Embed Size (px)

Citation preview

A

Guide for Members

Designed & produced by Mercer Limited©9376_11

MMC UK Pension Fund

This booklet applies to Marsh employees eligible to join the DC section only. A separate booklet is available for other employees.

DC section Explanatory Booklet

Marsh

Please see overleaf for Definitions

Page

Section 1 How the DC section of the Fund works

1

Section 2 The DC section of the Fund in brief 3

Section 3 The DC section of the Fund in detail 4

Contributions 4

Investment 5

Retirement benefits 6

Early and late retirement 7

Death in service 8

Death after retirement 8

Leaving 9

Section 4 Further information 10

ContentsDefinitions

Annual Allowance is a limit set by the Government on the amount by which your pension benefits and/or pension savings can grow in a year (1 April to 31 March) before being subject to tax. The growth in your benefits can be calculated by adding up the following:

l Any money purchase contributions (e.g. contributions to the DC section of the Fund or AVCs) made by you or paid or credited by the Company during the year; and, if applicable

l The amount by which any defined benefit pension entitlement has increased over the year, multiplied by 10; and, if applicable

l The growth in any other pension savings (excluding statutory revaluation on deferred pension benefits).

The Annual Allowance has been set at £215,000 for the 2006/07 tax year.

Basic Salary is your current annual base salary, excluding car allowances, bonuses or any other benefits.

Children are your children or your Spouse’s children who are financially dependent on you and are under age 18, or under age 23 if still in full-time education (or beyond if mentally or physically disabled).

Company is Marsh & McLennan Companies UK Ltd, the Principal Employer.

Contributing Member is a member who is currently paying contributions to the Fund and building up retirement benefits.

Core Contribution is the minimum contribution payable by you, or payable or credited by the Company to your Individual Account. The Company Core Contribution increases as you get older.

Final Pensionable Salary is the annual average of Pensionable Salary received in the last 24 calendar months of Pensionable Service or, if greater, the best 2 consecutive calendar years out of the last 10 consecutive calendar years.

Fund is the MMC UK Pension Fund.

Fund-specific Salary Cap is the upper limit on the amount of salary that can be taken into account when calculating pensions arising from and contributions payable under the Fund. The limit is normally increased annually.

Individual Account is an account set up in your name whilst contributing to the Fund.

Lifetime Allowance is a limit set by the Government on the amount of pension savings that will qualify for tax relief. This allowance will start at £1.5 million worth of benefits from registered pension arrangements from 2006, rising to £1.8 million in 2010. The Lifetime Allowance will apply to all of the pension benefits you build up over your entire working life and will be triggered by a benefit crystallisation event such as payment of retirement income or death benefits.

Lower Earnings is the level of earnings at which benefits under the State Second Pension start accruing.Limit (LEL) This figure is set by the Government and adjusted each year. It is broadly equal to the Basic

State Pension.

Match Contributions are optional contributions payable by members aged 31 and over in addition to their Core Contribution.

MatchPlus Contributions are contributions paid or credited to your Individual Account on behalf of the Company, in addition to Company Core Contributions, when you opt to pay Match Contributions.

Normal Retirement Age is 65.

Pensionable Salary is your Basic Salary less an amount equal to the LEL. For members working on a part-time basis, the LEL is pro-rated before being deducted. Where members earn over the Fund-specific Salary Cap, Pensionable Salary will be restricted to the Fund-specific Salary Cap less the LEL.

Qualifying Dependant is any adult person who immediately before your death was partly or wholly financially dependent on you.

Reckonable Salary is your annual salary immediately before your date of death or, if greater, the total amount of Pensionable Salary (before the deduction of the LEL) received during the 12 months ending on 31 December immediately before your date of death.

RPI increase means the percentage increase in the Retail Prices Index over a defined 12 month period.

Spouse is your legally married husband or wife. Under the Civil Partnership Act 2004, a registered civil partner will be treated the same as a Spouse for pension purposes.

State Pension Age for men is 65. For women born:

l before 6 April 1950 it is 60; l after 5 April 1955, it is 65; l between 6 April 1950 and 5 April 1955 it is on a sliding scale between 60 and 65.

State Second provides a pension in addition to the Basic State Pension. As a member of the DC sectionPension (S2P) of the Fund you participate fully in S2P.

Upper Earnings Limit (UEL) is the level of earnings at which benefits under the State Second Pension cease accruing. It is adjusted by the Government each year.

1

The Company believes that the provision of apension fund is an important part of your pay andbenefits package and offers a flexible pensionarrangement designed to help you plan for the futurewith confidence, whatever your age or personalcircumstances.

The purpose of the DC section of the Fund is to:

l give you a secure income when you retire

l provide financial protection for you and yourdependants should you die before retirement.

Who can joinThe Fund provides benefits on a ‘definedcontribution’ (DC) or ‘money purchase’ basis and isopen to all employees* under age 63, as notified bythe Company.

If you are a permanent employee, you will beautomatically entered into the Fund unless youindicate to the contrary (see “Opting out of the Fund”on page 10). If you are employed on a temporarycontract, you will be advised by the Companywhether you are eligible to join the Fund and willneed to complete an application form to join.

DefinitionsCertain terms have special meanings which are givenin a table of definitions on the fold out flap at theback of this guide. Where a defined word is used inthe main text it appears in italics.

ContributionsBoth your own and those contributions paid orcredited to you on behalf of the Company areallocated to an Individual Account in your name. This money will be invested on your behalf and thevalue of the fund you have built up will be used toprovide your benefits at retirement.

Annual statementEach year you will receive a personal statementshowing the value of your Individual Account, thecontributions credited or paid into it during the yearand the estimated pension that could possibly beprovided. The estimated pension will be based onexpected future investment returns, among otherfactors. You will be able to request a Fund annualreport with more details and performance figures.

Benefits from the FundYour pension, and any pension for a Spouse, Childrenor Qualifying Dependant, will be payable through anannuity bought from an insurance company. Thepension you receive will normally be paid in monthlyinstalments, direct to your bank account. Pensionsare subject to income tax and, if appropriate, this willbe deducted before payment.

In addition, subject to your National Insurancecontribution history, you should also receive theBasic State Pension and the pension you haveearned under State Second Pension (S2P) from State Pension Age (see page 13).

Transfer of pension from a previous arrangementTransfers from previous pension schemes are notbeing accepted into the Fund.

How the DC sectionof the Fund works

Section 1

*New employees of the Marsh Affinity Benefits call centre arenot eligible to join the Fund. Instead access to a stakeholderpension arrangement will be provided.

Expression of Wish formsOne of the duties of the Trustee is to decide whoshould receive any lump sum if a member dies. To help the Trustee make this decision, you shouldcomplete the Expression of Wish form whichaccompanies this guide if you have not already doneso. Although the Trustee is not bound to follow yourwishes it will take them into account. You should atall times ensure that your Expression of Wish form isup-to-date.

If you wish to change your beneficiaries, you shouldcomplete a new form immediately. Forms can bedownloaded from the Fund website, details of whichcan be found below.

Leaving the FundIf you leave the DC section of the Fund, no furthercontributions will be made, either by the Companyor by you. Details of the benefits payable from theDC section of the Fund on leaving can be found on page 9.

Administrator contact details:

MMC UK Pension FundPO Box 476Westgate House52 WestgateChichesterPO19 3WZ

Tel: 0845 6000293Fax: 01243 522001Email: [email protected]: www.pensions.uk.mmc.com

2

3

Section 2

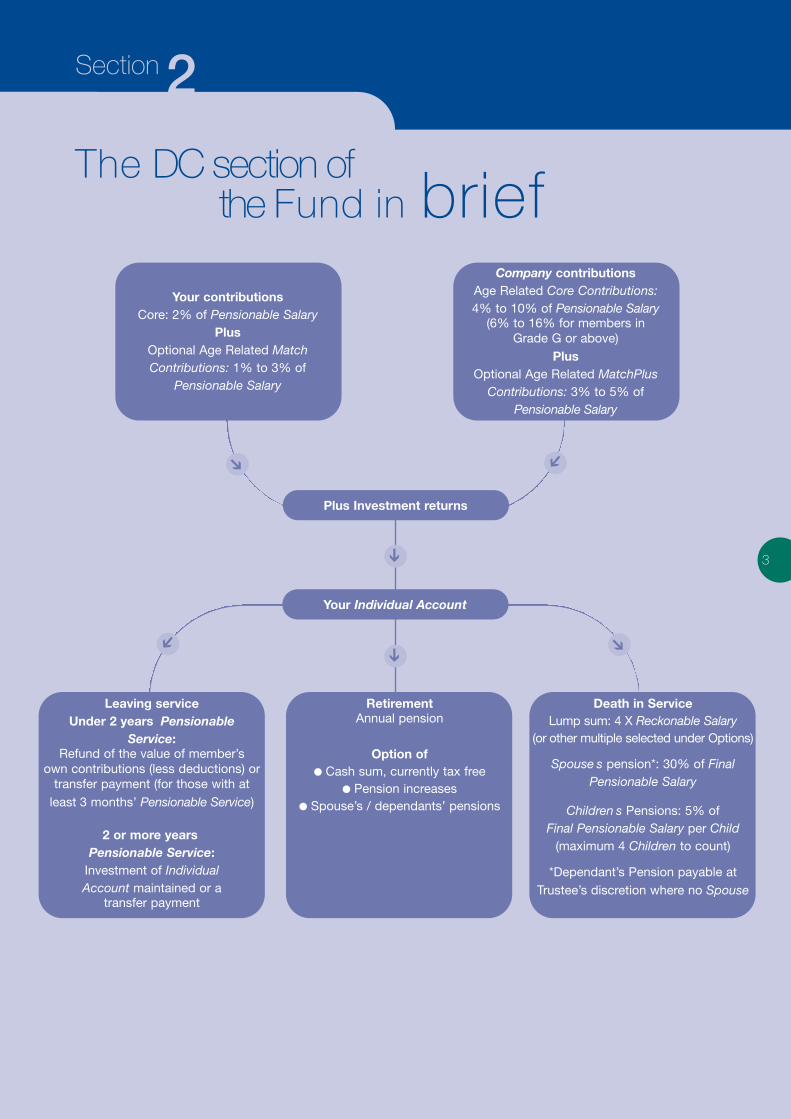

The DC section of the Fund in brief

Plus Investment returns

Company contributionsAge Related Core Contributions:4% to 10% of Pensionable Salary

(6% to 16% for members in Grade G or above)

PlusOptional Age Related MatchPlus

Contributions: 3% to 5% ofPensionable Salary

Your contributionsCore: 2% of Pensionable Salary

PlusOptional Age Related MatchContributions: 1% to 3% of

Pensionable Salary

Ô

Ô

ÔÔ

Death in ServiceLump sum: 4 X Reckonable Salary

(or other multiple selected under Options)

SpouseÕs pension*: 30% of FinalPensionable Salary

ChildrenÕs Pensions: 5% of Final Pensionable Salary per Child

(maximum 4 Children to count)

*Dependant’s Pension payable atTrustee’s discretion where no Spouse

RetirementAnnual pension

Option ofl Cash sum, currently tax free

l Pension increasesl Spouse’s / dependants’ pensions

Leaving serviceUnder 2 yearsÕ Pensionable

Service:Refund of the value of member’s

own contributions (less deductions) ortransfer payment (for those with at

least 3 months’ Pensionable Service)

2 or more yearsÕ Pensionable Service:

Investment of Individual Account maintained or a

transfer payment

Your Individual Account

Ô

Ô

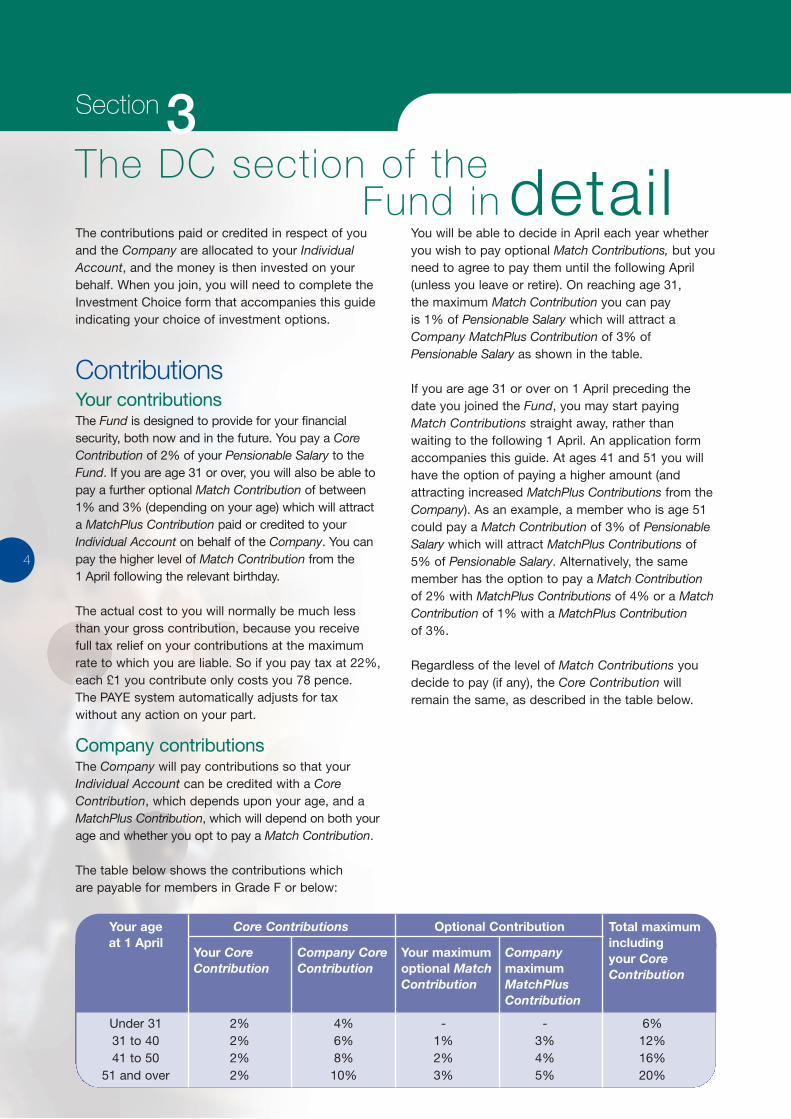

The contributions paid or credited in respect of youand the Company are allocated to your IndividualAccount, and the money is then invested on yourbehalf. When you join, you will need to complete theInvestment Choice form that accompanies this guideindicating your choice of investment options.

ContributionsYour contributionsThe Fund is designed to provide for your financialsecurity, both now and in the future. You pay a CoreContribution of 2% of your Pensionable Salary to theFund. If you are age 31 or over, you will also be able topay a further optional Match Contribution of between1% and 3% (depending on your age) which will attracta MatchPlus Contribution paid or credited to yourIndividual Account on behalf of the Company. You canpay the higher level of Match Contribution from the1 April following the relevant birthday.

The actual cost to you will normally be much lessthan your gross contribution, because you receivefull tax relief on your contributions at the maximumrate to which you are liable. So if you pay tax at 22%,each £1 you contribute only costs you 78 pence.The PAYE system automatically adjusts for taxwithout any action on your part.

Company contributionsThe Company will pay contributions so that yourIndividual Account can be credited with a CoreContribution, which depends upon your age, and aMatchPlus Contribution, which will depend on both yourage and whether you opt to pay a Match Contribution.

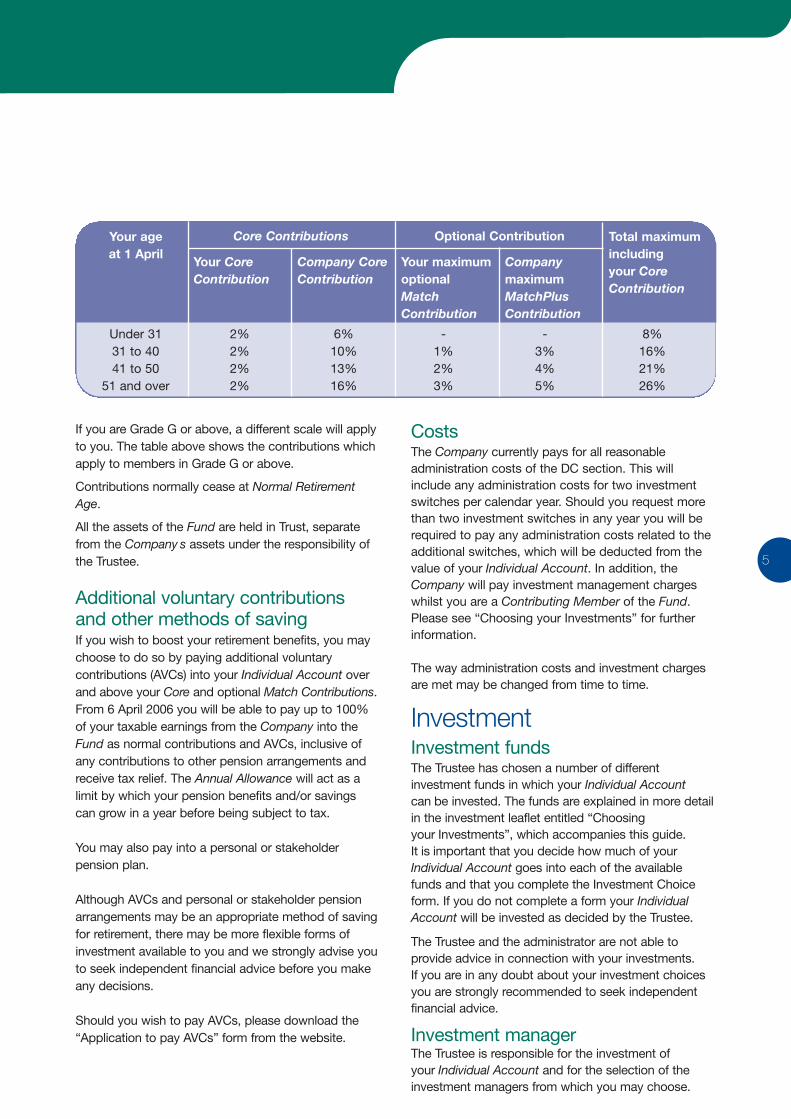

The table below shows the contributions which are payable for members in Grade F or below:

You will be able to decide in April each year whetheryou wish to pay optional Match Contributions, but youneed to agree to pay them until the following April(unless you leave or retire). On reaching age 31,the maximum Match Contribution you can pay is 1% of Pensionable Salary which will attract aCompany MatchPlus Contribution of 3% ofPensionable Salary as shown in the table.

If you are age 31 or over on 1 April preceding thedate you joined the Fund, you may start payingMatch Contributions straight away, rather thanwaiting to the following 1 April. An application formaccompanies this guide. At ages 41 and 51 you willhave the option of paying a higher amount (andattracting increased MatchPlus Contributions from theCompany). As an example, a member who is age 51could pay a Match Contribution of 3% of PensionableSalary which will attract MatchPlus Contributions of5% of Pensionable Salary. Alternatively, the samemember has the option to pay a Match Contributionof 2% with MatchPlus Contributions of 4% or a MatchContribution of 1% with a MatchPlus Contributionof 3%.

Regardless of the level of Match Contributions youdecide to pay (if any), the Core Contribution willremain the same, as described in the table below.

4

Section 3The DC section of the

Fund in detail

Your age at 1 April

Your CoreContribution

Company CoreContribution

Your maximumoptional MatchContribution

CompanymaximumMatchPlusContribution

Total maximumincluding your CoreContribution

Core Contributions Optional Contribution

Under 31 2% 4% - - 6%31 to 40 2% 6% 1% 3% 12%41 to 50 2% 8% 2% 4% 16%

51 and over 2% 10% 3% 5% 20%

5

Your age at 1 April

Your CoreContribution

Company CoreContribution

Your maximumoptionalMatchContribution

CompanymaximumMatchPlusContribution

Total maximumincludingyour CoreContribution

Core Contributions Optional Contribution

Under 31 2% 6% - - 8%31 to 40 2% 10% 1% 3% 16%41 to 50 2% 13% 2% 4% 21%

51 and over 2% 16% 3% 5% 26%

If you are Grade G or above, a different scale will applyto you. The table above shows the contributions whichapply to members in Grade G or above.

Contributions normally cease at Normal RetirementAge.

All the assets of the Fund are held in Trust, separatefrom the CompanyÕs assets under the responsibility ofthe Trustee.

Additional voluntary contributionsand other methods of savingIf you wish to boost your retirement benefits, you maychoose to do so by paying additional voluntarycontributions (AVCs) into your Individual Account overand above your Core and optional Match Contributions.From 6 April 2006 you will be able to pay up to 100%of your taxable earnings from the Company into theFund as normal contributions and AVCs, inclusive ofany contributions to other pension arrangements andreceive tax relief. The Annual Allowance will act as alimit by which your pension benefits and/or savingscan grow in a year before being subject to tax.

You may also pay into a personal or stakeholderpension plan.

Although AVCs and personal or stakeholder pensionarrangements may be an appropriate method of savingfor retirement, there may be more flexible forms ofinvestment available to you and we strongly advise youto seek independent financial advice before you makeany decisions.

Should you wish to pay AVCs, please download the“Application to pay AVCs” form from the website.

CostsThe Company currently pays for all reasonableadministration costs of the DC section. This willinclude any administration costs for two investmentswitches per calendar year. Should you request morethan two investment switches in any year you will berequired to pay any administration costs related to theadditional switches, which will be deducted from thevalue of your Individual Account. In addition, theCompany will pay investment management chargeswhilst you are a Contributing Member of the Fund.Please see “Choosing your Investments” for furtherinformation.

The way administration costs and investment chargesare met may be changed from time to time.

InvestmentInvestment fundsThe Trustee has chosen a number of differentinvestment funds in which your Individual Accountcan be invested. The funds are explained in more detailin the investment leaflet entitled “Choosingyour Investments”, which accompanies this guide.It is important that you decide how much of yourIndividual Account goes into each of the availablefunds and that you complete the Investment Choiceform. If you do not complete a form your IndividualAccount will be invested as decided by the Trustee.

The Trustee and the administrator are not able toprovide advice in connection with your investments.If you are in any doubt about your investment choicesyou are strongly recommended to seek independentfinancial advice.

Investment managerThe Trustee is responsible for the investment ofyour Individual Account and for the selection of theinvestment managers from which you may choose.

Retirement benefitsAny examples given to you concerning the value ofyour Individual Account or your possible benefits atretirement depend on the assumptions made aboutcontribution levels, investment returns and the costof buying a pension when you retire. Whether theexamples accurately predict the benefits ultimatelypayable depends on whether these assumptions areborne out in practice. The amount of your benefitscannot be guaranteed.

Choosing your benefits at retirementYour pension, and any pension for a Spouse, Childrenor Qualifying Dependant, will be payable through anannuity bought from an insurance company. You willbe given details shortly before retirement of the optionsand costs of converting your Individual Account into apension and the fees for arranging this. At retirementyou will need to decide the form of benefits you wishto provide for yourself and your dependants. Theprocess of setting up your pension may take severalweeks because of the procedures involved. You canhelp to reduce this delay by telling the Trustee whichoptions you want to take and by returning any formsas soon as possible.

Your retirement benefits may include the following:

l Five year guarantee

If you die within the first five years of yourretirement, the unpaid balance of five years’pension payments will be paid to yourdependants or estate as a lump sum.

l SpouseÕs/DependantsÕ pensions

l Pension increases

You may use your Individual Account to buy apension with any level of pension increases ornone at all.

l Cash sum

You may be able to take up to 25% of the valueof your Individual Account (including any AVCs)as a cash sum when you retire, subject to amaximum of 25% of the Lifetime Allowance.

Under current legislation your cash sum willbe tax free unless the value of your benefitsfrom all pension arrangements exceeds theLifetime Allowance.

You should note, however, that any cash you takewill reduce the amount available in your IndividualAccount to purchase your pension.

If you have built up benefits above the LifetimeAllowance they will be subject to additional tax, whichmay be deducted from your benefits or collectedthrough self-assessment tax returns.

The Government will allow employees to protect theirpension rights where they are likely to have benefitsthat are in excess of the Lifetime Allowance. However,this is a complex area and you should contact anindependent financial adviser for further information.

6

7

MMC UK Pension Fund

Early and late retirementChoosing to retire early from Company serviceCurrently, you may choose to retire with animmediate pension from the Fund at any time afteryour 50th birthday, subject to the agreement of theCompany and the Trustee, although you should notethat, from 6 April 2010, the earliest age at which itwill be possible to start receiving your pension willincrease to 55. Your benefits will depend on the valueof your Individual Account, the sort of pension youchoose and the cost of buying a pension at the timeyou retire.

Generally speaking, the younger you are when youretire the shorter the time your Individual Account willhave been invested and the more it will cost to buyeach £1 of pension per annum. So, if you plan toretire early, you should ensure your financial planningmeets your retirement needs. To assist you in thisyou may wish to seek independent financial advice.

Retiring early on medical groundsThe Company operates an Income ProtectionScheme, which may provide an income on disability,subject to insurer acceptance. This benefit is notprovided from the Fund. Full details are availablefrom your Human Resources department.

Under exceptional circumstances, it may be possiblefor you to retire with an immediate ill-health pensionfrom the Fund. The pension may be reduced due tothe higher cost of buying the pension at an earlier age.If the cost of annuities is high, this may result in alower pension, depending on your age and the natureof your illness.

Provision of an ill-health pension is subject to theconsent of the Company and the Trusteee and theprovision of appropriate medical evidence.

Late retirementEmployment after Normal Retirement Age is entirely atthe discretion of the Company. If the Company wereto exercise this discretion, your own and thecontributions paid or credited to your account on theCompanyÕs behalf will cease. Your Individual Accountwill normally remain invested and will be used topurchase a pension at your actual retirement date.

AVC benefits – deferred paymentWhen you retire and start taking your main benefitsunder the Fund, you may defer taking your AVCbenefits up to, but not beyond, your 75th birthday.Your AVCs will remain invested during any periodof deferment.

If you die while you are receiving your main benefitsbut deferring your AVCs, the AVCs will normally bepaid as an additional lump sum death benefit asdecided by the Trustee.

You cannot normally pay any further AVCs to theFund once you retire.

There are possible financial risks in choosing thisoption. Your AVCs that remain invested may not growas you hope. When you wish to use the AVCs toprovide retirement benefits, the cost of doing so mayhave increased. Before choosing to defer payment ofAVC benefits, you may want to obtain independentfinancial advice on whether this is a suitable optionfor you.

8

MMC UK Pension Fund

Death in serviceIf you die in service as a Contributing Member of the DC section of the Fund the following benefits willbe payable:

Death in service lump sumThe core death in service lump sum is equal to 4 times your Reckonable Salary at the date of yourdeath (together with the value of any AVCs you havemade) although you may select a different multiplethrough Options, subject to a maximum of theLifetime Allowance. It is important that you completean Expression of Wish form to assist the Trustee inthe distribution of this lump sum payment. Pleaserefer to the section on ‘Inheritance tax’ on page 14for further details of how this benefit will be paid.

If you earn in excess of the Fund-specific Salary Cap,your total death in service lump sum will be equal to4 times your uncapped Reckonable Salary (or othermultiple as selected through Options), subject to amaximum of the Lifetime Allowance. Any lump sumbenefits payable on your death will be paid from theFund where possible. You will be advised separatelyif any of your cover will be provided outside the Fund.

Spouse’s pensionYour Spouse will receive a pension equivalent to 30%of your Final Pensionable Salary at the date of death.If, at the date of your death, your Spouse is at least 15 years younger than you, the pension may be reduced.

Children’s pensionsIn addition to the SpouseÕs pension, ChildrenÕspensions are payable for up to a maximum of4 Children. Each Child will receive a pension of 5% of your Final Pensionable Salary at date of death.

This pension will stop once the Child reaches age 18 (or 23 if in full-time education). It can continuebeyond this age if, at the time of your death, theChild was dependent on you through physical ormental impairment.

Dependant’s pensionIf you do not have a Spouse, the Trustee may chooseto pay a pension to a Qualifying Dependant wherethere is financial interdependency at the date of yourdeath, subject to certain criteria.

Any pension paid to a Spouse, Qualifying Dependantor Child will be subject to income tax but its valuedoes not count towards your Lifetime Allowance orthe recipient’s own Lifetime Allowance.

Death after retirementIn the event of your death after retirement, yourdependants will be entitled to the benefits youspecified on retirement (see page 6). For example:

l When you retired you may have chosen to have apension that pays a lump sum if you were to diewithin 5 years of your pension starting.

l Alternatively, you may have chosen to have apension with no lump sum payable on death.

l You may have chosen to provide a pensionpayable to a Spouse, Qualifying Dependant orChildren upon your death.

l You may have chosen to buy a pension with anylevel of annual increase, or none at all and anypension payable to a Spouse, QualifyingDependant or Child will be increased accordingly.

Pension increasesThe timing of any annual increases applied to the pension will be determined by the insurancecompany with whom the pension has beenpurchased.

9

LeavingIf you leave the Fund, your own contributions and thecontributions paid or credited to you on behalf of theCompany will cease.

Less than two years’ Pensionable ServiceLess than 3 monthsÕ Pensionable ServiceYou will be entitled to a refund of the value of yourIndividual Account built up from your own Core andMatch Contributions together with any AVCs, less tax.

More than 3 monthsÕ but less than 2 yearsÕPensionable ServiceYou will be entitled to a refund of the value of yourIndividual Account as described above. As analternative to taking a refund, you may transfer thevalue of your Individual Account to another pensionarrangement. You will receive a transfer valuequotation when you leave and you will have threemonths in which to decide whether to transfer yourpension or to take the cash refund less deductions.See “Transferring your Individual Account” in the nextcolumn for further details.

You may not leave your Individual Account in the Fund.

Two or more years’ Pensionable ServiceYour Individual Account will remain invested until yourNormal Retirement Age and a pension will be boughtat that time. On leaving the Fund, investmentmanagement charges will, going forward, be deductedfrom your Individual Account. In practice this meansyour Individual Account will, going forward, be switchedinto funds where the investment managementcharges are reflected in the price.

As an alternative to leaving your Individual Accountinvested in the Fund, you may transfer it to anotherpension arrangement.

You may ask the Trustee for a statement of the valueof your Individual Account at any time. The Fund isnot obliged to provide another statement within 12 months of the date of your last request.

Transferring your Individual AccountYou may ask the Trustee to transfer the value of yourIndividual Account to one of the following pensionarrangements as long as the transfer takes place atleast one year before your Normal Retirement Age:

l a registered pension plan with your new employer;or

l a registered approved personal or stakeholderpension plan of your choice, or

l an individual insurance policy in your name(commonly known as a “buy-out” policy).

The transfer value will be equal to the value of yourIndividual Account at the date of transfer. If you have made any AVCs, their value will be in addition to the transfer value. A deduction may be madefor expenses.

You should seek independent financial advice beforeproceeding with a transfer.

Death before retirementIf you leave the Company but keep your benefits inthe Fund, the full value will be used to provide apension for your Spouse or Qualifying Dependant andChildren in the event of your death before retirement.

Looking after your interestsThe Fund is established under a trust andadministered by a corporate trustee, MMC UKPension Fund Trustee Ltd. Amongst other things,this means that the FundÕs assets are legally separatefrom those of the Company and the Trustee isresponsible for ensuring that members’ interests areprotected, as required by law. The administration ofbenefits and the investment of the FundÕs assets fallwithin the responsibility of the Trustee.

The members of the board of MMC UK Pension FundTrustee Ltd serve as individual Trustee Directors.Most of the Trustee Directors are appointed by theCompany but at least a third of them are MemberRepresentative Trustee Directors (“MRTDs”).The procedure for appointing MRTDs is throughtheir nomination by the Pensions Forum from amongits elected staff members and subject to approval bythe other Trustee Directors. The Pensions Forum isa committee established by MMC UK Pension FundTrustee Ltd., to which a number of active members ofthe Fund and pensioners are elected by active Fundmembers and pensioners from the same constituency.

You can contact the Trustee through theadministrator at the address on page 2.

Keeping you in the pictureKnowing where you stand with your pension is veryimportant. As a Contributing Member of the Fund,you will be sent regular information designed to keepyou in the picture about your benefits and the Fund in general. You will also receive details of specificchanges, events and options relating to the Fund.

Opting out of the FundIf you are employed on a permanent contract, youwill be automatically entered into the Fund unlessyou indicate to the contrary.

You may decide not to join the Fund at all or to optout at a later date and make your own pensionarrangements. This decision should not be takenlightly and you are encouraged to take independentfinancial advice before doing so as the Company willno longer provide pension benefits for you or yourdependants, other than standard benefits for leavers(see page 9) in respect of any benefits accrued to thedate of opt out. Your core level of life assurancecover will remain at 4 times your Reckonable Salary,although you may select a different multiple throughOptions.

Should you decide to opt out of the Fund, you willneed to complete a form, which can be obtainedfrom the administrator at the address shown on page 2. If you wish to rejoin the Fund subsequently,you will only be able to do so with the CompanyÕsand the Trustee’s consent, and you may be subjectto special terms.

If you leave the Fund to take out a personal orstakeholder pension arrangement the Company willnot contribute towards it on your behalf. For furtherinformation, you should contact the administrator atthe address on page 2.

10

Section 4

Further information

11

MMC UK Pension Fund

Staying in touchKeeping in touch while you are with the Company isone thing, but it’s easy to lose touch if you move on.

If you leave the Company and your benefits remain in the Fund, the Trustee will keep a record of your lastknown address so that you can be contacted aboutyour benefits or any issues affecting the Fund.It is important that you keep the administratorinformed of any change of address once you have left.

If for any reason you lose track of the Trustee’s or theCompanyÕs address, you will be able to contact themthrough the Pension Tracing Service. In common withother pension schemes, the Trustee providesinformation about the Fund, including a contactaddress for inclusion in a pension registry.

The address to write to is:

Pension Tracing ServiceTyneview ParkWhitley RoadNewcastle upon TyneNE98 1BA

Help at handThe aim of the Trustee is to give you clear,straightforward information which is timely andeasy to understand. However, communication is atwo way process and we recognise that there may beoccasions when there are questions you want to ask,or issues you would like to discuss with someone.In the first instance, please contact the administratorat the address on page 2.

Seeing eye to eyeMost queries or problems can be dealt with andresolved, informally, as they arise. However, in rarecases a disagreement may occur which requires amore formal procedure for its resolution. In thesecircumstances a formal request may be made toinvoke the FundÕs Internal Dispute ResolutionProcedure (IDRP).

The IDRP does not apply to disputes betweenemployees and the Company, or the Company andthe Trustee. Also, it cannot be used for complaintsor disputes which are already the subject of courtproceedings or under investigation by the PensionsOmbudsman.

The IDRP is a two-stage process. Under the firststage your complaint or dispute will be consideredand decided upon by the Pensions Manager of theMMC UK Pension Fund. If you are happy with thedecision, the process ends there. However, if youare not satisfied with the result of the first stage,you will have six months in which to ask the Trusteeto reconsider and decide upon your complaint understage two. Normally, a decision under either stagewill be made within two months.

Complaints and appeals must be made in writingand must provide some specific information. If youare unable, or you do not wish, to make the complaintor an appeal yourself, you can nominate someoneelse to act on your behalf.

The Trustee aims to make the need for formalcomplaints the exception rather than the rule.However, should the need arise, full details of theprocedure are available from the administrator atthe address on page 2.

Outside helpIn addition to the FundÕs own arrangements, theGovernment has established two independentagencies to help, should an issue arise which cannotbe resolved directly between a pension scheme anda member or beneficiary. They are The PensionsAdvisory Service (TPAS) and the PensionsOmbudsman. TPAS is available to assist membersand beneficiaries of the Fund in connection withqueries at any time, or difficulties encountered at anystage of the disputes procedure. TPAS will offeradvice on a particular case and, if necessary, mayrefer it to the Pensions Ombudsman who acts as anindependent arbitrator in disputes between pensionschemes and their members.

The address of both TPAS and the PensionsOmbudsman is:

11 Belgrave RoadLondonSW1V 1RB

The Pensions RegulatorThe Pensions Regulator was set up by the PensionsAct 2004 to help ensure that work-based pensionschemes in the UK are properly run. It is able tointervene in the running of schemes where trustees,employers or professional advisers have failed in theirduties. The Pensions Regulator can be contacted atthe following address:

The Pensions RegulatorNapier HouseTrafalgar PlaceBrightonEast SussexBN1 4DW

Tel: 0870 606 3636Email: [email protected]: www.thepensionsregulator.gov.uk

Data protection legislationThe Trustee works together with the Company toprovide the benefits as set out in this guide.The information shared will be used to administer anybenefits under the Fund. Only such details as arerequired to fulfil obligations to members and legaland regulatory obligations will be collected andstored. Your personal data will be treated in strictestconfidence and will only be disclosed to others inlimited circumstances, for example to productproviders in the course of preparing or implementingadvice or to meet legal or regulatory requirements.

Where you are asked to supply information relating to your dependants, you should inform thoseindividuals first; they might like to read this guide to find out how personal data is handled. Whereinformation from your doctor is required, this will notbe sought without your permission. If you have afinancial representative or independent financialadviser, the Trustee will liaise with that person or firmand share information only on your writteninstructions. If you die while you are a member of theFund the Trustee will liaise with your personalrepresentative(s), relatives and possibly your workcolleagues who may supply us with informationrelating to you. If information is used to conductstatistical analysis and surveys, you would not beidentified personally.

Please note that all the information asked for isnecessary and without it the Trustee would not beable to administer your benefits under the Fund.

Supplementary fund Any assets in the DC section of the Fund which arenot allocated to a particular member’s IndividualAccount and AVCs are held in a supplementary fundwithin the Fund. This fund, or any other assets of theFund, may from time to time be used to credit amember’s Individual Account with the contributionsdue from the Company.

12

MMC UK Pension Fund

The State Pension SchemeThe State Pension Scheme is in two parts:

l the Basic Pension (the “old age” pension) which isa flat-rate pension paid to everyone who has paidenough National Insurance contributions, and

l the State Second Pension (S2P) which is based on an employee’s earnings between a Lower andan Upper Earnings Limit throughout his or herworking life.

State pensions are paid from State Pension Age,which is currently 65 for men, 60 for women.

However, a common State Pension Age of 65, forboth men and women, is being phased in by theGovernment between the years 2010 and 2020.

As a member of the Fund you will participate fully inthe State Pension Scheme, so you will be entitled toreceive the Basic State Pension, subject to a fullNational Insurance record, and to earn benefits in theState Second Pension which are payable from StatePension Age.

You may obtain a forecast from the Department forWork and Pensions (DWP) of how much pension youare likely to receive from the State. This can be doneat any time by completing Form BR19, available fromyour local Benefits Agency office, and returning it tothe DWP.

Temporary absenceIf you stop receiving contractual pay or statutory sickpay, your membership of the Fund may, under certaincircumstances, be continued with the CompanyÕs andthe Trustee’s consent.

Ordinary maternity leaveDuring ordinary maternity leave (the first 26 weeks ofmaternity leave) your membership of the Fund,including your cover for death benefits, will becontinued. Your contributions to your IndividualAccount will also be continued, but will be based onyour actual pay, not the pay you would have receivedhad you been working normally. The Company willmake up any difference in your Core Contributions(and any Match Contributions that you have electedto pay) and will continue to pay Companycontributions based on the pay you would havereceived had you been working normally.

Additional maternity leaveAny additional maternity leave that you take will beunpaid. Your own and the CompanyÕs CoreContributions (and any Match Contributions that youhave elected to pay) will stop during this period butyou may be able to make up your missedcontributions (and thereby the associated Companycontributions) when you return to work. Your deathbenefits will be continued during this period.

Paternity leaveSubject to certain qualifying conditions, you may takeup to two weeks of paid Paternity Leave on the birth(or adoption) of a child. Your death benefits and yourown and the CompanyÕs contributions will becontinued on the same basis as for ordinarymaternity leave during this period.

Adoption leaveDuring adoption leave your death benefits and yourown and the CompanyÕs contributions will becontinued on the same basis as for maternity leave.

13

14

Marital statusIt is your responsibility to ensure that the Trustee iskept informed of any change in your marital status. If you are not legally married to your partner (or arenot registered as civil partners) and there is noSpouseÕs pension payable, the Trustee may considerpaying a pension to a Qualifying Dependant, subjectto certain criteria. Any such payments are given atthe absolute discretion of the Trustee.

DivorceThe Trustee must comply with any order made by aCourt following a divorce or dissolution of a civilpartnership.

Insured benefitsThe lump sum benefit payable on death is securedunder an insurance policy specifically to providethose benefits. In normal circumstances, the fullbenefit will be provided automatically without anyenquiry into your state of health. Restrictions may beimposed on your benefit in certain circumstances andyou will be notified if these apply to you.

Income taxAll Fund pensions are paid subject to income tax, as appropriate.

Inheritance taxUnder present legislation, lump sum death benefitspaid under the Fund will not normally be subject toInheritance Tax. To achieve this the Fund is arrangedso that the Trustee has absolute discretion to decidewho receives the lump sum payments. Normally theTrustee will follow your wishes. You should let theTrustee know who you would like to receive themoney by completing the Expression of Wish formaccompanying this guide. Expression of Wish formscan be downloaded from the Fund website shouldyour circumstances change or you change your mindat any time.

HM Revenue & Customs registration and restrictionsThe Fund is registered with HM Revenue & Customs.This means that the Fund and its members receiveimportant tax concessions. However, these taxconcessions only apply to the value of your benefitsup to certain levels, each year and in total. Theselimits are increased annually by HM Revenue &Customs. Any pension paid by the Fund is taxedunder the PAYE system.

Tax advantagesThe Fund has been registered with HM Revenue &Customs under the Finance Act 2004. Membershipof the Fund currently brings with it several importanttax advantages under this Act:

l Full tax relief on your contributions up to 100% ofyour earnings and the Annual Allowance.

l A cash sum option on retirement, which will betax free unless the value of your benefits from allpension arrangements exceeds the LifetimeAllowance.

l Lump sum death benefits paid to yourbeneficiaries or dependants are normally tax free.

l You are not taxed on the CompanyÕs contributions.

l Favourable tax relief on the FundÕs investments.

15

Trust Deed and RulesThe Trustee administers the Fund in accordancewith the Trust Deed and Rules which meet currentlegislative requirements.

This guide provides a summary of the Fund anddoes not cover all the FundÕs detailed provisionswhich are set out in the formal Rules. The Rulesmay be inspected at the office of the administratorby prior arrangement. Alternatively, copies may beobtained from the administrator, at the address onpage 2, although a charge may be made.

In the event of a conflict between the terms of thisguide and those of the Rules, the Rules will prevail.

Amendment and discontinuanceSubject to the Fund Rules, the Company reservesthe right to amend or discontinue the Fund at anytime. If your benefits or rights are affected you willbe given written notice. Retirement benefits to whichyou have already become entitled would, however,be safeguarded in accordance with the detailedprovisions laid down in the Trust Deed and Rules.

Benefits non-assignableYour benefits under the Fund cannot be assigned orused as security for a loan.

MMC UK Pension Fund

MMC UK Pension Fund

16

Notes

Page

Section 1 How the DC section of the Fund works

1

Section 2 The DC section of the Fund in brief 3

Section 3 The DC section of the Fund in detail 4

Contributions 4

Investment 5

Retirement benefits 6

Early and late retirement 7

Death in service 8

Death after retirement 8

Leaving 9

Section 4 Further information 10

ContentsDefinitions

Annual Allowance is a limit set by the Government on the amount by which your pension benefits and/or pension savings can grow in a year (1 April to 31 March) before being subject to tax. The growth in your benefits can be calculated by adding up the following:

l Any money purchase contributions (e.g. contributions to the DC section of the Fund or AVCs) made by you or paid or credited by the Company during the year; and, if applicable

l The amount by which any defined benefit pension entitlement has increased over the year, multiplied by 10; and, if applicable

l The growth in any other pension savings (excluding statutory revaluation on deferred pension benefits).

The Annual Allowance has been set at £215,000 for the 2006/07 tax year.

Basic Salary is your current annual base salary, excluding car allowances, bonuses or any other benefits.

Children are your children or your Spouse’s children who are financially dependent on you and are under age 18, or under age 23 if still in full-time education (or beyond if mentally or physically disabled).

Company is Marsh & McLennan Companies UK Ltd, the Principal Employer.

Contributing Member is a member who is currently paying contributions to the Fund and building up retirement benefits.

Core Contribution is the minimum contribution payable by you, or payable or credited by the Company to your Individual Account. The Company Core Contribution increases as you get older.

Final Pensionable Salary is the annual average of Pensionable Salary received in the last 24 calendar months of Pensionable Service or, if greater, the best 2 consecutive calendar years out of the last 10 consecutive calendar years.

Fund is the MMC UK Pension Fund.

Fund-specific Salary Cap is the upper limit on the amount of salary that can be taken into account when calculating pensions arising from and contributions payable under the Fund. The limit is normally increased annually.

Individual Account is an account set up in your name whilst contributing to the Fund.

Lifetime Allowance is a limit set by the Government on the amount of pension savings that will qualify for tax relief. This allowance will start at £1.5 million worth of benefits from registered pension arrangements from 2006, rising to £1.8 million in 2010. The Lifetime Allowance will apply to all of the pension benefits you build up over your entire working life and will be triggered by a benefit crystallisation event such as payment of retirement income or death benefits.

Lower Earnings is the level of earnings at which benefits under the State Second Pension start accruing.Limit (LEL) This figure is set by the Government and adjusted each year. It is broadly equal to the Basic

State Pension.

Match Contributions are optional contributions payable by members aged 31 and over in addition to their Core Contribution.

MatchPlus Contributions are contributions paid or credited to your Individual Account on behalf of the Company, in addition to Company Core Contributions, when you opt to pay Match Contributions.

Normal Retirement Age is 65.

Pensionable Salary is your Basic Salary less an amount equal to the LEL. For members working on a part-time basis, the LEL is pro-rated before being deducted. Where members earn over the Fund-specific Salary Cap, Pensionable Salary will be restricted to the Fund-specific Salary Cap less the LEL.

Qualifying Dependant is any adult person who immediately before your death was partly or wholly financially dependent on you.

Reckonable Salary is your annual salary immediately before your date of death or, if greater, the total amount of Pensionable Salary (before the deduction of the LEL) received during the 12 months ending on 31 December immediately before your date of death.

RPI increase means the percentage increase in the Retail Prices Index over a defined 12 month period.

Spouse is your legally married husband or wife. Under the Civil Partnership Act 2004, a registered civil partner will be treated the same as a Spouse for pension purposes.

State Pension Age for men is 65. For women born:

l before 6 April 1950 it is 60; l after 5 April 1955, it is 65; l between 6 April 1950 and 5 April 1955 it is on a sliding scale between 60 and 65.

State Second provides a pension in addition to the Basic State Pension. As a member of the DC sectionPension (S2P) of the Fund you participate fully in S2P.

Upper Earnings Limit (UEL) is the level of earnings at which benefits under the State Second Pension cease accruing. It is adjusted by the Government each year.

Page

Section 1 How the DC section of the Fund works

1

Section 2 The DC section of the Fund in brief 3

Section 3 The DC section of the Fund in detail 4

Contributions 4

Investment 5

Retirement benefits 6

Early and late retirement 7

Death in service 8

Death after retirement 8

Leaving 9

Section 4 Further information 10

ContentsDefinitions

Annual Allowance is a limit set by the Government on the amount by which your pension benefits and/or pension savings can grow in a year (1 April to 31 March) before being subject to tax. The growth in your benefits can be calculated by adding up the following:

l Any money purchase contributions (e.g. contributions to the DC section of the Fund or AVCs) made by you or paid or credited by the Company during the year; and, if applicable

l The amount by which any defined benefit pension entitlement has increased over the year, multiplied by 10; and, if applicable

l The growth in any other pension savings (excluding statutory revaluation on deferred pension benefits).

The Annual Allowance has been set at £215,000 for the 2006/07 tax year.

Basic Salary is your current annual base salary, excluding car allowances, bonuses or any other benefits.

Children are your children or your Spouse’s children who are financially dependent on you and are under age 18, or under age 23 if still in full-time education (or beyond if mentally or physically disabled).

Company is Marsh & McLennan Companies UK Ltd, the Principal Employer.

Contributing Member is a member who is currently paying contributions to the Fund and building up retirement benefits.

Core Contribution is the minimum contribution payable by you, or payable or credited by the Company to your Individual Account. The Company Core Contribution increases as you get older.

Final Pensionable Salary is the annual average of Pensionable Salary received in the last 24 calendar months of Pensionable Service or, if greater, the best 2 consecutive calendar years out of the last 10 consecutive calendar years.

Fund is the MMC UK Pension Fund.

Fund-specific Salary Cap is the upper limit on the amount of salary that can be taken into account when calculating pensions arising from and contributions payable under the Fund. The limit is normally increased annually.

Individual Account is an account set up in your name whilst contributing to the Fund.

Lifetime Allowance is a limit set by the Government on the amount of pension savings that will qualify for tax relief. This allowance will start at £1.5 million worth of benefits from registered pension arrangements from 2006, rising to £1.8 million in 2010. The Lifetime Allowance will apply to all of the pension benefits you build up over your entire working life and will be triggered by a benefit crystallisation event such as payment of retirement income or death benefits.

Lower Earnings is the level of earnings at which benefits under the State Second Pension start accruing.Limit (LEL) This figure is set by the Government and adjusted each year. It is broadly equal to the Basic

State Pension.

Match Contributions are optional contributions payable by members aged 31 and over in addition to their Core Contribution.

MatchPlus Contributions are contributions paid or credited to your Individual Account on behalf of the Company, in addition to Company Core Contributions, when you opt to pay Match Contributions.

Normal Retirement Age is 65.

Pensionable Salary is your Basic Salary less an amount equal to the LEL. For members working on a part-time basis, the LEL is pro-rated before being deducted. Where members earn over the Fund-specific Salary Cap, Pensionable Salary will be restricted to the Fund-specific Salary Cap less the LEL.

Qualifying Dependant is any adult person who immediately before your death was partly or wholly financially dependent on you.

Reckonable Salary is your annual salary immediately before your date of death or, if greater, the total amount of Pensionable Salary (before the deduction of the LEL) received during the 12 months ending on 31 December immediately before your date of death.

RPI increase means the percentage increase in the Retail Prices Index over a defined 12 month period.

Spouse is your legally married husband or wife. Under the Civil Partnership Act 2004, a registered civil partner will be treated the same as a Spouse for pension purposes.

State Pension Age for men is 65. For women born:

l before 6 April 1950 it is 60; l after 5 April 1955, it is 65; l between 6 April 1950 and 5 April 1955 it is on a sliding scale between 60 and 65.

State Second provides a pension in addition to the Basic State Pension. As a member of the DC sectionPension (S2P) of the Fund you participate fully in S2P.

Upper Earnings Limit (UEL) is the level of earnings at which benefits under the State Second Pension cease accruing. It is adjusted by the Government each year.

A

Guide for Members

Designed & produced by Mercer Limited©9376_11

MMC UK Pension Fund

This booklet applies to Marsh employees eligible to join the DC section only. A separate booklet is available for other employees.

DC section Explanatory Booklet

Marsh

Please see overleaf for Definitions

A

Guide for Members

Designed & produced by Mercer Limited©9376_11

MMC UK Pension Fund

This booklet applies to Marsh employees eligible to join the DC section only. A separate booklet is available for other employees.

DC section Explanatory Booklet

Marsh

Please see overleaf for Definitions