Embed Size (px)

Citation preview

Page 1 of 62

» Real Estate «

Init

ial

co

vera

ge

«

In

ADO Properties S.A. (Adler Real Estate Group)

WKN: A14U78 | ISIN: LU1250154413 | Bloomberg: ADJ GY

Eagles (Adler) are going to fly

We initiate coverage of ADO Properties S.A. (ADLER Real Estate Group) with a BUY

recommendation and a target price of EUR 35.00 (=~50% upside). Our TP is based

on our EPRA NAV valuation (EUR 35.54) for ADO on a stand-alone basis.

New real estate group is created: The integration of ADLER and renaming to ADLER

Real Estate Group creates one of the largest German real estate companies with a

current gross asset value (GAV) of EUR 8.5bn. For comparison: ADO Standalone had

a GAV of EUR 3.6bn at the end of 2019, while ADLER will integrate a value of EUR

4.9bn. Together, the two companies currently own 75,721 units, with 58,000 units

coming from ADLER. ADO previously operated exclusively in the Berlin region. The

acquisition of ADLER reduces this regional concentration to 25% of the total

portfolio. Overall, ADO/ADLER will become a serious German player in the

residential real estate sector.

Option to consolidate Consus offers opportunity for sustainable growth:

Currently, the new ADLER holds about 25% of Consus - with an option for additional

51% until the end of June 2021. With this step, the new ADLER would also include

the fast-growing project developer Consus into the group, which speaks for a clear

fundamental strength and promising strategic orientation. Since ADO and Consus

have already agreed on a strategic cooperation agreement in which both parties

agree to work together on current and future projects, and ADO also has a right to

follow up on offers, ADO can already benefit from Consus' market strength (at-

equity result) without having rating problems or even having to pay higher interest

rates. Investors have always seen Consus as "the weakest link", but ADO/ADLER

have taken a strategically valuable path with the cooperation plus option, without

having to make direct changes in LTV or net debt.

Impact of COVID-19: As a residential player, ADO assumes only a minor impact

from COVID-19. Which will have an impact, however, is the rent cap in Berlin.

Published: 22.04.2020

BUY Before: -

Price target EUR 35.00 (-)

Share price* EUR 23.88 (47%)

*last XETRA closing price

Initial 2020e 2021e 2022e

Rental income 131.7 138.0 143.6

EBIT 162.0 165.1 168.6

NAV per share 63.24 65.20 67.21

Key share data

Number of shares (million) 44.2:

Free Float (in %) 80%

Market Cap (in EURm) 1055:

Trading volume (Ø) 290k

High (EUR, 52 weeks) 49.84

Low (EUR, 52 weeks) 13.00

Shareholder structure

ADO Group 20,4%

Free Float 79,6%

Corporate calendar

Q1 2020 report 20.05.2020

Analysts

Mariya Lazarova

Analyst

+49 (0) 69 – 920 389 10

Robel Tesfeom

Analyst

+49 (0) 69 – 920 389 10

xxx

xx

+49 (0) 69 - 920 389 12

Contakt

FMR Frankfurt Main Research AG

Schillerstrasse 16

60313 Frankfurt am Main

Germany

+49 (0) 69 - 920 389 10

www.fmr-research.de

Source: Factset

May-19 Jul-19 Sep-19 Nov-19 Jan-20 Mar-20

10

15

20

25

30

35

40

45

50

55

ADO Properties S.A. Germany SDAX Germany CDAX

FY end: 31.12.; in EURm CAGR (19-22e) 2017 2018 2019 2020e 2021e 2022e

Net rental income -5.4% 103.3 128.0 134.1 105.6 109.5 113.6

EBITDA -3.1% 81.0 96.3 93.8 78.8 82.1 85.2

EBIT -35.0% 463.6 499.3 613.9 162.0 165.1 168.6

Net income before minorities -42.0% 356.0 386.9 601.9 112.2 114.7 117.4

EPS (EUR) -46.3% 8.07 8.77 13.63 2.02 2.07 2.11

FFO 1 -7.5% 54.3 66.8 63.2 46.9 48.5 50.0

FFO 1 per share (EUR) 1.23 1.51 1.43 0.84 0.87 0.90

EPRA NAV 8.7% 1,988.8 2,429.5 2,905.7 3,510.5 3,619.7 3,731.0

EPRA NAV per share (EUR) 45.10 55.05 65.79 63.24 65.20 67.21

DPS (EUR) 0.60 0.75 0.75 0.42 0.44 0.45

Market cap/sqm (EUR) 1,749.1 1,526.2 927.1 1,178.0 1,259.1 1,199.1

EV/sqm (EUR) 3,331.4 2,808.6 2,038.0 3,107.5 2,979.7 2,842.9

FFO 1 Yield (%) 2.91% 3.33% 4.46% 3.53% 3.26% 3.36%

Source: ADO, FMR

ADO Properties S.A. (Adler Real Estate Group)

Page 2 of 62

Inhalt Investment Thesis .............................................................................................................................................. 4

SWOT ................................................................................................................................................................. 7

The ADO/ADLER/Consus takeover process ....................................................................................................... 9

Current Group structure .............................................................................................................................. 12

Valuation .......................................................................................................................................................... 13

Summary ...................................................................................................................................................... 13

ADO: stand-alone valuation ......................................................................................................................... 14

ADLER: stand-alone valuation...................................................................................................................... 15

Consus: stand-alone valuation ..................................................................................................................... 16

Peer group valuation ................................................................................................................................... 17

ADO + ADLER: combined valuation ............................................................................................................. 18

ADO’s company profile .................................................................................................................................... 20

Group structure ........................................................................................................................................... 20

Management/supervisory board ................................................................................................................. 21

Shareholder structure .................................................................................................................................. 22

ADLER’s company profile ................................................................................................................................. 23

Company history .......................................................................................................................................... 23

Group structure ........................................................................................................................................... 24

Management ............................................................................................................................................... 24

Shareholder structure .................................................................................................................................. 25

Consus’s company profile ................................................................................................................................ 25

Group structure ........................................................................................................................................... 26

Management ............................................................................................................................................... 26

Shareholder structure .................................................................................................................................. 27

ADO’s business model ..................................................................................................................................... 28

ADLER’s business model .............................................................................................................................. 29

The residential portfolio .............................................................................................................................. 29

Acquisition strategy ..................................................................................................................................... 29

Financing strategy ........................................................................................................................................ 30

Key management metrics ............................................................................................................................ 30

Employees .................................................................................................................................................... 30

Research and development ......................................................................................................................... 30

Consus’s business model ................................................................................................................................. 31

ADO Properties S.A. (Adler Real Estate Group)

Page 3 of 62

Real estate project development for institutional buyers........................................................................... 31

Real estate development for private buyers ............................................................................................... 32

Development of income properties............................................................................................................. 32

Cost advantages from digitalisation and prefabrication ............................................................................. 32

Portfolio ....................................................................................................................................................... 33

Market environment ........................................................................................................................................ 36

Supply of residential real estate .................................................................................................................. 36

Demand for residential properties .............................................................................................................. 37

The residential market ................................................................................................................................. 38

North Rhine-Westphalia & Lower Saxony ................................................................................................... 40

The Big 8 ...................................................................................................................................................... 42

Forecast ....................................................................................................................................................... 45

Financials ......................................................................................................................................................... 47

ADO FY 2019 ................................................................................................................................................ 47

Adler FY 2019 ............................................................................................................................................... 48

Guidance for 2020 ....................................................................................................................................... 48

Balance sheet structure ............................................................................................................................... 51

Appendix .......................................................................................................................................................... 53

ADO Properties S.A. (Adler Real Estate Group)

Page 4 of 62

Investment Thesis ADO Properties is a listed residential real estate company active solely in the Berlin

market. The lion’s share of its portfolio consists of centrally located properties or

properties located in interesting areas on the city’s outskirts.

The ADO Properties Group, with the help of its subsidiaries, covers the entire

property asset management value chain, from screening to acquisitions to the

administration of suitable properties. ADO Properties’ strategic focus is to increase

the value of the real estate portfolios. By investing in the modernisation of its

portfolios it can achieve higher rents and lower vacancies. ADO Properties has

roughly 18,000 units. Another business is the privatisation business, which was

launched in 2014.

After ADLER took over ADO Group (a listed holding in Israel), ADO Properties’ major

shareholder, ADO Properties then announced on 15 December 2019 a voluntary

public takeover bid for ADLER. According to its announcement dated 30 March,

ADO now owns 91.93% of ADLER. The deal was settled and the shares were

delivered on 09 April.

The integration of ADLER and rebranding as ADLER Real Estate Group will result in

one of the largest German real estate companies, with a gross asset value (GAV) of

currently EUR 8.5bn. For the sake of comparison, ADO’s stand-alone GAV stood at

EUR 3.6bn at the end of 2019, while ADLER will contribute GAV of EUR 4.9bn.

Together, the two companies currently own 75,721 units, with ADLER accounting

for 58k.

In order to simplify the group structure somewhat, ADO submitted a public bid a

few days ago for the remaining 3% of WESTGRUND (market value of roughly EUR

25m). The majority of WESTGRUND’s shares were bought by ADLER in 2015. We

consider this a step towards a more simplified company structure for ADLER Real

Estate Group.

ADO expects to achieve net rental (NRI) income post ADLER merger of around

EUR 280-300m in 2020. On an annualised basis management sees NRI of EUR 340-

360m. In 2019 ADLER generated NRI of EUR 248.7m, while ADO achieved

EUR 134.1m. On a combined basis, their NRI in 2019 stood at EUR 382.8m. As ADO

sold the Carlos portfolio (5,900 units) at the end of 2019 for EUR 920m,

management estimates its 2020 net rental income (stand-alone) at just under

EUR 106m. We estimate ADO’s NRI in 2020e at EUR 105.6m, and ADLER’s at

EUR 256.7m.

Assuming ADLER is consolidated for just under 8 months in 2020, its contribution

to consolidated NRI in 2020e would be ~EUR 180m. Adding to this ADO’s EUR

105.6m, we currently estimate NRI for 2020e at EUR 286m, which puts us within

management’s range. On an annualised basis we estimate NRI of EUR 360m.

For combined FFO 1 (ADO+ADLER), management expects a range of EUR 105-125m

for 2020. In 2019 ADO and ADLER achieved FFO 1 of EUR 63m and ~EUR 84m

respectively or EUR 147m combined. For 2020e, the company targets annualised

ADO Properties is a listed

residential real estate

company

ADO Properties covers the

entire property asset

management value chain

ADO Properties’ takeover bid

for ADLER

Renaming to ADLER Real

Estate Group with GAV of EUR

8.5bn

Public bid by ADO Properties

for the remaining 3% of

WESTGRUND

ADLER Real Estate Group

expects net rental income of

EUR 280-300m in 2020e

Assuming ADLER is

consolidated for just under

8 months in 2020

Estimations in line with

management expectations

ADO Properties S.A. (Adler Real Estate Group)

Page 5 of 62

FFO 1 of EUR 120-140m. We estimate 2020e FFO 1 of EUR 46.9m for ADO and

EUR 96.6m for ADLER. On an annualised basis we estimate combined FFO 1 of EUR

143m in 2020e but assume FFO 1 of EUR 111.3m (ADLER will be consolidated for 8

months in 2020e) in our valuation model. Thus, our estimates are in line with

management’s NRI and FFO 1 targets both for ADO and ADLER individually and on

a combined basis.

With regard to EPRA NAV, for 2019 ADLER Real Estate Group reported combined

EPRA NAV of EUR 4.9bn (2018: EUR 4.1bn), with ADO contributing EUR 2.9bn and

ADLER EUR 2.0bn.

Our current estimate for combined 2020e EPRA NAV – i.e. EUR 4.9bn – matches the

2019 numbers. For 2021e we estimate EPRA NAV to increase to EUR 5.3bn and for

2022e to EUR 5.7bn. On a per-share basis we expect EPRA NAV to exceed the

EUR 100 mark for the first time in 2022e (FMRe: EUR 103.35).

As per 31.12.2019 ADO Properties has a stable financial structure and a strong

liquidity position of EUR 500m in directly accessible cash (ADO cash stand-alone:

EUR 387m; ADLER stand-alone: EUR 237m). The company has no major refinancing

scheduled until the end of 2021 – a 2017 ADLER bond of EUR 500m is due in

December 2021.

ADO Properties’ LTV stands at 27% (end of 2019) and its average interest rate is

1.6%. The average term to maturity of its debt obligations is ~4.2 years. Virtually all

of its debt is either fixed interest or interest-rate hedged. ADO Properties intends

to continue this sustainable financing strategy and targets an LTV of no more than

50%. For ADO stand-alone we expect its LTV below 25% for the next few years.

Although ADO’s and ADLER’s fundamental data look strong, both stand-alone and

combined, the shares’ performance over the past few weeks has been clearly

negative. Many investors are afraid of having difficulties with the tenants due to

the Covid-19 crisis. Nonetheless, so far we have not noticed any significant effects

on the residential rental market. Residential property companies have stated that

currently they are not experiencing payment issues or have problems with only a

limited number of tenants. Furthermore, the rent prices remain stable despite the

pandemic and as per end of March there were no fluctuations in prices that were

caused by the current health situation. ADLER appears to be more protected

against the pandemic as a large portion of its portfolio is rented to people with low

to medium income, which have either already received government support or are

going to be protected in this phase. Although the risk for commercial real estate is

larger, the new ADLER Group has only a limited risk exposure.

Obviously, COVID-19 has rattled the entire equity market, but all three individual

shares (ADO, ADLER, Consus) have fallen more strongly – in some cases far more

strongly – than their peers. It seems the market has either reacted completely

negatively to the merger, or the timing of the deal proved to be bad due to the

Corona crisis, thus leading to the shares’ strong negative reactions.

ADLER Real Estate Group

reported EPRA NAV of EUR

4.9bn

…2020e EUR 4.9bn

2021e: EUR 5.3bn

2022e: EUR 5.7bn

ADO has a stable financial

structure and a strong

liquidity position

2019 LTV stands at 27% and its

average interest rate is 1.6%

Negative share performance

over the past few weeks

ADO Properties S.A. (Adler Real Estate Group)

Page 6 of 62

Stock impact amid the corona crisis

Source: Factset, FMR

All three shares are currently trading at discounts to EPRA NAV of >60% whereas

most peers are trading at discounts of around 30%. We see no reason why the

ADLER Real Estate Group should trade at a deeper discount than the peers. We see

a structural deficit only in the Company's lack of institutional investors to date, but

this also offers a considerable opportunity for the new ADLER to attract larger

investors as partners.

Several points clearly indicate fundamental strength and a promising strategic

outlook: a GAV of EUR 8.5bn, a free float of 80% after the transaction is closed, and

an option to bring Consus – Germany’s most successful project developer – on

board in the next few months (option expires in mid-2021). Admittedly, the

integration of Consus would increase LTV somewhat (1.9% for ADO + ADLER), but

on the other hand ADO and ADLER would gain an advantage in terms of new

projects. We see this trade-off as positive for the business model, and this is also

reflected in our valuation.

On a stand-alone basis we value ADO at EUR 35.00, ADLER at EUR 17.50 and Consus

at EUR 10.50 per share. Each of these valuations suggest significant undervaluation.

While it may take a while for normalcy and calm to return to the equity market, all

three shares still look very interesting in the long term. An important assumption

here is that the current health crisis does not lead to a deep economic crisis.

Combining ADO and ADLER, we derive a fair value per share (FVpS) of EUR 46.58,

which in Corona times should probably be viewed as a best-case scenario (current

upside: almost 100%). Nonetheless, we believe that going forward, especially in H2

2020e and in 2021e as well, the merged entity will achieve significant synergies that

should further increase the attractiveness of the share. One should not forget that

prior to the announcement of the deal and prior to COVID-19, the ADO share was

already trading above EUR 30.

We initiate coverage with a BUY recommendation and a target price of EUR 35.00

(based solely on our stand-alone valuation of ADO Properties), which nonetheless

suggests upside of currently around 50%.

CompanyStock at start of Corona-

crisisLowest price Current stock price

21.02.2020 21.04.2020

ADO Properties 31.38 13.00 -58.6% 23.88

ADLER Real Estate 13.00 5.57 -57.2% 12.50

Consus 7.08 3.74 -47.2% 5.00

Vonovia SE 53.66 36.71 -31.6% 44.45

Deutsche Wohnen SE 38.91 27.66 -28.9% 35.11

Grand City Properties SA 23.94 13.82 -42.3% 18.58

LEG Immobilien AG 117.80 75.12 -36.2% 103.24

TAG Immobilien AG 25.04 14.16 -43.5% 18.52

Aroundtown SA 8.78 2.88 -67.1% 4.73

CORESTATE Capital Holding SA 42.05 21.20 -49.6% 26.16

PATRIZIA AG 23.34 16.08 -31.1% 19.60

Stock decline

amid corona-crisis

All three shares are currently

trading at discounts to EPRA

NAV of >60%

GAV of EUR 8.5bn, a free float

of 80% and Consus-option→

promising strategic outlook

ADO at EUR 35.00, ADLER at

EUR 17.50 and Consus at EUR

10.50

Fair value for ADO and ADLER

combined: EUR 46.58 (Best-

Case Scenario)

We initiate coverage with a

BUY recommendation and a

target price of EUR 35.00

ADO Properties S.A. (Adler Real Estate Group)

Page 7 of 62

SWOT

Strengths

• Strong and experienced management team: Co-CEOs from ADO and ADLER

• Improved corporate governance; 5 out of 7 board members are fully

independent

• Higher liquidity in the stock (around 80% free-float post-merger) and

potential MDAX-candidate according to the criteria set by the German

stock exchange (Deutsche Börse)

• Combination of FFO 1 from ADO and ADLER increases the value for ADO’s

shareholders

• One of the largest European residential real estate companies

• Owning properties across Germany decreases the regional risks (ADO

focuses on Berlin’s real estate market)

• ADO has a strong liquidity position of EUR 500m with directly accessible

cash as a result of the Carlos portfolio sale in 2019

• No large refinancing until end of 2021 (maturing bond of EUR 500m)

• ADLER has a strong and traceable M&A track-record since 2011; ADLER

made the first steps on the merger with ADO by acquiring ADO Group

Weaknesses

• Around 25% of the portfolio is exposed to the regulated market of Berlin

• Increased interest rates for ADO after the takeover of ADLER (from 1.6% to

1.9% in 2019), which is likely to further increase once Consus is acquired

• Lacking institutional investors in the scale of larger investment companies

ADO Properties S.A. (Adler Real Estate Group)

Page 8 of 62

Opportunities

• Starting a more simplified company structure through the takeover bid to

Westgrund

• Further simplification of the company structure by overall takeover of the

old ADLER Real Estate

• 25% stake in Consus with an option to acquire 51% in order to transition

into a “build-to-hold” strategy

• Project development strategies with the help of Consus to tackle the

housing shortage in the Top 7 cities

• The merger between ADO/ADLER/Consus has the potential to lead to

significant synergy effects and market advantages given that an efficient

strategic objective is pursued

Treats

• Increased risk due to the takeover bid to Consus could lead to higher

interest rates

• Effects of Covid-19 pandemic on the overall economic stability; at first

effects on rental income from the commercial real estate could be noticed,

followed by residential real estate in the mid-term as well as on the

purchasing of properties and on project developers.

ADO Properties S.A. (Adler Real Estate Group)

Page 9 of 62

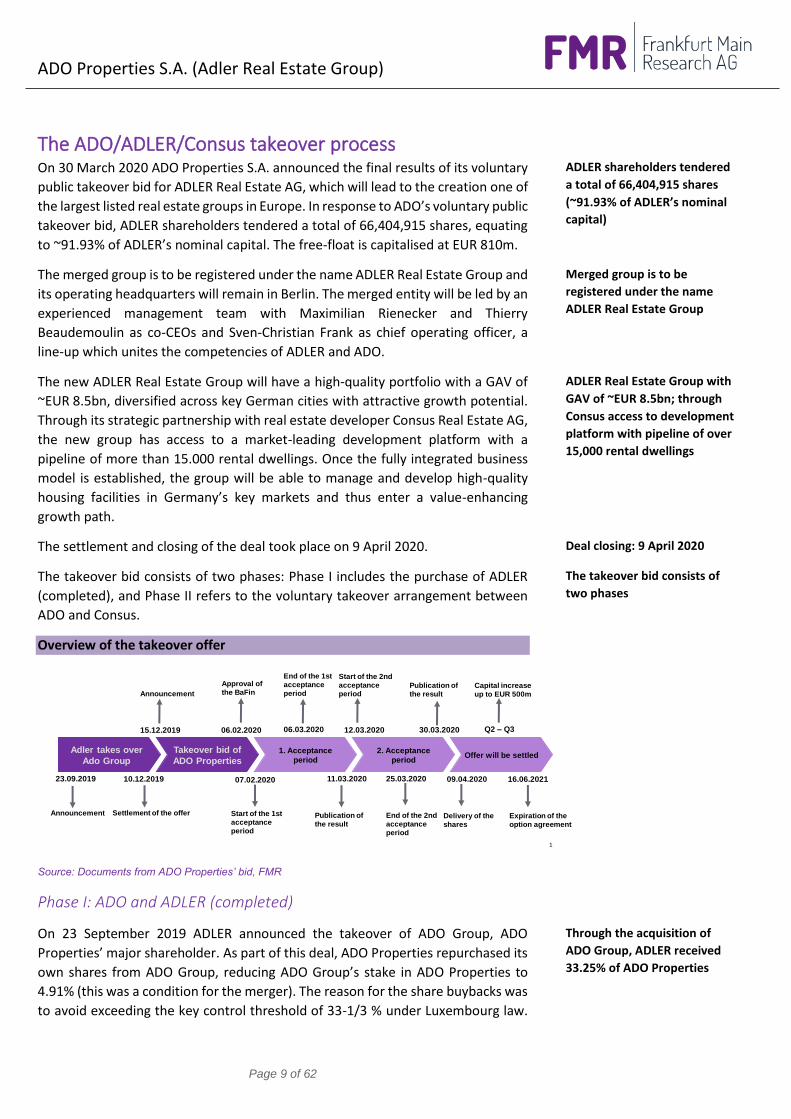

The ADO/ADLER/Consus takeover process On 30 March 2020 ADO Properties S.A. announced the final results of its voluntary

public takeover bid for ADLER Real Estate AG, which will lead to the creation one of

the largest listed real estate groups in Europe. In response to ADO’s voluntary public

takeover bid, ADLER shareholders tendered a total of 66,404,915 shares, equating

to ~91.93% of ADLER’s nominal capital. The free-float is capitalised at EUR 810m.

The merged group is to be registered under the name ADLER Real Estate Group and

its operating headquarters will remain in Berlin. The merged entity will be led by an

experienced management team with Maximilian Rienecker and Thierry

Beaudemoulin as co-CEOs and Sven-Christian Frank as chief operating officer, a

line-up which unites the competencies of ADLER and ADO.

The new ADLER Real Estate Group will have a high-quality portfolio with a GAV of

~EUR 8.5bn, diversified across key German cities with attractive growth potential.

Through its strategic partnership with real estate developer Consus Real Estate AG,

the new group has access to a market-leading development platform with a

pipeline of more than 15.000 rental dwellings. Once the fully integrated business

model is established, the group will be able to manage and develop high-quality

housing facilities in Germany’s key markets and thus enter a value-enhancing

growth path.

The settlement and closing of the deal took place on 9 April 2020.

The takeover bid consists of two phases: Phase I includes the purchase of ADLER

(completed), and Phase II refers to the voluntary takeover arrangement between

ADO and Consus.

Overview of the takeover offer

1

Adler takes over

Ado Group

Takeover bid of

ADO Properties

1. Acceptance

period

2. Acceptance

periodOffer will be settled

Announcement

15.12.2019 06.02.2020

09.04.202023.09.2019

Settlement of the offer

11.03.202010.12.2019

Announcement

Approval of

the BaFin

07.02.2020

Start of the 1st

acceptance

period

Publication of

the result

06.03.2020

End of the 1st

acceptance

period

12.03.2020

Start of the 2nd

acceptance

period

Q2 – Q3

Publication of

the result

25.03.2020

End of the 2nd

acceptance

period

Expiration of the

option agreement

16.06.2021

Delivery of the

shares

30.03.2020

Capital increase

up to EUR 500m

Source: Documents from ADO Properties’ bid, FMR

Phase I: ADO and ADLER (completed)

On 23 September 2019 ADLER announced the takeover of ADO Group, ADO

Properties’ major shareholder. As part of this deal, ADO Properties repurchased its

own shares from ADO Group, reducing ADO Group’s stake in ADO Properties to

4.91% (this was a condition for the merger). The reason for the share buybacks was

to avoid exceeding the key control threshold of 33-1/3 % under Luxembourg law.

ADLER shareholders tendered

a total of 66,404,915 shares

(~91.93% of ADLER’s nominal

capital)

Merged group is to be

registered under the name

ADLER Real Estate Group

ADLER Real Estate Group with

GAV of ~EUR 8.5bn; through

Consus access to development

platform with pipeline of over

15,000 rental dwellings

Deal closing: 9 April 2020

The takeover bid consists of

two phases

Through the acquisition of

ADO Group, ADLER received

33.25% of ADO Properties

ADO Properties S.A. (Adler Real Estate Group)

Page 10 of 62

On 10 December 2019 this deal was completed, and as a result ADLER held 33.25%

of the voting rights in ADO Properties. ADLER financed the takeover with new

shares, internally available funding, and debt.

On 15 December 2019 it was announced that ADO Properties had made a voluntary

takeover bid for ADLER at EUR 11.10 per ADLER share. This price corresponds to the

3-month average share price prior to the announcement of the takeover. Under a

business combination agreement, a share ratio was set at 0.4164 ADO shares = 1

ADLER share. The share ratio was agreed on the basis of each company’s diluted

EPRA NAV per share (as per end of September 2019). The NAV p/s calculation

assumes the conversion of ADLER’s outstanding convertible bonds. The business

combination agreement is valid for two years from its signing and can be

terminated by either party if one of the parties fails to adhere to its terms or the

deal is not consummated by the end of June 2020.

The takeover was secured by irrevocable acceptance commitments representing a

total of 52.2% of the shares. These include the shares of ADLER Co-CEO Tomas de

Vargas Machuca. On 14 February ADO announced that these shareholders have

already submitted declarations that they have accepted the deal to their custodian

banks. The shares held by ADO Group will be deemed non-voting treasury stock

(own shares) once the takeover is successfully completed. On 6 January Germany’s

federal financial supervisory authority BaFin examined the offer documentation

and permitted its publication.

On 6 March 2020 the first acceptance period ended. The results were published on

11 March. One day later the second acceptance period began, which ended on 25

March. On 9 April 2020 the offer was settled and the shares (91.93% of total) were

delivered. The combined entity will bear the name ADLER Real Estate Group

The new company owns 75.721 rental units in its portfolio. Since the shares of the

new company will have more trading volume (market cap of ~EUR 1.8bn), it will be

a candidate for inclusion in the MDAX index. Considering the criteria of market

value (ADO standalone: rank 119) and turnover (ADO standalone: rank 109), ADO

is likely to be included in the index soon from technical perspective.

The free float should be around 80%. 33% of the ADLER shares in ADO will become

treasury stock post takeover, so these shares are not included in shareholder

structure calculation. Existing and new shareholders in ADO will be entitled to

dividends for 2019. Since ADLER stand-alone has not distributed any dividends so

far, dividend payments are unlikely to be made in the short or medium term.

Once the takeover is done, a capital increase of EUR 500m is planned in order to

further strengthen the balance sheet structure. This capital increase has already

been discussed with banks and the new shares’ issue is expected in Q2 or Q3 2020.

The exact date depends on the market situation.

ADO can secure the share-financed part of the offer through capital increases from

authorised capital (EUR 750m). On 06 Feb 2020 ADO Properties had cash totalling

EUR 500m, which it can use to cover the offer costs (EUR 20m).

ADO Properties had made a

voluntary takeover bid for

ADLER at EUR 11.10 per

ADLER share

The takeover was secured by

irrevocable acceptance

commitments

On 6 March 2020 the first and

on 25 March 2020 the second

acceptance period ended

Market cap of ~EUR 1.8bn →

ADLER Real Estate Group will

be a candidate for inclusion in

the MDAX index

Capital increase of EUR 500m

is planned

ADO Properties S.A. (Adler Real Estate Group)

Page 11 of 62

To refinance ADLER’s financial obligations in the case of a change of control, a

bridge financing facility was agreed with J. P. Morgan with a face value of up to

EUR 2.963bn. This facility can also be used for bonds issued via the ADO Group.

On 25 March 2020 ADO had announced a voluntary, public takeover bid to

Westgrund shareholders. ADLER had acquired the majority of Westgrund in 2015.

By taking over ADLER, ADO acquired an indirect stake of 96.9% in Westgrund. ADO

will finance the acquisition with cash and the full acquisition of Westgrund will

serve to simplify the structure of the new group. The current market capitalisation

of Westgrund is over EUR 825m and hence, a takeover of 3% of the stocks will cost

roughly EUR 25m. We consider the offered purchase price of EUR 11.71 per

Westgrund share to be fair and see only minor risks that are financially negligible

for the new group as part of the upcoming review of the takeover offer.

Phase II: ADO and Consus

On 15 December 2019 ADO Properties acquired 22.18% of Consus’s shares for an

average price of EUR 9.72, paying a total of EUR 294m. This purchase was paid in

cash which basically came from the sale of the Carlos portfolio. ADO closed the sale

of the Carlos portfolio (rental residential properties) on 29 November 2019. The

price for the transaction was EUR 920m (less net debt of the sold companies

totalling EUR 340m). Hence, the proceeds after the sale of Carlos portfolio and the

purchase of Consus should amount to EUR 580m.

Together with the shares that ADLER Real Estate already has, this amounts to a

stake of ~25% in Consus. Additionally, ADO and Consus have signed a strategic

cooperation agreement under which the two parties agree to collaborate on

current and future projects. In the case of projects where both parties have already

collaborated, ADO has the right to match the bid of a third party in order to be able

to acquire capital assets that pertain to the project. In addition, ADO and Consus’

main shareholder Aggregate Holdings Luxemburg have entered the following

option agreements:

Call option for ADO: If ADO exercises this option, it will acquire a 50.97%

stake in Consus at a share ratio of 0.2390 ADO share = 1 Consus share.

Aggregate Holdings currently holds 50.97% of Consus. The exercise of this

option will also trigger a voluntary bid by ADO to the minority shareholders

at the same share ratio of 0.2390 (obligatory).

Put option for Aggregate Holdings: This option agreement is contingent on

a change of control at ADO. By exercising this put option, Aggregate would

sell its stake in Consus Real Estate to ADO at a price of either i) EUR 8.35

per share in cash or ii) at a share ratio of 1 newly issued ADO share = 0.2390

Consus share, whichever ADO chooses.

The option agreements expire on 16 June 2021.

A bridge financing facility was

agreed with J. P. Morgan

Public takeover bid by ADO

Properties for the remaining

3% of Westgrund

ADO Properties acquired

22.18% of Consus’s shares

plus call option for further

50.97%

ADO Properties S.A. (Adler Real Estate Group)

Page 12 of 62

Through its cooperation agreement with Consus, ADO aims to implement a “build-

to-hold” strategy and expand it in the future. This should serve to reduce its

marketing and distribution costs and ultimately make it more cost-efficient.

On 17 January 2020 ADO signed a letter of intent with Consus Swiss Finance AG to

acquire 89.90% of all companies belonging to the Holsten Quartier development

project. The preliminary purchase price for 100% of the shares stands at EUR 350m.

Part of the bridge financing facility agreed with J. P. Morgan – namely EUR 1.428bn

– can also be used for the debt of Consus Real Estate if ADO acquires a majority of

Consus.

Current Group structure Chart of the current group structure

Ado Group

ADO Properties

ADLER Real Estate

BCP Accentro Westgrund

Consus

CG GroupConsus Swiss

Finance

25,0% (incl. 3% shares of ADLER)94,2% (incl. Treasury stocks)

75% 93%96,9%69,8%

33,3%

3,1%

Holding Takeover bid

100%

4,8%

Source: ADO, ADLER, Consus, FMR

Through its cooperation

agreement with Consus, ADO

aims to implement a “build-

to-hold” strategy

LOI to acquire the Holsten

Quartier development project

Part of the bridge financing

facility can also be used for

the debt of Consus Real Estate

ADO Properties S.A. (Adler Real Estate Group)

Page 13 of 62

Valuation Note regarding the merger:

Since there is still no joint income statement, balance sheet and cash flow

statement, it is more difficult to come to an overall outlook (especially as a result of

the fair value adjustments of the properties and assets). Therefore, our income

statement, balance sheet and cash flow estimates in the appendix are limited to

ADO Properties Standalone. At this point in time, we also did not include Consus in

the group, as the option had not yet been executed and it is therefore not possible

to make a more detailed assessment of the new planned group. In particular, no

reliable statements can be made about the interest-bearing liabilities (net debt,

interest rate and LTV). Currently no reliable statements about the market situation

can be made either because of the distortions caused by Covid-19 and planned

capital increase and the execution of the option on Consus need to be carried out.

For the valuation of ADO we have considered solely the current situation as of 2019

as well as the already completed points from phase 1.

Summary To derive the fair value of the individual companies and of the new ADLER Real

Estate Group, we applied one valuation approach, EPRA NAV. We focused on the

multiples for the year 2022e, as this would be the first year in which ADO, ADLER

and Consus would be fully integrated.

EPRA NAV is a good model for real estate companies, because it incorporates net

asset value based on the attributable market values of the property assets.

Since the takeover process is still in progress, we have decided to conduct both

stand-alone valuations for all companies and a combined valuation. With regard to

our combined valuation, we would point out that we do not include any potential

synergy effects given that certain data points are missing due to the integration of

ADO and ADLER which is still to follow.

In the following sections we have valued all companies both individually and on a

combined basis. Our target price for ADO stand-alone works out to EUR 35.00; for

ADO + ADLER, i.e. the new ADLER Real Estate Group, we derive a fair value per share

of EUR 46.58. Under normal circumstances we would base our target price on a

combined entity valuation, since this is corresponding to the new group. But these

are not normal circumstances. The ADO share continues to trade at ~EUR 24, and

even we assume that COVID-19 has no negative operating impact on the group, the

equity market at large remains in negative territory compared to pre-Corona levels.

And since there is currently no way of knowing how long the lockdown, the worries,

fears, and panic will continue to dominate the market, we have cautiously decided

to use ADO’s stand-alone fair value as our TP, as we assume that in least in H2 2020e

the equity markets will “normalise” and investors will no longer be purely risk-off

on mid-cap shares but will return to the segment with a view to its fundamental

strength. In the current period of market uncertainty, we consider our stand-alone

FVpS for ADO of EUR 35.54, which still suggests upside of around 50%, a more

EPRA NAV valuation approach

applied to derive the fair

value

EPRA NAV is a good model for

real estate companies

We have decided to conduct

stand-alone valuations for all

companies and a combined

valuation

Our target price for ADO

stand-alone: EUR 35.00;

ADLER Real Estate Group:

EUR 46.58

Cautiously decided to use

ADO’s stand-alone fair value

as our TP

ADO Properties S.A. (Adler Real Estate Group)

Page 14 of 62

realistic price target than our fair value per share for the “new group”. In view of

this upside, we initiate coverage with a clear BUY recommendation. Our price target

stands at EUR 35. Nonetheless, we would point out that the share could outperform

strongly once the markets have fully freed themselves from COVID-19.

ADO: stand-alone valuation ADO: EPRA NAV valuation

Source: Factset, FMR

ADO sold its largest portfolio, the Carlos portfolio, in 2019, and so we expect its NRI

to be lower in 2020e. The core of ADO’s business model is modernisation. That is

why we assume that despite the Berlin rent cap ADO will achieve slight rent

increases in its portfolio in the coming years. ADO itself projects a decrease in its

2020 NRI of not quite EUR 1m, which will be largely offset going forward by positive

modernisation effects.

ADO KPIs

Source: ADO, Factset, FMR *Share prices for 2020-2022e are the current Factset’s Consensus for the target share price

We continue to estimate no major impact from the Berlin rent cap either on fair

values of the real estate assets or on the current large gap between market values

and rent prices. Consequently, we estimate a diluted EPRA NAV p/s of EUR 47.82

for 2022e. Discounting this value back to present at ROE, we derive an absolute

value per share of EUR 35.54, which corresponds to upside of more than 50%.

kEUR 2017 2018 2019 2020 (currently) 2020e 2021e 2022e

Share price 42,28 45,52 32,10 24,32 26,80 26,80 26,80

Market cap 1.864.548 2.007.478 1.417.247 1.350.116 1.487.792 1.487.792 1.487.792

Lettable area in sqm 1.066.014 1.315.357 1.528.613 1.125.391 1.181.660 1.240.743 1.240.743

Market cap/sqm 1,75 1,53 0,93 1,20 1,32 1,26 1,20

Enterprise Value 3.551.318 3.694.248 3.115.267 3.359.524 3.497.200 3.521.028 3.527.362

EV/sqm 3,33 2,81 2,04 3,11 3,11 2,98 2,84

EPRA NAV 1.988.757 2.429.544 2.905.699 3.510.518 3.510.518 3.619.658 3.731.043

EPRA NAV per share 45,10 55,05 65,79 63,24 63,24 65,20 67,21

Book value per share 40,71 48,73 59,93 58,30 58,30 59,96 61,64

Lower NRI expected for 2020e

No major impact on market

values expected

ADO Properties S.A. (Adler Real Estate Group)

Page 15 of 62

The reason for this high upside is that ADO is currently trading at a discount to EPRA

NAV of more than 60%, while peers are trading at discounts of around 30%. While

the share prices of many companies have been hit by COVID-19, ADO’s share price

has plunged by as much as 60% in the last 2 months. In our opinion, investors in

this current phase have perceived the uncertainty related to the ongoing takeover

process for ADLER as a negative signal, and this is probably what drove the sell-off.

But now, as the deal is closed, we see no reason why ADO should not return to a

normal discount level of 30%. For even without synergies and excluding ADLER’s

NAV, ADO is currently favourably valued and thus a clear BUY.

ADLER: stand-alone valuation ADLER: EPRA NAV valuation

Source: Factset, FMR

Our stand-alone valuation of Adler renders a fair value per share of EUR 23.90

based on diluted EPRA NAV per share in 2022e. After discounting this value back to

present value at ROE, we derive an absolute value per share of EUR 17.77.

Despite a good underlying business performance in 2019, the share is trading at a

discount to EPRA NAV of more than 60%. We see this discount as exaggerated, even

on a stand-alone basis, since ADLER should continue to generate growth in 2020e,

2021e, and 2022e, according to our estimates.

Upside exists, as ADO is

currently trading at a discount

to EPRA NAV of more than

60%, while peers are trading

at discounts of around 30%

ADLER stand-alone -

EUR 17.77 per share

Positive outlook for

the next years

ADO Properties S.A. (Adler Real Estate Group)

Page 16 of 62

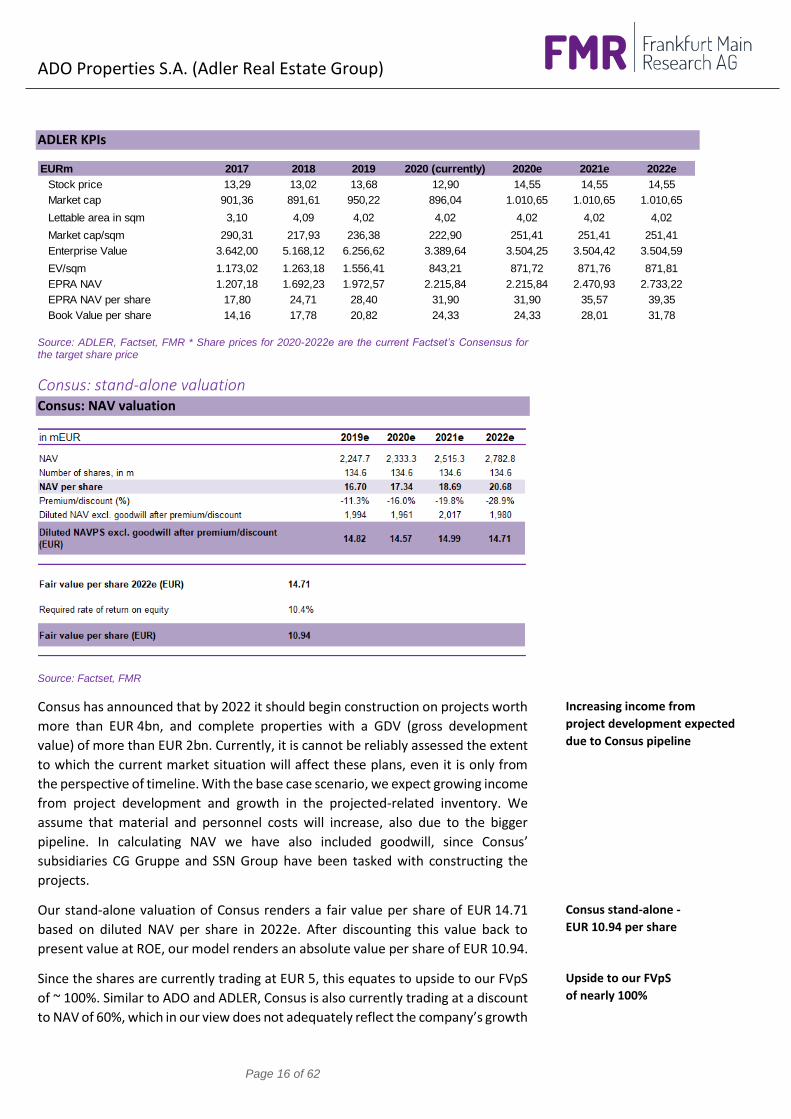

ADLER KPIs

Source: ADLER, Factset, FMR * Share prices for 2020-2022e are the current Factset’s Consensus for the target share price

Consus: stand-alone valuation Consus: NAV valuation

Source: Factset, FMR

Consus has announced that by 2022 it should begin construction on projects worth

more than EUR 4bn, and complete properties with a GDV (gross development

value) of more than EUR 2bn. Currently, it is cannot be reliably assessed the extent

to which the current market situation will affect these plans, even it is only from

the perspective of timeline. With the base case scenario, we expect growing income

from project development and growth in the projected-related inventory. We

assume that material and personnel costs will increase, also due to the bigger

pipeline. In calculating NAV we have also included goodwill, since Consus’

subsidiaries CG Gruppe and SSN Group have been tasked with constructing the

projects.

Our stand-alone valuation of Consus renders a fair value per share of EUR 14.71

based on diluted NAV per share in 2022e. After discounting this value back to

present value at ROE, our model renders an absolute value per share of EUR 10.94.

Since the shares are currently trading at EUR 5, this equates to upside to our FVpS

of ~ 100%. Similar to ADO and ADLER, Consus is also currently trading at a discount

to NAV of 60%, which in our view does not adequately reflect the company’s growth

EURm 2017 2018 2019 2020 (currently) 2020e 2021e 2022e

Stock price 13,29 13,02 13,68 12,90 14,55 14,55 14,55

Market cap 901,36 891,61 950,22 896,04 1.010,65 1.010,65 1.010,65

Lettable area in sqm 3,10 4,09 4,02 4,02 4,02 4,02 4,02

Market cap/sqm 290,31 217,93 236,38 222,90 251,41 251,41 251,41

Enterprise Value 3.642,00 5.168,12 6.256,62 3.389,64 3.504,25 3.504,42 3.504,59

EV/sqm 1.173,02 1.263,18 1.556,41 843,21 871,72 871,76 871,81

EPRA NAV 1.207,18 1.692,23 1.972,57 2.215,84 2.215,84 2.470,93 2.733,22

EPRA NAV per share 17,80 24,71 28,40 31,90 31,90 35,57 39,35

Book Value per share 14,16 17,78 20,82 24,33 24,33 28,01 31,78

Increasing income from

project development expected

due to Consus pipeline

Consus stand-alone -

EUR 10.94 per share

Upside to our FVpS

of nearly 100%

ADO Properties S.A. (Adler Real Estate Group)

Page 17 of 62

opportunities. Even if the discount to NAV should “only” shrink to 30%, the shares

could double in value. Questionable is whether the investors are willing to grant

project developers like Consus a low discount on the NAV.

Project developers, for example in UK, the Netherlands or Austria, are traded on

average at a discount of 30% to the NAV, which also reflects the increased risk

appetite among investors there. In Germany, real estate project developers have

had difficulties in all of the pervious real estate stock cycles.

Consus KPIs

Source: Consus, Factset, FMR * Share prices for 2020-2022e are the current Factset’s Consensus for the target share price

Peer group valuation To incorporate a market-based approach into our valuation, we have introduced a

peer multiple. The peer group consists of other real estate companies which rent

flats throughout Germany. Most of the peer group companies focus on residential

properties and as such are comparable to ADO and ADLER. PATRIZIA should be

viewed with caution, however, since it has a very broad business mix with

residential properties making up only a fourth of its total real estate portfolio.

Our peer group includes 30 companies. Having said that, a large share of peers

either have no consensus estimates available or only stale ones, which means it

makes little sense to use these companies for comparison purposes.

Peer group overview

Source: Factset, FMR

EURm 2017 2018 2019e 2020 (currently) 2020e 2021e 2022e

Stock price 8,07 7,60 7,32 5,00 7,00 7,00 7,00

Market cap 263,5 649,9 984,9 672,8 941,9 941,9 941,9

Project volume (GDV) 4,5 9,6 10,3 10,3 10,3 10,3 10,3

Market cap/project volume 58,0 67,7 95,6 65,3 91,4 91,4 91,4

Enterprise Value 2.073,5 3.232,4 5.531,6 5.167,2 5.436,3 5.648,4 6.183,7

EV/project volumes 456,1 336,7 537,0 501,7 527,8 548,4 600,4

NAV incl. Goodwill 749,8 1.125,3 2.247,7 2.333,3 2.333,3 2.515,3 2.782,8

NAV per share 22,97 13,16 16,70 17,34 17,34 18,69 20,68

Book value per share 19,79 11,82 7,54 8,02 8,02 8,02 8,02

Peer group includes

companies with a focus on

renting properties

Reduced peer group due to

database

ADO Properties S.A. (Adler Real Estate Group)

Page 18 of 62

ADO + ADLER: combined valuation ADO + ADLER: EPRA NAV valuation

Source: Factset, FMR

Our valuation of ADO and ADLER combined renders a fair value per share of

EUR 65.79 based on diluted EPRA NAV per share in 2022e. Discounting this back to

present value at ROE, our model renders an absolute value per share of EUR 46.58.

This would be almost 31% above our stand-alone fair value for ADO.

In this calculation we have include no potential takeover synergies since the

integration has not provided many data points yet. Management assumes there

will be significant synergy effects from the integration – an assumption we also

consider realistic – but at present we cannot reliably quantify such effects. In

contrast to our stand-alone valuation of ADO, we have stripped ADLER’s value back

out of ADO in 2019, which we had factored in for 2019, since here we include ADLER

as a separate entity.

This valuation shows that this deal is a clear BUY, and that as soon as the equity

market and the company return to a certain “normalcy” post COVID-19 and the

shares are analysed again based on underlying fundamentals, the new ADLER Real

Estate Group will be one of the most interesting shares in the real estate space. Not

only will the new group be a direct MDAX candidate, but it will also have massive

catch-up potential given that the shares of all three constituent companies (ADO,

ADLER, Consus) have fallen drastically.

For investors who wish to position themselves for the long term now, the new

ADLER Real Estate is well worth looking at. Because these elevated discounts

compared to most other peers will only be temporary – of that we are very

confident.

Fair value per share of ADLER

Real Estate Group: EUR 46.58

Scenario without consi-

deration of synergy effects

Valuation shows that this deal

is a clear BUY

For investors who wish to

position themselves for the

long term now, the new

ADLER Real Estate is well

worth looking at

ADO Properties S.A. (Adler Real Estate Group)

Page 19 of 62

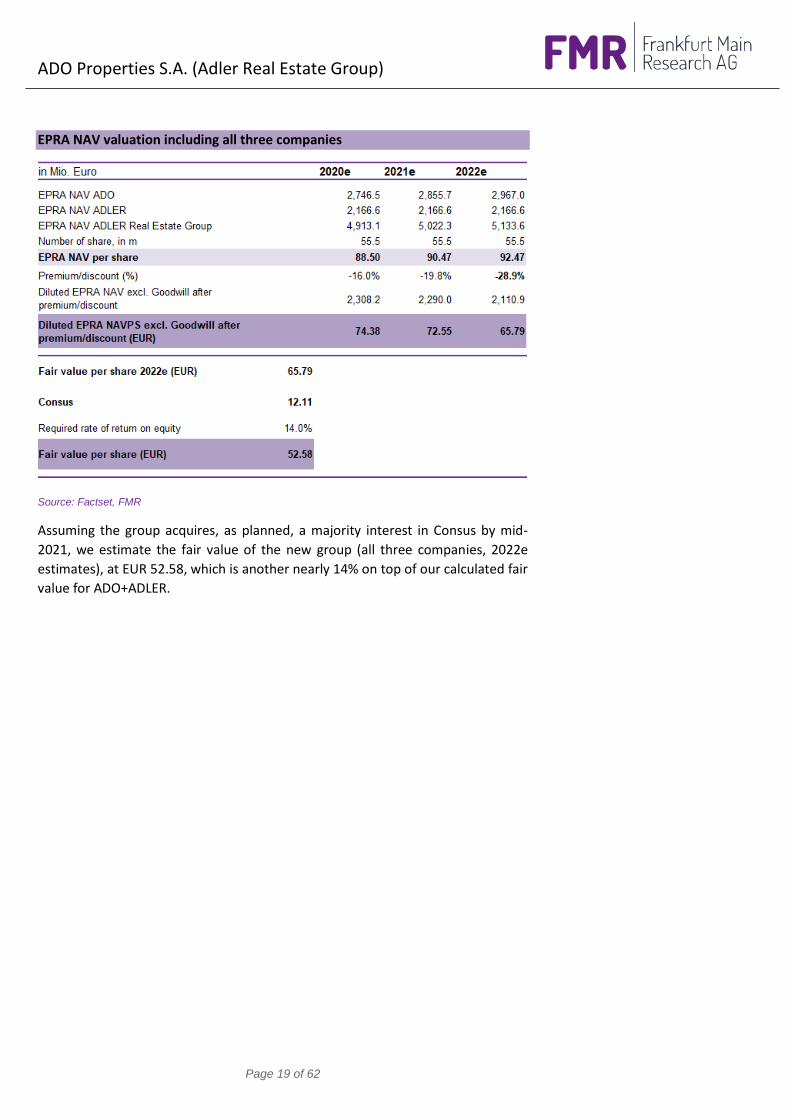

EPRA NAV valuation including all three companies

Source: Factset, FMR

Assuming the group acquires, as planned, a majority interest in Consus by mid-

2021, we estimate the fair value of the new group (all three companies, 2022e

estimates), at EUR 52.58, which is another nearly 14% on top of our calculated fair

value for ADO+ADLER.

ADO Properties S.A. (Adler Real Estate Group)

Page 20 of 62

ADO’s company profile ADO Properties is a listed residential real estate company active solely in the Berlin

market. The lion’s share of the ADO Properties portfolio consists of centrally

located properties or properties in interesting peripheral locations.

The ADO Properties Group, with the help of its subsidiaries, covers the entire

property asset management value chain, from screening to acquisitions to the

administration of suitable properties. The strategic focus of the ADO Properties

Group is increasing the value of its real estate portfolios. By investing in the

modernisation of its portfolios, it can achieve higher rents and lower vacancies.

ADO Properties has about 18,000 units (source: Fact Sheet dated 20 February

2020). Another business, launched by ADO Properties in 2014, is the privatisation

business.

After ADLER acquired the ADO Group (a listed holding from Israel), ADO Properties’

main shareholder, ADO Properties, publicly announced on 15 December 2019 a

voluntary public takeover bid for ADLER. According to its announcement dated 30

March, ADO now owns 91.93% of ADLER. On 09 April the deal was settled and the

shares were delivered.

With the cooperation agreement that it signed on 15 December 2019 with project

developer Consus Real Estate, ADO Properties intends to pursue a “build-to-hold”

strategy. Options agreed with the Consus’s main shareholder, Aggregate Holding,

could, if exercised, make ADO the main shareholder in Consus.

ADO Properties was founded in 2007, first as a limited liability company (GmbH)

under the name of “Swallowbird Trading & Investments Limited“ with domicile in

Cypress. In 2015 the company moved its domicile to Luxembourg and changed its

legal form to that of a limited liability company under Luxembourg law. After that

it became a public company limited by shares (Aktiengesellschaft) and changed its

name to “ADO Properties.”

Group structure ADO Properties is a holding company of the ADO Properties group. Its operating

activities are generally carried out by its 197 subsidiaries (date of information: 30

September 2019). ADO Properties provides management and administrative

functions. The organisational chart below shows the group’s key subsidiaries.

ADO Properties covers the

entire property management

value chain

ADO Properties’ takeover bid

for ADLER

Cooperation agreement with

Consus Real Estate

Founded in 2007, listed since

2015

The holding company of the

ADO Properties Group

ADO Properties S.A. (Adler Real Estate Group)

Page 21 of 62

Group structure

ADO Properties S.A.(Luxembourg)

ADO Lux-EEME S.a.r.l.

(Luxembourg)

ADO FC Management Unlimited Company

(Ireland)

ADO Lux FinanceS.a.r.l.

(Luxembourg)

ADO Malta Limited (Malta)

ADO Properties GmbHADO Immobilien Management GmbHCCM City Construction Management

Central Facility ManagementADO Treasury GmbH

ADO Living GmH(Germany)

31SPVs (GmbH) Plus 2 BV and 2 ApS

(Germany/NL/DK)

30 SPV s (29 GmbH and1 S.a.r.l.) Plus 1 BV

(Germany/LU/NL)

4 SPVs (BV) (Netherlands)

50 SPVs (GmbH) Plus 1 BV

(Germany/NL)

EPF Acqusition Co 86 S.a.r.l.

(Luxembourg)

ADO SBI Holdings S.A. & Co. KG (Germany)

Consus Real Estate AG (Germany)

59 SPVs (GmbH) (Germany)

Residential properties

Berlin

Residential properties

Berlin

Residential properties

Berlin

Residential properties

Berlin

Residential properties

Berlin

6% Kommanditist

94%

94%

6%

100% 100%94,9% 93,7% - 94,9% 60%

100%100%

100%100%

22,18%

Source: ADO Properties, FMR (date of information: 07 Feb 2020)

Management/supervisory board Thierry Beaudemoulin has been CEO at ADO Properties since 10 December 2019.

After earning his master’s degree in real estate and urban planning, Thierry

Beaudemoulin’s positions included special advisor to the chief executive officer

(Batigere), head of property management (Foncia), asset manager (ING REIM) and

managing director France (ING REIM). His last position before he became CEO at

ADO Properties was that of executive board member from 2006 to 2019 at Covivio

and CEO of Covivio Deutschland. He will be Co-CEO at the newly created ADLER Real

Estate Group (which will integrate ADLER and change its name from ADO to ADLER

Real Estate Group).

At present ADO Properties’ supervisory board has seven members. The supervisory

board chairman is Dr Peter Maser. Dr Maser received his doctorate from the

University of Tübingen. He is admitted to the German bar. Prior to partnerships at

a law firm in Freiburg im Breisgau and at Deloitte Legal Rechtsanwaltsgesellschaft

mbH, he was employed at various auditing firms, trust firms, and the Ebner Media

Group. Dr. Maser is also currently deputy chairman of the supervisory board at

Volksbank Stuttgart eG, and supervisory board chairman at both BF direkt AG and

EURAM Bank AG.

Dr. Ben Irle, after his academic training at a partnership, founded a law firm in

Berlin (2005-2011). In the ensuing years he was a managing partner at Irle

Kalckreuth LLP (2012-2013) and Irle Moser Rechtsanwälte PartG (since 2014). Dr.

Ben Irle currently holds additional positions at ADO Group Ltd. (member of

supervisory board) and Focus Hören AG (chairman of supervisory board).

Florian Sitta successfully completed his legal studies in 2002. The following year he

was admitted to the German bar. He began his professional career as a legal counsel

and head of the legal department at Beate Uhse AG (2004-2015). He has been the

head of the legal department at Adler Real Estate AG in Hamburg and Berlin since

Thierry Beaudemoulin - CEO

Dr. Peter Maser - Chairman of

Supervisory Board

Dr. Ben Irle -

Supervisory board member

Florian Sitta -

Supervisory board member

ADO Properties S.A. (Adler Real Estate Group)

Page 22 of 62

2016. He also currently holds positions at ADO Group Ltd. (member of supervisory

board) and Sitta & Partner Gesellschaft für Logistik mbH (managing director).

Arzu Akkemik began her career as an analyst at Barings Securities in London after

completing her studies of international finance and accounting. Besides her

activities as an analyst, she was active in the company areas of corporate finance

and fund management. From 2005 to 2013 she was employed in London at Rexiter

Capital as a director/senior fund manager. In 2013 she founded Cornucopia

Advisors Limited and Cornucopia Asset Management Limited.

Dr. Michel Bütter has a doctorate in law. He is admitted to the German bar and has

gathered experience at various law firms (2001-2008). He has also held numerous

other positions in corporate management bodies. Currently Dr. Bütter holds

positions at ASSMANN BERATEN+ PLANEN AG (deputy chairman of supervisory

board), RCIS (member of board of management), Realconnext.com (chairman of

advisory council) and Bots4YouGmbH (member of advisory council and

shareholder).

Jörn Stobbe began his professional career in 1995 after completing his law studies

and passing his second state law examination. His first employer was

Landgesellschaft Schleswig-Holstein mbH. In the years thereafter we worked at the

law firm Clifford Chance (2000-2013) and RREEF Management GmbH (2013-2017).

Mr Stobbe currently holds additional positions at Union Investment Real Estate

GmbH (executive board member), Union Investment Institutional Properties GmbH

(management member) and at 1. FC Köln KGaA (chairman of supervisory board).

Shareholder structure The shareholder structure of the company includes a substantial free float

component of 80%. ADLER Real Estate holds 20.45% of the shares. Further

shareholders are Klaus Rudolf Wecken (5.74%), Mirabella Malta Ltd. (5.52%),

Mezzanine IX Investors S.A. (5.31%) and Union Investment Privatfonds GmbH

(4.37%).

Current shareholder structure

Source: ADO Properties, FMR (date of information: 31 March 2020)

20,45%

5,74%

5,52%

5,31%

4,37%

58,61%

ADO Group Ltd. Klaus Rudolf Wecken Mirabella

Mezzanine IX Union Investment Freefloat

Arzu Akkemik -

independent member of

supervisory board

Dr. Michael Bütter -

independent member of

supervisory board

Jörn Stobbe -

Independent member of

supervisory board

Shareholder structure: free

float of about 80%

ADO Properties S.A. (Adler Real Estate Group)

Page 23 of 62

ADLER’s company profile ADLER Real Estate has been active in the real estate industry for more than 20

years. Its focus lies on buying residential properties and managing permanently

held properties. At present ADLER manages more than 58,000 rental units

throughout Germany. ADLER’s business model also includes the purchase of real

estate portfolios and interests in other real estate companies.

Since the end of 2018 ADLER has invested in development projects in A-locations,

which constitute ~14% of its GAV (gross asset value). It pursues a “build-and-hold”

strategy, which will lead to growth in the existing residential portfolio. The

acquisition of 70% of the Brack Capital Properties N.V. (BCP) in 2018 brought new

development projects into the portfolio.

Since the group has a strict residential focus, it is selling BCP’s commercial portfolio.

67% of the commercial properties have already been sold, and the remaining assets

will follow as soon as possible. The disposal proceeds will be used mainly to pay

down bank debt, leading to a lower LTV ratio.

ADLER invests primarily in peripheral locations and growing metropolitan areas in

northern western, and eastern Germany. The idea here is to benefit from the

favourable real estate growth in B cities. The company’s geographic focus is on

Lower Saxony and North Rhine-Westphalia. Most of the properties are acquired in

a finished state with initially higher vacancies. The company endeavours to reduce

vacancies through active asset management. Its facility and property management

services are provided by the group’s subsidiaries.

Company history In 1880, Adlerwerke vorm. H. Kleyer AG was founded in Frankfurt and

manufactured automobiles, motor cycles, bicycles and typewriters.

In 1993 the company was sold to the real estate investor Roland Ernst and the

Philipp Holzmann construction group.

In 1998 typewriter production was discontinued and the company’s main business

became property rental. The company had already discontinued its other product

areas long ago: cars in 1945, motorcycles in 1958, and bicycles in 1945.

In 2002 the company’s name was changed to ADLER Real Estate, and its corporate

domicile was relocated to Berlin. ADLER’s real estate portfolio has grown strongly

in the last five years through the acquisition of real estate companies:

2014: Takeover of 92.7% of Accentro Real Estate (at the time: ESTAVIS AG) for

EUR 23.2m

2015: Acquired Mountain Peak Trading Ltd. (an investment holding company).

This acquisition gave ADLER a minority (24.79%) interest in Conwert

Immobilien Invest SE.

Acquired Treuhaus Hausbetreuungs-GmbH, which oversees the property

management activities for south-western Germany.

ADLER Real Estate focuses on

the management of properties

held on a long-term basis

2018 ADLER has invested in

development projects, which

constitute ~14% of its GAV;

ADLER pursues a “build-and-

hold” strategy

BCP’s commercial portfolio

will be sold

ADLER invests primarily in

peripheral locations and

growing metropolitan areas in

northern western, and eastern

Germany

1880 the Adlerwerke was

founded

1993 the company was sold

1998 the company’s main

business became property

rental

2002 the name was changed

and 2016 its corporate domi-

cile was relocated to Berlin

2014 Takeover of Accentro

2015 Takeover of Mountain

Peak Trading Ltd.

2015 Takeover of Treuhaus

Hausbetreuungs-GmbH

ADO Properties S.A. (Adler Real Estate Group)

Page 24 of 62

Acquired ~95% of Wohnungsbaugesellschaft JADE with a portfolio of 6,750

residential units. Wohnungsbaugesellschaft JADE’s subsidiary JADE

Immobilien Management is the property manager for properties in north-

western Germany.

Acquired the vast majority of WESTGRUND AG. At the end of 2016 ADLER’s

interest in WESTGRUND exceeded 95%, and so it acquired the remaining

shares in a squeeze-out. WESTGRUND focuses on acquiring, managing, and

servicing German residential properties.

2017: Sold Accentro Real Estate AG to Vestigo Capital Advisors.

2018: Acquired ~70% of Brack Capital Properties NV. (BCP) BCP is a private equity

company focusing on properties in Germany. This acquisition added

~12,000 residential units to ADLER’s portfolio.

2019: Acquired ADO Group, which gave ADLER Real Estate a minority (33.25%)

interest in ADO Properties

Group structure The ADLER Group encompasses nearly 230 individual companies and contribute to

a high level of complexity, also due to the many acquisitions made. Most of these

subsidiaries are property companies whose portfolios represent the entirety of

ADLER Real Estate’s property assets. The acquired companies Westgrund and BCP

still exist as sub-groups. Property management of the residential units is carried out

primarily by ADLER Wohnen Service. ADLER Gebäude Service performs facility

management functions at nearly all locations. Heating and energy supply is

concentrated at ALDER Energie Service.

ADLER reports on two main segments: Portfolio and Other. The Portfolio segment

includes existing properties from which rental income is generated. This also

includes the asset and property management activities. This segment also includes

the BCP properties earmarked for disposal as well as project developments. The

“Other” segment includes older development projects or other group activities that

cannot be formed into a separate segment.

Management Tomas de Vargas Machuca (1974) has been the chairman of the executive

committee since 2013 and Co-CEO since the end of 2017. He completed his studies

of business and economics at Bocconi University in Milan (Italy) and has more than

15 years’ experience in the real estate industry. Tomas de Vargas Machuca has 10

years of experience in executive positions. His areas of activity have included

banking, private equity, finance and investment.

Maximilian Rienecker (1985) has been head of corporate finance & strategy since

February 2017 and Co-CEO since December. He completed his management studies

at the University of Nottingham. Rienecker has been employed in the areas of sales

& marketing, corporate strategy and M&A. He has four years of experience in the

real estate industry. On 9 April 2020 he was appointed as Co-CEO of the newly

created ADLER Real Estate Group.

2015 Acquired JADE

2015 Acquired WESTGRUND

2017 Sold Accentro

2018 Acquired BCP

2019 Acquired ADO Group

Tomas de Vargas Machuca –

Co-CEO

Maximilian Rienecker –

Co-CEO

Two segments: Portfolio and

Other

The ADLER Group encompasses

nearly 230 individual companies

ADO Properties S.A. (Adler Real Estate Group)

Page 25 of 62

Sven-Christian Frank (1965) has been COO since June 2016. He has been with the

company since 2015 and had previously served in management positions at real

estate companies such as Gestrim Deutschland AG and Deutsche Real Estate AG.

Sven-Christian Frank completed his law studies at Ludwig Maximilian University of

Munich.

Shareholder structure The shareholder structure of the company includes a substantial free float

component of 43.11%. The company’s anchor shareholders are Mezzanine IX,

Wecken and Fairwater, which together hold 42.95% of its shares. ADLER Real Estate

holds 2.3% of its own shares, Thomas Bergander has another 6.7%, and the

investment management company Fil Investments International holds a stake of

5% of shares in issue.

Current shareholder structure

Source: ADLER Real Estate, FMR (date of information: 31 Dec 2019)

Consus’s company profile Consus Real Estate AG is the fastest growing real estate developer and has a

pipeline of more than 15,000 residential units (a total of 67 projects) in Germany’s

Top 9 cities (Berlin, Munich, Frankfurt, Düsseldorf, Cologne, Hamburg, Stuttgart,

Leipzig and Dresden). These locations represent Germany’s most important cities

for the real estate economy.

One of Consus’s key points of focus is the development of quartiers (entire

neighbourhoods or districts) and standardised multi-story flat blocks. The company

develops mixed-use development projects that incorporate commercial and retail

space. Additionally, Consus develops residential properties by repurposing and

reconstructing former commercial and industrial properties. Most of these

properties are sold forward to institutional clients. Such forward sales are intended

to minimise project development risks.

Free Float; 43,11%

Wecken; 14,97%

Mezzanine IX; 14,44%

Fairwater; 13,54%

Thomas Bergander;

6,66%

FIL; 5,02%Treasury

Shares; 2,26%

Sven-Christian Frank –

COO

Shareholder structure of the

company includes a

substantial free float

component of 43.11%

Consus Real Estate AG is the

leading real estate developer

and has a pipeline of more

than 15,000 residential units

Consus: focus on development

of quartiers and standardised

multi-story flat blocks

ADO Properties S.A. (Adler Real Estate Group)

Page 26 of 62

Thanks to the process of digitalisation in the construction industry and the

company’s own construction expertise, Consus covers the entire real estate

development value chain. The individual steps along the value chain are performed

by subsidiaries CG Gruppe AG and Consus Swiss Finance AG.

Group structure Consus Real Estate had already acquired 50.0% of the project developer CG Gruppe

in 2017. The following year, in 2018, it increased its holding to 71.0%. The company

founder Christoph Gröner (“CG”) is still committed with 25.0%

In December 2018 Consus Real Estate acquired 93.4% of the small project

developer SSN for EUR 245m. After it was acquired, SSN became a segment at

Consus Real Estate. In 2019 SSN Group was renamed “Consus Swiss Finance“.

Group structure

Source: Consus, FMR

The group generates its revenue from the following five segments:

property rental, changing portfolio assets, property sales, project development as

well as service, maintenance and management activities.

The company is organised into three segments:

1. Consus Real Estate: The focus of this segment is to support the subsidiaries

by performing centralised functions and in letting out properties mainly for

commercial use.

2. CG Gruppe: This includes the development of residential and commercial

properties. CG also lets out properties and provides the services that this

entails.

3. Consus Swiss Finance: This segment is involved in project development,

planning, construction and building technology. It also operates in the area

of letting out residential and commercial properties.

Management Andreas Steyer has been Consus’s CEO since May 2018 and has more than 30 years

of experience in the real estate industry. Prior to joining Consus he was the

Consus covers the entire real

estate development value

chain

Acquisition of CG Gruppe and

SSN Gruppe

Revenues from five segments

Three segments

Andreas Steyer – CEO

ADO Properties S.A. (Adler Real Estate Group)

Page 27 of 62

managing director of the listed real estate company DEMIRE, CEO of Deka

Immobilien Invest and a partner at Ernst & Young Real Estate. Prior to becoming

CEO, Steyer was COO at Consus.

Benjamin Lee has been CFO at Consus since April 2018. Lee has 25 years of

experience in the financial industry including 14 years in investment banking at

UBS. Before joining Consus he was the investment director at Aggregate Holdings,

Consus’s main shareholder. Lee already has experience as a CFO at a listed

company.

Theo Gorens has been the CRO and deputy CFO since May of 2019. Since 2012 he

has sat on the supervisory board and is responsible for risk management and

corporate development of Consus subsidiary SSN Group. Prior to that he held

executive positions in the financial services industry including CFO at Fortis ABN

AMRO and he was a member of Bethmann Bank’s expanded executive board

responsible for structured finance.

Shareholder structure The shares of Consus Real Estate AG are listed in the Scale Segment of Frankfurter

Börse. As shown in the chart below, Aggregate Group owns 51% of the shares. ADO

Properties (22.18%) and ADLER Real Estate (~3.00%) hold another 25%. Christoph

Gröner, CEO of CG Gruppe, holds 6%. The free float is 18% of shares in issue.

Current shareholder structure

Source: Consus, FMR (date of information: 01 Feb 2020)

Aggregate Group; 51%

ADO Properties& ADLER Real Estate; 25%

Christoph Gröner; 6%

Free Float; 18%

Benjamin Lee – CFO

Theo Gorens – CRO and

Deputy CFO

ADO Properties S.A. (Adler Real Estate Group)

Page 28 of 62

ADO’s business model ADO Properties is focused solely on the Berlin residential real estate market. It

specialises in letting out residential properties within Berlin’s city limits. Although

residential units account for just under 95% of the ADO’s portfolio, it also has some

commercial properties. In the past 5 years the number of commercial properties in

the portfolio has doubled and commercial rents have increased by more than 10%.

Thus, the company does not plan to sell any of its commercial portfolio in the

foreseeable future.

ADO also offers a broad spectrum of services. It not only lets out properties, but

also offers property and asset management services. Through active portfolio

management, ADO achieves stable rental growth and declining vacancies.

The company focuses on modernising and renovating its existing portfolio. As a

result, such properties are repositioned and generate higher rental income. Be

letting freshly modernised properties to new tenants, rents increased in 2019 by

2.6%. This strategy could prove to be especially successful in light of the new rent

cap in Berlin. The new regulation in Berlin allows rents to be increased by up to

EUR 1 per sqm. if the property has been renovated. Thus, by modernising the older

flats in its portfolio ADO can increase its rental income despite the new legislation.

ADO is currently investing more than EUR 40 per square meter for modernisation

and repairs, but it intends to lower this figure.

Its vacancy rate stands at 2.5% for residential and 4.6% for commercial properties.

In most cases, the vacant units are under construction, and some are for sale. As a

result, the vacancy rate for rental units is only 0.8%, which is in line with the city of

Berlin’s overall average vacancy rate.

ADO has also been in the privatisation business since 2014. The sale of individual