Embed Size (px)

Citation preview

Global ShortsU.S. AutomotiveGentex Corporation (GNTX US)

Beware: Objects Are Smaller Than They Appear

Gentex seems to be overstating profit. If profit is overstated, the excess may be tucked into the mysterious “other assets” line on the balance sheet. Meanwhile, the chairman has been richly compensated with the highly valued stock.

The technology in Gentex mirrors is relatively simple and commoditized, and we are highly skeptical of claimed margins that beat those of everyone else in the industry. We are equally skeptical of Gentex’s capex. Costs look understated and capex overstated. The company leaves a long trail of discontinued technologies with no associated write-offs. We suspect this is the plug for profits that are not actually there.

The “mirror as a technology platform” that forms Gentex’s strongest argument for its competitive advantage is challenged by increasing penetration of LCD screens in cars.

We believe more realistic margins for these mirrors are about 20%. Applying that assumption, we value the company on a DCF basis at USD 9.10 and recommend that owners SELL.

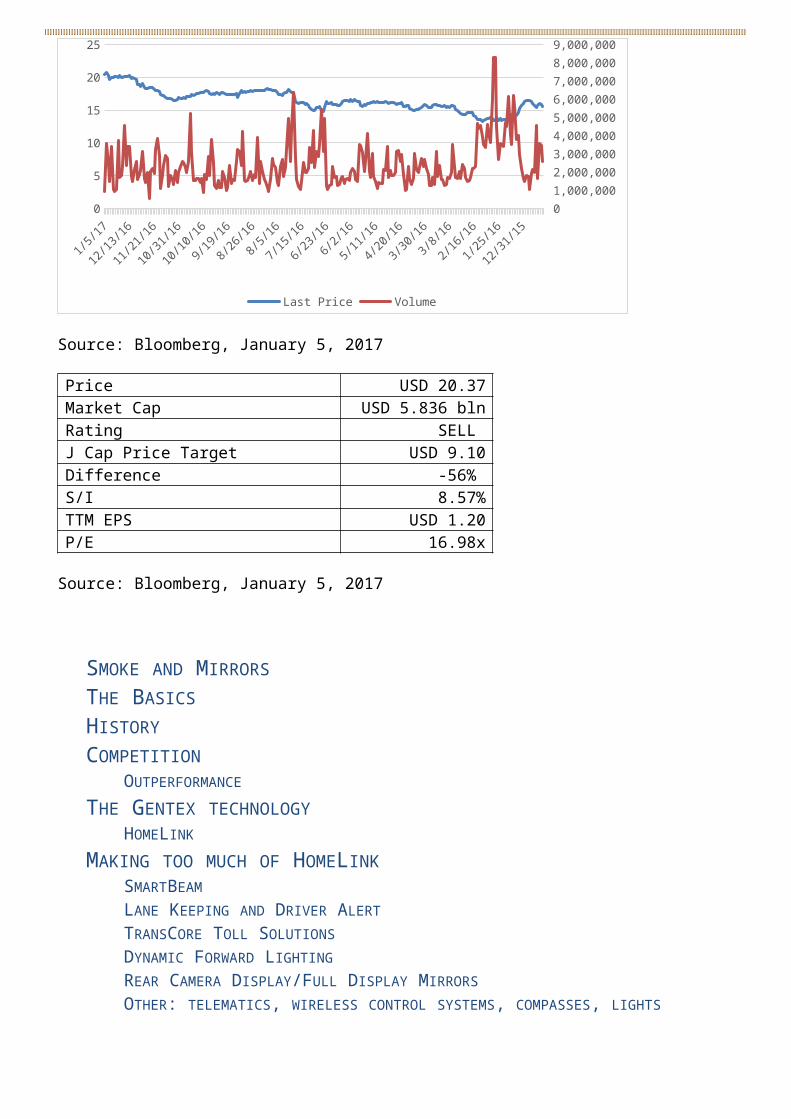

Chart 1. Gentex Price and Volume (USD, average shares/day)

12/14/1

51/1

/16

1/19/16

2/6/16

2/24/16

3/13/16

3/31/16

4/18/16

5/6/16

5/24/16

6/11/16

6/29/16

7/17/16

8/4/16

8/22/16

9/9/16

9/27/16

10/15/1

6

11/2/16

11/20/1

6

12/8/16

12/26/1

60

5

10

15

20

25

01,000,0002,000,0003,000,0004,000,0005,000,0006,000,0007,000,0008,000,0009,000,000

Last Price Volume

Source: Bloomberg, January 5, 2017

Price USD 20.37Market Cap USD 5.836 bln

1

Disclaimers: Last Oct 7, 2012

Rating SELL J Cap Price Target USD 9.10Difference -56% S/I 8.57%TTM EPS USD 1.20P/E 16.98x

Source: Bloomberg, January 5, 2017

SMOKE AND MIRRORSTHE BASICSHISTORYCOMPETITION

OUTPERFORMANCETHE GENTEX TECHNOLOGY

HOMELINKMAKING TOO MUCH OF HOMELINK

SMARTBEAMLANE KEEPING AND DRIVER ALERTTRANSCORE TOLL SOLUTIONSDYNAMIC FORWARD LIGHTINGREAR CAMERA DISPLAY/FULL DISPLAY MIRRORSOTHER: TELEMATICS, WIRELESS CONTROL SYSTEMS, COMPASSES, LIGHTS

BREAKING DOWN THE COMPONENTSTHE MARGINSTHE CAPEX BLOWOUT

THE SPIKE: 1996DEPRECIATIONJUST A SLIP?

MECHANISMSHOW THE BUSINESS WORKS

SALES CHANNELSAFTERMARKET

REGIONSTHE CHALLENGE FROM CAMERASBLOATED CAPEX

DISTILLED WATERSEMICONDUCTORSCHINA FACILITYGERMANYORCAALSMICROPHONES

THE CHINA PLAN

2

Disclaimers: Last Oct 7, 2012

AUDIT FEESTHE ULTIMATE TELL: THE CASHORIGINAL SIN?

SEC CORRESPONDENCEWHY?CATALYSTSCOMPANY RESPONSEVALUATIONRISKS

3

Disclaimers: Last Oct 7, 2012

Smoke and MirrorsAnne Stevenson-Yang

The BasicsGentex makes high-end mirrors for automobiles. While much larger companies in this cutthroat industry struggle to make gross margins of 18% or 19%, Gentex regularly reports margins of around 40%. The company attributes this success to its commanding share of the market in auto-dimming mirrors. Auto-dimming is the electro-chemical process that enables mirrors to darken automatically at night and avoid the glare from oncoming headlights that can blind the driver. Auto-dimming has been around for 30 years and is a mature technology, and several other components companies also have auto-dimming technology—one of them, Magna, pretty much exactly the same technology--because Magna’s Donnelley subsidiary helped develop it.

Gentex itself admits that the auto-dimming mirrors are technological Trojan horses with just so-so gross margins, but they are the platforms onto which Gentex packs other electronics, such as a remote control device to open garage doors, turning signals and compasses, a sensor that dims high beams, and other components. Gentex says that half of its mirrors are sold with these additional features, many of which command very high margins.

The company’s secret sauce is complete vertical integration that enables Gentex to exercise maniacal quality control. Gentex says that it designs and manufactures everything from the chemicals used in the layer behind the glass on the mirrors to the semiconductors that drive the lighting components.

Gentex is a happy company that gets positive reviews from employees who post on Glassdoor, with a long-tenured, close-knit staff and a founder and chairman who is highly regarded in the industry and still in control of the company.

This is the company narrative. Our narrative is different. It goes like this:

Gentex margins exceed those of Apple. Gentex reported a 32.1% operating margin in the most recent quarter while Apple reported 25.1%. Gentex argues that it makes a high-technology product. Common sense suggests that Apple has more secret sauce and commands higher price premiums than Gentex. Why the difference? Is Gentex genuinely more high tech or could Gentex be making it up?

Gentex posted questionable numbers when it first listed over-the-counter in 1981. The company then was making fire alarms for mobile homes, and 79% of revenue came from a single, undisclosed customer.

The broker was convicted of securities fraud later that year and fled the United States. This 1994 SEC decision states that Juan Carlos Schlidowski, president of the brokerage, was guilty of manipulating Gentex and other companies’ stock.

The Gentex founder’s company, which sold the original mirror technology to Gentex, was financed by Donnelly Corp., a large auto components company just five miles away from Gentex that had

4

Disclaimers: Last Oct 7, 2012

extensive supply relationships with automakers. Donnelly appears to have retained rights to the technology and at any rate has its own auto-dimming technology. Donnelly, now part of Magna Corp., also has all the added electronics that Gentex says are so profitable. Yet Donnelly has never managed to claim profits remotely approaching those of Gentex.

When companies overstate their profits, they are forced into overstating the value of their balance sheets as a mathematical consequence of the phantom profit. In the case of Gentex, we calculate that capital expenditure is roughly three times that of peers. Yet we believe that only simple printed circuit board design and lamination is required for the electronics portion of the mirrors.

We estimate that the company is profitable but modestly so, and we think the plant and equipment value is likely overstated. The principal catalysts we see on the horizon are SEC action and shareholder demands that Gentex raise its dividend, because we are skeptical that Gentex generates the cash reported.

However, if Gentex is reporting inflated results, as we think it is, the company will need to continue reporting industry-beating growth and trundling the phantom earnings into acquisitions or capex. Where to find untraceable growth? Maybe in the supremely opaque China market, where Gentex plans to sell garage openers, with profits offset by a new acquisition. If any of that happens, we will be watching.

HistoryFred Bauer founded Gentex in Zeeland, Michigan, one of a string of towns along the east side of Lake Michigan in the heart of America’s auto country. Zeeland lies just a few miles down the road from Holland, home to the 80-year-old Donnelly Corp., now a division of Magna, whose USD 32 bln in annual component sales include some part of just about every American car.

Now 72 and still heading Gentex, Bauer appears to be a gifted inventor who in his twenties developed a heat-control switch for furnaces and marketed it through a company he called Simicon. In 1972, he sold Simicon to Robertshaw Controls in Zeeland. After serving for seven years as general manager of Robertshaw’s Simicon division, Bauer formed a partnership called Integrity Design Company, which developed a photoelectric fire detector and, later, a motorized mirror.

He formed Gentex initially to market a fast-reacting fire-alarm system for mobile homes. The company then began to market the adjustable mirrors. It listed in 1981. Total sales in 1980 were USD 4.31 mln, of which the great majority came from intrusion alarms sold via a single direct-sales organization. Gentex became profitable in 1985.

Using the proceeds from the listing, Gentex acquired from Bauer’s company the rights to a motorized night-vision mirror that Bauer had developed with funding from Donnelley.

In 1983, Bauer met Harlan Byker, a research scientist from Battelle Laboratories, who was working on an electro-chemical process for auto-dimming. Believing Gentex could apply the technology to mirrors, Byker joined the company as a research scientist in 1985 and then as vice president for

5

Disclaimers: Last Oct 7, 2012

electrochemical research from 1993. With Byker’s help, Gentex added auto-dimming capability to its motorized mirrors and shipped its first Night Vision Safety (NVS) mirror to Ford Motor Company in 1987. In 1991, the company developed an exterior auto-dimming mirror. By 1993, Gentex was shipping mirrors with headlight control features, compasses, sensors, and interior lights.

Since the early 1990s, Gentex has made steady progress penetrating first the high end then mid-end auto models with this technology that is apparently so desirable and so difficult to replicate that Gentex has margins well over double those of any competitor. Gentex shipped 33 mln auto-dimming units in 2015, representing a 5% increase in interior mirrors and a 37% increase in exterior mirrors and representing a near-90% market share in auto-dimming mirrors. Back in 1995, Donnelley, then the world’s second-largest supplier of mirrors, was shipping just 70,000 auto-dimming mirrors, primarily to Ford, Range Rover, and Jaguar, to Gentex’s 1.8 mln units. Although Magna Donnelly has raised its share of auto-dimming mirrors, Magna sits at a mere 10% of the market.

In 2002, Donnelley merged with Magna International Inc., a Canadian components company, but never expanded its share of auto-dimming mirrors. Like Gentex, Magna also sells automatic garage door openers, Electronic Toll Collection devices, compass and temperature displays, and telematics embedded in the mirrors. Magna’s gross margins are less than half Gentex’s, and Magna also trades at half Gentex’s earnings multiple.

Why is it that a much larger company headquartered very close to Gentex that separately owns all the technologies that Gentex identifies as key to its success and that has relationships with all major automakers around the world, why is it that this company cannot achieve even half the margins that Gentex can? Even though the two have been competing in this segment for 20 years?

CompetitionGentex reports that its competitors include Magna, Samvardhana Motherson Reflective, Murakami Kaimeido Company, Ichikoh Industries, Tokai Rika Company, and Grupo Ficosa International and that it supplies auto-dimming rearview mirrors to “certain of these rearview mirror competitors.” In interviews, we have learned that Gentex and Magna have the same technology, while Murakami and Tokai Ricoh have another, less popular auto-dimming technology that is less cost-competitive. One executive told us that Murakami had mothballed its auto-dimming technology and was purchasing dimming glass from Gentex.

Gentex now ships glass assemblies to a few of these companies, for example, Murakami. Tokai Rika has its own auto-dimming mirrors. In 2015, the company identified a new group of competitors, adding YH America, Inc., BYD Auto Company, Steelmate, Ningbo Kingband, and Beijing Sincode. In China’s electronics markets, dimming mirrors with embedded cameras can be purchased retail for about USD 30. The China market swarms with competitors for this space, something that Gentex readily admits, but Gentex says that no one else has the manufacturing rigor to meet OEM requirements for mass production. The local start-ups come and go.

6

Disclaimers: Last Oct 7, 2012

Maybe. But there is no good reason why mirrors should require a more sophisticated process than, say, airbags, and the advent of new competitors suggests that the technology is not that hard to master.

Outperformance

The auto parts business is a brutal one that has felled many great companies from Delphi to Visteon. The Wisconsin behemoth Johnson Controls restructured and divested its auto components division. Few survive the brutal cost-cutting ways of the big OEMs, which act virtually as monopsonies and hold their supply chain to very tight margins. The most technology-rich of the companies, making drive trains and continuous transmissions and air bags, struggle to make 20% gross margins. Start-up companies may capture a bit more margin, but once they are supplying at volume, no one gets 40%.

Gentex outperforms every single automotive components company in the world and not by just a little—by at least 100%. Of these companies, Denso is a standout in the level of technological input to the components. Denso spends 9% of much higher gross revenue on R&D (Gentex: 5.7%). High-value powertrain control systems make up 36% of revenue, truck refrigeration and air purification systems 31%, and safety systems including four-camera surround vehicle monitoring systems, blind-spot detection, and night vision, 14%--non-trivial technologies.

Autoliv (ALV), whose average margin is 19.5%, principally makes airbags, a complex technology originally developed for heat-seeking missiles in which tiny fractions of seconds in reaction time can make the difference in saving lives. Autoliv also has significant business in “active safety systems” including: “. . . camera-based vision systems, night driving assist, automotive radars, brake controls, positioning systems, electronic control units, and other active safety systems, and passive safety electronic products, such as restraint electronics and crash sensors.” Autoliv, like Gentex, spent 5.7% of revenue on R&D in 2015.

It is hard to understand why mirrors with some added features should offer higher margins than do these clearly higher-tech components.

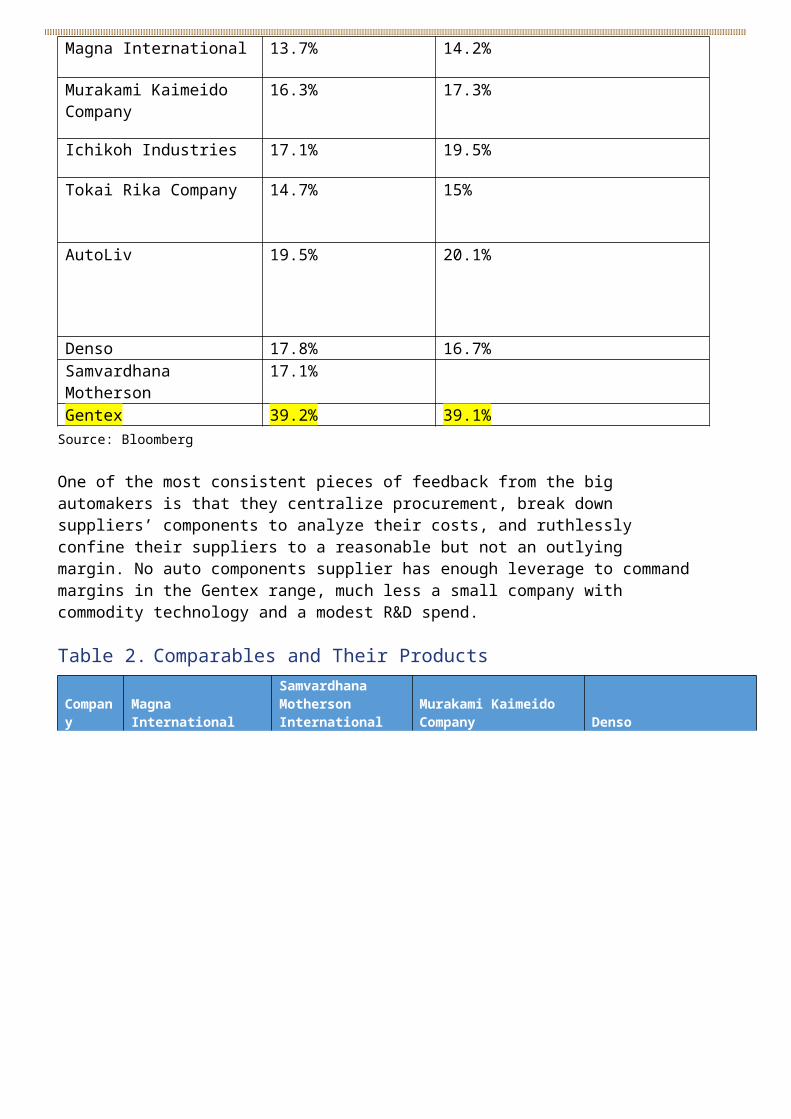

Table 1. Gross Margins 2014-20152014 2015

Magna International 13.7% 14.2%

Murakami Kaimeido Company

16.3% 17.3%

Ichikoh Industries 17.1% 19.5%

Tokai Rika Company 14.7% 15%

7

Disclaimers: Last Oct 7, 2012

AutoLiv 19.5% 20.1%

Denso 17.8% 16.7%Samvardhana Motherson

17.1%

Gentex 39.2% 39.1%Source: BloombergOne of the most consistent pieces of feedback from the big automakers is that they centralize procurement, break down suppliers’ components to analyze their costs, and ruthlessly confine their suppliers to a reasonable but not an outlying margin. No auto components supplier has enough leverage to command margins in the Gentex range, much less a small company with commodity technology and a modest R&D spend.

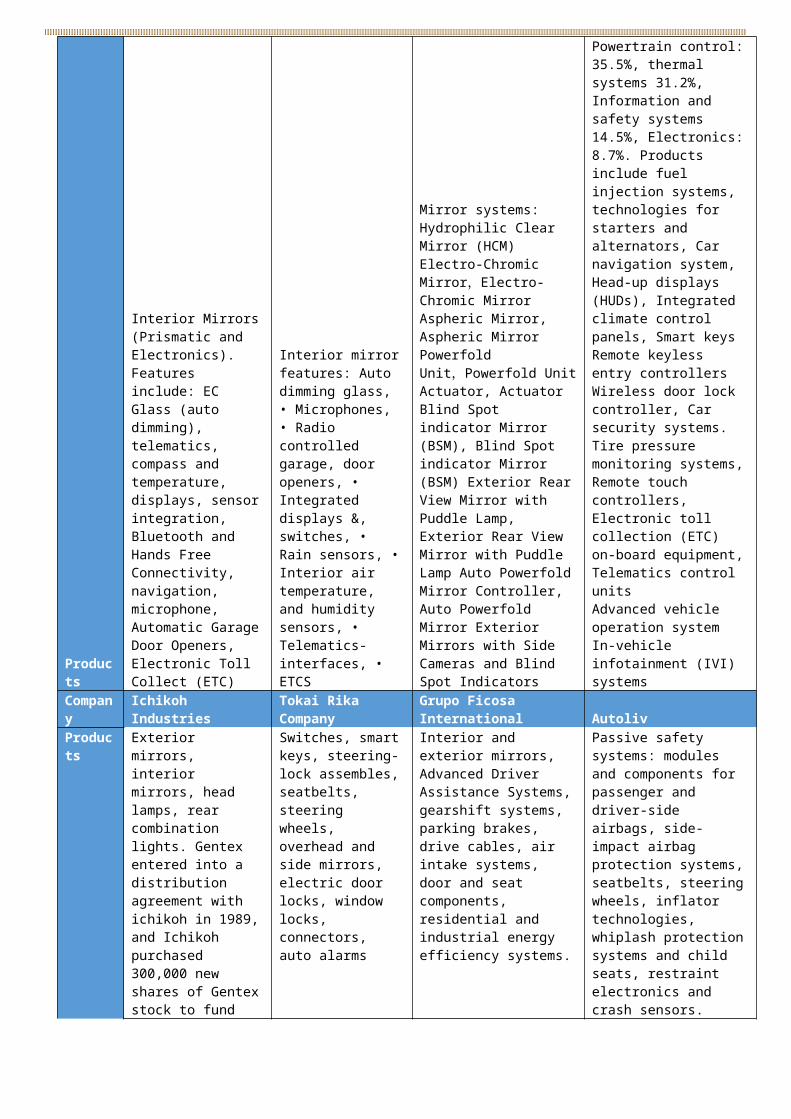

Table 2. Comparables and Their ProductsCompany

Magna International

Samvardhana Motherson International

Murakami Kaimeido Company Denso

Products

Interior Mirrors (Prismatic and Electronics). Features include: EC Glass (auto dimming), telematics, compass and temperature, displays, sensor integration, Bluetooth and Hands Free Connectivity, navigation, microphone, Automatic Garage Door Openers, Electronic Toll Collect (ETC)

Interior mirror features: Auto dimming glass, • Microphones, • Radio controlled garage, door openers, • Integrated displays &, switches, • Rain sensors, • Interior air temperature, and humidity sensors, • Telematics-interfaces, • ETCS

Mirror systems: Hydrophilic Clear Mirror (HCM) Electro-Chromic Mirror,Electro-Chromic Mirror Aspheric Mirror, Aspheric Mirror Powerfold Unit,Powerfold Unit Actuator, Actuator Blind Spot indicator Mirror (BSM), Blind Spot indicator Mirror (BSM) Exterior Rear View Mirror with Puddle Lamp, Exterior Rear View Mirror with Puddle Lamp Auto Powerfold Mirror Controller, Auto Powerfold Mirror Exterior Mirrors with Side Cameras and Blind Spot Indicators

Powertrain control: 35.5%, thermal systems 31.2%, Information and safety systems 14.5%, Electronics: 8.7%. Products include fuel injection systems, technologies for starters and alternators, Car navigation system, Head-up displays (HUDs), Integrated climate control panels, Smart keysRemote keyless entry controllersWireless door lock controller, Car security systems.Tire pressure monitoring systems, Remote touch controllers, Electronic toll collection (ETC) on-board equipment, Telematics control unitsAdvanced vehicle operation systemIn-vehicle infotainment (IVI) systems

Company

Ichikoh Industries

Tokai Rika Company

Grupo Ficosa International Autoliv

8

Disclaimers: Last Oct 7, 2012

Products

Exterior mirrors, interior mirrors, head lamps, rear combination lights. Gentex entered into a distribution agreement with ichikoh in 1989, and Ichikoh purchased 300,000 new shares of Gentex stock to fund the Gentex expansion.

Switches, smart keys, steering-lock assembles, seatbelts, steering wheels, overhead and side mirrors, electric door locks, window locks, connectors, auto alarms

Interior and exterior mirrors, Advanced Driver Assistance Systems, gearshift systems, parking brakes, drive cables, air intake systems, door and seat components, residential and industrial energy efficiency systems.

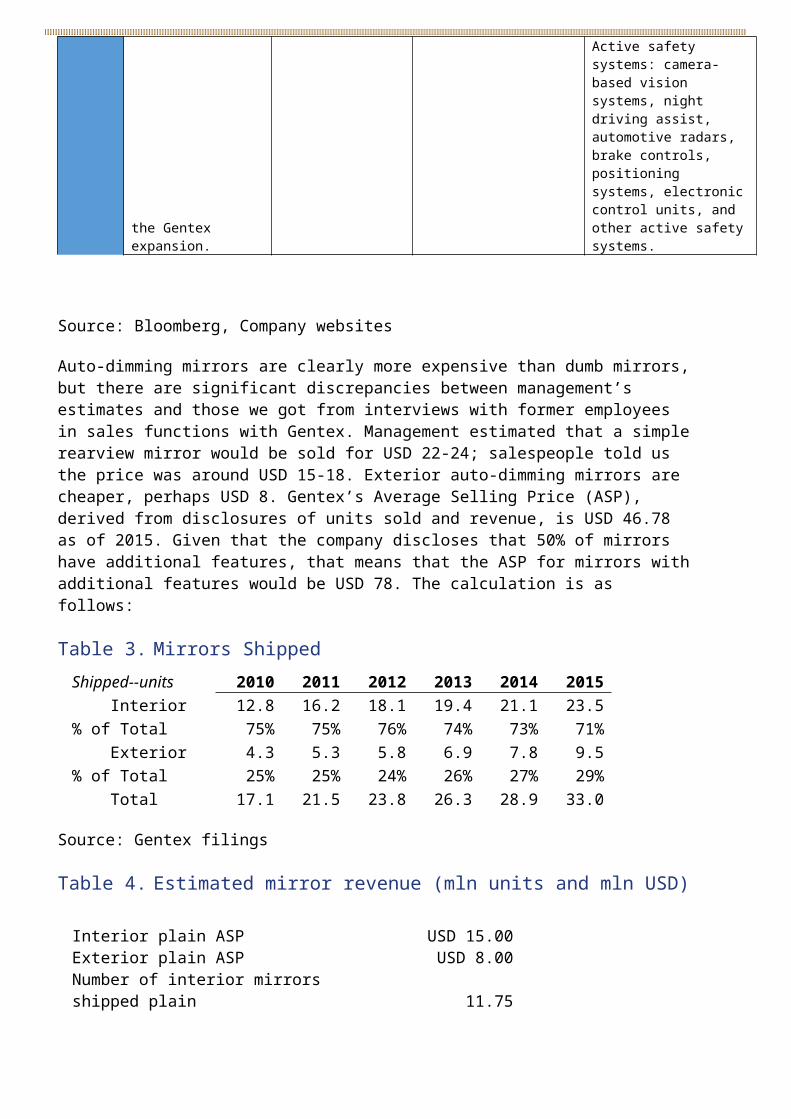

Passive safety systems: modules and components for passenger and driver-side airbags, side-impact airbag protection systems, seatbelts, steering wheels, inflator technologies, whiplash protection systems and child seats, restraint electronics and crash sensors. Active safety systems: camera-based vision systems, night driving assist, automotive radars, brake controls, positioning systems, electronic control units, and other active safety systems.

Source: Bloomberg, Company websites

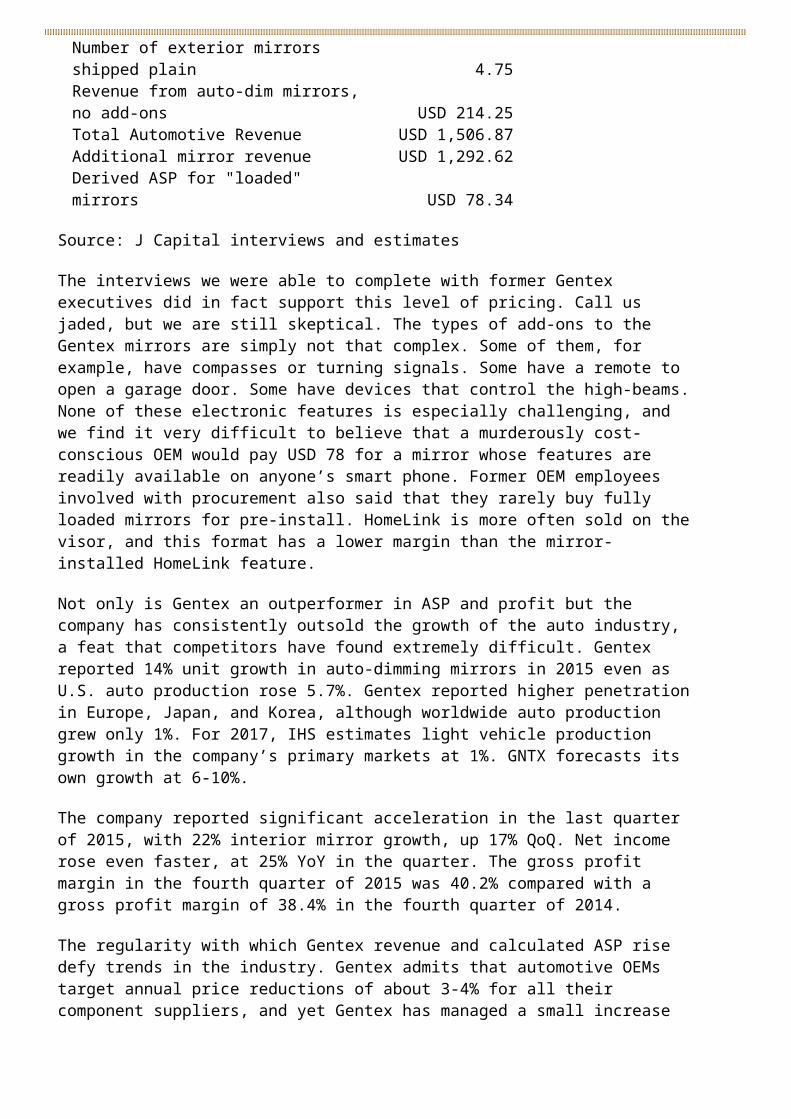

Auto-dimming mirrors are clearly more expensive than dumb mirrors, but there are significant discrepancies between management’s estimates and those we got from interviews with former employees in sales functions with Gentex. Management estimated that a simple rearview mirror would be sold for USD 22-24; salespeople told us the price was around USD 15-18. Exterior auto-dimming mirrors are cheaper, perhaps USD 8. Gentex’s Average Selling Price (ASP), derived from disclosures of units sold and revenue, is USD 46.78 as of 2015. Given that the company discloses that 50% of mirrors have additional features, that means that the ASP for mirrors with additional features would be USD 78. The calculation is as follows:

Table 3. Mirrors ShippedShipped--units 2010 2011 2012 2013 2014 2015 Interior 12.8 16.2 18.1 19.4 21.1 23.5 % of Total 75% 75% 76% 74% 73% 71% Exterior 4.3 5.3 5.8 6.9 7.8 9.5 % of Total 25% 25% 24% 26% 27% 29% Total 17.1 21.5 23.8 26.3 28.9 33.0

Source: Gentex filings

Table 4. Estimated mirror revenue (mln units and mln USD)

Interior plain ASP USD 15.00 Exterior plain ASP USD 8.00

9

Disclaimers: Last Oct 7, 2012

Number of interior mirrors shipped plain 11.75Number of exterior mirrors shipped plain 4.75Revenue from auto-dim mirrors, no add-ons USD 214.25 Total Automotive Revenue USD 1,506.87 Additional mirror revenue USD 1,292.62 Derived ASP for "loaded" mirrors USD 78.34

Source: J Capital interviews and estimates

The interviews we were able to complete with former Gentex executives did in fact support this level of pricing. Call us jaded, but we are still skeptical. The types of add-ons to the Gentex mirrors are simply not that complex. Some of them, for example, have compasses or turning signals. Some have a remote to open a garage door. Some have devices that control the high-beams. None of these electronic features is especially challenging, and we find it very difficult to believe that a murderously cost-conscious OEM would pay USD 78 for a mirror whose features are readily available on anyone’s smart phone. Former OEM employees involved with procurement also said that they rarely buy fully loaded mirrors for pre-install. HomeLink is more often sold on the visor, and this format has a lower margin than the mirror-installed HomeLink feature.

Not only is Gentex an outperformer in ASP and profit but the company has consistently outsold the growth of the auto industry, a feat that competitors have found extremely difficult. Gentex reported 14% unit growth in auto-dimming mirrors in 2015 even as U.S. auto production rose 5.7%. Gentex reported higher penetration in Europe, Japan, and Korea, although worldwide auto production grew only 1%. For 2017, IHS estimates light vehicle production growth in the company’s primary markets at 1%. GNTX forecasts its own growth at 6-10%.

The company reported significant acceleration in the last quarter of 2015, with 22% interior mirror growth, up 17% QoQ. Net income rose even faster, at 25% YoY in the quarter. The gross profit margin in the fourth quarter of 2015 was 40.2% compared with a gross profit margin of 38.4% in the fourth quarter of 2014.

The regularity with which Gentex revenue and calculated ASP rise defy trends in the industry. Gentex admits that automotive OEMs target annual price reductions of about 3-4% for all their component suppliers, and yet Gentex has managed a small increase in ASP every year of the last six except for 2012, when the calculated ASP fell by 3.4% YoY, from USD 46.71 to USD 45.19. Executives say that they are able to pass the price reductions on to their own suppliers. But executives also claim that glass is virtually the only component the company purchases.

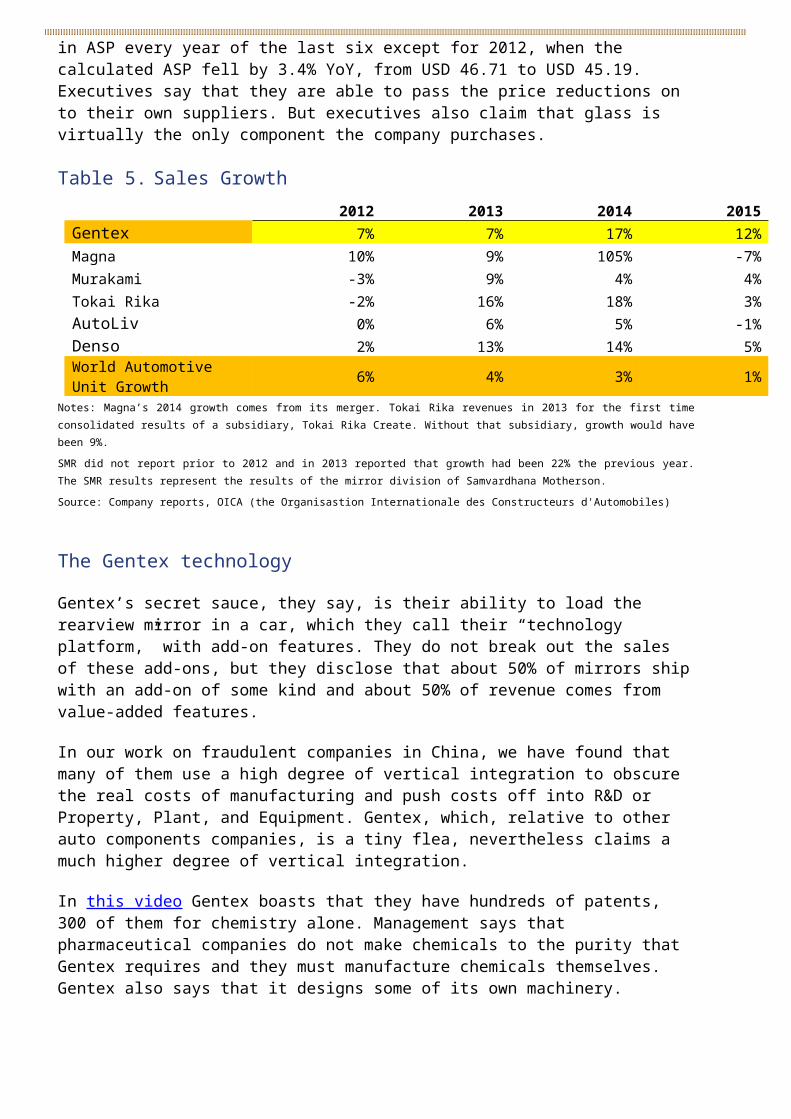

Table 5. Sales Growth2012 2013 2014 2015

Gentex 7% 7% 17% 12%

10

Disclaimers: Last Oct 7, 2012

Magna 10% 9% 105% -7%Murakami -3% 9% 4% 4%Tokai Rika -2% 16% 18% 3%AutoLiv 0% 6% 5% -1%Denso 2% 13% 14% 5%World Automotive Unit Growth 6% 4% 3% 1%

Notes: Magna’s 2014 growth comes from its merger. Tokai Rika revenues in 2013 for the first time consolidated results of a subsidiary, Tokai Rika Create. Without that subsidiary, growth would have been 9%.SMR did not report prior to 2012 and in 2013 reported that growth had been 22% the previous year. The SMR results represent the results of the mirror division of Samvardhana Motherson.Source: Company reports, OICA (the Organisastion Internationale des Constructeurs d'Automobiles)

The Gentex technologyGentex’s secret sauce, they say, is their ability to load the rearview mirror in a car, which they call their “technology platform,” with add-on features. They do not break out the sales of these add-ons, but they disclose that about 50% of mirrors ship with an add-on of some kind and about 50% of revenue comes from value-added features.

In our work on fraudulent companies in China, we have found that many of them use a high degree of vertical integration to obscure the real costs of manufacturing and push costs off into R&D or Property, Plant, and Equipment. Gentex, which, relative to other auto components companies, is a tiny flea, nevertheless claims a much higher degree of vertical integration.

In this video Gentex boasts that they have hundreds of patents, 300 of them for chemistry alone. Management says that pharmaceutical companies do not make chemicals to the purity that Gentex requires and they must manufacture chemicals themselves. Gentex also says that it designs some of its own machinery.

We did find more than 200 patents registered to Gentex on Google Patents (Note that a Carbondale, PA company that makes military equipment is also called Gentex Corp. and also owns many patents). While we do not dispute the utility of registering hundreds of patents, many seem fairly trivial. For example, Patent US 5689370 A, “Image/information displays on electro-optic devices,” described thus:

An improved electro-optic rearview mirror for motor vehicles, the mirror incorporating an improved display, such as "HEATED" or "OBJECTS IN MIRROR ARE CLOSER THAN THEY APPEAR" or the like, and wherein the mirror colors and clears uniformly and the display is effected in an aesthetically pleasing manner.

HomeLink

HomeLink is an automatic garage-door remote opening device that Gentex licensed from Johnson Controls and began incorporating into its mirrors in 2001. Despite requests from the SEC, Gentex has never disclosed how many

11

Disclaimers: Last Oct 7, 2012

HomeLink units are sold. The device is sold by a number of distributors including Liftmaster, Mito, and Brandmotion.

In September 2013, Gentex completed the acquisition of the HomeLink product from Johnson Controls for USD 701 mln. In that year, Gentex recorded USD 307.4 mln in goodwill as a result of the HomeLink acquisition plus USD 366 mln in intangibles, suggesting that the acquisition might have been overvalued by about 300 mln.

JCI had never disclosed revenue specifically for the HomeLink product. HomeLink was part of JCI’s automotive electronics unit. In 2014, JCI sold the remainder of the unit to Visteon Corp. for USD 265 mln.1 Visteon disclosed that the portion of the business it acquired had generated USD 1.3 bln in revenues in 2012 and USD 58 mln in earnings.

JCI had acquired HomeLink in 1996 with the acquisition of Prince Holding Corporation, a USD 850 mln company making interior components such as sun visors.

The HomeLink feature had been integrated into Gentex mirrors since 2001. Yet Gentex reported that the HomeLink acquisition would increase revenue by USD 125-150 mln while also reducing cost, since Gentex would no longer be paying licensing fees.

Gentex acquired some JCI customers who were buying the HomeLink feature as a standalone or attached to a front seat window visor, but sales of that nature should have dragged down Gentex’s margins. The more likely answer lies in the terms of the acquisition. When Gentex acquired HomeLink from Johnson Controls, the companies also made an agreement under which Gentex would sell HomeLink products back to JCI in perpetuity, at an undisclosed price.2 Later questioned by the SEC, Gentex said that the agreement was made on an arm’s-length basis and at a market price.

This arrangement suggests that Gentex could have overpaid for the HomeLink technology to seed its future revenue.

Making too much of HomeLinkThe HomeLink acquisition in Q4 2013 cluttered up the Gentex balance sheet and could plausibly have been made in order to accommodate overstated profits: HomeLink added a big chunk of goodwill, which grew in that year to 15% of total assets, while goodwill plus intangibles rose to 39% of assets. A plausible explanation for the HomeLink sales growth post acquisition is that Gentex overpaid JCI in order to enable JCI to repurchase HomeLink units at a higher ASP than it has commanded as the technology’s owner. In that way, Gentex could have double-dipped on its acquisition, setting up USD 300 mln in new revenues from JCI while also booking the USD 300 mln as goodwill. If that narrative is true, it suggests that Gentex has to work harder these days to maintain its purported margins.

1 The JCI 8-K describing the deal is available here.2 See page 55 of the Gentex 2013 Annual Report

12

Disclaimers: Last Oct 7, 2012

The second half of 2015 marked some of the fastest growth compared with growth in the automotive market that Gentex has ever experienced. It also in some ways marked the start of the new, more aggressive share-management regime post-Steve Dykman. In 2013, CFO Steve Dykman left abruptly to take a position as CFO of C.H.I. Overhead Doors Inc. , and the new CFO, Steve Downing, seems promotional. Downing is not excessively paid for a listed company CFO but he does have incentive to drive the share price higher. With an annual salary of USD 337,500 plus a bonus in 2015 bringing total compensation to nearly USD 500,000, Downing was granted 17,730 stock options and 6,500 restricted shares after being appointed in June 2015. The option exercise price equals the stock’s market price on date of grant, and the options vest after one to five years. A 25% increase in the share price would therefore mean roughly USD 70,000 in additional compensation for Downing.

There are some signs that the situation is deteriorating for Gentex. The company shows rapidly expanding accruals and deteriorating FCF margin, inventory growth, and depreciation and amortization that are unsustainably low. We see HomeLink as a warning sign.

In correspondence in November 2014, the SEC asked Gentex to disclose the revenue and margin boost it achieved from acquiring HomeLink. In a June 2015 response, Gentex refused to do so, claiming that current disclosures were adequate.

The range of universal remotes for garage doors is large. Chamberlain and Genie appear to be the market leaders, and their products can be controlled using a smart phone app. Universal remotes can be purchased at Home Depot for between USD 20-49. Although there is some value associated with adding a remote to the overhead mirror, we do not believe that the value is sufficient to bring ASPs for HomeLink-equipped mirrors to over USD 100, as some former salespeople have represented in interviews.

To estimate the portion of sales for which HomeLink is responsible, we look at Gentex’s disclosure in Q4 2013 that HomeLink sales would grow by between USD 125-150 mln in 2014 as a consequence of the acquisition. Guessing that the USD 150 mln doubled Gentex’s 2013 revenue for HomeLink, 2014 would have seen USD 300 mln in HomeLink sales or 22% of the company’s total.

SmartBeam

Gentex announced the launch of SmartBeam technology in 2001 and said it had preliminary agreements from customers to install the technology in the first half of 2004 and in 2005. SmartBeam uses a light sensor to determine whether the high beams should be used and turns them on and off as needed. The company says: “SmartBeam uses a miniature, mirror-borne CMOS image sensor (camera on an electronic chip) to monitor surrounding traffic conditions and automate high-beam usage, making nighttime driving safer by maximizing forward lighting.” We think SmartBeam may be responsible for around 10-15% of company revenue.

A SmartBeam-like feature is also available from Bosch, AutoLiv, and other components companies.

13

Disclaimers: Last Oct 7, 2012

Now that cars are all required to install backing cameras, companies like Mobileye can add a highbeam-control feature basically for free. An engineer familiar with the technology told us that adding the feature to an existing camera costs just USD 5 or so, while Gentex says it charges USD 70 for a second camera in its mirror.

Lane Keeping and Driver Alert

Starting in 2012, Gentex has used MobileEye graphics chips for a new High-Beam Control, Lane Keeping, and Driver Alert system. The system uses a camera on the car to identify whether the driver has wandered from his lane, triggering the Lane Keeping function to vibrate the steering wheel and jog the driver to be more alert. In 2015, Gentex stopped working with Mobileye and will make the camera itself. The Mobileye-based cameras are on Ford, Jaguar, and Land Rover models; for new launches with other OEMs, they will develop their own technology.

TransCore Toll Solutions

In 2015, Gentex made an agreement with TransCore LP to integrate that company’s Universal Toll Module in the mirror, enabling the driver to avoid adding a second RFID tag to the windshield area. The module is designed to be integrated into vehicle manufacturing rather than added in the aftermarket. The UTM is a prospective add-on to Gentex mirrors.

Dynamic Forward Lighting

This feature is used to control high-beam glare by diverting the beam around oncoming and preceding vehicles. The system has been approved only for sale in Europe.

Rear Camera Display/Full Display Mirrors

In 2006, Gentex announced that it had plans to supply Rear Camera Display (RCD) mirrors to OEMs. The mirror was already available that year on the Toyota Camry sold via Gulf States Toyota, with the RCD mirror installed at port by Gulf States. The mirrors display images from a rear camera for backing.

Gentex’s new Full Display Mirrors show images from behind the car continuously for when drivers prefer to watch the road using the panoramic camera rather than the mirror. Gentex said it shipped only 150-200 Full Display Mirrors in 2015 but will be ramping the inclusion of these mirrors in many new vehicle programs going forward.

Other: telematics, wireless control systems, compasses, lights

Gentex also embeds in some of its mirrors compasses, turning signals (for the exterior mirrors), LED lights, blind-zone indicators, and other features.

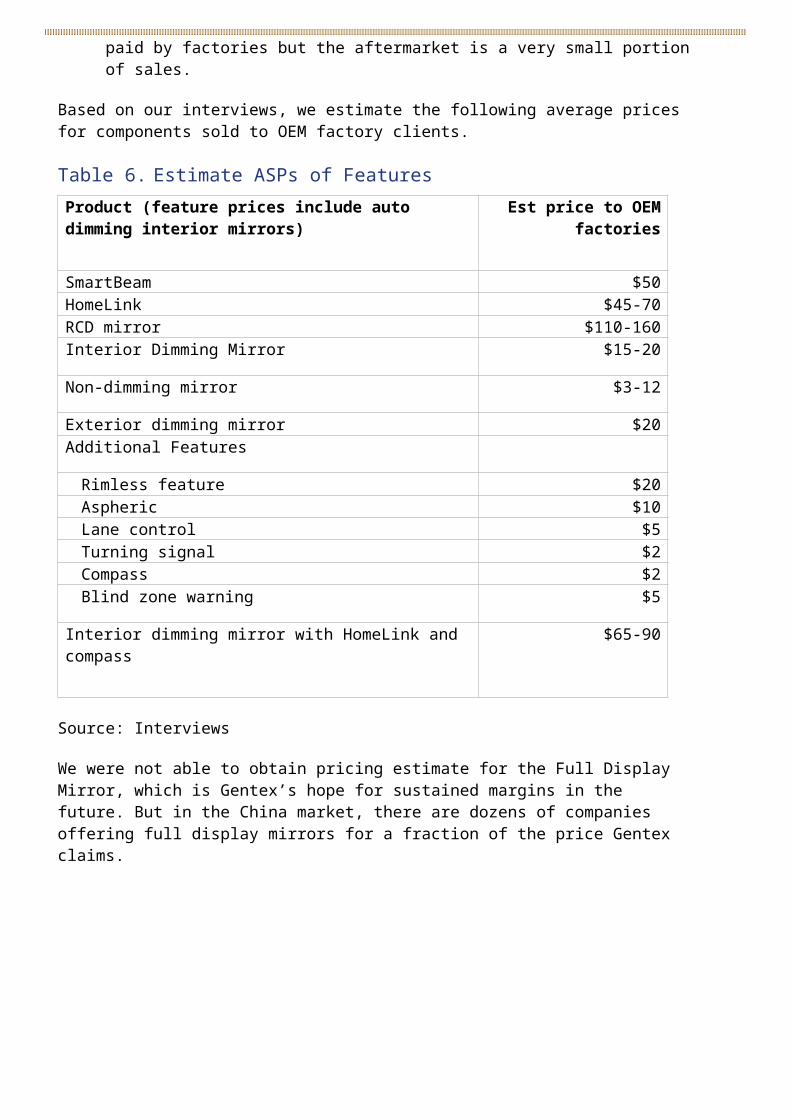

Breaking down the components

14

Disclaimers: Last Oct 7, 2012

In interviews with industry and ex-Gentex executives, we have pulled together estimates of prices that Gentex receives from automotive OEMs for its mirrors and added features. Those prices generally seem to line up with the prices charged by competitors who have far lower margins. Since it’s unlikely that Gentex manufacturing is twice as efficient as that of competitors, we think the margins are overstated.

Components companies typically charge different prices depending on the channel in which the component is sold.

The lowest prices are those at which the company sells to OEM factories. The company sells two-thirds interior mirrors and one-third exterior. About half the mirrors have add-on components. The typical interior mirror with add-ons has a compass and the HomeLink feature. This channel represents about 75% of sales.

Tier 1 distributors provide pre-assembled components to OEM factories. The Tier 1 partner may get the same price as the OEM but takes low-end components. Gentex sells plain side mirrors and glass assemblies for exterior dimming mirrors through Tier 1 distributors. These are very low-value components. This channel represents about 20% of sales. Tier 1 partners include SMR, Tokai Ricoh, Ficosa, and others. The company claims that margins are much higher on these glass assemblies than on the interior mirrors but we doubt it.

Automotive OEMs have subsidiaries that attach components at port before the cars go to the dealers. This might be done when components are added to certain trim levels or certain regions of the world. The accessory channels pay around 20-30% more than the factories. This channel is worth around 3% of sales.

Consumers buy some components in the aftermarket, when the original component has been damaged or by request to a dealer before buying the car. The aftermarket pays 3-4x the price paid by factories but the aftermarket is a very small portion of sales.

Based on our interviews, we estimate the following average prices for components sold to OEM factory clients.

Table 6. Estimate ASPs of FeaturesProduct (feature prices include auto dimming interior mirrors)

Est price to OEM factories

SmartBeam $50 HomeLink $45-70 RCD mirror $110-160 Interior Dimming Mirror $15-20

Non-dimming mirror $3-12

Exterior dimming mirror $20 Additional Features

Rimless feature $20

15

Disclaimers: Last Oct 7, 2012

Aspheric $10 Lane control $5 Turning signal $2 Compass $2 Blind zone warning $5

Interior dimming mirror with HomeLink and compass

$65-90

Source: Interviews

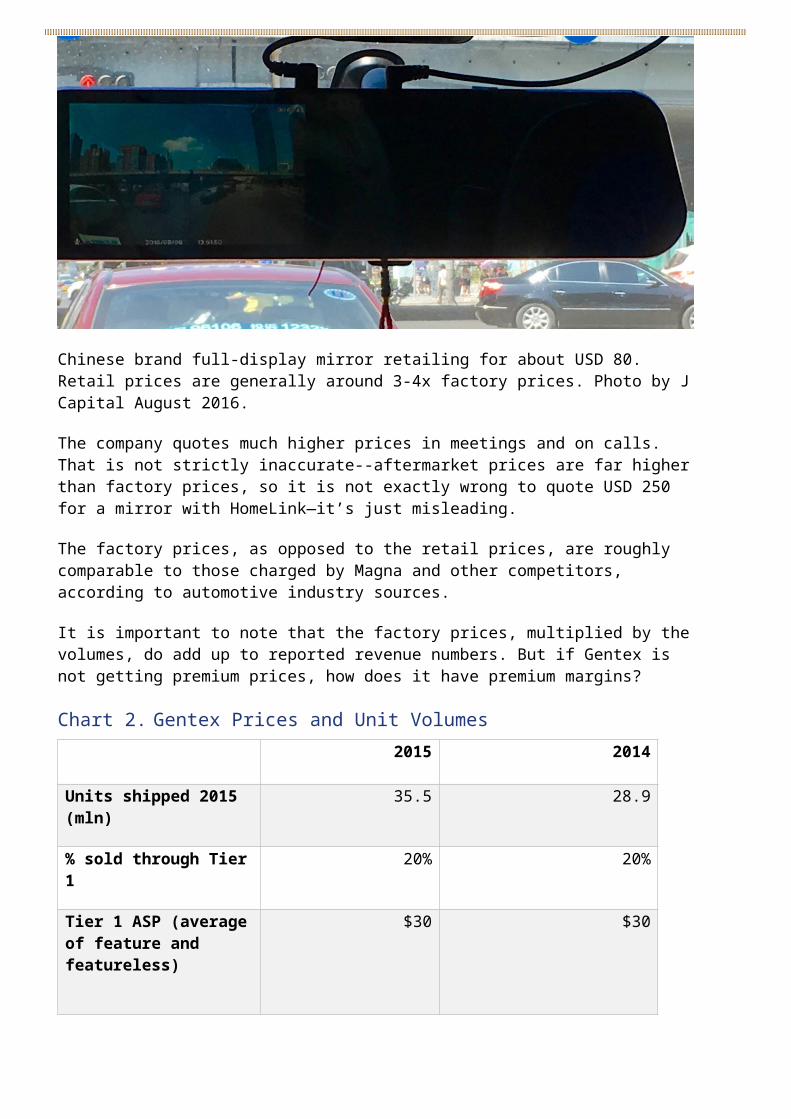

We were not able to obtain pricing estimate for the Full Display Mirror, which is Gentex’s hope for sustained margins in the future. But in the China market, there are dozens of companies offering full display mirrors for a fraction of the price Gentex claims.

Chinese brand full-display mirror retailing for about USD 80. Retail prices are generally around 3-4x factory prices. Photo by J Capital August 2016.

The company quotes much higher prices in meetings and on calls. That is not strictly inaccurate--aftermarket prices are far higher than factory prices, so it is not exactly wrong to quote USD 250 for a mirror with HomeLink—it’s just misleading.

The factory prices, as opposed to the retail prices, are roughly comparable to those charged by Magna and other competitors, according to automotive industry sources.

It is important to note that the factory prices, multiplied by the volumes, do add up to reported revenue numbers. But if Gentex is not getting premium prices, how does it have premium margins?

Chart 2.Gentex Prices and Unit Volumes

16

Disclaimers: Last Oct 7, 2012

2015 2014

Units shipped 2015 (mln)

35.5 28.9

% sold through Tier 1

20% 20%

Tier 1 ASP (average of feature and featureless)

$30 $30

Bare mirror ASP (USD)

$18 $18

Av add-on (USD) $60 $60

% of add-ons 50% 50%

Source: Company reports, J Capital estimates

The MarginsGentex’s gross margin contrasts with those reported by Magna, the largest manufacturer in the world of automotive mirrors, which were 14.2% for the 2015 calendar year. Magna does not break out the margins for its Vision Systems division, but the technological content and likely margins would seem to sit in the middle of Magna’s range of products, which run from seating and exteriors to powertrain and electronics.

Gentex used to claim that auto-dimming was the impossible-to-replicate feature that made their mirrors much more valuable. Auto-dimming mirrors, they say, are gaining in industry penetration but, with a current 25% or so share, they still have a long runway for growth.

But industry experts suggest that dimming is just not enough of a selling point to persuade customers to pay a lot more.

Some say that Magna’s auto-dimming technology is just not as good as Gentex’s. One accessories executive told of a case in which Magna dimming mirrors leaked and damaged car dashboards. But the two companies are intimately familiar with one another, and OEM clients routinely take bids from both and yet Magna, which could easily undersell Gentex to capture market, has only about 10% of the auto-dimming market. Says a former Gentex executive:

“I have a confused perspective like you do [about why Magna does not have a bigger share of the auto-dimming market]. It looks like a great opportunity for Magna … and OEMs are not so endeared to Gentex as

17

Disclaimers: Last Oct 7, 2012

they used to be. There’s a price opening, a technology opening, and an OEM relationship opening.”

The principal reason, Gentex says, that it can earn margins 2.66x those of the industry leader is because it adds electronics to about half the mirrors. This is an argument that analysts have been buying for two decades, but it makes little sense, for two reasons.

First, Magna’s mirrors—more than 125 million of them--like Gentex’s, offer proprietary auto-dimming technology, lane-keeping assistance, glare-free high beam, collision mitigation, rear-vision video, and other features. In short, Magna has all the features Gentex has except for the garage-door opening feature, HomeLink. Magna also has the advantage of enormous scale. Gentex reported producing 34 mln mirrors in 2015 (in the Investor Day presentation, executives said 35.5 mln instead), meaning that Magna’s mirror division alone is 3.5 times the size of Gentex’s business. Gentex says that its production is more efficient, but we do not know of businesses that out-scale their competitors by a factor of three and yet make the same devices at higher cost.

The second, more pertinent issue with Gentex is that its added electronics are neither technically challenging nor, in most cases, proprietary. These are panes of bent and coated glass backed by printed circuit boards that control simple circuitry to light up a compass and a thermometer, activate a turning signal, or send a radio signal to a garage door, all in plastic casing and stuck to a windshield.

Gentex mirror. Screenshot from http://www.bodenzord.com/archives/513

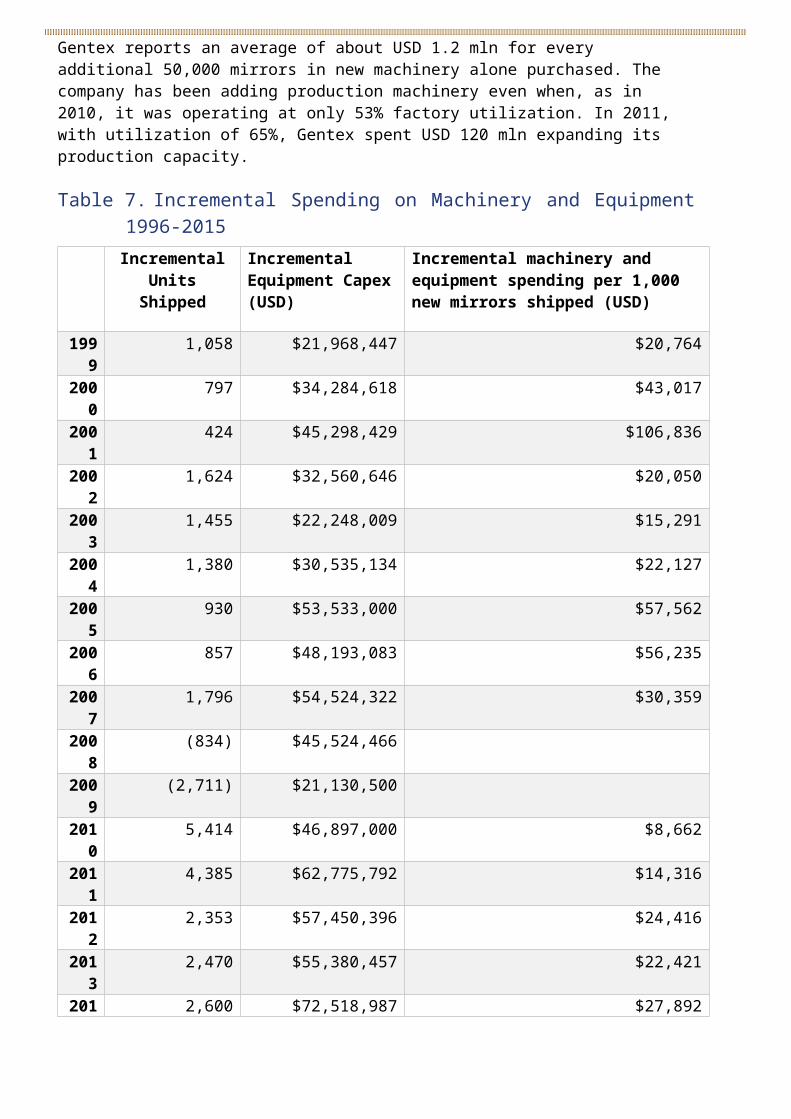

The Capex BlowoutThe portion of Gentex’s financials that bothers us most is the capital budget. Gentex brings everything in house, from the chemicals it needs for dimming glass to the semiconductor packaging facility. Doing everything in house, though, makes costs non-transparent.

Gentex reports an average of about USD 1.2 mln for every additional 50,000 mirrors in new machinery alone purchased. The company has been adding production machinery even when, as in 2010, it was operating at only 53%

18

Disclaimers: Last Oct 7, 2012

factory utilization. In 2011, with utilization of 65%, Gentex spent USD 120 mln expanding its production capacity.

Table 7. Incremental Spending on Machinery and Equipment 1996-2015

Incremental Units

Shipped

Incremental Equipment Capex (USD)

Incremental machinery and equipment spending per 1,000 new mirrors shipped (USD)

1999

1,058 $21,968,447 $20,764

2000

797 $34,284,618 $43,017

2001

424 $45,298,429 $106,836

2002

1,624 $32,560,646 $20,050

2003

1,455 $22,248,009 $15,291

2004

1,380 $30,535,134 $22,127

2005

930 $53,533,000 $57,562

2006

857 $48,193,083 $56,235

2007

1,796 $54,524,322 $30,359

2008

(834) $45,524,466

2009

(2,711) $21,130,500

2010

5,414 $46,897,000 $8,662

2011

4,385 $62,775,792 $14,316

2012

2,353 $57,450,396 $24,416

2013

2,470 $55,380,457 $22,421

2014

2,600 $72,518,987 $27,892

2015

6,600 $97,941,762 $14,840

Source: Gentex annual reports, J Capital calculations

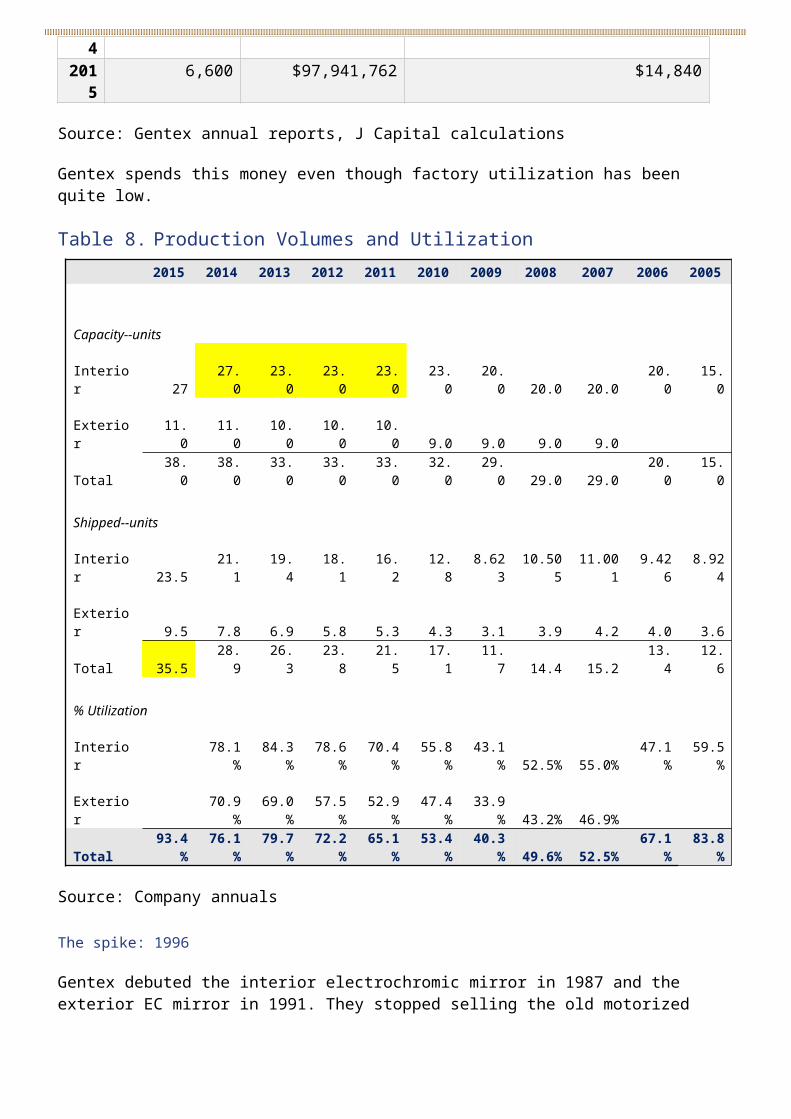

Gentex spends this money even though factory utilization has been quite low.

Table 8. Production Volumes and Utilization

19

Disclaimers: Last Oct 7, 2012

2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005

Capacity--units Interior 27 27.0 23.0 23.0 23.0 23.0 20.0 20.0 20.0 20.0 15.0 Exterior 11.0 11.0 10.0 10.0 10.0 9.0 9.0 9.0 9.0 Total 38.0 38.0 33.0 33.0 33.0 32.0 29.0 29.0 29.0 20.0 15.0 Shipped--units Interior 23.5 21.1 19.4 18.1 16.2 12.8 8.623

10.505

11.001 9.426 8.924

Exterior 9.5 7.8 6.9 5.8 5.3 4.3 3.1 3.9 4.2 4.0 3.6 Total 35.5 28.9 26.3 23.8 21.5 17.1 11.7 14.4 15.2 13.4 12.6 % Utilization Interior

78.1%

84.3%

78.6%

70.4%

55.8%

43.1% 52.5% 55.0%

47.1%

59.5%

Exterior

70.9%

69.0%

57.5%

52.9%

47.4%

33.9% 43.2% 46.9%

Total93.4

%76.1

%79.7

%72.2

%65.1

%53.4

%40.3

%49.6

%52.5

%67.1

%83.8

%

Source: Company annuals

The spike: 1996Gentex debuted the interior electrochromic mirror in 1987 and the exterior EC mirror in 1991. They stopped selling the old motorized mirror in 1991 and started to add features like a compass, reading light, and headlight dimming to the interior mirror starting in 1991. Yet when the mirror offering was merely a simple, motorized mirror, gross margins were 37.3% (1990), 39.7% (1991), and 43.9% (1992). Margins for this mechanical device were expanding. Why bother to invest in new technology?

The spike in capital expenditures began in 1996, when spending jumped from USD 4.86 mln in 1995 to USD 16.4 mln in 1996 and grew from there. There was a burst of capex in 2001. Since 2005, with the exception of the auto industry’s disaster year, 2009, Gentex has been adding around USD 50 mln per year in machinery and equipment spending that seems to be of dubious value; all it has achieved is unit volume growth in manufacturing at an average of USD 32 per mirror produced just for the machinery.

As this has been happening, Gentex has been racking up “other assets” on the balance sheet, reaching USD 752 mln in 2015. Those Other Assets consist of Goodwill, Long-term Investments, Intangibles, and Patents.

There are few indications in the reports of what the capex is for. That fact alone is concerning. In many cases, the capex increment is material: in 1998 for example, Gentex added USD 25.6 mln worth of machinery and equipment to a base of USD 58.3 mln in machinery and total plant and equipment of USD

20

Disclaimers: Last Oct 7, 2012

59.4 mln without disclosing anything about why it was necessary to add 50% to the existing fixed-asset base. By 2011, the company had more than USD 600 mln in plant and equipment but, with a utilization rate of just 65%, saw fit to invest an additional USD 120 mln. As to why, Gentex referred only to “strong customer demand for our auto-dimming mirrors and more complex product mix.”

Early on, Gentex did provide more detail, and it suggested a company that was either making highly ill-advised investments or perhaps simply inflating the capex line. In 1991, Gentex spent USD 21 mln on “glass coating equipment” to bring the coating process in-house. The company attributed its 700 bps margin improvement over 18 months to this coating process.

In the 2001 Annual Report, Gentex reported spending for development of white LEDs, which it called Orca.

“Thanks to Orca, Gentex’s original white-light LED illuminator, which consisted of a pod of fourblue-green and two amber LEDs, has been reduced to a single LED package. Complete Orca assemblies will be built in prototype quantities in a new, state-of-the-art microelectronics line,” the company reported on page 17. “Orca white LEDs have already been integrated into new automatic-dimming mirrors as map lamps. These second-generation map-lamp assemblies decrease overall mirror complexity and footprint size while increasing light output. We plan to begin shipping these new lighted mirrors this year for 2003 model vehicles.”

In other words, Gentex engaged in the hideously expensive business of developing white-LED technology in order to put a little light on the mirror, the kind that normally sits between the visors and that you turn on to read a map, the kind that costs maybe USD 2 when companies like Visteon sell it as part of the overhead console. In the late 1990s, when Japanese companies like Toyoda Gosei and Nichia were developing white LEDs, they spent around USD 85 mln per year on the effort.

The last mention of Orca came in the 2007 10-K:

In 1999, the Company announced the development of its LED technology, which represented the first time that white light for illumination purposes could be achieved using high intensity Orca power LEDs on a cost-effective basis. LEDs as illuminators have many advantages over incandescent lamps, including extremely long life, low heat generation, lower current draw, more resistance to shock, and lower total cost of ownership. The Company continually evaluates LEDs that are offered in the market place and is currently working with suppliers that can provide high quality LEDs in a more cost effective manner.

(2007 10-K page 7)

Gentex mothballed the Orca technology, yet there is no place in the accounts where Gentex recognizes a write-off of the R&D and machinery that went into this effort.

21

Disclaimers: Last Oct 7, 2012

The company also says that it hired acoustic engineers to develop a superior microphone to embed in the mirror. "Gentex even manufactures its own noise-cancellation microphones designed specifically to enhance hands-free cellular communications in the harsh automotive environment." (2003 AR page 10) That may be true, but procurement staff from the automotive manufacturers are very clear that they will not pay more for a better microphone, since this technology is available as a commodity from many manufacturers. The same is true of the “telematic” features such as the compass.

Since 2001, Gentex has been talking about its proprietary design for CMOS chips:

“During 2001, the Company announced a revolutionary new technology, called SmartBeam(TM), using a custom, activepixel, CMOS (complementary metal oxide semiconductor) sensor, that maximizes a driver's forward vision by significantly improving utilization of the vehicle's highbeam headlamps during nighttime driving.” (2001 10-K page 6)

The most recent mention of the CMOS imaging was in the 2015 10-K, when Gentex referred to “Our CMOS imager technology when used as a rearward facing automotive video camera . . “ (page 9).

But CMOS chips are sensors, the less-valuable portion of driver-assist technology. More difficult is the complex software that processes images taken from the cameras. The driver-assist technology was licensed from Mobileye. The Mobileye driver-assist features were integrated into Gentex mirrors in 2013, and Gentex subsequently decided to end its cooperation with Mobileye in order to capture better economics. There was no visible effect on margins.

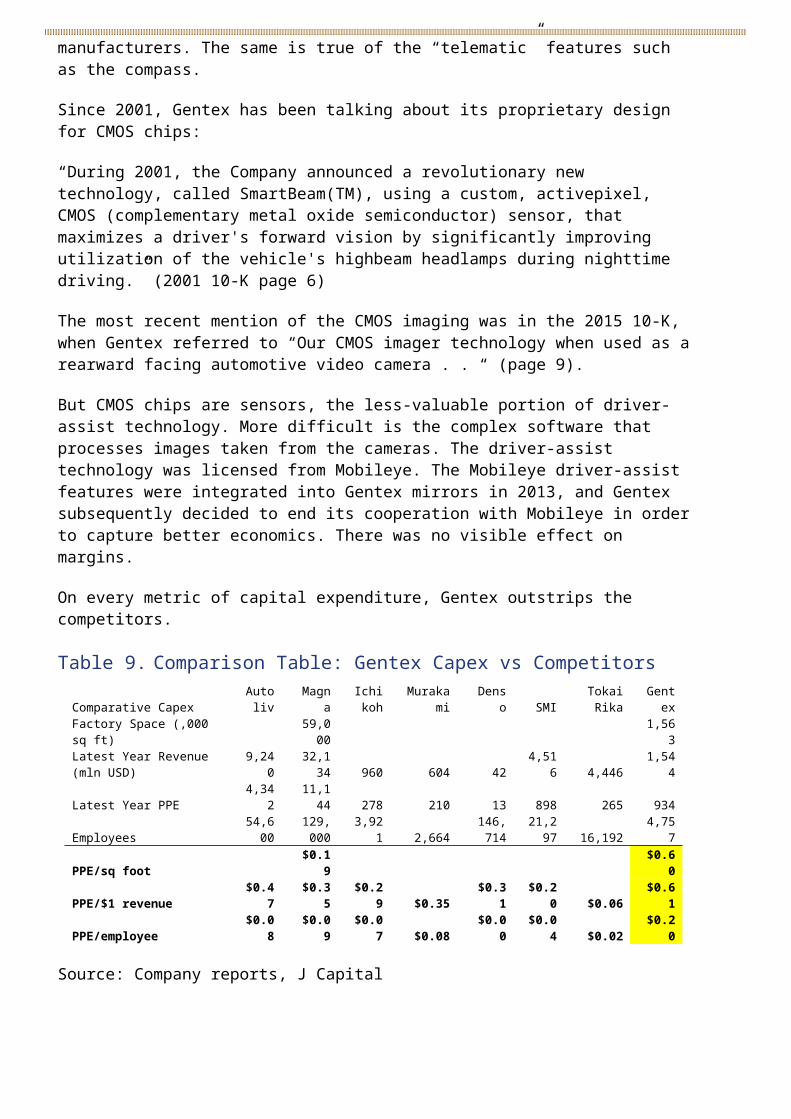

On every metric of capital expenditure, Gentex outstrips the competitors.

Table 9. Comparison Table: Gentex Capex vs CompetitorsComparative Capex

Autoliv

Magna

Ichikoh

Murakami Denso SMI

Tokai Rika

Gentex

Factory Space (,000 sq ft)

59,000

1,563

Latest Year Revenue (mln USD)

9,240

32,134 960 604 42

4,516 4,446

1,544

Latest Year PPE 4,34

2 11,14

4 278 210 13 898 265 934

Employees 54,6

00 129,0

00 3,92

1 2,664 146,7

14 21,2

97 16,192 4,75

7

PPE/sq foot $0.19 $0.6

0

PPE/$1 revenue $0.4

7 $0.35 $0.2

9 $0.35 $0.31 $0.2

0 $0.06 $0.6

1

PPE/employee $0.0

8 $0.09 $0.0

7 $0.08 $0.00 $0.0

4 $0.02 $0.2

0

Source: Company reports, J Capital

The reality is that Gentex has not come up with anything since auto-dimming. It licensed and then purchased HomeLink, which sustains sales. As a former executive comments, “They have gone through a long period without innovation. They are very conservative.”

22

Disclaimers: Last Oct 7, 2012

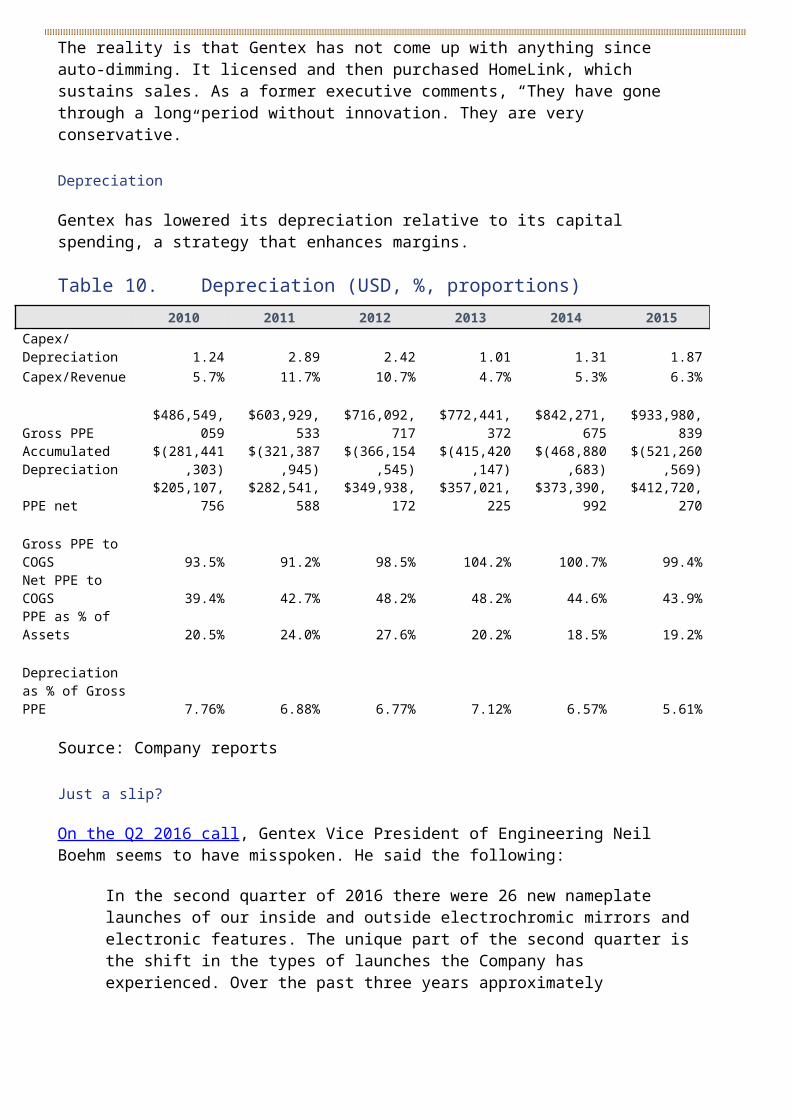

Depreciation

Gentex has lowered its depreciation relative to its capital spending, a strategy that enhances margins.

Table 10. Depreciation (USD, %, proportions) 2010 2011 2012 2013 2014 2015Capex/Depreciation 1.24 2.89 2.42 1.01 1.31 1.87Capex/Revenue 5.7% 11.7% 10.7% 4.7% 5.3% 6.3%

Gross PPE $486,549,0

59 $603,929,5

33 $716,092,7

17 $772,441,3

72 $842,271,6

75 $933,980,8

39 Accumulated Depreciation

$(281,441,303)

$(321,387,945)

$(366,154,545)

$(415,420,147)

$(468,880,683)

$(521,260,569)

PPE net $205,107,7

56 $282,541,5

88 $349,938,1

72 $357,021,2

25 $373,390,9

92 $412,720,2

70

Gross PPE to COGS 93.5% 91.2% 98.5% 104.2% 100.7% 99.4%Net PPE to COGS 39.4% 42.7% 48.2% 48.2% 44.6% 43.9%PPE as % of Assets 20.5% 24.0% 27.6% 20.2% 18.5% 19.2%

Depreciation as % of Gross PPE 7.76% 6.88% 6.77% 7.12% 6.57% 5.61%

Source: Company reports

Just a slip?On the Q2 2016 call, Gentex Vice President of Engineering Neil Boehm seems to have misspoken. He said the following:

In the second quarter of 2016 there were 26 new nameplate launches of our inside and outside electrochromic mirrors and electronic features. The unique part of the second quarter is the shift in the types of launches the Company has experienced. Over the past three years approximately two/thirds of launches have been base interior and exterior autodimming mirrors with no added electronic features.

However, in the second quarter of 2016, of the 26 nameplate launches, approximately two/thirds of them were advanced feature launches.

Historically, the Company has been able to demonstrate that it has delivered higher-than-average contribution margins when it's not only growing unit penetration, but also adding electronic content faster than unit growth.

In the past, however, the company has consistently reported that advanced features are included in about half of the mirrors shipped.

23

Disclaimers: Last Oct 7, 2012

MechanismsWe believe that Gentex is understating its costs by bringing everything to Zeeland, Michigan. Management has said, for example, that Gentex owns its own fab. The company does have a small facility where semiconductors are cut and packaged in a clean-room setting, but that is a far cry from the highly capital-intensive business of fabbing one’s own chips, and we think management knows the difference. We know that the company owns several hundred Surface Mount Technology machines for laminating PCBs, but this is commoditized equipment; adding to SMT equipment requires tens of thousands of dollars, not millions.

In general, Gentex tends to state every technological development in the most promotional of terms and to mislead as to its costs.

How the Business WorksSales channels

All sales of inside mirrors are direct; most sales of exterior mirrors are through partners. The exterior mirrors are providing all the growth. Gentex claims that the exterior mirrors are cheaper but offer higher margins than the interior ones. But even if the exterior dimming mirrors are more profitable when sold direct, with added features, our interviews indicate that the majority of exterior mirrors are sold as sub-assemblies to other components companies, and interviews suggest that these components companies, not Gentex, engineer the assemblies to fit the glass and contain the components relevant to a specific car. It is very rare for an exterior mirror to be sold pre-loaded with features and specifically designed for the purchasing OEM. This type of sale is unlikely to attract a high margin.

AftermarketRoughly 5% of Gentex sales come from the aftermarket, but this does not mean retail sales: the largest portion of aftermarket sales are made to the port-based subsidiary of an OEM or to a dealer, and those companies apply the mirrors. These sales are attractive to Gentex because dealers and port-based OEM assembly companies are much less price-sensitive than the OEMs themselves.

Regions

Gentex reports that most of its international sales are disclosed in the automotive portion of the “other” income category, which also includes revenue from the smoke alarms and the airplane windows. Only automotive sales in the U.S., Germany, and Japan are included in the “Automotive Products” sales category. Sales in all other nations, therefore, are less than 2.3% of total sales.

Automotive Products revenues in the “Other” category are sales to customer automotive manufacturing plants in Korea, Mexico, Canada, Hungary, China,

24

Disclaimers: Last Oct 7, 2012

and the United Kingdom as well as other foreign automotive customers. Most of the Company’s non-U.S. sales are invoiced and paid in U.S. dollars. (page 58 2015 10-K)

Gentex may not treat as “overseas” sales to vehicles that ship from the U.S., Europe, or Japan even if the vehicles are sold elsewhere. But given the large distributor relationships Gentex discloses in Mexico and India, it is surprising that more revenue does not come from these regions. In China, Gentex has low penetration but has nevertheless maintained a presence for a decade. Management says that Gentex no longer maintains its assembly plant in China because shipping from overseas leads to less breakage. But China requires that its domestically made autos must include at least 75% locally made content, and to meet that standard, the components probably need to be invoiced in Renminbi. So we find it unlikely that OEMs in China would not require the mirror to be installed in China in order to meet localization requirements. Magna, Murakami, Ichikoh, and other competitors have large presences in China with manufacturing facilities and sales forces talking to the Chinese OEMs. It seems unlikely that Gentex could compete in China on an export basis alone.

The Challenge from CamerasNew rules issued by the Highway Traffic Safety Administration (NHTSA) require vehicles to begin installing rearview cameras as of May 1. The phase-in schedule requires that 10% of vehicles have the cameras after May 2016, 40% after May 2017, and 100% of vehicles after May 2018. In this release, NHTSA estimated that 57% of model year 2014 vehicles already had a rear video system, and that even without a final rule, 73% of the vehicles sold into North America would have already included a rearview video system by 2018.

Camera installation undermines Gentex’s bid to make the rearview mirror the automobile’s “technology platform.” With the technology content of cars increasing, most higher-end models include LCD screens that host the navigation and entertainment system, and this larger screen is the natural location for mirror-embedded electronics. A former executive of Gentex told us that the company had put a lot of money into research to prove that the mirror was the safest place to put technologies like backing cameras. But the OEMs want pricing leverage and do not want to be confined to one company’s platform.

Gentex responds that backing cameras have a lot of failure risk and can be blocked by ice and snow. They say that drivers use rearview mirrors to view the cabin as well as the car exterior, and the ability to switch between camera display and a dumb mirror is useful. Finally, Gentex points out that the company is already shipping RCD mirrors, while they portray the threat from backing cameras as something automakers face in the future.

But as long ago as 2012, Gentex itself contradicted this story in the Q4 call. Then-Senior Vice President and CFO Steve Dykman said on that call:

RCD Mirror unit shipments decreased by approximately 8% in calendar year 2012 compared with calendar year 2011. In calendar year 2013, RCD Mirror unit shipments are estimated to decrease by approximately

25

Disclaimers: Last Oct 7, 2012

25% to 35% compared with 2012, which incorporates estimated reduced RCD Mirror unit shipments to automotive customers who have previously notified the Company of their plans to have the display for the rear camera and the radio instead of the rear view mirror.

- Seeking Alpha transcript

For the backing camera system itself, competitors include Continental, Bosch, and Mobileye, all offering low-cost systems.

Mobileye, whose technology Gentex purchased and incorporated into its camera-based driver assist systems in 2012-14, designs and develops vision-based driver assistance systems for automobile collision prevention and mitigation. Mobileye claims OEM integrations into car models from 20 global automakers including BMW, Ford, General Motors, Nissan, and Volvo.

Gentex concedes that backing systems from Mobileye are relatively inexpensive though Mobileye does not disclose the ASP on its cameras. Mobileye sales are growing very rapidly, suggesting that Mobileye is more likely to take share in backing systems.

As to how Gentex can compete with Mobileye’s low cost, CFO Steve Downing said on the Q2 2015 conference call:

Gentex historically has been focused on a custom solution, in other words, we're not just competing Mobileye or other large Tier 1s, trying to go head-to-head against Mobileye or any of the other Tier 1s who are becoming more involved in active driver-assist. Gentex is looking at a very customized solution, in other words, it's a homegrown developed camera and imager solution that we bring to the market, and we offer that at a much lower price point than what most of the driver-assist systems are selling for today.

Steve Downing, Q3 2015 call

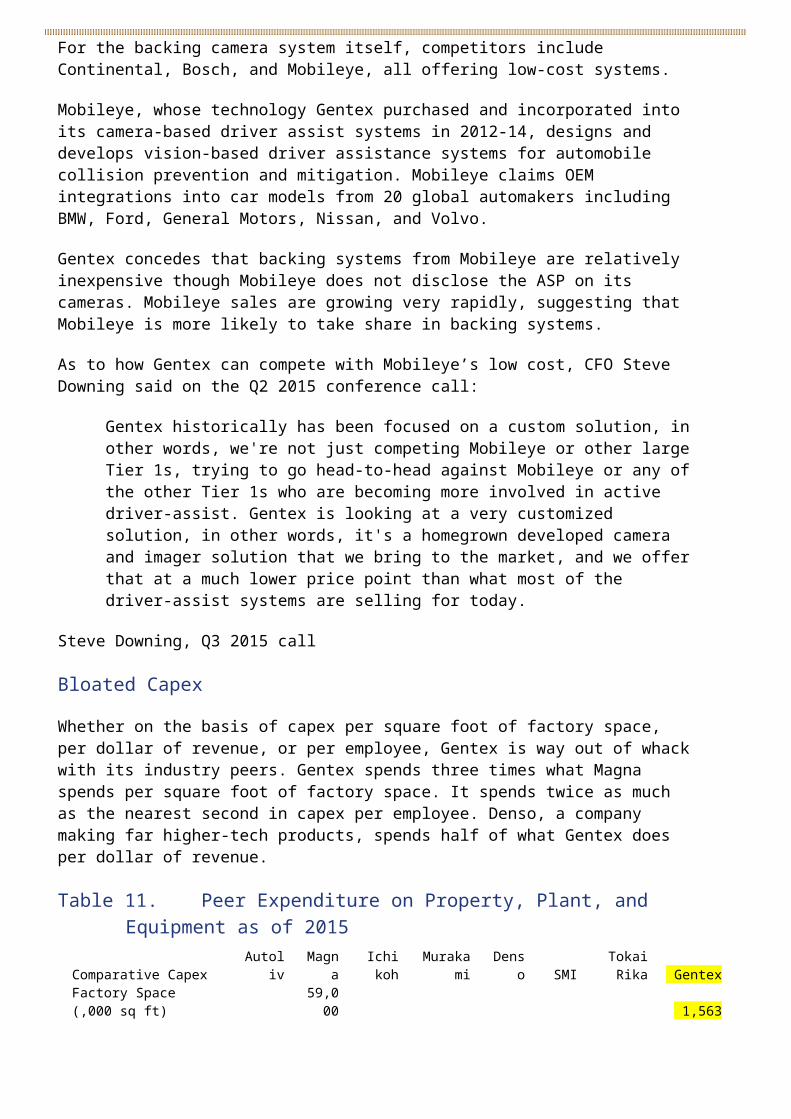

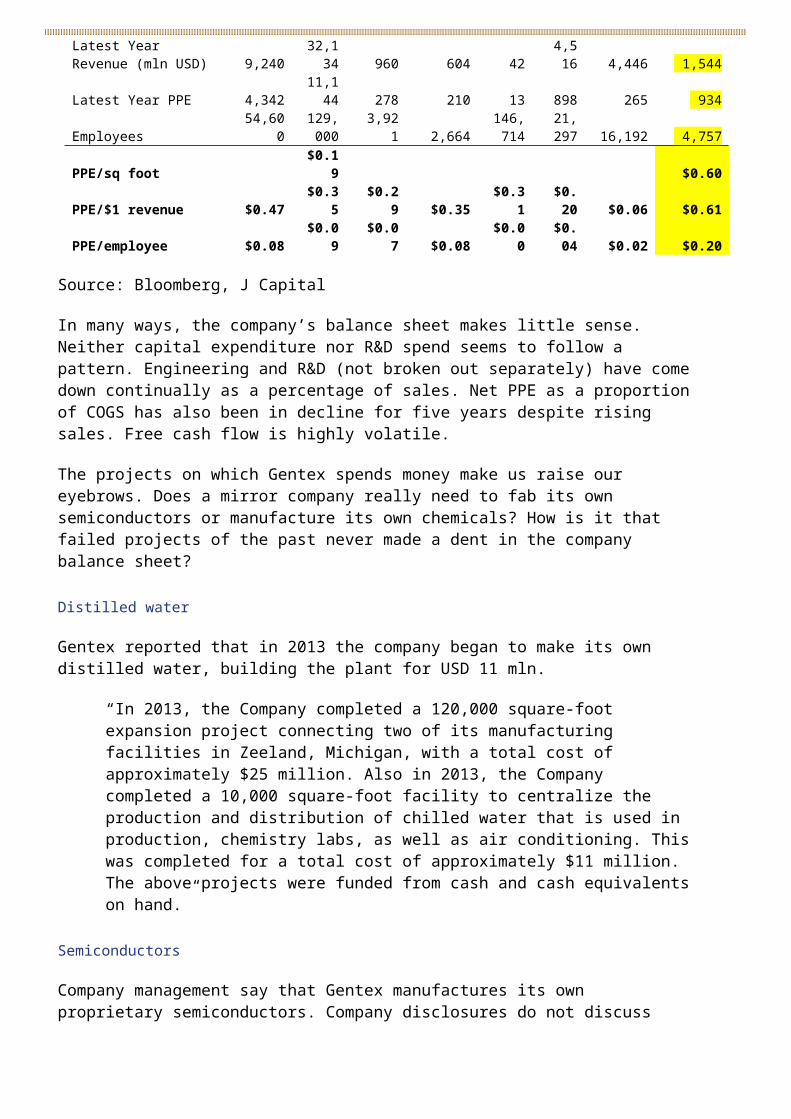

Bloated CapexWhether on the basis of capex per square foot of factory space, per dollar of revenue, or per employee, Gentex is way out of whack with its industry peers. Gentex spends three times what Magna spends per square foot of factory space. It spends twice as much as the nearest second in capex per employee. Denso, a company making far higher-tech products, spends half of what Gentex does per dollar of revenue.

Table 11. Peer Expenditure on Property, Plant, and Equipment as of 2015

Comparative Capex Autoliv Mag

na Ichiko

h Muraka

mi Dens

o SMI Tokai

Rika Gentex Factory Space (,000 sq ft)

59,000 1,563

Latest Year Revenue (mln USD) 9,240

32,134 960 604 42

4,516 4,446 1,544

26

Disclaimers: Last Oct 7, 2012

Latest Year PPE 4,342 11,1

44 278 210 13 898 265 934

Employees 54,600 129,000 3,921 2,664

146,714

21,297 16,192 4,757

PPE/sq foot $0.1

9 $0.60

PPE/$1 revenue $0.47 $0.3

5 $0.2

9 $0.35 $0.3

1 $0.2

0 $0.06 $0.61

PPE/employee $0.08 $0.0

9 $0.0

7 $0.08 $0.0

0 $0.0

4 $0.02 $0.20

Source: Bloomberg, J Capital

In many ways, the company’s balance sheet makes little sense. Neither capital expenditure nor R&D spend seems to follow a pattern. Engineering and R&D (not broken out separately) have come down continually as a percentage of sales. Net PPE as a proportion of COGS has also been in decline for five years despite rising sales. Free cash flow is highly volatile.

The projects on which Gentex spends money make us raise our eyebrows. Does a mirror company really need to fab its own semiconductors or manufacture its own chemicals? How is it that failed projects of the past never made a dent in the company balance sheet?

Distilled water

Gentex reported that in 2013 the company began to make its own distilled water, building the plant for USD 11 mln.

“In 2013, the Company completed a 120,000 square-foot expansion project connecting two of its manufacturing facilities in Zeeland, Michigan, with a total cost of approximately $25 million. Also in 2013, the Company completed a 10,000 square-foot facility to centralize the production and distribution of chilled water that is used in production, chemistry labs, as well as air conditioning. This was completed for a total cost of approximately $11 million. The above projects were funded from cash and cash equivalents on hand.”

Semiconductors

Company management say that Gentex manufactures its own proprietary semiconductors. Company disclosures do not discuss this fab, and visitors are not permitted to view it. We cannot think of a good reason why the simple electronic devices Gentex markets should require a proprietary semiconductor; the level of complexity is something approximating LED Christmas lights that flash alternating colors: printed circuit boards are entirely sufficient to manage the electronic signals. And semi fabs require very significant capital investment.

China facility

In 2006, Gentex purchased a 25,000-square-foot facility in Shanghai at a cost of USD 750,000 to localize final assembly of the mirrors. This was done

27

Disclaimers: Last Oct 7, 2012

because Chinese government policies require automakers to localize at least 75% of their bill of materials, and Gentex was under pressure from OEMs to invoice in local currency. Company executives say that it was inefficient to ship the glass assemblies to Shanghai, and there was breakage, so they closed the facility in the first half of 2014 and resumed shipping from Michigan.

But disclosures say that there was no foreign currency billing at all before 2011. Although executives say that the company was assembling mirrors, the disclosures never indicate any manufacturing in China.

Germany

Gentex’s office and distribution facility in Erlenbach, Germany, is 60% larger than the one in Shanghai yet cost 5.5x as much—USD 5 mln for the 40,000 square foot office and distribution facility. In 2015, the company began building a 50,000 square-foot expansion that is expected to cost USD 7 mln.

Orca

In 1999, the company announced the development of high-intensity white-LED technology under a program called Orca. Gentex never announced a cost for the later-mothballed technology development, but research and development expenses rose by 25% that year. In 2001, Gentex reported that some of the Orca lights had been installed on a limited number of mirrors and sold. Equipment costs rose by USD 42 mln in 2000 and by USD 50 mln in 2001. The company now does not manufacture or sell LEDs and yet it has never recorded any impairment to its investments.

In the 2001 Annual Report, Gentex told investors the company was offering exterior mirrors with LED turning signals based on this technology. In that year, Gentex reported, “. . . [W]e have built new clean-room facilities to house new microelectronics assembly equipment that is capable of producing prototype quantities of LEDs..”

Gentex announced only one vehicle program that would pilot the Orca LED, the Chrysler Sebring Couple. “Strategic discussions with potential alliance partners in the automotive lighting industry, LED component industry and LED chip industry are continuing although discussions are taking longer than anticipated, primarily due to changing business conditions in the LED industry,” the company reported in the 2003 10-K. By the time the 2005 10-K was published, Orca and the LED program had disappeared.

ALS

Another technology that has come and gone at Gentex is “ALS,” which stands for Active Light Sensor, defined as an “intelligent CMOS light sensor to control the dimming of its rearview mirrors,” which Gentex started shipping at volume in 2002, according to its reports. Again. The company never reported any specific R&D or equipment spend for ALS, which it quietly stopped mentioning in reports. Currently, Gentex makes a range of claims for its own CMOS chips used in a variety of imaging devices:

28

Disclaimers: Last Oct 7, 2012

SmartBeam is the Company's proprietary high beam control system integrated into its auto-dimming mirror. SmartBeam Generation 4, which was developed using the fourth generation of the Company's custom designed CMOS imager, has an advanced feature set made possible by the high dynamic range of the imager including: high beam assist; dynamic forward lighting with high beams constantly on; LED matrix beam; and a variety of specific detection applications including tunnel, fog and road type as well as certain lane tracking features to assist with lighting control. The Company believes it has a unique advantage in the automotive industry with SmartBeam. The camera chip is designed by the Company specifically for certain driver assist applications, with custom optics and algorithms written by the Company and specifically tailored for its chip and optical systems. The Company packages the control electronics inside of its interior rearview mirrors with a self-calibrating camera attached to the mirror mount with optimal mechanical packaging which also provides for ease of service.

We believe, however, that Complementary Metal Oxide Semiconductors are overkill for the simple sensors that Gentex requires. In fact, light recognition sensors, extremely simple and commoditized technology, have been used in Gentex’s technology since the days of their “photoelectric” smoke alarms.

Screenshot of a Gentex smoke alarm from eBay May 7, 2016

Microphones

During 2001, the Company developed a new microphone designed specifically for use in the automotive environment for telematics applications. The first volume Gentex microphone application was part of DaimlerChrysler's "U-Connect(R)" telematics system, beginning in 2003. During 2006, our proprietary integrated hands-free microphone was available as part of an optional navigation package at Ford.

The China PlanAmong the growth drivers on which Gentex is depending in garage door opener remotes in China. Unfortunately, there are no home garages in China. Gentex claims this does not matter because their remote device will work with all the public and residential parking lots in China.

On the Q1 2015 call, CFO Steve Downing said:

29

Disclaimers: Last Oct 7, 2012

One of the things we've been working on is introducing HomeLink in the China market, and that includes getting compatibility in place with the garage door industry and the active control industry in China. And over the next several years, we believe there's a lot of opportunity for HomeLink penetration to grow in the China market.

China is a country of very fragmented parking where every housing compound has guards and its own proprietary system where, for example, access has to be updated annually. The cost of integrating all those systems, if it were possible at all, would be prohibitive, and we doubt drivers would care. They generally have to pause for the guards anyway.

The company seems never to have gotten traction in the China market with its mirrors, so there is no particular reason why remotes should be a good business. Staff who formerly worked at the Shanghai facility say that the volume of orders slowed down considerably in 2013 and early 2014 prior to plant closing.

Audit feesAccording to a study by Audit Analytics looking at the audit fees paid by public companies from 2005-2012, the average company paid about 0.08% of revenues for its audit. According to an article that ran in CFO Magazine on February 26, 2015, citing Audit Analytics, smaller firms pay more, averaging USD 5,000 per million in revenues.

Gentex is lucky in that its audit by Ernst & Young cost only USD 380,000 in 2015, up from USD 342,7000 in 2014. That is 0.25% of revenue and much less than the USD 750,000 that the Audit Analytics standards would indicate for a company with USD 1.54 bln in sales in 2015.

The ultimate tell: the cashIn 2014, the company issued a dividend equivalent to 100% of the share price, and yet Gentex did not issue cash to its shareholders: the company issued one new share per existing share, enacting in essence a share split. Management explained that this method was more tax efficient. But the method also conserves cash.

Over the last five years, Gentex has reported average EPS growth of 30% and yet dividend growth has been 7%. While the company does pay a dividend—a rarity with companies we cover—the yield is just over 2%, which seems low when the company reports such high profit and a conservative acquisition strategy. Gentex is sitting on USD 555 mln in cash, representing 25% of its total assets. Apple, perhaps the company in the world that generates the most cash, has 18% of its assets in cash.

Original ListingGentex came to market in 1981 as a client of OTC Net, a penny stock promoter that was closed later in the year under a barrage of SEC complaints. OTC was founded by a Denver-based broker called Juan Carlos Schidlowski. In 1982, the

30

Disclaimers: Last Oct 7, 2012

Securities and Exchange Commission filed a civil complaint against Schidlowski with reference to the Gentex IPO.

A 1982 article in Forbes magazine had called him “salesman of the year,” heavily suggesting that Schidlowski was a con man, and Schidlowski later fled the United States rather than serve a jail term for stock fraud.

The case finding against Schidlowski finds him guilty of the following:

(1)fraud in the purchase and sale of securities, (2) the sale of unregistered securities, (3) bidding for or purchasing securities being distributed before completing participation in the distribution, (4) aiding and abetting OTC Net in violating section 15(c) (3) of the Exchange Act and Rule 15c3-1 by inducing or attempting to induce the purchase and sale of securities while OTC Net's capital was less than the minimum required, and (5) aided and abetted OTC Net in violation of the customer protection rule, the books and records requirements, the preservation of books and records, reporting and notice requirements.

Mickey Fouts, a manager at OTC.net, subsequently sat on the Gentex board for 20 years. Fouts was named in a 2010 civil case claiming unjust enrichment in real estate speculation.3

When Gentex listed, it was a very different company, a manufacturer of smoke detectors, principally for mobile homes, with about USD 5 mln in annual revenues. In the company Prospectus, Gentex discloses that in 1980, the year before the IPO, 79% of sales, USD 3.4 mln, were made to one, undisclosed customer, identified as a direct sales company. Interestingly, based on company disclosures, that customer spent USD 1.969 mln in the last quarter of 1980, as the prospectus was being prepared, compared with an average of USD 850,000 in previous quarters.

SEC Correspondence

In letters in 2007, 2009, 2011, 2012, 2014, and 2015, the SEC has requested that Gentex provide more detailed disclosure: as to the earnings of the HomeLink segment, how Goodwill and Intangibles are calculated and amortized, how the Compensation Committee works. In almost all instances, Gentex’s response was “we already did that.” Here is one example of such a letter, from July 27, 2015; the full correspondence is available on the SEC’s EDGAR platform.

Why?Zeeland, Michigan is a small community of 5,600 people, many of whom are of Dutch origin and belong to the Christian Reformed Church. It is not a wealthy community though it is pleasant, with a low cost of living and proximity to Michigan lakes. Executives at the firm have personal use of a corporate jet and earn high compensation relative to what they might achieve elsewhere, heavily weighted toward share compensation.

3 An article about the suit can be found here.

31

Disclaimers: Last Oct 7, 2012

Online reviews by anonymous employees writing in Glassdoor.com consistently said Gentex pay was below industry average and the company did not pay regular overtime. Share-based compensation at Gentex averages about USD 20 mln per year, a reasonable 6% of profit but a motivator for staff in small Zeeland, Michigan. Reviews for competitor Magna Donnelley. Whose margins are less than half those of Gentex, said the pay was generous.

In November 2015, Chairman Fred Bauer sold USD 25 mln in shares.

We know that Gentex compensation is low by industry standards and that the company relies on share compensation to make up for that. Stock-based compensation reported in the 2015 cash flow statement was USD 21.4 mln, or 6.7% of net income, not Alibaba-style outlandish but still high.

Running this company is a great job if you can get it. At the time of the company’s IPO, Chairman Fred Bauer and two brothers held nearly 50% of the company’s shares. Now Fred Bauer holds less then 2% and the brothers appear to have sold out, yet Bauer remains active as chairman of the company. The sell-down has made Bauer nearly USD 100 mln richer in just the last six years.

Chart 3.Fred Bauer’s Share Sales

Source: Washington Insider

Table 12. Bauer Share Sales Since 2010Name Date Type Shares Gain

(USD ,000) Fred T. Bauer

6/24/16 Exercise 228,000 $1,900.00

Chairman 6/3/16-6/8/16 Sale 618,000 $10,200.00 11/10/15 Sale 762,000 $12,500.00

7/31/15 Exercise 216,000 $1,700.00 10/31/14-11/4/14

Sale 534,000 $17,500.00

7/29/14 Exercise 103,000 $804.00 7/26/13 Exercise 98,000 $827.10

5/8/13 Sale 418,632 $10,300.00 8/9/10 Exercise 189,000 $2,000.00

12/10/10-12/14/10

Sale 500,000 $14,500.00

32

Disclaimers: Last Oct 7, 2012

8/9/10 Exercise 180,000 $466.20 2/9/10-2/17/10 Sale 1,000,000 $18,900.00

Bauer Total $91,597.30

Source: Washington Insider

CatalystsWhere does this end? If Gentex is relying on share price appreciation to pay employees and management, the company needs to keep beating industry growth and profit, as it has done regularly for two decades.

That becomes more difficult if the real base in sales and margins is eroding. It is especially hard in a very transparent industry like automotive components.

Gentex owns no intellectual property in the camera-enhanced mirrors that the company says will bring in big ticket prices and high margins, and competition from companies like Mobileye will make it tough for Gentex to make extravagant claims for the Full Display Mirror. Meanwhile, with technologies like self-driving penetrating automobiles, a garage door opener is a thin reed on which to hang a claim to superior margins, and HomeLink’s market advantage is rapidly being drowned by inexpensive telephone apps. HomeLink is likely to go the way of Garmin and Tomtom GPS devices.

The wider promulgation of LCD screens in cars also makes the argument that the mirror is a “platform” for technology much harder to sustain.

To cope with these headwinds, we are guessing that Gentex will start to announce dramatic gains from the last large but opaque market, China. It may also make a large acquisition. We figure one or both of those events will occur in the coming 12 months. In China, Gentex says it will sell a lot of HomeLink devices modified to open gates at private compounds and public parking lots, given that China has virtually no private garages. We can state with a high degree of assurance that that is not practicable and that Gentex will never be able to make high-margin sales in China.

As to an acquisition, perhaps of a company making toll-pass devices or self-driving technology of some description, that may be a little harder, but if it happens, Gentex will almost certainly report lifting the margins at the acquired company.

Company responseGentex IR has been open and generous with its time. However, after we provided them with our initiation report, the company was extremely angered and vowed not to communicate with us again. We find company management amiable but promotional.

Valuation

33

Disclaimers: Last Oct 7, 2012

We value Gentex on a DCF basis. We estimate income growth of 10% for 2016 but apply a 20% gross margin instead of the 40% that is reported. Other numbers in our model remain as reported by Gentex, and we assume no new debt. Given estimates for increases in interest rates, we believe our terminal WACC of 6.4% is generous and, given current growth of the auto industry, terminal growth of 3% fair. Based on these assumptions, we derive a share price of USD 9.10.

On a price to earnings basis, if we apply our estimated 20% margin, the model yields net income for 2016 of about USD 110 mln. At the current 17x P/E ratio, the target price would be USD 7.01.

Risks The mirror-embedded, RCD camera may prove extremely popular and

have an advantage over cameras displayed on auto LCD screens. Gentex may have industry value that we underestimate by virtue of

misunderstanding the automotive industry’s purchasing dynamics. Gentex may be small enough to have created its own niche distinct from

the rest of the auto industry’s dynamics.