Embed Size (px)

Citation preview

Introductory Financial Accounting

ACCT11081

Lecturer: Martin Turner

S0174168

Assignment – Step 7 - 11

Step 7 – Inventory

Step 8 – MYOB

Step 9 – Business Transactions

Step 10 – Depreciation

Step 11 - Feedback

C h r i s ti C h a p m a n P a g e | 2

Step 7 – Inventory

From the Lecture on Wednesday, I had a few KC&Qs about exactly how am I supposed to remember the four types of cost of inventory methods. I mean is that another thing that we are to memorise? I think it is best to say yes. I understood when Maria explained about the two types of inventory accounting systems: perpetual and periodic. I know perpetual because when I use to help my mate over at her electrical business, whenever an item would be sold, she would just double check that there were ‘X’ number of items left as the same as the current inventory list they had in their systems. To double check everything though, every financial year she does do a stock take inventory just in case. So, a KC&Q that I have is where exactly am I going to find the information to answer this question. What is it going to tell me? I already know so much about the company. Inventory would affect RCG because it relies a lot on their sales. So, usually I would start from the most recent financial year, which would have been 2016 but because I have looked over the annual reports I have decided I want to start with 2013 and move so I can show some history of this step. Why would you do that you might also. I tend to ask myself but when was going over these I found something interesting… so keep reading 😊……

2013

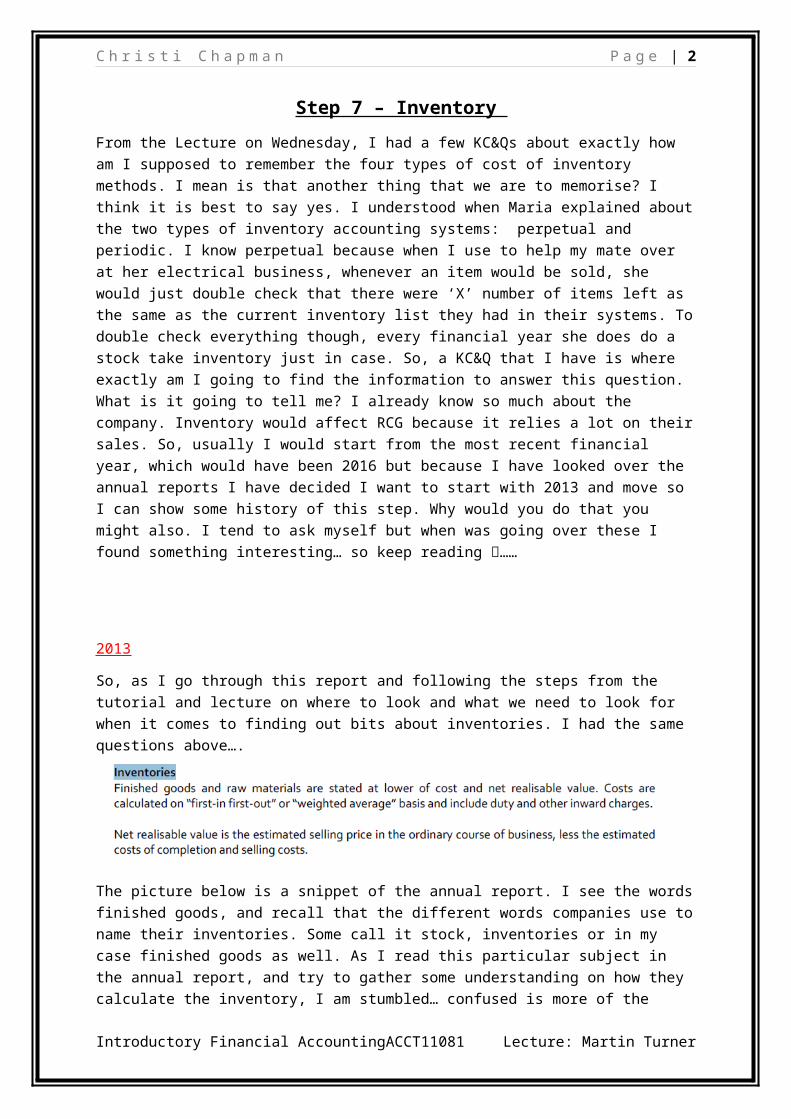

So, as I go through this report and following the steps from the tutorial and lecture on where to look and what we need to look for when it comes to finding out bits about inventories. I had the same questions above….

The picture below is a snippet of the annual report. I see the words finished goods, and recall that the different words companies use to name their inventories. Some call it stock, inventories or in my case finished goods as well. As I read this particular subject in the annual report, and try to gather some understanding on how they calculate the inventory, I am stumbled… confused is more of the correct term. I mean it clearly states that the costs are calculated on ‘First-in, first-out (FIFO)’ or ‘weighted average’. Big KC&Q comes to my head in logically thinking, why would you have two methods, wouldn’t that throw out all figures? Or does half the business do FIFO and the other half do the weighted average. As we had learnt this in the lecture FIFO is when the company assumes that the cost of the first units attained is the cost of the first units sold and the Weighted Average is the average cost per unit is calculated to regulate the price of ending inventory. That the cost of the units on hand is the cost of the units recently purchased. As I wrote that last sentences, it dawned on me, maybe its certain brands of RCG that uses FIFO and certain ones use the weighted average. But it still brings me question to light wouldn’t that throw everything out?

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 3

2014

Now first I just want to point out, I will be putting the inventories paragraph from each of the annual reports. It’s for my learning. It might seem unnecessary but for me this is what I need, and to clarify, it’s not the same picture as 2013. Lol…. Even though they do state the same exact information, it’s not the same picture. Anyways, so this is telling me that RCG is being consistent and using the same methods for calculating the costs of inventory as the previous year.

2015

Now 2015 has some text changes to this financial report. It shows the same method of calculating the cost of inventory however there is more detailed information. There is information regarding what the cost comprises of. This makes me think and question, have they had management change in the finance department that has explained to them that this detail might be required. Because in previous years, it just states ‘includes duty and other inward charges’. Why would RCG have to divulge that specified information? I also

2016

This annual report really took me by surprise. I was expecting to see the same consistent information that RCG uses FIFO and the average weighted to calculate their inventory. Fortunately for me, yes it’s pretty sweet when you find out more information about your company. Anyhow, for this financial

year, RCG decided that it dropped the FIFO method and only use the average weighted method to calculate their inventory. A KC&Q straight away for me is why did they drop FIFO as a method. Was it a strategy that finance suggested to the board that on method is necessary for calculating the cost of inventory, or was it another department? I only ask this question because if my three week internship at BOQ. I was an intern as a procurement analyst. I learnt that as a procurement analyst, your role is to work towards making sure the company has the best saves.

Overall over the past four years of annual reports it seems that RCG has made some adjustments, however unfortunately for me, I was unable to determine if the system of accounting RCG used was

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 4

wither perpetual or periodic. However, I will just state that with the amount of brands that RCG has I am assuming that they use the perpetual system to keep track of their inventory.

When I look at RCG’s assets both current and non-current it makes me question the detail of how these figured come to light.

Assets 2016($’000)

2015($’000)

2014($’000)

2013($’000)

Current Cash and cash equivalents 44,573 29,990 16,097 15,105Trade and other receivables 25,472 23,701 11,576 10,342

Inventories 78,534 71,445 13,221 8,455Derivative financial instruments

- 2,412 - 493

Other 2,730 1,231 1,449 1,260Total current assets 151,309 128,779 42.325 35,664

Non-Current Asset 2016($’000)

2015($’000)

2014($’000)

2013($’000)

Receivables 869 869 506 -Property, plant and equipment

42,620 28,403 6,604 4,202

Intangibles 245,875 248,486 22,896 17,495Deferred Tax 10,652 5,699 1,429 937Total Non-Current Assets 300,016 283,457 31,525 22,634

I mean I cash and cash equivalent are pretty straight forward but trade receivables had me confused? I noticed the in the breakdown of the assets within note 10, it had ‘provisions for impairment of receivables’. Also at the bottom of that particular note section it states for more information to see Note 34 and so I did. It revealed to me that RCG recognised loss of $321,000 in 2016, whereas in 2015 there was only a loss of $24,000. To me that seems like a massive jump in figures. It just brings a big KC&Q of what could cause such a high spike in loss??

However, what the receivables in the non-current assets made me look at the notes and to gather a better understanding of where those figures came from made me question. Then looking at Note 14, I see the same amount of loans to outside shareholders in the TAF Partnership stores, which seems that business is consistent. I see the words TAF Partnership stores it raises a big KC&Q who are the TAF Partnership stores or what does TAF stand for? I actually feel a little stupid right now though in realising that TAF is the acronym they use for The Athlete’s Foot…. Well makes my KC&Q seem irrelevant. Talk about blonde moments. Anyhow, as I read though the breakdown of each current asset, I am drawn to the fact that it shows plant and equipment, intangible, and deferred with their

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

Total Assets 451,325 412,236 73,850 58,298

C h r i s ti C h a p m a n P a g e | 5

figures of actual costs (at costs) then it shows where the depreciation or amortisation has taken place. I will cover this further in Step 10 – Depreciation.

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 6

Step 8 – MYOB

Understanding Mind Your Own Business (MYOB). Please note that this step seems to show a lot of screenshots, but it explains why as you read on. I figure, it might seem messy and confusing but it does explain my trail of learning.

So, as I start this step I have followed the steps according to the assignment. First issue I have is once the software is downloaded the softeware does not setup to the computer due to the message below.

When I started to download the MYOB AccountRight software, I clicked the next buttons and when I selected finished, this message showed up stating that the Setup Failed. I asked John about it, and he said he would raise this with Martin and Maria as he said he had a similar situation when he downloaded this software. John asked some of the other students to do the same and see if they were to have the same issue. There were about 4 others in our group that showed the same Setup Failed issue.

John enquired this to Maria and Martin. Maria explained that we are to watch the tutorials which would take about an hour and a half to watch and complete. From that tutorial, it is suppose to explain about setting up of MYOB and understanding it. There is a quiz at the end of the tutorial and according to the step 8, we are to take screenshots of our progress. So, I guess I know what I will have to do before the Tutorial class this afternoon. I did express to John though, that I was just following what I was reading in the assignment steps, and it clearly states to download MYOB before watching the tutorials.

Setting up ready to watch this tutorial, my first issue is that the tutorial page would not work in google chrome. I recall Maria stating in the lecture we just had that this might occur, so I may have to use another internet gateway. So I used Internet Explorer and it works just fine. As I am moving through the tutorial, I thought to myself, maybe it may have been the internet search engine itself,

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 7

so I downloaded the MYOB from Internet Explorer and it downloaded…

Progressing through the 3hour tutorial…..

After an afternoon of watching these tutorials, a break is really equired… Its so exausting sitting there hour after hour watching tutorials. Even though they are educational, a break is always required. I was just luckyenough that I had an appointment and then trainings for sports so I had a big break.. This meant that I had to be up early, to continue working on the assignments.

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 8

Finally, I have completed the three-hour tutorial… now to complete the quizzes.

When I first read the assignment I read the steps of the screen shots as the screenshots above, but watching the tutorial that maria put up, and glad I did, because it clarified my understanding and made me realise I have the wrong screenshots that are required. So, here I go again, of screenshotting the setup of MYOB. 😊

Excuses I know however, my laptops mouse pad is really touchy and I clicked next before screen shotting the last page that is needed…..

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 9

Now it is time to complete the MYOB Online Training Skills Test.

Quiz 1

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 10

Quiz 2

Quiz 3

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 11

Quiz 4

Quiz 5

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 12

Quiz 6

Quiz 7

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 13

Quiz 8

Quiz 9

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 14

Quiz 10

This was the only question I got wrong. I guess, it seems so simple when I relook at it. I think I should sit and read the question properly next time.

Quiz 11

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 15

Quiz 12

Quiz 13

These tutorials and the online tests have really helped me gain more of an understanding of MYOB. I have used a few operating accounting systems when I have helped mates out with book keeping in their business but never MYOB.

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 16

Step 9 – Business Transactions

Business transactions for my company was a little hard for me to create at first. I mean RCG Corporation Limited is a huge company. My point being that due to the company having so many brands. After reading the annual reports and knowing that RCG is the parent head of the company, it has three major sub groups that the brands are broken up into a group called RCG Brands, The Accent Group and The Athlete’s Foot. I make that clear as I thought to show everyday transactions of this company I had to create three different accounts under the assets account. It was later explained to me that that is just creating more finances and reports. It was ok to do the way I was thinking, but when if it would be time to do a financial report for the year, it’d just create more paper than needed. So, I created only one main account in assets.

Also, I state that I had a little hard time to create my first transaction, only because of the amount of detail I wanted to have in my transactions. I wanted to put all these transactions and explained them to John in one tutorial and he just explained to me that I get that but we just to know you are learning and understanding that you know how to use MYOB. So, here I was creating some basic transactions from customer’s purchases of certain footwear, paying employee’s wages, paying the executive board members their remuneration, paying suppliers and bills from the time period of 7 th August to the 22nd of September.

There are two customers that are training/employment companies. I added these in for sales because I know employment/training companies help their students with equipment or gear when necessary.

List of Transactions

Transaction 1

Tony Stark is a miner that prides himself in having good presentation. As he works in the mines, sometimes he doesn’t have much time to shop, so he buys in quantities of five for his boots each month because he says he can never have enough boots. Tony also like having good style shoes when he is home and goes out for a night on the town and joggers for when he goes to the gym at camp and work out when he’s home. So, this transaction sees Tony purchasing TEN (10) different types of DC Hype shoe products @ $189.89, five (5) CAT boots @ $200.99, and three (3) different types of Athlete’s Foot joggers @ $122.69.

Total Transaction = DC Hype products + CAT products + Athlete’s Foot products

= $(189.89 x 10) + (200.99 X 5) + (122.69 X 3)

= $ 3, 271.92

Broken down = sales of income will cost $2,974.47 and Goods and Services Tax (GST) collected will be $297.45.

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 17

Transaction 2

As stated earlier, there are training/employment groups who order footwear from RCG or certain brands retailers to help assist their clients gain employment or help with needs of their employment. Wide Bay Training has purchased 25 CAT boots @ $199.89 and 25 Athlete’s Foot joggers @ $189.89. However due to the quantity sizes of each footwear apparel the store gave a 10% discount on each.

Total Transaction

= ((CAT products x 25) - CAT products x 25 x 10%) + ((Athlete’s Foot products x 25) – Athlete’s Foot products x 25 x 10%)

= (199.89 X 25) – 199.89 X 25 X 0.10) + ((189.89 X 25) – 189.89 X 25 X 0.10)

= $ 8,770.06

Total sales of income = $7972.78 and GST Collected = $797.28

Transaction 3

Alike Wide Bay Training, Glasco Training purchases uniform and equipment for their clients. GLasco Training required 5 pairs of joggers from The Athlete’s foot. These products were purchased at $189.89 each.

Total transaction - Athlete’s Foot Products x 5

= $ 189.89 x 5

= $ 949.45

$863.14 went to sales of income and $86.31 went to GST Collected.

Transaction 4

Wide Bay Training needed to purchase more footwear apparel for clients. This purchase was for ten CAT boots @ $189.89.

Total transaction = CAT Boots x 10

= $189.89 x 10

= $1,898.90

$1,726.27 went to Sales Income and $172.63 went to CST Collected.

Transaction 5

David Wall was just a one-off customer that came to purchase 2x joggers @ $189.89 and a pair DC Hype shoes @ $155.00 at one of the outlets. The only thing is in the transactions doesn’t show that he paid cash for this transaction. This means I probable have put it in a different account that I should have placed it in. Wooops….

Total purchase = DC procucts + (Athlete’s Foot products x 2)

= $155.00 + $189.89 x 2

= $ 949.45

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 18

Transaction 6

This transaction is the payment of Tessa Baldwin’s wages. Tessa is an employee of RCG, that works 15 hours per week at one of the brands retail stores in Bundaberg. She earns $16.72 per hour. Tessa gets paid weekly. Tessa’s weekly wage she earns is under the tax threshold, so she doesn’t have to pay tax each week.

Tessa’s Weekly Wage = $16.72 x 15 hours

= $ 250.80

Transaction 7

This transaction is the payment of John Snow’s weekly wages. John is a sales assistant of one of the brands retail stores in Bundaberg. John gets paid $21.78 per hour. HE also gets paid weekly. Unlike Tessa, john earns enough that he must pay tax.

John’s Weekly Wage = $21.76 x 20

= $ 435.60

$435.60 is deducted from Wages and Salaries expenses and $418.60 paid into John’s elected bank account and $17.00 is paid into PAYG Withholding payable account (Tax).

Transaction 8

Transaction 8 is the payment of Regional Manager Christi Chapman. This employee that is on the executive committee and is on a salary (please note this employee and the figures are made up). Christi receives her wages weekly. She earns an annual salary of $150,000.

Total weekly wages = Annual Salary / 52 weeks

= $150,000 / 52

= $2,884.62

Each week Christi receives $1,996.62 in her elected electronic bank account and $888.00 of the $2884.62 that is deducted from Wages and Salaries expenses is paid into PAYG Withholding payable account.

Transaction 9

In any company, the executive board members are payed remuneration. Ivan Hammerschlag is RCG Corporation’s Chairman. Mr Hammerschlag has over 35 years of experience in specialised retail and is a former Chief Executive Office (CEO). As the Chairman Mr Hammerschlag earns $180,000 remuneration. I have provided this transaction twice in the transactions journal as I suggested that he gets paid fortnightly.

Calculations of Remuneration:

Fortnightly Remuneration = Annual remuneration / 26 weeks

$180,000 / 26 weeks = $6,923.078 = $6,923.08

Total Fortnights Earnings = fortnightly Remuneration – Tax

$6,923.08 - $2,226.00 = $4,697.08

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 19

Transaction 10

This final transaction is to pay a supplier for their services that RCG is currently using. To have stores functioning well, stores need to have electricity to power the lights, the tills and so forth. Hypothetically RCG has a partnership agreement with Ergon Energy to facilitate all their stores throughout Australia. This bill that is paid seems like an extremely large amount, however this bill is a combined bill of 5 stores varying from certain states in one for the three-month period of July-September. This was a total of $58,697.08. this transaction shows that it hasn’t been paid and is waiting to be paid. This is the same for transaction 11. It is a bill for Telstra, with similar background to Ergon Energy, except this is a combined bill for 4 stores for the month of August which is still outstanding.

However, if you see in Transaction 12 and Transaction 13, it shows the purchases of these services are paid. With each figure being deducted from their expenses and GST Paid accounts and credited to the trade creditors account.

RCG Limited Corporation #1719 Elizabeth Street

Waterloo NSW

2017

All Journals7/08/2017 To 20/09/2017

ID No.Account

No.Account

Name Debit CreditJob No.

SJ 8/08/2017 Tony, Stark

00000001 1-1310 Trade Debtors

$3,271.92

00000001 4-1000 Sales Income #1

$2,974.47

00000001 2-1210 GST Collected

$297.45

SJ 9/08/2017 Sale; Wide Bay Training

00000002 1-1310 Trade Debtors

$8,770.06

00000002 4-1000 Sales Income #1

$7,972.78

00000002 2-1210 GST Collected

$797.28

SJ 9/08/2017 Sale; Glasco Training

00000003 1-1310 Trade Debtors

$949.45

00000003 4-1000 Sales Income #1

$863.14

00000003 2-1210 GST Collected

$86.31

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 20

SJ 9/08/2017 Sale; Wide Bay Training

00000004 1-1310 Trade Debtors

$1,898.90

00000004 4-1000 Sales Income #1

$1,726.27

00000004 2-1210 GST Collected

$172.63

SJ 9/08/2017 Wall, David

00000005 1-1310 Trade Debtors

$534.78

00000005 4-1000 Sales Income #1

$486.16

00000005 2-1210 GST Collected

$48.62

CD

14/08/2017

BALDWIN, TESSA

5 1-1110 Business Bank Account #1

$250.80

5 6-4100 Wages & Salaries Expenses

$250.80

CD

14/08/2017

SNOW, JOHN

5 1-1220 Electronic Clearing Account

$418.60

5 6-4100 Wages & Salaries Expenses

$435.60

5 2-1410 PAYG Withholding Payable

$17.00

CD

14/08/2017

CHAPMAN, CHRISTI

6 1-1220 Electronic Clearing Account

$1,996.62

6 6-4100 Wages & Salaries Expenses

$2,884.62

6 2-1410 PAYG Withholding Payable

$888.00

CD

4/09/2017 HAMMERSCHLAG, IVAN

3 1-1220 Electronic Clearing Account

$4,697.08

3 6-4100 Wages & Salaries Expenses

$6,923.08

3 2-1410 PAYG Withholding Payable

$2,226.00

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 21

CD

6/09/2017 Ergon Energy 239 Hills Street Melbourne QLD 2342 Australia

2 1-1110 Business Bank Account #1

$58,697.00

2 2-1510 Trade Creditors

$58,697.00

CD

6/09/2017 Telstra 8773 Ann Street Brisbane QLD 4000 Australia

3 1-1110 Business Bank Account #1

$27,700.00

3 2-1510 Trade Creditors

$27,700.00

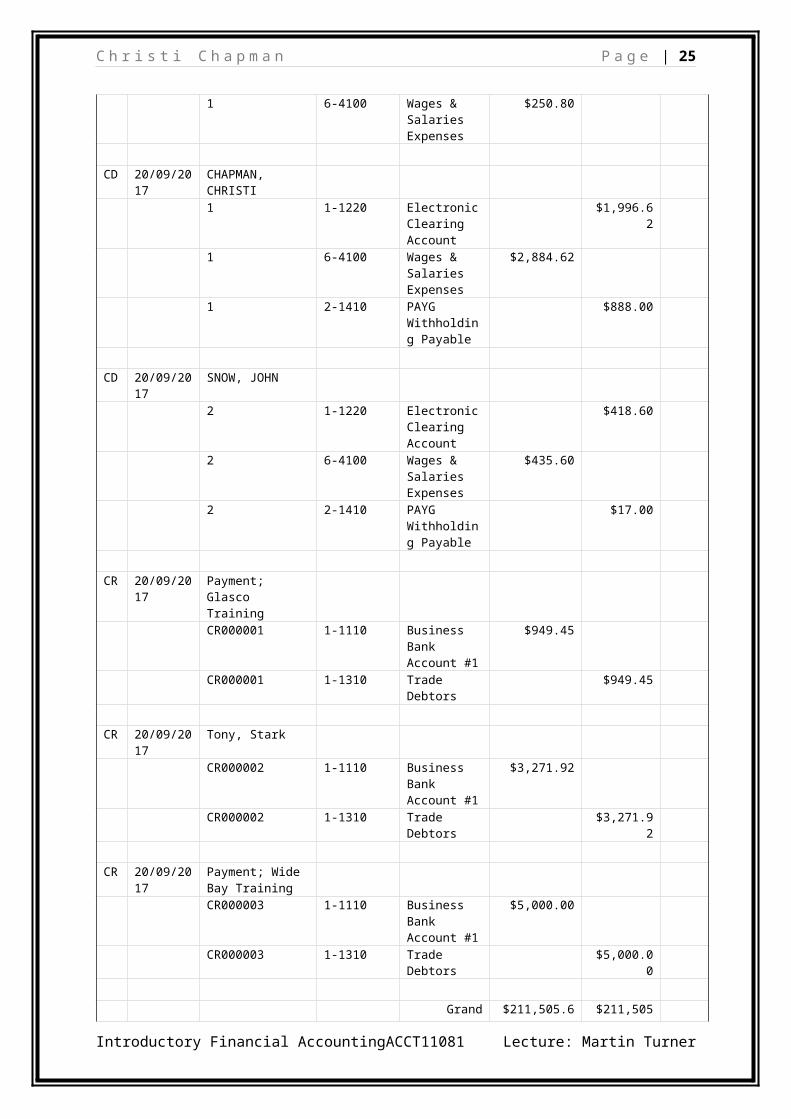

PJ 20/09/2017

Purchase; Ergon Energy

00000001 2-1510 Trade Creditors

$58,697.00

00000001 6-1700 Electricity Expenses

$53,360.91

00000001 2-1220 GST Paid $5,336.09

PJ 20/09/2017

Purchase; Telstra

00000002 2-1510 Trade Creditors

$27,700.00

00000002 6-2000 Telephone Expenses

$25,181.82

00000002 2-1220 GST Paid $2,518.18

CD

20/09/2017

BALDWIN, TESSA

1 1-1110 Business Bank Account #1

$250.80

1 6-4100 Wages & Salaries Expenses

$250.80

CD

20/09/2017

CHAPMAN, CHRISTI

1 1-1220 Electronic Clearing Account

$1,996.62

1 6-4100 Wages & Salaries Expenses

$2,884.62

1 2-1410 PAYG Withholding Payable

$888.00

CD

20/09/2017

SNOW, JOHN

2 1-1220 Electronic Clearing

$418.60

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 22

Account 2 6-4100 Wages &

Salaries Expenses

$435.60

2 2-1410 PAYG Withholding Payable

$17.00

CR

20/09/2017

Payment; Glasco Training

CR000001 1-1110 Business Bank Account #1

$949.45

CR000001 1-1310 Trade Debtors

$949.45

CR

20/09/2017

Tony, Stark

CR000002 1-1110 Business Bank Account #1

$3,271.92

CR000002 1-1310 Trade Debtors

$3,271.92

CR

20/09/2017

Payment; Wide Bay Training

CR000003 1-1110 Business Bank Account #1

$5,000.00

CR000003 1-1310 Trade Debtors

$5,000.00

Grand Total: $211,505.60 $211,505.60

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 23

RCG Limited Corporation #1719 Elizabeth Street

Waterloo NSW2017

Balance SheetAs of 22/09/2017

Assets Current Assets Bank Accounts Business Bank Account #1 $41,927,991.73 Total Bank Accounts $41,927,991.73 Clearing Accounts Electronic Clearing Account

($14,224.60)

Total Clearing Accounts ($14,224.60) Other Current Assets Trade Debtors $534.78 Total Other Current Assets $534.78 Total Current Assets $41,914,301.91 Total Assets $41,914,301.91Liabilities Current Liabilities GST Liabilities GST Collected $1,402.29 GST Paid ($7,854.27) Total GST Liabilities ($6,451.98) Payroll Liabilities PAYG Withholding Payable

$6,262.00

Total Payroll Liabilities $6,262.00 Total Current Liabilities ($189.98) Total Liabilities ($189.98)Net Assets $41,914,491.89Equity Current Year Earnings ($85,508.11) Historical Balancing $42,000,000.00 Total Equity $41,914,491.89

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 24

RCG Limited Corporation #1719 Elizabeth Street

Waterloo NSW2017

Profit & Loss Statement7/08/2017 To 22/09/2017

Income Sales Income #1 $14,022.82 Total Income $14,022.82 Total Cost Of Sales $0.00 Gross Profit $14,022.82 Expenses General Expenses Electricity Expenses $53,360.91 Telephone Expenses $25,181.82 Total General Expenses $78,542.73 Payroll Expenses Wages & Salaries Expenses $20,988.20 Total Payroll Expenses $20,988.20 Total Expenses $99,530.93 Operating Profit ($85,508.11) Total Other Income $0.00 Total Other Expenses $0.00 Net Profit/(Loss) ($85,508.11)

So, this profit and loss statement shows that for this period of shows that RCG would be at a loss with the amount of spending they are doing. This is only for a small proportion of a time that shows more expense transactions than income sales. To do this task to show my understanding of MYOB I had more expensive bills than they are of sales to customers. If I had done that Then the transactions list would have been so long and then the first 10 transactions probable would have just been sales.

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 25

RCG Limited Corporation #1719 Elizabeth Street

Waterloo NSW2017

Statement of Cash Flow7/08/2017 To 22/09/2017

Account Name

Cash Flow from Operating Activities

Net Income ($85,508.11) Trade Debtors ($534.78) GST Collected $1,402.29 GST Paid ($7,854.27) PAYG Withholding Payable $6,262.00 Net Cash Flow from Operating Activities

-$86,232.87

Cash Flow from Investing Activities Net Cash Flow from Investing Activities

$0.00

Cash Flow from Financing Activities

Net Cash Flow from Financing Activities

$0.00

Net Increase/Decrease for the period

-$86,232.87

Cash at the Beginning of the period $42,000,000.00Cash at the End of the period $41,913,767.13

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 26

Step 10 – Depreciation

Depreciation is defined as the decrease in the worth of an asset over a period time that affects their economic worth through use, wear and tear and uselessness. So, my understanding would be if a company buys a brand-new company car that is being used over the next four years. A car might have a life of 10 plus years, however the depreciation cost of the car for this company is for the next four years. As I go through my annual reports about depreciation in the Statement of Profits or Loss and Comprehensive Income, under expenses it doesn’t just state ‘depreciation’, it states ‘Depreciation and Amortisation expense’. This brings a KC&Q of what is the difference. Amortisation is process of allocating the cost of an intangible asset over a period of time. So, to me it is putting aside money to pay off debts over tome. This made me look for the accounting policies to see which is used. I found the accounting policies pretty quick as they were at the start of in Notes 2. This is very informative as it gave me more understanding on how RCG applies these policies to assets and liabilities.

What I found interesting is when I read each of the assets and non-current asset it gave me a lot more understanding. For example: trade and other receivables are recognised at their value and are measured at an amortised coast using th effective interest method. It also states that usually settled within 30 – 60 days. Some investments and other financial assets are measured at either amortised cost or at fair value depending on their classifications.

RCG calculates its depreciation on a straight-line basis to write off the net cost of each item of property, plant and equipment (excluding land) over their expected lives as the following:

Plant and Equipment: 5-8 years

Assets under construction: Not depreciated

A KC&Q that raises a flag straight is what assets would be under construction? Why wouldn’t it become depreciated? Finite life intangible assets are amortised. Indefinite life intangibles assets are not. This made me look at the notes nine to seventeen to see figures of how its broken down.

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 27

Step 11 – Feedback

Step 11 – Feedback Feedback from: Christi ChapmanFeedback to:

CommentsStep 7 - Inventory

Step 8 – MYOB

Step 9 – Transactions

Step 10 – Depreciation

Overall

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 28

Step 11 – Feedback Feedback from: Christi ChapmanFeedback to:

CommentsStep 7 - Inventory

Step 8 – MYOB

Step 9 – Transactions

Step 10 – Depreciation

Overall

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner

C h r i s ti C h a p m a n P a g e | 29

Step 11 – Feedback Feedback from: Christi ChapmanFeedback to:

CommentsStep 7 - Inventory

Step 8 – MYOB

Step 9 – Transactions

Step 10 – Depreciation

Overall

Introductory Financial Accounting ACCT11081 Lecture: Martin Turner