Embed Size (px)

Citation preview

Fir

st N

ational B

ank -

a d

ivis

ion o

f F

irst

Rand B

ank L

imited. A

n A

uth

ori

sed F

inancia

l Serv

ices

and C

redit P

rovid

er (N

CR

CP

20).

Property in 2012

- Change, change and more change

February 2012

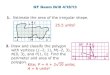

Aspiration/Expectation Mismatches through cycles

• Introduction phase –

aspirations/expectations lag reality

• Growth Phase –

aspirations/expectations accelerating but

still lagging reality

• Mature Phase –

Aspirations/expectations catching up with

“slowing” reality

• Decline Phase –

Aspirations/Expectations “Ahead” of

“Weakening” Reality = TENSION

The Industry/Product Life Cycle

Introduction

Phase

Growth

Phase

Mature

Phase

Decline

Phase

Time

25% “Over-valued”??? – Pick a Number – but further real price decline likely

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

1995 1998 2001 2004 2007 2010

2005 R

an

d T

erm

s

Real House Prices - 1995-2011

Real house price (adjusted using PCE deflator) year-on-year % change Source: Absa; SARB

Long term trend line

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

1966 1972 1978 1984 1990 1996 2002 2008

2005 R

an

d T

erm

s

Real House Prices - 1966-2011

Real house price (adjusted using PCE deflator) year-on-year % change

Source: Absa; SARB

Long term trend line

Government fixed investment slowed sharply from the mid-70s

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002

% o

f G

DP

General Government Fixed Investment -

Construction Works (Civils)

General Government Construction Works (Civils) as a Percentage of GDP

Infrastructure in short supply

0

200000

400000

600000

800000

1000000

1200000

1400000

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006

20

05

Ra

nd

sReal Value of Capital Stock of General

Government and Parastatals

Real Value of Capital Stock - 2005 Prices(Rands) - General Government and Parastatals

Flattish period of general government and

parastatal capital stock growth started seeing

noticeable increase in pressure on urban

infrastructure

Urbanisation continues at speed

20

25

30

35

40

45

50

55

60

65

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

% o

f S

A P

op

ula

tio

n U

rba

nis

ed

Percentage of Population Urbanised - South

Africa

No co-incidence that avg. stand size began long term declining trend from the mid-70s

1061.451908

524.0513584

0

200

400

600

800

1000

1200

1950 -

1954

1955 -

1959

1960 -

1964

1965 -

1969

1970 -

1974

1975 -

1979

1980 -

1984

1985 -

1989

1990 -

1994

1995 -

1999

2000 -

2004

2005 -

2009

2010+

Long Term Average Residential Stand Size

Trend (Square Metres)

Average stand size for homes valued by FNB Valuers from 2000 to the present - According

to year in which homes were built

Average building size also showing broad declining trend

203.3422154

146.6587545

50

70

90

110

130

150

170

190

210

230

1950 -

1954

1955 -

1959

1960 -

1964

1965 -

1969

1970 -

1974

1975 -

1979

1980 -

1984

1985 -

1989

1990 -

1994

1995 -

1999

2000 -

2004

2005 -

2009

2010+

Sq

ua

re M

etr

es

Average Building Sizes According to Building

Year (Square Metres)

Average Residential Building Size By Year in which the home was builtFull Title Properties - Average Size By Building YearSectional Title Properties - Average Size By Building Year

Translating into rising land utilisation rates

20.3%

31.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

1950 -

1954

1955 -

1959

1960 -

1964

1965 -

1969

1970 -

1974

1975 -

1979

1980 -

1984

1985 -

1989

1990 -

1994

1995 -

1999

2000 -

2004

2005 -

2009

2010+

Full Title Average Land Utilisation Rate

(Building Only)

Sectional title has become more common over time

94.6%

75.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

1950 -

1954

1955 -

1959

1960 -

1964

1965 -

1969

1970 -

1974

1975 -

1979

1980 -

1984

1985 -

1989

1990 -

1994

1995 -

1999

2000 -

2004

2005 -

2009

2010+

Proportion of Full Title Properties

- Long Term Trend

Full title properties expressed as a percentage of total properties valued - according to

year in which properties were built

And luxuries such as pools and workers’ quarters are becoming less common

40.0%

9.1%

51.5%

11.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

1950 -

1954

1955 -

1959

1960 -

1964

1965 -

1969

1970 -

1974

1975 -

1979

1980 -

1984

1985 -

1989

1990 -

1994

1995 -

1999

2000 -

2004

2005 -

2009

2010+

Proportion of Homes with Domestic Workers'

Quarters and Swimming Pools

Percentage of Homes with Swimming Pools - By year in which the home was built

Percentage of Homes with Domestic Workers' Quarters - According to year in which the

home was built

Garage building is cyclical, and currently features less often. In the absence of public transport, are homes without garages or allocated parking bays marketable

69.2%

57.4%

69.5%

51.6%

40.0%

45.0%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

1950 -

1954

1955 -

1959

1960 -

1964

1965 -

1969

1970 -

1974

1975 -

1979

1980 -

1984

1985 -

1989

1990 -

1994

1995 -

1999

2000 -

2004

2005 -

2009

2010+

Proportion of Properties With Garage(s)

Percentage of Properties with Garage - According to the year in which the home was built

4-5 bedroom homes declining in popularity as household size decreases

4.3% 7.4%1.0% 3.7%

13.8%10.6%

28.2% 33.5%

49.6%56.8%

59.7%

52.0%

20.6%25.2%

7.5%11.4% 11.9%

3.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 -

1954

1955 -

1959

1960 -

1964

1965 -

1969

1970 -

1974

1975 -

1979

1980 -

1984

1985 -

1989

1990 -

1994

1995 -

1999

2000 -

2004

2005 -

2009

2010+

Percentage of Properties by Room Number

According to Year in Which Home Was Built5 Bedrooms+

4 Bedrooms

3 Bedrooms

2 Bedrooms

1 Bedroom

Less than 1

Bedroom

Composition of the FNB House Price Index over time

Global Economic Growth Broad Slowdown expected to continue, risk perception rises

• UN – 2.6% GDP Growth forecast in 2012, down from 4% in 2010, and 2.8% in 2011 (Downward revision)

• World Bank – 2.5% GDP growth in 2012, down from 4.1% in 2010 and 2.7% in 2011 (Downward Revision)

• IMF - “Slowing Growth, Rising Risks”. 4% GDP growth forecast in 2012, but downward revision set to occur, after 4% in 2011 and 5.1% in 2010

• IMF - Some slowing in 2011 had been expected due to end in inventory replenishment cycle. Rise in oil prices and Japan Tsunami also negative events in 2011. But concerns have increased due to “lack of global re-balancing”, “increased fiscal and financial uncertainty” (concerns expanded from Europe to Japan and US), and overheating in some emerging economies

• SARB – CPI inflation peak at 6.6% in Q2 2012 and stay outside target range for entire 2012. Inflation expectations have risen.

• 2.8% GDP growth forecast in 2012, down from 3.1% in 2011

• JL – house price growth down from 6% in 2010, 3.1% in 2011 to 2 % in 2012, based on assumption of reasonable though slower economic growth. Recession expected to equal nominal price decline

Global “Bumps” are seen on a month-on-month basis

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

Jan-06 Jan-08 Jan-10 Jan-12

Key OECD Leading Indicators- amplitude adjusted - month-on-month %

change

OECD Leading Indicator USA Leading Indicator

But year-on-year things remain flat

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2005 2006 2007 2008 2009 2010 2011

Key Leading Indicators vs FNB Residential Demand Indicator - year-on-year % change

USA Leading Indicator OECD Leading Indicator

SA Residential Demand Rating - y/y%

“Bump” was seen locally too

0.15

-80

-60

-40

-20

0

20

40

60

80

100

120

-20

-10

0

10

20

30

Jan-06 Jan-08 Jan-10 Jan-12

%

%SARB Leading Indicator vs New Mortgage

Loans Granted

Leading Business Cycle Indicator - year-on-year percentage change

New Mortgage Loans and Re-Advances Granted - year-on-year % change

Retail sales point to 4th Quarter 2011 “Bump” passing through the numbers

59.0%

33.3%

5.7%

-60%

-40%

-20%

0%

20%

40%

60%

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Nominal Value of New Vehicle Sales - Growth

Value of New Vehicle Sales - y/y% 3-Month Moving Average

29.5%

5.6%

-2.0%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Nominal Value of Used Vehicle Sales - Growth

Value of Used Vehicle Sales - y/y% 3-Month Moving Average

-10%

-5%

0%

5%

10%

15%

20%

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

Real Retail sales growth (2008 Prices)

Real Retail Sales - y/y% 3-month moving average - y/y%

House price slightly up recently, but don’t expect wonders yet

Residential market balance shows no improvement

Residential market balance shows no improvement

FNB Valuers point to Market Imbalance continuing

Debt-to-Disposable Income Ratio still very high for a bottom turning point

82.7

75.0

5

7

9

11

13

15

17

19

21

23

25

40

50

60

70

80

1990 1993 1996 1999 2002 2005 2008 2011

%%

Household Debt to Disposable Income Ratio vs Interest Rates

Household debt-to-disposable income ratio (Left Axis) Prime Rate

Financial Pressure-related selling still significant

Reasons for selling (As % of Total Sales)Total

High Net

Worth

Upper

income

Middle

income

Lower

income

Downscaling due to financial pressure21% 16% 22% 21% 27%

Downscaling with life stage 22% 29% 20% 23% 13%

Emigrating 4% 5% 6% 2% 5%Relocating within SA 8% 10% 7% 8% 8%

Upgrading 17% 16% 16% 16% 19%Moving for safety and security reasons9% 8% 9% 9% 9%

Change in family structure 12% 11% 13% 12% 12%Moving to be closer to work or amenities7% 6% 7% 8% 8%

Agents were at their most confident in Q1 2010 – broad weakening since then.

6.35

5.66

4

4.5

5

5.5

6

6.5

7

7.5

8

2004 2005 2006 2007 2008 2009 2010 2011

Acti

vit

y L

evels

on

a s

cale

of

1-1

0

Levels of Activity

National Demand Activity Rating (Scale 1 to 10)

Mortgage Loans Growth Slows through 2011

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

200401 200501 200601 200701 200801 200901 201001 201101

Ye

ar-

on

-ye

ar

% c

ha

ng

eGrowth in Mortgages Registered by Individuals below R5m

Value

Volume of Transactions - 3-month moving average - y/y%

Value of Transactions - 3-month moving average - y/y%

In Short, yes, it’s overvalued

• Yes, we believe the residential market is over-valued, and has to adjust to a myriad of challenges, but NO, we don’t believe it is possible to quantify the extent to which it is overvalued

• The residential market heads into the next growth slowdown still unbalanced with regard to demand and supply

• The World economy remains in a high risk period due to the big imbalances wrtsavings vs consumption and high debt levels

• Consensus appears to be that 2012 will bring slower global and local economic growth

• 2011 already saw a broad slowing of house price growth and commercial property returns in tandem with a slowing economy

Toll Roads are a Shock – SA Res. Property designed for cheap private transport

• Joburg National Roads Toll affects YOU – sets a precedent

• Toll roads push a lot of traffic off onto “free roads” – Congestion elsewhere

• Toll roads greatly increase the importance of “location location location”

• Toll roads may see an increase in de-centralisation of business nodes

• Fuel levy would spread the financial load far more evenly, thus reducing market distortions

• Fuel levy cheap administratively

• Fuel levy would enable a co-ordinated transport strategy – raise the general cost of private transport, create demand for public transport, and could even be used to subsidise public transport

• Fuel levy could be gradually phased up, thus reducing the shock to a property market designed around cheap private transport.

Why NOW could be the time for competition levels to rise

• “Static market share” philosophy of banks, as opposed to “cyclical market share” philosophy (need to move with competitors)

• Availability (or “recency”) bias in market players’ thinking

– Recent history has improved wrt market performance and bad debt

- Interest rates have been low for long, therefore this is the “new normal”

- For households – Have experienced better financial times of late (largely due to rate cuts), therefore trouble is over and we can borrow more

• Perceptions of risk are derived largely from recent historic performance and not from key risk indicators (Didn’t die on recent Everest trip therefore risk is not so high as we thought)

• Slowing market growth – Targets are normally expected to show growth, and market growth has been slowing. Solution – make internal plan to grow (credit appetite and pricing NB)

• New sales normally more a focus than retention and slowing the paying down of a loan

• Lack of clarity of how credit quality improvements have been achieved

Households want to borrow and lenders increasingly want to lend – just waiting for mortgage lenders

6.83

18.89

-15

-5

5

15

25

35

Jan-02 Jan-04 Jan-06 Jan-08 Jan-10

%

Mortgage vs Non-Mortgage Household Credit Growth (Lent by Banks)

Household Credit Growth (Lent by Banks) Non-Mortgage Households Sector Credit Growth (Lent by Banks)

US Household De-Leveraging may have years to run

In the mean time we live in hope that US Govtborrow and Fed printing will keep economy going

SARB has warned on inflation

SARB has warned on inflation

SARB has warned on inflation

Basics In, “Clever stuff” Out – Still a Wise strategy

Basics In, “Clever stuff” Out – Still a Wise Strategy

Key Focal Points – Slow periods are opportunities to get fundamentals right

• The next “Groot Trek” – FNB moving north into Africa. Long term – African growth prospects appear good off a low base, may grow as an FDI destination faster than SA which is the most geographically isolated

• Affordability is king – market adapting to financial pressure and huge municipal and rates cost increases – Relatively good for the affordable end but bad for the luxury end

• Size counts – far smaller is going to be far better

• Going Green – How? Do we have the expertise to advise our clients?

• Transport cost increases – looming

• Location near to work place, important facilities, open space

• Weak market and financial pressure = Need for reliable information and expertise

• Poor client knowledge – Need for far more help – Emergence of the “Buyers Agent a result of this need”?

• Industry “Clean Ups” and Professional Standards

People First – A Winning Strategy – “It’s not about the toys”

• Materialism has destroyed human relationships and happiness, and hampers performance

• Time to say it – Our industry has a shaky reputation (rightly or wrongly)

• Short term profit has become King

• Property is a low frequency purchase, which possibly explains the lack of relationship building with clients

• But property buying’s low frequency nature means that most sellers and buyers are uneducated

• However, property is a daily event – we live there, we maintain it, we upgrade it, let it, and periodically buy or sell it

• Are YOU top of mind in your area when it comes to any property advice/help/expertise???

• Is your personal brand as strong as the agency brand you represent???

• If the answer is NO to these 2 questions, then why would you be top of my mind when wanting to buy/sell or acquire a home loan????

• Back to basics – PEOPLE FIRST (Client for Life) is the long term winning strategy.

Follow our Research on:

http://blog.propertyleader.co.za

Research mailing list:

John Loos on Twitter:

@john_loos