Embed Size (px)

Citation preview

Restriction of Publication of Part Claimed

-,mission in su ort of the Application .:fir Authorisation

U L Venture [Public version]

9 July 2009

Contents

Executive summary

1 The Applicants

1 . Virgin Blue Group

1.2 Delta

Virgin Blue 1 Delta Joint Venture

2.1 Interline, Codeshare and Marketing Agreements

2.2 Joint Venture

2.3 Term

3 Overview of carrier cooperation arrangements

3.1 'Marketing Alliances" and 'Integrated Alliances"

3.2 Codesharing

3.3 Interline agreements

3.4 Integrated alliances vs. codesharing

4 Industry Overview - the supply of Trans-Pacific air services

4.1 Overview

4.2 Regulatory Framework

4.3 Australia - United States Open Skies Agreement

4.4 Trans-Pacific routes

4.5 Historic trends in relation to the supply of passenger services on Trans-Pacific routes

4.6 The need for effective beyond-networks for caniers operating on Trans-Pacific routes

4.7 The supply of freightlcargo services

5 Caniers currently providing Trans-Pacific air passenger services

5.1 Qantas

5.2 United Airlines

5.3 Air New Zealand

5.4 Other carriers

6 Framework for analysis of competitive effect and public benefits arising from the Virgin Blue I Delta Joint Venture

. . . . . . . - . - . . -. . . . . . . . . . , - . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 2 ~ 8 6 2 s - 1 . d ~

Page

1

6

6

6

7

7

7

8

8

8

9

10

10

12

12

12

13

15

6.1 Market definition

6.2 Market concentration 9 Australia - United States Air Passenger Market 29

6.3 Market concentration 9 Australia - United States Air Freight Market 32

7 The future with and without the Virgin Blue 1 Delta Joint Venture

7.1 The factual

7.2 The counterfactual

8 Public Benefits arising from the Virgin Blue I Delta Joint Venture 34

8.1 Routes and frequencies

8.2 Greater choice and convenience for customers

8.3 Lower fares

8.4 Sustained effective price and product competition on Trans-Pacific routes 37

8.5 Increased tourism

8.6 Additional employment

9 The Virgin Blue 1 Delta Joint Venture will not result in anti- competitive detriment

Annexure A - Virgin Blue Group

. Annexure B - Delta Los Angeles Netwok P

Confidential Annexure C - Overview of Virgin Blue 1 Delta Joint Venture

Annexure D - Summary of passenger traffic rights involving the United States route in Australia's air services agreements 48

Annexure E - Summary of major carriers operating Trans-Pacific Routes (excluding Hawaii) (1 991 .) present) 49

Annexure F - Overview of oneworld carriers 9 Qantas and American Airlines

Annexure G - Overview of Star Alliance Carriers 9 United Airlines I Air New Zealand I Air Canada

Annexure H - Overview of other carriers

Annexure I - Executed copies of agreements

. . . . . . . . . . . . .. . . . . .. . . . . -. . . . . . . . .

Gilbert + Tobin ~ - 1 . d o o

Executive summary

Application This submission is made by Virgin Blue Airlines Pty Ltd (ACN 125 580 823), Virgin for Blue International Airlines Pty Ltd (ACN 125 580 823), Pacific Blue Airlines (Aust) Pty

Authorisation Ltd (ACN 097 892 389) and Pacitic Blue Airlines (NZ) Ltd (together Virgin Blue) and Delta Air Lines, Inc (Delta) (together the Applicants) in support of applications for authorisation pursuant to s 88(1) of the Trade Practices Act 1974 (TPA), to give effect to the Coordination Agreement, the Cooperation Agreement and Joint Venture Agreement (together the Virgin Blue I Delta Joint Venture).

For the reasons set out in this submission, the Applicants consider that the Virgin Blue / Delta Joint Venture meets the net public benefit test imposed under the TPA and should be authorised by the Australian Competition and Consumer Commission (ACCC).

Overview of Through the Virgin Blue / Delta Joint Venture, the Applicants are seeking to establish Virgin Blue I a deep commercial relationship in order to provide customers with a broad and c e

Delta Joint ordinated Trans-Pacific air passenger network (Trans-Pacific routes being those Venture between Australia and mainland United States). Such a network would enable the

Applicants to more effectively compete with the incumbent carriers on the Trans- Pacific routes (being Qantas with its oneworld partner American Airlines and United Airlines with its Star Alliance partners -Air New Zealand and Air Canada).

Subject to regulatory approval, the Virgin Blue / Delta Joint Venture contemplates coordination and agreement between the Applicants in respect of Trans-Pacific routes in relation to:

I schedules, capacity and routes flown;

passenger sales and marketing activities;

I pricing and revenue management;

I enhancement of frequent flyer and lounge program offerings; and

purchasing and procurement.

It also contemplates the pooling of revenue under arrangements founded on the principle of 'metal neutrality". This means the Applicants will adopt revenue allocation arrangements that make it irrelevant, from the perspective of either Applicant, which Applicant's aircraft a passenger travels on.

Background On 14 February 2008, Australia and the United States concluded the Open Skies to the Agreement. This permits airlines of both Australia and the United States to operate

Virgin Blue I unrestricted capacity on routes between any point or points in either country. Delta Joint

Venture Prior to entry into the Open Skies Agreement, new airline entrants between Australia and the United States were only guaranteed a start-up of four services a week. This made it very difficult for new airlines to commence operations on a commercial basis and compete effectively with incumbent airlines, such as Qantas, which were operating many more sewices than this. Moreover, camers from each country were restricted in the markets which they could serve between and beyond the temtory of the other country with local traffic rights. The Open Skies Agreement removed all these routing and capacity restrictions.

A key policy rationale behind the introduction of the Open Skies Agreement was the Australian Government's desire to introduce fur&her and sustained competition on what it considers to be 'one of Australia's most important air routes", particularly by

Gilbert + Tobin zew82s-l.doc PeSeII

enabling new entrants such as V Australia to operate. At the time the Open Skies Agreement was concluded, the only airlines operating direct services between Australia and the mainland United States, in what has often been described as a "virtual duopoly", were Qantas and United Airlines.

The lack of effective competition to the incumbent carriers on these routes was widely acknowledged to have led to higher fare levels, restricted seat availability, a concentration of direct services originating or terminating in Sydney and a corresponding negative impact on tourism and employment growth.

As a result of the Open Skies Agreement, the Virgin Blue Group launched its new longhaul international carrier V Australia. It commenced direct services between Sydney and Los Angeles on 27 February 2009 (now daily) and direct services between Brisbane and Los Angeles on 8 April 2009 (now 3 times a week). V Australia is scheduled to commence direct sewices between Melbourne and Los Angeles in September 2009. Delta also commenced daily services between Los Angeles and Sydney on 1 July 2009 as a result of the Open Skies Agreement.

Historic The Applicants, as new entrants, face a particularly difficult set of challenges in background developing and sustaining a durable network of competitive services on Trans-Pacific

to Trans- routes. These difficulties are exacerbated by the current volatile economic conditions. Pacific route They indude:

= the geography involved on Trans-Pacific routes, which necessitates the use of specialised long range and large gauge aircraft (not easily redeployed on other routes). It also means there is a limited set of city-pairs and an absence of intermediate points;

the need for access to effective beyond networks at either end of Trans-Pacific routes. These beyond networks are required in order to attract customers and feed traffic onto Trans-Pacific services (for example, the Applicants estimate that 60% of Sydney-Los Angeles traffic travels beyond Los Angeles). They are also necessary to maximise passenger load and to enable an airline to effectively respond to any changes in directional passenger flows driven by external factors such as exchange rates; and

the strong position of the incumbent carriers servicing Trans-Pacific routes being:

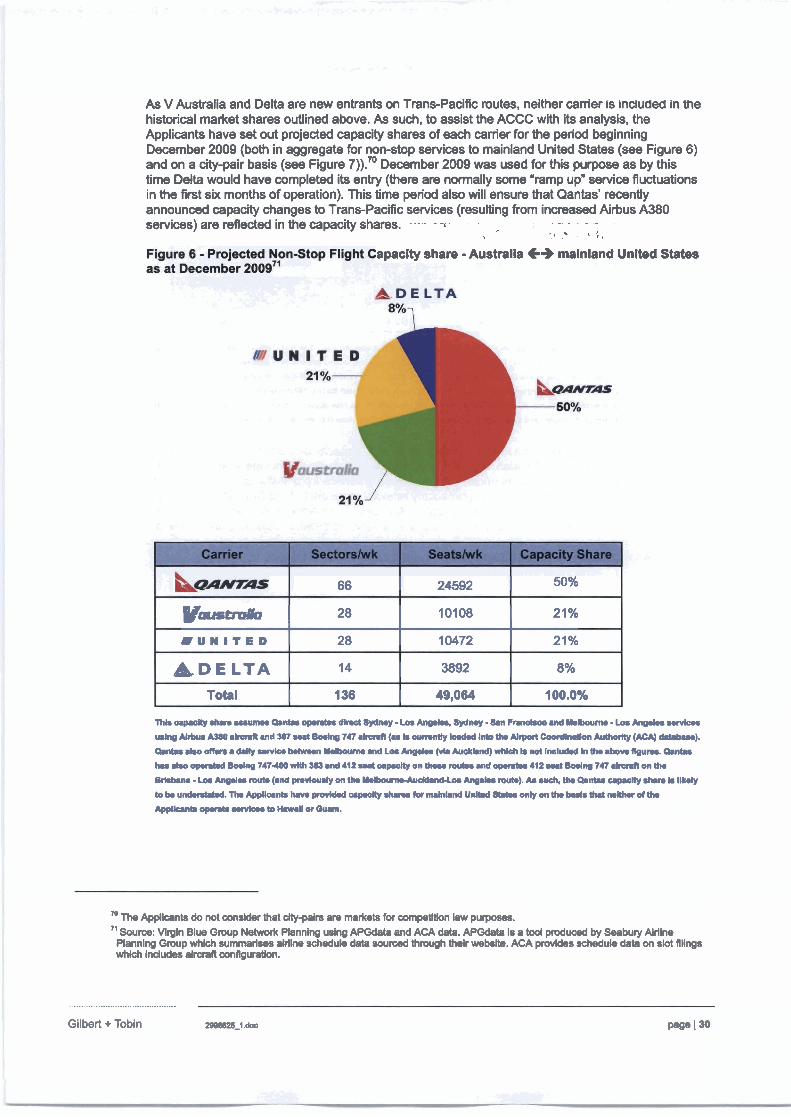

- Qantas, which has developed an unparalleled market presence on Trans-Pacific routes. It has a deep schedule and extensive network of city-pairs in Australia and the United States, fed by its codesharing and oneworld alliance partner American Airlines. This enables it to strongly respond to any new Trans-Pacific entrants. Qantas cartied 53.9% of all passengers between Australia and the United States in 2008. Based on projections for December 2009 Qantas will represent 50% of seat capacity on non-stap flights between Australia and mainland United States.

The dose relationship between Qantas and American Airlines has given Qantas deep penetration on Trans-Pacific routes and has been a key factor in Qantas' success - giving it an ability to sell a broad range of city-pairs, increase its load factors, achieve and maintain its current scale (in terms of routes and frequencies); and

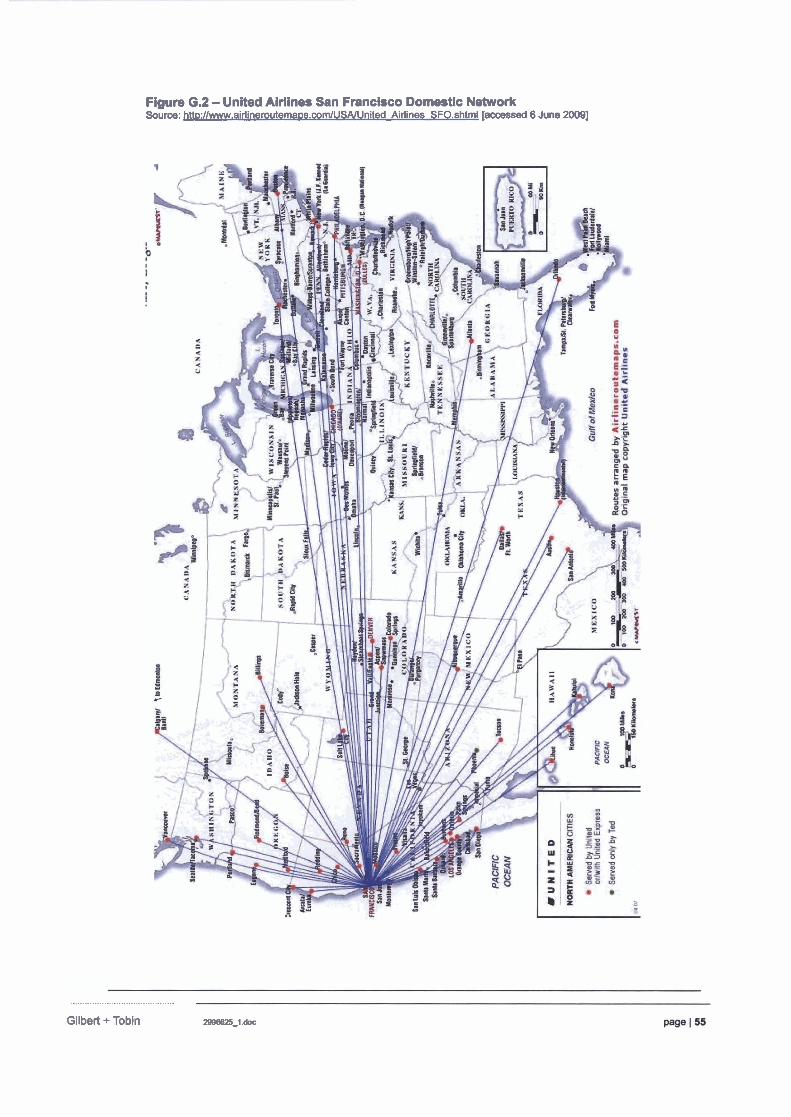

- United Airlines, which has its own extensive United States domestic network meaning it can offer the largest number of connection options for customers flying from Australia. It operates the largest number of domestic US flights at both Los Angeles and San Francisco airports which are the two key hubs on the US west coast for Trans-Pacific

Gilbert + Tobin 2eamzs-1 .do0 paae 12

flights. United Airlines carried 15.6% of all passengers between Australia and the United States in 2008. Based on projections for December 2009, United Airlines will represent 21 % of seat capacity on non-stop flights between Australia and mainland United States

United Airlines has an enhanced Transpacific presence through cooperation with its Star Alliance partners -Air New Zealand and Air Canada. United Airlines codeshares on Air New Zealand's flights from Auckland to Sydney, Brisbane and Melbourne and on Air New Zealand's beyond flights to Los Angeles and San Francisco. Similarly, Air New Zealand codeshares on United's Sydney to San Francisco and Sydney to Los Angeles services. Additionally Air New Zealand and United Airlines have been granted broad antitrust immunity by the United States Department of Transportation enabling them to coordinate all international services, induding between United States and New Zealand and the South Pacific region.

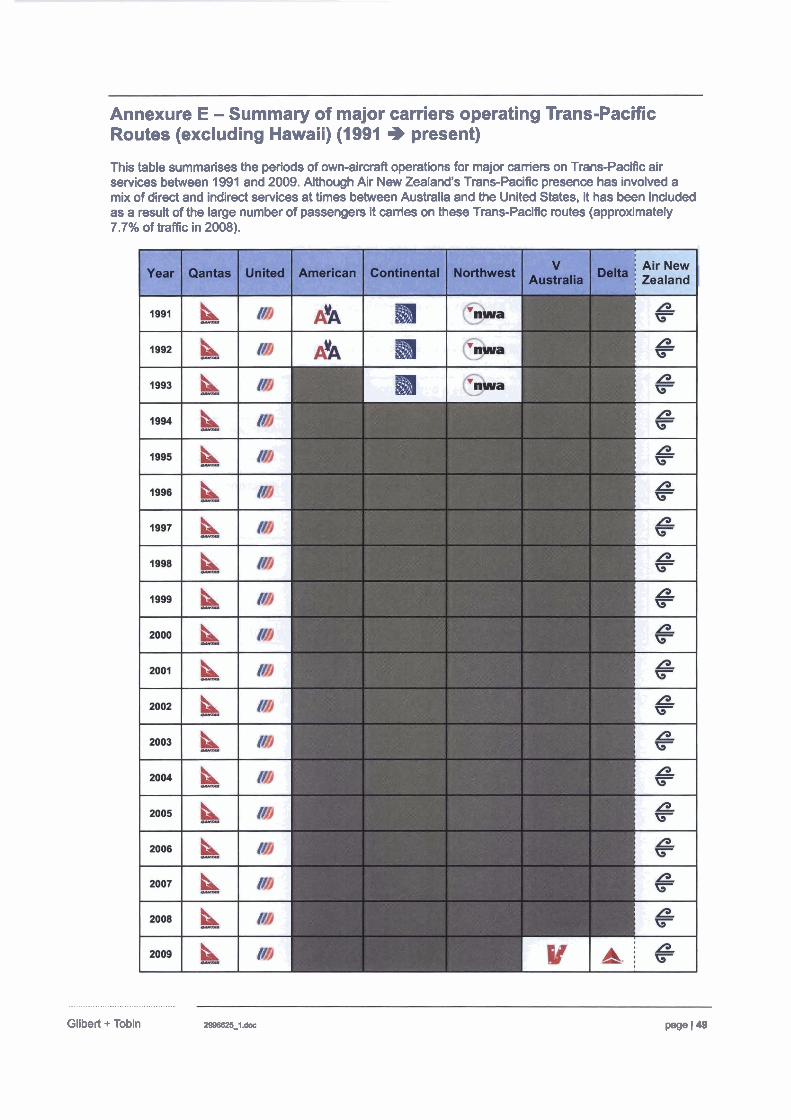

The diiculty of competing effectively on Transpacific routes can be seen from the fact that three major United States airlines have withdrawn from the route since 1991, whilst Air New Zealand also commenced and ceased its own direct services between Australia and the United States over this period.

Rationale for The overriding policy objective which led to the Open Skies Agreement was a desire the Virgin to introduce further and sustained competition on Trans-Pacific routes (with

Blue I Delta corresponding increases in services and routes and reductions in airfares). Joint Venture

Whilst the Applicants consider their entry has gone a considerable way to promoting this objective, in light of the difficulties outlined above the Applicants consider that the Virgin Blue I Delta Joint Venture best achieves the key objective of the Open Skies Agreement. It does this through better positioning the Applicants to:

maintain existing routes and services and develop new routes, schedules and frequencies whilst optimising use of the carriers' aircraft and facilities (both existing and new), creating operating efficiencies and increasing consumer choice and benefits;

achieve operational and overhead cost savings and drive increased passenger numbers in a way that cannot be achieved under codesharing and interlining agreements;

optimise their existing networks and activities to feed traffic onto new routes and thereby reduce the commercial risk in the establishment of such new routes. It will therefore increase the likelihood of such routes being established as well as the speed of their establishment; and

more effectively develop a deeper, coordinated and integrated Trans-Pacific passenger network to better rival and more effectively and comprehensively compete with the incumbent airlines in the market on a long term basis.

As a result it will give passengers a greater degree of flexibility in terms of city-pairs, anival and departure times and beyond connection options.

In turn, it drives the public benefits outlined below.

"Metal As noted above, the Virgin Blue 1 Delta Joint Venture is intended to be a 'metal Neutral" neutral" joint venture - that is, based on the pooling of revenue in such a way that it is

Joint irrelevant to the Applicants which Applicant's aircraft a passenger travels on. In order Ventures to achieve this 'metal neutrality", the Applicants need to jointly coordinate scheduling,

yield management, inventory allocation, pricing and network planning to ensure that

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . , . . .

Gilbert + Tobin zseem-l.doc pasel3

schedules, prices and availability across the joint network are set efficiently.

The Applicants consider that such an integrated alliance is necessary to achieve the objectives of the Virgin Blue 1 Delta Joint Venture and the public benefits that flow from them - that is, the same result cannot be achieved solely with standard forms of airline cooperation (such as codesharing).

In codesharing and other standard arrangements, parties continue to have an incentive to maximise their own economic benefit. They are therefore unwilling to reduce the profitability of their own operations and will seek to individually profit maximise within the scope of the codeshare. They will develop a network that is optimal for each individual airline rather than for their pooled capacity, often resulting in a concentration of routes or timings as each partner seeks the same 'sweet spotn in the market. They also will price the seats they operate themselves to induce passengers to buy these, rather than seats the airline buys on codeshared services operated by its partner (with each airline seeking a profit margin on the same seat), even if the partner offers better routing or timing.

Under a 'metal neutral" integrated alliance, where the airlines share the revenue, the airlines have an incentive to focus on maximising the benefits for the alliance parties as a whole. The revenue of each carrier will be the same regardless of which alliance carrier actually transports the passenger. As such, the carriers will seek to win the passenger's booking for the alliance by creating a joint network with the best spread of routes, frequencies and the most competitive fares. The alignment of financial incentives in this manner drives the carriers to grow and to optimise their product offering. Such an alliance eliminates 'double marginalisation", enables more efficient codesharing and convenient scheduling. It also enables the carriers to jointly introduce new routes and services that would not be sustainable as a product for each individual carrier. Their joint network thus has a greater scope and more convenience than their individual timetables.

The economic and consumer benefits that flow from these alliances include the offering of a better optimised network with a better spread of routes and timings; considerable increases in passenger loads, which lowers fares by lowering the cost per seat sold; and further lowering of fares through the removal of the 'double marginalisation" incentive. The presence of a more comprehensive, integrated network will provide more effective competition against the dominant incumbents than will two more marginal separate networks with simple codeshare connections.

The Applicants consider that Qantas and American Airlines have effectively achieved a key benefit of a 'metal neutral" integrated alliance by having Qantas operate all Trans-Pacific sectors whilst American Airlines operate all domestic United States sectors. As Qantas is the sole operator of the critical Trans-Pacific sectors, it controls all scheduling and with regard to pricing, American Airlines is neutral regarding which Trans-Pacific sectors it sells.

Public In enabling the Applicants, both new entrants, to replicate the network advantages of Benefits the incumbent carriers to effectively compete and grow their presence on the Trans-

Pacific routes in a way not facilitated by codeshare, the Virgin Blue I Delta Joint Venture promotes the public policy objectives underpinning the Open Skies Agreement. More specifically, the Applicants will be better able to maintain existing and introduce further Trans-Pacific services (routes and frequencies) faster than would occur absent the Virgin Blue I Delta Joint Venture. This is particularly true in respect of direct services. This in turn:

means customers travelling between Australia and the United States will be offered greater choice and convenience;

- facilitates lower fares on the Trans-Pacific (as a result of new capacity

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin m - 1 h e paae 14

supported by the Virgin Blue I Delta Joint Venture, the removal of 'double marginalisation" incentives and the facilitation of cost savings);

results in sustained effective price and product competition on Trans-Pacific routes in the medium to long term; and

will facilitate increased tourism and employment in aviation and other sectors.

No anti- Not only does the proposed Virgin Blue 1 Delta Joint Venture drive the public benefits competitive outlined above, it will not result in any anti-competitive detriment. More specifically:

detriment the Applicants are new entrants on the Trans-Pacific routes. The Virgin Blue I Delta Joint Venture will assist their entry, and continued survival and growth in this market. It therefore has a fundamentally pro-competitive effect on what, until recently, has been a virtual duopoly;

the Applicants have limited incentive and ability to remove capacity from Trans- Pacific routes (either before or after commencement of the Joint Venture). Further, the Joint Venture does not give the applicants the incentive to remove capacity where, even together, the Applicants will still be relatively small in the market;

the purpose of the Virgin Blue 1 Delta Joint Venture is to enable the Applicants to maintain existing capacity as well as to develop new routes, schedules and frequencies in order to more effectively compete against the entrenched incumbent carriers' alliances;

following the commencement of the Virgin Blue I Delta Joint Venture, the Applicants will continue to vigorously compete with Qantas and United Airlines as well as the range of indirect carriers including Air New Zealand and Air Canada. Air New Zealand also retains the ability and capacity to offer direct services between Australia and the United States; and

there are a large number of alternative air freight I cargo providers to the Applicants including Qantas, United Airlines, UPS and FedEx (as well as those carriers that fly via Asia). Additionally, the Applicants are currently small suppliers of air freight I cargo services on Trans-Pacific routes.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 2 ~ 6 ~ - I .do0 -1s

1 - 3-f-lL.6- ,- a , <-:fT ,, ... .. .. .

1 The Applicants ;.; k; ::. . . :,... . ! * , , p., ,. . . , p.-& '. . ., ' , .; . +. , .., 8

1.1 Virgin Blue Group

The Virgin Blue Group (Virgin Blue Group) commenced operations in Australia in August 2000. Since that time, it has grown from having two aircraft ftying one domestic route to having a fleet of 81 aircraft with annual revenues of $2.4 billion in 200849. The Virgin Blue Group is now

.CW comprised of the following domestic and international brands: Virgin Blue, Pacific Blue, Polynesian Blue (a joint venture with the Samoan Gwern~e-no and VvAustraJia. - . --7->-*. ; p u r -9-

\ -.

Virgin Blue is the flagship carrier of the Virgin Blue Group and is based in Brisbane. Marketing itself as a 'New World Carrier" (pitched between a full service carrier and a low-cost carrier), Virgin Blue operates a fleet of 69 Boeing 737-700,737-800 and Embraer El90 and El70 EJet aircraft. Virgin Blue currently operates approximately 2800 flights a week to more-than 25 Australian .-; , -.r-~F?--cTp... ,i.-- 7-->...-2- , , .-- * ,; r -. .,- -

. , . . . .

destinations. . . - . .

Pacific Blue was launched in 2004. It consists of two carriers. Pacific Blue Airlines (NZ) Limited (PBNZ) is the New Zealand-based subsidiary of the Virgin Blue Group and operates domestic services within New Zealand, as well as Trans-Tasman services between Australia and New Zealand. Pacific Blue Airlines (Aust) Pty Ltd (PBA) operates services between Australia and New

:Zealand, Fiji, Bali, Samoa, Vanuatu, Papua New Guinea, the Cook Islands, the Solomon Islands and Tonga as a designated Australian international carrier. PBA operates aircraft wet leased from PBNZ and Virgin Blue. PBNZ has hubs in Christchurch and Auckland. Pacific Blue currently operates a fleet of 9 Boeing 737-800 aircraft. .h -

a* .? ,w h i f , ¶ . - . > , - ! I . : - ---. :Y-- ,<;,.+. . . . , : :,.-- , L

*I I L I C R ~ ~ )UTM??CI .&zA~,! r'.>Jt+=.. ,P>L err* - h i . 1 1 , lr , , . v ui 4

V Australia is the Virgin Blue Group's newest carrier. It commenced flight operations on;-,, 27 February 2009, providing non-stop Sydney - Los Angeles services 3 times a week. C)n 20 March 2009, V Australia introduced daily Sydney - Los Angeles services. In April 2009, V Australia began flying on the Brisbane - Los Angeles route 3 times a week. A third Trans-Pacific route,

,gss between Melbourne and Los Angeles, is scheduled to begin operations in September 2009. V ~:@j Australia is currently operating a fleet of three Boeing 777-300ER aircrafl : +,. %

I

The Virgin Blue Group also has a joint venture with the Samoan Government: Polynesian Blue. Polynesian Blue is a designated carrier of the Government of Samoa. It operates between Sydney. - -

-. ~risbane, Auckland and &ia with a single Boeing 737-800. Polynesian ~ i u e is not a participant in "' ' .l4 the Virgin Blue I Delta Joint Venture.

I . b.\ . , I L&l - .-a .-7 I

A more detailea overview or the Virgin Blue Group's operations, as well as its route network, is set out in Annexure A.

1.2 Delta

\ . Delta Air Lines (Delta) is a United States carrier with hubs in Atlanta, Cincinnati, Detroit, Memphis, Minneapolis-St. Paul, New York (JFK), Salt Lake City, Amsterdam and Tokyo (Narita). Delta, its Northwest Airlines subsidiary, and its Delta Connection regional partners operate a combined

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 2m6625-1 .doc pasel6

network of service to 368 destinations in 66 countries and serve more than 170 million passengers each year. Delta, Northwest and Delta's wholly owned regional caniers operate a combined fleet of more than 1,000 aircraft, ranging in size from the 403-seat Boeing 747-400 to the 34-seat Saab 340.

Delta began non-stop services on the Sydney - Los Angeles route on 1 July 2009 operating Boeing 777-200LR aircraft. These aircraft are relatively new to Delta's fleet.

Delta is the fourth largest operator of domestic services from Los Angeles after United Airlines, American Airlines and Southwest Airlines respectively.

A route map of connections available from Delta's Los Angeles hub is set out in Annexure 6.

2 Virgin Blue 1 Delta Joint Venture

The Applicants are seeking to establish a broad commercial relationship in order to provide customers with a m-ordinated Trans-Pacific air passenger network. '

2.1 Interline, Codeshare and Marketing Agreements

The Applicants have entered into a joint codeshare and marketing agreement and have previously completed an interline agreement2

Under the codeshare agreements, subject to relevant regulatory approval:

V Australia will codeshare on Delta's United States domestic network;

Delta will codeshare on Virgin Blue's Australian domestic network and Pacific Blue's network; and

both Delta and V Australia will codeshare on each other's Trans-Pacific services.

The terms of the marketing agreement provide for reciprocal airport lounge access for Delta and Virgin Blue and reciprocal recognition and participation in each other's frequent flyer programs - including the ability to eam and redeem frequent flyer points on each other's network.

2.2 Joint Venture

The Applicants are seeking Authorisation in respect of a deeper joint venture arrangement that will enable them to better develop an integrated and highly competitive Trans-Pacific air passenger network.

The Applicants have therefore entered into a Cooperation Agreement, a Coordination Agreement and a Joint Venture Agreement, together establishing a joint venture between the Applicants (Virgin Blue I Delta Joint Venture).

Subject to regulatory approval, the Virgin Blue 1 Delta Joint Venture contemplates coordination and agreement between the Applicants in respect of Trans-Pacific routes in relation to:

schedules, capacity and routes flown;

' As noted above, Polynesian Blue (the joint venture between the Samoan Government and the Virgin Blue Group) wlll not be DarUdDaUtW in the Vlmin Blue I Delta ldnt venture. ' V &lralG, 'V Au&lb and Delta Airlines sign interline agreement' avallabk at hll~://www.vaustralia.wm.aulabout-uslmedia- reieases/viewedia-release* 008186.hlrnl [accessed 2 July 20091.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 2sw82-l.d~~ -17

passenger sales and marketing activities;

pricing and revenue management;

enhancement of frequent flyer and lounge program offerings; and

purchasing and procurement.

It also contemplates the pooling of revenue under arrangements founded on the principle of 'metal neutrality". This means the Applicants will adopt revenue allocation arrangements that make it irrelevant, from the perspective of either Applicant, which Applicant's aircraft a passenger travels on.

A detailed overview of the terms and governance arrangements of the Virgin Blue 1 Delta Joint Venture is set out in Confidential Annexure C. Copies of the Cooperation Agreement, the Coordination Agreement and the Joint Venture Agreement are set out in Confidential Annexure I.

The Applicants submit that the ACCC should authorise the Virgin Blue 1 Delta Joint Venture for a period of not less than 5 years.

3 Overview of carrier cooperation arrangements

3.1 "Marketing Alliances" and "Integrated Alliances"

A development in international aviation in recent years, as previously acknowledged by the ACCC, has been the 'proliferation of airline alliancesw 3. Of the rationale for these alliances and broader cooperation arrangements, the ACCC noted that they represented:

... an industry response to strong competition, low yields and low ptvfftability [that] enabled airlines to ex nd networks and services whilst controling costs and increasing productivity. P

The ACCC has classified alliances as generally being either a 'marketing alliancew or an 'integrated alliancew.

The ACCC has stated that 'marketing alliances":

. . .omr the consumer the benefits of broader networks, more seamless travel and expanded loyatfy programs. However, alliance airlines generally continue to offer their fares, schedules and services independently and airlines within the same marketing alliance may compete with each other if on the same route.=

In respect of Trans-Pacific routes, the key marketing alliances are oneworld (members of which include Qantas and American ~irlines)' and Star Alliance (members of which include United Airlines, Air Canada and Air New zealand)'. Delta is a member of the SkyTeam alliancea The Virgin Blue Group is not currently a member of a marketing alliance.

' ACCC, Qentas Airnays Limited end Brlblsh Ainveys PYc Applk.eMMs lbreuthorkretion (A30226 end A30227) Final Determination, 8 Febnraty 2005 at [4.42]. ' ibid. ' Id at [4.45].

For informatJon regding maworld see htt~://www.oneworld.co~ ' For information regarding Star Alliance $80 ~tt~://www.s1araiiiance.com/enltraveiie~.htmi

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 2somw-1.h pase 18

The ACCC has stated that 'integrated alliances":

. . .fupicaIly involve a high degree of integration of the airlines concerned, including coordination of fares, schedules, s e ~ c e levels and yield and capaciiy management.'

The proposed Virgin Blue / Delta Joint Venture is properly characterised as an 'integrated alliancen.

Codesharing is the arrangement that allows carriers to use their brand to sell tickets on flights that are operated by a different carrier. The ACCC has noted that codesharing can occur "within both integrated alliances and marketing alliances, as well as outside such

The International Air Transport Association (IATA) assigns each camer a code used to identify it in international schedules. Each flight is designated by the relevant carrier's code followed by a flight number. For example, the codes for V Australia and Delta are VA and DL respectively.

Codesharing allows a single flight to carry the codes and flight numbers of multiple carriers. Although the individual flight is maintained, staffed and scheduled entirely by the carrier that owns and operates the aircraft, the flight is listed on the schedules of multiple carriers under their own codes.

This allows multiple caniers to sell seats on the same flight through their own ticketing system, with each carrier using its own designator code and flight number to refer to the same flight. This can be arranged using blocked space (one carrier pre-purchasing a predetermined number of seats on the other carrier's metal) or freesale (a direct sale of seats on the other carrier's aircraft, with no obligation to pre-purchase any volume of seats) arrangements.

The ACCC has noted that the competitive impact of codesharing:

..will depend upon the nature of both the codeshare payment arrangements and the market in which it occurs. It is fair to say that competition benefits generally will only arise where the codeshare invokes a blocked seat arrangement whereby the purchasing airline effectively commits to purchase a fixed number of seats and therefore has an incentive to market them. When codeshares involve '?be sale" arrangements (where the marketing camer effectively only pays for the seats it sells), there is nonnally no increase in competitive pressure. "

Additionally, the ACCC stated:

Codesharing may add competition, albeit at the margin, on mutes where multiple airline operation is not economically feasible.. .I2

... Generally, where codeshating is used to extend mutes by offering seats on other carriers' flights, there is litfle competitive impact.. .13

. . Codesharing may give rise to competitive benefits if it allows an airline to develop a market to a stage where own aimraft operation is feasible. It may also allow an airline to

For informath regarding the SkyTearn alliance, see htta:lhnrww.skvtearn,wm/ ACCC, Qentas Airways UmHed and Wtish Aimeys Plc Applhthms Ibr autlmifsathm (A30226 and A30227) Final Detemination, 8 FeaUaly 2005 at [4.44].

lo Id at (4.461. " Id at [4.473-(4.50]. lZ Id at [4.48]. '' Id at [4.49].

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin zso6625-1.m~ pase 1 9

maintain a pmsence following withdrawal from an unsustainable market pending possible m-entry at a later stage.14

The Virgin Blue I Delta codeshare outlined in section 2.1 is a freesale codeshare.

3.3 Interline agreements

lnterline agreements are arrangements between caniers designed to facilitate passengers travelling on itineraries that involve multiple carriers. Interlining operates through the reservation or ticketing system of the carriers in the agreement. Where codesharing involves applying multiple codes to a given flight, interline agreements allow a customer to purchase separate flights from multiple carriers in one transaction and with one ticket. One canier (the plating carrier) receives all the revenue and is responsible for redistributing it proportionally among the other caniers in the itinerary.

As noted above, the Virgin Blue has already entered into an interline agreement with Delta. Virgin Blue also has interline agreements with Alaska Airlines and Virgin ~merica."

3.4 Integrated alllances vs. codesharing

The benefits flowing to customers of an integrated alliance, such as the proposed 'metal neutral" Virgin Blue I Delta Joint Venture, are substantially greater than under more standard forms of carrier cooperation (such as codesharing).

In codesharing and other standard arrangements, parties continue to have an incentive to maximise their own economic benefit. They are therefore unwilling to reduce the profitability of their own operations and will seek to individually profit maximise within the scope of the codeshare through:

operating on the routes and with the frequencies that each carrier perceives to provide the greatest potential for profit, such that codeshare partners will often end up competing head- to-head (in some cases, flying Wng-tip to wing-tip"). A party to a codeshare agreement is unlikely to unilaterally cede a particular timing or route to their codeshare partner in order to offer a different time of day or city of departure where it considers it is giving up a potentially more profitable service. This results in a continuation of wing-tip flying end therefore continuing loss of potential scheduling efficiencies; and

- channelling passengers onto their own aircraft regardless of whether their codeshare partner may offer a better routing or more convenient timing, because their profit margin is higher.

In addition, they will also ordinarily seek a profit margin on the passengers they put on their respective codeshare partner's aircraft, which in turn will be seeking a profit on the seat they are selling to the booking carrier (termed 'double marginalisation"). The effect of this "double marginalisatiin" is to increase fares compared with the position under an integrated 'metal neutral" alliance.

As an illustration, consider a United States passenger seeking to fly from Los Angeles to Brisbane under a standard codeshare arrangement involving Delta and Virgin Blue (absent a revenue sharing arrangement). When booking this passenger, Delta would have an incentive to accommodate them on its own non-stop Sydney flight, with a subsequent intra-Australia connection operated by Virgin Blue canying the Delta code. This is because Delta maximises its

'' Virgin Blue and Vlrgin America signed the interbe agreement on 3 June 2009. The Interline agreement became fully operational on 8 June 2009. VWn America is a rekthrely new carrier In the United St-, having launched in August 2007. Vhgln America flies to San Frandsco, L a Angeles, New York, Washington D.C., Seattle, La8 Vegecl, San Dlego, Bcyston and Orange County.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 2s~mu-1 .doc FWeI 10

share of the profit from the transport of the passenger by canying them itself. 'Buying" a seat from Virgin Blue on the direct Los Angeles-Brisbane flight will generally be less profitable for Delta than providing the seat on its own service and the short connecting flight because Virgin Blue will be seeking a profit on the sale of the seats.

The better and more efficient routing would be to fly the passenger under the Delta code on V Australia's non-stop Los Angeles-Brisbane service. To give Delta the incentive to do this (by attractively pricing its codeshared Los Angeles-Brisbane service), it needs to achieve the same profit as it would by canying that passenger over Sydney on its own aircraft (or 'metal"). Revenue sharing and co-ordinated pricing achieve this so-called 'metal neutral" state of affairs.

Under a 'metal neutral" integrated alliance, where the airlines share the revenue, the airlines have an incentive to focus on maximising the benefits for the alliance parties as a whole. The revenue of each carrier will be the same regardless of which alliance carrier actually transports the passenger. As such, the carriers will seek to win the passenger's booking for the alliance by creating a joint network with the best spread of routes, frequencies and the most competitive fares. With the alignment of financial incentives, caniers that are part of the 'integrated alliance" will drive to grow and optimise the convenience and scope of their overall product offering such that they:

avoid 'double marginalisation" by jointly pricing a fare without separate profit mark ups;

efficiently codeshare without pricing or other restriction^;'^

agree on schedules that increase passenger convenience by adding flights or shifting flights to provide broader time of day coverage;

- route customers between city-pairs via the most efficient routing regardless of which carrier ultimately operates the flights; and

seek to jointly introduce new routes and services that they may not be able to launch unilaterally so as to expand the scope and breadth of their joint network to the benefit of consumers.

Importantly, in order to achieve these outcomes it is necessary for caniers to jointly coordinate scheduling, yield management, inventory allocation, pricing and network planning to ensure that schedules, prices and availability across the joint network are set efficiently.

The overall result in the integrated alliance (not achieved under a standard codeshare) is the optimisation of the joint network offering such that it is more attractive to potential customers and more competitive - leading to overall increased passenger loads across the network and subsequently lower average seat costs.

In generating the incentives and outcomes outlined above, 'integrated alliances" facilitate key economic and consumer benefits:

first, as already outlined above, it enables carriers to offer lower fares overall as a result of the absence of 'double marginalisation" incentives. In this respect, the elimination of double- marginalisation has been shown to lead to fare decreases of approximately 16%.17

second, it enables the carriers to offer a more comprehensive joint network with better spread of routes and frequencies that services the broader market rather than both aiming

" The United States Government Accountability Office noted the practical difficulties involved in network-wide codeshare arrangements stating Ulithout Immunity, airlines that are slgnMcant competilors cannot discuss pricing hues and must develop prorate agreements in 'arms-length' negotiations to divide revenues, a cumbersome process when thousands of dty-pain are involve&. (United States Government Accountability O h , GAO Repott, April lSW, OAOIRCED-9599 at page 29). " J.K. B~erJcner, 'International Airfares in the Age of Alliances: The Effects of CodeShatlng and Antitrust Immunity' in Review of Ecanatnics mi Stalistics (2003) 85 at pages 1061 18.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . , .

Gilbert + Tobin 2 ~ 8 6 ~ - 1 . m ~ PWWIl l

for the same 'sweet-spot" resulting in wingtip-to-wingtip flying. The more comprehensive network also facilitates recovery when operations are disrupted by operational issues (such as weather or technical issues); and

third, considerable increases in passenger loads and incremental revenue per available seat kilometre are delivered under an 'integrated alliance" as opposed to standard codeshare arrangements. These increased loads are facilitated by the existence of aligned commercial incentives and the consequent lower fares, optimally planned network (in terms of routes and frequencies) and the increased customer convenience. In general, the Applicants consider the improvements in terms of incremental passenger loads and incremental revenue per available seat kilometre are substantial and are the greatest under an 'integrated alliance" (such the Virgin Blue 1 Delta Joint Venture).

The net effect of the 'integrated alliance" as opposed to standard codeshare arrangements is that with higher passenger loads and revenues, as well an ability to share risk, carriers are better positioned to maintain services (in the face of volatile economic times) as well as to develop new routes and enhance their joint network schedules and frequencies. Moreover, the increased loads lower the cost per occupied seat, and competitive forces will place downward pressure on prices so the benefits are shared between the carriers and consumers.

- - -- -

4 Industry Overview - the supply of Trans-Pacific air services

The Applicants participate in the airline industry, providing international and domestic air services for the public transport of passengers and freight by aircraft.

Relevantly, the Applicants are involved in the provision of air services between Australia and the United States (following the launch of sales for flights by Delta on 1 July 2009). Both Applicants also operate extensive domestic networks in their home countries and service a range of other international routes.

Whilst both carriers carry freightlcargo in addition to passengers, neither carrier is currently a significant carrier of freiclhtlcargo on the Trans-Pacific route.

As is discussed further in the following section, both V Australia and Delta have only commenced services on the Trans-Pacific route since the conclusion of the Open Skies Air Services Agreement between Australia and the United States (Open Skies ~greement)."

4.2 Regulatory Framework

International aviation is subject to several layers of regulation. The basic regulatory system was established by the 1944 Convention on International Civil Aviation (the Chicago Convention) and the 1945 International Air Sewices Transit Agreement (IASTA). The basis of this framework is that individual countries have absolute sovereignty over their airspace. IASTA, however, provides for basic reciprocal rights between all of its 118 signatories. These basic rights are limited to:

flying over the sovereign territory of another signatory; and

landing in the sovereign territory of another signatory, provided it is for non-traffic purposes (i.e. does not involve picking up or dropping off passengers or freightlcargo).

However, this basic regulatory system clearly does not provide a sufficient level of access to operate an international airline.

'' Air Transport Agmement between the Government of the Unlted States of Americe and the Government of Australia. 1944.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 2~6025-1 do^ m e 1 12

International aviation is primarily regulated through intergovernmental bilateral air services agreements. These agreements determine the terms and conditions under which respective national carriers can access routes which terminate or begin in the countries concerned. There are currently more than 3,000 aviation treaties worldwide, which represent more than 900,000 city-pair combinations. This network of treaties constitutes the practical regulatory framework for the international air services network.

International air services treaties are complex trade agreements and involve a number of national interest considerations. As a consequence, access to markets is conditional. In general, bilateral agreements are premised on reciprocal rights. They generally grant the same rights to national carriers from both participating countries in respect of international travel between (or occasionally in) the two countries.

An open skies arrangement is a form of air services arrangement between countries, usually in a bilateral format. Although there is no formal definition of an open skies arrangement, it generally involves the removal of air traffic and market access restrictions.

4.3 Australia - United States Open Skies Agreement

On 14 February 2008, Australia and the United States concluded the Open Skies Agreement. This permits carriers of both Australia and the United States to operate unrestricted capacity on routes between any point or points in either country." Atthough the points to be served are theoretically unlimited, as a practical matter the initial point of entry in each country must be an international gateway (implying that not all points are open for access). Any Australian or United States carrier can now, should they desire, operate services between Australia and the United States, provided they are a propriately licensed and are effectively controlled and substantially owned by their nationals. #

Prior to entry into the Open Skies Agreement, new airline entrants between Australia and the United States were only guaranteed a start-up of four services a week. This made it very difficult for new airlines to commence operations on a commercial basis and compete effectively with incumbent airlines, such as Qantas, which were operating many more services than this. Moreover, carriers from each side were restricted in the markets which they could serve between and beyond the territory of the other country with local traffic rights. The Open Skies Agreement removed all these routing and capacity re~trictions.~'

Under the Open Skies Agreement, the carriage of ~ a b o t a g e ~ ~ traffic is not permitted.23 Consequently, the carriage of traffic over domestic sectors is reserved for national carriers. While the treaty permits the beyond-carriage of genuine international traffic between international gateways (for example Qantas' own traffic between Los Angeles and New York) there are few points which can support extra sector operation^.^^ Consequently, commercially viable access to beyond gateway markets effectively remains dependent on robust and expansive commercial arrangements with domestic carriers (for example, the strong relationships between Qantas and American Airlines or United Airlines and Air New Zealand).

Is Id at Article 3. " Id at Article 3, section 2(a). " Id at Article 3. 27. Cabotage is a Right between two points within a foreign country, canying residents whose travel begins and ends in that country. The relevant definition in the Chicago Convention is that "[]a& state shall have the right to refuse permission to the airaaft of other contracting states to take on Its temHory passengers, mail, and cargo destined for another point within L territory.' This prevents, for example, an American canier from operating a domestic service behveen Sydney and Melbourne. Air Transport Agreement between the Gomment of the United Slates of America and the Government ofAustmlla, 1944,

Aliide 2. Air Tmnsport Agreement behvgen the Government of the United States of America and the Government of AustmIia, 1944,

Annex I, secbion 1.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin ~ - 1 . d 0 0 page1 13

Under the Open Skies Agreement any carrier of one party may enter into cooperative marketing arrangements such as blocked-space, codesharing, or leasing arrangements with:

a carrier or carriers of either party;

a carrier or carriers of a third country; and

a surface (land or maritime) transportation provider of any country;

provided that all participants in such arrangements hold the appropriate authority and meet the requirements normally applied to such arrangement^.^'

A key policy rationale behind the introduction of the Open Skies Agreement was the Australian Government's desire to introduce further and sustained competition on what it considers to be 'one of Australia's most important air routes". Of the rationale and effect of the Open Skies Agreement, when announcing its signing, the Minister for Aviation, Infrastructure, Transport, Regional Development and Local Government stated:

Over the last 10 years, the Australia-U.S. route has seen an avemge annual growth of 3.3 per cent, a figure with real hope of substantial improvement through this landmark open skies agreement. The Rudd Labor government is committed to opening furfher opportunities for Australian aviation, trade and tourism, resulting in the creation of jobs for Australians. Tourism is already responsible for around haFa million jobs in Australia, and this agreement should help to further strengthen our tourism industry. The agreement allows airlines to determine how many flights they opemte and the destinations they wish to setve in the United States and beyond, based on consumer demand and commerciel decisions without interference from government. This enables a wider range of options for consumers and a more competitive market.. . Libemlising Australian skies and opening markets for Australian camers will drive growth through competition and remove unnecessary regulatory burden on businesses. Aviation is a major industry in Australia and growth can only mean more jobs h r Austraian workers in the aviation industry and more choice for Australian consumers. Australia has been a long- standing leader in the benems of libemlisation, and the international aviation sector has been no small element of the picturn. Australla has extensive experience of the benefits of libemli~ation.~

The Minister went on to state:

Australian travellers, trade and tourism will benefit as designated airlines will be able to opemte unlimited services between the two countries, via other countries and beyond to other countries. Over time this will lead to greater choice through increased competition, and provide significant employment opportunities for Australians in the aviation and tourism industries.. . The new agreement will provide great opportunities for increasing trade and commercial links between Australia and the United States. We will have more competition in the market for Australian travellers through the entry of new caniers, such as v ~ u s t m l i a . ~ ~

" Id at A M 8, aectbn 7. as Commonweallh House of RepmmtaUve~, M I n M SWementrr, Monday 18 February 2008 at page 534. w.

as The Hon Anthony Albaneae MP (Minister br Infrastwcture, Tran$port Regkmal Dw&pmmt and Local Government), 'Historic AusbaliaUnited state^ 'Open Skkw' Avtath Agmmmt Reeched', 15 February 2008 avPUeMe at m D : l ~ . m i n i s t e r . i n f r a s t r u ~ r e r e a o v . a ~ 1 2 2008.htm [accessd 2 July 20091.

Gilbert + Tobin --l .doc page 1 14

The United States Secretary of Transportation similarly stated:

This agreement will strengthen the already close ties between the United States and Australia.. . Today's agreement begins a new era where American and Australian consumers, airlines and economies can enjoy the benefits of lower fares and more convenient service.29

The Australian and United States Governments have not been alone in identifying and emphasising the benefits the Open Skies Agreement potentially generates. For example, Tourism ~ustralia~' released a press release noting that the United States travel market provides around $2 billion in export income to Australia annually whilst stating that the Open Skies Agreement would:

. . . help Australia to grow tourism from the important U. S. travel market.. .

. . . provide a further boost in air services from one of Australia's most important tourist markets; and

. . . allow airlines to more readily increase airline semMces on the Trans-Pacific route. Once new services begin, increased seat capacity promises easier access to Australia particularly during peak periods?'

The Tourism and Transport Forum stated:

[t]he new arrangements will result in more choice and improved access for U.S. visitors, enabling the industry to more etbctively market Australia's tourism experiences in the USA."

In addition, the Victoria Tourism Industry Council (WlC) focused on the likelihood of new andlor increased direct routes to cities other than Sydney, stating:

... the agreement to expand air travel and competition on the Trans-Pacific mute augurs well for Melbourne and the Victorian tourism industry.. .

. . .Curmnt incumbent providers have tended to priotitise Sydney as a hub and it is hoped the increased opportunities for other airlines will cater for the strong demand for Melbourne as a destination.. .33

For the reasons set out in more detail below, the Applicants consider that the Virgin Blue 1 Delta Joint Venture is consistent with the intent behind the Open Skies Agreement as it will deliver passengers a wider range of options, whilst maintaining the competitive market established since the commencement of operations by V Australia and Delta.

4.4 Trans-Pacific routes

Travel between Australia and the United States is possible on both direct and indirect flights, although under the terms of the Open Skies Agreement only Australian and American owned caniers are able to provide unlimited direct services (with the exception of Air New Zealand, which

United States Department of Transportation, 'U.S. Transportation Secmtary Peters Announces New OpenSkiea Avlation Agreement with Australia', 14 February 2008 available at ~lt~:llwww.dot.aovlaffairsldo12208.htm [accessed 2 July 20091.

SO Established in 2004, Tourism Australia is a statutory authority of the Australian Government, which promotes Australia as a tourism deatiWn internationally and dotneetically and delivers research and fomcasts for the sedor. " Tourism Australia, 'Tourism Awtrelia Welcomes US Open Skies Agiwment', 15 Fekuary 2008 available at h~~:/lwww.twrism.australia.com~NewsCentre.as~?lana=EN&sub=0315&al=281 Q [accessed 2 July 20091. " Commonwearth House of RepresentaUves, MiniWal Statements, Monday 18 February 2008 at page 534. " Victoria Tourism Industry Council, Open W s to benefit Melbourne end Violwian Toun'sm, 15 February 2008 avaiiabta at

.vecci.om.au/vecdnews+reieases/boen+skies+to+benefit+melume+and+victorian+lourisml .asp [acceswd 2 July

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin ~ - l . d o o pagel 15

can provide unlimited direct services by combining rights established under the US-NZ Open and the Australia-NZ Open Skies arrangement^.^' There are currently four direct city-pain offered between Australian cities and mainland cities on the west coast of the United States:

SydneyC3Los Angeles;

SydneyC3San Francisco;

MelboumeC+Los Angeles; and

BrisbaneC3Los Angeles.

The SydneyC3Los Angeles route offers the greatest number of frequencies.

In addition to these direct routes, there are also a number of indirect one-stop routes (from both East and West Coast Australian cities) largely provided by foreign owned (i.e. non-Australian or non-United States) carriers. The major one-stop services are via New Zealand and Hawaii as these are substantially more convenient than most routings over Asian intermediate gateways. Indirect services include:

AustraliaCAuckland (NZ)+Los Angeles and San Francisco;

AustraliaCVancouver (Canada)+Los Angeles, San Francisco, Las Vegas and New York;

AustraliaCBeijing (China)+Los Angeles and San Francisco;

AustraliaCHong Kong (China)+Los Angeles and San Francisco;

AustraliaCTaipei (Taiwan)+San Francisco and Los Angeles;

AustraliaCSingapore+Los Angeles and New York;

AustraliaCNadi (Fiji)+Los Angeles;

AustraliaCPapeete (Tahiti)+Los Ange le~ ;~~ and

AustraliaCHonolulu (United States)+Los Angeles, Oakland, Sacramento, San Diego, San Francisco, San Jose, Las Vegas, Phoenix, Portland and Seattle.

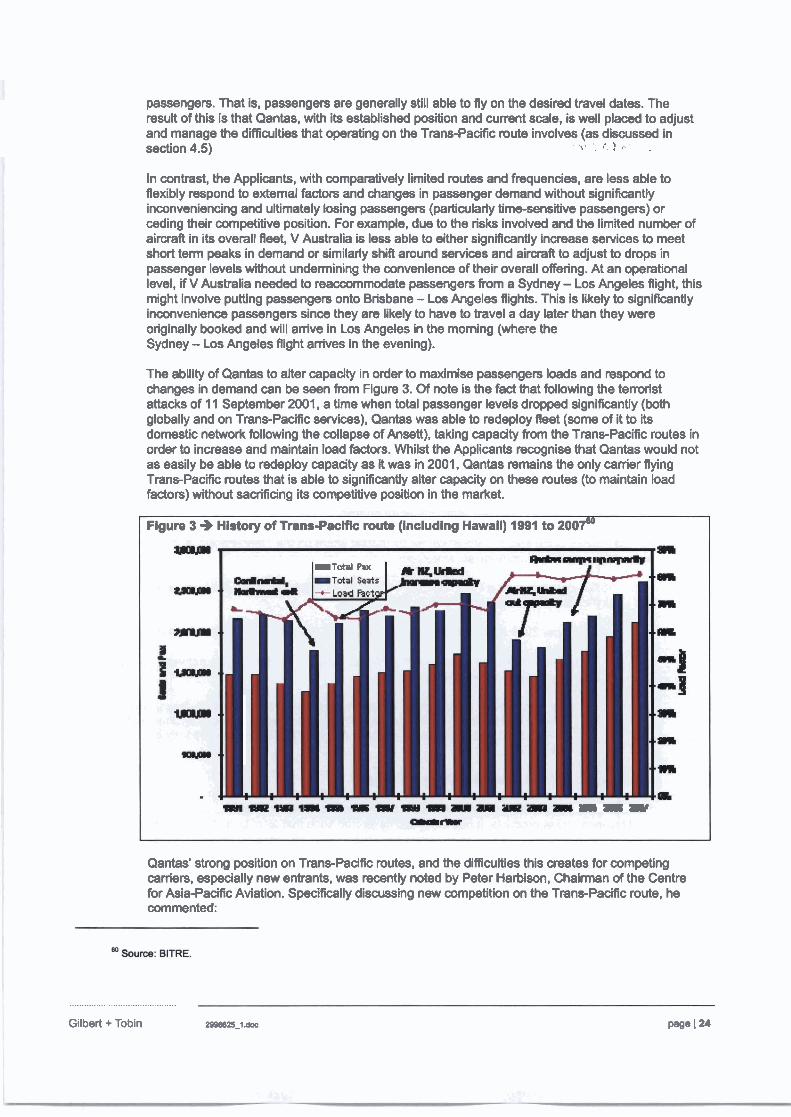

4.5 Historic trends in relation to the supply of passenger services on Trans-PacIfic routes

The ACCC has previously contemplated the considerable commercial risk and costs (both capital and operating) involved in operating air passenger services, particularly long haul services. The Applicants consider that introducing services, continuing operation and expanding operations on Trans-Pacific routes, particularly in respect of direct services, involves additional risk for a carrier (particularly for a new cartier). This is particularly so in the current1 volatile economic climate - where carriers face both a global recession and rising fuel prices!& such, the Applicants face a

Multilateral Agreement on the Uberallzation of international Air Transportatbn, available at htt~:l/www.maliat.aovt.~aareemmVenaIishtext.Ddf [accessed 2 July 091. DFAT, Agreement between the Gornemment ofAurbr,Iie and the Government of New Zealand ReleUng b Air Services [2003]

ATS 18. Australia has entered into bilateral air mvkes agreements with a number of countries that give same limited rights b carry passengers behwm Australia and the United States. A summary table of those dghb is set out in krrwxuro D. Theee servhe, prwMed by Air Tahiti Nui, are seasonal. '' The cumnt finand diffiarltleQ faced by airlines globally has been widely reported in the media. See for example Aviation Week, 'IATA predicts airline losses of $9B', 8 June 2009 available at h : .avia. w ri I . ? nn I= id=n I . ml [acceswd 2 July &% a i . o e ~ f l ~ ~ n $ ~ I d ~ o " & C " , " M ? n ~ ~ Lha9 d i I ~ u ~ % l a ~ ~ G b 0 8 " J " ~ 0 ~ g o s X available at

Gilbert + Tobin 2ewm5-l.doc

particularly difficult set of challenges in developing and sustaining a durable network of competitive services.

The key difficulty of launching and providing Trans-Pacific services is the geography involved. Trans-Pacific services generally involve non-stop flight segments of over 12,000km and in excess of 14 hours travelling time. There is also an absence of intermediate stopover points with the limited exception of Hawaii. This geography has a number of key flow on effects.

First, the geography necessitates the use of specialised long-range aircraft to service the routes, such as the Boeing 747-400, the Boeing 777-200LR or 777-300ER, the Airbus A380, the Airbus 340-500 or 340-600. These types of aircraft are not part of many carriers' fleets due to their specialised nature and the fact that their use is optimised on long-haul routes such as those across the Pacific. These aircraft are not easily redeployed on other routes. This is particularly true for new carriers such as V Australia that do not have established long-haul operations in other markets.

Second, the large gauge of aircraftm capable of operating the route non-stop means that additions of capacity are relatively large compared to the annual rate of growth of the route. That is, it is not possible to easily increase or decrease seat capacity in increments matched to small changes in demand. This means the route is subject to capacity digestion issues from time to time, especially when capacity is added by more than one player simultaneously.

Third, due to the distances involved, there are relatively few city-pairs available to carriers (for example, it is not currently possible to fly non-stop from New York or Toronto to Sydney or Melbourne with a viable payload). This means that all routes connect on the east coast of Australia and the west coast of the United States, leading to a hubbing of operations in Los Angeles, San Francisco and Sydney. This was recently acknowledged by Tourism Australia which noted:

Los Angeles-Sydney is the busiest route with over a third of all flights from the U.S. to Australia operating on this mute. The current frequencies and capacity to Australia's key gateways are focused on the east coast of Australia and West Coast due to current aircraff ranges.39

Finally, the absence of intermediate points (in contrast to the 'Kangaroo" route) mean that carriers operating on Trans-Pacific routes operating without the benefit of an alliance partner are particularly susceptible to any changes in demand and directional passenger flows between Australia and the United States (for example as a result of currency depreciation in either the A$ or $US). The absence of an ability to market services between intermediate points (not affected by factors such as currency depreciation) means it is not possible to readily offset any changes in passenger flow between Australia and the United States or respond to changes in demand.

The difficulty of competing effectively on Trans-Pacific routes can be seen from the fact (shown in Figure 1) that three major United States carriers have withdrawn from the route since 1991, whilst Air New Zealand also commenced and ceased direct services between Australia and the United States over this period. This has created the situation detailed in section 5, where Qantas and United Airlines (both part of major carrier alliances) have been the only carriers servicing this market with direct flights for many years.

htta:llnews.amh.com.aulbreakina-new-~0dd/~IobaI-aidin8&to-10~e9biI1'm-~sdolIar&in-2009-20090608cOd6.htm [accessed 2 July 20091. For example, V Australia's Boeing 777300ER in a threedass configuration has 361 seats, Qantas' Airbus A380 in a fwrclass

conliguration has 450 seats, United Aidin68 747-400 in a threedeso conffguratlan has 374 seats and Delta's 777-200 in a two- dass conflguratlon has 278 seats. Tourism Australia, USA Avlefkn~ Pmtlk,: Understanding the USA to Au86nlk) Aviation Envlmnment, June 2008 at page 1.

Gilbert + Tobin

A summary table of carriers operating to Australia since 1991 is set out in Annexure E.

Figure 1 - Summary of carrier withdrawal from Australia - United States routes

Amdcan Airlines ceased Australia - United States operations in 3 1992. American Airlines now codeshares on Australia - United - States mutes with Qantas. --------------------------.-------------------------------------------------------------------------

Continental Continental Airlines ceased Australla - United States operations in Ahlines m. OctDber 1993.

., ... ,, , Northwest Airlines ceased Australia - United States oparations in

---------------------------.------------------------------------------------------------------------- Air New Zealand ceased direct Australia - United States operations in 2003. Air New Zealand continues to codeshare on United Airlines'

MNEWML*ND~ Australia - United States services and operates indirect services via Auckland. . - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

This pattern of carrier withdrawal should be contrasted with the large number of carriers and setvices offered between Australia and Europe (which benefits significantly from the existence of multiple intermediate points not existent on the Australia - United States routes). A number of carriers have entered these markets in recent years including Virgin Atlantic, Gulf Air, Emirates, Qatar Airways, Ethihad and AirAsia X. There have also been increases in the number of Australian city-pair connections and frequencies offered by mid-point carriers such as Singapore Airlines, Malaysia Airlines, Thai Airways and Cathay Pacific.

4.6 The need for effective beyond-networks for carriers operating on Trans-Pacific routes

A key issue for caniers on Trans-Pacific routes is the need for access to effective beyond domestic and Trans-Tasman networks. Such networks are required in order to attract customers and feed passenger traffic onto Trans-Pacific setvices in order to maximise passenger loads. The need for this access is a result of two factors.

First, as noted above, aircraft range limitations mean that passengers are generally required to travel through gateway points being either Los Angeles, San Francisco and Vancouver (when

.-r travelling to North America) or Sydney, Brisbane, Melbourne and Auckland (when travelling to Australasia). Where a significant number of passengers are travelling to destinations other than those gateway cities it is important for carriers to be able to offer these additional city-pair connections. It is particularly important for Australian carriers to have access to a strong United : States domestic network that enables travel connections beyond existing gateway ports because Los Angeles and San Francisco's catchments are only approximately 8% of the population of the United States contiguous states (with the whole of California representing only slightly more than 10% of the United States population). In this respect, the Applicants estimate that 60% of

., Sydney - Los Angeles traffic travels beyond Los Angeles. As such, a carrier flying to the United States with an Australian network behind it but no United States domestic network can only service a small proportion of the United States market without being able to reach beyond the United -, States gateway port. In contrast, a carrier flying on Trans-Pacific routes with a comprehensive

., I United States domestic network but no Australian domestic network is better able to service a , significant proportion of the United States - Australia market because of the relative concentration

of the population on the east coast of Australia. For example, the Australian gateway city airports of Sydney, Melbourne and Brisbane are within a few hours driving distance of approximately 60% of the entire national population (with Sydney alone accounting for 26% of the national population).

A second feature of Trans-Pacific air passenger travel is what is called 'Dual Destination" traffic. Because of the length of the trip and the crossing of multiple time zones, a significant proportion of North Americans visit both Australia and New Zealand in the one trip, usually passing into one country outbound from North America and home via the other country. For example, Auckland International Airport, drawing on information from Statistics NZ, estimates that 32% of Americans arriving in Auckland do so from Australia, 57% direct from the United States and the remaining

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin 7~e1m-l.da m e 1 18

11 % via the Pacific Islands and other points.40 In addition, figures from the Australian Department of Immigration and Citizenship shows that 10% of Americans arriving in Australia do so via New Zealand. Conversely, many Australians and New Zealanders visit both the United States and Canada in the one trip.

As discussed in section 5, the incumbent carriers on the Trans-Pacific routes have well established domestic and Trans-Tasman networks - Qantas, through its oneworld, codeshare and interline arrangements with American Airlines (in addition to its own extensive Australian~Trans-Tasman network) and United Airlines through its Star Alliance, codeshare and interline arrangements with Air New Zealand and Air Canada (in addition to its own extensive United States domestic network). Air New Zealand and United Airlines have been granted broad antitmst immunity by the United States Department of Transportation (DOT) enabling them to coordinate all international services, including between the United States and New Zealand and the South Pacific regi~n.~'

From a commercial perspective, the ability to penetrate domestic markets in Australia and the United States is particularly important where it allows carriers on the Transpacific routes to more effectively respond to changes in passenger flows driven by factors such as currency depreciation. As can be seen from Figure 2, passenger flows on Transpacific routes are substantially influenced by fluctuations in the A$/US$ exchange rate - i.e. the weaker the Australian dollar, the weaker departures are from Australia and vice versa.

Figure 2 -The Australia I United States InboundlOutbound Ratio and the A S R I S ~

I - lnboundlOutbound RRlo (Trend Serln, LHS) - A$IUS$ (reverse scale, RHS) I 160 0.40

150 0.50

140

130 0.60

120 0.70

110

100 0.80

90 0.90

80

70 1.00

$9 , ,ac*~' , ,,p' ,*c*+' ,&" ,*NQ' ,&"' ,&

By having a strong United States and Australian domestic network (beyond the Transpacific gateway points) and being able to service traffic originating from either end equally well, a carrier is better able to manage load factors and yields to cope with the inevitable changes in demand on either side of the Pacific caused by currency depreciation or other external factors. Because a carrier can operate a domestic network at only one end of its Trans-Pacific routes it is, of course, much more limited in its ability to respond to swings in the balance of demand towards the market where it has poor penetration.

40 Source: Statistics New Zealand. " DOT Order 2001-3-4 (UnitedIAir New Zealand). This Order is a grant of broed-based world-wlde immunity from Unlted States antbust law for United airline^^ and Air New Zealand. This immunity allows a very high level of operational cooperation for all United Airlines and Air New Zealand alliance acthrih indudlng rerenue sharing, route planning, flight scheduling, purchasing, marketing sales and distribution. Source: Reserve Bank of Australla, Australian Bureau of Statistics

.................... ~ .......................

Gilbert + Tobin 29nma-1.doc f ~ e 1 19

The need for an effective network partner in order to compete on Trans-Pacific routes has been a key issue noted and discussed by analysts in recent months. See, for example, the following comments regarding V Australia and Delta's operations:

V Australia's product is sttvng, but both V Australia and Delta face distribution issues, V Australia in the U.S. and Delta in Australia. V Australia has more choice for pertners (Detta can real& only choose from W N or VBA, both of which compete with Delta) and management indicated it is pursuing a solution.43

Management also indicates that it is in the process of addressing the distribution disadvantage that it is at relative to Qantas for the U.S. market. Whilst this is not expected to include the Star Alliance, it is likely to include Virgin U.S. which we believe still leaves Qantas with a significant distribution advantage in the U.S. market4

Distribution network lacking: Qantas will pit its oneworld alliance connections from LAX with Ametican Airlines against United's Star Alliance and Delta's SkyTeam. V Australia will compete with no alliance but a series of agreements with airlines ... 46

While we believe the opportunity exists for V Australia to secure a significant presence in the Trans-Pacific market, the lack (as yet) of any North American dimbution is likely to weigh on VBA's efforts in building position in this market in what are possibly the worst conditions possible.. .46

...we do however anticipate that Delta Airlines will ultimately need a strong distribution & feeder presence in the Australan market for their foray into the Trans-Pacific market to be successful. We do not expect Qantas Ainvays to provide this support - being the main competitor. As a result, Delta will have to rely on Virgin Blue domestic - having their own domestic operations seems impractical given their nominal presence in the Trans-Pacific market. Intuitively, such an outcome would bode well for Vitgn Blue and may even allow V Australia to enter into an earnings accretive arrangement with Delta (e.g. a codeshare); however, we consider these possibilities to be p m t u r e to consider in our financial forecast.. .47

4.7 The supply of frelghtlcargo sewices

Air cargo I freight is carried between Australia and the United States via:

a mix of dedicated air freighter services and in the cargo hold of passenger jets; and

on both direct and indirect flights with a large amount of freight being transported via intermediate points in Asia.

As is discussed in section 6.3, Qantas and United Airlines are significant carriers of air cargo 1 freight between Australia and the United States. Qantas carries air freight both in the cargo hold of its passenger fleet (including on both Jetstar and Qantas) as well as via dedicated Boeing 747-400 freighter services. In respect of its cargo services, Qantas Freight states:

We have the most extensive airline network into and out of Australia. Internationally, Qantas and Jetstar combined operates nearly 750 flights a week, offering services to 86 international destinations (including codeshare semMces) in 40 countries. Add to that the

" CommSec, 'EquMes Research Report, Virgin Blue Limited lH09 Result: Riding the skwdom', 23 February 2009 at page 7. Credit Sulsae, Equity Research, 'Virgin Blue Holdings lH09 result - beats expecbtrOns', 24 Febrwry 2009 at peee 4.

" Galdman Sachs JB Were, 'ResuM Commentary - Virgin Blue Wings Limited 1 H09 Result, Tough Operating Conditions to Continue', 23 February 2009 at page 3. " Id at page 1. '' Deutsche Bank, 'Emerging Companies - Virgin Blue', 23 February 2009 at page 5.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Gilbert + Tobin =-I .doc Page 120

added strength of the Qantas domestic network you can rely on fast and efficient delivery of your goods to any de~tination.~'

FedEx and UPS also transport a significant volume of air cargo / freight between Australia and the United States via their dedicated freighter service^.^'

5 Carriers currently providing Trans-Pacific air passenger services

Currently, the majority of Trans-Pacific air services (on either a one-stop or non-stop) are provided by incumbent carriers Qantas and United Airlines. As noted above, the Applicants have only recently entered onto the Trans-Pacific routes.

Between them, Qantas and United Airlines, account for a large majority of all air travel between Australia and the United States. As described in further detail in section 6.2, in 2008:

Qantas and United Airlines carried 100% of direct passenger traffic between Australia and the mainland United States;

Qantas and United Airlines carried 69.5% of all Trans-Pacific passengers when both direct and indirect travel routes are taken into account (this proportion is higher when United Airlines' extensive codeshare arrangements with Air New Zealand and Air Canada are taken into account); and

over 65% of Trans-Pacific bookings were for Qantas services (i.e. flights booked on Qantas or American Airlines) or for United Airlines services.

It is for these reasons that the Trans-Pacific routes have often been described, prior to the entry of the Applicants, as a "virtual duopo~y".~~

5.1 Qantas

(a) Ovetview of Qantas Trans-Pacific operations

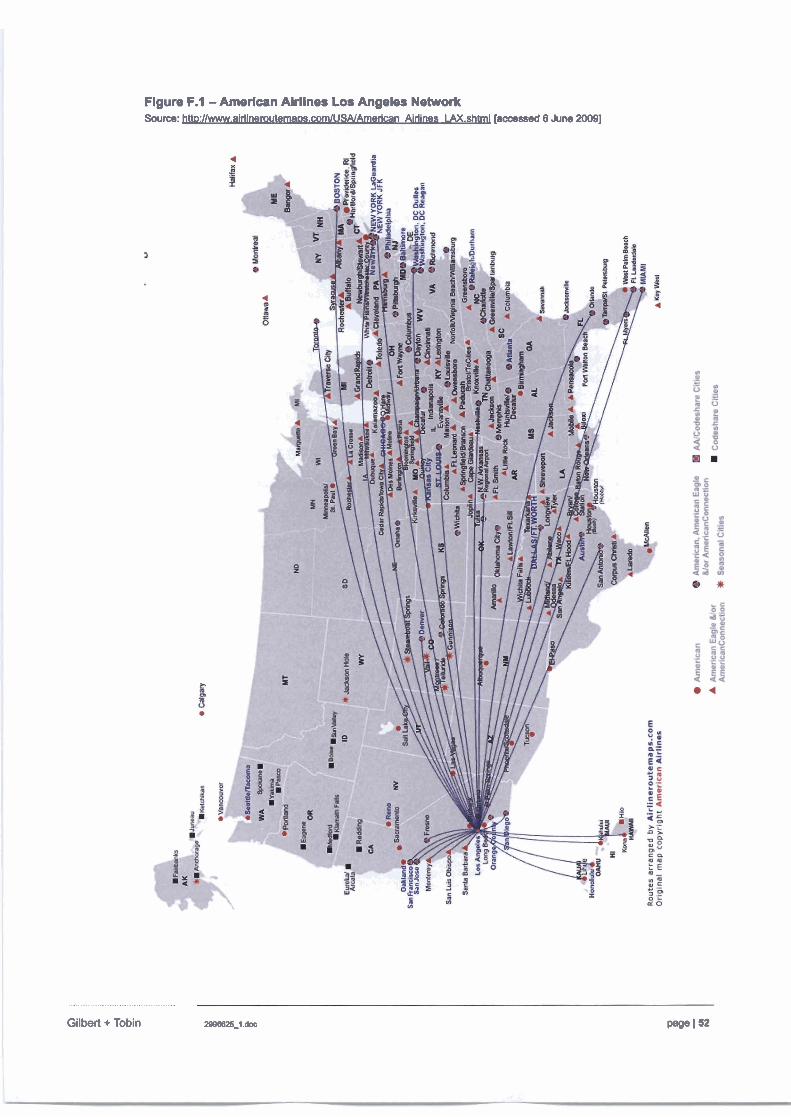

A general overview of Qantas' operations, and its oneworld partner American Airlines is set out in Annexure F.

Qantas commenced Trans-Pacific services in 1954.~' In recent years, Qantas has developed an unparalleled market presence on Trans-Pacific routes providing a deep schedule and extensive network of city-pairs in Australia and the United States (with its oneworld alliance partner American Airlines which has the second most numerous United States domestic flights onwards from Los Angeles after United ~ i r l i nes ) .~ Qantas has recently announced an expansion of its codesharing arrangements with American Airlines such that it now boasts a North American network of 42 cities - 36 in the United States and 6 in Canada.

a Qantas Freight, 'About Us' available at htt~:l/www.aantas.corn.auKreiaht~dvnlaboutUs [accessed 2 July 20091. a As at February 2009. For information regarding UPS see htto:l/www.u~s.com and for information regarding FedEx see htt~:/lfedex.wm/~ " Shu-Ching Jean Chen, Forbes.com 'Door Opened b Competition on U.SAussie Air Route, 15 February 2009 available at httD://www.forbes.~)~2008102115/ausbalia-uir-maeu-cx ic 0215marketsl orint.htrnl [acoesoed 2 July 20091. " Qantas, 'Qantas at a Glance' available at htt~:l/www.aantas.com.au/infodetaiVabouffFactFiI~.Ddf [accessed 2 July 20091. " Qantas' strong relatkmhip with American Airlines is discussed bekw in sedkn 5.1 (c). An overview of American Airlines' operations is set out in Annexure E.

Gilbert + Tobin --1 .doc pace 1 21

As at December 2009, Qantas will operate 40 return services per week between Australia and mainland United States consisting of:

35 to Los Angeles - 14 non-stop from Sydney, 14 from Melbourne, (7 non-stop and 7 via Auckland) and daily services from Brisbane; and

5 between Sydney and San Francisco.

Qantas also offers one beyond daily service between New York and Los Angeles.

Qantas and Jetstar (part of the Qantas Group) also operate services to Honolulu, combining to a daily service.

Qantas has recently announced that it will increase its Airbus A380 offering on the Sydney - Los Angeles and Melbourne - Los Angeles routes.53 The changes will increase Qantas' Airbus A380 flights between Sydney and Los Angeles from three to four a week on 6 August 2009. This will increase again in November. From November, Qantas will offer a daily Airbus A380 service . between Sydney and Los Angeles whilst flights between Melbourne and Los Angeles on the Airbus A380 will increase from two to three per week. It has been reported that these new capacity changes and the expanded codeshare arran ent between Qantas and American Airlines are a specific 'pre-emptive move" to Delta's entry. F

Qantas services mainland United States routes using Boeing 747-400 and Airbus A380 aircraft.

(b) Qantas' Trans-PacMc capacity shares