Embed Size (px)

Citation preview

Ⓒ

Olo

f S

.

Future directions of EU agricultural policies

The CAP towards 2020

Tassos Haniotis, DirectorEconomic Analysis, Perspectives and Evaluations

DG for Agriculture and Rural Development

European Commission

ABARES Outlook 2011, 2 March 2011

Haniotis - ABARES Outlook 20112

Outline

1. The objectives of CAP reform

2. The context of CAP reform

3. The CAP at a glance

4. Policy challenges and options

5. Next steps

Haniotis - ABARES Outlook 20113

CAP reform objectives at a glanceFuture challenges

Economicchallenges

Environmentalchallenges

Territorialchallenges

• Food security

• Price volatility

• Economic crisis

• GHG emissions

• Soil depletion

• Water/air quality

• Habitats/biodiversity

• Vitality of rural areas

• EU rural diversity

• Regional growth

Equity and balance of support

Contribution to Europe 2020 strategy

Viable food production Sustainable management of natural resources

Balanced territorial development

CAP2020 reform objectives

Haniotis - ABARES Outlook 20114

The wider context of CAP reform

The future of the CAP is debated within the context of:

• A cost-driven commodity price boom– the “baseline” to assess the impact of potential policy changes is full of major

uncertainties, mostly of uncertainties outside agriculture

• A new set of EU institutional realities– co-decision after the Lisbon Treaty increases the role not just of the EP in the

decision process, but also of the wider public in the consultation process

• A parallel process of multiple EU policy decisions – CAP reform is linked to the debate about the future EU budget and the wider EU 2020

strategy of “smart, sustainable and inclusive growth”

Haniotis - ABARES Outlook 20115

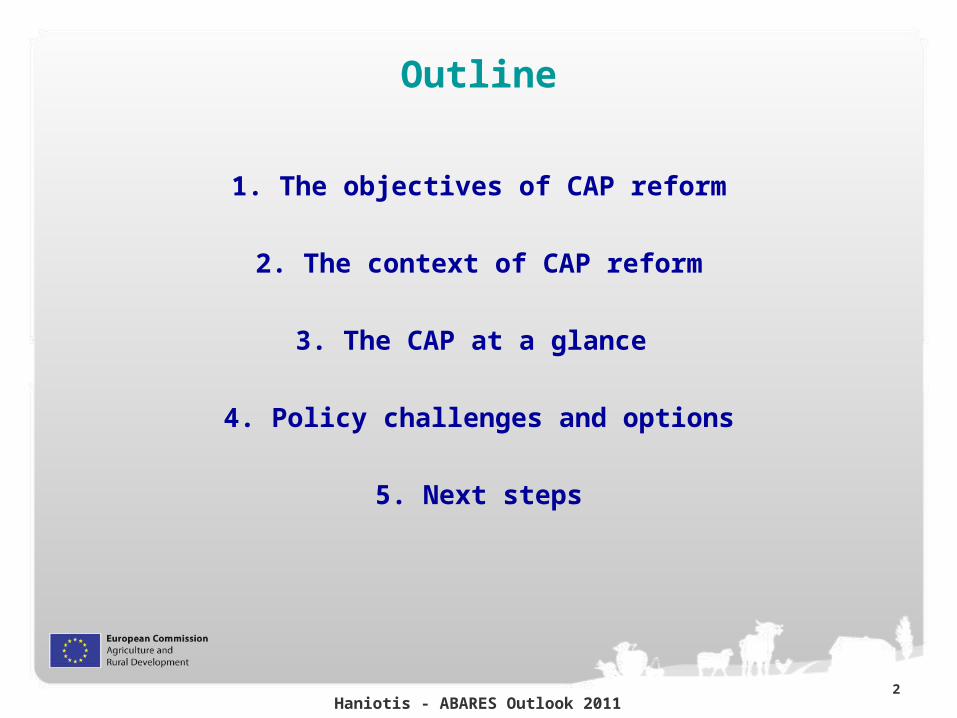

Real commodity prices

(World Bank real price indices, 2000 = 100)

0

100

200

300

400

500

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Agriculture Food Energy Fertilizers Metals/minerals

Haniotis - ABARES Outlook 20116

Energy and agricultural prices

Source: World Bank.

(nWorld Bank nominal price indices, 2000=100)

0

50

100

150

200

250

300

350

400

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Agriculture + 50 % Energy + 223 %

Haniotis - ABARES Outlook 20117

Price developments in the EU food chain

95

100

105

110

115

120

Jan

-07

Ma

r-0

7

Ma

y-0

7

Jul-

07

Se

p-0

7

No

v-0

7

Jan

-08

Ma

r-0

8

Ma

y-0

8

Jul-

08

Se

p-0

8

No

v-0

8

Jan

-09

Ma

r-0

9

Ma

y-0

9

Jul-

09

Se

p-0

9

No

v-0

9

Jan

-10

Ma

r-1

0

Ma

y-1

0

Jul-

10

Se

p-1

0

No

v-1

0

Source: European Commission – DG Economic and Financial Affairs, based on Eurostat data

FOOD PRICE CRISIS

PRODUCER LAG

RETAIL LAG DEJA VU?

Agriculturalcommodity prices

Overall inflation(HICP)

Food producer prices

Food consumer prices

Haniotis - ABARES Outlook 20118

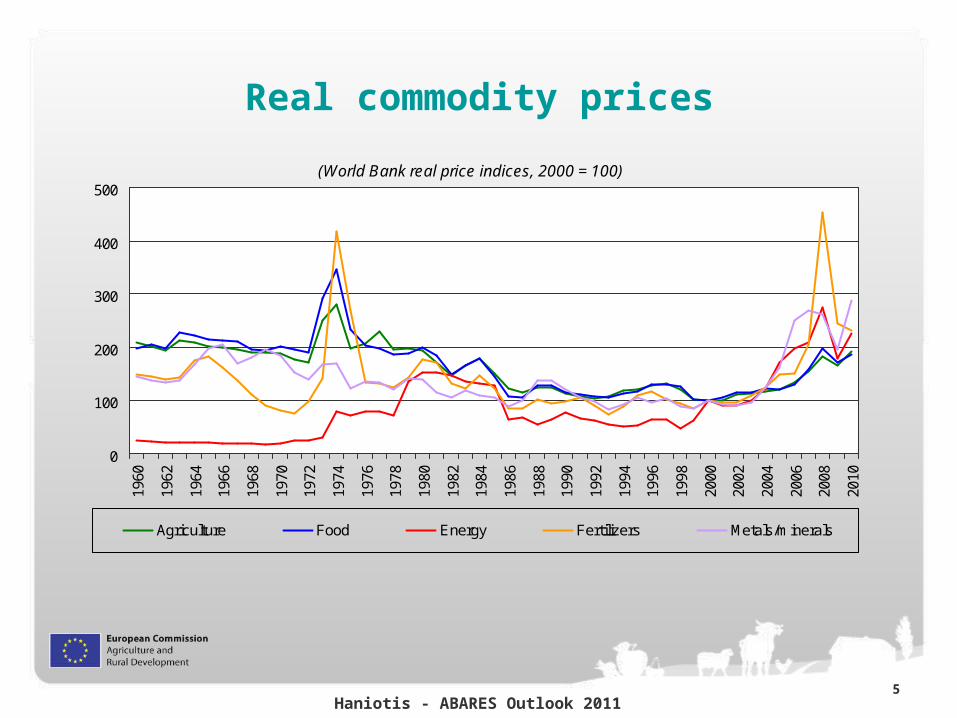

EU agricultural prices

Source: Eurostat

(real price index, 1996 = 100)

70

80

90

100

110

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Output prices - EU-27 Input prices - EU-27

Haniotis - ABARES Outlook 20119

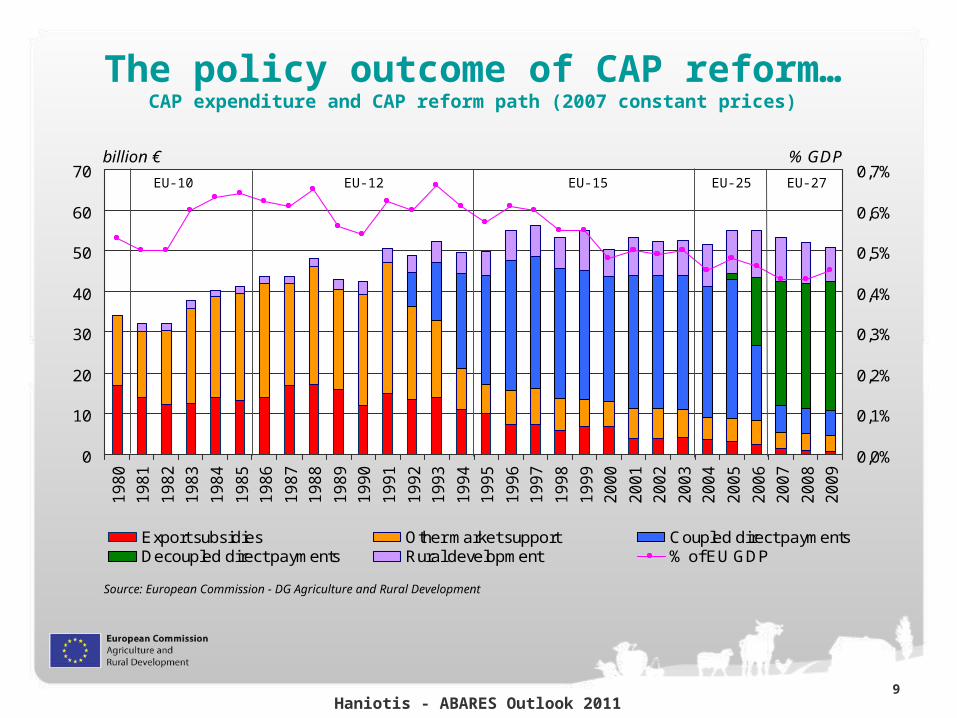

The policy outcome of CAP reform…CAP expenditure and CAP reform path (2007 constant prices)

0

10

20

30

40

50

60

70

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

% GDPbillion €

0,0%

0,1%

0,2%

0,3%

0,4%

0,5%

0,6%

0,7%

Export subsidies Other market support Coupled direct paymentsDecoupled direct payments Rural development % of EU GDP

Source: European Commission - DG Agriculture and Rural Development

EU-10 EU-12 EU-15 EU-25 EU-27

Haniotis - ABARES Outlook 201110

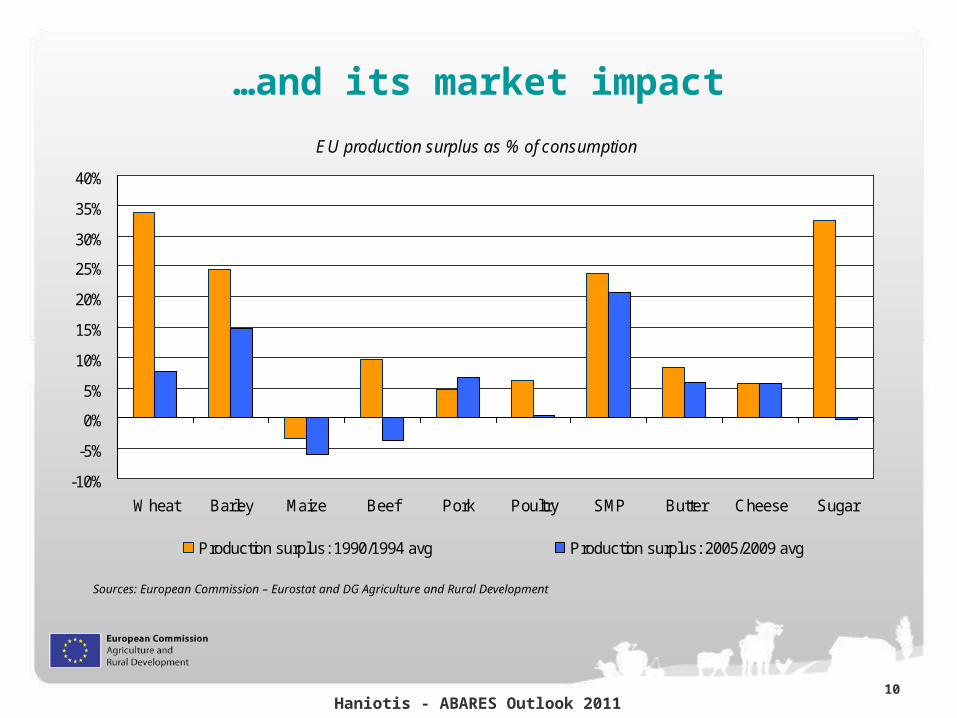

…and its market impact

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Wheat Barley Maize Beef Pork Poultry SMP Butter Cheese Sugar

EU production surplus as % of consumption

Production surplus: 1990/1994 avg Production surplus: 2005/2009 avg

Sources: European Commission – Eurostat and DG Agriculture and Rural Development

Haniotis - ABARES Outlook 201111

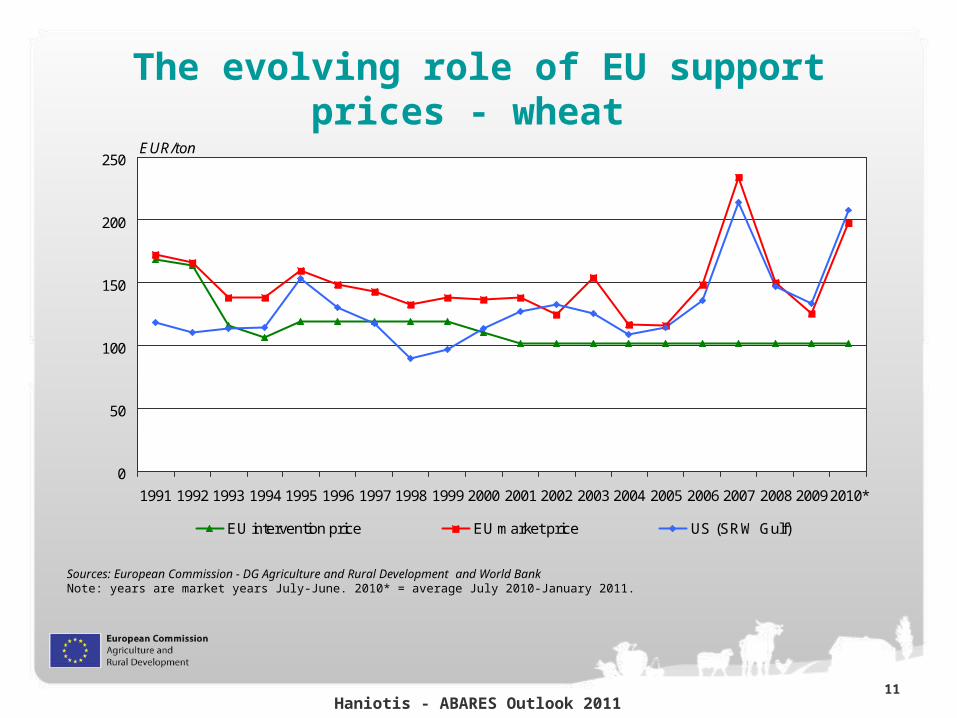

The evolving role of EU support prices - wheat

0

50

100

150

200

250

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20092010*

EUR/ton

EU intervention price EU market price US (SRW Gulf)

Sources: European Commission - DG Agriculture and Rural Development and World BankNote: years are market years July-June. 2010* = average July 2010-January 2011.

Haniotis - ABARES Outlook 201112

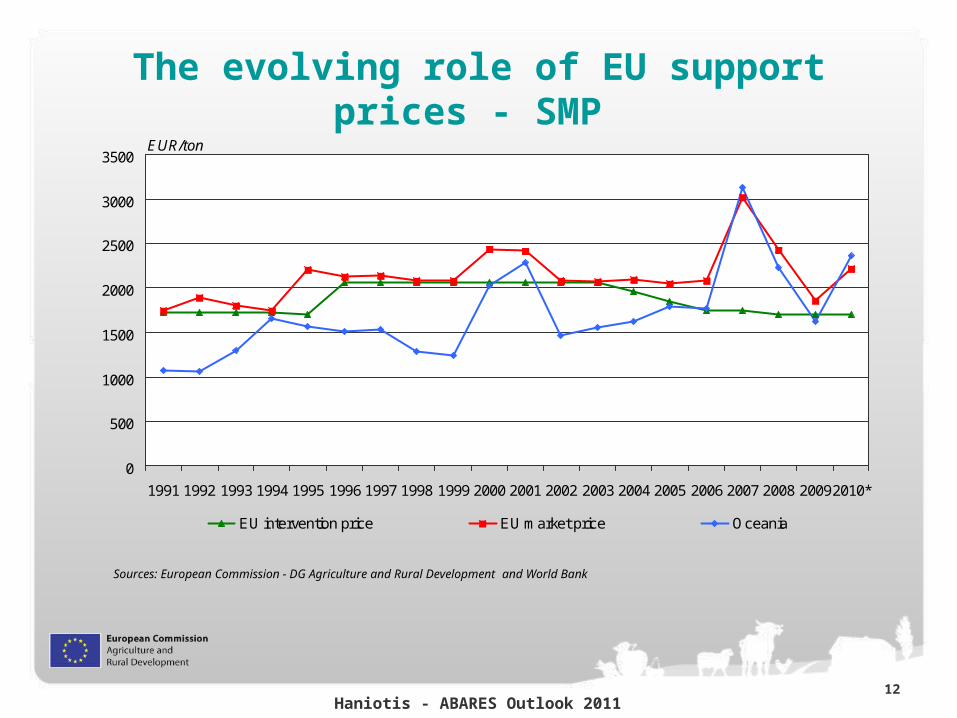

The evolving role of EU support prices - SMP

0

500

1000

1500

2000

2500

3000

3500

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20092010*

EUR/ton

EU intervention price EU market price Oceania

Sources: European Commission - DG Agriculture and Rural Development and World Bank

Haniotis - ABARES Outlook 201113

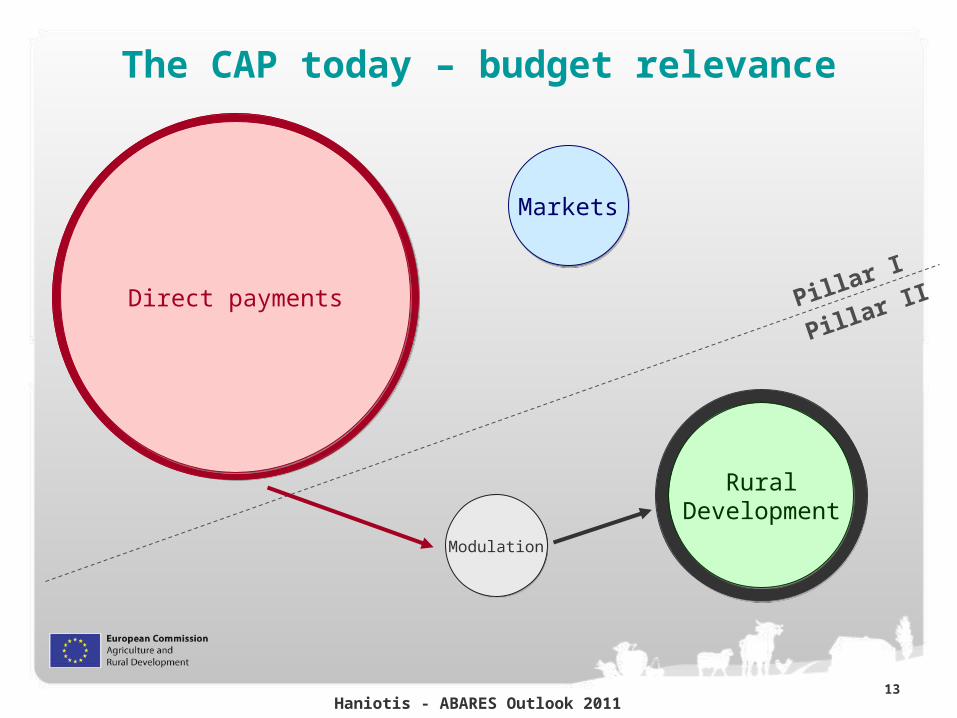

The CAP today – budget relevance

RuralDevelopment

Direct payments

Markets

Pillar I

Pillar II

Modulation

Haniotis - ABARES Outlook 201114

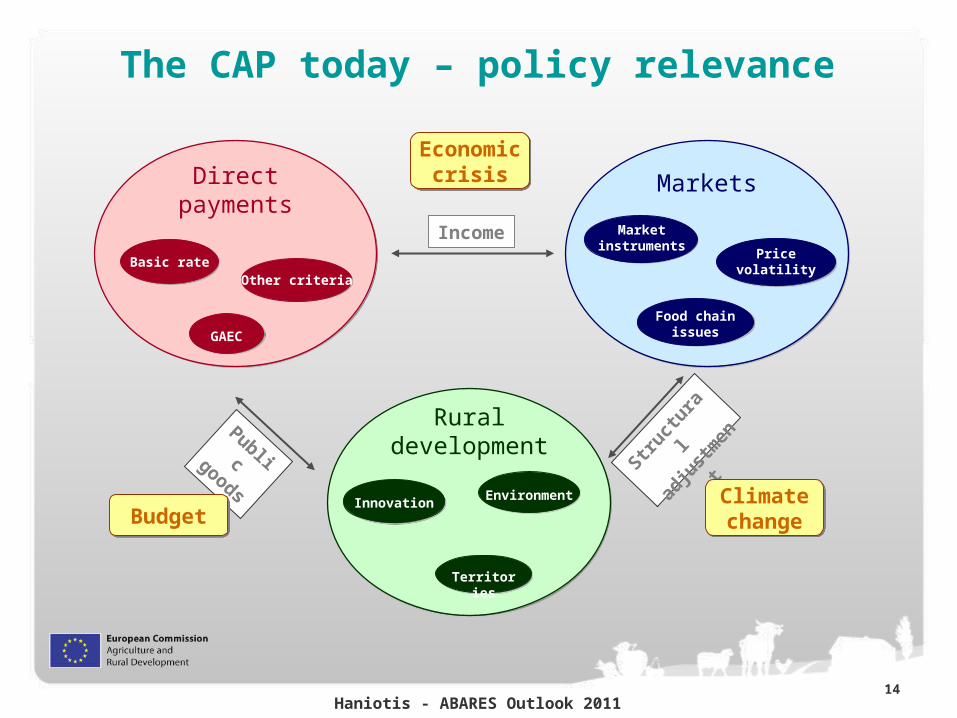

The CAP today – policy relevance

Directpayments

Basic rate

Markets

Ruraldevelopment

InnovationEnvironment

Territories

Income

Public goods

Struct

ural

adju

stm

ent

Pricevolatility

Marketinstruments

Food chainissues

Other criteria

GAEC

BudgetBudget

Economiccrisis

Economiccrisis

ClimatechangeClimatechange

Haniotis - ABARES Outlook 201115

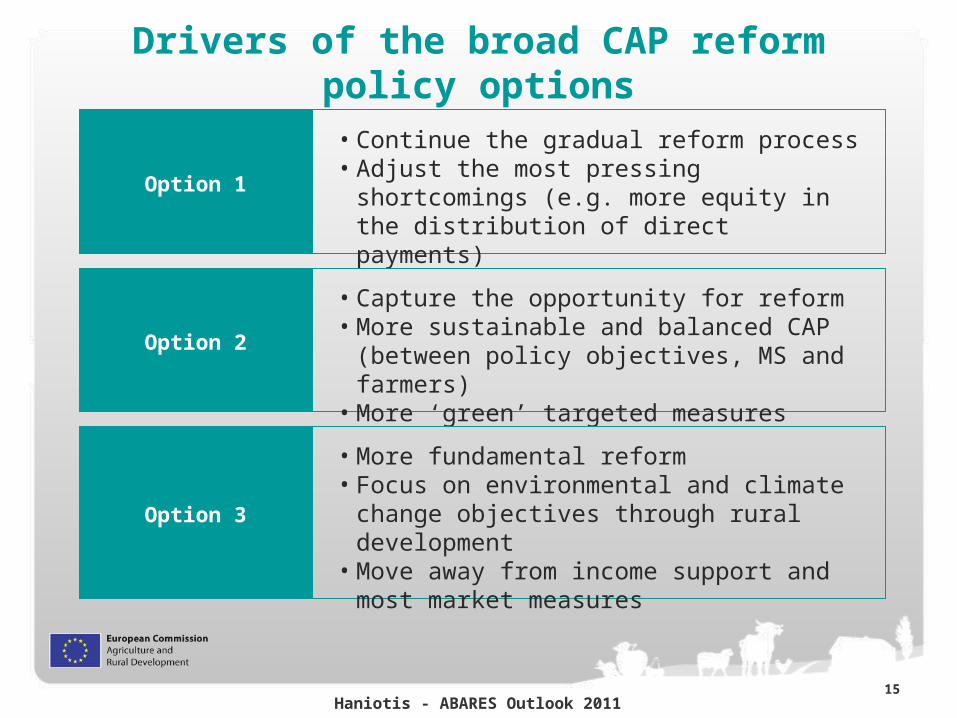

Drivers of the broad CAP reform policy options

Option 1

• Continue the gradual reform process• Adjust the most pressing shortcomings (e.g.

more equity in the distribution of direct payments)

Option 2

• Capture the opportunity for reform• More sustainable and balanced CAP (between

policy objectives, MS and farmers)• More ‘green’ targeted measures

Option 3

• More fundamental reform• Focus on environmental and climate change

objectives through rural development• Move away from income support and most

market measures

Haniotis - ABARES Outlook 201116

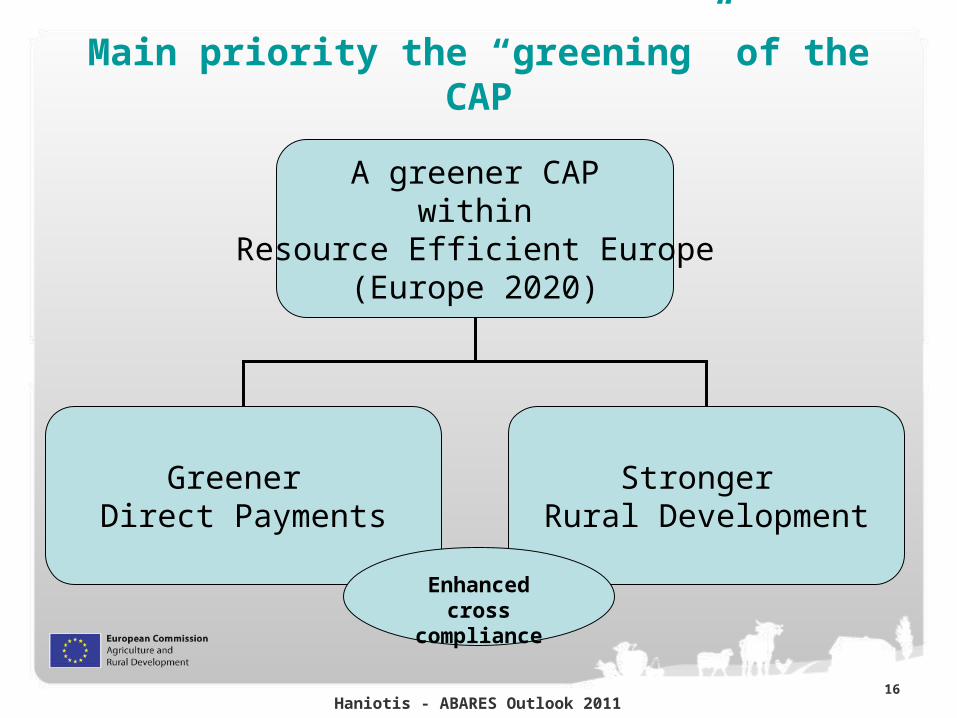

Main priority the “greening” of the CAP

A greener CAPwithin

Resource Efficient Europe(Europe 2020)

Greener Direct Payments

Stronger Rural Development

Enhancedcross compliance

Haniotis - ABARES Outlook 201117

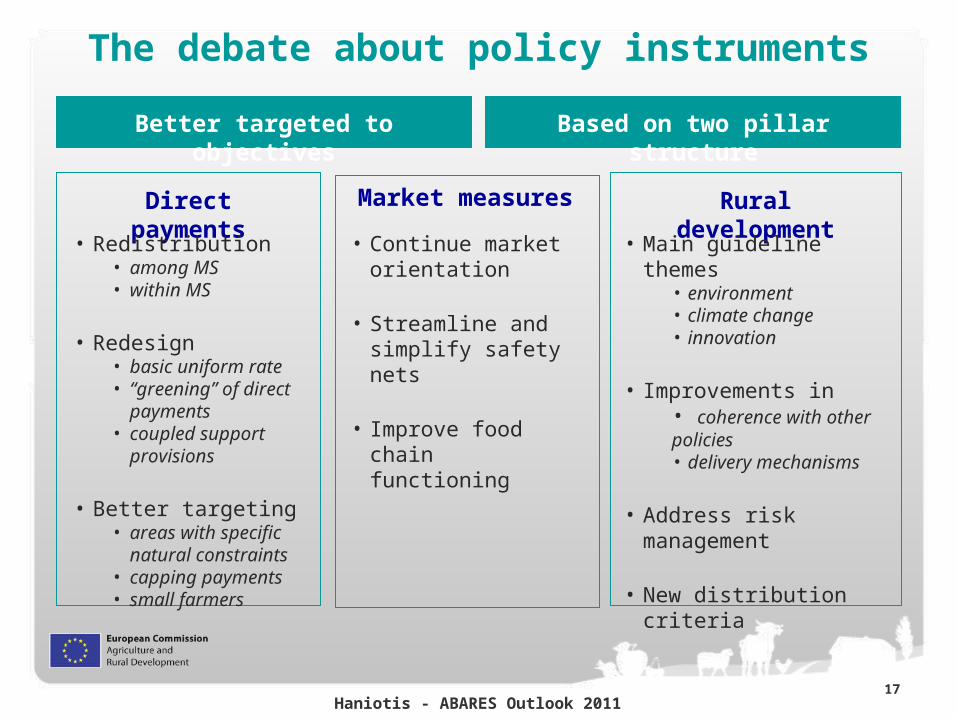

The debate about policy instruments

Better targeted to objectives Based on two pillar structure

Direct payments Market measures Rural development

• Continue market orientation

• Streamline and simplify safety nets

• Improve food chain functioning

• Main guideline themes• environment• climate change• innovation

• Improvements in• coherence with other policies• delivery mechanisms

• Address risk management

• New distribution criteria

• Redistribution• among MS• within MS

• Redesign• basic uniform rate• “greening” of direct

payments• coupled support

provisions

• Better targeting• areas with specific

natural constraints• capping payments• small farmers

Haniotis - ABARES Outlook 201118

Average direct payments per potentially eligible area and beneficiary

Direct payments net ceilings fully phased-in (in 2016)

Source: European Commission - DG Agriculture and Rural Development

0

100

200

300

400

500

600

700

800

Mal

ta

Bel

gium

Net

herla

nds

Italy

Gre

ece

Cyp

rus

Den

mar

k

Slo

veni

a

Ger

man

y

Fra

nce

EU

-15

Luxe

mbo

urg

EU

-27

Irel

and

Aus

tria

Hun

gary

Cze

ch R

epub

lic

Spa

in

Fin

land

Sw

eden

Uni

ted

Kin

gdom

Bul

garia

Pol

and

EU

-12

Slo

vaki

a

Rom

ania

Por

tuga

l

Lith

uani

a

Est

onia

Latv

ia

EUR/ben.EUR/ha

0

8000

16000

24000

32000

40000

48000

DP net ceilings fully phased-in (EUR/ha)EU-27 average (EUR/ha)DP net ceilings fully phased-in (EUR/beneficiary)

Haniotis - ABARES Outlook 201119

Next steps

Inter-institutional debate on the Commission Communication

Preparation of Impact Assessment (IA)Preparation of Impact Assessment (IA)

Preparation of Legal Proposals

• In-depth Commission analysis of new policy settings, options and their In-depth Commission analysis of new policy settings, options and their economic, social, environmental and administrative impactseconomic, social, environmental and administrative impacts

• Stakeholders consultation: analytical contributions from stakeholders Stakeholders consultation: analytical contributions from stakeholders based on a Consultation documentbased on a Consultation document

Legal proposals presented in 2011

Haniotis - ABARES Outlook 201120

Thank you

http://ec.europa.eu/agriculture/cap-post-2013