Embed Size (px)

Citation preview

© Grant Thornton International. All rights reserved.

IFRS workshopAll India Chartered Accountants Society

Session: AS convergence to IFRS

Aseem VohraJuly 10, 2010

© Grant Thornton India. All rights reserved.

IFRS transition in India – Road AheadIFRS transition in India – Road Ahead

Impact of convergenceImpact of convergence

Process of transitioning financial reportingProcess of transitioning financial reporting

© Grant Thornton International. All rights reserved.

IFRS transition in India… Road Ahead

© Grant Thornton International. All rights reserved.

IFRS transition in India – an introduction

Need for Adoption in India

• Global economy - need to speak in a language which is globally accepted.

• International Financial Reporting Standards (‘IFRS’) has now evolved into being the most widely accepted and trusted financial reporting language

• Considering the emerging role of India in the global economy, it was imperative for India to harmonize with global financial reporting standards

• In August 2007, ICAI announced India’s intention to converge its reporting standards with IFRS - ICAI released a concept paper on convergence

• MCA has set up a core group to develop a roadmap for India's transition to IFRS – roadmap released in January 2010

• MCA also released a separate roadmap for Banking and Insurance Companies in March 2010

• SEBI amended the listing agreement to permit voluntary early adoption of IFRS (as issued by IASB) by listed parent companies

© Grant Thornton International. All rights reserved.

IFRS transition in India – an introduction

Progress to date

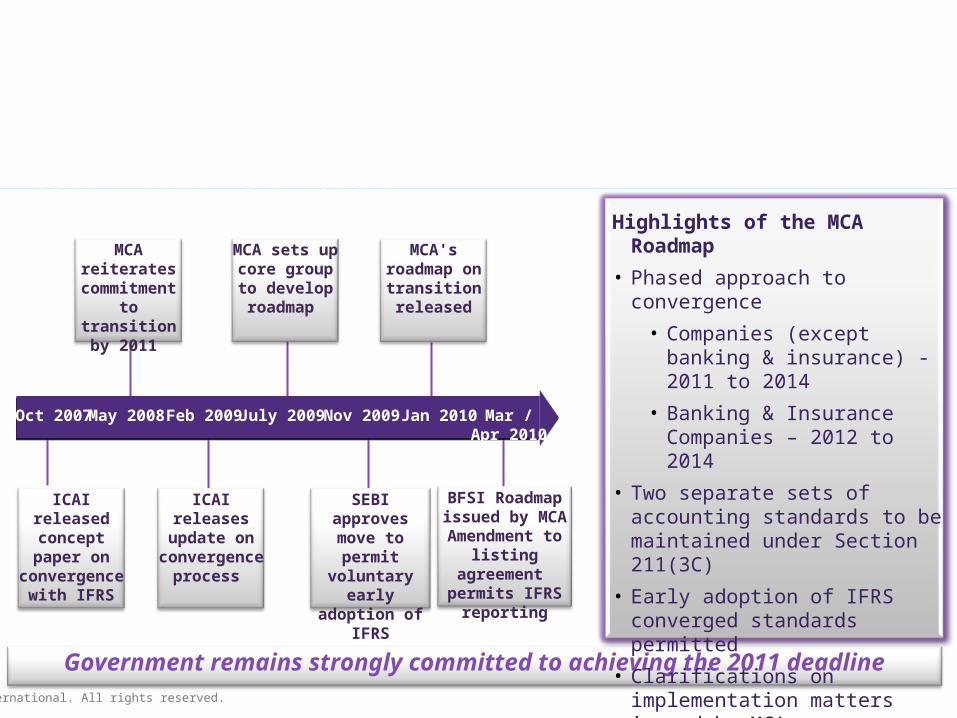

Government remains strongly committed to achieving the 2011 deadline

ICAI released concept paper on

convergence with IFRS

MCA reiterates

commitment to transition

by 2011

MCA's roadmap on

transition released

SEBI approves move to permit voluntary early

adoption of IFRS

MCA sets up core group to

develop roadmap

ICAI releases update on

convergence process

BFSI Roadmap issued by MCAAmendment to

listing agreement permits IFRS

reporting

Oct 2007 Feb 2009 Nov 2009May 2008 July 2009 Jan 2010Mar / Apr 2010

Highlights of the MCA Roadmap

• Phased approach to convergence

• Companies (except banking & insurance) - 2011 to 2014

• Banking & Insurance Companies – 2012 to 2014

• Two separate sets of accounting standards to be maintained under Section 211(3C)

• Early adoption of IFRS converged standards permitted

• Clarifications on implementation matters issued by MCA

• Clarity still required on several practical aspects

© Grant Thornton India. All rights reserved.

IFRS transition in India – an introduction

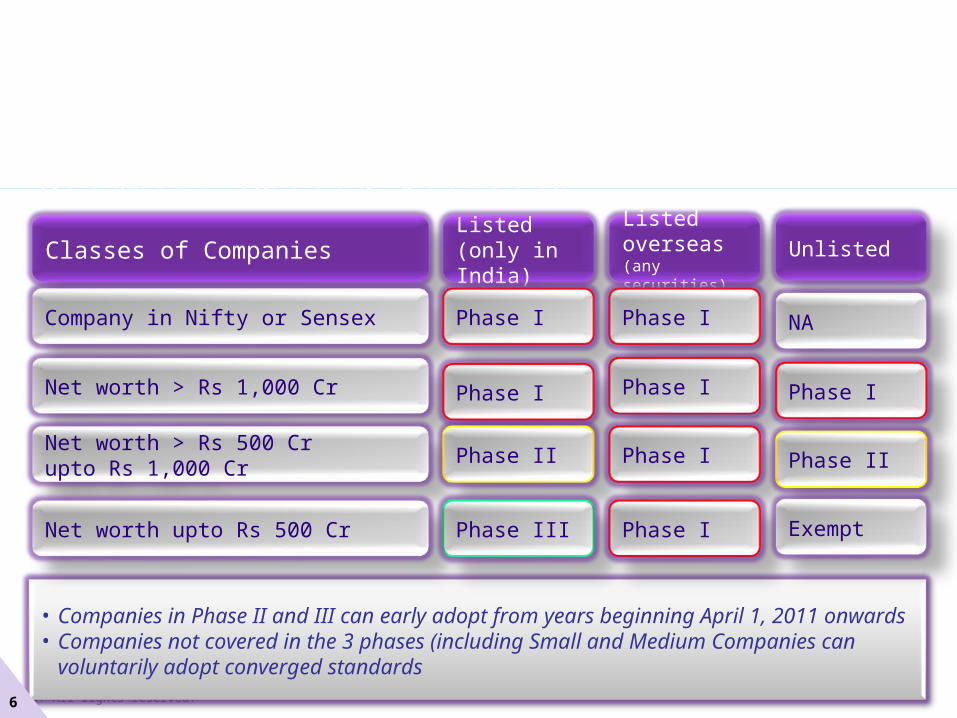

Roadmap: Phased Approach

• Companies in Phase II and III can early adopt from years beginning April 1, 2011 onwards• Companies not covered in the 3 phases (including Small and Medium Companies can

voluntarily adopt converged standards

Classes of CompaniesListed (only in India)

Listed overseas (any securities)

Unlisted

Company in Nifty or Sensex Phase I Phase I NA

Net worth > Rs 1,000 Cr Phase I Phase I Phase I

Net worth > Rs 500 Cr upto Rs 1,000 Cr

Phase II Phase I Phase II

Net worth upto Rs 500 Cr Phase III Phase I Exempt

6

© Grant Thornton India. All rights reserved.

IFRS transition in India – an introduction

Roadmap: Phased Approach

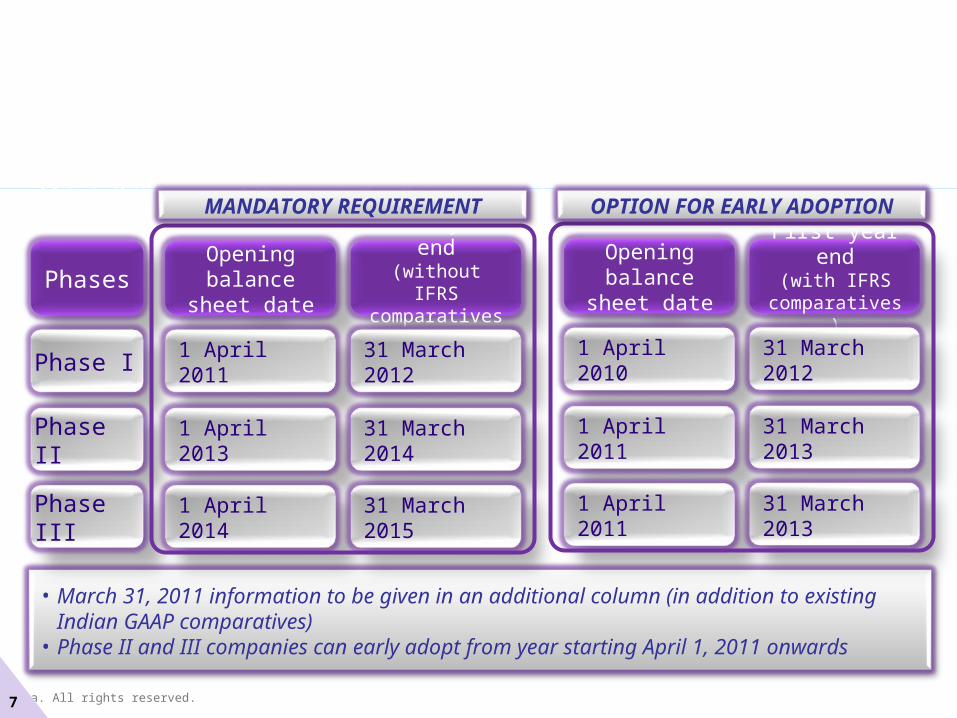

• March 31, 2011 information to be given in an additional column (in addition to existing Indian GAAP comparatives)

• Phase II and III companies can early adopt from year starting April 1, 2011 onwards

Phases

Phase I

Phase II

Phase III

Opening balance sheet

date

First year end(without IFRS comparatives)

1 April 2011 31 March 2012

1 April 2013 31 March 2014

1 April 2014 31 March 2015

Opening balance sheet

date

First year end(with IFRS

comparatives)

1 April 2010 31 March 2012

1 April 2011 31 March 2013

1 April 2011 31 March 2013

MANDATORY REQUIREMENT OPTION FOR EARLY ADOPTION

7

© Grant Thornton India. All rights reserved.

IFRS transition in India – an introduction

MCA roadmap - BFSI: A phased approach

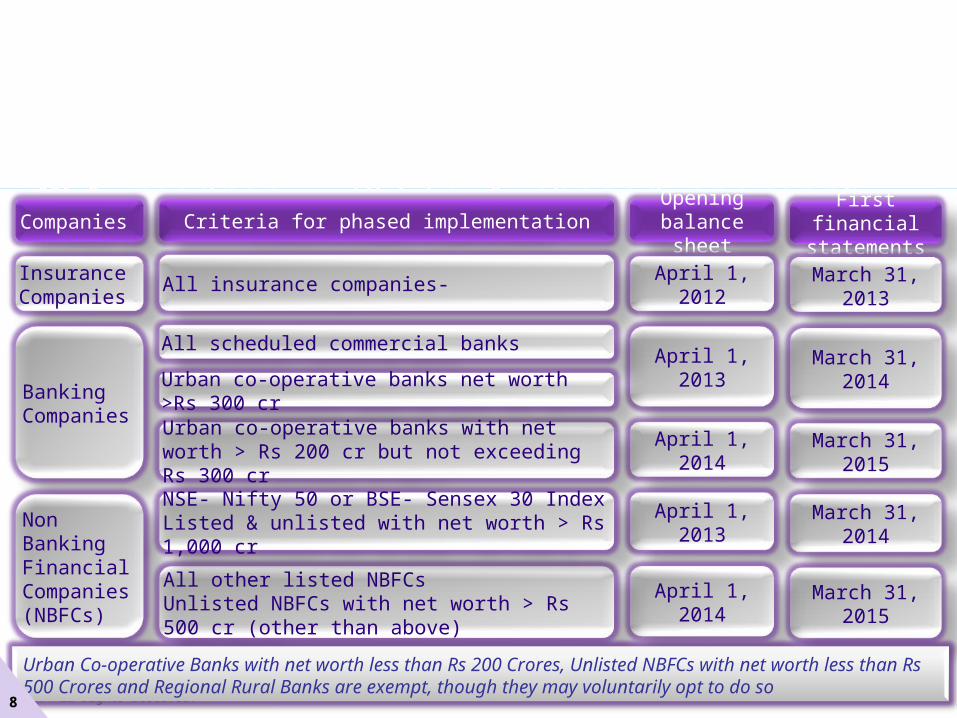

Criteria for phased implementation First financial statements

March 31, 2013

Opening balance sheet

April 1, 2012

Companies

Insurance Companies

All insurance companies-

March 31, 2014April 1, 2013Banking Companies

All scheduled commercial banks

March 31, 2015April 1, 2014Urban co-operative banks with net worth > Rs 200 cr but not exceeding Rs 300 cr

March 31, 2014April 1, 2013Non Banking Financial Companies (NBFCs) March 31, 2015April 1, 2014

All other listed NBFCs Unlisted NBFCs with net worth > Rs 500 cr (other than above)

NSE- Nifty 50 or BSE- Sensex 30 IndexListed & unlisted with net worth > Rs 1,000 cr

Urban co-operative banks net worth >Rs 300 cr

Urban Co-operative Banks with net worth less than Rs 200 Crores, Unlisted NBFCs with net worth less than Rs 500 Crores and Regional Rural Banks are exempt, though they may voluntarily opt to do so

8

© Grant Thornton India. All rights reserved.

IFRS transition in India – an introduction

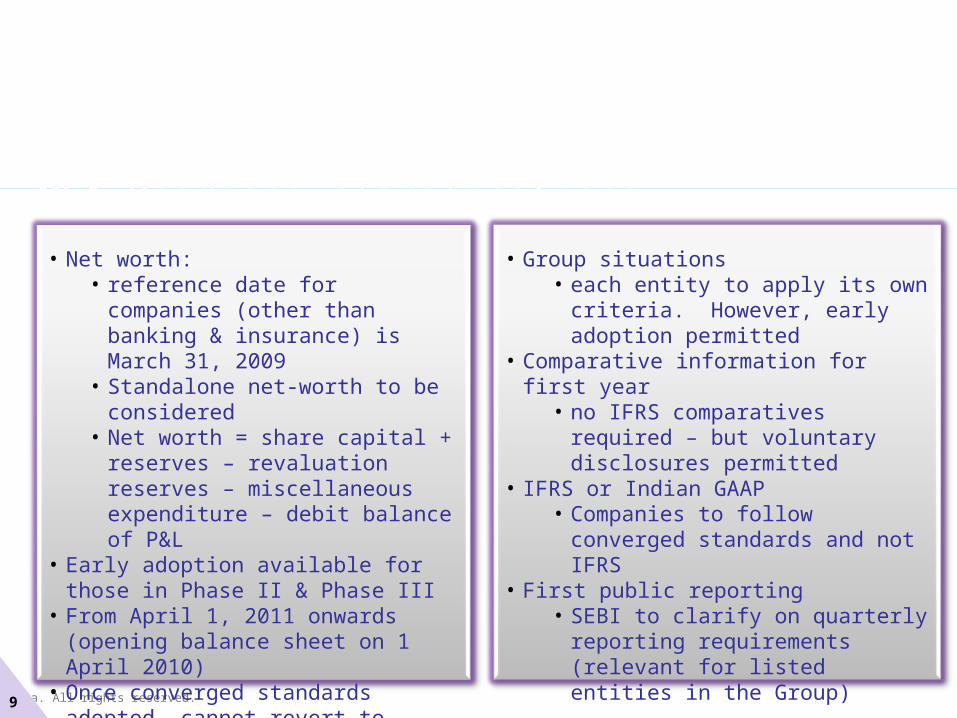

MCA Roadmap: clarifications

• Net worth:• reference date for companies (other

than banking & insurance) is March 31, 2009

• Standalone net-worth to be considered

• Net worth = share capital + reserves – revaluation reserves – miscellaneous expenditure – debit balance of P&L

• Early adoption available for those in Phase II & Phase III

• From April 1, 2011 onwards (opening balance sheet on 1 April 2010)

• Once converged standards adopted, cannot revert to existing Indian GAAP

• Group situations • each entity to apply its own criteria.

However, early adoption permitted• Comparative information for first year

• no IFRS comparatives required – but voluntary disclosures permitted

• IFRS or Indian GAAP • Companies to follow converged

standards and not IFRS • First public reporting

• SEBI to clarify on quarterly reporting requirements (relevant for listed entities in the Group)

9

© Grant Thornton India. All rights reserved.

IFRS transition in India – an introduction

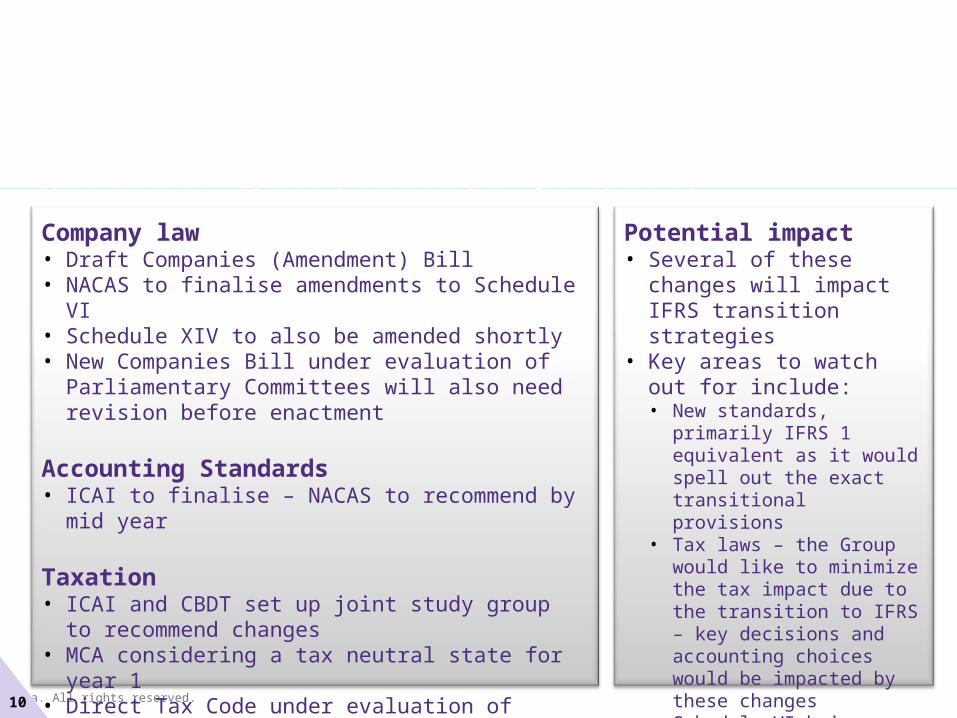

Roadmap: Developments to track

Company law• Draft Companies (Amendment) Bill• NACAS to finalise amendments to Schedule VI• Schedule XIV to also be amended shortly• New Companies Bill under evaluation of Parliamentary

Committees will also need revision before enactment

Accounting Standards• ICAI to finalise – NACAS to recommend by mid year

Taxation• ICAI and CBDT set up joint study group to recommend

changes• MCA considering a tax neutral state for year 1• Direct Tax Code under evaluation of Parliamentary

Committees will also need revision before enactment

Potential impact• Several of these changes will

impact IFRS transition strategies

• Key areas to watch out for include:• New standards, primarily

IFRS 1 equivalent as it would spell out the exact transitional provisions

• Tax laws – the Group would like to minimize the tax impact due to the transition to IFRS – key decisions and accounting choices would be impacted by these changes

• Schedule VI being amended – may require additional disclosures and possibly functional classification

10

© Grant Thornton India. All rights reserved.

IFRS transition in India – an introduction

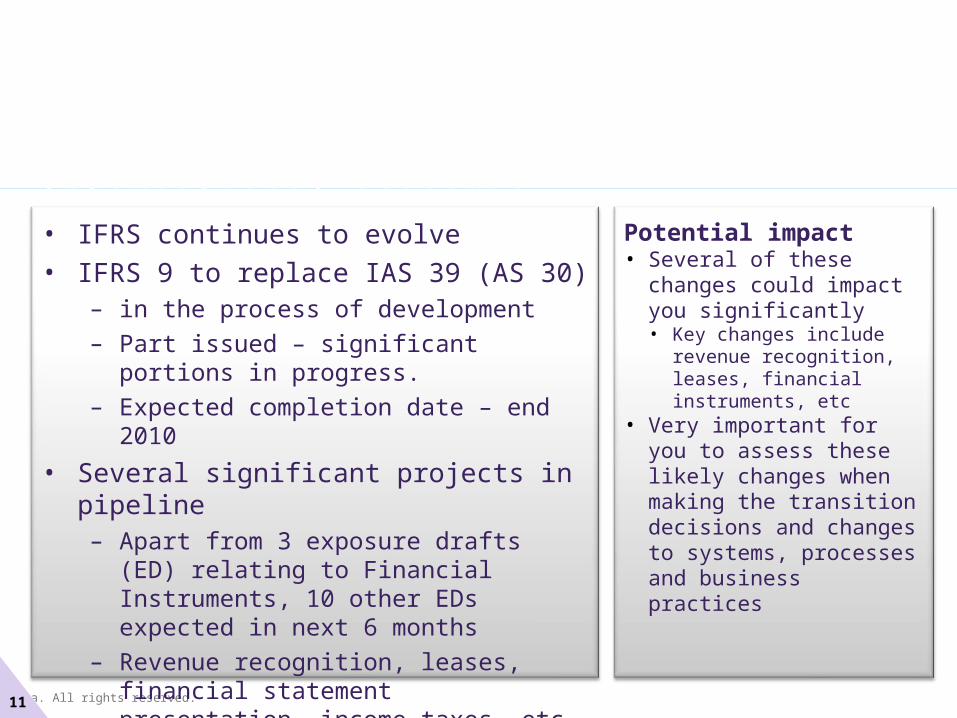

International scenario

• IFRS continues to evolve• IFRS 9 to replace IAS 39 (AS 30)

– in the process of development

– Part issued – significant portions in progress.

– Expected completion date – end 2010

• Several significant projects in pipeline– Apart from 3 exposure drafts (ED) relating

to Financial Instruments, 10 other EDs expected in next 6 months

– Revenue recognition, leases, financial statement presentation, income taxes, etc

• India working to a moving target

Potential impact• Several of these changes

could impact you significantly• Key changes include revenue

recognition, leases, financial instruments, etc

• Very important for you to assess these likely changes when making the transition decisions and changes to systems, processes and business practices

11

© Grant Thornton International. All rights reserved.

IFRS transition in India – an introduction

Convergence

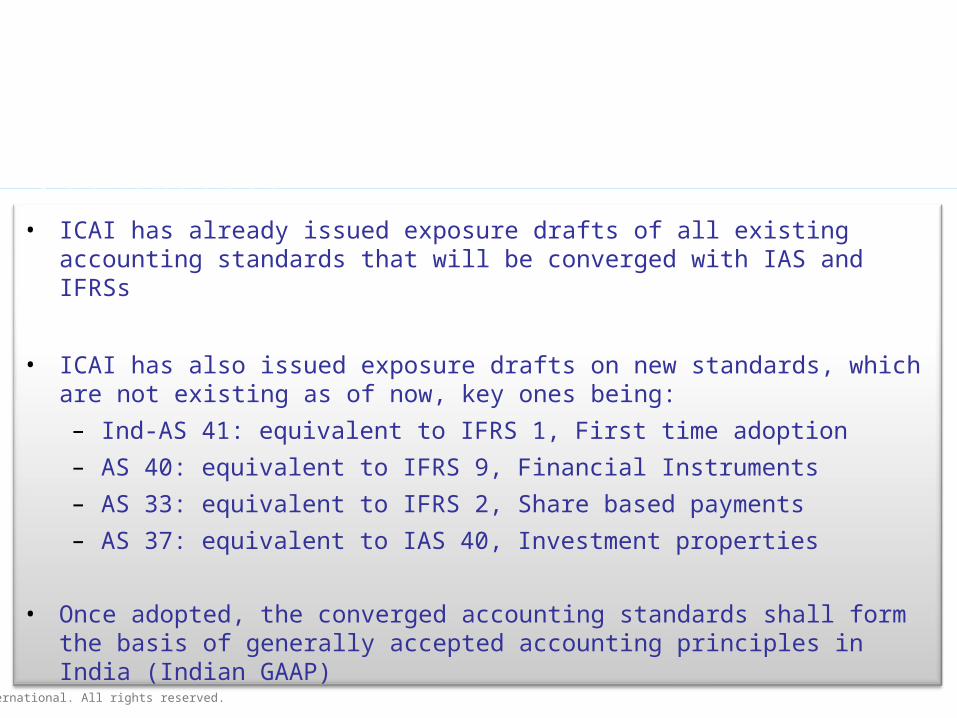

• ICAI has already issued exposure drafts of all existing accounting standards that will be converged with IAS and IFRSs

• ICAI has also issued exposure drafts on new standards, which are not existing as of now, key ones being:

– Ind-AS 41: equivalent to IFRS 1, First time adoption

– AS 40: equivalent to IFRS 9, Financial Instruments

– AS 33: equivalent to IFRS 2, Share based payments

– AS 37: equivalent to IAS 40, Investment properties

• Once adopted, the converged accounting standards shall form the basis of generally accepted accounting principles in India (Indian GAAP)

© Grant Thornton International. All rights reserved.

Impact of convergenceImpact of convergence

© Grant Thornton International. All rights reserved.

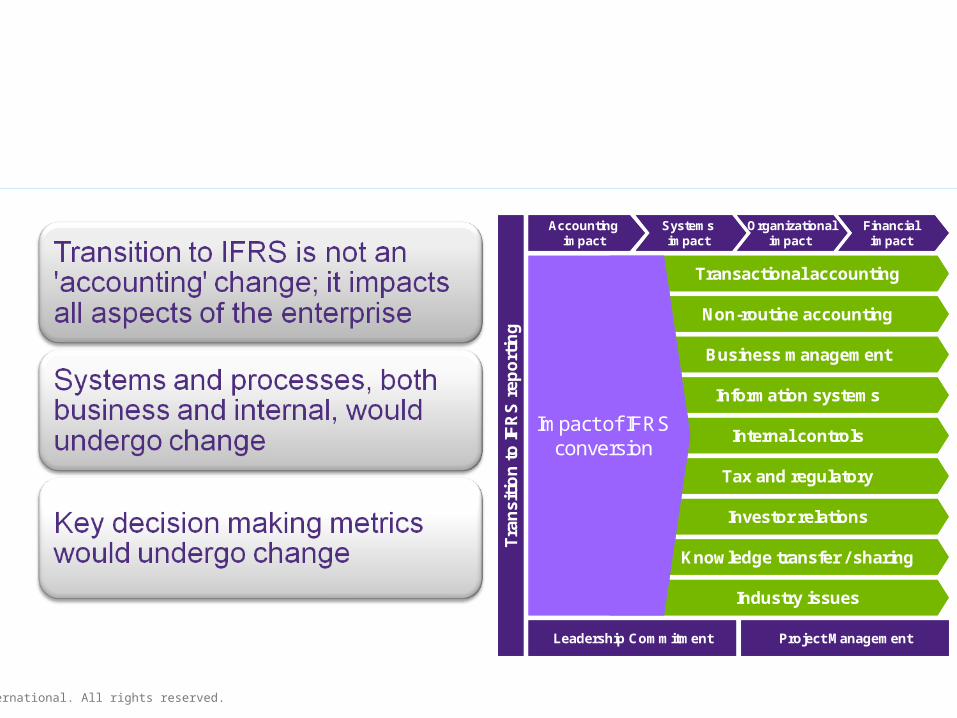

Impact of convergence

Potential Areas of Impact

Internal controls

Information systems

Non-routine accounting

Business management

Tax and regulatory

Investor relations

Knowledge transfer / sharing

Industry issues

Transactional accounting

Impact of IFRS conversion

Tra

nsi

tio

n t

o IF

RS

rep

ort

ing

Leadership Commitment Project Management

Accounting impact

Systems impact

Organizational impact

Financial impact

Internal controls

Information systems

Non-routine accounting

Business management

Tax and regulatory

Investor relations

Knowledge transfer / sharing

Industry issues

Transactional accounting

Impact of IFRS conversion

Tra

nsi

tio

n t

o IF

RS

rep

ort

ing

Leadership Commitment Project Management

Accounting impact

Systems impact

Organizational impact

Financial impact

© Grant Thornton International. All rights reserved.

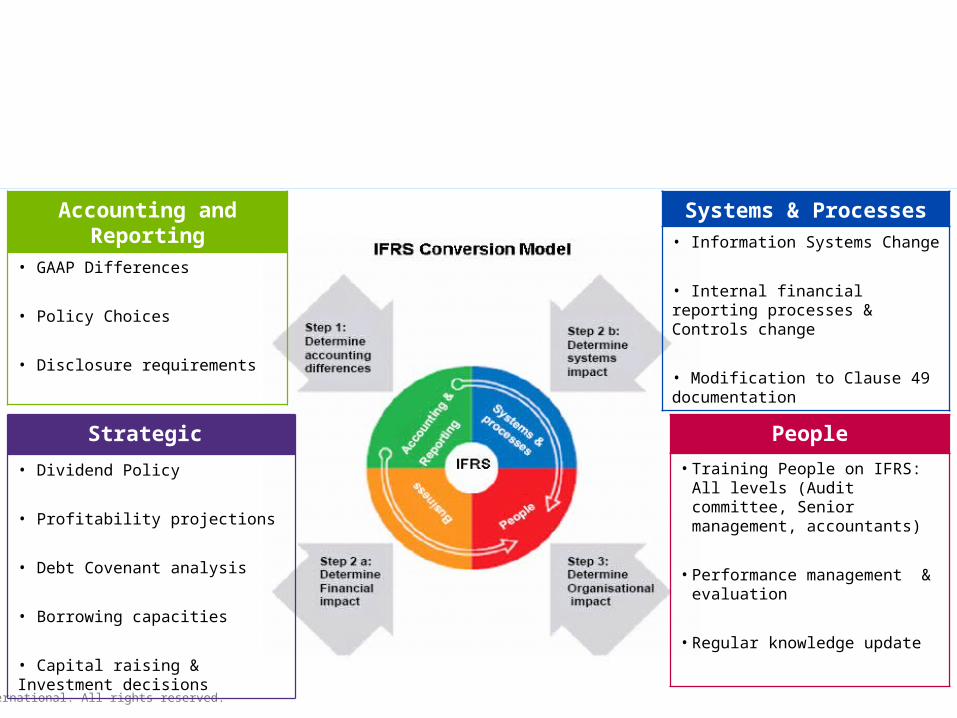

Accounting and Reporting

• GAAP Differences

• Policy Choices

• Disclosure requirements

Systems & Processes• Information Systems Change

• Internal financial reporting processes & Controls change

• Modification to Clause 49 documentation

Strategic

• Dividend Policy

• Profitability projections

• Debt Covenant analysis

• Borrowing capacities

• Capital raising & Investment decisions

People

• Training People on IFRS: All levels (Audit committee, Senior management, accountants)

• Performance management & evaluation

• Regular knowledge update

Impact of convergence

Wider Impact

© Grant Thornton International. All rights reserved.

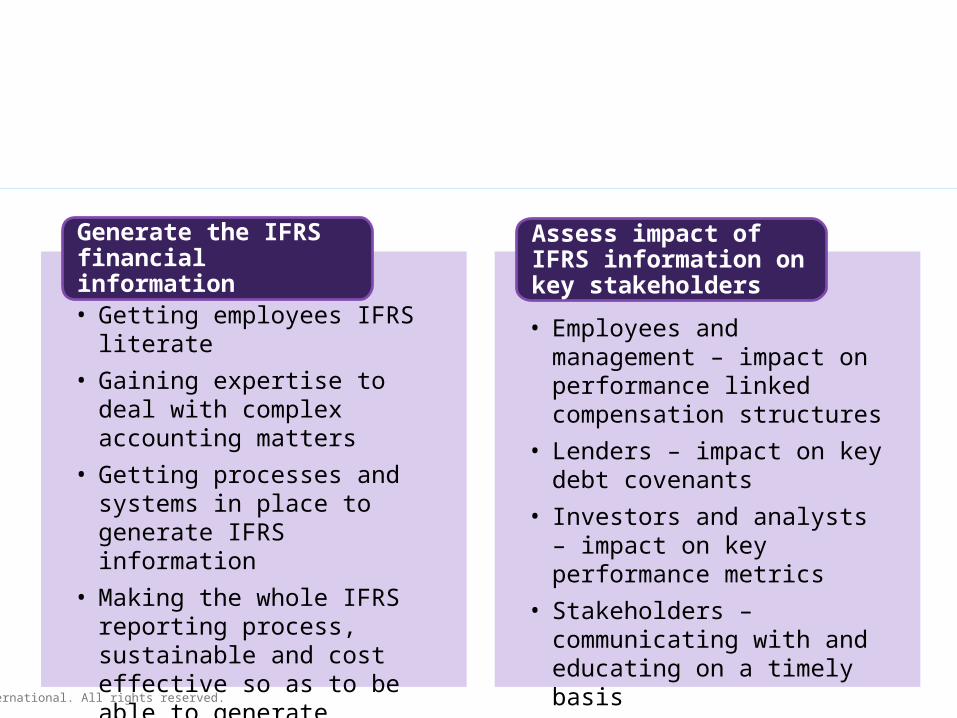

Impact of convergence

Challenges to a enterprise

• Getting employees IFRS literate

• Gaining expertise to deal with complex accounting matters

• Getting processes and systems in place to generate IFRS information

• Making the whole IFRS reporting process, sustainable and cost effective so as to be able to generate information every quarter

Generate the IFRS financial information

• Employees and management – impact on performance linked compensation structures

• Lenders – impact on key debt covenants

• Investors and analysts – impact on key performance metrics

• Stakeholders – communicating with and educating on a timely basis

• Tax authorities – still unclear on how IFRS impacts taxation

Assess impact of IFRS information on key stakeholders

© Grant Thornton International. All rights reserved.

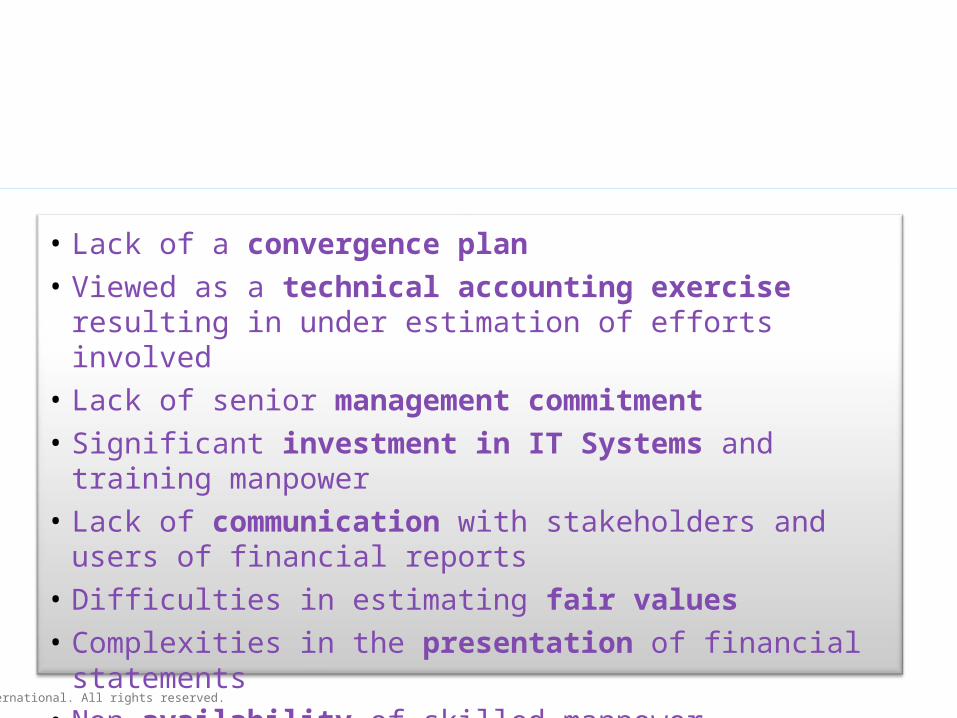

Impact of convergence

Common issues and pitfalls

• Lack of a convergence plan

• Viewed as a technical accounting exercise resulting in under estimation of efforts involved

• Lack of senior management commitment

• Significant investment in IT Systems and training manpower

• Lack of communication with stakeholders and users of financial reports

• Difficulties in estimating fair values

• Complexities in the presentation of financial statements

• Non availability of skilled manpower

© Grant Thornton International. All rights reserved.

Process of transitioning financial Process of transitioning financial reportingreporting

© Grant Thornton International. All rights reserved.

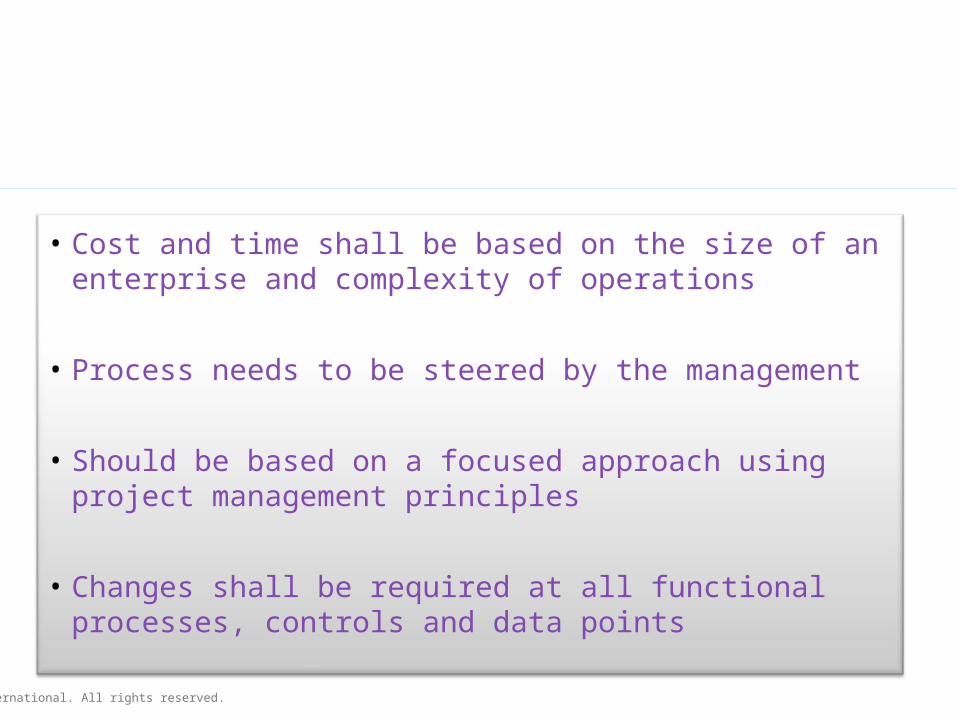

Process of transitioning financial reporting

• Cost and time shall be based on the size of an enterprise and complexity of operations

• Process needs to be steered by the management

• Should be based on a focused approach using project management principles

• Changes shall be required at all functional processes, controls and data points

© Grant Thornton India. All rights reserved.

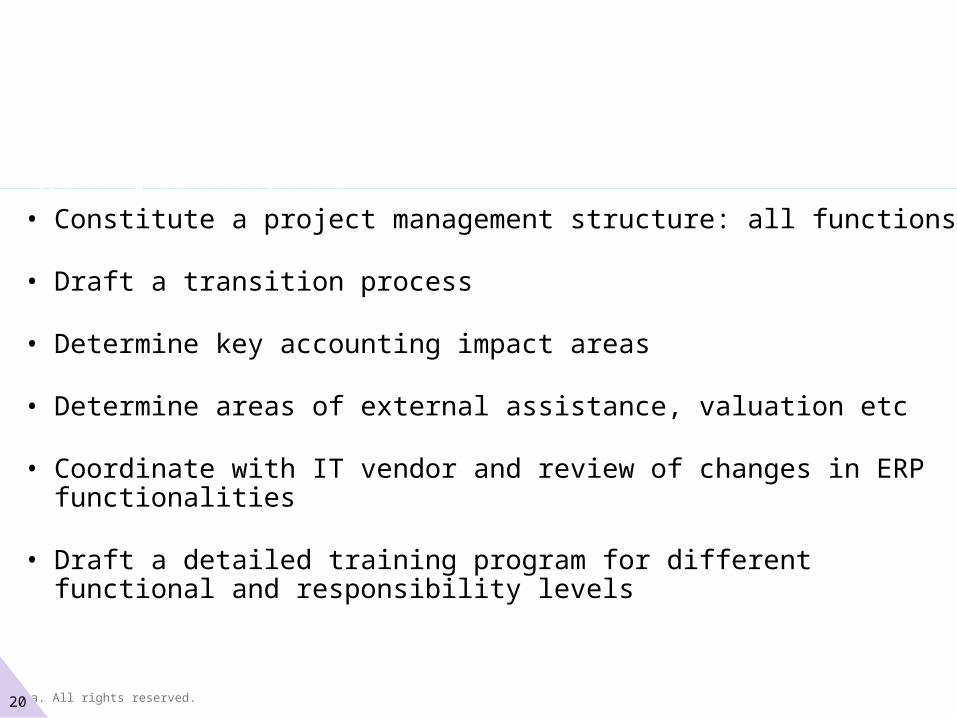

Process of transitioning financial reporting

Key Activities

• Constitute a project management structure: all functions

• Draft a transition process

• Determine key accounting impact areas

• Determine areas of external assistance, valuation etc

• Coordinate with IT vendor and review of changes in ERP functionalities

• Draft a detailed training program for different functional and responsibility levels

20

© Grant Thornton India. All rights reserved.

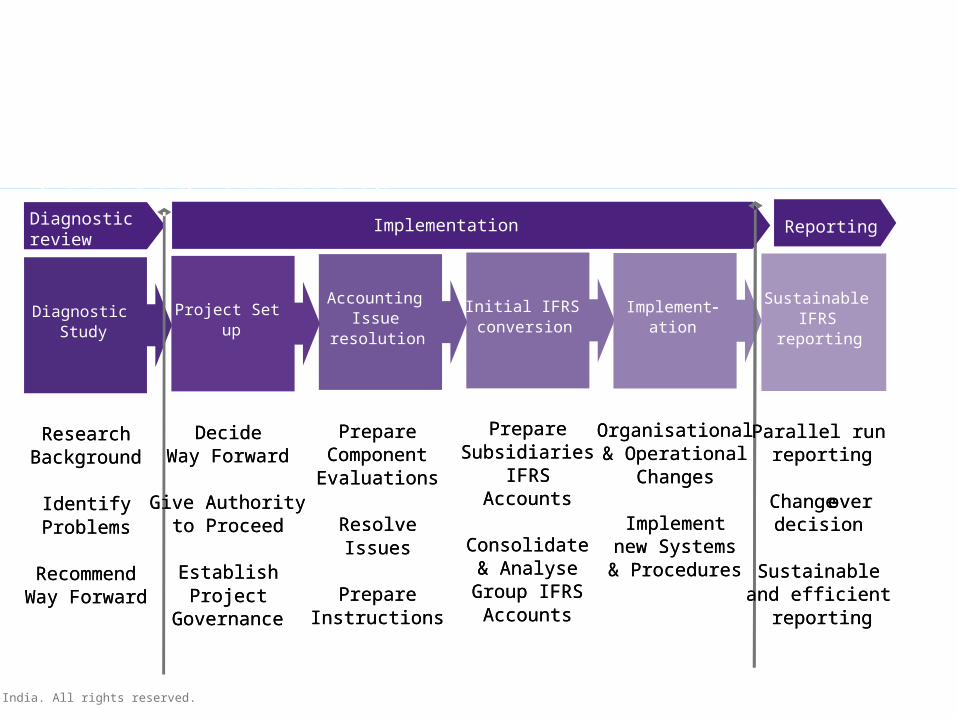

Process of transitioning financial reporting

Focused approach

Diagnostic Study

Sustainable IFRS

reporting

Initial IFRS conversion

Accounting Issue

resolution

Project Set up

Diagnostic review

DecideWay Forward

Give Authorityto Proceed

EstablishProject

Governance

ResearchBackground

IdentifyProblems

RecommendWay Forward

PrepareComponentEvaluations

ResolveIssues

PrepareInstructions

PrepareSubsidiaries

IFRSAccounts

Consolidate& Analyse

Group IFRSAccounts

Organisational& Operational

Changes

Implementnew Systems& Procedures

Implement -ation

Parallel run reporting

Change -over decision

Sustainable and efficient

reporting

Implementation Reporting

DecideWay Forward

Give Authorityto Proceed

EstablishProject

Governance

ResearchBackground

IdentifyProblems

RecommendWay Forward

PrepareComponentEvaluations

ResolveIssues

PrepareInstructions

PrepareSubsidiaries

IFRSAccounts

Consolidate& Analyse

Group IFRSAccounts

Organisational& Operational

Changes

Implementnew Systems& Procedures

-

Parallel run reporting

Change -over decision

Sustainable and efficient

reporting

© Grant Thornton International. All rights reserved.

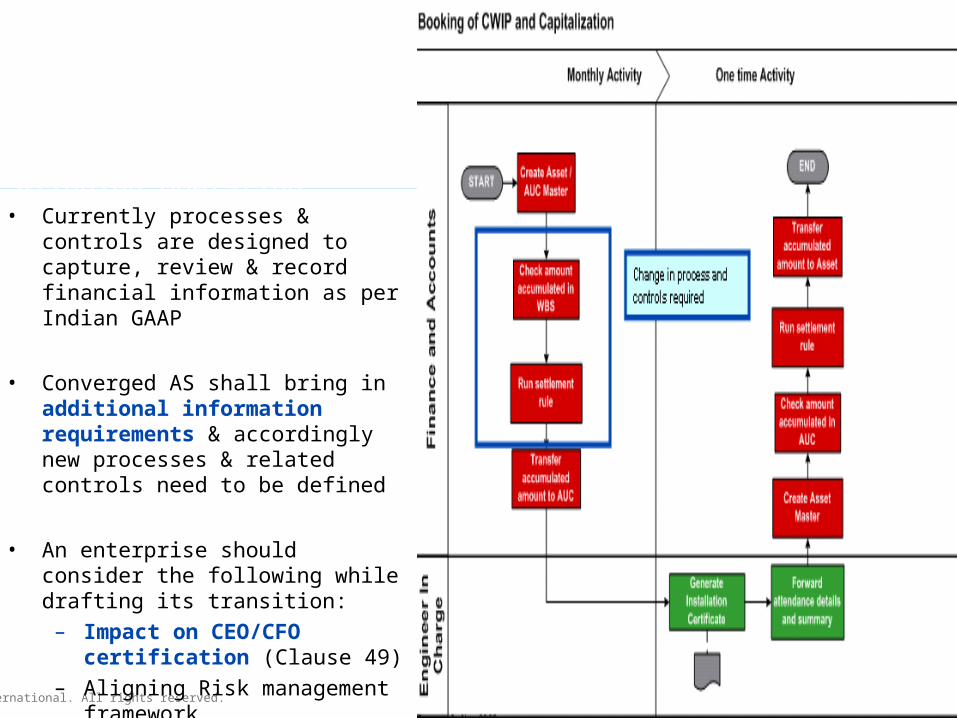

Process of transitioning financial reporting Aligning Operating processes & controls

• Currently processes & controls are designed to capture, review & record financial information as per Indian GAAP

• Converged AS shall bring in additional information requirements & accordingly new processes & related controls need to be defined

• An enterprise should consider the following while drafting its transition:

– Impact on CEO/CFO certification (Clause 49)

– Aligning Risk management framework

– Aligning Internal audit function & activity

© Grant Thornton International. All rights reserved.

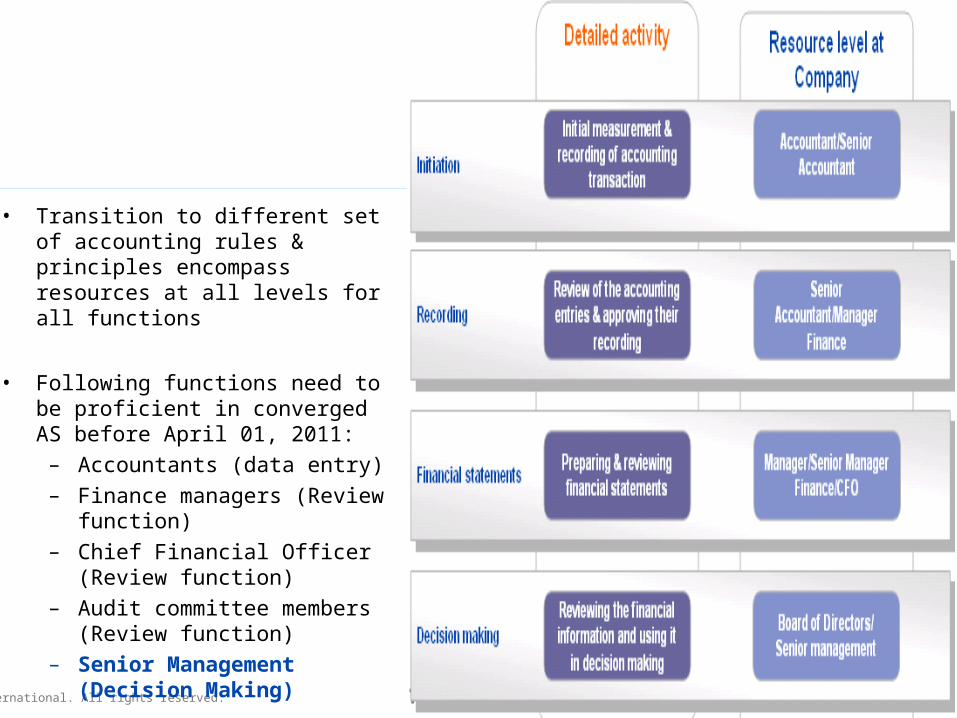

Process of transitioning financial reporting

Human resources needs

• Transition to different set of accounting rules & principles encompass resources at all levels for all functions

• Following functions need to be proficient in converged AS before April 01, 2011:

– Accountants (data entry)– Finance managers (Review

function)– Chief Financial Officer (Review

function)– Audit committee members

(Review function)– Senior Management (Decision

Making)

© Grant Thornton India. All rights reserved.

Process of transitioning financial reporting

Human resources needs – Training programs

Sessions Indicative area of coverage

Induction workshops • Overview of IFRS and impacts• Introduction of Project Team and roles & responsibilities• Discussion on industry specific issues

Workshop for senior management

• Introduction to IFRS and potential impact• Areas of concern and questions they need to be asking to increase awareness• Impact on management reporting and human resources• Times lines, roles and responsibilities & risk management framework

Focused workshop on areas of impact

• Topical sessions run by specialists on detailed impact and way forward• Policy changes and disclosure required by an enterprise • Statement of procedures and interdependencies • Potential change management discussions

Workshop for non accounting personnel

• Introduction to IFRS and potential impacts for their business process• Discussions on specific areas of non accounting impact

24

© Grant Thornton International. All rights reserved.

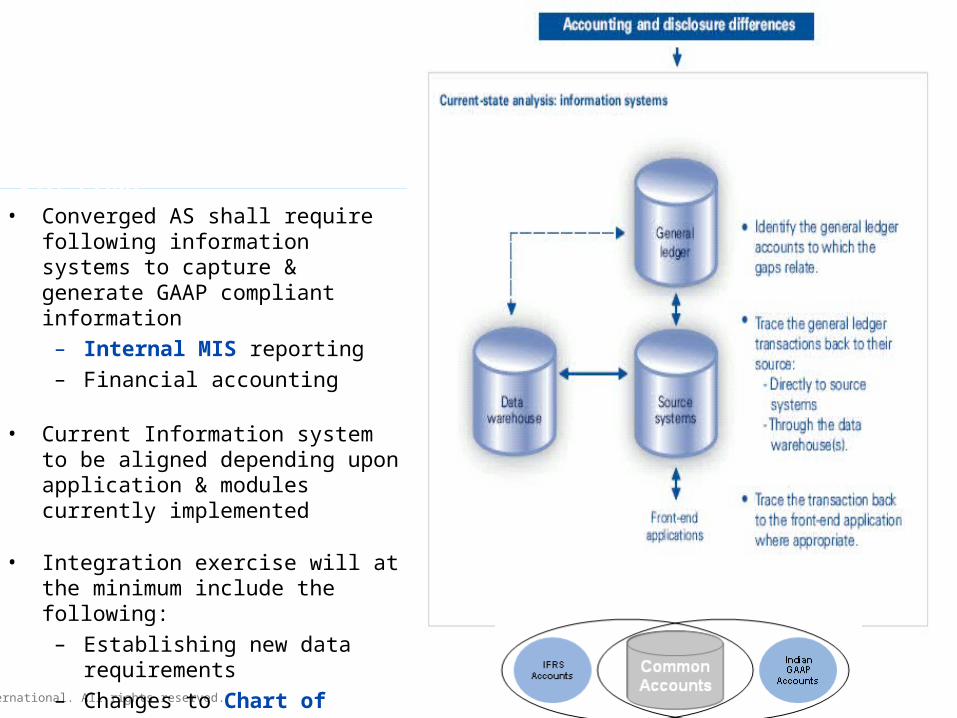

Process of transitioning financial reporting Aligning Information Systems

• Converged AS shall require following information systems to capture & generate GAAP compliant information

– Internal MIS reporting– Financial accounting

• Current Information system to be aligned depending upon application & modules currently implemented

• Integration exercise will at the minimum include the following:

– Establishing new data requirements

– Changes to Chart of Accounts– Re-configuration of applications– Manage parallel systems

© Grant Thornton International. All rights reserved.

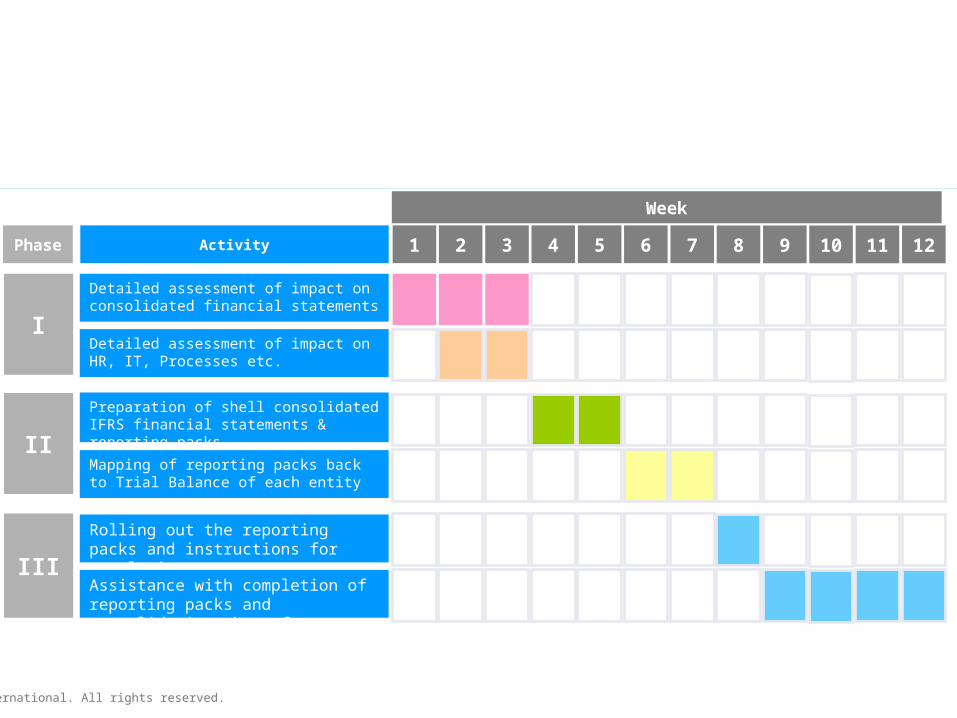

Illustrative timeline

Week

1 2 3 4 5 6 7Activity

Detailed assessment of impact on consolidated financial statements

Detailed assessment of impact on HR, IT, Processes etc.

Preparation of shell consolidated IFRS financial statements & reporting packs

Mapping of reporting packs back to Trial Balance of each entity

Phase 8 9 10 11 12

Rolling out the reporting packs and instructions for completion

Assistance with completion of reporting packs and consolidation thereof

I

II

III

© Grant Thornton International. All rights reserved.

Questions

© Grant Thornton International. All rights reserved.

Thank you

About Grant Thornton International Ltd. (Grant Thornton International)

Grant Thornton International is one of the world’s leading organisations of independently owned and managed accounting and consulting firms. These firms provide assurance, tax and specialist advisory services to privately held businesses and public interest entities. Clients of member and correspondent firms can access the knowledge and experience of more than 2400 partners in over 100 countries and consistently receivea distinctive, high quality and personalised service wherever they choose to do business. Grant Thornton International strives to speak out on issues that matter to business and which are in the wider public interest and to be a bold and positive leader in its chosenmarkets and within the global accounting profession.

Grant Thornton India is a member firm within Grant Thornton International. Grant Thornton International and the member firms are not a worldwide partnership. Services are delivered independently by the member firms.