Embed Size (px)

Citation preview

Page 1 of 10

West African Resources Ltd (WAF)

Gold

: D

evelo

per

/ E

xp

lore

r

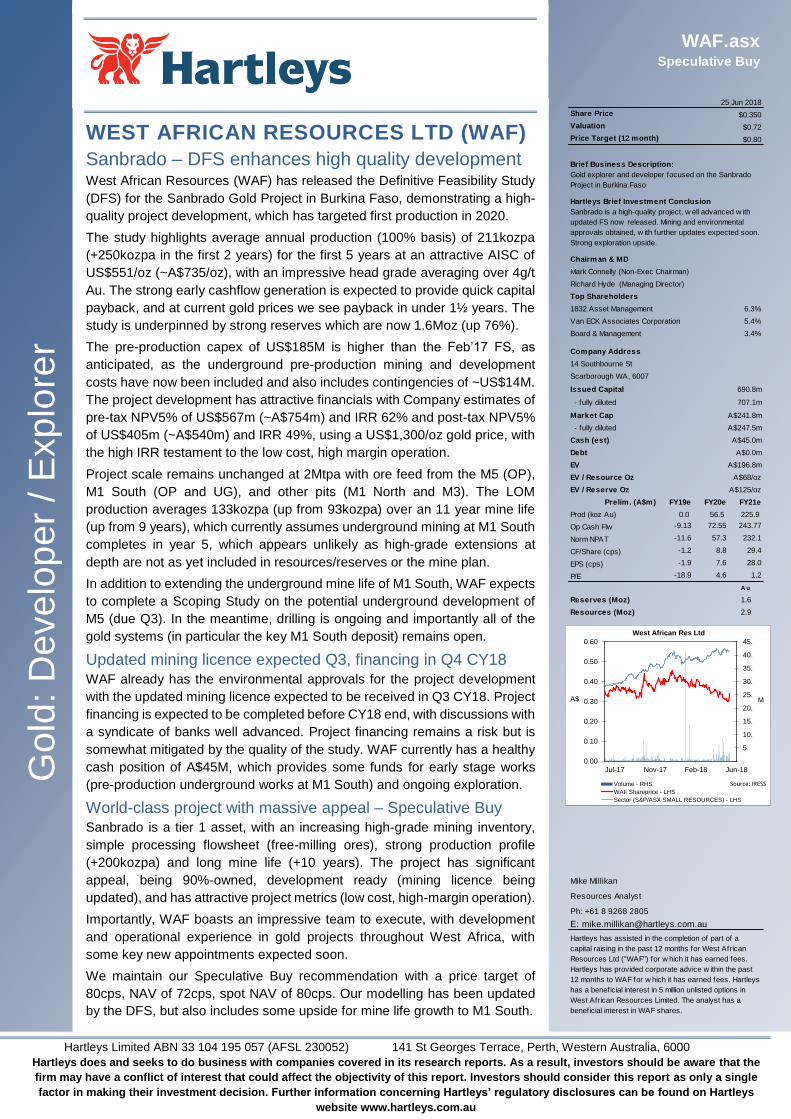

WAF.asxSpeculative Buy

Share Price

Valuation $0.72

Price Target (12 month) $0.80

Brief Business Description:

Hartleys Brief Investment Conclusion

Chairman & MD

Top Shareholders

1832 Asset Management 6.3%

Van ECK Associates Corporation 5.4%

Board & Management 3.4%

Company Address

Issued Capital

- fully diluted

Market Cap

- fully diluted

Cash (est)

Debt

EV

EV / Resource Oz

EV / Reserve Oz

Prelim. (A$m) FY19e FY20e FY21e

Prod (koz Au) 0.0 56.5 225.9

Op Cash Flw -9.13 72.55 243.77

Norm NPAT -11.6 57.3 232.1

CF/Share (cps) -1.2 8.8 29.4

EPS (cps) -1.9 7.6 28.0

P/E -18.9 4.6 1.2

A u

Reserves (Moz) 1.6

Resources (Moz) 2.9

Mike Millikan

Resources Analyst

Ph: +61 8 9268 2805

690.8m

25 Jun 2018

$0.350

Richard Hyde (Managing Director)

14 Southbourne St

Scarborough WA, 6007

Sanbrado is a high-quality project, w ell advanced w ith

updated FS now released. Mining and environmental

approvals obtained, w ith further updates expected soon.

Strong exploration upside.

Mark Connelly (Non-Exec Chairman)

Gold explorer and developer focused on the Sanbrado

Project in Burkina Faso

707.1m

A$241.8m

A$247.5m

A$196.8m

Hartleys has assisted in the completion of part of a

capital raising in the past 12 months for West African

Resources Ltd ("WAF") for w hich it has earned fees.

Hartleys has provided corporate advice w ithin the past

12 months to WAF for w hich it has earned fees. Hartleys

has a beneficial interest in 5 million unlisted options in

West African Resources Limited. The analyst has a

beneficial interest in WAF shares.

A$125/oz

A$0.0m

A$45.0m

A$68/oz

WEST AFRICAN RESOURCES LTD (WAF)

Sanbrado – DFS enhances high quality development West African Resources (WAF) has released the Definitive Feasibility Study

(DFS) for the Sanbrado Gold Project in Burkina Faso, demonstrating a high-

quality project development, which has targeted first production in 2020.

The study highlights average annual production (100% basis) of 211kozpa

(+250kozpa in the first 2 years) for the first 5 years at an attractive AISC of

US$551/oz (~A$735/oz), with an impressive head grade averaging over 4g/t

Au. The strong early cashflow generation is expected to provide quick capital

payback, and at current gold prices we see payback in under 1½ years. The

study is underpinned by strong reserves which are now 1.6Moz (up 76%).

The pre-production capex of US$185M is higher than the Feb’17 FS, as

anticipated, as the underground pre-production mining and development

costs have now been included and also includes contingencies of ~US$14M.

The project development has attractive financials with Company estimates of

pre-tax NPV5% of US$567m (~A$754m) and IRR 62% and post-tax NPV5%

of US$405m (~A$540m) and IRR 49%, using a US$1,300/oz gold price, with

the high IRR testament to the low cost, high margin operation.

Project scale remains unchanged at 2Mtpa with ore feed from the M5 (OP),

M1 South (OP and UG), and other pits (M1 North and M3). The LOM

production averages 133kozpa (up from 93kozpa) over an 11 year mine life

(up from 9 years), which currently assumes underground mining at M1 South

completes in year 5, which appears unlikely as high-grade extensions at

depth are not as yet included in resources/reserves or the mine plan.

In addition to extending the underground mine life of M1 South, WAF expects

to complete a Scoping Study on the potential underground development of

M5 (due Q3). In the meantime, drilling is ongoing and importantly all of the

gold systems (in particular the key M1 South deposit) remains open.

Updated mining licence expected Q3, financing in Q4 CY18 WAF already has the environmental approvals for the project development

with the updated mining licence expected to be received in Q3 CY18. Project

financing is expected to be completed before CY18 end, with discussions with

a syndicate of banks well advanced. Project financing remains a risk but is

somewhat mitigated by the quality of the study. WAF currently has a healthy

cash position of A$45M, which provides some funds for early stage works

(pre-production underground works at M1 South) and ongoing exploration.

World-class project with massive appeal – Speculative Buy Sanbrado is a tier 1 asset, with an increasing high-grade mining inventory,

simple processing flowsheet (free-milling ores), strong production profile

(+200kozpa) and long mine life (+10 years). The project has significant

appeal, being 90%-owned, development ready (mining licence being

updated), and has attractive project metrics (low cost, high-margin operation).

Importantly, WAF boasts an impressive team to execute, with development

and operational experience in gold projects throughout West Africa, with

some key new appointments expected soon.

We maintain our Speculative Buy recommendation with a price target of

80cps, NAV of 72cps, spot NAV of 80cps. Our modelling has been updated

by the DFS, but also includes some upside for mine life growth to M1 South.

Hartleys Limited ABN 33 104 195 057 (AFSL 230052) 141 St Georges Terrace, Perth, Western Australia, 6000

Hartleys does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single

factor in making their investment decision. Further information concerning Hartleys’ regulatory disclosures can be found on Hartleys

website www.hartleys.com.au

0.00

0.10

0.20

0.30

0.40

0.50

0.60

.

5.

10.

15.

20.

25.

30.

35.

40.

45.

Jun-18Feb-18Nov-17Jul-17

Volume - RHS

WAF Shareprice - LHS

Sector (S&P/ASX SMALL RESOURCES) - LHS

A$ M

West African Res Ltd

Source: IRESS

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 2 of 10

SUMMARY MODEL

West African Res Ltd Share Price

WAF $0.350 Speculative Buy

Key Market Information Directors & Management Company InformationShare Price $0.350 Mark Connelly (Non-Exec Chairman) 14 Southbourne StMarket Capitalisation - ordinary A$242m Richard Hyde (Managing Director) Scarborough WA, 6007Net Debt (cash) -$45m Simon Storm (Non-Exec Director & Comp Sec) +61 8 9481 7344Market Capitalisation - fully diluted A$247m +61 8 9481 7355EV A$202m Lyndon Hopkins (COO)Issued Capital 690.8m Vincent Morel (Expl Manager) www.westafricanresources.com.auOptions 16.2m Joanne Thompson (Sustainability Manager)Issued Capital (fully diluted inc. all options) 707.1m Nick Harch (Project Finance)Issued Capital (fully diluted inc. all options and new capital) 834.2m Pierre Tapsoba (National Director)

Valuation $0.72 Top Shareholders (est) m shares %12month price target $0.80 1832 Asset Management 43.5 6.3%

Van ECK Associates Corporation 37.6 5.4%

P&L Unit 30 Jun 18 30 Jun 19 30 Jun 20 30 Jun 21 30 Jun 22 Board & Management 23.8 3.4%

Net Revenue A$m 0.0 0.0 94.3 372.9 354.9Total Costs A$m -11.9 -7.7 -6.2 -60.8 -72.5EBITDA A$m -11.9 -7.7 88.1 312.1 282.4 - margin - - 93% 84% 80% Reserves & Resources Mt g/t Au Koz LCDepreciation/Amort A$m -0.5 -4.9 -17.1 -29.3 -32.4 Reserves 22-Jun-18

EBIT A$m -12.3 -12.5 71.0 282.8 250.0 Open Pit 18.9 1.7 1021

Net Interest A$m -1.5 -1.5 -1.5 -1.5 -1.5 Underground 1.5 11.7 553

Norm. Pre-Tax Profit A$m -13.8 -14.0 69.5 281.3 248.5 20.4 2.4 1,574 Reported Tax Expense A$m 0.0 0.0 -7.1 -49.2 -43.5 Resources 22-Jun-18

Normalised NPAT A$m -11.4 -11.6 57.3 232.1 205.0 M1 South OP 0.9 6.6 180 0.5g/t AuAbnormal Items A$m -2.4 -2.5 5.0 0.0 0.0 M1 South UG 1.0 21.2 680 3.0g/t AuReported Profit A$m -13.8 -14.0 62.4 232.1 205.0 M5 50.0 1.2 1,960 0.5g/t AuMinority A$m 0 0 0 0 0 M1 North 1.3 2.0 80 0.5g/t AuProfit Attrib A$m -13.8 -14.0 62.4 232.1 205.0 M3 0.4 1.8 20 0.5g/t Au

Total 53.5 1.7 2,900

Balance Sheet Unit 30 Jun 18 30 Jun 19 30 Jun 20 30 Jun 21 30 Jun 22Cash A$m 44.6 190.5 57.2 240.9 417.0 Production Summary Unit Jun 19 Jun 20 Jun 21 Jun 22

Other Current Assets A$m 0.1 0.1 7.9 30.9 29.5 Mill Throughput Mt 0.0 0.5 1.8 1.9

Total Current Assets A$m 44.7 190.6 65.0 271.8 446.5 Strip Ratio x 21.1 8.8 8.6 7.6

Property, Plant & Equip. A$m 4.7 49.8 223.3 216.7 210.2 Milled grade g/t 0.00 4.7 4.6 4.3

Exploration A$m 16.0 24.0 32.0 40.0 48.0 Combined Recovery & Payability % 0% 93% 93% 93%

Investments/other A$m 0.0 0.0 0.0 0.0 0.0 Gold (koz) 0.0 63 251 240

Tot Non-Curr. Assets A$m 20.7 73.8 255.3 256.7 258.2 Gold attr. 90% (koz) 0.0 57 226 216

Total Assets A$m 65.4 264.5 320.3 528.5 704.8 Implied Resource Conversion % 18% 16% 13% 11%

Mine Life yr 11.0 11.0 10.00 9.00

Short Term Borrowings A$m - - - - -Other A$m 1.0 1.0 1.9 7.4 8.6 Costs Unit Jun 19 Jun 20 Jun 21 Jun 22Total Curr. Liabilities A$m 1.0 1.0 1.9 7.4 8.6 Cost per milled tonne $A/t - 39.0 41.8 49.9

Long Term Borrowings A$m 0.0 145.9 137.9 107.9 77.9 EBITDA / tonne milled ore $A/t - 195.7 171.0 150.6

Other A$m - - - - -

Total Non-Curr. Liabil. A$m 0.0 145.9 137.9 107.9 77.9 C1: Operating Cash Cost = (a) $A/oz - 252 273 350

Total Liabilities A$m 1.0 146.9 139.8 115.3 86.5 (a) + Royalty = (b) $A/oz - 327 348 424

Net Assets A$m 64.3 117.5 180.5 413.2 618.3 C2: (a) + depreciation & amortisation = (c) $A/oz - 524 390 485

Net Debt A$m -44.6 -44.7 80.7 -133.0 -339.2 (a) + actual cash for development = (d) $A/oz - 730 396 491 C3: (c) + Royalty $A/oz - 599 464 559

Cashflow Unit 30 Jun 18 30 Jun 19 30 Jun 20 30 Jun 21 30 Jun 22 (d) + Royalty $A/oz - 805 470 565

Operating Cashflow A$m -1.5 -7.6 81.2 294.5 285.1 All In Sustaining Cost (AISC) $A/oz - 733 629 639

Income Tax Paid A$m 0.0 0.0 -7.1 -49.2 -43.5 All In Sustaining Cost (AISC) $US/oz - 559 485 497

Interest & Other A$m -1.5 -1.5 -1.5 -1.5 -1.5

Operating Activities A$m -3.0 -9.1 72.6 243.8 240.1 Price Assumptions Unit Jun 19 Jun 20 Jun 21 Jun 22

AUDUSD A$/US$ 0.76 0.76 0.77 0.78

Property, Plant & Equip. A$m -5.0 -50.0 -190.5 -22.7 -25.9 Gold US$/oz 1325 1288 1275 1275

Exploration and Devel. A$m -16.0 -8.0 -8.0 -8.0 -8.0

Other A$m 0.0 0.0 0.0 0.0 0.0 Hedging Jun 19 Jun 20 Jun 21 Jun 22

Investment Activities A$m -21.0 -58.0 -198.5 -30.7 -33.9 Hedges maturing? No No No No

Borrowings A$m 0.0 145.9 -8.0 -30.0 -30.0 Sensitivity Analysis

Equity or "tbc capital" A$m 58.1 67.2 0.6 0.7 0.0 Valuation

Dividends Paid A$m 0.0 0.0 0.0 0.0 0.0 Base Case 0.72

Financing Activities A$m 58.1 213.1 -7.4 -29.3 -30.0 Spot Prices 0.80 (10.7%)

Spot USD/AUD 0.74, Gold $1271/oz.

Net Cashflow A$m 34.0 145.9 -133.4 183.7 176.2 AUDUSD +/--10% 0.62 / 0.84 (-13.6% / 16.5%) 56.4 / 69.7 (-9.6% / 11.8%)

Gold +/--10% 0.86 / 0.59 (18.4% / -18.6%) 69.8 / 55.0 (11.9% / -11.9%)

Shares Unit 30 Jun 18 30 Jun 19 30 Jun 20 30 Jun 21 30 Jun 22 Production +/--10% 0.86 / 0.58 (19.3% / -19.5%) 70.1 / 54.6 (12.5% / -12.5%)Ordinary Shares - End m 688.1 824.7 826.7 829.5 829.5 Operating Costs +/--10% 0.70 / 0.75 (-3.6% / 3.5%) 61.6 / 63.2 (-1.3% / 1.3%)Ordinary Shares - Weighted m 586.2 756.4 825.7 828.1 829.5Diluted Shares - Weighted m 586.2 751.7 815.2 815.2 815.2 Unpaid Capital - ITM

Year Expires No. (m) $m Avg price % ord

Ratio Analysis Unit 30 Jun 18 30 Jun 19 30 Jun 20 30 Jun 21 30 Jun 22 30-Jun-18 0.0 0.0 0.00 0.0%

Cashflow Per Share A$ cps -0.5 -1.2 8.8 29.4 28.9 30-Jun-19 9.5 1.0 0.11 1.4%

Cashflow Multiple x -68.4 -29.0 4.0 1.2 1.2 30-Jun-20 2.0 0.6 0.28 0.3%

Earnings Per Share A$ cps -2.4 -1.9 7.6 28.0 24.7 30-Jun-21 4.8 1.5 0.31 0.7%

Price to Earnings Ratio x -14.9 -18.9 4.6 1.2 1.4 TOTAL 16.2 3.0 0.19 2.3%

Dividends Per Share AUD - - - - -

Dividend Yield % 0.0% 0.0% 0.0% 0.0% 0.0%

Net Debt / Net Debt + Equity % -226% -61% 31% -47% -122% Share Price Valuation (NAV) Risked Est. A$m

Interest Cover X na na 47.7 189.9 167.9 90% Sanbrado (pre-tax NAV at disc. rate of 12%) 587

Return on Equity % na na 32% 56% 33% Exploration upside, other assets etc 70

Forwards 0Corporate Overheads -17Net Cash (Debt) 45Tax (NPV future liability) -84Options & Other Equity 1

Hedging 0

Total 603

Analyst: Mike Millikan

+61 8 9268 2805

"tbc capital" could be equity or debt. Our valuation is risk-adjusted for how this may be obtained.

Sources: IRESS, Company Information, Hartleys Research

0.00

0.72

63.8 (2.3%)

FY19 NPAT

62.4

0.08

0.00-0.020.05-0.100.00

Last Updated: 25/06/2018

Est. A$/share

0.70

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 3 of 10

SANBRADO GOLD PROJECT – BURKINA FASO The Sanbrado Gold Project (formerly Tanlouka Gold Project) is located ~90km

southeast of Ouagadougou, Burkina Faso. The project comprises one granted mining

permit and one granted exploration licence, covering an area of ~116km².

WAF has a 90% interest in the project, with the Government of Burkina Faso entitled

to a free-carried 10% interest. The project was acquired by WAF through an all scrip

transaction with TSX-V listed gold junior Channel Resources. At the time of the

acquisition the project contained the ~1Moz (0.5g/t LC) Mankarga 5 deposit.

Subsequently WAF has discovered the high-grade M1 South deposit and extended

mineralisation at M5, M1 North and M3 prospects.

Fig. 1: Sanbrado Project Location

Source: West African Resources Limited

Reserves are now estimated to be 20.4Mt @ 2.4g/t Au for 1.57Moz gold (up some

76% on the previous estimate). The latest Sanbrado resource estimate (total) is

53.5Mt grading 1.7g/t Au for 2.9Moz, with over 2.3Moz now Indicated.

Fig. 2: Sanbrado Project – Resource Statement June 2018

Source: West African Resources Limited; Hartleys Estimates

Deposit Type Cut-off Tonnes Grade (g/t) Oz Tonnes Grade (g/t) Oz Tonnes Grade (g/t) Oz

Open Pit (<120m) 0.5 800,000 6.6 170,000 50,000 4.8 10,000 850,000 6.6 180,000

Underground (>120m) 3.0 750,000 25.5 620,000 250,000 7.6 60,000 1,000,000 21.2 680,000

Total Combined 1,550,000 15.9 780,000 300,000 6.9 70,000 1,850,000 14.3 850,000

M5 Open Pit 0.5 37,150,000 1.3 1,510,000 12,800,000 1.1 450,000 49,950,000 1.2 1,960,000

M1 North Open Pit 0.5 750,000 2.0 50,000 500,000 2.0 30,000 1,250,000 2.0 80,000

M3 Open Pit 0.5 150,000 2.0 10,000 200,000 1.5 10,000 350,000 1.8 20,000

Total Combined 39,600,000 1.8 2,350,000 13,850,000 1.2 550,000 53,450,000 1.7 2,900,000

Indicated Inferred Total

M1 South

Sanbrado is located

~90km southeast of

Ouagadougou in

Burkina Faso

Burkina Faso remains

a mining fr iendly

jur isdict ion

The project comprises

one granted mining

permit ( to be updated

in Q3) and one

granted exploration

l icence, cover ing an

area of ~116km²

A reserve posi t ion in

excess of 1.5Moz has

been achieved

Reserves and

resources have been

upgraded

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 4 of 10

Sanbrado is proposed to be a conventional CIL operation, with free-milling ores and

anticipated low reagent consumption and a good portion of gravity recoverable gold.

Recent DFS work optimised the processing flowsheet, with the P80 90μm grind size

considered to be the most cost-effective option based on the economic parameters

applied for M5 and M1 South open pits and a grind size of P80 75μm was determined

to be appropriate for the higher grade M1 South fresh ores.

The average gold recoveries over the LOM is expected to be ~93%.

Fig. 3: Sanbrado Site Layout

Source: West African Resources Limited

Fig. 4: Sanbrado Processing Flowsheet

Source: West African Resources Limited

Sanbrado is proposed

to be a convent ional

CIL operation, with

free-mi l l ing ores and

anticipated low

reagent consumpt ion

and a good por t ion of

gravi ty recoverable

gold

Average gold

recoveries over the

LOM is expected to be

~93%

2Mtpa SABC CIL Plant

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 5 of 10

Fig. 5: Sanbrado – M5 Open Pit (bulk feed)

Source: West African Resources Limited

Fig. 6: Sanbrado – M1 South Underground (high-grade feed)

Source: West African Resources Limited

Sanbrado is a high

qual ity gold project

contain ing the key

deposits: M5 ( large

system, open at depth

and along str ike) and

M1 South (ul tra-high

grade deposit ,

growing at depth)

M5 ore from surface

with over 50% oxide,

remains open at depth

and provides potent ial

for a future

underground mine

(current ly being

scoped)

M1 South is expected

to provide 300-350kt

per annum from the

underground mine

Latest dr i l l ing has

conf irmed high-grade

mineralisat ion at M1

South extends to

vert ical depths of

+580m, system

remains open

Underground advance

is expected to be

~80m vert ical, which

impl ies another 2

years could added to

the mine l i fe once

addit ional resources

are added and

converted to reserves

WAF remains wel l

funded for exploration

dri l l ing to extend and

converted resources

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 6 of 10

VALUATION – UPDATED BY THE DFS Our modelling uses inputs from the Combined Open Pit and Underground DFS but

also includes some upside for the M1 South. We assume a project scale of 2.0Mtpa

(unchanged), with a slightly adjusted mine plan and updated cost estimates.

We have maintained our LOM gold recoveries at 93%, which could be considered

conservative given the high contribution from the M1 South underground, which is

expected to have recoveries over 95%. We now assume pre-production capex of

~US$185M (~A$250M), up from ~US$161M (~A$217M). Our modelling assumptions

are summarised below.

Fig. 7: Sanbrado Project Model Assumptions

Source: Hartleys Estimates* BC= Base Case

We now assume a blended LOM head grade of ~2.6/t Au, improved gold recoveries

and total mining inventory of ~1.59Moz, versus the current reserve of 1.6Moz (which

we expect with grow through resource extension and conversion). Our production

profile provides average LOM production of ~145kozpa over a mine-life of ~11 years.

We see significant potential for additional higher grade tonnes at M1 South as the

deposit remains open at depth. The exploration potential of the project are remains

strong and we continue to model a nominal A$70m ($0.08/share) value for exploration

upside.

Fig. 8: Hartleys Sum of Parts Valuation for WAF

Source: Hartleys Estimates

Sanbrado Open Pit FSSanbrado Combined OP/UG

DFSHartleys BC (old) Hartleys BC (new)

LOM Strip Ratio (x) 5.0x 4.6x 5.0x 4.7x

Reserve or Mining Inventory - Base 16.8Mt @ 1.7g/t Au for 0.89Moz 20.4Mt @ 2.4g/t Au for 1.6Moz 20Mt @ 2.6g/t Au for 1.6Moz 20.4Mt @ 2.4g/t Au for 1.6Moz

Resource - Base 21.1Mt @ 2.36g/t Au for 1.55Moz 53.5Mt @ 1.7g/t Au for 2.9Moz 24Mt @ 2.7g/t Au for 2.1Moz 53.5Mt @ 1.7g/t Au for 2.9Moz

Operation Scale (Mtpa) 2.0Mtpa 2.0Mtpa 2.0Mtpa 2.0Mtpa

LOM Head Grade g/t 1.7g/t 2.4g/t 2.6g/t 2.6g/t

LOM Recovered Grade g/t 1.4g/t 2.1g/t 2.4g/t 2.3g/t

LOM Gold recovery 90.7% 93% 93% 93%

Total Gold Produced 0.81Moz 1.46Moz 1.53Moz 1.59Moz

Total Gold Produced pa 93Kozpa 133Kozpa 153Kozpa 145Kozpa

Current Assumed Mine Life (yrs) 8.75yrs 11.0yrs 10.0yrs 11.0yrs

Commencement Date (qtr) Jun-19 Jun-20 Jun-20 Jun-20

LOM avg selling price (US$/gold oz) US$1200/oz US$1300/oz US$1242/oz US$1240/oz

LOM Cash Costs (US$/gold oz) US$717/oz US$577/oz US$515/oz US$545/oz

LOM AISC (US$/gold oz) US$759/oz US$640/oz US$613/oz US$633/oz

LOM Operating Margin (US$mpa) US$41mpa US$88mpa US$96mpa US$88mpa

Capex - Pre-production US$131m US$185m US$161m US$185m

Pre-tax NPV @ 5% US$143m US$567m US$554m US$592m

Share Price Valuation (NAV) Risked Est. A$m90% Sanbrado (pre-tax NAV at disc. rate of 12%) 587Exploration upside, other assets etc 70Forwards 0Corporate Overheads -17Net Cash (Debt) 45Tax (NPV future liability) -84Options & Other Equity 1

Hedging 0

Total 603

Est. A$/share0.700.080.00-0.020.05-0.100.00

0.00

0.72

We now assume

~US$185M capex

requirement in FY19

to build a 2.0Mtpa CIL

plant , open pit and

underground mine (M1

South)

We assume a nominal

A$70M value

(unchanged) for

explorat ion upside and

other gold assets

within the port fol io

Hart leys sum of par ts

valuation for WAF is

72cps (up from 67cps)

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 7 of 10

PRICE TARGET Our price target is based on our Base Case valuation at both Hartleys commodity price

and current spot prices, using our development discount rate of 12% and future

production discount rate of 8%. We have included a small weighting for the current net

cash backing.

Fig. 9: WAF Price Target Methodology

Source: Hartleys Estimates

WAF Price Target Methodology Weighting Spot 12 mth out

50% $0.72 $0.80

25% $0.80 $0.88

15% $0.85 $0.90

5% $0.95 $1.01

Net Cash 5% $0.07 $0.07

Risk weighted composite $0.74

12 Months Price Target $0.80

Shareprice - Last $0.350

12 mth total return (% to 12mth target ) 128%

Sanbrado NPV@ 12% - Base Case

Sanbrado NPV@ 12% - Base Case - Spot

Sanbrado NPV@ 8% - Upside Case

Sanbrado NPV@ 8% - Upside Case - Spot

Hart leys 12 month

price target is 80cps

(up from 77cps)

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 8 of 10

EV/EBITDA BANDS

Fig. 10: Using Hartleys base case commodity forecasts

Source: Hartleys Estimates, IRESS

Fig. 11: Using spot commodity prices

Source: Hartleys Estimates, IRESS

.00

.50

1.00

1.50

2.00

2.50

3.00

3.50

WAF Actual

Hartleys Target

8x EV/EBITDA

6x EV/EBITDA

4x EV/EBITDA

2x EV/EBITDA

1x EV/EBITDA

Shareprice

.00

.50

1.00

1.50

2.00

2.50

3.00

3.50

WAF Actual

8x EV/EBITDA

6x EV/EBITDA

4x EV/EBITDA

2x EV/EBITDA

1x EV/EBITDA

Shareprice

Hartleys Limited West African Resources (WAF) 25 June 2018

Page 9 of 10

RISKS

Fig. 12: Key assumptions and risks for valuation Assumption Risk of not realising

assumption Risk to valuation if

assumption is incorrect

Comment

Feasible project development

Moderate Meaningful WAF is leveraged to the success of the Sanbrado project. We model a 2.0Mtpa project for 11 years. If the project varies largely from these metrics our valuation will be at risk to

upside and downside Model parameters

Moderate

Meaningful

We have made a number of assumptions in our

valuation of WAF, changes in these assumptions can change our valuation to both the upside and

downside. Our model is largely based on the latest DFS inputs.

Exploration upside potential

Moderate

Meaningful

We assume exploration upside at Sanbrado.

Our valuation will be at risk if WAF has no further exploration success

Funding Risk

Moderate

High

We assume a ~60:40 debt:equity funding

scenario to develop the 2.0Mtpa CIL project, if this funding scenario is not achievable our

valuation will be at risk, equity dilution is the highest risk to our valuation

Conclusion At this early stage we have made significant assumptions but believe these are achievable.

Source: Hartleys Research

Page 10 of 10

HARTLEYS CORPORATE DIRECTORY Research Trent Barnett Head of Research +61 8 9268 3052

Mike Millikan Resources Analyst +61 8 9268 2805

John Macdonald Resources Analyst +61 8 9268 3020

Paul Howard Resources Analyst +61 8 9268 3045

Aiden Bradley Research Analyst +61 8 9268 2876

Oliver Stevens Research Analyst +61 8 9268 2879

Michael Scantlebury Junior Analyst +61 8 9268 2837

Janine Bell Research Assistant +61 8 9268 2831

Corporate Finance Dale Bryan Director & Head of

Corp Fin.

+61 8 9268 2829

Richard Simpson Director +61 8 9268 2824

Ben Crossing Director +61 8 9268 3047

Ben Wale Director +61 8 9268 3055

Stephen Kite Director +61 8 9268 3050

Scott Weir Director +61 8 9268 2821

Scott Stephens Associate Director +61 8 9268 2819

Rhys Simpson Associate Director +61 8 9268 2851

Registered Office

Level 6, 141 St Georges Tce Postal Address:

Perth WA 6000 GPO Box 2777

Australia Perth WA 6001

PH:+61 8 9268 2888 FX: +61 8 9268 2800

www.hartleys.com.au [email protected]

Note: personal email addresses of company employees are structured

in the following manner: [email protected]

Hartleys Recommendation Categories

Buy Share price appreciation anticipated.

Accumulate Share price appreciation anticipated but the risk/reward is

not as attractive as a “Buy”. Alternatively, for the share

price to rise it may be contingent on the outcome of an

uncertain or distant event. Analyst will often indicate a

price level at which it may become a “Buy”.

Neutral Take no action. Upside & downside risk/reward is evenly

balanced.

Reduce /

Take profits

It is anticipated to be unlikely that there will be gains over

the investment time horizon but there is a possibility of

some price weakness over that period.

Sell Significant price depreciation anticipated.

No Rating No recommendation.

Speculative

Buy

Share price could be volatile. While it is anticipated that,

on a risk/reward basis, an investment is attractive, there

is at least one identifiable risk that has a meaningful

possibility of occurring, which, if it did occur, could lead to

significant share price reduction. Consequently, the

investment is considered high risk.

Institutional Sales Carrick Ryan +61 8 9268 2864

Justin Stewart +61 8 9268 3062

Simon van den Berg +61 8 9268 2867

Digby Gilmour +61 8 9268 2814

Jayme Walsh +61 8 9268 2828

Veronika Tkacova +61 8 9268 3053

Wealth Management Nicola Bond +61 8 9268 2840

Bradley Booth +61 8 9268 2873

Adrian Brant +61 8 9268 3065

Nathan Bray +61 8 9268 2874

Sven Burrell +61 8 9268 2847

Simon Casey +61 8 9268 2875

Tony Chien +61 8 9268 2850

Tim Cottee +61 8 9268 3064

David Cross +61 8 9268 2860

Nicholas Draper +61 8 9268 2883

John Featherby +61 8 9268 2811

Ben Fleay +61 8 9268 2844

James Gatti +61 8 9268 3025

John Goodlad +61 8 9268 2890

Andrew Gribble +61 8 9268 2842

David Hainsworth +61 8 9268 3040

Murray Jacob +61 8 9268 2892

Gavin Lehmann +61 8 9268 2895

Shane Lehmann +61 8 9268 2897

Steven Loxley +61 8 9268 2857

Andrew Macnaughtan +61 8 9268 2898

Scott Metcalf +61 8 9268 2807

David Michael +61 8 9268 2835

Jamie Moullin +61 8 9268 2856

Chris Munro +61 8 9268 2858

Michael Munro +61 8 9268 2820

Ian Parker +61 8 9268 2810

Matthew Parker +61 8 9268 2826

Charlie Ransom

(CEO)

+61 8 9268 2868

Mark Sandford +61 8 9268 3066

David Smyth +61 8 9268 2839

Greg Soudure +61 8 9268 2834

Sonya Soudure +61 8 9268 2865

Dirk Vanderstruyf +61 8 9268 2855

Samuel Williams +61 8 9268 3041

Disclaimer/Disclosure

The author of this publication, Hartleys Limited ABN 33 104 195 057 (“Hartleys”), its Directors and their Associates from time to time may hold

shares in the security/securities mentioned in this Research document and therefore may benefit from any increase in the price of those securities.

Hartleys and its Advisers may earn brokerage, fees, commissions, other benefits or advantages as a result of a transaction arising from any advice

mentioned in publications to clients.

Hartleys has assisted in the completion of part of a capital raising in the past 12 months for West African Resources Ltd ("WAF") for which it has

earned fees. Hartleys has provided corporate advice within the past 12 months to WAF for which it has earned fees. Hartleys has a beneficial

interest in 5 million unlisted options in West African Resources Limited.

Any financial product advice contained in this document is unsolicited general information only. Do not act on this advice without first consulting

your investment adviser to determine whether the advice is appropriate for your investment objectives, financial situation and particular needs.

Hartleys believes that any information or advice (including any financial product advice) contained in this document is accurate when issued.

Hartleys however, does not warrant its accuracy or reliability. Hartleys, its officers, agents and employees exclude all liability whatsoever, in

negligence or otherwise, for any loss or damage relating to this document to the full extent permitted by law.