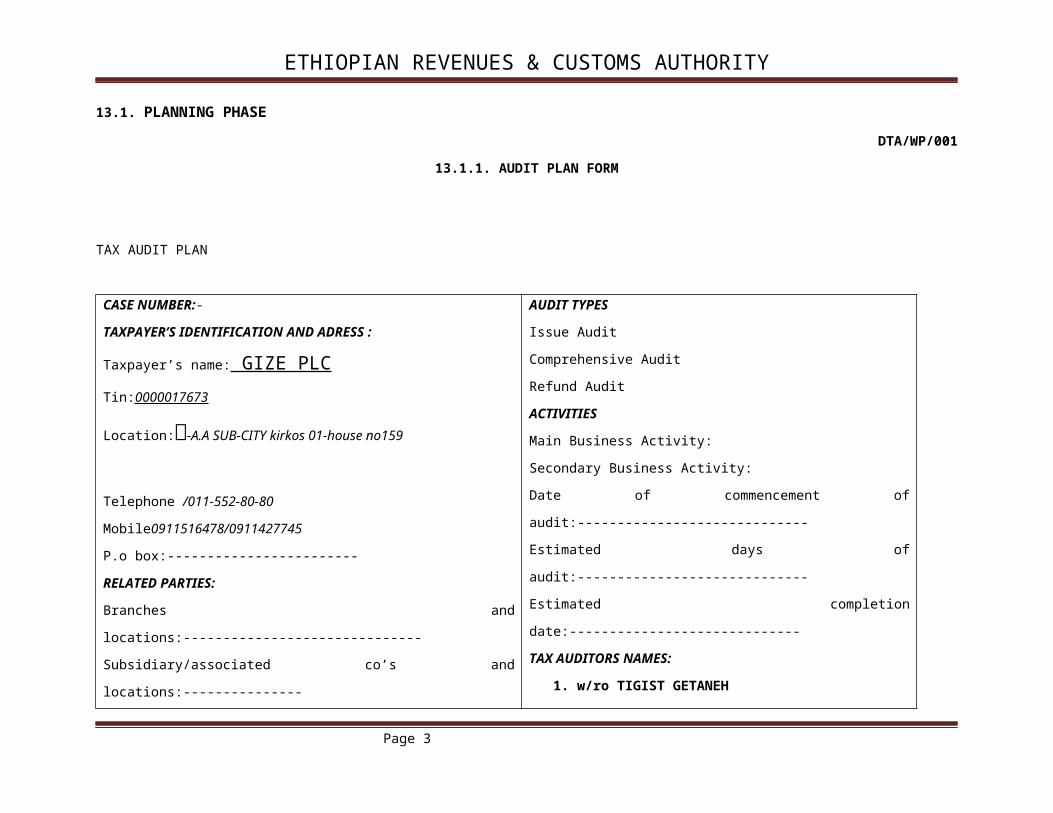

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

13.1. PLANNING PHASEDTA/WP/001

13.1.1. AUDIT PLAN FORM

TAX AUDIT PLAN

Page 2

CASE NUMBER:-

TAXPAYER’S IDENTIFICATION AND ADRESS :

Taxpayer’s name: GIZE PLC

Tin:0000017673

Location:፡-A.A SUB-CITY kirkos 01-house no159

Telephone /011-552-80-80 Mobile0911516478/0911427745P.o box:------------------------

RELATED PARTIES:

Branches and locations:------------------------------

Subsidiary/associated co’s and locations:---------------

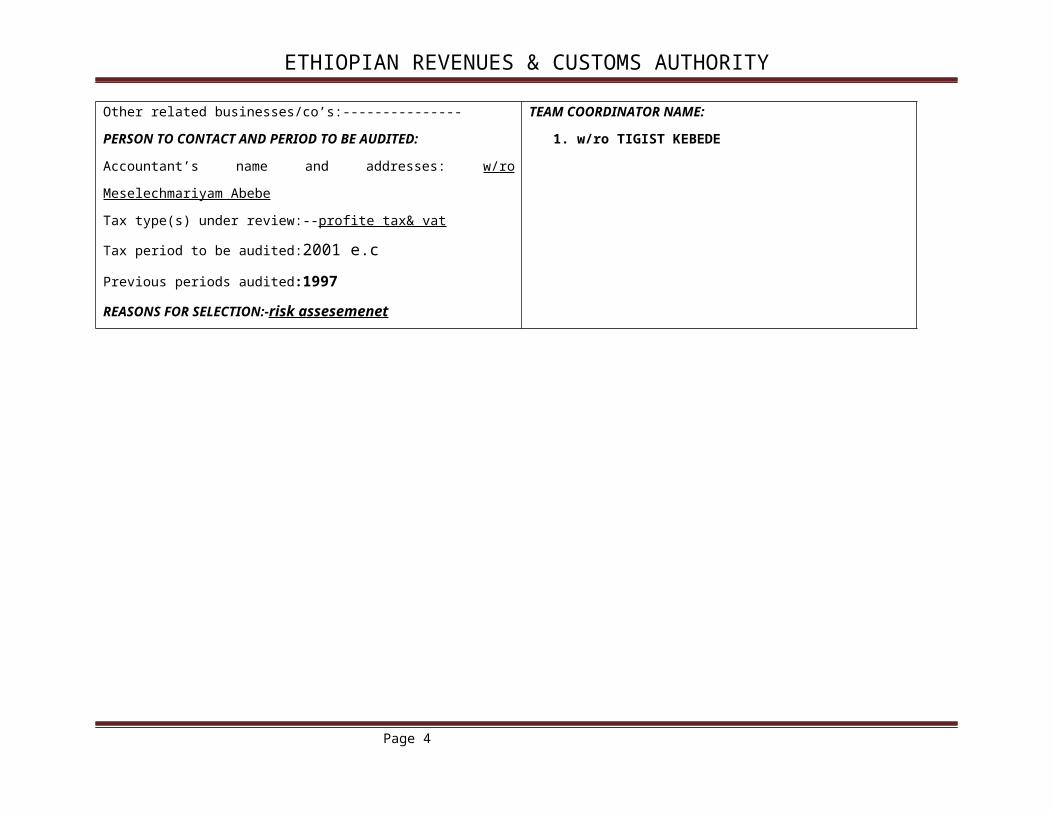

Other related businesses/co’s:---------------

PERSON TO CONTACT AND PERIOD TO BE AUDITED:

Accountant’s name and addresses: w/ro Meselechmariyam Abebe

Tax type(s) under review:--profite tax& vat

Tax period to be audited:2001 e.c

Previous periods audited:1997

REASONS FOR SELECTION:-risk assesemenet

AUDIT TYPES

Issue Audit

Comprehensive Audit

Refund Audit

ACTIVITIES

Main Business Activity:

Secondary Business Activity:

Date of commencement of audit:-----------------------------

Estimated days of audit:-----------------------------

Estimated completion date:-----------------------------

TAX AUDITORS NAMES:

1. w/ro TIGIST GETANEH

TEAM COORDINATOR NAME:

1. w/ro TIGIST KEBEDE

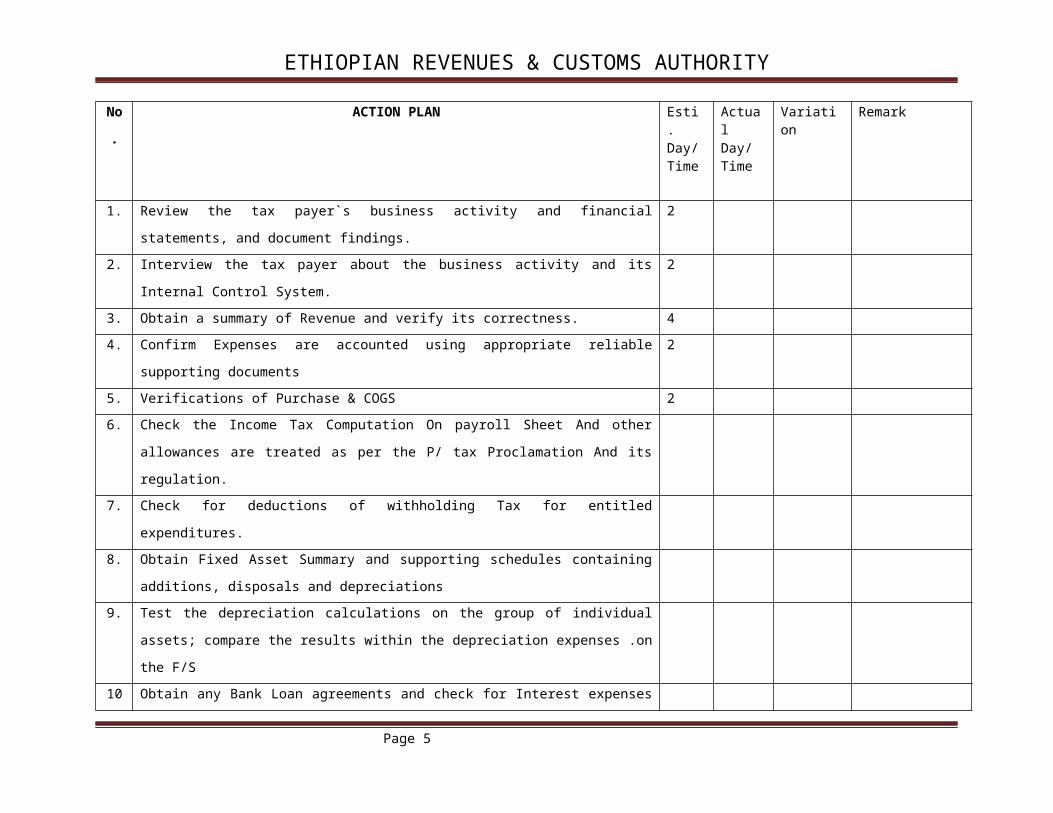

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

No. ACTION PLAN Esti. Day/Time

ActualDay/Time

Variation Remark

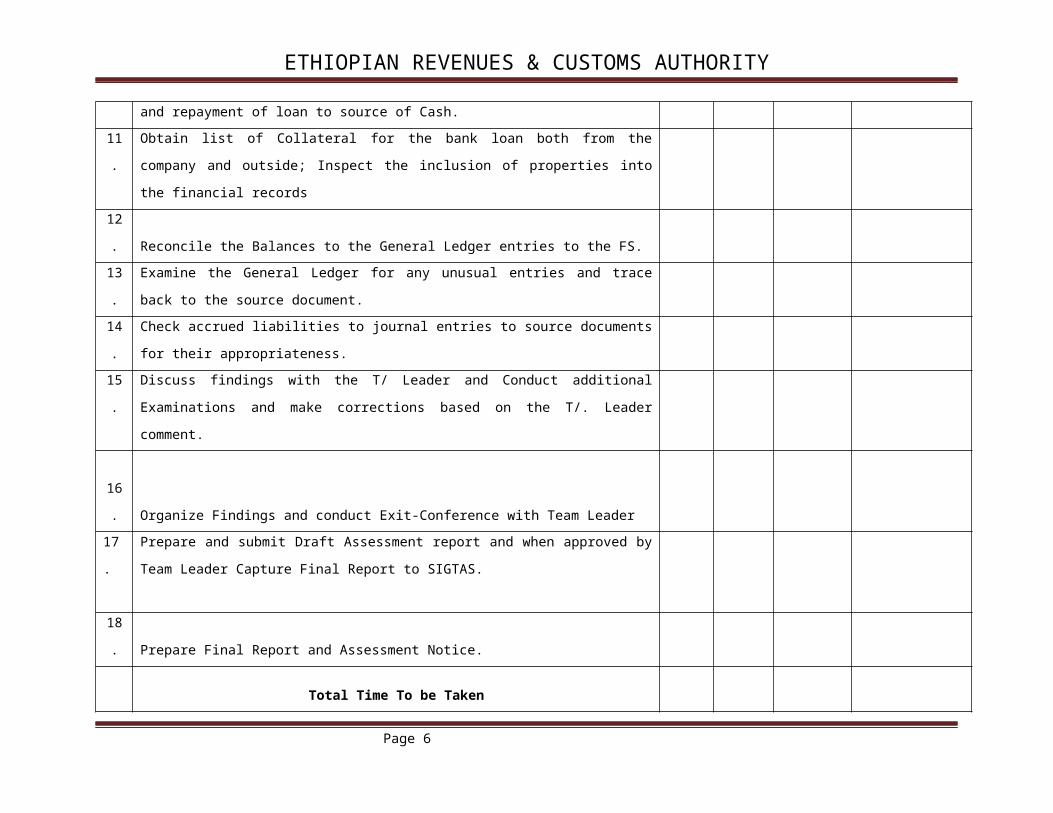

1. Review the tax payer`s business activity and financial statements, and document findings. 2

2. Interview the tax payer about the business activity and its Internal Control System. 2

3. Obtain a summary of Revenue and verify its correctness. 4

4. Confirm Expenses are accounted using appropriate reliable supporting documents 2

5. Verifications of Purchase & COGS 2

6. Check the Income Tax Computation On payroll Sheet And other allowances are treated as per

the P/ tax Proclamation And its regulation.

7. Check for deductions of withholding Tax for entitled expenditures.

8. Obtain Fixed Asset Summary and supporting schedules containing additions, disposals and

depreciations

9. Test the depreciation calculations on the group of individual assets; compare the results within

the depreciation expenses .on the F/S

10 Obtain any Bank Loan agreements and check for Interest expenses and repayment of loan to

source of Cash.

11. Obtain list of Collateral for the bank loan both from the company and outside; Inspect the

inclusion of properties into the financial records

12. Reconcile the Balances to the General Ledger entries to the FS.

13. Examine the General Ledger for any unusual entries and trace back to the source document.

14. Check accrued liabilities to journal entries to source documents for their appropriateness.

15. Discuss findings with the T/ Leader and Conduct additional Examinations and make corrections

based on the T/. Leader comment.

16. Organize Findings and conduct Exit-Conference with Team Leader

Page 3

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

17. Prepare and submit Draft Assessment report and when approved by Team Leader Capture Final

Report to SIGTAS.

18.Prepare Final Report and Assessment Notice.

Total Time To be Taken

Tax Auditors Name Signature Tax Audit Team Coordinator signature

Page 4

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

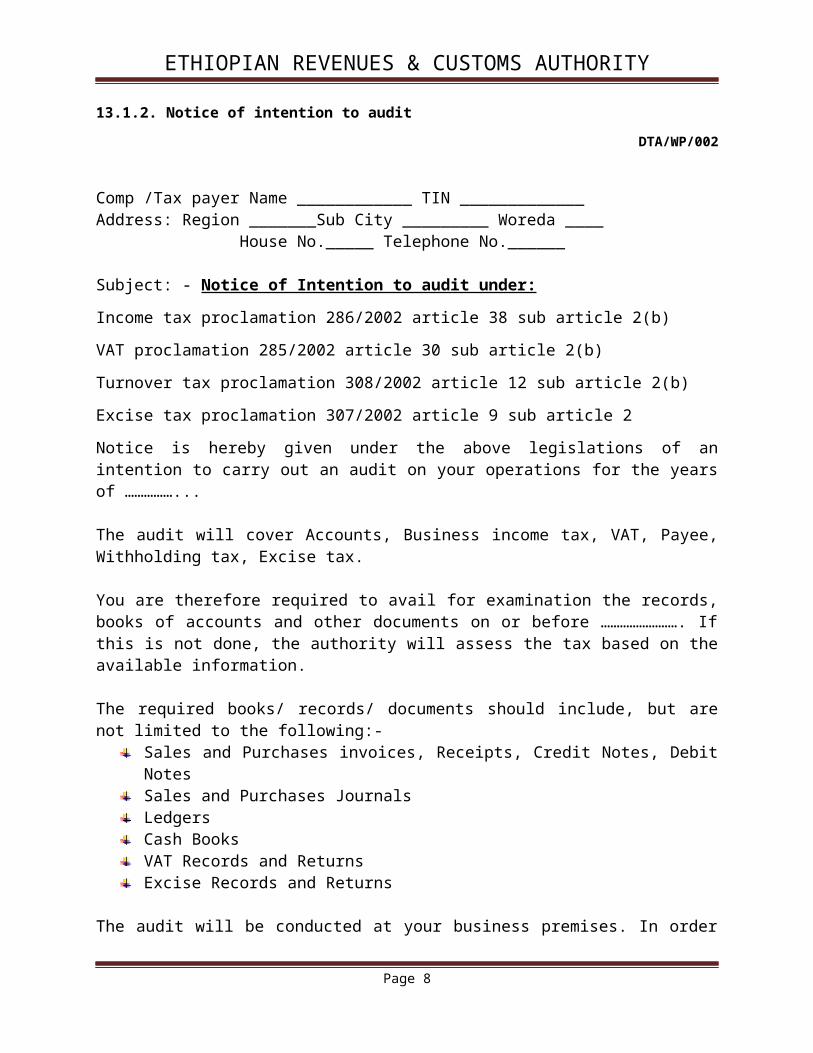

13.1.2. Notice of intention to auditDTA/WP/002

Comp /Tax payer Name ____________ TIN _____________Address: Region _______Sub City _________ Woreda ____ House No._____ Telephone No.______

Subject: - Notice of Intention to audit under:

Income tax proclamation 286/2002 article 38 sub article 2(b)

VAT proclamation 285/2002 article 30 sub article 2(b)

Turnover tax proclamation 308/2002 article 12 sub article 2(b)

Excise tax proclamation 307/2002 article 9 sub article 2

Notice is hereby given under the above legislations of an intention to carry out an audit on your operations for the years of ……………...

The audit will cover Accounts, Business income tax, VAT, Payee, Withholding tax, Excise tax.

You are therefore required to avail for examination the records, books of accounts and other documents on or before ……………………. If this is not done, the authority will assess the tax based on the available information.

The required books/ records/ documents should include, but are not limited to the following:-Sales and Purchases invoices, Receipts, Credit Notes, Debit NotesSales and Purchases Journals LedgersCash BooksVAT Records and ReturnsExcise Records and Returns

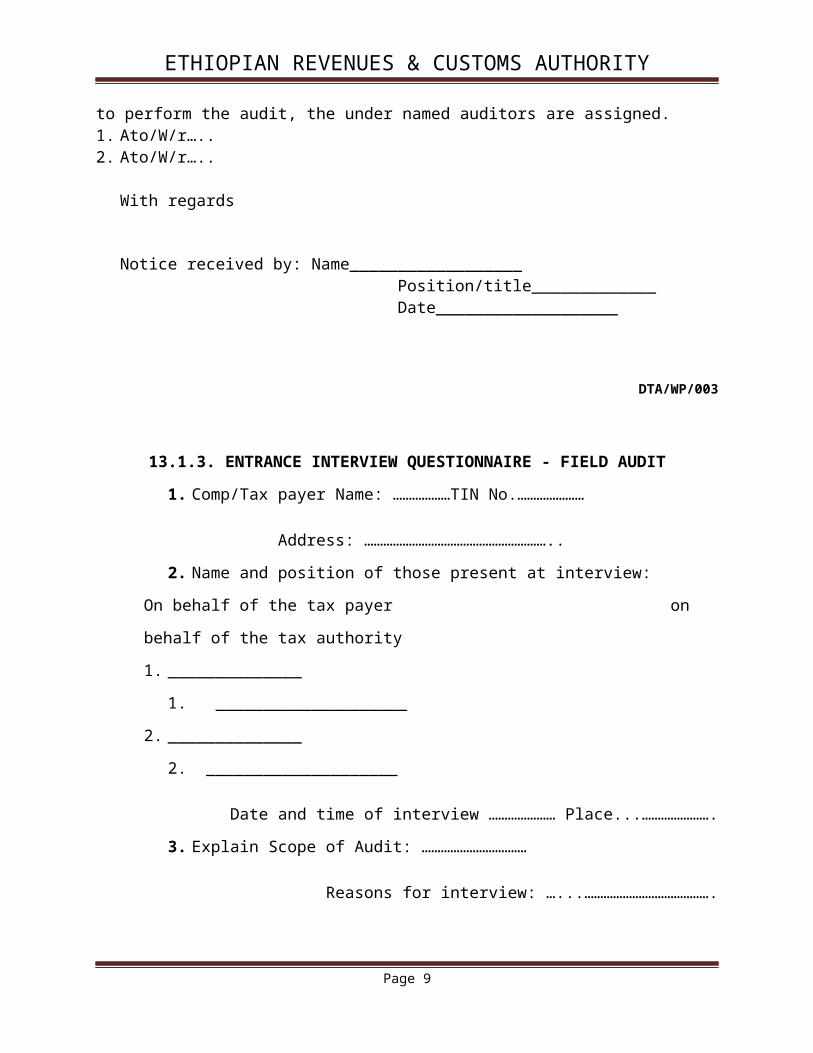

The audit will be conducted at your business premises. In order to perform the audit, the under named auditors are assigned.1. Ato/W/r…..2. Ato/W/r…..

With regards

Notice received by: Name__________________ Position/title_____________ Date___________________

Page 5

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/003

13.1.3. ENTRANCE INTERVIEW QUESTIONNAIRE - FIELD AUDIT

1. Comp/Tax payer Name: ………………TIN No.…………………

Address: …………………………………………………..

2. Name and position of those present at interview:

On behalf of the tax payer on behalf of the tax authority

1. ______________ 1. ____________________

2. ______________ 2. ____________________

Date and time of interview ………………… Place...………………….

3. Explain Scope of Audit: ……………………………

Reasons for interview: …...………………………………….

4. Agend

a-------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------

---------------------------------------------------------------------------------------------------

----------------------------------------

5. Business Activities:

A. Income cash – How are cash receipts reconciled?

Who is responsible for reconciling them?

What supporting records are available?

Are receipts banked entire? If not what records are kept of gross takings and payments

made?

How was the sales figure in the accounts arrived at? Is same agreed with above records?

B. Payments – Are all payments made by cheque?. Who draws cheque?

If there are cash payments including private items how are these recorded dealt with in

the accounts? Are invoices and receipts available for verification?

C. Debtors – Are there credit sales?

Page 6

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

What records are kept?

Is a debtors control account maintained?

Is a list of balances available?

If not how is end-of-year figure arrived at

D. Creditors – End of year figure

How arrived at. What records? Obtain copy.

E. Stock-Is there any stock or works in progress.

What stock records are kept?

Obtain copy of stock sheets

What is the basis of valuation?

F. Private Use – Goods and cash taken for private use.

What adjustments are made?

How are they computed?

Are they regularly reviewed?

What supporting documents are available?

How are they recorded in the accounts?

Motor Vehicles and private premises

Is adjustments made?

How is it calculated?

What justification for business portion is there evidence to support this?

G. Obtain authorities for all business bank accounts, and solicitor trust Accounts.

Full list of all bank accounts (including Savings Banks).

Current Accounts_________________

Fixed Accounts____________________

Term Deposits______________

Investment Accounts_________________

Savings Accounts______________________

Treasury Bills_______________________

Treasury Bonds._______________________

H. Internal check – Enquire as to the allocation, of staff duties and employees relationship

to proprietor, in particular.

Page 7

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

I. Income Cash – What is system for recording cash sales?

Who receipts debtors’ remittances?

Who reconciles the cash taken with the total of cash sales and debtors’ remittances and

what record of such reconciliation are available?

Who banks the cash and at what intervals?

II. Debtors – What is the system for ensuring that all goods dispatched are invoiced?

How is debtors’ cash posted?

Who controls credit note issue?

Who balances Debtors’ Control Account?

Creditors – How is the receipt of goods verified and recorded and by whom?

Who draws cheque in payments of suppliers’?

Who codes payments and what is coded? cheque butts, invoiced

III. Wage payments – from what base data are wages calculated?

Is same available for inspection?

Who calculates wages?

Who draws wages cheques?

Who makes up pay packets?

Who actually pays the employees?

Are wages paid from cash and if so are the wages and

PAYE correctly recorded?

5. What are the major customers of the company? __________________ __________________6. What are the major suppliers of the company? _______________________________ _______________________________7. Are there related parties with transactions under the definition of related party under income

tax proclamation 286/2002 article 2(4)? If yes, state the names, nature of relationship and

amounts of transactions.

13.2. EXECUTION PHASE

13.2.1. Audit programs EDTA/WP/004

Page 8

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR CASH /BANK BALANCES

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. AssertionsCash collected or deposited is recognized as income or Revenue of the company. Cash receipts and cash disbursements are recorded correctly as to account, amount, and

period. Cash balances include funds at all locations, funds with custodians and deposits in transit.

Completeness Cash is properly classified and presented in the financial statements, and adequate

disclosures are made with respect to restricted cash.

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working paper

Reference

Cash1. Review the internal controls and systems with respect to the reconciliation of daily cash

receipts and banking.2. Compare the balances indicated in the books of account, general ledger, and financial

statements.3. Determine the roles played by the key shareholder/officials are involved in the

maintenance of records and in the banking of revenues.4. Determine if cash collected is used for petty cash operational requirements, wage

payments, remuneration of official and non-business expenditures.5. Test the daily deposits to the cashbook, bank deposit and bank statements.6. Determine if the company employees are bonded by an insurance company and the

requirements placed by the insurer with respect to controls, reporting etc. Check if the taxpayer has lodged claims with the insurer for the loss or theft of funds.

7. If the auditor has reason to suspect that the controlling shareholders or executives of the company may be suppressing income and siphoning funds, review the details of their personal bank accounts and request explanations of deposits which are inconsistent with the remuneration made;

8. As a follow up to the above, conduct a net worth assessment of the major shareholders or company executives to establish the changes in net assets in relation to the salaries and compensation paid by the taxpayer. The taxpayer will be required to disclose the sources of income;

9. Determine if the taxpayer has taken police or legal action with respect to funds, which have been misappropriated.

Page 9

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

10. Consider attending the cash reconciliation process at the end of the day to ascertain the reliability of the reconciliation process.

11. Verify the role of the external or internal auditors with respect to surprise and year-end cash counts.

Bank Balances1. Review the internal controls and systems with respect to the banking of deposits and

disbursements. 2. Determine the policies and procedures with respect to the maintenance of foreign

currency accounts, payments and transfers, particularly to overseas accounts. 3. Confirm the agreement of the bank balances indicated in the books of account and

financial statements with the banks’ statements, including foreign accounts;4. Ascertain if the independent auditor confirmed the account balances directly with all of

the banking institutions, including foreign banks;5. Test the monthly banking transactions, paying particular attention to cheques made out to

“Cash”, Bearer” or company officials that are supposedly used for business purposes. Check the endorsements on cheques that seem to be out of the ordinary.

6. Test the transfers to foreign accounts to the bank’s transmittal advice notice.7. Determine the source of deposits that are from non-operational sources, such as bank

loans, shareholder capital contributions etc.;8. Consider requesting the confirmation of bank balances directly with the banking

institution if there are doubts as to the validity or accuracy of the taxpayer’s records.

Cash/Bank Balances Tax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

DTA/WP/005

Page 10

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR ACCOUNTS RECEIVABLE

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions

Completeness

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working paper

Reference

1. Reconcile Accounts Receivable per return to general ledger (schedule: General Ledger account number, account description, & amount). Explain any differences. Secure an analysis of the receivable by class that is, by note or open account status, and by obligors, such as customers, affiliated companies, stockholders, officers, employees and others.

2. Compare beginning general ledger balance to ending general ledger balance. Investigate significant changes.

3. Review the subsidiary receivable ledgers or a trial balance based on these ledgers. They should agree in total with the control accounts. Any unusual credit entries, in real amount; by source (posting reference), in nature (descriptions), or a credit balance should be investigated. Credit entries may indicate deposits or overpayments which could be considered as additional income or unrecorded sales. Accounts Receivable postings are usually from sales journal & cash receipts journal. Unusual entry would be credit entry not from cash receipts journal.

4. Obtain Trial Balance of accounts receivable & compare total to the controlling accounts receivable general ledger account. Investigate any differences e.g. diversion of funds, large credit balances. Income ? e.g. deposits, overpayments received.

5. Sample debit entries in accounts receivable subsidiary ledger (individual customers) and trace to sales journal for unreported sales in accounts receivable ledger & trace to cash receipts journal. If no entry in cash receipts journal did company write off as bad debt? Debit Sales? Diversion of funds?

6. In cash receipts journal, sample credit entries to accounts receivable where Debit is to cash & verify sale was previously recorded.

7. Ask company what percentage of sales represents cash (vs. sales on account). Then review cash receipts journal for a month or two & compare total cash sales to sales for same two months in sales journal (sales on account).

8. Verification of the list of receivables with the subsidiary ledger general ledger and financial statements;

9. The inclusion of non-trade accounts on the list, for example, advances to shareholders that may represent a form of remuneration which should be taxed at the personal income level;

Page 11

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

10. Notation of credit balances on individual customers' accounts for further examination. The credit could represent a bona-fide credit for goods returned, an advance payment, a misclassified loan or a payment for goods purchased by the customer for which the sale has not been recorded in the records;

11. Discussions with the external auditor to determine the extent of his/her independent verification of receivables;

12. Review of agreements covering loans payable to determine the value of accounts receivable pledged as security by the taxpayer. Direct verification with the lender may be necessary.

13. For bad debts the auditor will have to satisfy himself that the taxpayer has complied with Article 25 of the Income Tax Proclamation and consider the following;

The transactions which gave rise to the debt to confirm validity as a trade debt, age of debt etc.

Efforts by the taxpayer to collect the debt (i.e. has taken all steps reasonably necessary to recover the debt)

Correspondence between the taxpayer and his customer payments, if any, by the customer subsequent to the year-end

The taxpayer's practice of continuing to sell to the customer despite the doubtful collection status

If possible, determine the financial status of the customer i.e. bankrupt, non-operating, etc.

The existence of security or guarantees pledged by the customer to secure the debt.

ACCOUNTS RECEIVABLETax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

DTA/WP/006

Page 12

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR INVENTORY

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions

Completeness

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working paper

Reference

Inventory for merchandise

1. If practical, for example in the case of a retailer, visit the business premises of the taxpayer before the commencement of the audit and observe the taxpayer’s practices with respect to inventory management, invoicing, and cash management.

2. Determine the extent of the verification performed by the independent external auditor;3. Compare the taxpayer’s inventory records (or year-end inventory list) with the books of

account, financial statements and tax declaration. Note the locations, costing method and any provisions made for obsolescence. Test the costs from the suppliers invoices, import entries etc. for the items that comprise the majority of the reported inventory. Determine the inventory valuation method used by the taxpayer and its acceptability in relation to Article 22 of the Income Tax Proclamation-Trading Stock.

4. If the taxpayer maintains perpetual inventory records, compare the physical inventory stock taking record, on a test basis, and review any adjustments made by the taxpayer with respect to shortages, values and the like;

5. Review the taxpayer’s accounting system and internal controls related to the movement and storage of finished goods, particularly with respect to goods stored at the premises of company officials. Determine if the taxpayer takes periodic inventories; maintains formal or temporary inventory records and a stock level/recorder process;

6. In the event that the auditor suspects that the taxpayer may be suppressing sales or income, identify the personnel who have knowledge of the taxpayers inventory management practices and procedures for the purposes of obtaining information under the provisions of Article 38 and Article 79, or taking enforcement action under the provisions of Articles 97 and Article 98 of the Income Tax Proclamation;

7. Compare the regular selling price of the major items in inventory to the invoiced cost to determine if the indicated profit margins are reasonable and consistent with the financial statements and the tax declaration;

Page 13

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

8.Estimate the retail value of the inventory of goods for sale, the gross trading margin, and the frequency of the annual inventory turnover in order to determine the reasonableness of the inventory value;

9. Visit the taxpayer’s premises where goods are stored and identify the types of goods that the auditor suspects may be contraband or counterfeit and request the taxpayer to provide supporting documentation. Inform the audit superior if there is reason to believe that the taxpayer is evading taxes and customs duties for direction on the course of action to be taken.

10. Test the values of inventories of imported goods to the supplier’s invoice, ERCAs evaluations and entries.

11.Depending on the date the taxpayer took the physical inventory, test the taxpayer’s system and procedures with respect to making adjustments for sales and purchases in order to arrive at an accurate inventory on the closing date of the taxation year;

12.Review any loan agreements to determine the description, quantities, value and location of inventories pledged by the taxpayer as security. The lender may have a floating charge on all inventories and the borrower may be required to provide updates of inventory levels. In addition, the lender may insist on insurance coverage and the auditor should review the insurance policies for details and the supporting independent inventory valuations.

13. Determine the composition of the inventory that may have been supplied by the foreign parent or associated company for subsequent investigation with respect to transfer pricing or fair market issues.

Inventory for manufacturingGoods of the taxpayer’s own manufacture should be valued on the basis of the aggregate of the cost of material, direct labor and overhead. 1. Match the physical inventory records with the perpetual inventory or warehousing records

(if maintained) to the general ledger, financial statements and tax declaration; 2. Determine the extent of the verification conducted by the independent external auditor; 3. Review the costing methods used by the taxpayer to value closing inventories, work in

process and sales of finished goods. Review the periodic or annual adjustments made by the taxpayer to update standard costs and the adjustments made to the values of inventories and cost of goods sold. Ensure that the excise tax is treated as part of the cost of production and not as an operating expense. Ensure that custom work provided by third parties, such as specialized machining of the product, are include in the production costs and not as an expense;

4. Review the method and basis used by the taxpayer to value goods below cost, due to such matters as product obsolescence, faulty production runs and the like. Determine if some of these products have been sold subsequent to the year-end and the sale value thereof;

5. Determine if the inventories have been pledged as security for loans and review the insurance coverage.

6. Determine the raw materials and components that may be supplied by the foreign parent for subsequent review under the transfer pricing considerations;

7. Compare the established selling prices of the major items in the inventory to the manufacturing costs, and subsequently to the financial statements and tax declaration for reasonableness and consistency;

Page 14

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

COST OF INVENTORYTax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

DTA/WP/007

Page 15

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR FIXED ASSETS

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions

To ve Completeness

Audit Steps: (Document audit steps taken or to be taken.)Prepared by Working

paper reference

1. Review general ledger accounts- Insure that ending balance reconciles to tax return. Determine that

any book & tax differences are reflected in separate schedules.

2. Reconcile additions and/or deletions to other gain or loss entries.

3. Independently trace selected debits from depreciation reserve to verify removal from reserve & possible

omitted sale of depreciable assets.

4. Scan depreciation schedule for proper lives, methods, etc.

5. Examine asset additions (basis in fixed assets or depreciation schedule:

Verify that tax basis included all related costs to place the asset in service; e.g. transportation,

installation, taxes, legal fees, etc. Verify ownership; review invoices paid, review contracts,

property tax, and physical inspection.

Analyze lump sum acquisition for allocation of basis.

Analyze land/building allocation.

When an asset acquisition occurs via tax-free exchange? Verify correct basis cost of assets traded

plus other cash or consideration given.

Verify value of assets acquired from related parties. In addition to purchase documents, verify

values from third party sources for comparisons.

Verify property transferred as capital; proper value and actually transferred.

6. Verify proper costs being charged to asset account of self constructed assets. Review internal costing

practices on self constructed assets to ensure all costs from all active expense accounts are properly

Page 16

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

included in basis of self constructed asset. Inspect asset for further ideas on which expense areas may

have related costs.

7. Where acquisition consideration is other than cash, review method used in arriving at basis. In these

acquisitions, the basis of the property or properties traded must be verified and properly allocated to the

new property.

8. Corporate acquisition? Is there a stepped up basis? You will need purchase documents, appraisals,

allocation schedules, and any other documents related to the purchase.

9. Check company policy on capitalization of minor items. Inquire into change to the company’s

accounting for major repairs, additions, deletions etc. Inquire if remodeling/renovation done.

10. Did new asset replace old? Gain/Loss correctly computed? If old asset traded in on new asset, was gain

or loss on old asset correctly adjusting basis of new asset.

11. Dispositions of obsolete assets or obsolete repairs parts: verify that they are actually disposed - sold,

junked, etc. If they remain under company control, lack of use does not justify recording the possible or

estimated loss.

Depreciation

1. Reconcile the amount(s) per return to Taxpayer’s records.

2. Check depreciation method to determine compliance with tax law and consistency with prior years.

3. Determine assets included in depreciation deduction (proper classification).

4. Ensure items depreciated are depreciable (land not depreciable) and are ordinary and necessary to

taxpayer business.

5. Examine purchase invoices, receipts, etc. to verify ownership of assets.

Examine purchase invoices, receipts, etc. to verify cost of assets and date assets were6. placed in service.

7. Determine appropriate cost basis for depreciation (consider capital improvements, prior depreciation,

adjust the cost basis of a depreciable automobile by the trade-in value of a prior automobile, etc.).

8. Determine if any assets were sold by comparing with prior year depreciation schedules. Recapture any

depreciation from sale of assets if applicable (balancing charge).

9. Examine logbooks and other records to determine percent business use of assets depreciated.

10. Determine if proper useful life of the asset is utilized.

11. Calculate depreciation deduction. Check the mathematical calculations.

Page 17

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

FIXED ASSETSTax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

Page 18

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/008

AUDIT PROGRAM FOR COST OF GOODS SOLD

Tax Payer Name: GIZE PLC Auditor:-W\RO TIGIST GETANEH

TIN:-0000017673

Tax Year 2001 Date:

Audit Objectives F/st. Assertions How mach cost of gods sold have legal document

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working paper

Reference

Action Required-Confirm that the taxpayer’s claim for expenses deducted in computing

taxable business income comply with the provisions of Articles 20 and 21 of the Income Tax

Proclamation and the supporting Regulations 9 to 11 inclusive.

1. Compare the financial statements and tax declaration for the current year with those of the

two preceding years, in order to determine significant changes in gross trading margins,

significant variances in labor, overhead and other expenditures that will require

examination;

2. Reconcile the purchases and expenses recorded in the books of account, general ledger

and financial statements with the income tax declaration;

3. Reconcile the list of accounts payable with the general ledger, subsidiary ledger, financial

statements and tax declaration. Test the statements of the major creditors for agreement.

Identify liabilities which may be trade accounts payable, such as loans or advances made

by shareholders or company officials, which will require further review in relation to

interest charges and the application of Article 21 (3) and supporting Regulation 10;

4. Review long-outstanding debts to suppliers, which may be indication of goods returned

but not recorded to offset the debt; disputes between the taxpayer and supplier; false

purchase transactions intended to overstate costs and, possibly, VAT input tax credits;

Page 19

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

5. Determine the degree to which the independent external auditor verified the trade

accounts payable;

6. Review and test the accounting system and internal controls/checks that exist over the

ordering, receipt, storage, payment and withdrawal of goods and the recording in the

Purchase Journal, subsidiary ledger, and general ledger.

7. Test the taxpayer’s recording of the purchase invoices to the purchase Journal, subsidiary

accounts payable ledger, and subsidiary asset or expense ledgers and to the general ledger.

Pay particular attention to cash purchase and consider disallowance if the expenses can

not be substantiated by the taxpayer;

8. Obtain a summary of the taxpayer’s importations for the year form the ECuA, analyzed by

tariff item or other criteria, for comparison to the books of account. This information is

required also for the purposes of verifying business income tax paid on imports and to

ascertain if there is reason to believe that the taxpayer is also marketing smuggled goods.

The latter situation would be indicated by the taxpayer’s sales, or inventory levels of a

specific product being inconsistent with the recorded value of the importations;

9. Test the taxpayer’s purchases that involve claims for VAT input tax credit to confirm that

the supplier is a VAT registrant; the purchase is for VAT taxable operations;

10. Confirm that the taxpayer pro-rates purchases/overheads are pro-rated where the taxpayer

is engaged in VAT taxable and VAT exempt operations;

11. Confirm that the taxpayer is not claiming duplicate input tax credit on the importation of

goods that are also subject to Duty Drawback Claims in relation to Article 21(7) of the

VAT Proclamation;

12. Test purchase of goods and service where VAT has not been charged by the supplier and

the suppliers of imported services, the latter to ensure that the taxpayer has withheld and

paid VAT and Income Tax;

13. List (in the working papers) the suppliers of good/services who are not registered for VAT

for which follow-up action by the ERCA is warranted;

14. List the major foreign and domestic suppliers, by transaction volume, for subsequent

testing of product costs, trading margins on sales in order to test the reasonableness of the

reported gross profit margin in the financial statements;

COST OF MANUFACTURING

Action Required-Confirm that the taxpayer is accurately accounting for the costs of

manufacturing and inventories of raw materials/components, work in progress, finished goods

and operating supplies.

1. Review the taxpayers costing method, policies and procedures with respect to the

Page 20

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

determination of manufacturing cost and inventory valuations. Review the adjustments

made during the year and/or at year-end to standard costs for price adjustments, revise

labor rates, charges for custom work and overhead rates.

2. Reconcile the costs of goods manufactured and the related inventories for the year to the

production records, general ledger, financial statements and the excise tax and income tax

declarations. Confirm that inventories have been valued in accordance with Article 22 of

the Income Tax Proclamation –Trading Stock. Confirm that the taxpayer has included the

appropriate cost items in the overhead computation. Determine the extent of Verification

made by the independent external auditor.

3. Test the taxpayer’s actual systems of accounting and internal controls with respect to the

manufacturing process with respect to:

Raw materials and components – purchases transfer to stores, withdrawals from

stores, wastage or unauthorized diversions, completed production runs, unit cost

component, foreign exchange and cost adjustments;

Contracted services, such as machining for which the taxpayer does not have the

facility or the capacity and the taxpayer’s treatment as a direct cost or as overhead;

Labor-rate differentials according to personnel skills and experience, wage and

benefit packages, union agreements, treatment of employee termination payment’s

overtime payments, temporary employees and other matters;

Overhead-inclusion of all overhead costs, cross-reference to the books of account

and tests of suppliers to confirm the costs incurred;

Inclusion of the excise tax in the costs;

Finished goods-transfers to finished goods inventories, unit costing and cross-

reference to sales, valuation adjustments and the like;

Work in progress – production runs completed, reasonableness of the value of goods

transferred to the finished goods inventory during the period immediately following

the year-end date.

4. Compare the financial statements and tax declaration for the current year with those of the

two preceding years, in order to determine significant changes in gross trading margins,

significant variances in labor, overhead and other expenditures that will require

examination;

5. Reconcile the purchases and expenses recorded in the books of account, general ledger

and financial statements with the income tax declaration;

6. Reconcile the list of accounts payable with the general ledger, subsidiary ledger, financial

statements and tax declaration. Test the statements of the major creditors for agreement.

Identify liabilities which may be trade accounts payable, such as loans or advances made

by shareholders or company officials, which will require further review in relation to

Page 21

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

interest charges and the application of Article 21 (3) and supporting Regulation 10;

7. Review long-outstanding debts to suppliers, which may be n indication of goods returned

but not recorded to offset the debt; disputes between the taxpayer and supplier; false

purchase transactions intended to overstate costs and, possibly, VAT input tax credits;

8. Determine the degree to which the independent external auditor verified the trade

accounts payable;

9. Review and test the accounting system and internal controls/checks that exist over the

ordering, receipt, storage, payment and withdrawal of goods and the recording in the

Purchase Journal, subsidiary ledger, and general ledger.

10. Test the taxpayer’s recording of the purchase invoices to the purchase Journal, subsidiary

accounts payable ledger, and subsidiary asset or expense ledgers and to the general ledger.

Pay particular attention to cash purchase and consider disallowance if the expenses cannot

be substantiated by the taxpayer;

11. Obtain a summary of the taxpayer’s importations for the year form the ASYCUDA++,

analyzed by tariff item or other criteria, for comparison to the books of account. This

information is required also for the purposes of verifying business income tax paid on

imports and to ascertain if there is reason to believe that the taxpayer is also marketing

smuggled goods. The latter situation would be indicated by the taxpayer’s sales, or

inventory levels of a specific product being inconsistent with the recorded value of the

importations;

12. Test the taxpayer’s purchases that involve claims for VAT input tax credit to confirm that

the supplier is a VAT registrant; the purchase is for VAT taxable operations;

13. Confirm that the taxpayer pro-rates purchases/overheads are pro-rated where the taxpayer

is engaged in VAT taxable and VAT exempt operations;

14. Confirm that the taxpayer is not claiming duplicate input tax credit on the importation of

goods that are also subject to Duty Drawback Claims in relation to Article 21(7) of the

VAT Proclamation;

15. Test purchase of goods and service where VAT has not been charged by the supplier and

the suppliers of imported services, the latter to ensure that the taxpayer has withheld and

paid VAT and Income Tax;

16. List (in the working papers) the suppliers of good/services who are not registered for VAT

for which follow-up action by the ERCA is warranted;

17. List the major foreign and domestic suppliers, by transaction volume, for subsequent

testing of product costs, trading margins on sales in order to test the reasonableness of the

reported gross profit margin in the financial statements;

Page 22

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

COST OF GOODS SOLDTax Period Per Return Per Exam Adjustment

2001 9,055.56

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

DTA/WP/009

Page 23

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR ACCOUNTS PAYABLE & OTHER LIABILITIES

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working paper

Reference

ACCOUNTS PAYABLE & OTHER LIABILITIES

1. Reconcile the taxpayer’s list of accounts payable with the subsidiary ledger, general ledger,

financial statements and tax declaration.

2. Compare beginning & ending balances and investigate significant changes.

3. Review general ledger for unusual entries.

4. Accrued expenses:

Determine how accruals were computed; ask company; review amortization schedule where

applicable; review agreements/contracts if necessary.

Determine if accruals are deductible. E.g. Related parties - accrued bonuses not deductible until

paid.

Test subsequent year for payments

Were reversing entries properly made?

5. Check for Inter-company Loans

6. Review Deferred Income Taxes

7. Deferred Credits- investigate all significant credit balances. Deferred income?

8. Contingent & estimated liabilities:

Determine if estimated, contingent, disputed liabilities are present.

Determine if company is deducting.

Determine nature & purpose of contingent liabilities, how amount determined, how long

liability outstanding, & subsequent payment

Page 24

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

9. Other liabilities: Any liability that is not included in the above categories.

Examine any large/unusual accounts or entries within account.

Look for items that should be included/brought back into income such as, deposits, unclaimed

wages (longer than 12 Mo.), unclaimed sales allowances, and rebate to customers who can’t be

located.

10. Determine the degree of verification of the balances by the independent external auditor;

11. Confirm the balances of the major individual creditor accounts, either to monthly statements of

account or directly with the supplier;

12. Review the long outstanding balances owing to specific creditors, and supporting correspondence

between the taxpayer and the creditor, to determine the validity and reason for non-payment (i.e.

goods returned for credit but not recorded, payment dispute etc.). Pay particular attention to these

accounts if the creditor is a VAT supplier. Confirm with the ERCA VAT system that the creditor

is a valid VAT registrant).

13. Identify the trade accounts for the parent or associated company which will require subsequent

examination during the tests of purchases and expenses;

14. Identify non-trade debts that may represent advances to shareholders and, if so, review the terms,

accounting treatment, business and personal income tax implications etc;

LOANS PAYABLE

1. Verify the transactions that have given rise to new loan liabilities during the period under audit, or

previous periods if warranted. State the source of the funds, purpose of the loan, actual utilization

of the funds, terms of repayment and security pledged;

2. Confirm the accuracy of the deduction for interest paid in accordance with Article 21(e) of the

Income Tax Proclamation and supporting Regulation 10. Confirm that the agreement does not

include other charges that are designed to circumvent the limitation on interest deductibility.

3. With respect to interest paid on loans from shareholders, confirm those taxpayers has compiled

with the provisions of Article 21(3).

4. Review the details of loan agreements to determine if there are provisions related to share

acquisitions, transfer of management or voting control, and related business transactions at

preferential prices which may have income tax or VAT implications.

OTHER LIABILITIES

1. The auditor should test other liabilities indicated in the books of account, financial statements and

tax declaration that may lead to further audit tests, such as the following:

Reserves set up to cover such matters as the expected costs of services to be provided under

product warranties or completed contracts; disputes with customer over product quality;

legal actions lodged against the taxpayer, returnable packaging expected not to be

Page 25

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

returned;

Accrued wages or bonuses to key shareholders and management personnel for which

expenses deductions have been claimed. Confirm that the withholding tax on employment

income has been deducted. Since the recipient will need to declare the income in the

current year, even if not actually paid, the auditor should notify the respective

City/Regional tax authority for consideration of the income aggregating provision.

ACCOUNTS PAYABLE & OTHER LIABILITIESTax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

DTA/WP/010

Page 26

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR EXPENSE

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions Completeness

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working

paper Reference

Action Required-Confirm that the taxpayer’s claim for expenses deducted in computing taxable business

income comply with the provisions of Articles 20 and 21 of the Income Tax Proclamation and the supporting

Regulations 9 to 11 inclusive.

1. Identify large expenditures for repairs, rebuilding, renovations, refurbishment and other expenditures

that may require review as to classification as expenditure or as capital asset item;

2. Examine the wage records for payments to company shareholders, officials and family members,

including accrued bonuses to determine if disallowance of a portion of the expenses are warranted in

accordance with Regulation 8 (6),(7) and (8). Regulation 8(6) relates to the transaction with the foreign

parent, which is also referred to in the separate Audit Inter-Company Transactions and Tax Accounting

Treatment;

3. Confirm that the taxpayer is accruing expenses in the correct taxation year with respect to purchases of

service that apply to more than one taxation year-i.e. Insurance converge; contracts for services etc;

4. Confirm that the taxpayer’s expense claim for commission paid for services are deductible in

accordance with Regulation 8(5);

5. Confirm that expense deduction for “Representation Allowance” are allowable within the interpretation

of Article 21 (1) (i), Regulation 9(2) and the directive issue by the Ministry of Revenue.

6. Identify the purchases of goods or services that could be for the personal benefit of the shareholders or

officials of the company, such as building materials, furniture, items of personal adornment etc. Test the

delivery slips to support the purchase and physically inspect the goods where warranted;

7. Confirm that the taxpayer has taken all of the actions required to collect accounts receivable that are

being written-off as bad debts, in accordance with Article 25 of the Income Tax Proclamation;

8. Analyze the expenses incurred for legal costs to determine the nature of the case; establish the relation

Page 27

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR EXPENSE

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

to reserves established to provide for possible losses which have been deducted for tax purposes;

identify lawsuits that are not business-related and therefore not deductible; losses which will be covered

by insurance for which the expected realization should be offset against the legal costs/loss provisions;

identify cases which have been settled in the taxpayer’s favors and the accounting for the proceeds for

income declaration purposes etc;

9. With respect to payments made in cash to suppliers, not supported by invoices, request the taxpayer to

provide full information with respect to the name and address of the supplier, the nature and total value

of goods and/or services supplied. If the taxpayer fails to comply, as required by the tax Proclamations,

advise the taxpayer of the criminal offence for obstruction of an officer and the penalties provided for by

Article 98 of the Income Tax Proclamation;

10. Determine if the taxpayer has received an insurance settlement for goods lost, stolen or for other reasons

and confirm that VAT has been paid on the proceeds (if VAT taxable goods) and that the proceeds have

been included in the calculation of taxable income.

Advertisement expense

1. Reconcile account to return

2. If account contains expenditures for gifts/entertainment review for compliance.

3. Scrutinize account for evidence of advertising in political journals, magazines etc.

4. Determine if account contains items of a capital nature such as catalogues that are used over period of years.

5. Scrutinize the account and note any large or unusual items.

6. Test check vouchers on a selected basis depending upon materiality of account and amount. Test check should be expanded dependent upon initial results.

7. Journal entries of a significant nature should be noted and their correctness established.

8. A review should be made of the account to determine that all monthly entries are posted.

9. Review account for reversal of prior year accruals and correctness of current year accruals.

10. Follow up adjustments that originate as a result of prior examiner’s report.

Page 28

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR EXPENSE

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

BAD DEBT EXPENSE

1. Obtain schedule or list of company’s actual bad debt write-off

2. Trace entries on this schedule to debit entries in general ledger account.

3. Ask the company what factors are used to determine when an account is uncollectible.

4. Request and review customers’ files; what are the indications of an uncollectible account? What steps did the company take to collect the debt?

5. Request and review account receivable subsidiary ledger; Is there a credit entry to write-off? Have subsequent sales been made to the same customer? How long was the debt outstanding before it was written off?

6. Verify that amount was previously included in sales. Trace accounts receivable in customer ledger from accounts receivable ledger to sales journal.

7. If bad debt originated from loan (vs. sale) verify that company loaned the money. Trace to cancelled check or receipt for cash. Determine the business purpose for the loan.

8. Was there subsequent collection? Ask company about reviewing credit entries in the

allowance account. Was it brought back into income? Frequent recoveries means

write-off of bad debt happened too fast.

9. If the bad debt allowance method is used, verify the allowance by comparing it with

past historical percentages of actual writer-offs.

Prepaid Expenses

1. Confirm that the taxpayer accounts for the inventories of operating supplies, repair parts, consumables

Page 29

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

AUDIT PROGRAM FOR EXPENSE

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

and other articles as assets rather than treating the total expenditure as deductible expenses for the year;

2. Confirm that the taxpayer’s accounting for expenditures which cover a period longer than the taxation

year, such as insurance, provide for prorating over the periods;

3. Confirm that refundable security deposits (utilities) or retainers for services (legal, computer maintenance

etc.) are treated as assets for accounting and tax purposes.

Rent Expense

1. Reconcile account to return.

2. Review account & determine reason for fluctuations

3. Review originals and obtain copies of lease agreement and pertinent information.

4. Examine Lease-Purchase agreements & determine if correctly reflected.

5. Review account for cancellation of lease agreement.

6. Determine the reasonableness of rent paid to related entities.

7. Determine the accuracy of accruals.

8. Scrutinize the account and note any large or unusual items.

9. Test check vouchers on a selected basis depending upon maturity of account and amount. Test check

should be expanded dependent upon initial results.

10. Journal entries of a significant nature should be noted & their correctness established.

11. A review should be made of the account to determine that all monthly entries are

posted.

12. Review account for reversal of prior year accruals and correctness of current year

accruals. Follow up adjustments that originate as a result of prior auditor’s report

Page 30

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

COST OF EXPENSETax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

Page 31

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/011

AUDIT PROGRAM FOR INVESTMENT

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions Completeness

Audit Steps: (Document audit steps taken or to be taken.)Prepared by Working

paper Reference

The auditor should verify the taxpayers accounting practices with respect to investments, particularly with respect to:

1. The treatment of profits or losses on disposals; 2. Management or ownership control of a subsidiary or branch for which operating results

should be consolidated for tax purposes or for which non-arms length transactions should be audited for tax implications. Determine the extent of the shareholdings in other companies and ascertain if the taxpayer exercises management or voting control. Review minutes of director/shareholders meetings and contractual agreements with respect to the acquisition. Determine the extent of inter-company business transactions, including the provision for management fees that may need to be accrued as income if payment is not made;

3. Reconcile the values of investments recorded in the books of account/general ledger with the financial statements and the tax declaration. Not if the taxpayer has claimed deduction for reserves or write-downs in the realizable value of the investment, which would be disallowed as a deduction for tax purposes;

4. Determine the extent of verification of the investments by the independent external auditor; 5. The timing of the recognition of income. Review the investment instruments with respect to

dividends, interest to ensure that the income has been taken in to account, either on a cash or accrual basis by the taxpayer;

6. Ascertain if the investments have been pledged as security for loans to the taxpayer’s business or for personal loans of the executives. The latter may be a factor if the ERCA wishes to attach or seize assets to effect the payment of tax arrears and to pursue the executives for payment equivalent to the value of the investments pledged.

Page 32

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

InvestmentTax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

Page 33

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/012

AUDIT PROGRAM FOR SHAREHOLDER’S EQUITY

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working paper

Reference

1. Review the Articles of Incorporation and subsequent amendments to determine the scope of the authorized activities of the company, authorized capital stock from the standpoint of classification, number authorized, voting rights, preference as to dividend payment or distribution on wind-up, convertibility of preference shares, voting trusts and the like.

2. Confirm the accuracy of the Capital Stock Authorized and Issued reported in the books of account, financial statements and tax declarations;

3. Determine the ownership control of the corporation and holdings by related companies. 4. If the ownership control has changes during the period, review the transaction to

determine if the Loss Carry Forward provisions of Article 28 of the Income Tax Proclamation have been correctly applied;

5. Determine if the major shareholders have pledged personal shareholdings as security for loans, which could affect ownership control or dissolution of the business in the event of default, leaving unpaid tax liabilities;

6. With respect to the issuance of new capital stock, determine the names of the investors, address and, if warranted the source of the funds used for investment; with respect to investment from overseas, confirm that foreign exchange regulations have been complied with and the source of the funds;

7. Determine if the investors are nominees of other parties, identify the latter, and determine if subsequent business transactions give rise possible income tax implications (transfer pricing, money laundering etc.)

8. Determine if the funds have been invested in the firm, as contributed surplus, rather than stock issues, by the controlling members of a family-owned PLC. Determine the source of the funds;

9. Determine if contributed surplus actually represent business transactions that should be taken into taxable income and taxed accordingly;

10. Confirm that the taxpayer has withheld 10% tax on dividend payments, and has remitted the amounts to the ERCA, in accordance with Articles 34 and Article 67 of the Income Tax Proclamation. Confirm that the taxpayer treats the dividends as non-deductible expenses in accordance with Article 21 (d) of the Proclamation.

Page 34

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

11. Review any adjustments to the Retained Earnings that could indicate income that has not been included in the calculation of taxable income. Conversely, if the charge to Retained Earnings has not been deducted in the calculation of taxable income, confirm the correct accounting and tax treatment.

SHAREHOLDER’S EQUITY Tax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

Page 35

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/013

AUDIT PROGRAM FOR INCOME/REVENUE

Tax Payer Name: Auditor:

TIN:

Tax Year Date:

Audit Objectives F/st. Assertions Completeness

Audit Steps: (Document audit steps taken or to be taken.)

Prepared by Working paper Referen

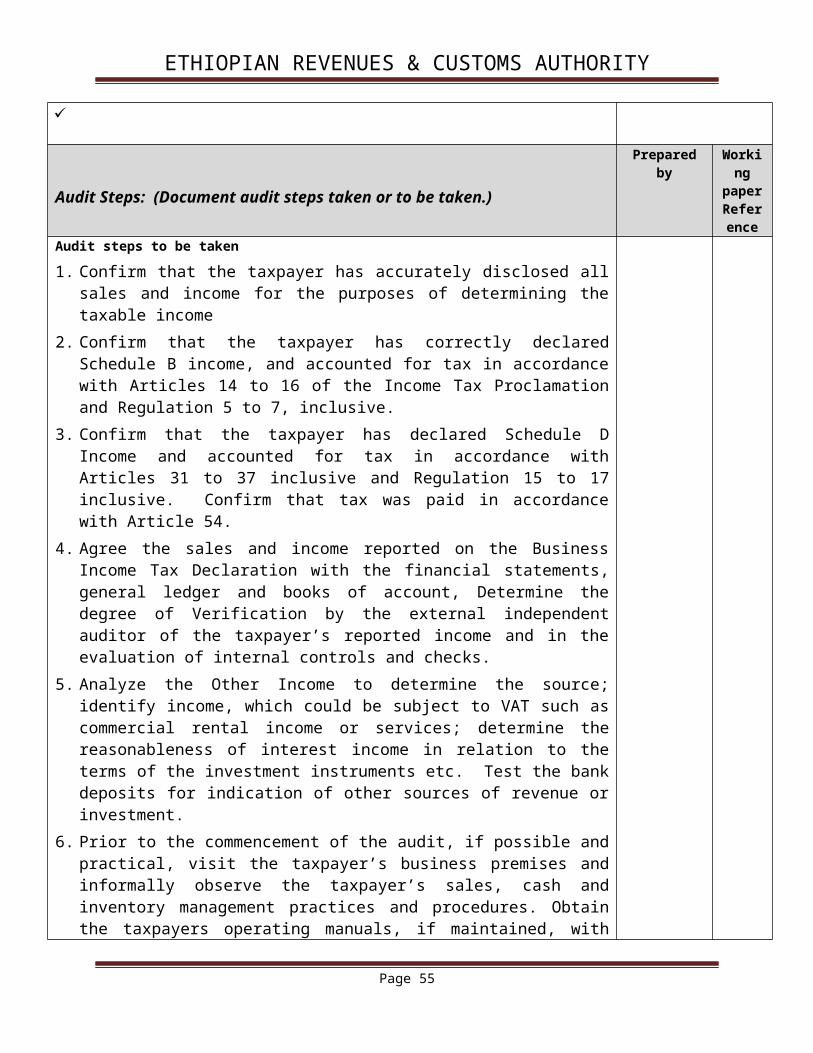

ceAudit steps to be taken

1. Confirm that the taxpayer has accurately disclosed all sales and income for the purposes of determining the taxable income

2. Confirm that the taxpayer has correctly declared Schedule B income, and accounted for tax in accordance with Articles 14 to 16 of the Income Tax Proclamation and Regulation 5 to 7, inclusive.

3. Confirm that the taxpayer has declared Schedule D Income and accounted for tax in accordance with Articles 31 to 37 inclusive and Regulation 15 to 17 inclusive. Confirm that tax was paid in accordance with Article 54.

4. Agree the sales and income reported on the Business Income Tax Declaration with the financial statements, general ledger and books of account, Determine the degree of Verification by the external independent auditor of the taxpayer’s reported income and in the evaluation of internal controls and checks.

5. Analyze the Other Income to determine the source; identify income, which could be subject to VAT such as commercial rental income or services; determine the reasonableness of interest income in relation to the terms of the investment instruments etc. Test the bank deposits for indication of other sources of revenue or investment.

6. Prior to the commencement of the audit, if possible and practical, visit the taxpayer’s business premises and informally observe the taxpayer’s sales, cash and inventory management practices and procedures. Obtain the taxpayers operating manuals, if maintained, with respect to sales and returns. Determine the internal controls and checks that exist over the recording of sales transactions i.e. pre-numbered, sequential invoices and credit notes approved by the ERCA cash

Page 36

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

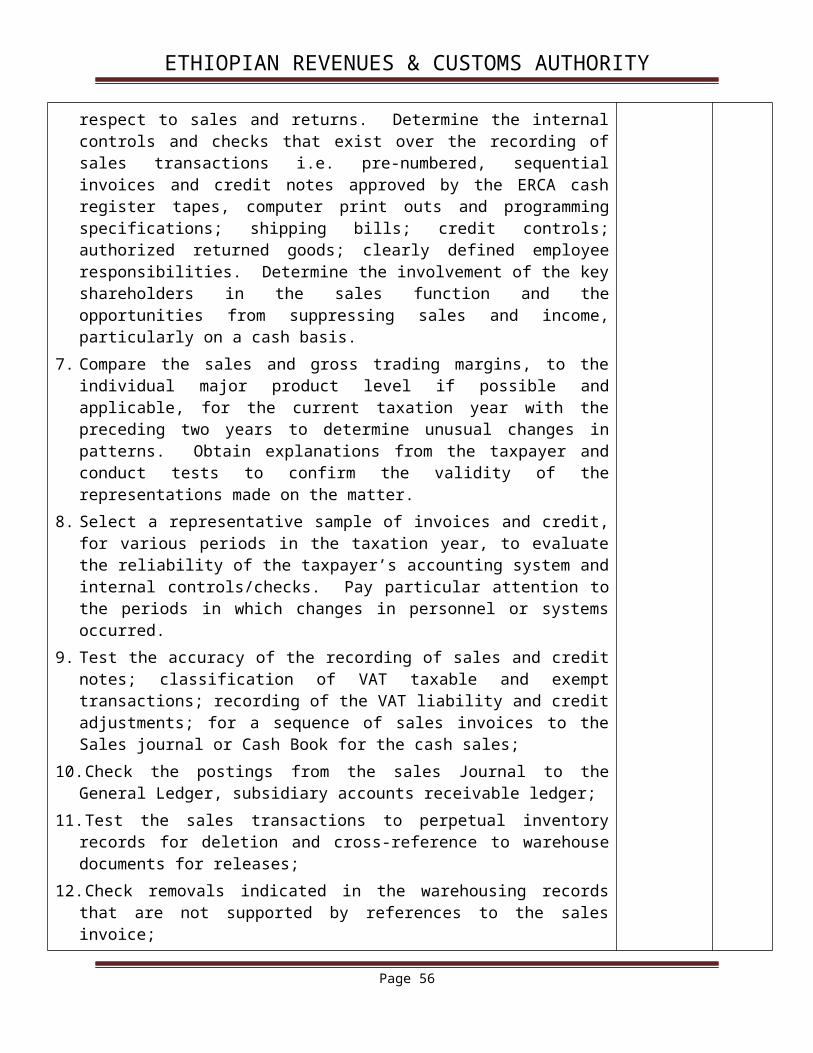

register tapes, computer print outs and programming specifications; shipping bills; credit controls; authorized returned goods; clearly defined employee responsibilities. Determine the involvement of the key shareholders in the sales function and the opportunities from suppressing sales and income, particularly on a cash basis.

7. Compare the sales and gross trading margins, to the individual major product level if possible and applicable, for the current taxation year with the preceding two years to determine unusual changes in patterns. Obtain explanations from the taxpayer and conduct tests to confirm the validity of the representations made on the matter.

8. Select a representative sample of invoices and credit, for various periods in the taxation year, to evaluate the reliability of the taxpayer’s accounting system and internal controls/checks. Pay particular attention to the periods in which changes in personnel or systems occurred.

9. Test the accuracy of the recording of sales and credit notes; classification of VAT taxable and exempt transactions; recording of the VAT liability and credit adjustments; for a sequence of sales invoices to the Sales journal or Cash Book for the cash sales;

10. Check the postings from the sales Journal to the General Ledger, subsidiary accounts receivable ledger;

11. Test the sales transactions to perpetual inventory records for deletion and cross-reference to warehouse documents for releases;

12. Check removals indicated in the warehousing records that are not supported by references to the sales invoice;

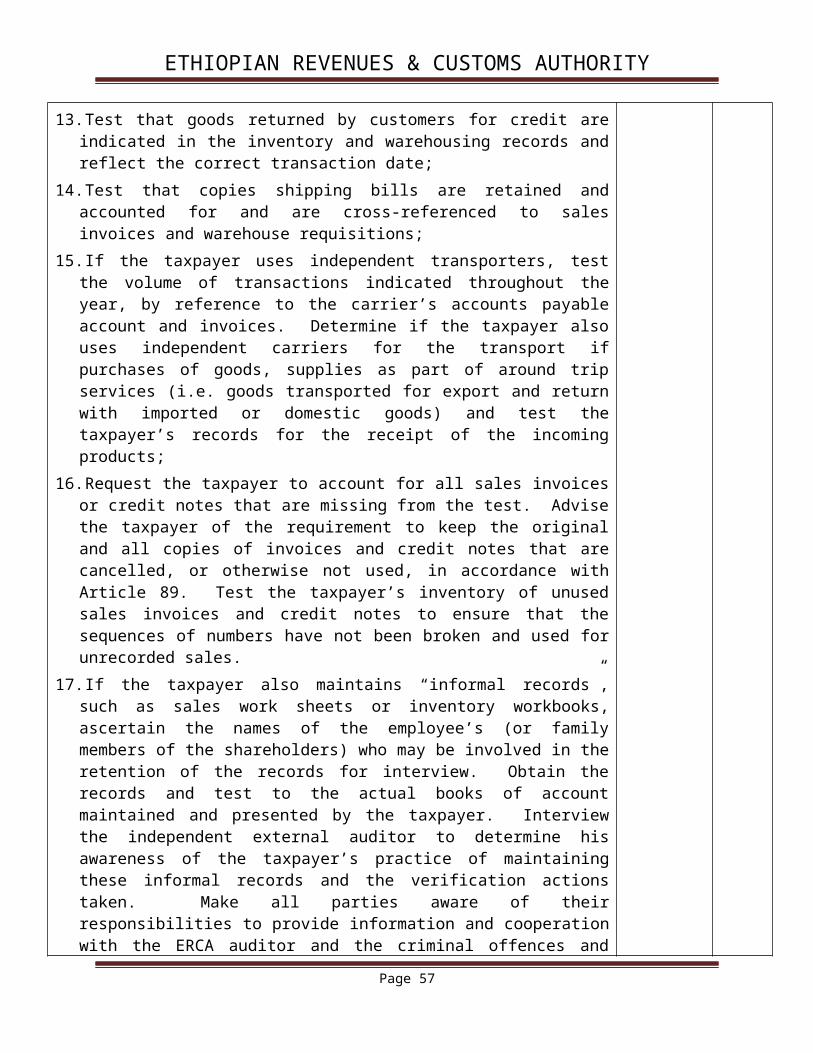

13. Test that goods returned by customers for credit are indicated in the inventory and warehousing records and reflect the correct transaction date;

14. Test that copies shipping bills are retained and accounted for and are cross-referenced to sales invoices and warehouse requisitions;

15. If the taxpayer uses independent transporters, test the volume of transactions indicated throughout the year, by reference to the carrier’s accounts payable account and invoices. Determine if the taxpayer also uses independent carriers for the transport if purchases of goods, supplies as part of around trip services (i.e. goods transported for export and return with imported or domestic goods) and test the taxpayer’s records for the receipt of the incoming products;

16. Request the taxpayer to account for all sales invoices or credit notes that are missing from the test. Advise the taxpayer of the requirement to keep the original and all copies of invoices and credit notes that are cancelled, or otherwise not used, in accordance with Article 89. Test the taxpayer’s inventory of unused sales invoices and credit notes to ensure that the sequences of numbers have not been broken and used for unrecorded sales.

17. If the taxpayer also maintains “informal records”, such as sales work sheets or inventory workbooks, ascertain the names of the employee’s (or family members of the shareholders) who may be involved in the retention of the records for

Page 37

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

interview. Obtain the records and test to the actual books of account maintained and presented by the taxpayer. Interview the independent external auditor to determine his awareness of the taxpayer’s practice of maintaining these informal records and the verification actions taken. Make all parties aware of their responsibilities to provide information and cooperation with the ERCA auditor and the criminal offences and penalties provided by Articles 97, 98, 101 and 102 of the Income tax Proclamation, among others.

18. Test the sales invoices and shipping bills, paying particular attention to the transactions that are close to the month-end or year –end, to determine if the taxpayer is correctly complying with the Article 11 of the VAT Proclamation-Time of Supply. Confirm that the taxpayer is recording the timing of sales for income tax purposes in the current taxation year, (where ownership or title to the goods have been transferred to the customer, or the taxable services have been rendered), even though the VAT liability may correctly be accounted for in the next taxation year. Test the inventory records of finished goods and cross-reference to sales invoices and shipping bills for transactions straddling the year-end date (i.e. three days before and after the year-end date) to ensure that the income has been reported in the appropriate taxation year.

19. In cases where the suppression of sales is suspected and the taxpayer stores goods for resale offsite, determine the records maintained to record the movement of the goods from storage to the sales outlet, or to the customer, and the taxpayer’s personnel involved in the process. Estimate the volumes of the sales volume recorded in the books of account and the sale value of the estimated inventory on hand in the sales outlet. Request the taxpayer to provide the advertised sale price, supplier’s cost supported by invoices/import entries and to explain variances.

20. In cases where the suppression of sales is suspected, identify a representative number of domestic suppliers and discuss, with the team leader, the possibility of verifying the volume of business transaction by direct review of the supplier’s records. If the latter action proceeds, review the supplier’s records for other indications of the volume of transactions and the eventual sales value. (For example, producers of beer, alcohol, tobacco, electronic and clothing products maintain extensive records of transactions by their customers, and of volumes in the general marketplace, in view of the completion form contraband goods.). The information can also be used to determine average mark-ups in the marketplace in the event the ERCA auditor has to prepare an estimated assessment on the taxpayer.

21. If the suspected suppression of sales by the taxpayer involves imported goods, obtain summary of the taxpayer’s imports from the Ethiopian Customs Authority If the Imported goods are of a nature that the taxpayer contends that the VAT paid on the import value exceeds or approximates the VAT liability on sales, due to ERCA valuations:

Identify the types of specific goods and the tariff classification; Obtain the value of importations, the differences in valuation and the VAT

assessed from asiycuda++

Page 38

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

Request the taxpayer to justify the quantities and values of goods in the opening and closing and the sales made during the period under review;

Confirm the invoiced price from the foreign suppliers involved, and review foreign exchange transaction documentation;

Determine the volume of the goods subject to ERCA valuation uplift in relation to the total sales of domestic and imported goods by the taxpayer;

confirm the average mark-up made by the taxpayer on sales of the goods subject to the ERCA valuation uplift and of the other goods sold by the taxpayer;

Determine the reasonableness of the sales volume, trading profit and VAT liabilities/credits declared by the taxpayer.

22. Review the accounts receivable subsidiary ledger to identify customers with credit balances, which may indicate sales or services rendered that have not been invoiced; installment sales not correctly recorded; income from other sources, such as rental income, customer deposits for large orders that are subject to progress billings etc.

23. For large contracts involving the supply of goods/services over a period of time, and multiple payments, review the contract for payment arrangements; confirm the work completed and in progress indicated in the taxpayer’s records and the certifications by an independent party. Confirm that the taxpayer has correctly recognized come in accordance with Article 63 of the Income Tax Proclamation and VAT in accordance with Article 11 of the VAT Proclamation.

24. With respect to the losses incurred by the taxpayers on long-term contract, confirm that the income tax accounting complies with the provisions of Article 28 and Article 63 of the Income Tax Proclamation and supporting Regulation 12.

25. Reconcile books to the return.26. Determine that nontaxable income is excluded is correct.27. Verify year-end accruals.28. Review subsidiary records and detail trial balance for interest bearing accounts.

Trace to interest income-assure for proper accruals. Compare to notes; if any Determine that nontaxable income excluded is correct. Cross-reference with investment account.

29. Consider possibility of interest on foreign bank accounts, foreign securities, tax refunds escrow accounts, etc.

30. Cross reference income accounts with investment accounts. Inquire into any investments for existence of dividends, rate of return, dispositions etc. and trace back to the return.

31. Consider whether company is properly reporting all miscellaneous income: scrap sales, sales to employees.

Page 39

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

INCOME/REVENUETax Period Per Return Per Exam Adjustment

Conclusion: (Reflects the final determination on the issue.)

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Reviewed and approved by Date

Page 40

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/014

13.2.2. STOCK SHEET

Company/Tax payer nameStock Count.

As at 21/04/03 E.C

Serial No. Item Description

unit of measur

e

Quantity

shortage/overage

Unit cost

Total cost Remark

as per physical count

as per stock card

Total

Store keeper(custodian ) Counted by Witnesses Name/sig/date Name/sig/date Name/sig/date

Page 41

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/015

13.2.3. QUERY SHEET

Tax payer Name:-----------------------------------------TIN No.-----------------------------------Audit year(s)-------------------------------- Prepared by: ----------------------------

Date:------------------------

No. Queries Dispositions Initials & Date

Page 42

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/016

13.2.4. TIME SHEET

Tax payer Name:---------------------------------------------------TIN No.-----------------------------------Audit year(s)--------------------------------Month_____________________

Work doneDays Total

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Audit preparation Audit planning Interview Total

Prepared by_______________ Date___________ Approved by__________________ Date________________

Work doneDays Total

16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 Total

Prepared by_______________ Date___________ Approved by__________________ Date________________

Page 43

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/017

13.2.5. INDIVIDUAL ACCOUNTS WORKING PAPERS

ACCOUNT NAME- ACCOUNT NO.-

Date Reference document No

DescriptionAmount

RemarkDr. Cr.

Page 44

Taxpayer Name: Auditor:

TIN:

Date:

Tax Year:

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

ACCOUNT NAME- ACCOUNT NO.-

Findings:

Conclusion

Based on the procedures performed and the results obtained, it is my opinion that the objectives listed in this audit

program have been achieved.

Performed by Date

Page 45

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

Reviewed and approved by Date

13.3. REPORTING PHASE

DTA/WP/018

13.3.1. REPORT FORMAT (BIT)

COMPANY/TAX PAYER NAME BUSINESS PROFIT TAX AUDIT REPORT

FOR THE YEARS 20XX - 20XY E.C

TIN: ____________________

VAT No._________________

Address: _____________ Region: _________

Sub city/Woreda/_____________ House No ____________ Tele.No____________

Background

X-PLC has been established on ____________E.C with a register paid up capital of birr

____________ consisting of _______shares with par contributed by _____________ share

holders. Later on Sep 30, 19xx the company increase its capital to ___________ and still the

company engaged in the _______________________.The Company has been registered for

VAT on December 23, 1995 E.C.

Audit Objective

The audit objective is to verify the company’s book of accounts, records and other related

documents so as to ascertain the taxpayer’s compliance with existing tax laws and regulations.

Audit Scope

The audit covers from 20xx to 20xy tax periods only.

Methodology

As the taxpayer’s business transaction is wide and bulky and making a detail examination of all

accounts is infeasible, we conduct our audit on a test basis. We used ___________________

sampling methods when selecting accounts for test and determining our sample size.

Documents Verified

We have examined the company’s book of accounts, records and other documents that we

considered relevant to the assessment of tax returns. Below are some of documents we have

verified in the course of audit.

Page 46

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

VAT and profit tax declarations

Financial statements

General ledger, Accounts Receivable ledger, fixed asset Subsidiary ledger etc….

General Journal, Sales Journal, Cash receipt Journal, Purchase/or expenditure/ Journal

etc…

Other source documents that support those financial statements.

Findings, Adjustments and Justification

During our audit engagement we have observed that the taxpayer has maintained its financial and

other aspects in line with Ethiopian tax laws except the adjustments listed below. We have added

back the adjustments to the taxpayer’s taxable income to determine its tax liability

1. Undeclared sales: - It is an Income recorded as unearned but service is delivered to

customer, debit balance of unearned income that must be credited by sales unless

otherwise the sales agreement is canceled, un posted sales to the general ledger,

understated sales based on undeclared purchase and understated purchase is adjusted to

taxable income of Birr _______, _______, and ______ for the tax years of ______, ____

and _____ respectively.

2. Over stated Cost of goods sold :- the Company over states the cost of goods sold by

recording of overage of stock, unofficial receipt, double and over recording of cost is as

adjusted to taxable income of Birr _______, _______, and ______ for the tax years of

______ , ____ and _____ respectively.

3. No source document : when we are examining the company’s disbursements & cost, we

come across with entries that are not properly backed with reliable evidence, and we are

not sure it is really incurred then finally adjusted to taxable income of Birr _______,

_______, and ______ for the tax years of ______ , ____ and _____ respectively.

4. Unofficial receipt : - It is transaction entries supported with illegal invoices as per directive

no.12/1996 and 28/2001 expense incurred without official receipt is adjusted to taxable

income of Birr _______, _______, and ______ for the tax years of ______ , ____ and

_____ respectively.

Page 47

DESCRIPTIONS 20xx 20xy 20xz TOTAL

Declare taxable income as per F/StatementAdd:-Adjustments

Undeclare income/Sales

Disallowed overstated cost

No source Document

Unofficial Receipts

Tota Adjustments

Total Adjusted taxable income

Tax(30%)

Payments: - by Receipt (a)

- Withholding tax claimed (b)

- Refund /c/

Total Payments (a+b-c)

Balance due

Interest

Penalties

Total Tax, Interest and Penalties

BUSINESS PROFIT TAX COMPUTATION FOR THE YEARS FROM 20xx -20xz E.C

COMPANY NAME

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

Summary of Findings, AdjustmentCOMPANY/TAX PAYER NAME

BUSINESS PROFIT TAX COMPUTATIONFOR THE YEARS FROM HAMLE, 20xx – 20xz

Prepared by-_______________ Verified by- ____________ Approved by-______________

Prepared by-_______________ Verified by- ___________ Approved by-_______________Signature _______________ Signature _____________ Signature ________________Date __________________ Date _____________ Date __________________

Page 48

ETHIOPIAN REVENUES & CUSTOMS AUTHORITY

DTA/WP/019

REPORT FORMAT (VAT)

COMPANY/TAX PAYER NAMEVALUE ADDED TAX AUDIT REPORT

FOR THE YEARS 20XX - 20XY E.CTIN: ____________________

VAT No._________________

Address: _____________ Region: _________