Embed Size (px)

Citation preview

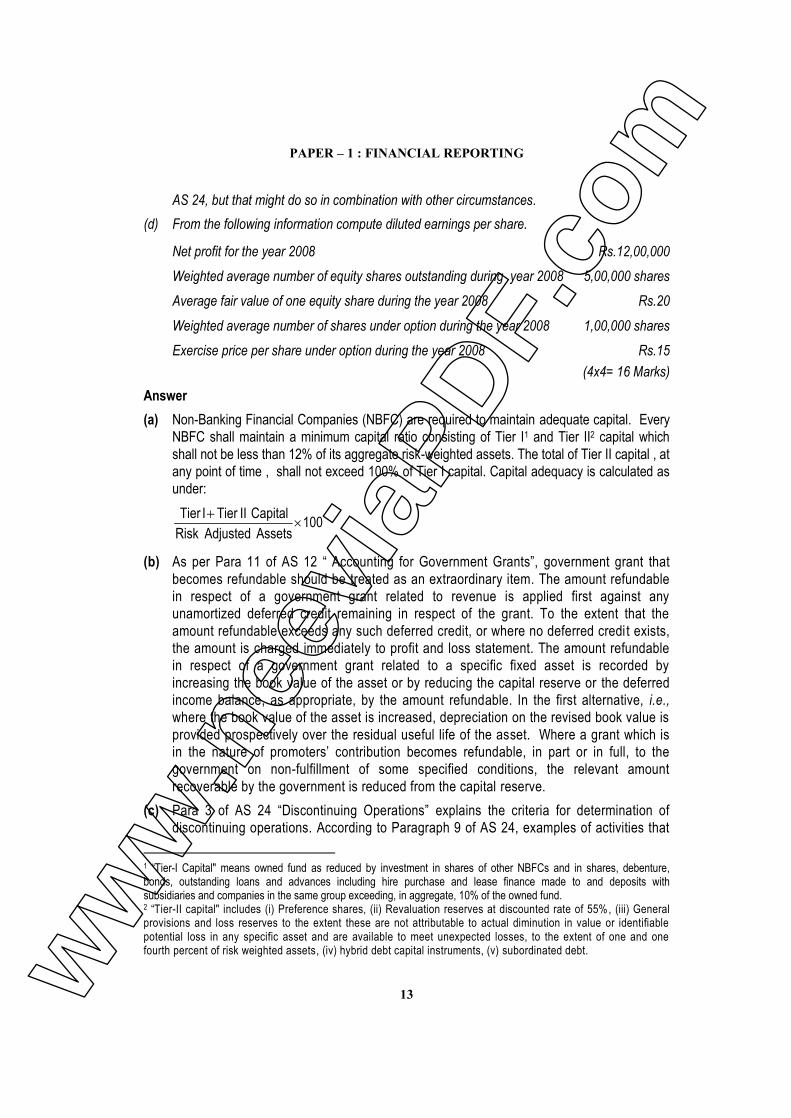

PAPER – 1 : FINANCIAL REPORTING

Question No. 1 is compulsory. Answer any five out of the remaining questions.

Working notes should form part of the answer.Wherever necessary, suitable assumptions may be made by the candidates.

Question 1Answer any four out of the following:(a) From the following details of an asset

(i) Find out impairment loss(ii) Treatment of impairment loss(iii) Current year depreciationParticulars of asset:

Cost of asset Rs.56 lakhsUseful life period 10 yearsSalvage value NilCurrent carrying value Rs. 27.30 lakhsUseful life remaining 3 yearsRecoverable amount Rs.12 lakhsUpward revaluation done in last year Rs.14 lakhs

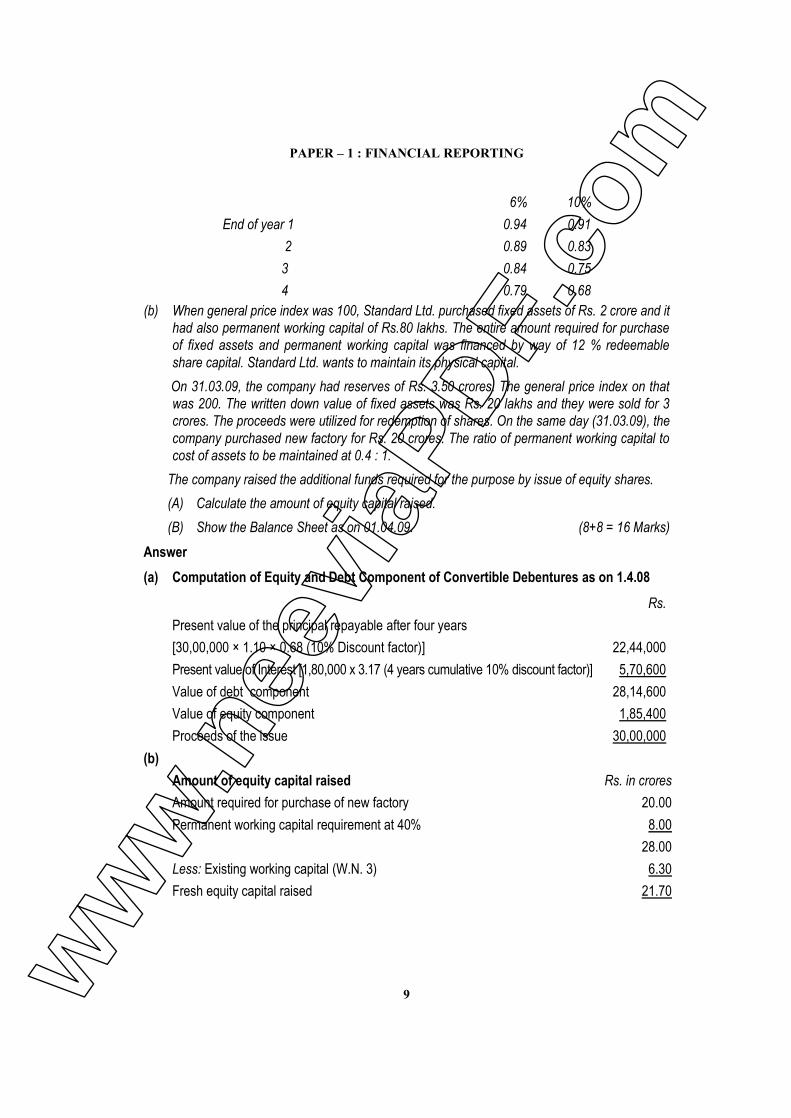

(b) Rainbow Limited borrowed an amount of Rs.150 crores on 1.4.2008 for construction ofboiler plant @ 11% p.a. The plant is expected to be completed in 4 years. Since theweighted average cost of capital is 13% p.a., the accountant of Rainbow Ltd. capitalizedRs.19.50 crores for the accounting period ending on 31.3.2009. Due to surplus fund, outof Rs.150 crores, an income of Rs.3.50 crores was earned and credited to profit and lossaccount. Comment on the above treatment of accountant with reference to relevantaccounting standard.

(c) Suraj Limited wishes to obtain a machine costing Rs.30 lakhs by way of lease. Theeffective life of the machine is 14 years, but the company requires it only for the first 5years. It enters into an agreement with Ashok Ltd., for a lease rental for Rs.3 lakhs p.a.payable in arrears and the implicit rate of interest is 15%. The chief accountant of SurajLimited is not sure about the treatment of these lease rentals and seeks your advise.

(d) Omega Limited is working on different projects which are likely to be completed within 3years period. It recognizes revenue from these contracts on percentage of completionmethod for financial statements during 2006, 2007 and 2008 for Rs.11,00,000,Rs.16,00,000 and Rs.21,00,000 respectively. However, for income-tax purpose, it hasadopted the completed contract method under which it has recognized revenue ofww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

2

Rs.7,00,000, Rs.18,00,000 and Rs.23,00,000 for the years 2006, 2007 and 2008respectively. Income-tax rate is 35%. Compute the amount of deferred tax asset/liabilityfor the years 2006, 2007 and 2008.

(e) While preparing its final accounts for the year ended 31st March, 2009, a company madea provision for bad debts @ 5% of its total debtors. In the last week of February 2009, adebtor for 2 lakhs had suffered heavy loss due to earthquake. The loss was not coveredby any insurance policy. In April, 2009, the debtor became bankrupt. Can the companyprovide for full loss arising out of insolvency of debtor in the final accounts for year ended31st March, 2009? (4x5 = 20 Marks)

Answer(a) According to para 59 of AS 28 “Impairment of Assets”, an impairment loss on a revalued

asset is recognised as an expense in the statement of profit and loss. However, animpairment loss on a revalued asset is recognised directly against any revaluationsurplus for the asset to the extent that the impairment loss does not exceed the amountheld in the revaluation surplus for that same asset.

Impairment Loss and its treatment Rs.

Current carrying amount (including revaluation amount of Rs.14 lakhs) 27,30,000Less: Current recoverable amount 12,00,000Impairment Loss 15,30,000Impairment loss charged to revaluation reserve 14,00,000Impairment loss charged to profit and loss account 1,30,000

As per para 61 of AS 28, “after the recognition of an impairment loss, the depreciation(amortization) charge for the asset should be adjusted in future periods to allocate theasset’s revised carrying amount, less its residual value (if any), on a systematic basisover its remaining useful life.”In the given case, the carrying amount of the asset will be reduced to Rs.12,00,000 afterimpairment. This amount is required to be depreciated over remaining useful life of 3years (including current year). Therefore, the depreciation for the current year will beRs.4,00,000.

(b) Para 10 of AS 16 ‘Borrowing Costs’ states, “to the extent that funds are borrowedspecifically for the purpose of obtaining a qualifying asset, the amount of borrowing costseligible for capitalisation on that asset should be determined as the actual borrowingcosts incurred on that borrowing during the period less any income on the temporaryinvestment of those borrowings.” The capitalisation rate should be the weighted averageof the borrowing costs applicable to the borrowings of the enterprise that are outstandingduring the period, other than borrowings made specifically for the purpose of obtaining aqualifying asset. Hence, in the above case, treatment of accountant of Rainbow Ltd. is

ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

3

incorrect. The amount of borrowing costs capitalized for the financial year 2008-2009should be calculated as follows:

Actual interest for 2008-2009 (11% of Rs.150 crores) Rs.16.50 croresLess: Income on temporary investment from specific borrowings Rs. 3.50 croresBorrowing costs to be capitalized during year 2008-2009 Rs. 13.00 crores

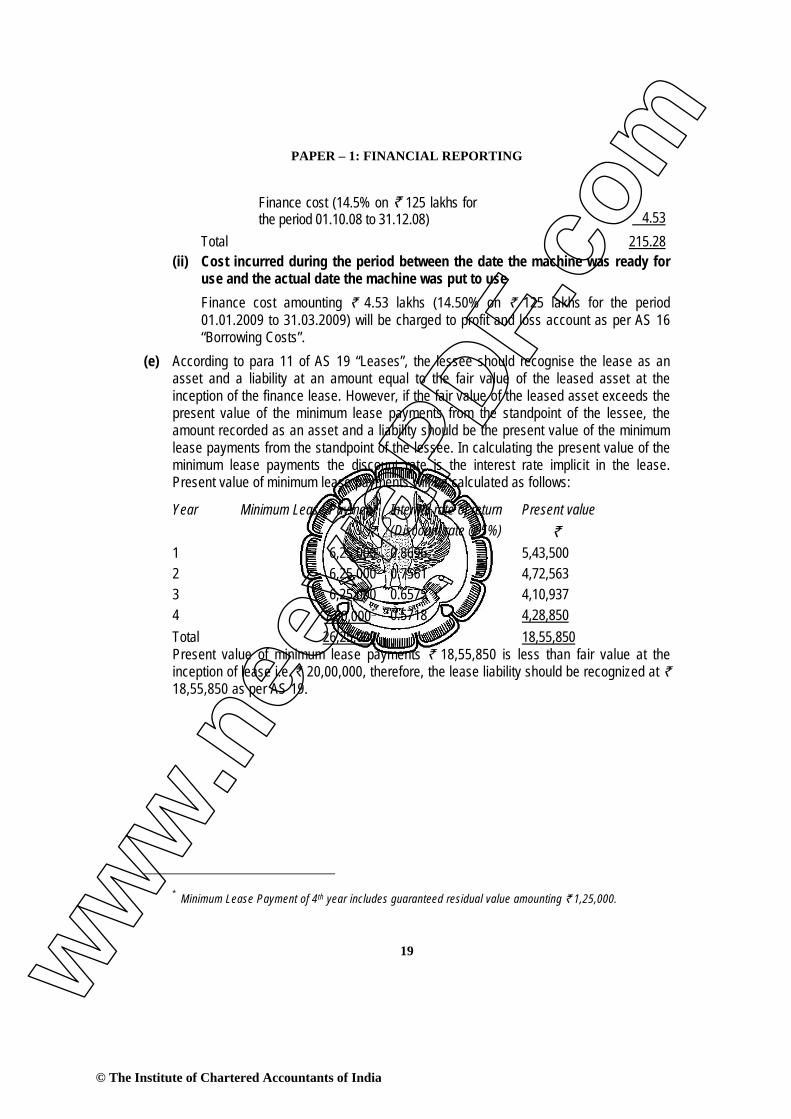

(c) As per AS 19 ‘Leases’, a lease will be classified as finance lease if at the inception of thelease, the present value of minimum lease payment amounts to at least substantially allof the fair value of leased asset. In the given case, the implicit rate of interest is given at15%. The present value of minimum lease payments at 15% using PV- Annuity Factorcan be computed as follows:

Annuity Factor (Year 1 to Year 5) 3.36 (approx.)Present value of minimum lease payments (for Rs.3 lakhs each year) Rs.10.08 lakhs (approx.)

Thus, present value of minimum lease payments is Rs.10.08 lakhs and the fair value ofthe machine is Rs.30 lakhs. In a finance lease, lease term should be for the major part ofthe economic life of the asset even if title is not transferred. However, in the given case,the effective useful life of the machine is 14 years while the lease is only for five years.Therefore, lease agreement is an operating lease. Lease payments under an operatinglease should be recognized as an expense in the statement of profit and loss on astraight line basis over the lease term unless another systematic basis is morerepresentative of the time pattern of the user’s benefit.

(d) Omega LimitedCalculation of Deferred Tax Asset/Liability

Year AccountingIncome

Taxable Income Timing Difference(balance)

Deferred TaxLiability (balance)

2006 11,00,000 7,00,000 4,00,000 1,40,0002007 16,00,000 18,00,000 2,00,000 70,0002008 21,00,000 23,00,000 NIL NIL

48,00,000 48,00,000

In calculating the present value of minimum lease payments, the discount rate is the interest rateimplicit in the lease. This is calculated using the following formula:

( ) ( ) ( ) ( ) ( )54321 15.+11

+15.+11

+15.+11

+15.+11

+15.+11ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

4

(e) As per para 8.2 and 13 of Accounting Standard 4 ‘Contingencies and Events occurringafter the Balance Sheet Date’, assets and liabilities should be adjusted for eventsoccurring after the date of balance sheet, that provide additional evidence to assistestimation of amounts relating to conditions existing at the Balance Sheet Date.Therefore, in the given case, full provision for bad debt amounting Rs.2 lakhs should bemade to cover the loss arising due to insolvency in the final accounts for the year ended31st March, 2009 as earthquake took place before the balance sheet date.

Question 2The Balance Sheet of Munna Ltd as on 31st March, 2009 is as follows:

Liabilities Rs. Assets Rs.Authorised and issued Share capital Goodwill 2,00,00020,000 Equity shares of Rs.100 each, fully paid 20,00,000 Plant & Machinery 18,00,00010,000, 7% Preference shares of Rs.100 each 10,00,000 Stock 3,00,000Sundry creditors 7,00,000 Debtors 7,50,000Bank overdraft 3,00,000 Cash 1,50,000

Preliminary expenses 1,00,000Profit and Loss A/c 7,00,000

40,00,000 40,00,000

Additional Information:Two years’ preference share dividend is in arrears. The company had bad time during the lasttwo years and hopes for better business in future, earning profit and paying dividend, providedthe capital base is reduced.An internal reconstruction scheme, agreed to by all concerned, is as follows:(i) Creditors agreed to forego 50% of their claim.(ii) Preference shareholders withdrew arrear dividend claim. They also agreed to lower

down their capital claim by 20% by reducing nominal value in consideration of 9%dividend effective after reconstruction, in case equity shareholder’s loss exceeded 50%on the application of the scheme.

(iii) Bank has agreed to convert overdraft into term loan to the extent required for makingcurrent ratio to 2:1.

(iv) Revalued amount for plant and machinery was accepted as Rs.15,00,000.(v) Debtors to the extent of Rs.4,00,000 were considered as good.(vi) Equity shares shall be exchanged for the same number of equity shares at a revised

denomination as required after the reconstruction.

ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

5

You are required to show the following:(a) Total loss to be borne by the equity and preference shareholders for the reconstruction.(b) Share of loss to the individual class of shareholders.(c) New structure of share capital after reconstruction.(d) Working capital of the reconstructed company, and(e) A Performa Balance Sheet after reconstruction. (16 Marks)

Answer(a) Loss to be borne by Equity and Preference Shareholders

Rs.Profit and loss account (debit balance) 7,00,000Preliminary expenses 1,00,000Goodwill 2,00,000Plant and machinery (Rs. 18,00,000 – Rs. 15,00,000) 3,00,000Debtors (Rs. 7,50,000 – Rs. 4,00,000) 3,50,000Amount to be written off 16,50,000Less: 50% of Sundry Creditors 3,50,000Total loss to be borne by the equity and preference shareholders 13,00,000

(b) Share of loss to preference shareholders and equity shareholdersTotal loss of Rs. 13,00,000 being more than 50% of equity share capital i.e. Rs.10,00,000Preference shareholders’ share of loss = 20% of Rs. 10,00,000 = Rs. 2,00,000Equity shareholders’ share of loss (Rs. 13,00,000 – Rs. 2,00,000)= Rs. 11,00,000Total loss Rs. 13,00,000

(c) New structure of share capital after reorganisation

Equity shares: Rs.20,000 equity shares of Rs. 45 each, fully paid up(Rs. 20,00,000 – Rs. 11,00,000) 9,00,000Preference shares:10,000, 9% preference shares of Rs. 80 each, fully paid up(Rs. 10,00,000 – Rs. 2,00,000) 8,00,000

17,00,000

Two years’ preference dividend (arrears) has been ignored in the computation of loss to be borne byequity and preference shareholders.ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

6

(d) Working capital of the reorganized company

Current Assets: Rs. Rs.Stock 3,00,000Debtors 4,00,000Cash 1,50,000

8,50,000Less: Current liabilities:

Creditors 3,50,000Bank overdraft 75,000 4,25,000

Working capital 4,25,000

(e) Balance Sheet of Munna Ltd. (and reduced)as on 31st March, 2009

Liabilities Rs. Assets Rs.Share Capital Authorised(issued and paid up)

Fixed Assets

20,000 equity shares of Rs. 45 each 9,00,000 Plant and Machinery 15,00,00010,000, 9% preference shares of Rs. 80each

8,00,000 Current Assets

Unsecured loan Stock 3,00,000Term loan with Bank 2,25,000 Debtors 4,00,000Current liabilities Cash 1,50,000Bank overdraft 75,000Creditors 3,50,000 ________

23,50,000 23,50,000

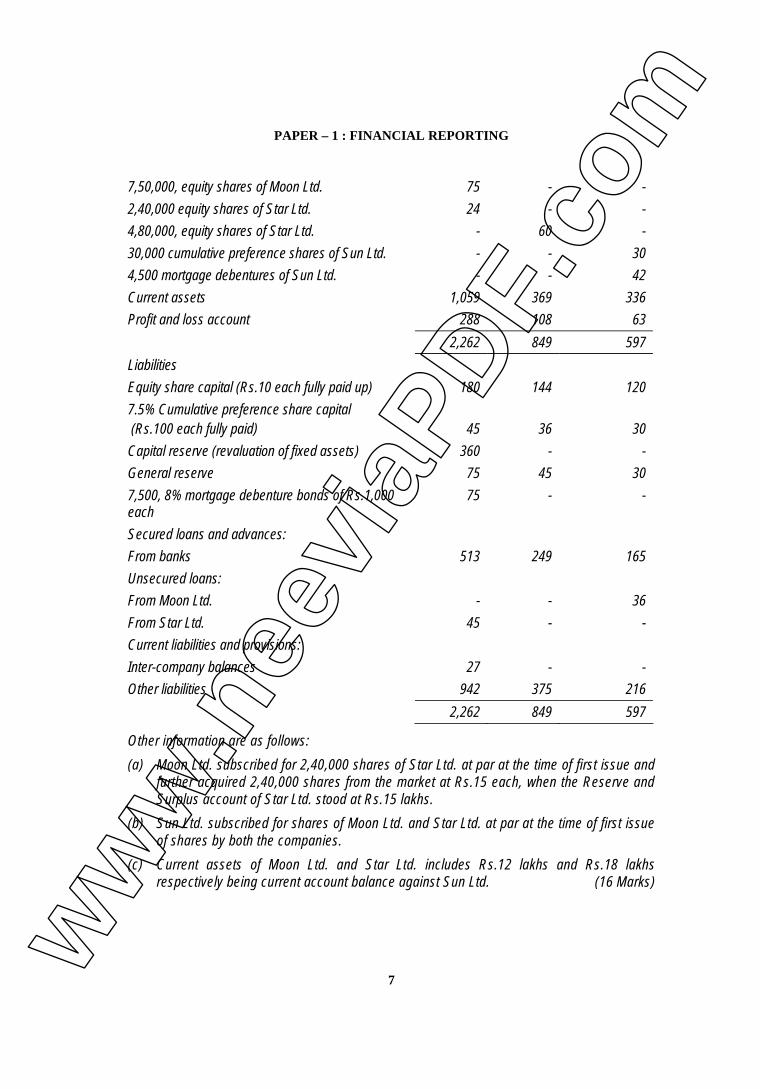

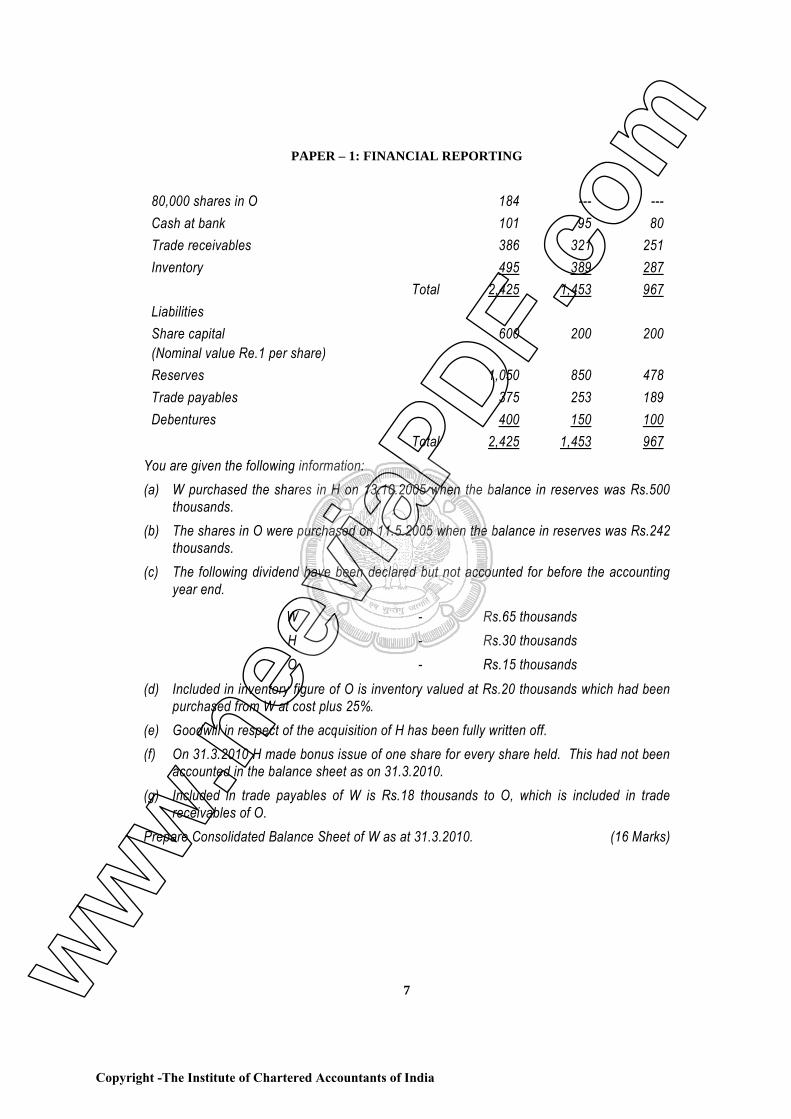

Question 3From the following details, prepare a consolidated Balance Sheet of Sun Limited and itssubsidiaries as on 31st March, 2009:

(Rs. in Lakhs)Assets Sun Ltd. Moon Ltd. Star Ltd.Fixed assets (net) 816 312 126Investment (at cost)

Current ratio shall be 2 : 1, i.e. total current liabilities shall be 50% of Rs. 8,50,000 (i.e. Rs. 3,00,000 +4,00,000 + 1,50,000) = Rs. 4,25,000. Therefore, Bank overdraft = Rs. 75,000 (Rs. 4,25,000 lesscreditors Rs. 3,50,000).ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

7

7,50,000, equity shares of Moon Ltd. 75 - -2,40,000 equity shares of Star Ltd. 24 - -4,80,000, equity shares of Star Ltd. - 60 -30,000 cumulative preference shares of Sun Ltd. - - 304,500 mortgage debentures of Sun Ltd. - - 42Current assets 1,059 369 336Profit and loss account 288 108 63

2,262 849 597LiabilitiesEquity share capital (Rs.10 each fully paid up) 180 144 1207.5% Cumulative preference share capital (Rs.100 each fully paid) 45 36 30Capital reserve (revaluation of fixed assets) 360 - -General reserve 75 45 307,500, 8% mortgage debenture bonds of Rs.1,000each

75 - -

Secured loans and advances:From banks 513 249 165Unsecured loans:From Moon Ltd. - - 36From Star Ltd. 45 - -Current liabilities and provisions:Inter-company balances 27 - -Other liabilities 942 375 216

2,262 849 597

Other information are as follows:(a) Moon Ltd. subscribed for 2,40,000 shares of Star Ltd. at par at the time of first issue and

further acquired 2,40,000 shares from the market at Rs.15 each, when the Reserve andSurplus account of Star Ltd. stood at Rs.15 lakhs.

(b) Sun Ltd. subscribed for shares of Moon Ltd. and Star Ltd. at par at the time of first issueof shares by both the companies.

(c) Current assets of Moon Ltd. and Star Ltd. includes Rs.12 lakhs and Rs.18 lakhsrespectively being current account balance against Sun Ltd. (16 Marks)

ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

8

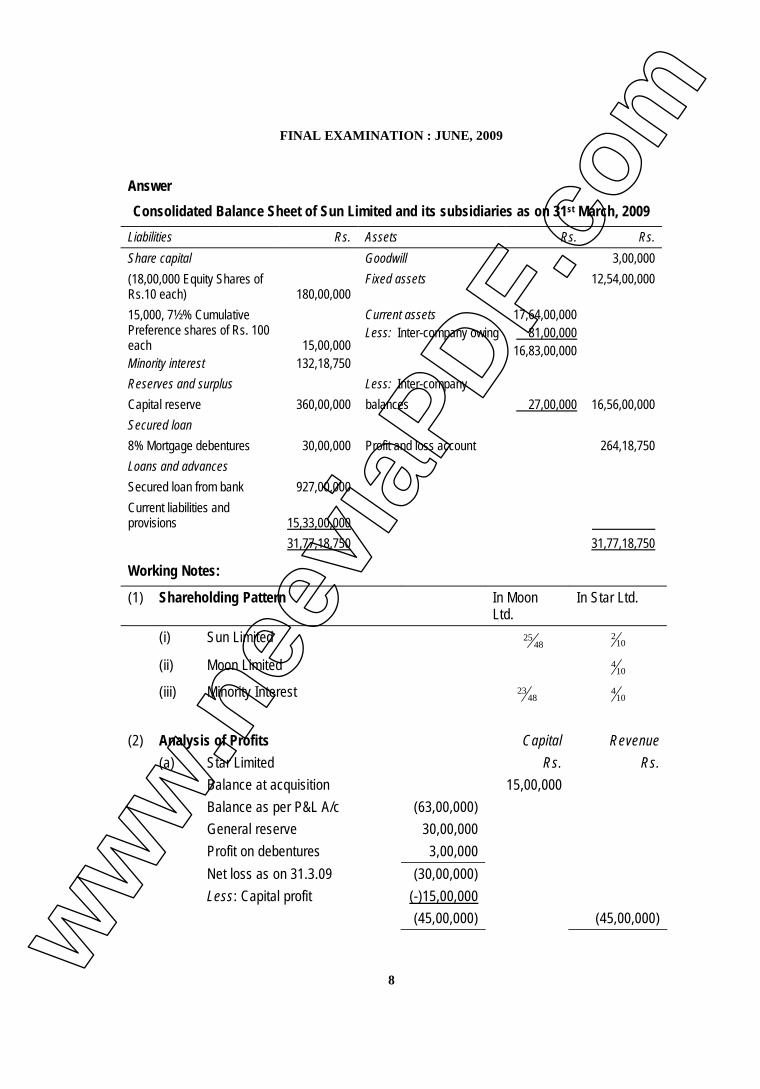

AnswerConsolidated Balance Sheet of Sun Limited and its subsidiaries as on 31st March, 2009

Liabilities Rs. Assets Rs. Rs.Share capital Goodwill 3,00,000(18,00,000 Equity Shares ofRs.10 each) 180,00,000

Fixed assets 12,54,00,000

15,000, 7½% CumulativePreference shares of Rs. 100eachMinority interest

15,00,000132,18,750

Current assetsLess: Inter-company owing

17,64,00,00081,00,000

16,83,00,000

Reserves and surplus Less: Inter-companyCapital reserve 360,00,000 balances 27,00,000 16,56,00,000Secured loan8% Mortgage debentures 30,00,000 Profit and loss account 264,18,750Loans and advancesSecured loan from bank 927,00,000Current liabilities andprovisions 15,33,00,000

31,77,18,750 31,77,18,750

Working Notes:

(1) Shareholding Pattern In MoonLtd.

In Star Ltd.

(i) Sun Limited48

2510

2

(ii) Moon Limited 104

(iii) Minority Interest 4823

104

(2) Analysis of Profits Capital Revenue(a) Star Limited Rs. Rs.

Balance at acquisition 15,00,000Balance as per P&L A/c (63,00,000)General reserve 30,00,000Profit on debentures 3,00,000Net loss as on 31.3.09 (30,00,000)Less: Capital profit (-)15,00,000

(45,00,000) (45,00,000)ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

9

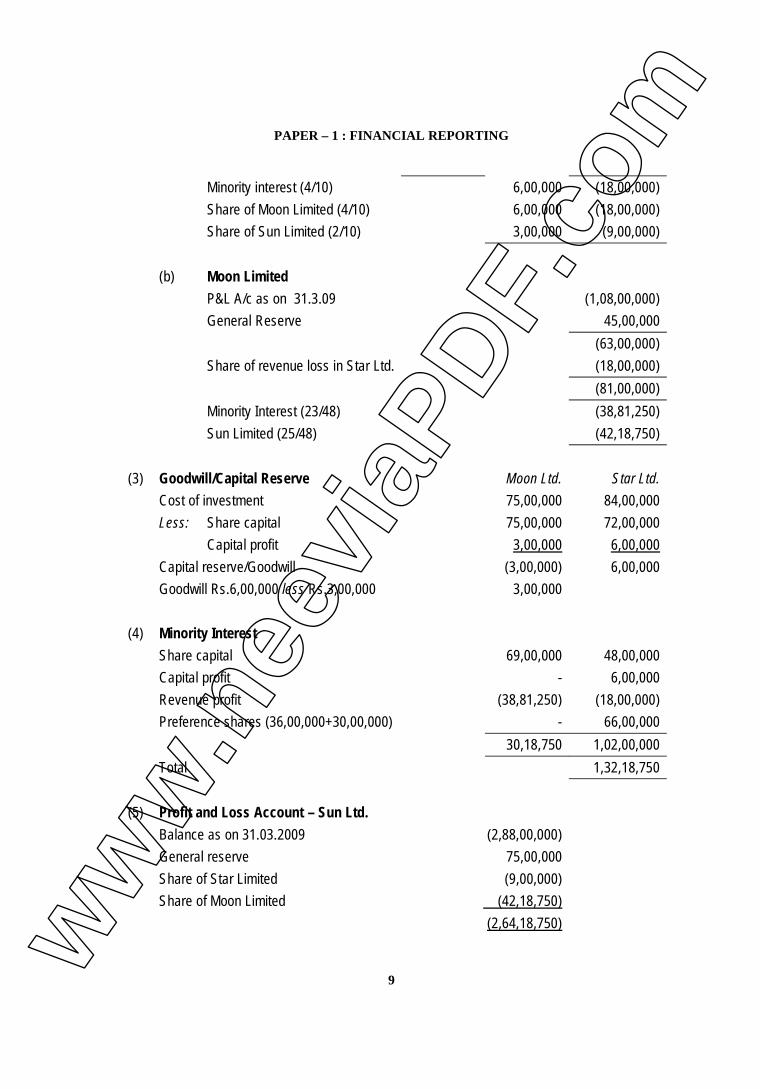

Minority interest (4/10) 6,00,000 (18,00,000)Share of Moon Limited (4/10) 6,00,000 (18,00,000)Share of Sun Limited (2/10) 3,00,000 (9,00,000)

(b) Moon LimitedP&L A/c as on 31.3.09 (1,08,00,000)General Reserve 45,00,000

(63,00,000)Share of revenue loss in Star Ltd. (18,00,000)

(81,00,000)Minority Interest (23/48) (38,81,250)Sun Limited (25/48) (42,18,750)

(3) Goodwill/Capital Reserve Moon Ltd. Star Ltd.Cost of investment 75,00,000 84,00,000Less: Share capital 75,00,000 72,00,000

Capital profit 3,00,000 6,00,000Capital reserve/Goodwill (3,00,000) 6,00,000Goodwill Rs.6,00,000 less Rs.3,00,000 3,00,000

(4) Minority InterestShare capital 69,00,000 48,00,000Capital profit - 6,00,000Revenue profit (38,81,250) (18,00,000)Preference shares (36,00,000+30,00,000) - 66,00,000

30,18,750 1,02,00,000Total 1,32,18,750

(5) Profit and Loss Account – Sun Ltd.Balance as on 31.03.2009 (2,88,00,000)General reserve 75,00,000Share of Star Limited (9,00,000)Share of Moon Limited (42,18,750)

(2,64,18,750)ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

10

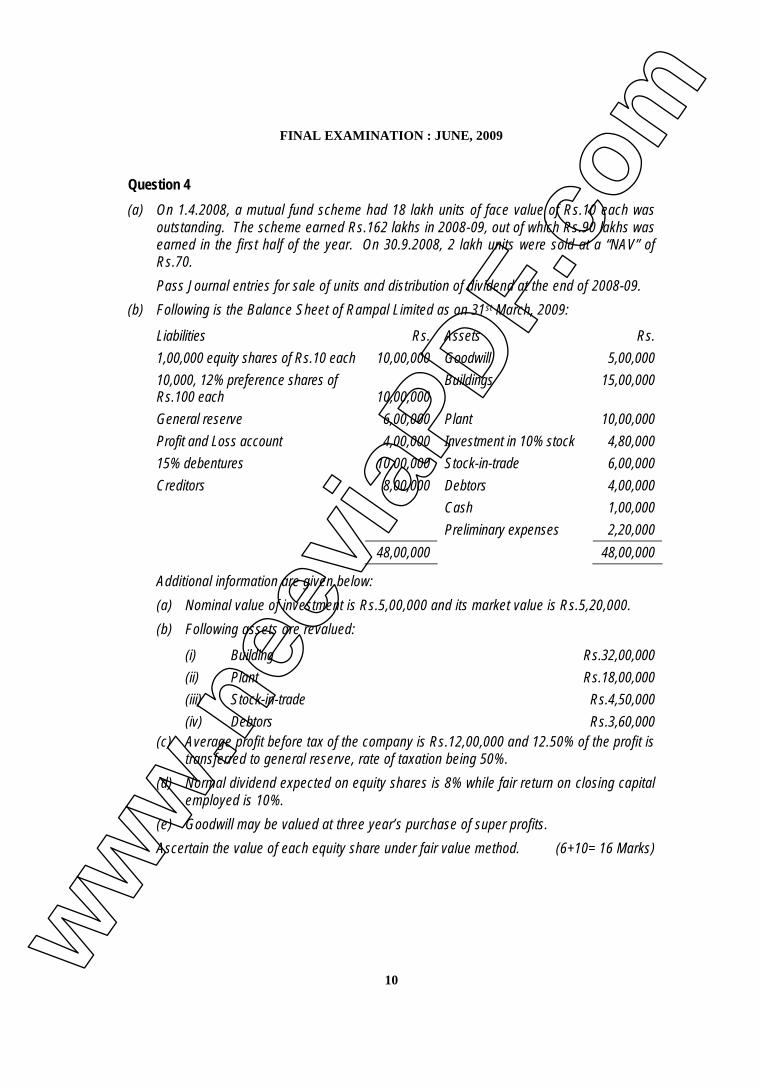

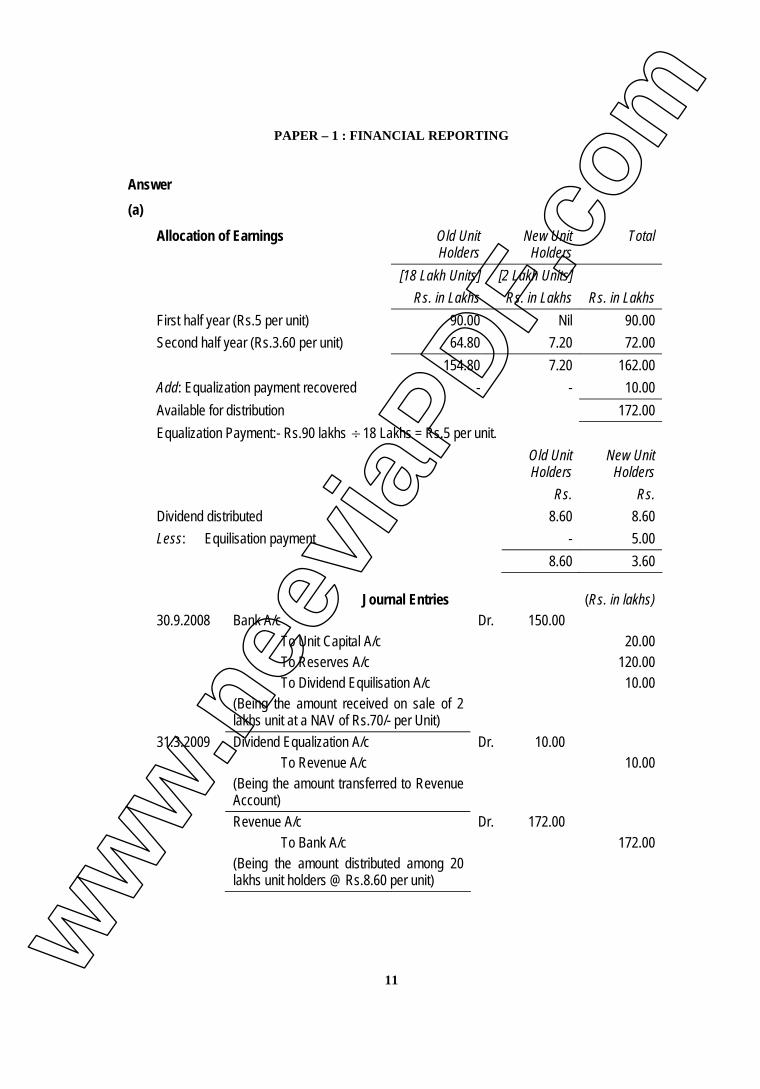

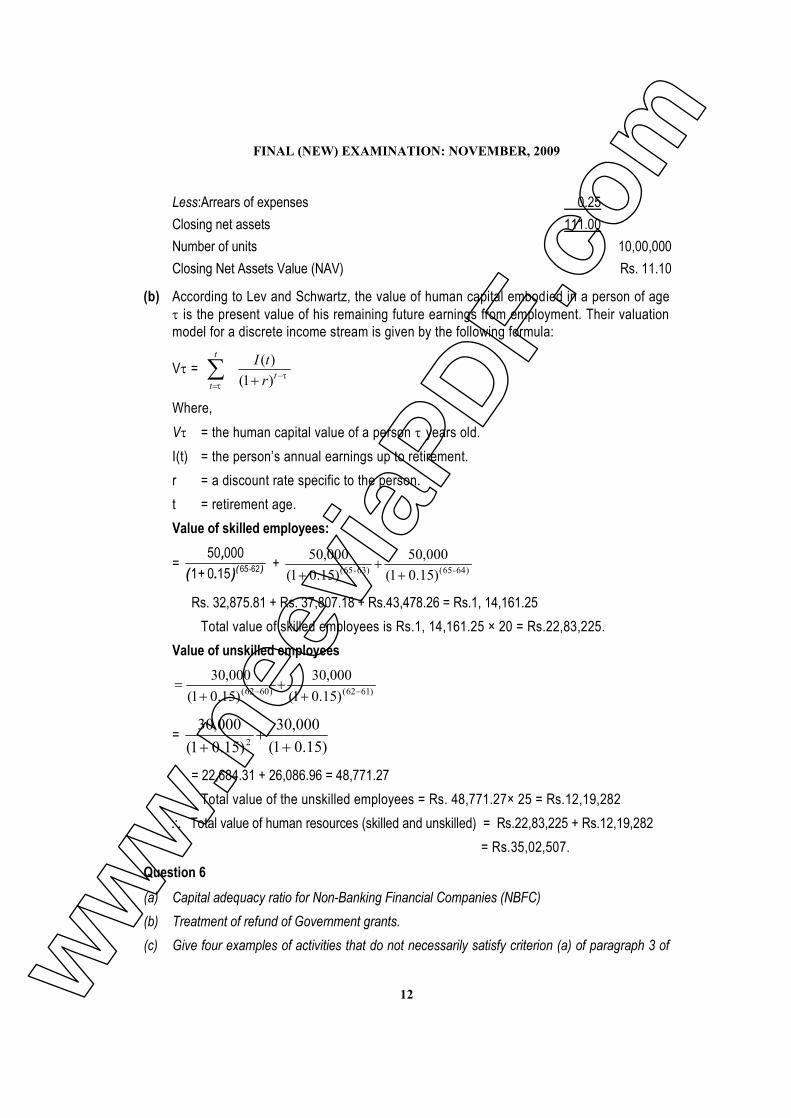

Question 4(a) On 1.4.2008, a mutual fund scheme had 18 lakh units of face value of Rs.10 each was

outstanding. The scheme earned Rs.162 lakhs in 2008-09, out of which Rs.90 lakhs wasearned in the first half of the year. On 30.9.2008, 2 lakh units were sold at a “NAV” ofRs.70.Pass Journal entries for sale of units and distribution of dividend at the end of 2008-09.

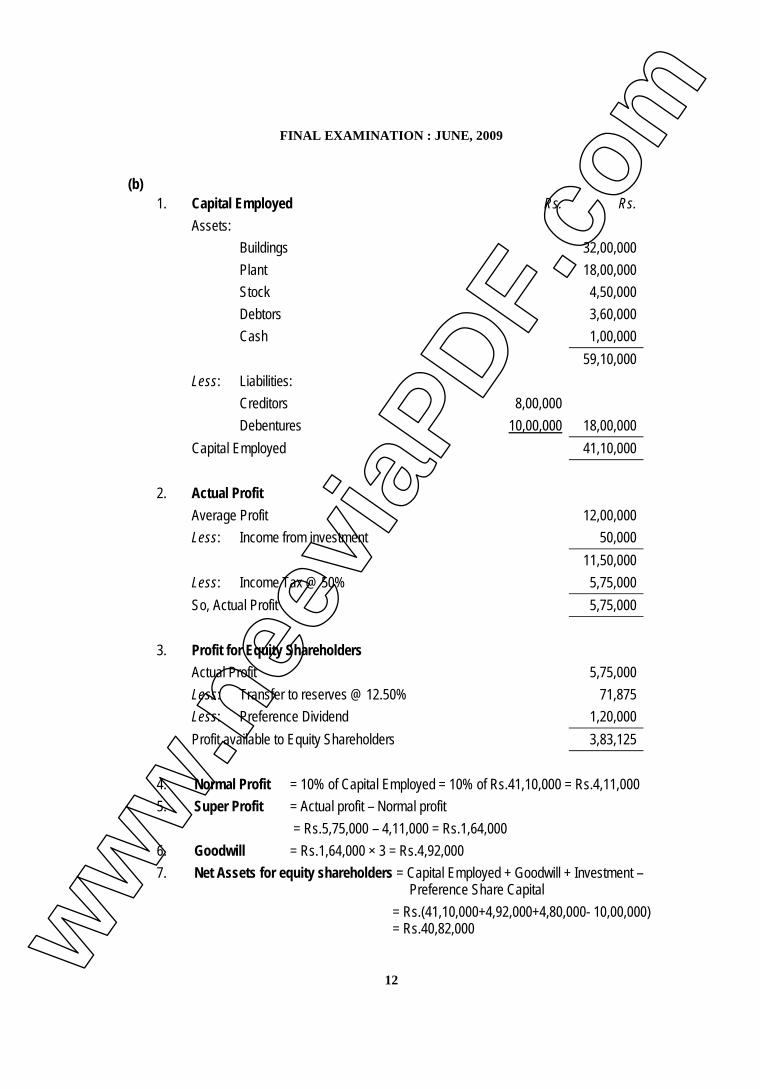

(b) Following is the Balance Sheet of Rampal Limited as on 31st March, 2009:

Liabilities Rs. Assets Rs.1,00,000 equity shares of Rs.10 each 10,00,000 Goodwill 5,00,00010,000, 12% preference shares ofRs.100 each 10,00,000

Buildings 15,00,000

General reserve 6,00,000 Plant 10,00,000Profit and Loss account 4,00,000 Investment in 10% stock 4,80,00015% debentures 10,00,000 Stock-in-trade 6,00,000Creditors 8,00,000 Debtors 4,00,000

Cash 1,00,000Preliminary expenses 2,20,000

48,00,000 48,00,000

Additional information are given below:(a) Nominal value of investment is Rs.5,00,000 and its market value is Rs.5,20,000.(b) Following assets are revalued:

(i) Building Rs.32,00,000(ii) Plant Rs.18,00,000(iii) Stock-in-trade Rs.4,50,000(iv) Debtors Rs.3,60,000

(c) Average profit before tax of the company is Rs.12,00,000 and 12.50% of the profit istransferred to general reserve, rate of taxation being 50%.

(d) Normal dividend expected on equity shares is 8% while fair return on closing capitalemployed is 10%.

(e) Goodwill may be valued at three year’s purchase of super profits.Ascertain the value of each equity share under fair value method. (6+10= 16 Marks)

ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

11

Answer(a)

Allocation of Earnings Old UnitHolders

New UnitHolders

Total

[18 Lakh Units] [2 Lakh Units]Rs. in Lakhs Rs. in Lakhs Rs. in Lakhs

First half year (Rs.5 per unit) 90.00 Nil 90.00Second half year (Rs.3.60 per unit) 64.80 7.20 72.00

154.80 7.20 162.00Add: Equalization payment recovered - - 10.00Available for distribution 172.00Equalization Payment:- Rs.90 lakhs 18 Lakhs = Rs.5 per unit.

Old UnitHolders

New UnitHolders

Rs. Rs.Dividend distributed 8.60 8.60Less: Equilisation payment - 5.00

8.60 3.60

Journal Entries (Rs. in lakhs)30.9.2008 Bank A/c Dr. 150.00

To Unit Capital A/c 20.00To Reserves A/c 120.00To Dividend Equilisation A/c 10.00

(Being the amount received on sale of 2lakhs unit at a NAV of Rs.70/- per Unit)

31.3.2009 Dividend Equalization A/c Dr. 10.00To Revenue A/c 10.00

(Being the amount transferred to RevenueAccount)Revenue A/c Dr. 172.00

To Bank A/c 172.00(Being the amount distributed among 20lakhs unit holders @ Rs.8.60 per unit)

ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

12

(b)1. Capital Employed Rs. Rs.

Assets:Buildings 32,00,000Plant 18,00,000Stock 4,50,000Debtors 3,60,000Cash 1,00,000

59,10,000Less: Liabilities:

Creditors 8,00,000Debentures 10,00,000 18,00,000

Capital Employed 41,10,000

2. Actual ProfitAverage Profit 12,00,000Less: Income from investment 50,000

11,50,000Less: Income Tax @ 50% 5,75,000So, Actual Profit 5,75,000

3. Profit for Equity ShareholdersActual Profit 5,75,000Less: Transfer to reserves @ 12.50% 71,875Less: Preference Dividend 1,20,000Profit available to Equity Shareholders 3,83,125

4. Normal Profit = 10% of Capital Employed = 10% of Rs.41,10,000 = Rs.4,11,0005. Super Profit = Actual profit – Normal profit

= Rs.5,75,000 – 4,11,000 = Rs.1,64,0006. Goodwill = Rs.1,64,000 × 3 = Rs.4,92,0007. Net Assets for equity shareholders = Capital Employed + Goodwill + Investment –

Preference Share Capital= Rs.(41,10,000+4,92,000+4,80,000- 10,00,000)= Rs.40,82,000w

ww

.nee

viaP

DF.c

om

PAPER – 1 : FINANCIAL REPORTING

13

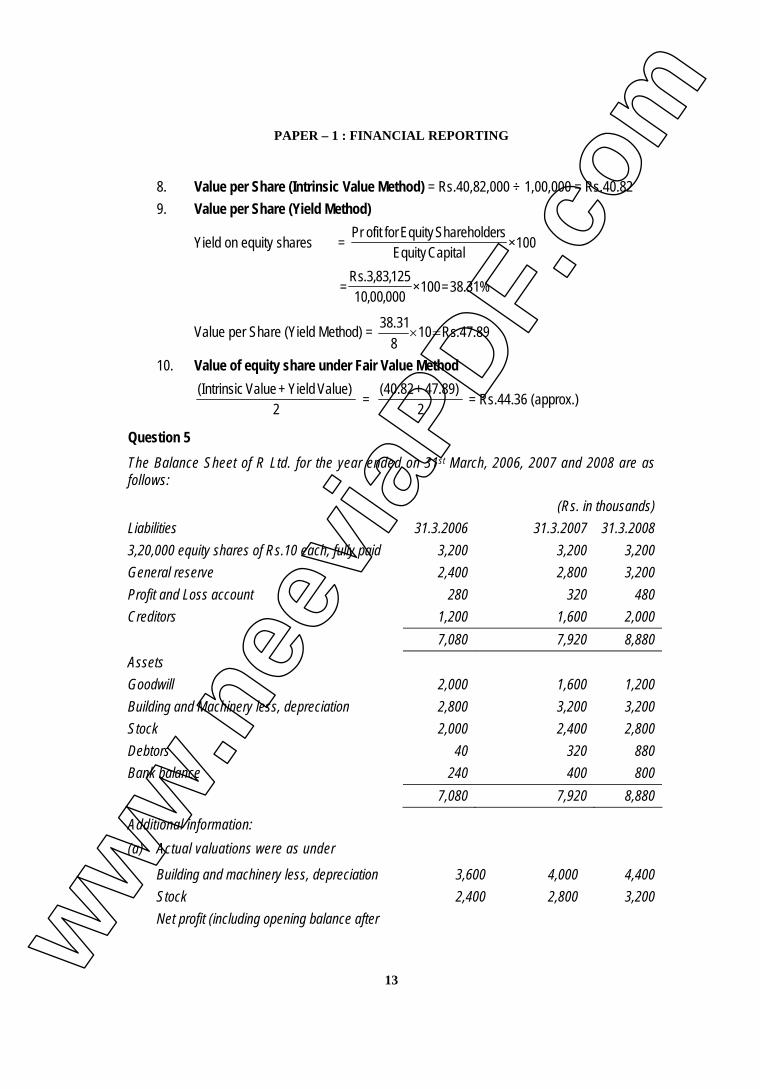

8. Value per Share (Intrinsic Value Method) = Rs.40,82,000 ÷ 1,00,000 = Rs.40.829. Value per Share (Yield Method)

Yield on equity shares = 100×CapitalEquityrsShareholdeEquityforofitPr

%31.38=100×000,00,10125,83,3.Rs

=

Value per Share (Yield Method) = 89.47.Rs10831.38

10. Value of equity share under Fair Value Method

2Value) Yield+Value(Intrinsic

= 247.89)+(40.82

= Rs.44.36 (approx.)

Question 5The Balance Sheet of R Ltd. for the year ended on 31st March, 2006, 2007 and 2008 are asfollows:

(Rs. in thousands)Liabilities 31.3.2006 31.3.2007 31.3.20083,20,000 equity shares of Rs.10 each, fully paid 3,200 3,200 3,200General reserve 2,400 2,800 3,200Profit and Loss account 280 320 480Creditors 1,200 1,600 2,000

7,080 7,920 8,880AssetsGoodwill 2,000 1,600 1,200Building and Machinery less, depreciation 2,800 3,200 3,200Stock 2,000 2,400 2,800Debtors 40 320 880Bank balance 240 400 800

7,080 7,920 8,880

Additional information:(a) Actual valuations were as under

Building and machinery less, depreciation 3,600 4,000 4,400Stock 2,400 2,800 3,200Net profit (including opening balance afterww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

14

writing off depreciation, goodwill, tax provisionand transferred to general reserve) 840 1,240 1,640

(b) Capital employed in the business at market value at the beginning of 2005-06 wasRs.73,20,000 which included the cost of goodwill. The normal annual return on averagecapital employed in the line of business engaged by R Ltd. is 12½%.

(c) The balance in the general reserve on 1st April, 2005 was Rs.20 lakhs.(d) The goodwill shown on 31.3.2006 was purchased on 1.4.2005 for Rs.20 lakhs on which

date the balance in the Profit and Loss account was Rs.2,40,000. Find out the averagecapital employed in each year.

(e) Goodwill is to be valued at 5 year’s purchase of Super profit (Simple average method).Find out the total value of the business as on 31.3.2008. (16 Marks)

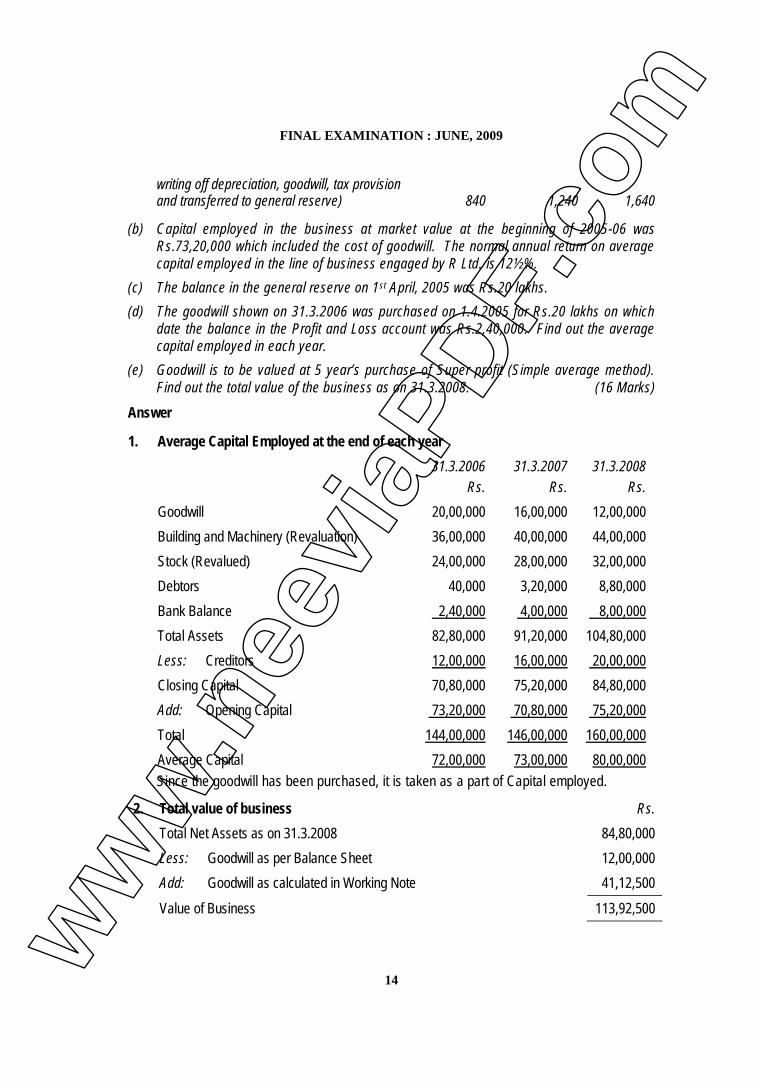

Answer

1. Average Capital Employed at the end of each year31.3.2006

Rs.31.3.2007

Rs.31.3.2008

Rs.Goodwill 20,00,000 16,00,000 12,00,000Building and Machinery (Revaluation) 36,00,000 40,00,000 44,00,000Stock (Revalued) 24,00,000 28,00,000 32,00,000Debtors 40,000 3,20,000 8,80,000Bank Balance 2,40,000 4,00,000 8,00,000Total Assets 82,80,000 91,20,000 104,80,000Less: Creditors 12,00,000 16,00,000 20,00,000Closing Capital 70,80,000 75,20,000 84,80,000Add: Opening Capital 73,20,000 70,80,000 75,20,000Total 144,00,000 146,00,000 160,00,000Average Capital 72,00,000 73,00,000 80,00,000Since the goodwill has been purchased, it is taken as a part of Capital employed.

2. Total value of business Rs.Total Net Assets as on 31.3.2008 84,80,000Less: Goodwill as per Balance Sheet 12,00,000Add: Goodwill as calculated in Working Note 41,12,500

Value of Business 113,92,500

ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

15

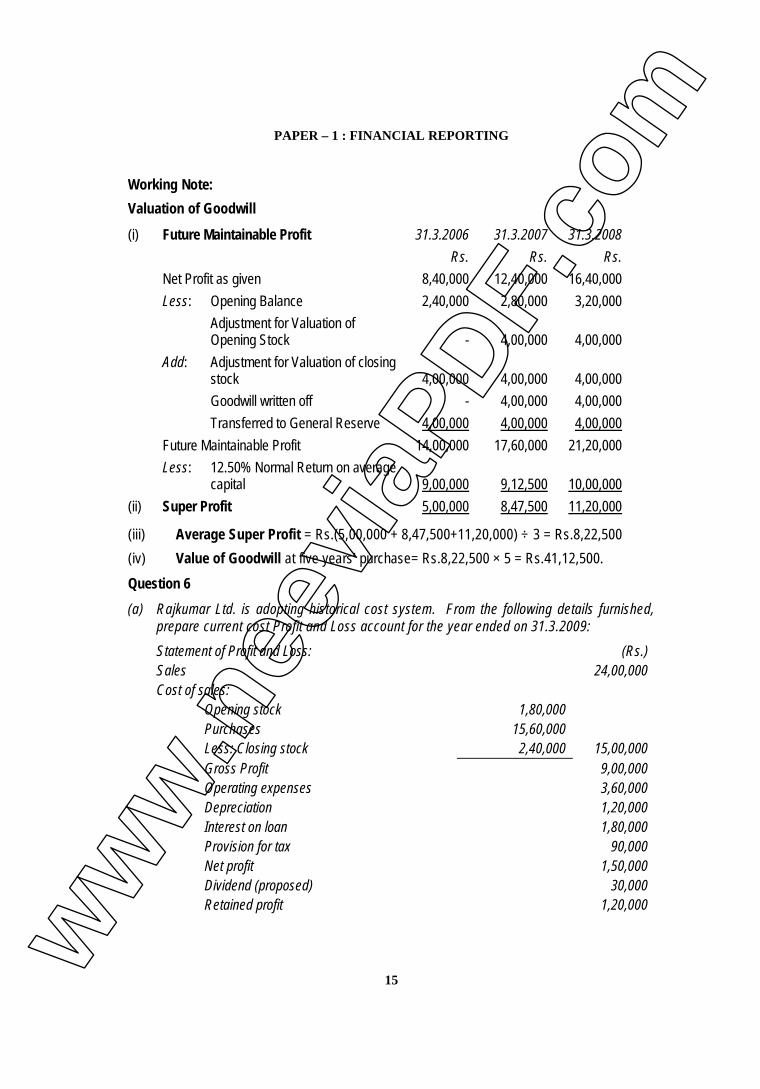

Working Note:Valuation of Goodwill

(i) Future Maintainable Profit 31.3.2006 31.3.2007 31.3.2008Rs. Rs. Rs.

Net Profit as given 8,40,000 12,40,000 16,40,000Less: Opening Balance 2,40,000 2,80,000 3,20,000

Adjustment for Valuation ofOpening Stock - 4,00,000 4,00,000

Add: Adjustment for Valuation of closingstock 4,00,000 4,00,000 4,00,000Goodwill written off - 4,00,000 4,00,000Transferred to General Reserve 4,00,000 4,00,000 4,00,000

Future Maintainable Profit 14,00,000 17,60,000 21,20,000Less: 12.50% Normal Return on average

capital 9,00,000 9,12,500 10,00,000(ii) Super Profit 5,00,000 8,47,500 11,20,000

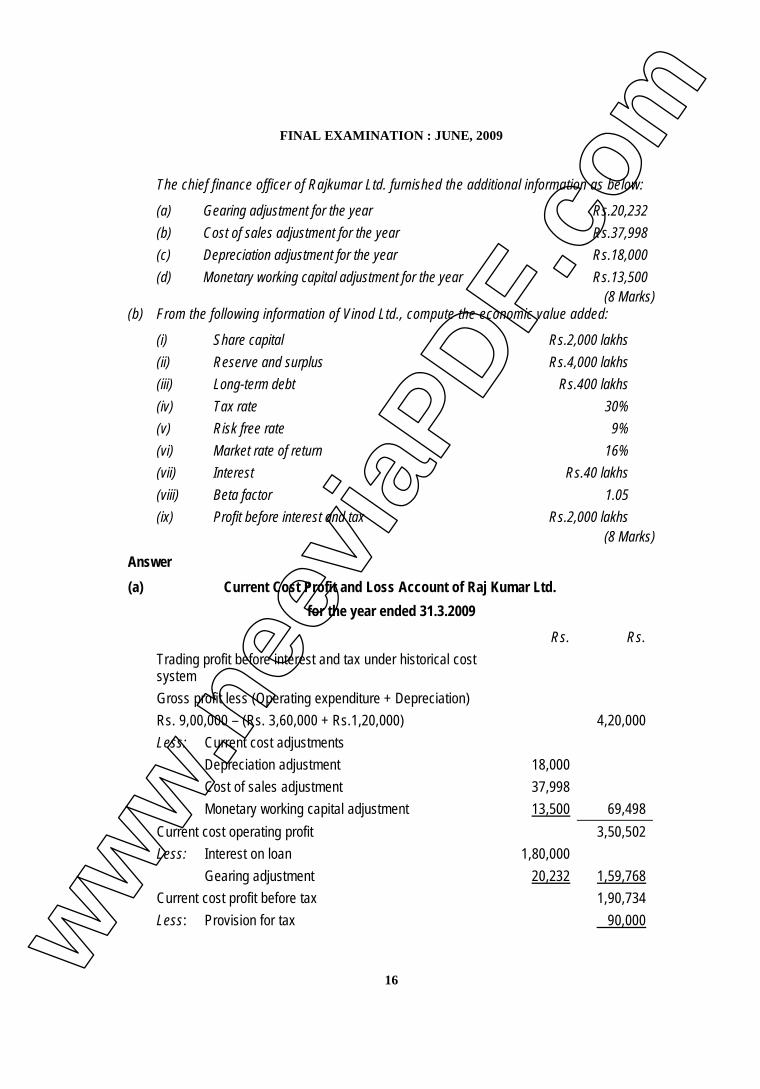

(iii) Average Super Profit = Rs.(5,00,000 + 8,47,500+11,20,000) ÷ 3 = Rs.8,22,500(iv) Value of Goodwill at five years’ purchase= Rs.8,22,500 × 5 = Rs.41,12,500.Question 6(a) Rajkumar Ltd. is adopting historical cost system. From the following details furnished,

prepare current cost Profit and Loss account for the year ended on 31.3.2009:Statement of Profit and Loss: (Rs.)Sales 24,00,000Cost of sales:

Opening stock 1,80,000Purchases 15,60,000Less: Closing stock 2,40,000 15,00,000Gross Profit 9,00,000Operating expenses 3,60,000Depreciation 1,20,000Interest on loan 1,80,000Provision for tax 90,000Net profit 1,50,000Dividend (proposed) 30,000Retained profit 1,20,000

ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

16

The chief finance officer of Rajkumar Ltd. furnished the additional information as below:

(a) Gearing adjustment for the year Rs.20,232(b) Cost of sales adjustment for the year Rs.37,998(c) Depreciation adjustment for the year Rs.18,000(d) Monetary working capital adjustment for the year Rs.13,500

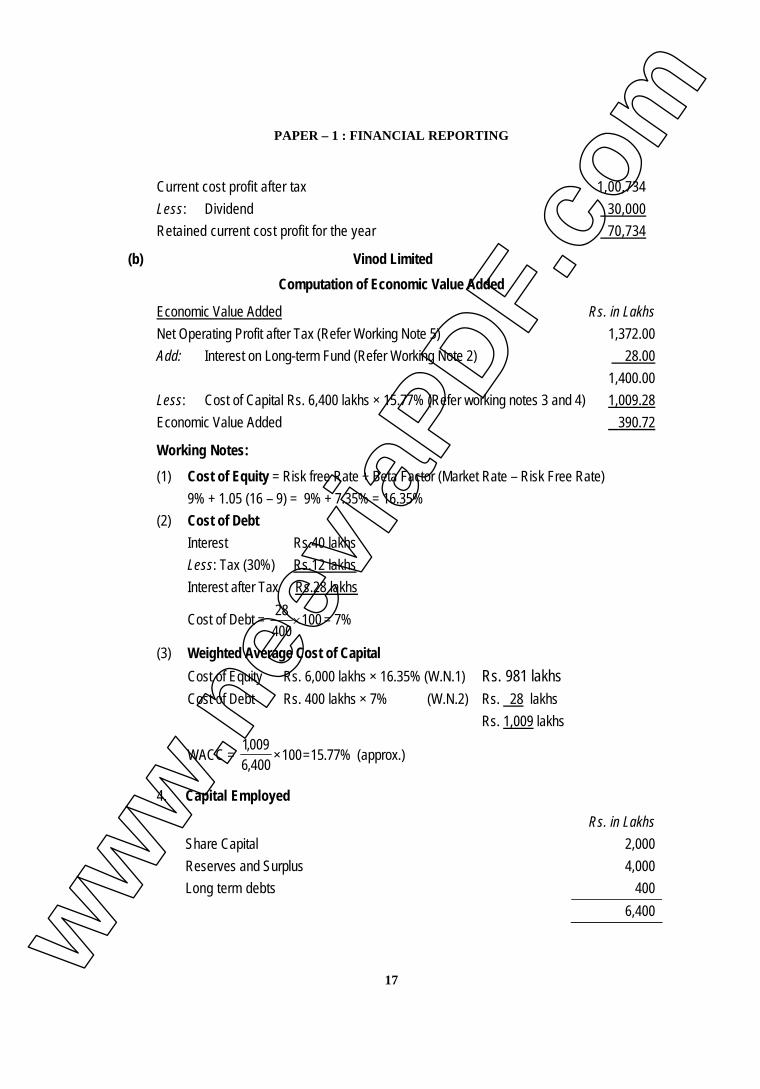

(8 Marks)(b) From the following information of Vinod Ltd., compute the economic value added:

(i) Share capital Rs.2,000 lakhs(ii) Reserve and surplus Rs.4,000 lakhs(iii) Long-term debt Rs.400 lakhs(iv) Tax rate 30%(v) Risk free rate 9%(vi) Market rate of return 16%(vii) Interest Rs.40 lakhs(viii) Beta factor 1.05(ix) Profit before interest and tax Rs.2,000 lakhs

(8 Marks)

Answer(a) Current Cost Profit and Loss Account of Raj Kumar Ltd.

for the year ended 31.3.2009

Rs. Rs.Trading profit before interest and tax under historical costsystemGross profit less (Operating expenditure + Depreciation)Rs. 9,00,000 – (Rs. 3,60,000 + Rs.1,20,000) 4,20,000Less: Current cost adjustments

Depreciation adjustment 18,000Cost of sales adjustment 37,998Monetary working capital adjustment 13,500 69,498

Current cost operating profit 3,50,502Less: Interest on loan 1,80,000

Gearing adjustment 20,232 1,59,768Current cost profit before tax 1,90,734Less: Provision for tax 90,000ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

17

Current cost profit after tax 1,00,734Less: Dividend 30,000Retained current cost profit for the year 70,734

(b) Vinod LimitedComputation of Economic Value Added

Economic Value Added Rs. in LakhsNet Operating Profit after Tax (Refer Working Note 5) 1,372.00Add: Interest on Long-term Fund (Refer Working Note 2) 28.00

1,400.00Less: Cost of Capital Rs. 6,400 lakhs × 15.77% (Refer working notes 3 and 4) 1,009.28Economic Value Added 390.72

Working Notes:

(1) Cost of Equity = Risk free Rate + Beta Factor (Market Rate – Risk Free Rate)9% + 1.05 (16 – 9) = 9% + 7.35% = 16.35%

(2) Cost of DebtInterest Rs.40 lakhsLess: Tax (30%) Rs.12 lakhsInterest after Tax Rs.28 lakhs

Cost of Debt = 10040028

= 7%

(3) Weighted Average Cost of CapitalCost of Equity Rs. 6,000 lakhs × 16.35% (W.N.1) Rs. 981 lakhsCost of Debt Rs. 400 lakhs × 7% (W.N.2) Rs. 28 lakhs

Rs. 1,009 lakhs

WACC = %77.15=100×400,6009,1

(approx.)

4. Capital Employed

Rs. in LakhsShare Capital 2,000Reserves and Surplus 4,000Long term debts 400

6,400ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : JUNE, 2009

18

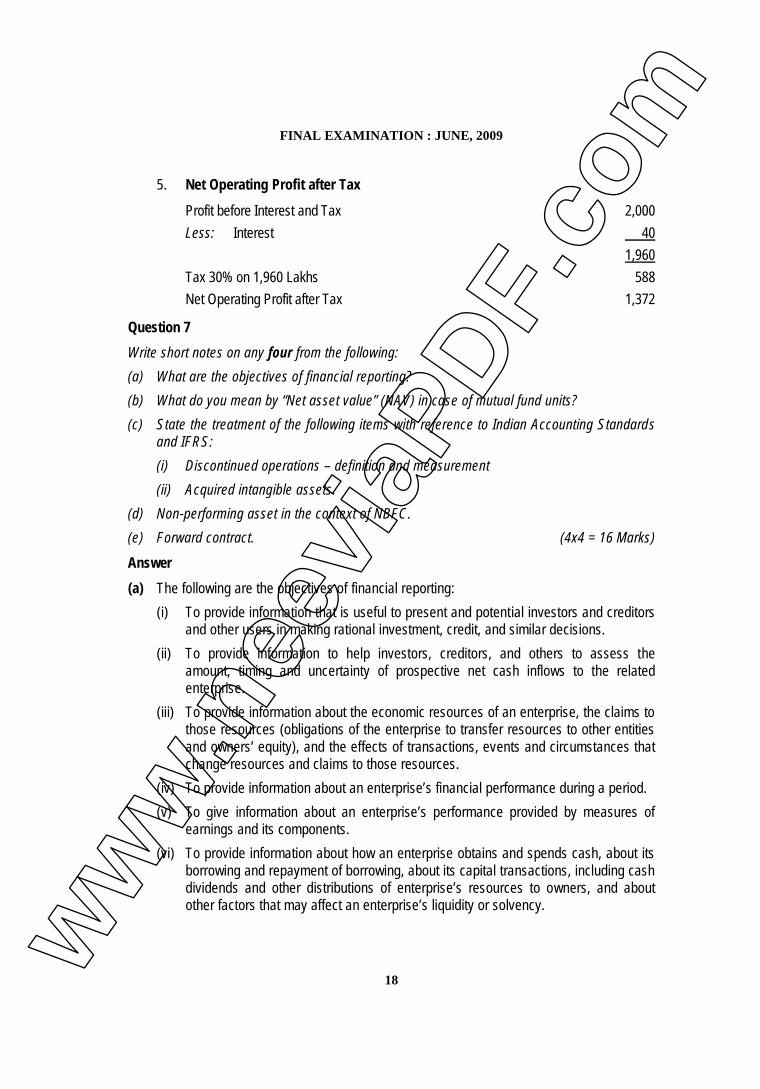

5. Net Operating Profit after Tax

Profit before Interest and Tax 2,000Less: Interest 40

1,960Tax 30% on 1,960 Lakhs 588Net Operating Profit after Tax 1,372

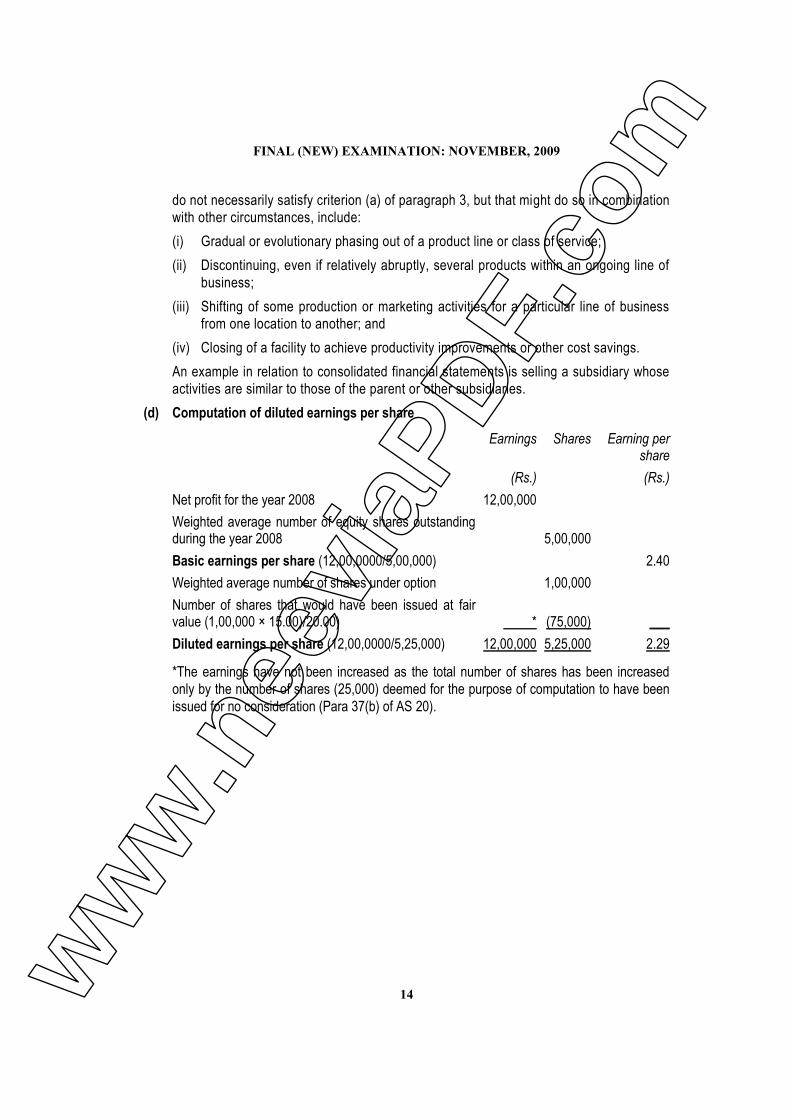

Question 7Write short notes on any four from the following:(a) What are the objectives of financial reporting?(b) What do you mean by “Net asset value” (NAV) in case of mutual fund units?(c) State the treatment of the following items with reference to Indian Accounting Standards

and IFRS:(i) Discontinued operations – definition and measurement(ii) Acquired intangible assets.

(d) Non-performing asset in the context of NBFC.(e) Forward contract. (4x4 = 16 Marks)

Answer(a) The following are the objectives of financial reporting:

(i) To provide information that is useful to present and potential investors and creditorsand other users in making rational investment, credit, and similar decisions.

(ii) To provide information to help investors, creditors, and others to assess theamount, timing and uncertainty of prospective net cash inflows to the relatedenterprise.

(iii) To provide information about the economic resources of an enterprise, the claims tothose resources (obligations of the enterprise to transfer resources to other entitiesand owners’ equity), and the effects of transactions, events and circumstances thatchange resources and claims to those resources.

(iv) To provide information about an enterprise’s financial performance during a period.(v) To give information about an enterprise’s performance provided by measures of

earnings and its components.(vi) To provide information about how an enterprise obtains and spends cash, about its

borrowing and repayment of borrowing, about its capital transactions, including cashdividends and other distributions of enterprise’s resources to owners, and aboutother factors that may affect an enterprise’s liquidity or solvency.

ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

19

(vii) To provide information about how management of an enterprise has discharged itsstewardship responsibility to owners (stockholders) for the use of enterpriseresources entrusted to it.

(viii) To provide information that is useful to managers and directors in making decisionsin the interest of owners.

(b) Mutual funds sell their shares to public and redeem them at current net assets value(NAV) which is calculated as under:–

sizeUnitsliabilitieFundMutual All-holdingsFundMutualallofvaluemarketTotal

The net asset value of a mutual fund scheme is basically the per unit market value of allthe assets of the scheme. Simply stated, NAV is the value of the assets of each unit ofthe scheme. Thus, if the NAV is more than the face value (Rs. 10), it means your moneyhas appreciated and vice versa. NAV also includes dividends, interest accruals andreduction of liabilities and expenses, besides market value of investments. NAV is thevalue of net assets under a mutual fund scheme. The NAV per unit is NAV of the schemedivided by number of units outstanding. NAV of a scheme keeps on changing withchange in market value of portfolio under the scheme.

(c) Treatment under Indian Accounting Standard and IFRSIndian AccountingStandards

IFRS

(i) Discontinuingoperation - definitionand measurement

Operations and cash flowsthat can be clearlydistinguished for financialreporting and representmajor line of business orgeographical area ofoperations are discontinuedoperations.Measurement ofdiscontinued operations isbased on AS 24.

Definition of discontinuedoperations under IFRS issimilar to Indian AccountingStandards. However, it alsoincludes a subsidiaryacquired exclusively with aview to resale. Discontinuedoperations are measured atlower of carrying amount andfair value less cost to sell.

(ii) Acquired intangibleassets

If recognition criteria aresatisfied then it can becapitalized. All intangiblesare amortized over usefullife with rebuttablepresumption of notexceeding 10 years.Revaluations are notpermitted.

If recognition criteria aresatisfied then it can becapitalized. It is amortizedover useful life. Intangiblesassigned an indefinite usefullife are not amortized butreviewed at least annually forimpairment. Revaluationsare permitted in rarecircumstances.w

ww

.nee

viaP

DF.c

om

FINAL EXAMINATION : JUNE, 2009

20

(d) “NonPerforming Asset” as per NBFC Prudential Norms (RBI) directions means:(i) An asset, in respect of which, interest has remained past due for six months;(ii) A term loan inclusive of unpaid interest, when the instalment is overdue for more

than six months of which interest amount remained past due for six months;(iii) A bill which remained overdue for six months;(iv) The interest in respect of a debt or the income on receivables under the head ‘other

current assets’ in the nature of short term loans/advances that remained overdue fora period of six months;

(v) Any dues on account of sales of assets or services rendered or reimbursementexpenses made, which remained overdue for a period of six months;

(vi) The lease rental and hire purchase instalment, which has become overdue for aperiod of more than twelve months;

(vii) In respect of loans, advances and other credit facilities (including bills purchasedand discounted), the balance outstanding under the credit facilities made availableto borrower /beneficiary when anyone of the credit facilities becomes NPA.

However, an NBFC may classify each such account on the basis of record of recovery asregards hire purchase and lease transactions.

(e) A forward contract is an agreement between two parties whereby one party agrees to buyfrom, or sell to, the other party an asset at a future time for an agreed price (usuallyreferred to as the ‘contract price’). The parties to forward contracts may be individuals,corporates or financial institutions. At maturity, a forward contract is settled by deliveryof the asset by the seller to the buyer in return for payment of the contract price. Forexample, a person (X) may enter into a forward contract with another person (Y) on June15, 20x3 to buy 10 kgs. of silver at the end of 90 days at a price of Rs. 8,200 per kg. Atthe end of the 90 days, Y will deliver 10 kgs. of silver to X against payment of Rs. 82,000.If the price of silver, at the end of the 90 days, is Rs. 8,300 per kg., X would make a profitof Rs. 1,000 and Y would lose Rs. 1,000, as X could sell silver bought at Rs. 82,000 forRs. 83,000, whereas Y would have to buy silver for Rs. 83,000 and sell for Rs. 82,000.On the other hand, if the price of silver at the end of the 90 days is Rs. 7,800 per kg., Xwould lose Rs. 4,000, whereas Y would make a profit of Rs. 4,000, as X would have tosell silver bought at Rs. 82,000 for Rs. 78,000, whereas Y would buy silver for Rs.78,000, which he would sell to X at Rs. 82,000.

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING Answer all questions.

Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates.

Question 1 (a) Mr. A bought a forward contract for three months of US $ 1,00,000 on 1st December at

1 US $ = Rs.47.10 when exchange rate was US $ 1 = Rs.47.02. On 31st December when he closed his books, exchange rate was US $ 1 = Rs.47.15. On 31st

(a) It is apparent from the facts given in the question that Mr. A entered into forward exchange contract for speculation purpose

January, he decided to sell the contract at Rs.47.18 per dollar. Show how the profits from contract will be recognised in the books.

(b) Sun Ltd. has entered into a sale contract of Rs.5 crores with X Ltd. during 2009-10 financial year. The profit on this transaction is Rs.1 crore. The delivery of goods to take place during the first month of 2010-11 financial year. In case of failure of Sun Ltd. to deliver within the schedule, a compensation of Rs.1.5 crores is to be paid to X Ltd. Sun Ltd. planned to manufacture the goods during the last month of 2009-10 financial year. As on balance sheet date (31.3.2010), the goods were not manufactured and it was unlikely that Sun Ltd. will be in a position to meet the contractual obligation. (i) Should Sun Ltd. provide for contingency as per AS 29? (ii) Should provision be measured as the excess of compensation to be paid over the

profit? (c) Rainbow Limited borrowed an amount of Rs.150 crores on 1.4.2009 for construction of

boiler plant @ 11% p.a. The plant is expected to be completed in 4 years. The weighted average cost of capital is 13% p.a. The accountant of Rainbow Ltd., capitalised interest of Rs.19.50 crores for the accounting period ending on 31.3.2010. Due to surplus fund out of Rs.150 crores, an income of Rs.3.50 crores was earned and credited to profit and loss account. Comment on the above treatment of accountant with reference to relevant accounting standard.

(d) Y Ltd. is a full tax free enterprise for the first ten years of its existence and is in the second year of its operation. Depreciation timing difference resulting in a tax liability in year 1 and 2 is Rs.200 lakhs and Rs.400 lakhs respectively. From the third year it is expected that the timing difference would reverse each year by Rs.10 lakhs. Assuming tax rate of 40%, find out the deferred tax liability at the end of the second year and any charge to the Profit and Loss account. (4 × 5 = 20 Marks)

Answer

∗

∗ The forward contract is sold before its due date, hence considered as speculative.

. According to paragraphs 38 and 39 of AS

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

2

11(Revised) ‘The Effects of Changes in Foreign Exchange Rates’, gain or loss on forward exchange contracts intended for trading or speculation purpose should be computed by multiplying the foreign currency amount of the forward exchange contract by the difference between the forward rate available at the reporting date for the remaining maturity of the contract and the contracted forward rate (or the forward rate last used to measure a gain or loss on that contract for an earlier period). The gain or loss so computed should be recognised in the statement of profit and loss for the period and the premium or discount on the forward exchange contract is ignored and not recognised separately. In recording such contract, at each balance sheet date, the value of the contract is marked to its current market value and the gain or loss on the contract is recognised.

Thus, the premium on contract i.e., the difference between the contract rate and the spot rate amounting Rs. 8,000 [US$ 1,00,000 x (Rs.47.10 – Rs.47.02)] will be ignored and not be recorded in the books. However, the profit on contract i.e. the difference between the sale rate and contract rate amounting Rs. 8,000 [US$ 1,00,000 x 0.08∗

(c) Para 10 of the AS 16 ‘Borrowing Cost’ states, “To the extent that funds are borrowed specifically for the purpose of obtaining a qualifying asset, the amount of borrowing costs eligible for capitalisation on that asset should be determined as the actual borrowing costs incurred on that borrowing during the period less any income on the temporary investment of those borrowings”. The capitalisation rate should be the weighted average of the borrowing costs applicable to the borrowings of the enterprise that are outstanding

(Rs.47.18 – Rs.47.10)] will be recognized in the books of Mr. A on 31st January.

Note: The answer has been given on the basis that Mr. A is a small and medium-sized entity and AS 30 “Financial Instruments: Recognition and Measurement” is not applicable to him.

(b) (i) AS 29 “Provisions, Contingent Liabilities and Contingent Assets” provides that when an enterprise has a present obligation, as a result of past events, that probably requires an outflow of resources and a reliable estimate can be made of the amount of obligation, a provision should be recognised. Sun Ltd. has the obligation to deliver the goods within the scheduled time as per the contract. It is probable that Sun Ltd. will fail to deliver the goods within the schedule and it is also possible to estimate the amount of compensation. Therefore, Sun Ltd. should provide for the contingency amounting Rs. 1.5 crores as per AS 29.

(ii) Provision should not be measured as the excess of compensation to be paid over the profit. The goods were not manufactured before 31st March, 2010 and no profit had accrued for the financial year 2009-2010. Therefore, provision should be made for the full amount of compensation amounting Rs.1.50 crores.

∗ The current market value of the forward contract on 31st December has not been given in the

question. Therefore, no gain or loss can be recognised in the books on 31st December. The profit amounting Rs. 8,000 will be recognised in the year of sale only.

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

3

during the period, other than borrowings made specifically for the purpose of obtaining a qualifying asset. In the given case, the amount of Rs. 150 crores was specifically borrowed for construction of boiler plant. Therefore, treatment of accountant of Rainbow Ltd. is not correct and the amount of borrowing costs to be capitalised for the financial year 2009-10 should be calculated as follows:

Rs. (in crores) Interest paid for 2009-10 (11% on Rs.150 crores) 16.50

Less: Income on temporary investment from specific borrowings 3.50 Borrowing costs to be capitalised during 2009-10 13.00

(d) As per Accounting Standards Interpretation (ASI) 5∗

“Accounting for Taxes on Income in the situations of Tax Holiday under sections 10A and 10B of the Income-tax Act, 1961 Accounting Standard (AS) 22, Accounting for Taxes on Income”, deferred tax in respect of timing differences which originate during the tax holiday period and reverse during the tax holiday period, should not be recognised to the extent deduction from the total income of an enterprise is allowed during the tax holiday period as per the provisions of sections 10A and 10B of the Income-tax Act. Deferred tax in respect of timing differences which originate during the tax holiday period but reverse after the tax holiday period should be recognised in the year in which the timing differences originate. However, recognition of deferred tax assets should be subject to the consideration of prudence as laid down in AS 22. For this purpose, the timing differences which originate first should be considered to reverse first. Out of Rs. 200 lakhs depreciation timing difference, amount of Rs. 80 lakhs (Rs. 10 lakhs x 8 years) will reverse in the tax holiday period and therefore, should not be recognised. However, for Rs. 120 lakhs (Rs. 200 lakhs – Rs. 80 lakhs), deferred tax liability will be recognised for Rs. 48 lakhs (40% of Rs. 120 lakhs) in first year. In the second year, the entire amount of timing difference of Rs. 400 lakhs will reverse only after tax holiday period and hence, will be recognised in full. Deferred tax liability amounting Rs. 160 lakhs (40% of Rs. 400 lakhs) will be created by charging it to profit and loss account and the total balance of deferred tax liability account at the end of second year will be Rs. 208 lakhs (48 lakhs + 160 lakhs).

Question 2 (a) While closing its books of account as on 31.12.2009 a non-banking finance company

(NBFC) has its advances classified as under: Rs. in lakhs

Standard assets 10,000 Sub-standard assets 1,000 Secured portion of doubtful debts

∗ This ASI has been incorporated as an explanation to para 13 of the notified AS 22.

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

4

-Upto one year 160 -One year to three year 70 -More than three years 20 Unsecured portion of doubtful debts 90 Loss assets 30

Calculate the provision to be made against advances by NBFC as per prudential norms. (b) Comforts Ltd. granted Rs.10,00,000 loan to its employees on January 1, 2009 at a

concessional interest rate of 4% per annum. Loan is to be repaid in five equal annual instalments along with interest. Market rate of interest for such loan is 10% per annum. Following the principles of recognition and measurement as laid down in AS 30 ‘Financial Instruments : Recognition and Measurement’, record the entries for the year ended 31st

Year end

December, 2009 for the loan transaction, and also calculate the value of loan initially to be recognised and amortised cost for all the subsequent years. The present value of Re.1 receivable at the end of each year based on discount factor of 10% can be taken as:

1 0.9090

2 0.8263 3 0.7512

4 0.6829 5 0.6208

(4 + 12 = 16 Marks) Answer (a) Calculation of provision on advances as on 31.12.2009

Amount Provision Rs. in lakhs % Rs. in lakhs Standard assets 10,000 Zero Nil Sub standard assets 1,000 10% 100 Secured portion of doubtful debts Upto one year 160 20% 32 One year to three years 70 30% 21 More than three years 20 50% 10 Unsecured portion of doubtful debts 90 100% 90 Loss assets 30 100% 30 Total provision 283

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

5

(b) (i) Journal Entries in the books of Comfort Ltd. for the year ended 31st December, 2009 (regarding loan to employees)

Dr. Amount

(Rs.)

Cr. Amount

(Rs.)

Staff loan A/c Dr. 10,00,000 To Bank A/c 10,00,000 (Being the disbursement of loans to staff)

Staff cost A/c (10,00,000 – 8,54,763) [Refer part (ii)]

Dr. 1,45,237

To Staff loan A/c 1,45,237 (Being the write off of excess of loan balance over present value thereof, in order to reflect the loan at its present value of Rs. 8,54,763)

Staff loan A/c Dr. 85,476 To Interest on staff loan A/c 85,476 (Being the charge of interest @ market rate of 10% to the loan)

Bank A/c Dr. 2,40,000 To Staff loan A/c 2,40,000 (Being the repayment of first instalment with interest for the year)

Interest on staff loan A/c Dr. 85,476 To Profit and loss A/c 85,476 (Being transfer of balance in staff loan Interest account to profit and loss account)

Profit and loss A/c Dr. 1,45,237 To Staff cost A/c 1,45,237 (Being transfer of balance in staff cost account to profit and loss account)

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

6

(ii) Calculation of initial recognition amount of loan to employees

Cash Inflow Total P.V. factor Present

value Year end

Principal Interest @ 4%

Rs. Rs. Rs. Rs. 2009 2,00,000 40,000 2,40,000 0.9090 2,18,160 2010 2,00,000 32,000 2,32,000 0.8263 1,91,702 2011 2,00,000 24,000 2,24,000 0.7512 1,68,269 2012 2,00,000 16,000 2,16,000 0.6829 1,47,506 2013 2,00,000 8,000 2,08,000 0.6208 1,29,126

Present value or Fair value 8,54,763 (iii) Calculation of amortised cost of loan to employees

Year

Amortised cost (Opening balance)

[1]

Interest to be recognised@10%

[2]

Repayment (including interest)

[3]

Amortised Cost

(Closing balance)

[4]=[1]+ [2] – [3]

Rs. Rs. Rs. Rs. 2009 8,54,763 85,476 2,40,000 7,00,239 2010 7,00,239 70,024 2,32,000 5,38,263 2011 5,38,263 53,826 2,24,000 3,68,089 2012 3,68,089 36,809 2,16,000 1,88,898 2013 1,88,898 19,102 (Bal. fig.)∗ 2,08,000 Nil

Question 3 The draft Balance Sheet of three companies, W, H, O, as at 31.3.2010 is as under:

Rs. in thousands Assets W H O Fixed assets 697 648 349 Investments 1,60,000 shares in H 562 --- ---

∗ The difference of Rs. 212 (Rs. 19,102 - Rs. 18,890) is due to approximation in computations.

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

7

80,000 shares in O 184 --- --- Cash at bank 101 95 80 Trade receivables 386 321 251 Inventory 495 389 287

Total 2,425 1,453 967 Liabilities Share capital (Nominal value Re.1 per share)

600 200 200

Reserves 1,050 850 478 Trade payables 375 253 189 Debentures 400 150 100

Total 2,425 1,453 967 You are given the following information: (a) W purchased the shares in H on 13.10.2005 when the balance in reserves was Rs.500

thousands. (b) The shares in O were purchased on 11.5.2005 when the balance in reserves was Rs.242

thousands. (c) The following dividend have been declared but not accounted for before the accounting

year end.

W - Rs.65 thousands H - Rs.30 thousands O - Rs.15 thousands

(d) Included in inventory figure of O is inventory valued at Rs.20 thousands which had been purchased from W at cost plus 25%.

(e) Goodwill in respect of the acquisition of H has been fully written off. (f) On 31.3.2010 H made bonus issue of one share for every share held. This had not been

accounted in the balance sheet as on 31.3.2010. (g) Included in trade payables of W is Rs.18 thousands to O, which is included in trade

receivables of O. Prepare Consolidated Balance Sheet of W as at 31.3.2010. (16 Marks)

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

8

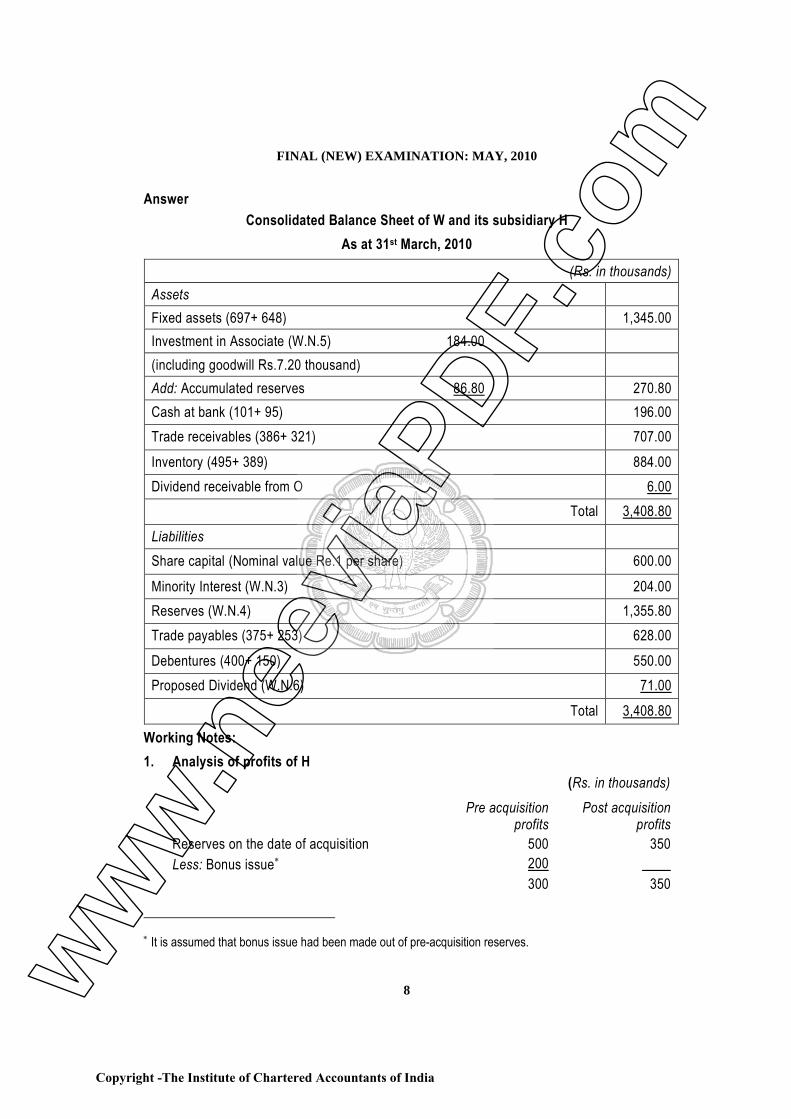

Answer Consolidated Balance Sheet of W and its subsidiary H

As at 31st March, 2010

(Rs. in thousands) Assets Fixed assets (697+ 648) 1,345.00 Investment in Associate (W.N.5) 184.00 (including goodwill Rs.7.20 thousand) Add: Accumulated reserves 86.80 270.80 Cash at bank (101+ 95) 196.00 Trade receivables (386+ 321) 707.00 Inventory (495+ 389) 884.00 Dividend receivable from O 6.00

Total 3,408.80 Liabilities Share capital (Nominal value Re.1 per share) 600.00 Minority Interest (W.N.3) 204.00 Reserves (W.N.4) 1,355.80 Trade payables (375+ 253) 628.00 Debentures (400+ 150) 550.00 Proposed Dividend (W.N.6) 71.00

Total 3,408.80

Working Notes: 1. Analysis of profits of H

(Rs. in thousands)

Pre acquisition profits

Post acquisition profits

Reserves on the date of acquisition 500 350 Less: Bonus issue∗ 200 300 350

∗ It is assumed that bonus issue had been made out of pre-acquisition reserves.

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

9

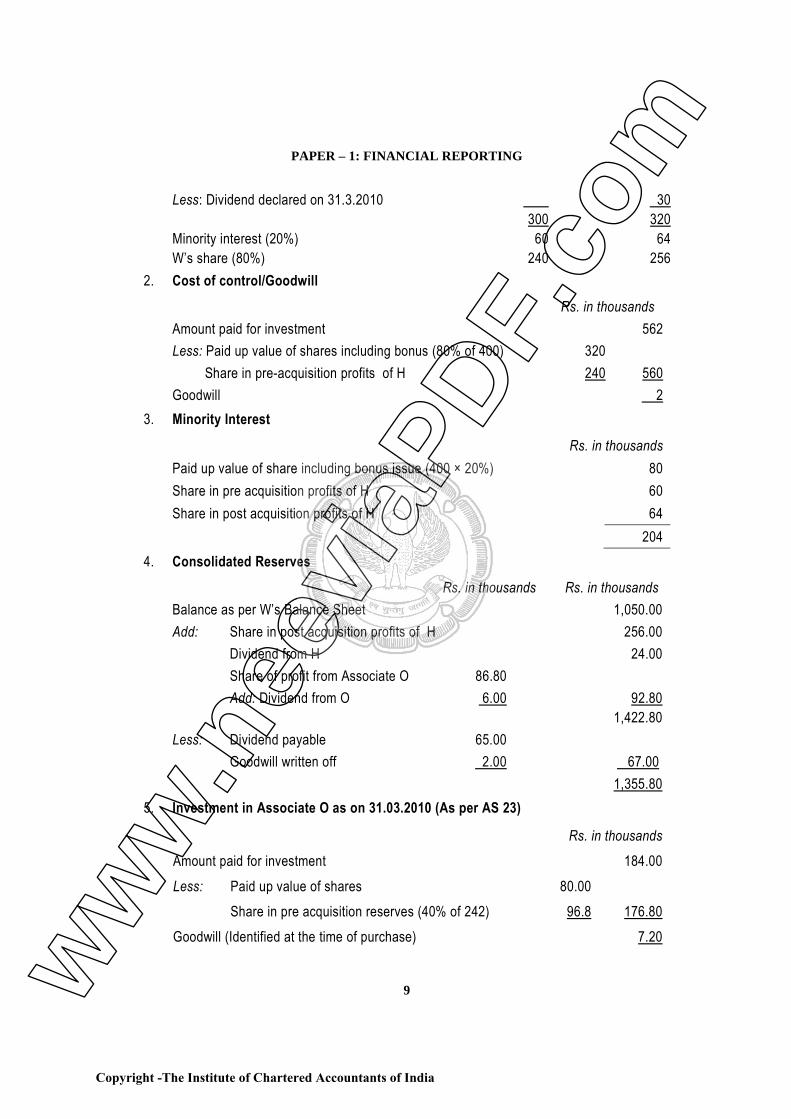

Less: Dividend declared on 31.3.2010 30 300 320 Minority interest (20%) 60 64 W’s share (80%) 240 256

2. Cost of control/Goodwill

Rs. in thousands Amount paid for investment 562 Less: Paid up value of shares including bonus (80% of 400) 320 Share in pre-acquisition profits of H 240 560 Goodwill 2

3. Minority Interest

Rs. in thousands Paid up value of share including bonus issue (400 × 20%) 80 Share in pre acquisition profits of H 60 Share in post acquisition profits of H 64 204

4. Consolidated Reserves

Rs. in thousands Rs. in thousands Balance as per W’s Balance Sheet 1,050.00 Add: Share in post acquisition profits of H 256.00 Dividend from H 24.00 Share of profit from Associate O 86.80 Add: Dividend from O 6.00 92.80

1,422.80 Less: Dividend payable 65.00 Goodwill written off 2.00 67.00 1,355.80

5. Investment in Associate O as on 31.03.2010 (As per AS 23)

Rs. in thousands Amount paid for investment 184.00 Less: Paid up value of shares 80.00 Share in pre acquisition reserves (40% of 242) 96.8 176.80 Goodwill (Identified at the time of purchase) 7.20

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

10

Initial cost 184.00 Add: Increase in equity reserves [40% of (478 – 15 – 242)] 88.40

Less: Unrealised profit ( %40)1252520 ×× ) (1.60) 86.80

Investment in Associate O as on 31.03.10 270.80 Share of profit from Associate O ( 270.80 – 184 + 6 ) 92.80

6. Proposed Dividend

Rs. in thousands W 65 Minority Interest (30 – 24) 6 71

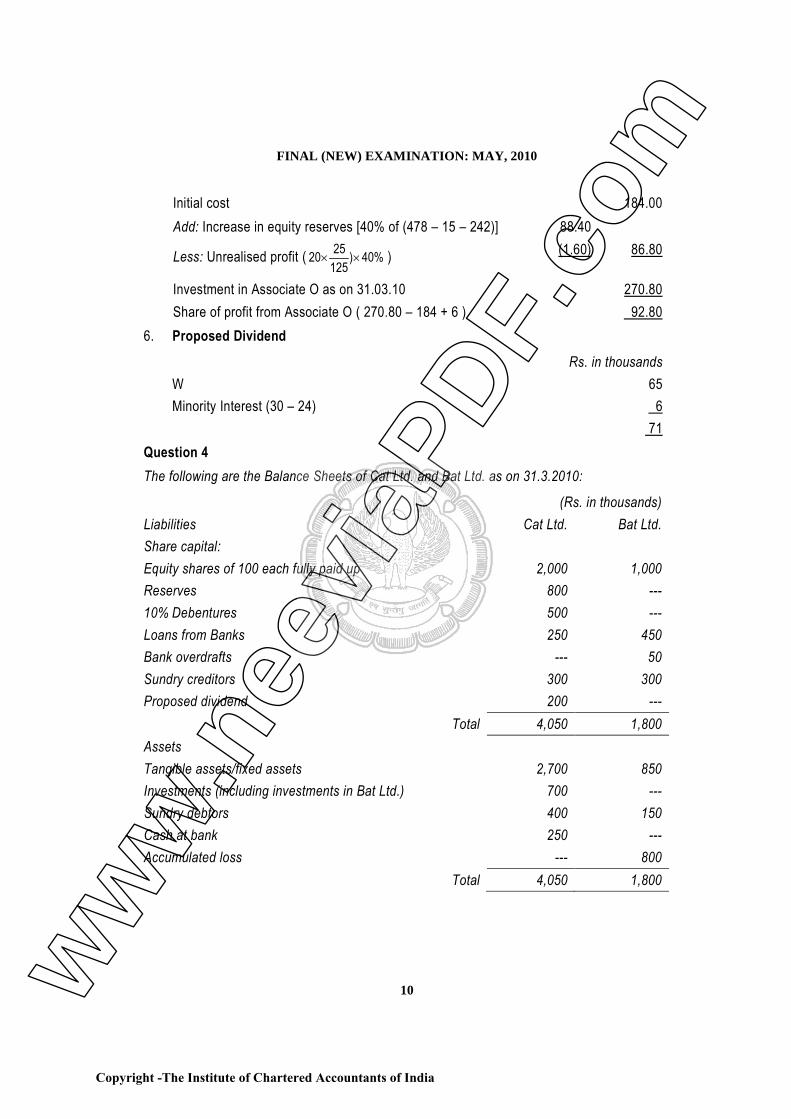

Question 4 The following are the Balance Sheets of Cat Ltd. and Bat Ltd. as on 31.3.2010:

(Rs. in thousands) Liabilities Cat Ltd. Bat Ltd. Share capital: Equity shares of 100 each fully paid up 2,000 1,000 Reserves 800 --- 10% Debentures 500 --- Loans from Banks 250 450 Bank overdrafts --- 50 Sundry creditors 300 300 Proposed dividend 200 ---

Total 4,050 1,800 Assets Tangible assets/fixed assets 2,700 850 Investments (including investments in Bat Ltd.) 700 --- Sundry debtors 400 150 Cash at bank 250 --- Accumulated loss --- 800

Total 4,050 1,800

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

11

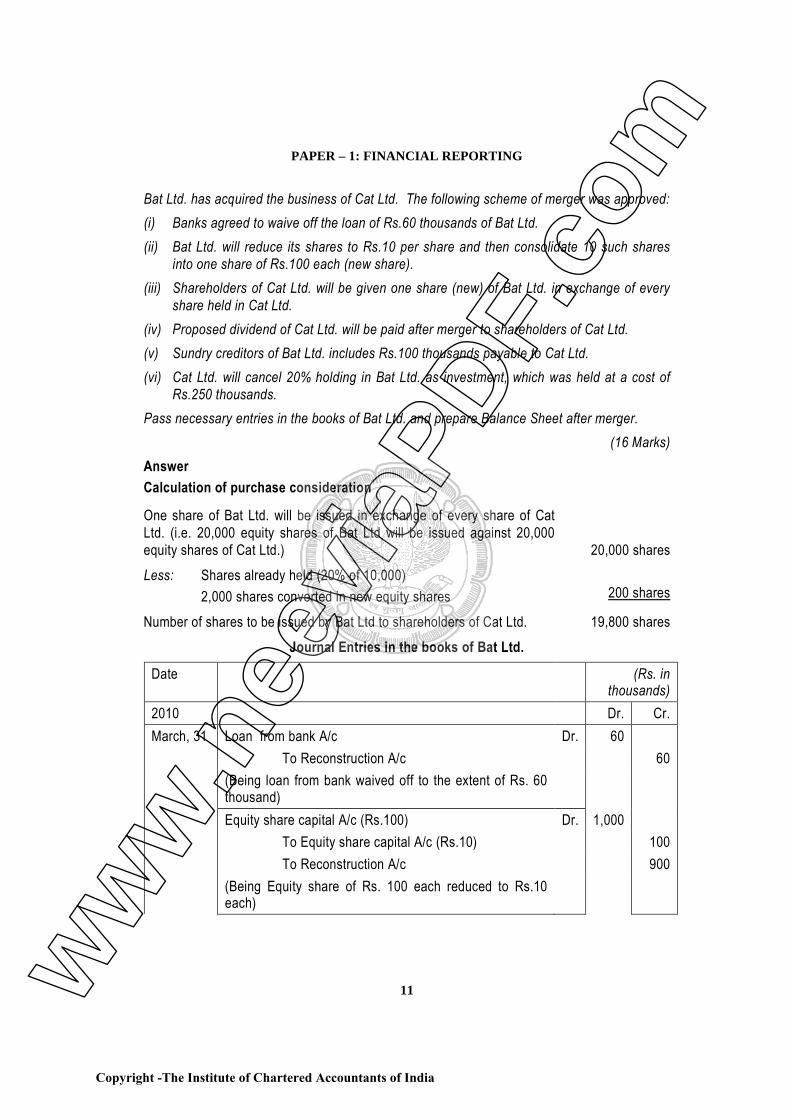

Bat Ltd. has acquired the business of Cat Ltd. The following scheme of merger was approved: (i) Banks agreed to waive off the loan of Rs.60 thousands of Bat Ltd. (ii) Bat Ltd. will reduce its shares to Rs.10 per share and then consolidate 10 such shares

into one share of Rs.100 each (new share). (iii) Shareholders of Cat Ltd. will be given one share (new) of Bat Ltd. in exchange of every

share held in Cat Ltd. (iv) Proposed dividend of Cat Ltd. will be paid after merger to shareholders of Cat Ltd. (v) Sundry creditors of Bat Ltd. includes Rs.100 thousands payable to Cat Ltd. (vi) Cat Ltd. will cancel 20% holding in Bat Ltd. as investment, which was held at a cost of

Rs.250 thousands. Pass necessary entries in the books of Bat Ltd. and prepare Balance Sheet after merger.

(16 Marks) Answer Calculation of purchase consideration

One share of Bat Ltd. will be issued in exchange of every share of Cat Ltd. (i.e. 20,000 equity shares of Bat Ltd will be issued against 20,000 equity shares of Cat Ltd.)

20,000 shares Less: Shares already held (20% of 10,000) 2,000 shares converted in new equity shares

200 shares

Number of shares to be issued by Bat Ltd to shareholders of Cat Ltd. 19,800 shares Journal Entries in the books of Bat Ltd.

Date

(Rs. in thousands)

2010 Dr. Cr. March, 31 Loan from bank A/c Dr. 60 To Reconstruction A/c 60 (Being loan from bank waived off to the extent of Rs. 60

thousand)

Equity share capital A/c (Rs.100) Dr. 1,000 To Equity share capital A/c (Rs.10) 100 To Reconstruction A/c 900 (Being Equity share of Rs. 100 each reduced to Rs.10

each)

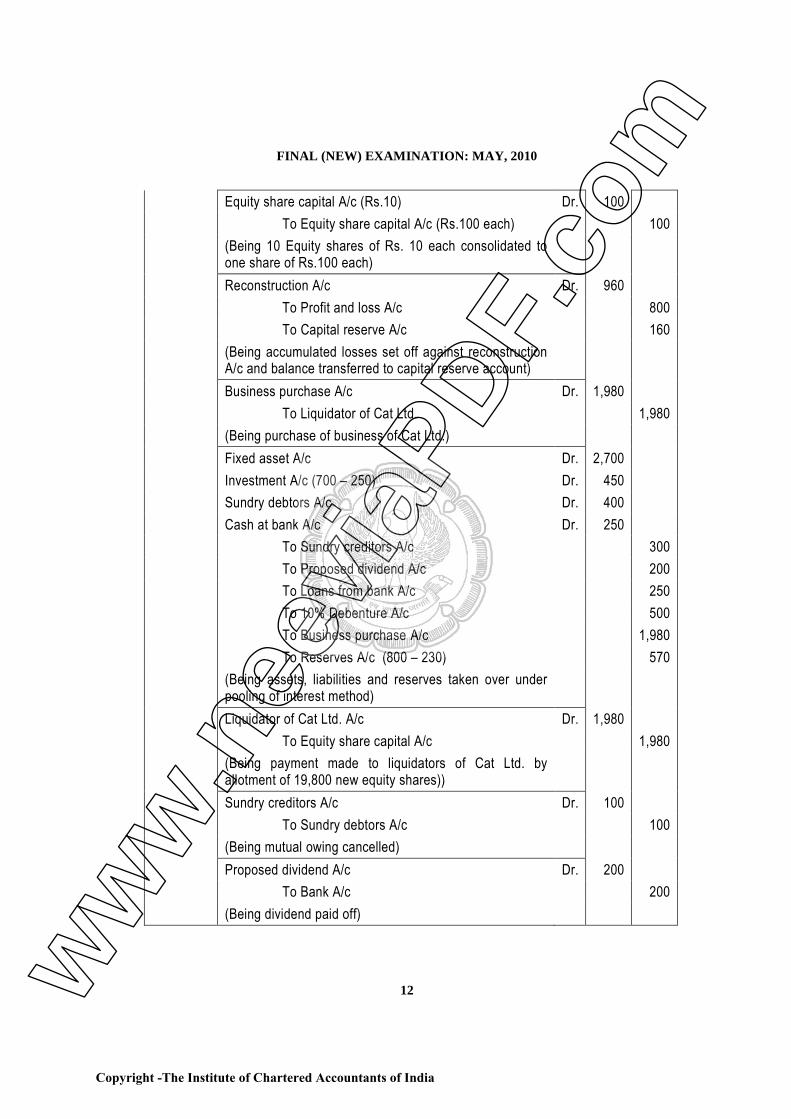

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

12

Equity share capital A/c (Rs.10) Dr. 100 To Equity share capital A/c (Rs.100 each) 100 (Being 10 Equity shares of Rs. 10 each consolidated to

one share of Rs.100 each)

Reconstruction A/c Dr. 960 To Profit and loss A/c 800 To Capital reserve A/c 160 (Being accumulated losses set off against reconstruction

A/c and balance transferred to capital reserve account)

Business purchase A/c Dr. 1,980 To Liquidator of Cat Ltd. 1,980 (Being purchase of business of Cat Ltd.) Fixed asset A/c Dr. 2,700 Investment A/c (700 – 250) Dr. 450 Sundry debtors A/c Dr. 400 Cash at bank A/c Dr. 250 To Sundry creditors A/c 300 To Proposed dividend A/c 200 To Loans from bank A/c 250 To 10% Debenture A/c 500 To Business purchase A/c 1,980 To Reserves A/c (800 – 230) 570 (Being assets, liabilities and reserves taken over under

pooling of interest method)

Liquidator of Cat Ltd. A/c Dr. 1,980 To Equity share capital A/c 1,980 (Being payment made to liquidators of Cat Ltd. by

allotment of 19,800 new equity shares))

Sundry creditors A/c Dr. 100 To Sundry debtors A/c 100 (Being mutual owing cancelled) Proposed dividend A/c Dr. 200 To Bank A/c 200 (Being dividend paid off)

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

13

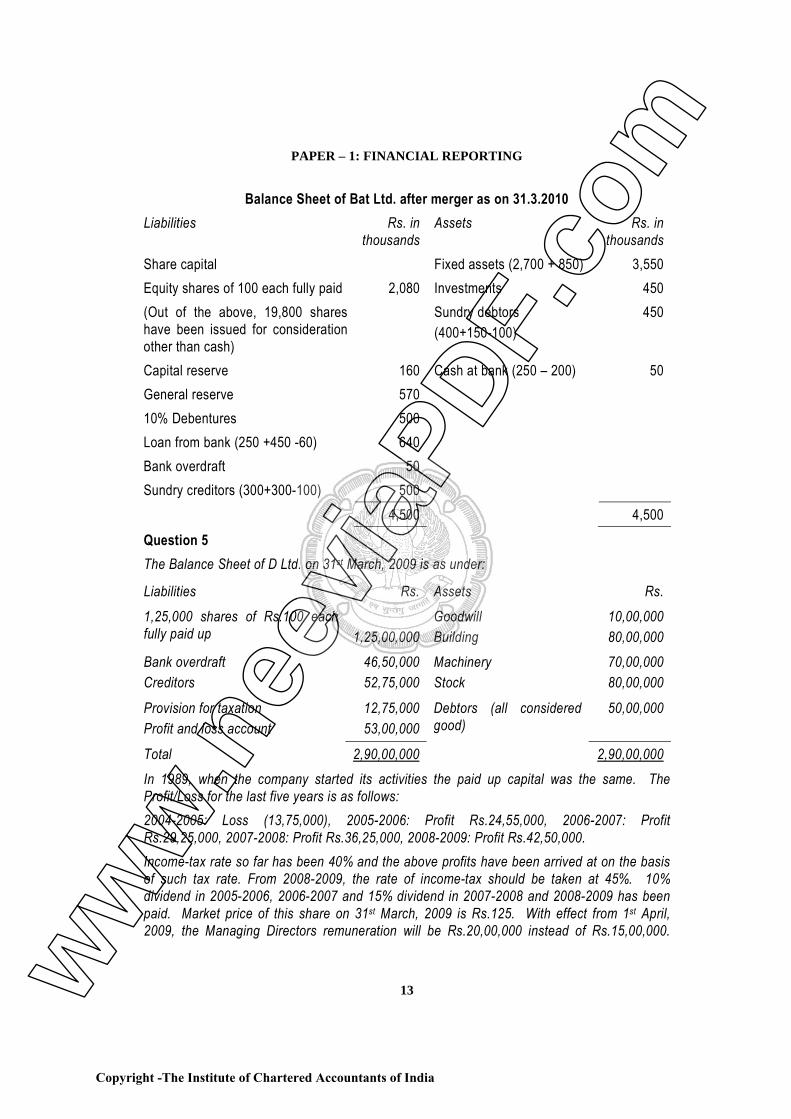

Balance Sheet of Bat Ltd. after merger as on 31.3.2010 Liabilities Rs. in

thousands Assets Rs. in

thousands Share capital Fixed assets (2,700 + 850) 3,550 Equity shares of 100 each fully paid 2,080 Investments 450 (Out of the above, 19,800 shares have been issued for consideration other than cash)

Sundry debtors (400+150-100)

450

Capital reserve 160 Cash at bank (250 – 200) 50 General reserve 570 10% Debentures 500 Loan from bank (250 +450 -60) 640 Bank overdraft 50 Sundry creditors (300+300-100) 500 4,500 4,500 Question 5 The Balance Sheet of D Ltd. on 31st

Liabilities

March, 2009 is as under:

Rs. Assets Rs.

1,25,000 shares of Rs.100 each fully paid up

1,25,00,000

Goodwill Building

10,00,000 80,00,000

Bank overdraft Creditors

46,50,000 52,75,000

Machinery Stock

70,00,000 80,00,000

Provision for taxation Profit and loss account

12,75,000 53,00,000

Debtors (all considered good)

50,00,000

Total 2,90,00,000 2,90,00,000

In 1989, when the company started its activities the paid up capital was the same. The Profit/Loss for the last five years is as follows: 2004-2005: Loss (13,75,000), 2005-2006: Profit Rs.24,55,000, 2006-2007: Profit Rs.29,25,000, 2007-2008: Profit Rs.36,25,000, 2008-2009: Profit Rs.42,50,000. Income-tax rate so far has been 40% and the above profits have been arrived at on the basis of such tax rate. From 2008-2009, the rate of income-tax should be taken at 45%. 10% dividend in 2005-2006, 2006-2007 and 15% dividend in 2007-2008 and 2008-2009 has been paid. Market price of this share on 31st March, 2009 is Rs.125. With effect from 1st April, 2009, the Managing Directors remuneration will be Rs.20,00,000 instead of Rs.15,00,000.

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

14

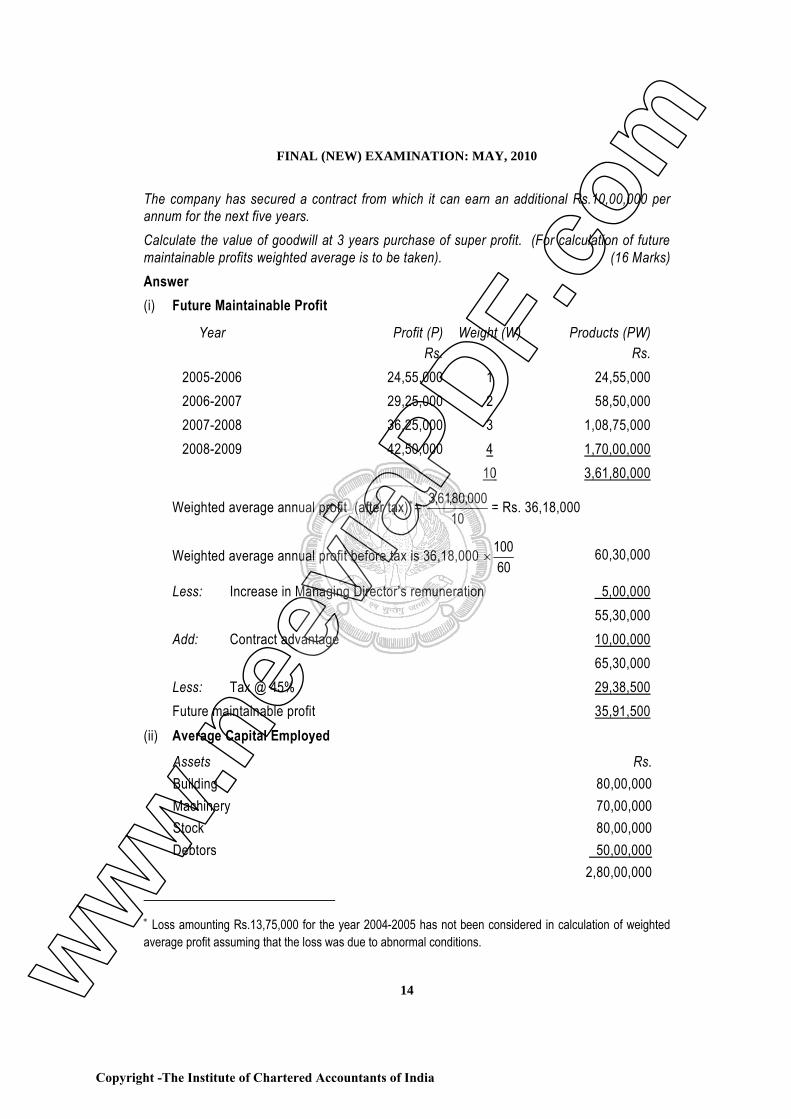

The company has secured a contract from which it can earn an additional Rs.10,00,000 per annum for the next five years. Calculate the value of goodwill at 3 years purchase of super profit. (For calculation of future maintainable profits weighted average is to be taken). (16 Marks) Answer (i) Future Maintainable Profit

Year Profit (P) Rs.

Weight (W) Products (PW) Rs.

2005-2006 24,55,000 1 24,55,000 2006-2007 29,25,000 2 58,50,000 2007-2008 36,25,000 3 1,08,75,000 2008-2009 42,50,000 4 1,70,00,000

10 3,61,80,000

Weighted average annual profit (after tax)∗10

000,80,61,3= = Rs. 36,18,000

Weighted average annual profit before tax is 36,18,000 10060

× 60,30,000

Less: Increase in Managing Director’s remuneration 5,00,000 55,30,000 Add: Contract advantage 10,00,000 65,30,000 Less: Tax @ 45% 29,38,500 Future maintainable profit 35,91,500

(ii) Average Capital Employed

Assets Rs. Building 80,00,000 Machinery 70,00,000 Stock 80,00,000 Debtors 50,00,000 2,80,00,000

∗ Loss amounting Rs.13,75,000 for the year 2004-2005 has not been considered in calculation of weighted average profit assuming that the loss was due to abnormal conditions.

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

15

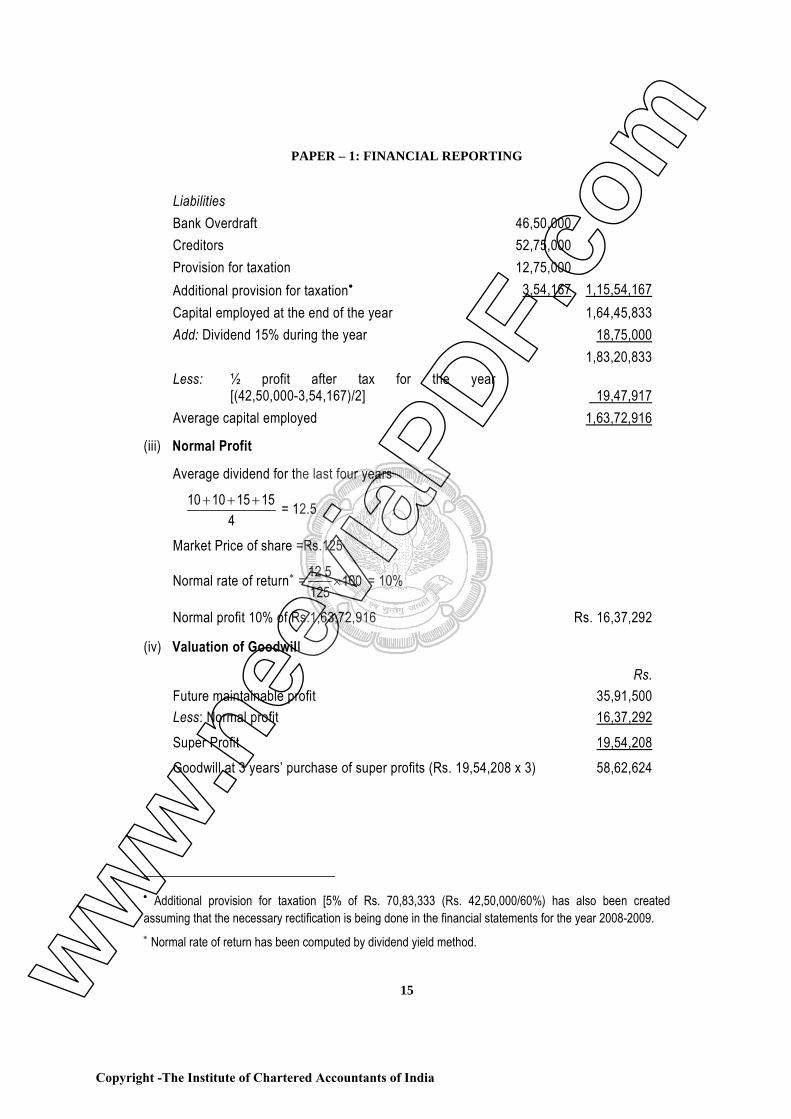

Liabilities Bank Overdraft 46,50,000 Creditors 52,75,000 Provision for taxation 12,75,000 Additional provision for taxation• 3,54,167 1,15,54,167 Capital employed at the end of the year 1,64,45,833 Add: Dividend 15% during the year 18,75,000 1,83,20,833 Less: ½ profit after tax for the year [(42,50,000-3,54,167)/2]

19,47,917

Average capital employed 1,63,72,916

(iii) Normal Profit

Average dividend for the last four years

10 10 15 154

+ + + = 12.5

Market Price of share =Rs.125

Normal rate of return∗ 12.5 100125

× = = 10%

Normal profit 10% of Rs.1,63,72,916 Rs. 16,37,292

(iv) Valuation of Goodwill

Future maintainable profit Less: Normal profit

Rs. 35,91,500 16,37,292

Super Profit 19,54,208 Goodwill at 3 years’ purchase of super profits (Rs. 19,54,208 x 3) 58,62,624

• Additional provision for taxation [5% of Rs. 70,83,333 (Rs. 42,50,000/60%) has also been created assuming that the necessary rectification is being done in the financial statements for the year 2008-2009. ∗ Normal rate of return has been computed by dividend yield method.

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

16

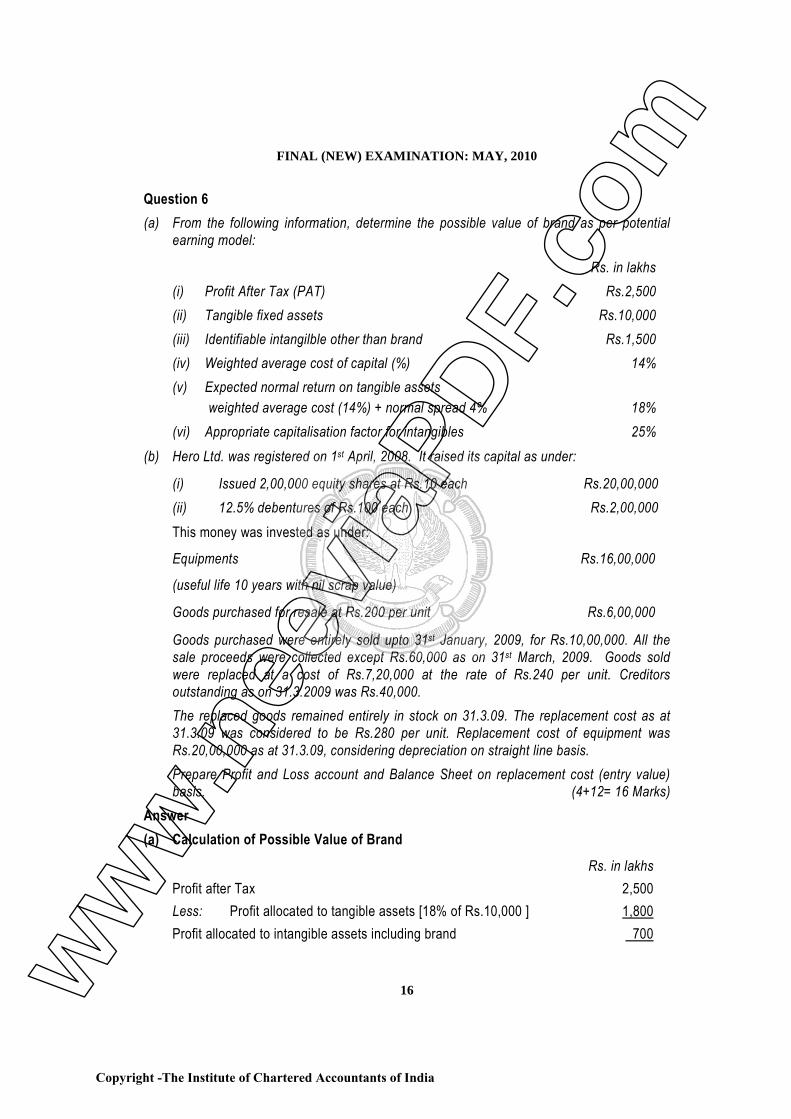

Question 6 (a) From the following information, determine the possible value of brand as per potential

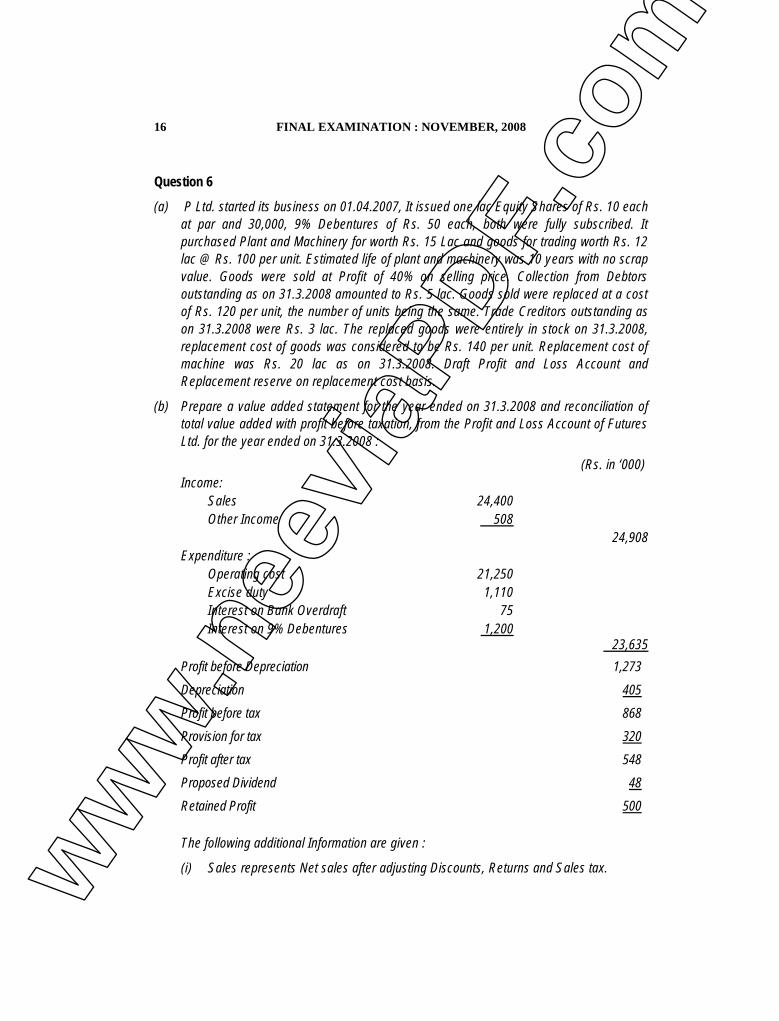

earning model:

Rs. in lakhs (i) Profit After Tax (PAT) Rs.2,500 (ii) Tangible fixed assets Rs.10,000 (iii) Identifiable intangilble other than brand Rs.1,500 (iv) Weighted average cost of capital (%) 14% (v) Expected normal return on tangible assets

weighted average cost (14%) + normal spread 4%

18% (vi) Appropriate capitalisation factor for intangibles 25%

(b) Hero Ltd. was registered on 1st

(i)

April, 2008. It raised its capital as under:

Issued 2,00,000 equity shares at Rs.10 each Rs.20,00,000 (ii) 12.5% debentures of Rs.100 each Rs.2,00,000

This money was invested as under:

Equipments Rs.16,00,000

(useful life 10 years with nil scrap value)

Goods purchased for resale at Rs.200 per unit Rs.6,00,000

Goods purchased were entirely sold upto 31st January, 2009, for Rs.10,00,000. All the sale proceeds were collected except Rs.60,000 as on 31st

The replaced goods remained entirely in stock on 31.3.09. The replacement cost as at 31.3.09 was considered to be Rs.280 per unit. Replacement cost of equipment was Rs.20,00,000 as at 31.3.09, considering depreciation on straight line basis.

March, 2009. Goods sold were replaced at a cost of Rs.7,20,000 at the rate of Rs.240 per unit. Creditors outstanding as on 31.3.2009 was Rs.40,000.

Prepare Profit and Loss account and Balance Sheet on replacement cost (entry value) basis. (4+12= 16 Marks)

Answer (a) Calculation of Possible Value of Brand

Rs. in lakhs Profit after Tax 2,500 Less: Profit allocated to tangible assets [18% of Rs.10,000 ] 1,800 Profit allocated to intangible assets including brand 700

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1: FINANCIAL REPORTING

17

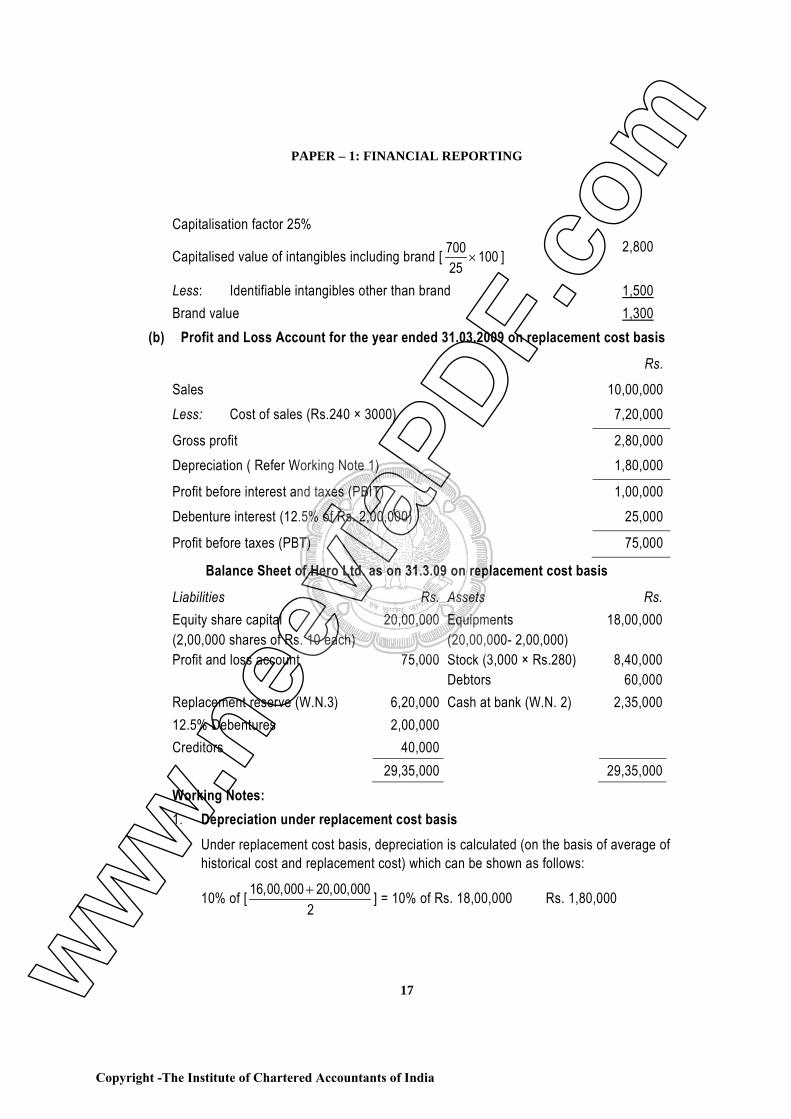

Capitalisation factor 25%

Capitalised value of intangibles including brand [ 10025700

× ] 2,800

Less: Identifiable intangibles other than brand 1,500 Brand value 1,300

(b) Profit and Loss Account for the year ended 31.03.2009 on replacement cost basis

Rs.

Sales 10,00,000 Less: Cost of sales (Rs.240 × 3000) 7,20,000

Gross profit 2,80,000 Depreciation ( Refer Working Note 1) 1,80,000

Profit before interest and taxes (PBIT) 1,00,000 Debenture interest (12.5% of Rs. 2,00,000) 25,000

Profit before taxes (PBT) 75,000

Balance Sheet of Hero Ltd. as on 31.3.09 on replacement cost basis

Liabilities Rs. Assets Rs. Equity share capital (2,00,000 shares of Rs. 10 each) Profit and loss account

20,00,000

75,000

Equipments (20,00,000- 2,00,000) Stock (3,000 × Rs.280) Debtors

18,00,000

8,40,000 60,000

Replacement reserve (W.N.3) 6,20,000 Cash at bank (W.N. 2) 2,35,000 12.5% Debentures 2,00,000 Creditors 40,000 29,35,000 29,35,000 Working Notes: 1. Depreciation under replacement cost basis Under replacement cost basis, depreciation is calculated (on the basis of average of

historical cost and replacement cost) which can be shown as follows:

10% of [ 16,00,000 20,00,0002+ ] = 10% of Rs. 18,00,000 Rs. 1,80,000

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

FINAL (NEW) EXAMINATION: MAY, 2010

18

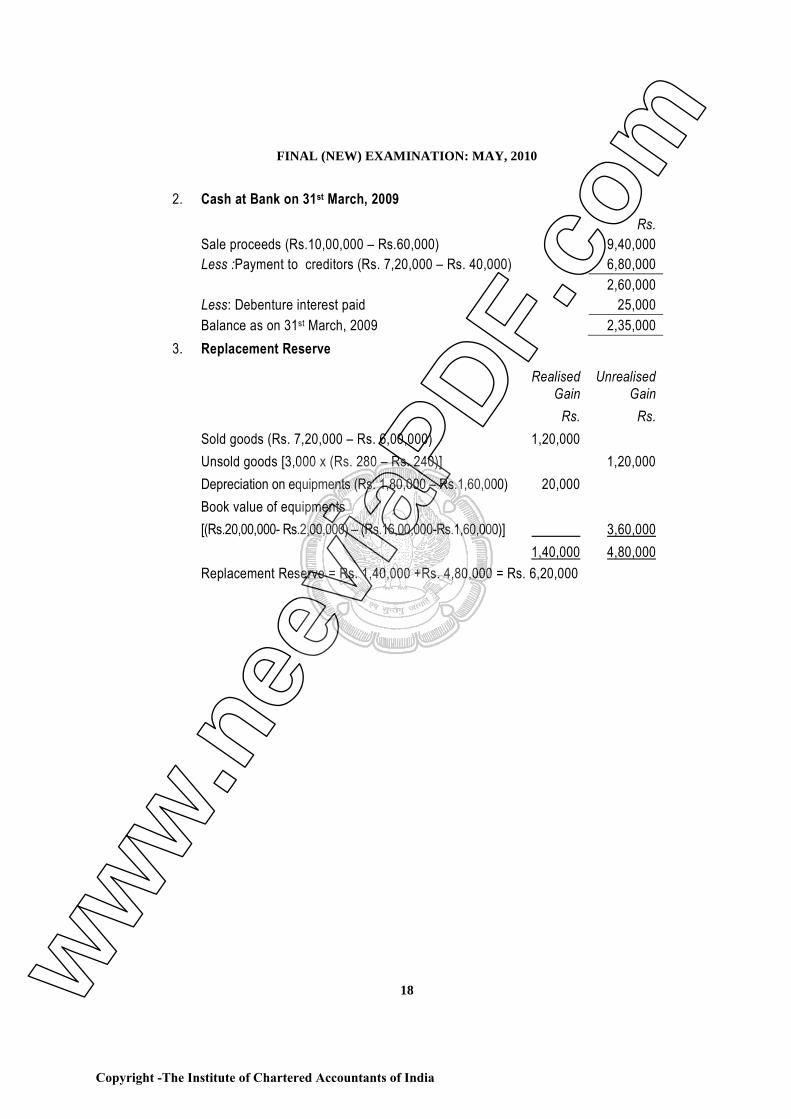

2. Cash at Bank on 31st March, 2009 Rs. Sale proceeds (Rs.10,00,000 – Rs.60,000) 9,40,000 Less :Payment to creditors (Rs. 7,20,000 – Rs. 40,000) 6,80,000 2,60,000 Less: Debenture interest paid 25,000 Balance as on 31st March, 2009 2,35,000

3. Replacement Reserve

Realised Gain

Unrealised Gain

Rs. Rs. Sold goods (Rs. 7,20,000 – Rs. 6,00,000) 1,20,000 Unsold goods [3,000 x (Rs. 280 – Rs. 240)] 1,20,000 Depreciation on equipments (Rs. 1,80,000 – Rs.1,60,000) 20,000 Book value of equipments [(Rs.20,00,000- Rs.2,00,000) – (Rs.16,00,000-Rs.1,60,000)] 3,60,000 1,40,000 4,80,000

Replacement Reserve = Rs. 1,40,000 +Rs. 4,80,000 = Rs. 6,20,000

Copyright -The Institute of Chartered Accountants of India

ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING

Question No. 1 is compulsory. Answer any five out of the remaining questions.

Working notes should form part of the answer.Wherever necessary, suitable assumptions may be made by the candidates.

Question 1

Answer any four out of the following:

(a) On 30.6.2007, Asmitha Ltd. incurred Rs. 2,00,000, net loss from disposal of a businesssegment. Also, on 30.7.2007, the company paid Rs. 60,000 for property taxes assessedfor the calendar year 2007. How the above transactions should be included indetermination of net income of Asmitha Ltd. for the six months interim period ended on30.9.2007.

(b) M/s XYZ Ltd. has three segments namely X, Y, Z. The total assets of the Company areRs. 10.00 crs. Segment X has Rs. 2.00 crs., segment Y has Rs. 3.00 crs. and segment Zhas Rs. 5.00 crs. Deferred tax assets included in the assets of each segments are X- Rs.0.50 crs., Y—Rs. 0.40 crs. and Z—Rs. 0.30 crs. The accountant contends that all thethree segments are reportable segments. Comment.

(c) M/s Dinesh & Company signed an agreement with workers for increase in wages withretrospective effect. The out-flow on account of arrears was for 2005-06—Rs. 10.00lakhs, for 2006-07—Rs. 12.00 lakhs and for 2007-08—Rs. 12.00 lakhs. This amount ispayable in September, 2008. The accountant wants to charge Rs. 22.00 lakhs as priorperiod charges in financial statement for 2008-09. Discuss.

(d) M/s Prima Co. Ltd. sold goods worth Rs. 50,000 to M/s Y and Company. M/s Y and Co.asked for discount of Rs. 8,000 which was agreed by M/s Prima Co. Ltd. The sale waseffected and goods were despatched. After receiving, goods worth Rs. 7,000 was founddefective, which they returned immediately. They made the payment of Rs. 35,000 to M/sPrima Co. Ltd. Accountant booked the sales for Rs. 35,000. Please discuss.

(e) Himalayas Ltd. is showing an intangible Asset at Rs. 72 lakhs as on 01.04.2007 and thatitem was required for Rs. 96 lakhs on 01.04.2004 and that item was available for usefrom that date. Himalayas Ltd. has been following the policy of amortisation of theintangible asset over a period of 12 years on straight line basis. Comment on theaccounting treatment of the above with reference to relevant accounting standard.

(4x5= 20 Marks)

ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : NOVEMBER, 20082

Answer

(a) According to Para 10 of AS 25 “Interim Financial Reporting”, If an enterprise preparesand presents a complete set of financial statements in its interim financial report, theform and content of those statements should conform to the requirements as applicableto annual complete set of financial statements. As on 30.9.2007, Asmitha Ltd., wouldreport the entire Rs.2,00,000 loss on the disposal of its business segment since the losswas incurred during interim period. A cost charged as an expense in an annual periodshould be allocated to Interim periods on accrual basis. Since Rs.60,000 Property Taxpayment relates to entire calendar year 2007, Rs.30,000 would be reported as anexpense for six months ended on 30th September, 2007 while remaining Rs.30,000would be reported as prepaid expenses.

(b) According to AS 17 “Segment Reporting”, segment assets do not include income taxassets. Therefore, the revised total assets are 8.8 crores [10 crores – (0.5+0.4+0.3)].Segment X holds total assets of 1.5 crores (2 crores – 0.5 crores); Segment Y holds 2.6crores (3 crores – 0.4 crores); and Segment Z holds 4.7 crores (5 crores – 0.3 crores).Thus all the three segments hold more than 10% of the total assets, all segments arereportable segments.

(c) According to AS 5(Revised) “Net Profit or Loss for the Period, Prior Period Items andChanges in Accounting Policies”, the term prior period item refers only to income orexpenses which arise in the current period as a result of errors or omission in thepreparation of the financial statements of one or more prior periods. The term does notinclude other adjustments necessitated by circumstances, which though related to priorperiods are determined in the current period. The full amount of wage arrears paid toworkers will be treated as an expense of current year and it will be charged to profit andloss account as current expenses and not as prior period expenses.

It may be mentioned that additional wages is an expense arising from the ordinaryactivities of the company. Although abnormal in amount, such an expense does notqualify as an extraordinary item. However, as per Para 12 of AS 5 (Revised), when itemsof income and expense within profit or loss from ordinary activities are of such size,nature or incidence that their disclosure is relevant to explain the performance of theenterprise for the period, the nature and amount of such items should be disclosedseparately.

(d) As per Para 4.1 of AS 9 “Revenue Recognition”, revenue is the gross inflow of cash,receivables or other consideration arising in the course of the ordinary activities of anenterprise from the sale of goods, from the rendering of services, and from the use byothers of enterprise resources yielding interest, royalties and dividends.

In the given case, M/s Prima Co. Ltd. should record the sales at gross value ofRs.50,000. Discount of Rs.8,000 in price and goods returned worth Rs.7,000 are to beww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING 3

adjusted by suitable provisions. M/s Prime Co. Ltd. might have sent the credit note ofRs. 15,000 to M/s Y & Co. to account for these adjustments. The contention of theaccountant to book the sales for Rs.35,000 is not correct.

(e) As per Para 63 of AS 26 “Intangible Assets”, the depreciable amount of an intangibleasset should be allocated on a systematic basis over the best estimate of its useful life.There is a rebuttable presumption that the useful life of an intangible asset will notexceed ten years from the date when the asset is available for use. Amortisation shouldcommence when the asset is available for use.

Himalayas Ltd. has been following the policy of amortisation of the intangible asset overa period of 12 years on straight line basis. The period of 12 years is more than themaximum period of 10 years specified under AS 26. Accordingly, Himalayas Ltd. wouldbe required to restate the carrying amount of intangible asset as on 1.4.2007 at Rs.96lakhs less Rs. 28.8 lakhs (Rs. 9.6 lakhs × 3 years) = Rs. 67.2 lakhs. If amortisation hadbeen as per AS 26, the carrying amount would have been Rs.67.2 lakhs. The differenceof Rs. 4.8 lakhs i.e. (Rs. 72lakhs – 67.2 lakhs) would be required to be adjusted againstthe opening balance of revenue reserves. The carrying amount of Rs.67.2 lakhs wouldbe amortised over 7 (10 less 3) years in future.

Question 2

System Ltd. and HRD Ltd. decided to amalgamate as on 01.04.2008. Their Balance Sheets ason 31.03.2008 were as follows: (Rs. in ‘000)

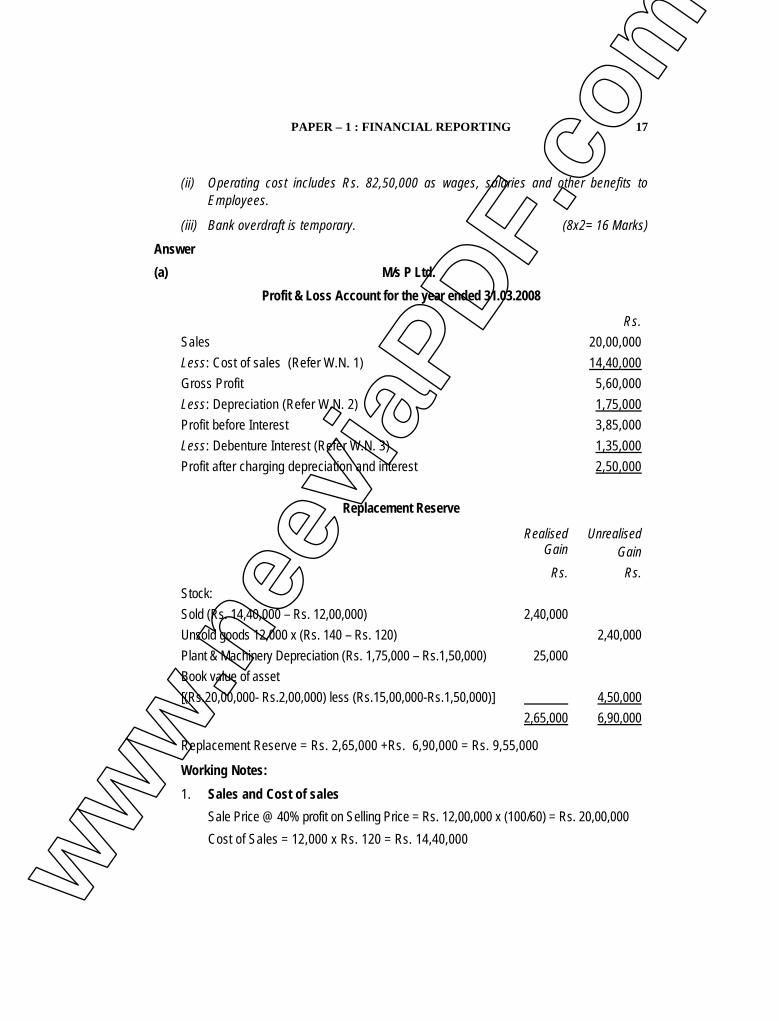

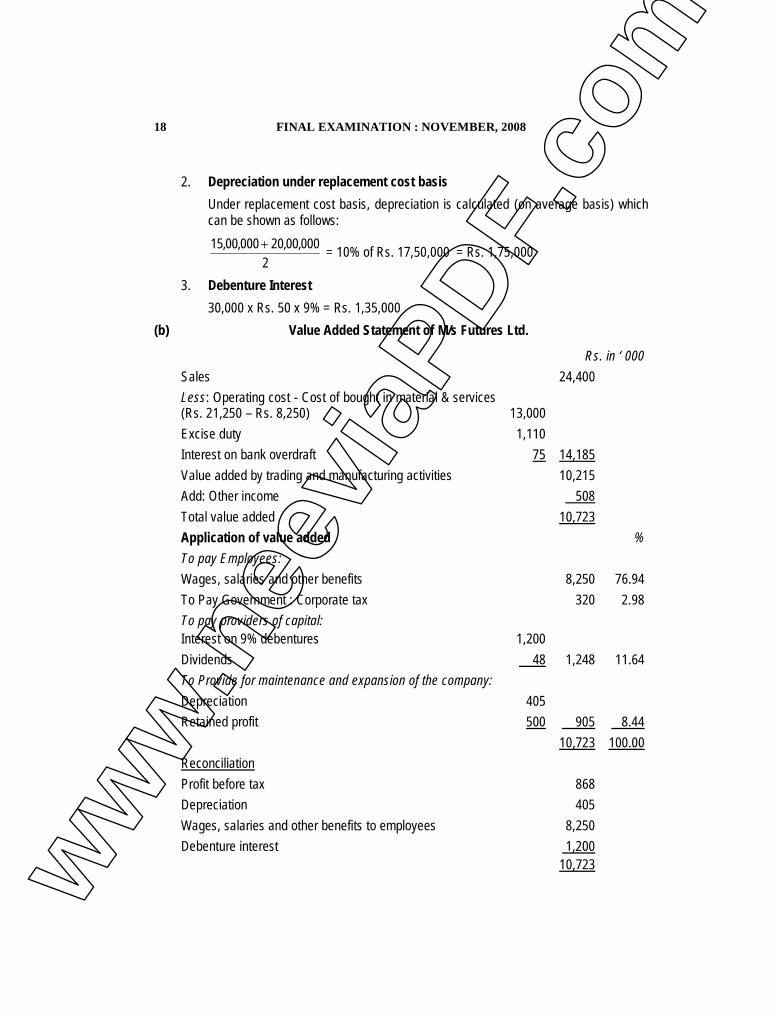

Particulars System Ltd. HRD Ltd.Source of Funds :Equity share capital (Rs. 10 each) 150 1409% preference share capital (Rs. 100 each) 30 20Investment allowance reserve 5 2Profit and Loss Account 10 610 % Debentures 50 30Sundry Creditors 25 15Tax provision 7 4Equity Dividend Proposed 30 28Total 307 245Application of Funds :Building 60 50Plant and Machinery 80 70Investments 40 25ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : NOVEMBER, 20084

Sundry Debtors 45 35Stock 36 40Cash and Bank 40 25Preliminary Expenses 6 ----Total 307 245

From the following information, you are to prepare the draft Balance Sheet as on 01.04.2008of a new company, Intranet Ltd., which was formed to take over the business of both thecompanies and took over all the assets and liabilities:

(i) 50 % Debentures are to be converted into Equity Shares of the New Company.

(ii) Out of the investments, 20% are non-trade investments.

(iii) Fixed Assets of Systems Ltd. were valued at 10% above cost and that of HRD Ltd. at 5%above cost.

(iv) 10 % of sundry Debtors were doubtful for both the companies. Stocks to be carried atcost.

(v) Preference shareholders were discharged by issuing equal number of 9% preferenceshares at par.

(vi) Equity shareholders of both the transferor companies are to be discharged by issuingEquity shares of Rs. 10 each of the new company at a premium of Rs. 5 per share.

Amalgamation is in the nature of purchase. (16 Marks)

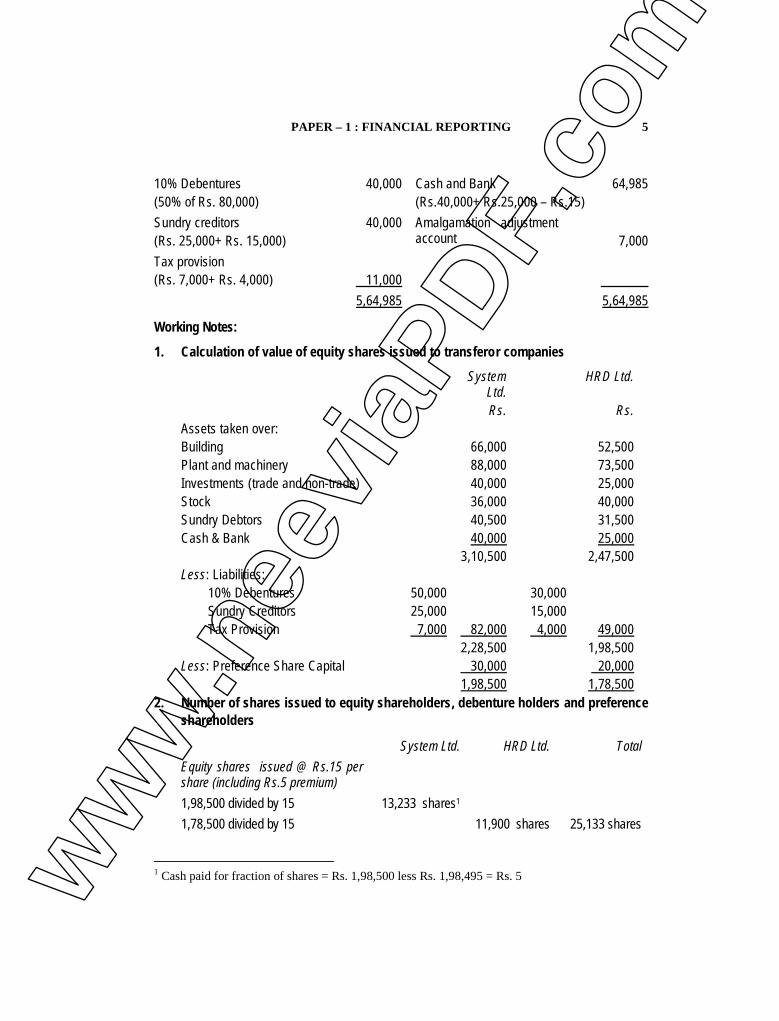

AnswerM/s Intranet Ltd.

Draft Balance Sheet as at 1.4.2008

Liabilities Rs. Assets Rs.Equity share capital27,799 Equity shares of Rs.10each, fully paid up(25,133 + 2,666) (W.N.2)

2,77,990Building(Rs. 66,000+Rs. 52,500))Plant and machinery(Rs. 88,000+Rs. 73,500)

1,18,500

1,61,5009% Preference share capital(Share of Rs.100 each) (W.N.2) 50,000

Investments(Rs. 40,000+ Rs. 25,000) 65,000

Securities premium(1,25,665 + 13,330) (W.N.2) 1,38,995

Stock(Rs. 36,000+ Rs. 40,000) 76,000

Investment allowance reserve(Rs. 5,000+ Rs. 2,000) 7,000

Sundry debtors90% of (Rs.45,000+ Rs. 35,000) 72,000w

ww

.nee

viaP

DF.c

om

PAPER – 1 : FINANCIAL REPORTING 5

10% Debentures(50% of Rs. 80,000)

40,000 Cash and Bank(Rs.40,000+ Rs.25,000 – Rs.15)

64,985

Sundry creditors(Rs. 25,000+ Rs. 15,000)

40,000 Amalgamation adjustmentaccount 7,000

Tax provision(Rs. 7,000+ Rs. 4,000) 11,000

5,64,985 5,64,985

Working Notes:

1. Calculation of value of equity shares issued to transferor companies

SystemLtd.

HRD Ltd.

Rs. Rs.Assets taken over:Building 66,000 52,500Plant and machinery 88,000 73,500Investments (trade and non-trade) 40,000 25,000Stock 36,000 40,000Sundry Debtors 40,500 31,500Cash & Bank 40,000 25,000

3,10,500 2,47,500Less: Liabilities:

10% Debentures 50,000 30,000Sundry Creditors 25,000 15,000Tax Provision 7,000 82,000 4,000 49,000

2,28,500 1,98,500Less: Preference Share Capital 30,000 20,000

1,98,500 1,78,5002. Number of shares issued to equity shareholders, debenture holders and preference

shareholders

System Ltd. HRD Ltd. TotalEquity shares issued @ Rs.15 pershare (including Rs.5 premium)1,98,500 divided by 15 13,233 shares1

1,78,500 divided by 15 11,900 shares 25,133 shares

1 Cash paid for fraction of shares = Rs. 1,98,500 less Rs. 1,98,495 = Rs. 5ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : NOVEMBER, 20086

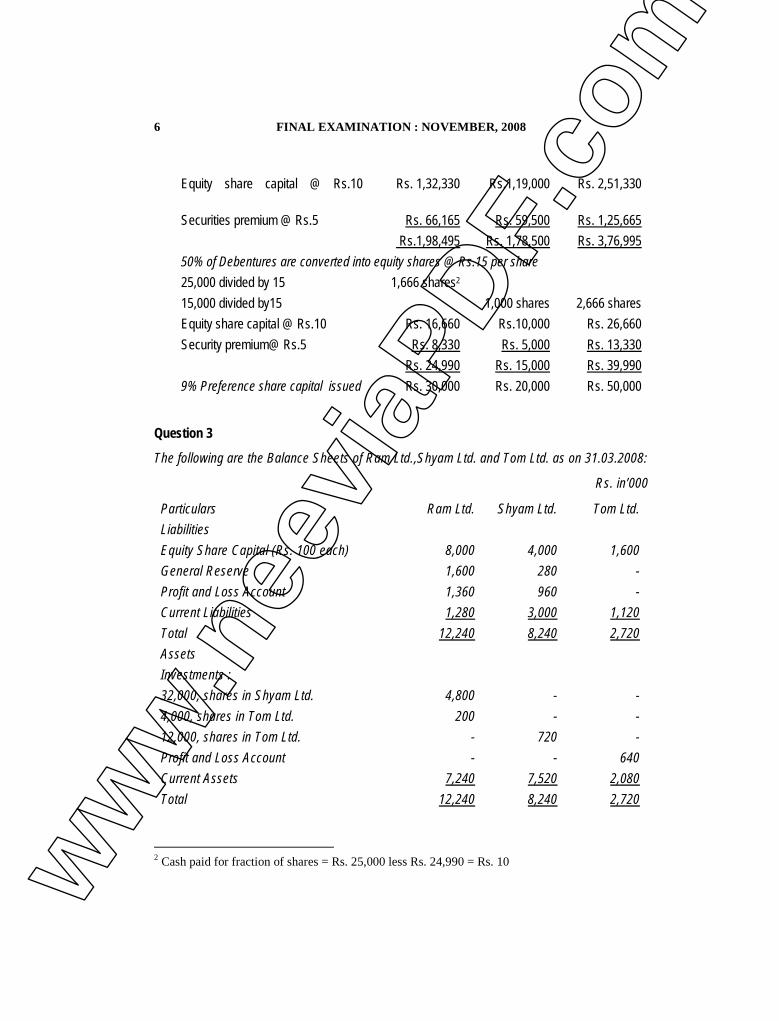

Equity share capital @ Rs.10 Rs. 1,32,330 Rs.1,19,000 Rs. 2,51,330

Securities premium @ Rs.5 Rs. 66,165 Rs. 59,500 Rs. 1,25,665 Rs.1,98,495 Rs. 1,78,500 Rs. 3,76,995

50% of Debentures are converted into equity shares @ Rs.15 per share25,000 divided by 15 1,666 shares2

15,000 divided by15 1,000 shares 2,666 sharesEquity share capital @ Rs.10 Rs. 16,660 Rs.10,000 Rs. 26,660Security premium@ Rs.5 Rs. 8,330 Rs. 5,000 Rs. 13,330

Rs. 24,990 Rs. 15,000 Rs. 39,9909% Preference share capital issued Rs. 30,000 Rs. 20,000 Rs. 50,000

Question 3

The following are the Balance Sheets of Ram Ltd.,Shyam Ltd. and Tom Ltd. as on 31.03.2008:

Rs. in’000

Particulars Ram Ltd. Shyam Ltd. Tom Ltd.LiabilitiesEquity Share Capital (Rs. 100 each) 8,000 4,000 1,600General Reserve 1,600 280 -Profit and Loss Account 1,360 960 -Current Liabilities 1,280 3,000 1,120Total 12,240 8,240 2,720AssetsInvestments :32,000, shares in Shyam Ltd. 4,800 - -4,000, shares in Tom Ltd. 200 - -12,000, shares in Tom Ltd. - 720 -Profit and Loss Account - - 640Current Assets 7,240 7,520 2,080Total 12,240 8,240 2,720

2 Cash paid for fraction of shares = Rs. 25,000 less Rs. 24,990 = Rs. 10ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING 7

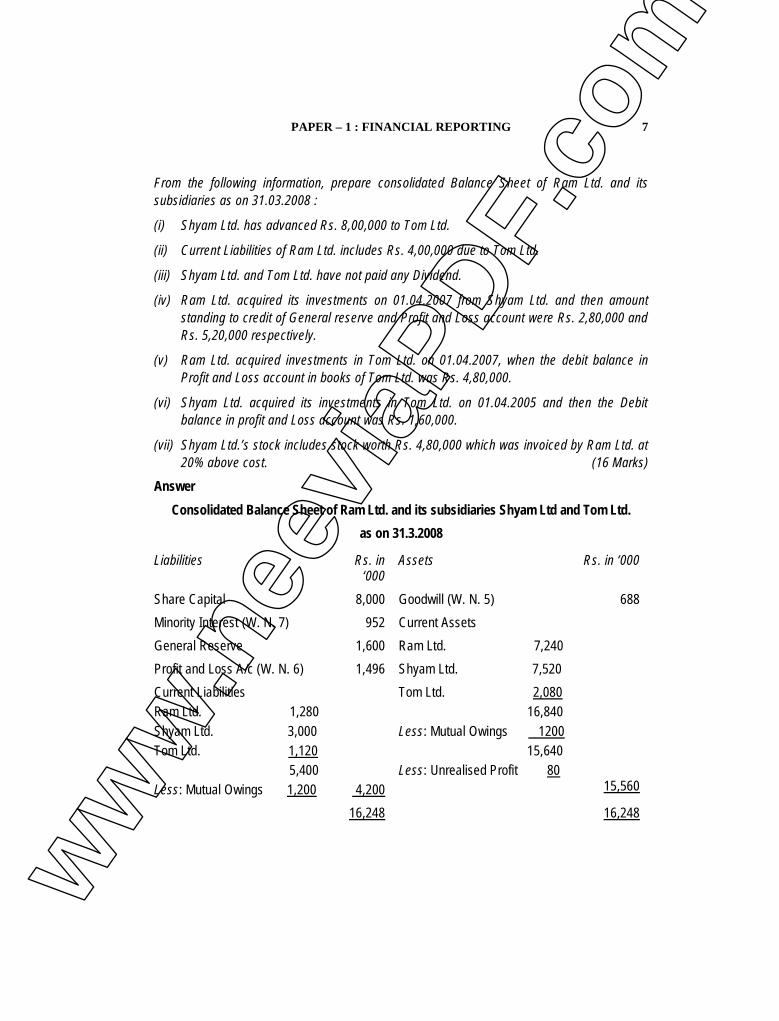

From the following information, prepare consolidated Balance Sheet of Ram Ltd. and itssubsidiaries as on 31.03.2008 :

(i) Shyam Ltd. has advanced Rs. 8,00,000 to Tom Ltd.

(ii) Current Liabilities of Ram Ltd. includes Rs. 4,00,000 due to Tom Ltd.

(iii) Shyam Ltd. and Tom Ltd. have not paid any Dividend.

(iv) Ram Ltd. acquired its investments on 01.04.2007 from Shyam Ltd. and then amountstanding to credit of General reserve and Profit and Loss account were Rs. 2,80,000 andRs. 5,20,000 respectively.

(v) Ram Ltd. acquired investments in Tom Ltd. on 01.04.2007, when the debit balance inProfit and Loss account in books of Tom Ltd. was Rs. 4,80,000.

(vi) Shyam Ltd. acquired its investments in Tom Ltd. on 01.04.2005 and then the Debitbalance in profit and Loss account was Rs. 1,60,000.

(vii) Shyam Ltd.’s stock includes stock worth Rs. 4,80,000 which was invoiced by Ram Ltd. at20% above cost. (16 Marks)

AnswerConsolidated Balance Sheet of Ram Ltd. and its subsidiaries Shyam Ltd and Tom Ltd.

as on 31.3.2008

Liabilities Rs. in‘000

Assets Rs. in ‘000

Share Capital 8,000 Goodwill (W. N. 5) 688Minority Interest (W. N. 7) 952 Current AssetsGeneral Reserve 1,600 Ram Ltd. 7,240Profit and Loss A/c (W. N. 6) 1,496 Shyam Ltd. 7,520Current LiabilitiesRam Ltd. 1,280Shyam Ltd. 3,000Tom Ltd. 1,120

5,400Less: Mutual Owings 1,200 4,200

Tom Ltd. 2,08016,840

Less: Mutual Owings 1200 15,640

Less: Unrealised Profit 8015,560

16,248 16,248

ww

w.n

eevi

aPDF

.com

FINAL EXAMINATION : NOVEMBER, 20088

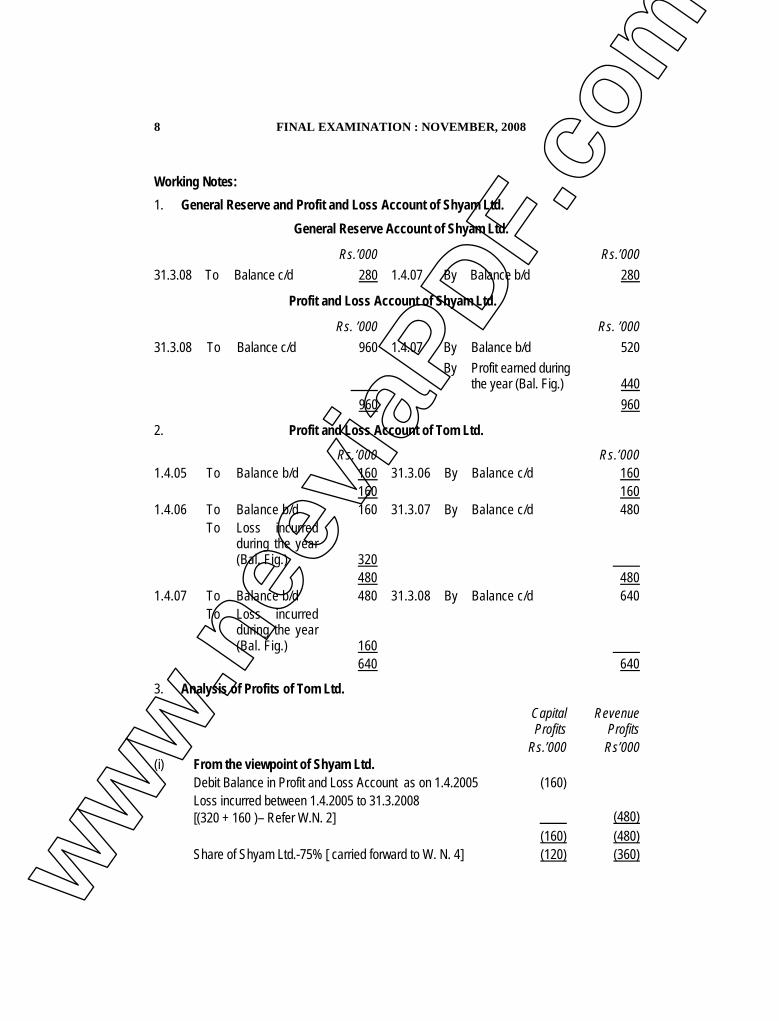

Working Notes:1. General Reserve and Profit and Loss Account of Shyam Ltd.

General Reserve Account of Shyam Ltd.

Rs.’000 Rs.’00031.3.08 To Balance c/d 280 1.4.07 By Balance b/d 280

Profit and Loss Account of Shyam Ltd.

Rs. ’000 Rs. ’00031.3.08 To Balance c/d 960 1.4.07 By Balance b/d 520

By Profit earned duringthe year (Bal. Fig.) 440

960 960

2. Profit and Loss Account of Tom Ltd.

Rs.’000 Rs.’0001.4.05 To Balance b/d 160 31.3.06 By Balance c/d 160

160 1601.4.06 To Balance b/d 160 31.3.07 By Balance c/d 480

To Loss incurredduring the year(Bal. Fig.) 320

480 4801.4.07 To Balance b/d 480 31.3.08 By Balance c/d 640

To Loss incurredduring the year(Bal. Fig.) 160

640 640

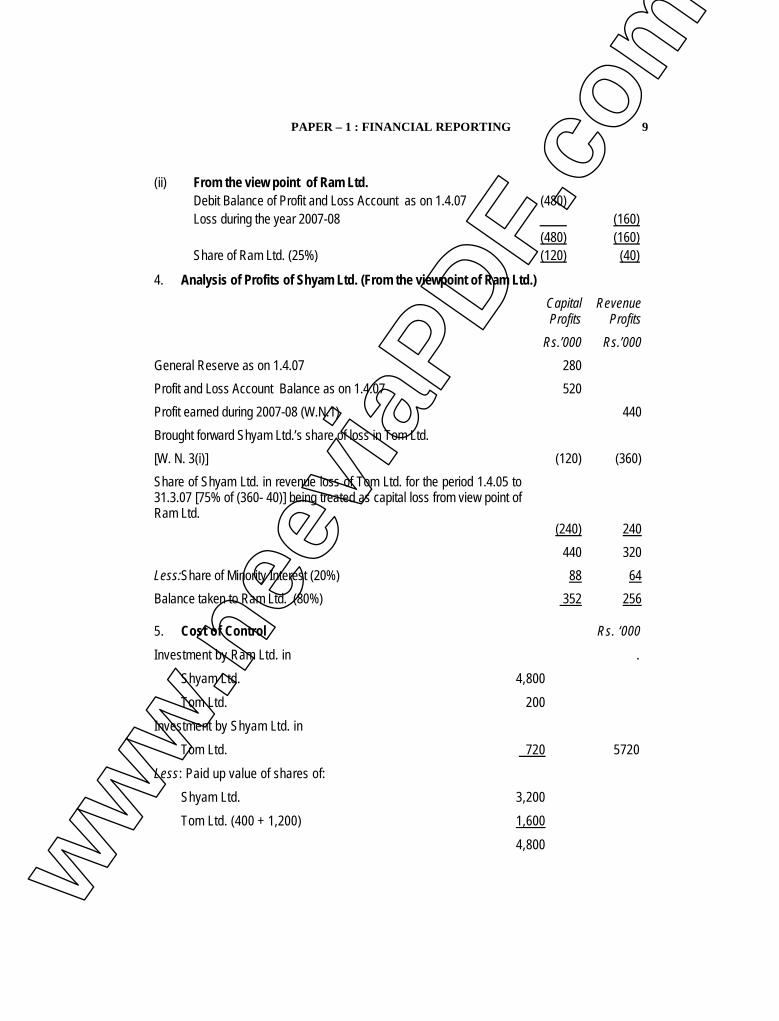

3. Analysis of Profits of Tom Ltd.

CapitalProfits

RevenueProfits

(i) From the viewpoint of Shyam Ltd.Rs.’000 Rs’000

Debit Balance in Profit and Loss Account as on 1.4.2005 (160)Loss incurred between 1.4.2005 to 31.3.2008[(320 + 160 )– Refer W.N. 2] (480)

(160) (480)Share of Shyam Ltd.-75% [ carried forward to W. N. 4] (120) (360)ww

w.n

eevi

aPDF

.com

PAPER – 1 : FINANCIAL REPORTING 9

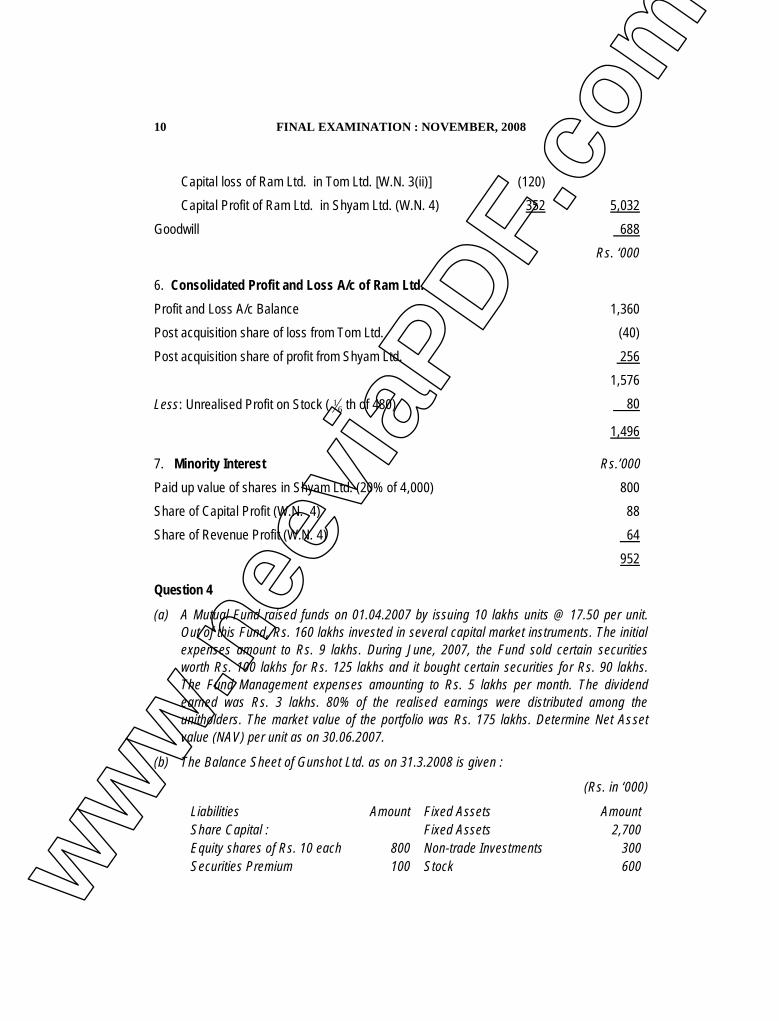

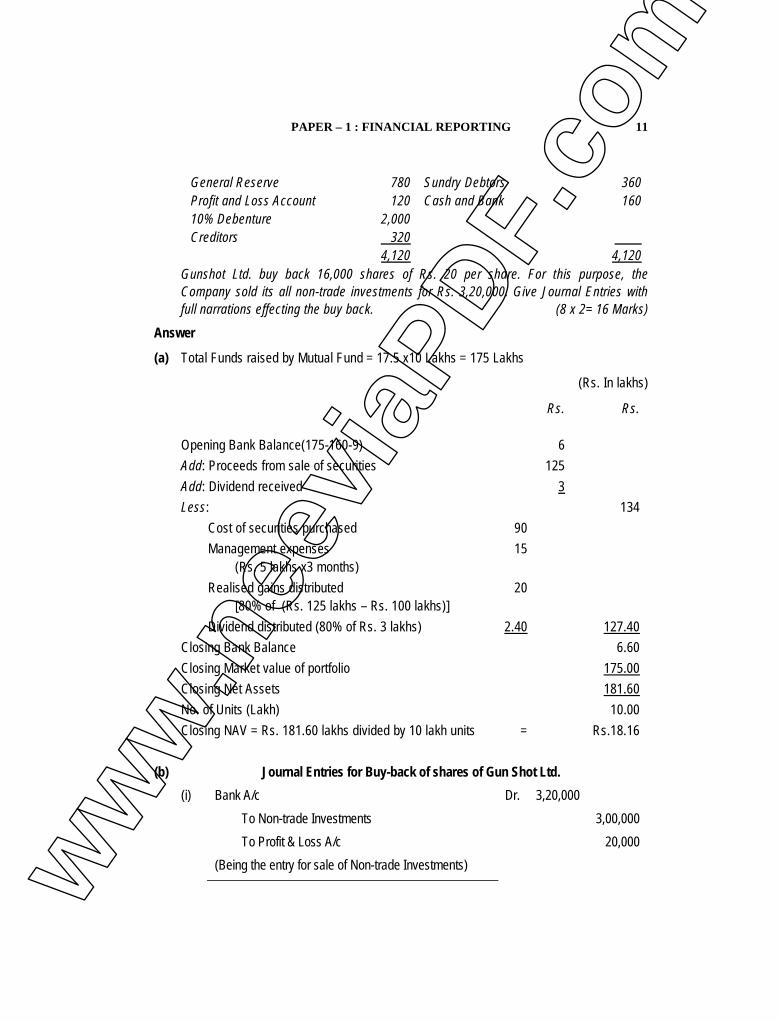

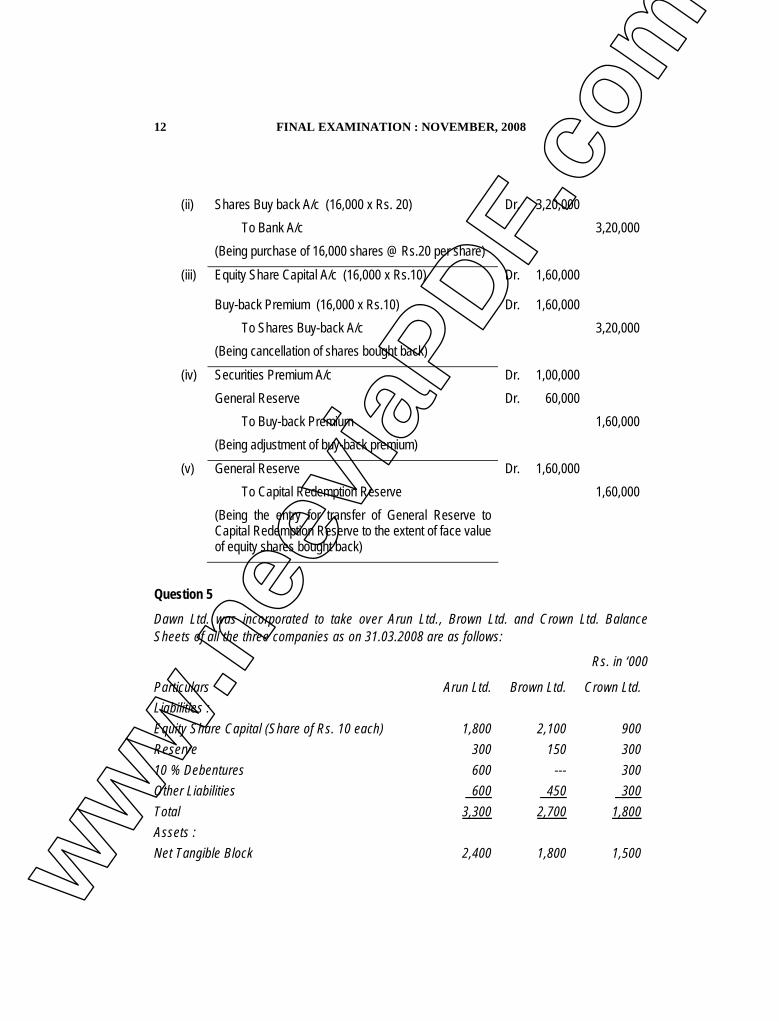

(ii) From the view point of Ram Ltd.Debit Balance of Profit and Loss Account as on 1.4.07 (480)Loss during the year 2007-08 (160)