Embed Size (px)

Citation preview

© 2020 RSM US LLP. All Rights Reserved. © 2020 RSM US LLP. All Rights Reserved.

© 2020 RSM US LLP. All Rights Reserved.

RSM ECONOMIC OUTLOOK The state of the economy as businesses reopen

June 18, 2020

© 2020 RSM US LLP. All Rights Reserved.

Presenter

3

New York, NY

+1 212 372 1502

Kevin DepewDeputy Chief Economist, National Industry Analyst Program Leader

© 2020 RSM US LLP. All Rights Reserved.

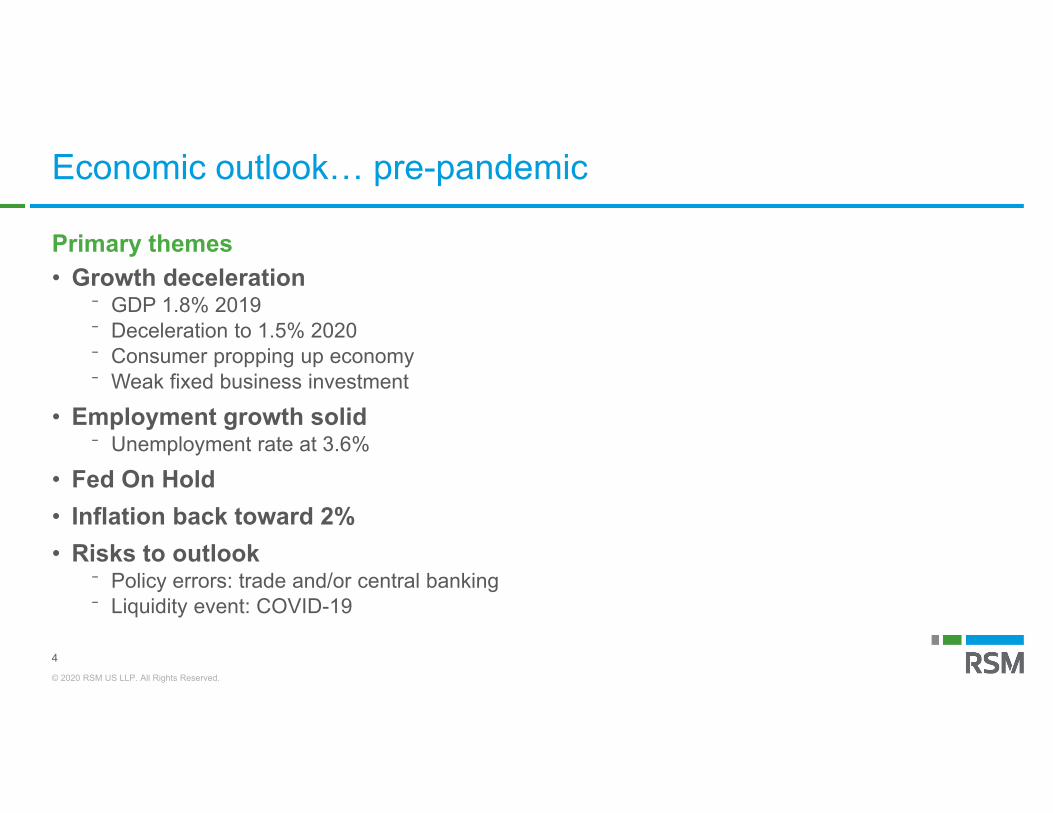

Economic outlook… pre-pandemic

Primary themes• Growth deceleration

⁻ GDP 1.8% 2019⁻ Deceleration to 1.5% 2020⁻ Consumer propping up economy⁻ Weak fixed business investment

• Employment growth solid⁻ Unemployment rate at 3.6%

• Fed On Hold• Inflation back toward 2% • Risks to outlook

⁻ Policy errors: trade and/or central banking⁻ Liquidity event: COVID-19

4

© 2020 RSM US LLP. All Rights Reserved.

US economic dashboard: Recession and recovery

U.S. Economy has suffered a series of shocks• Supply, demand and financial shocks• Minus -41.8% Q2 GDP • Depression like shocks, but no depression

• Policy choice, not fate • Recession will likely last 2-3 quarters

Policy Response• Robust fiscal and monetary policy response

Shape of recovery• Elongated and frustrating in some industries

© 2020 RSM US LLP. All Rights Reserved.

Real economy shock: May jobs report

Signs labor market is bottoming• 2.5 million new jobs• 2.7 million workers returned to work• Unemployment rate declined to 13.3% from 14.7%

Three main takeaways• The Paycheck Protection Program loans likely worked• Idea that $600 extra per week served as incentive to not to return to work was

oversold• The Pandemic Unemployment Assistance aid turned out to be a bridge, not a

barrier, to normalization of the labor market

© 2020 RSM US LLP. All Rights Reserved.

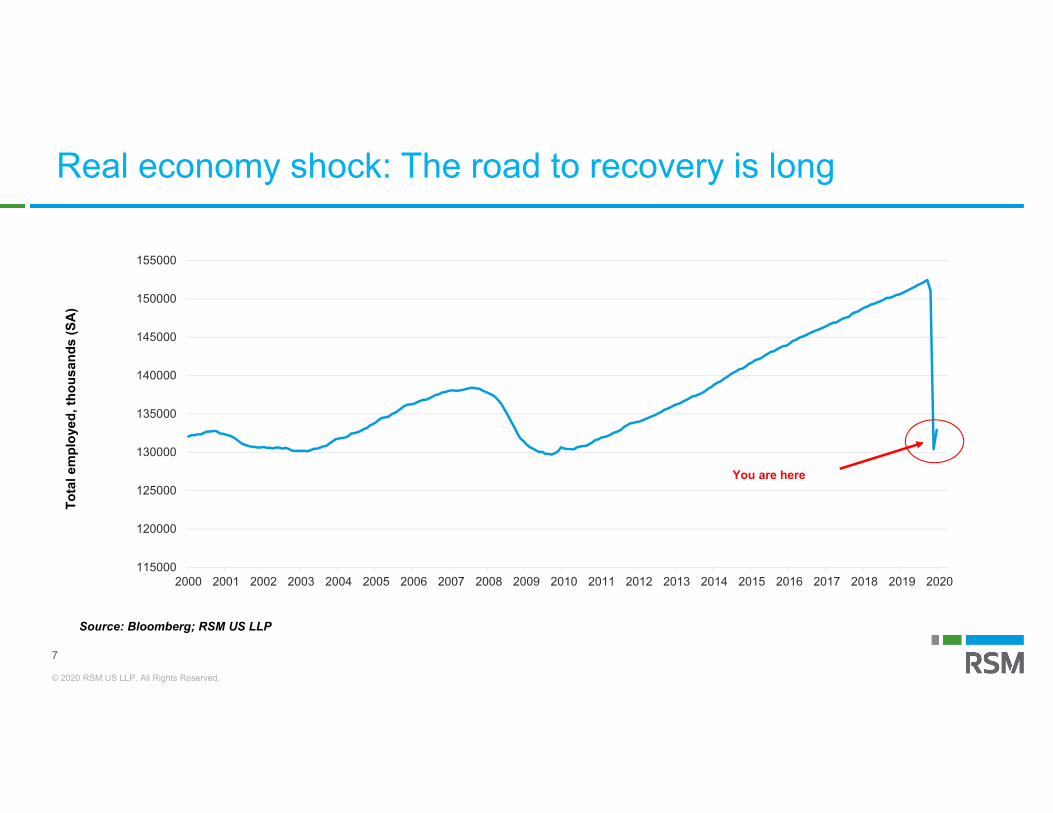

7

115000

120000

125000

130000

135000

140000

145000

150000

155000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Tota

lem

ploy

ed, t

hous

ands

(SA

)

Source: Bloomberg; RSM US LLP

You are here

Real economy shock: The road to recovery is long

© 2020 RSM US LLP. All Rights Reserved.

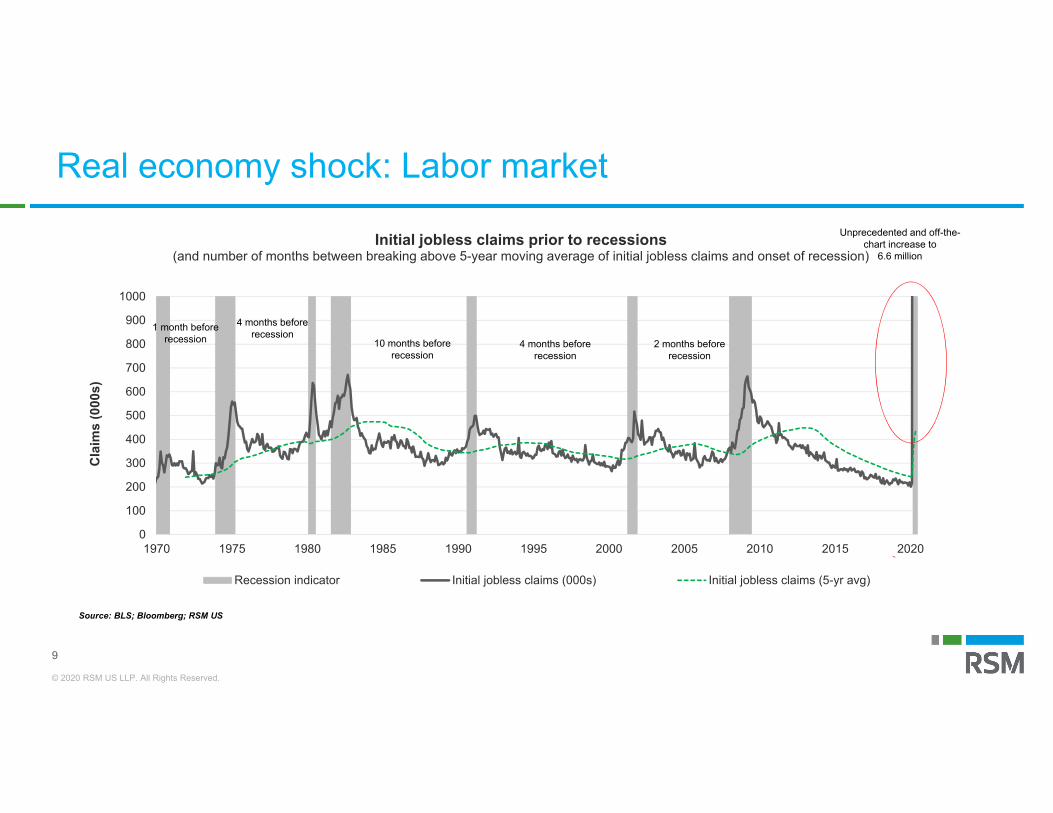

Real economy shock: Labor market

Labor market shock• 60 million jobs at risk• Damage implies -40% Q2 GDP

Initial jobless claims• 45.7 million jobs lost in 13 weeks• About 27.2% of those who held jobs prior to the pandemic have filed for

unemployment

Unemployment• ~20-25% peak in 2020, returning to ~10% by year’s end

© 2020 RSM US LLP. All Rights Reserved.

9

0

10

20

30

40

50

60

70

80

90

100

0

100

200

300

400

500

600

700

800

900

1000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Cla

ims

(000

s)

Initial jobless claims prior to recessions(and number of months between breaking above 5-year moving average of initial jobless claims and onset of recession)

Recession indicator Initial jobless claims (000s) Initial jobless claims (5-yr avg)

Source: BLS; Bloomberg; RSM US

10 months beforerecession

4 months beforerecession

2 months beforerecession

4 months beforerecession

1 month beforerecession

Unprecedented and off-the-chart increase to

6.6 million

Real economy shock: Labor market

© 2020 RSM US LLP. All Rights Reserved.

10

Real economy shock: Labor market

0

10

20

30

40

50

60

70

80

90

100

0

5,000

10,000

15,000

20,000

25,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Cla

ims

(000

s)

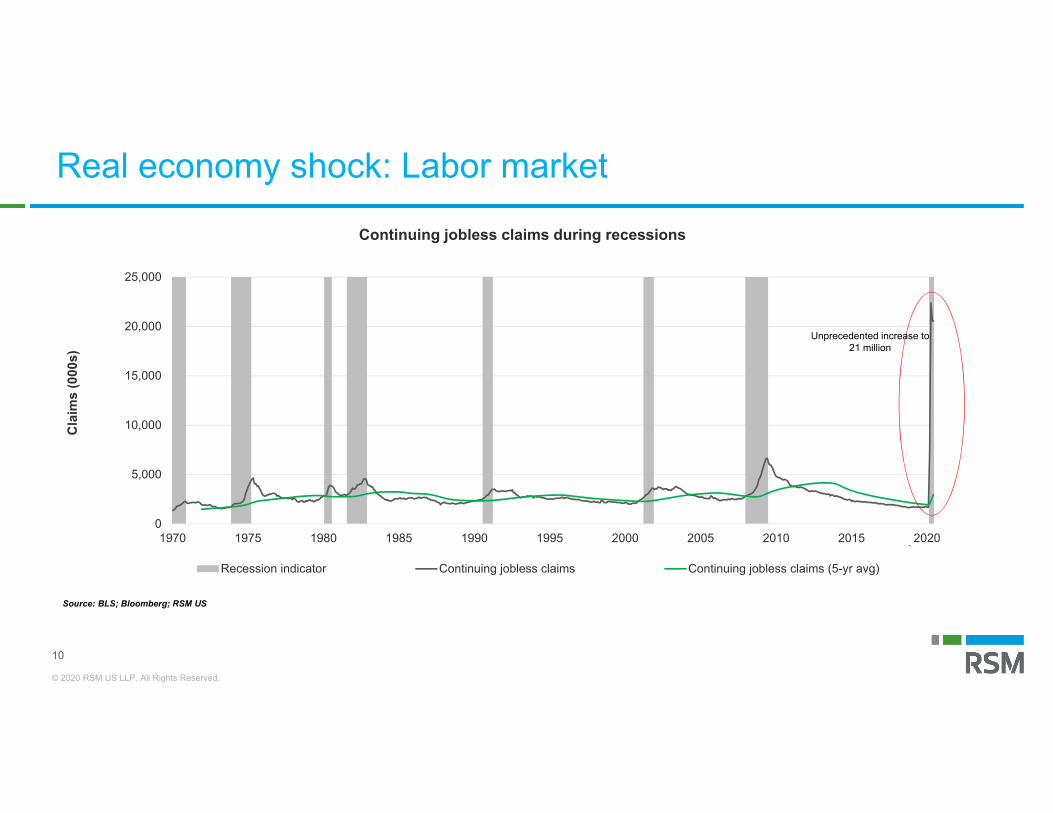

Continuing jobless claims during recessions

Recession indicator Continuing jobless claims Continuing jobless claims (5-yr avg)

Source: BLS; Bloomberg; RSM US

Unprecedented increase to21 million

© 2020 RSM US LLP. All Rights Reserved.

Real GDP implications

11

-60

-40

-20

0

20

40

60

80

100-6

-4

-2

0

2

4

6

8

10

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Initial Jobless Claim

s (YOY %

)

Rea

l GD

P (Y

OY

%)

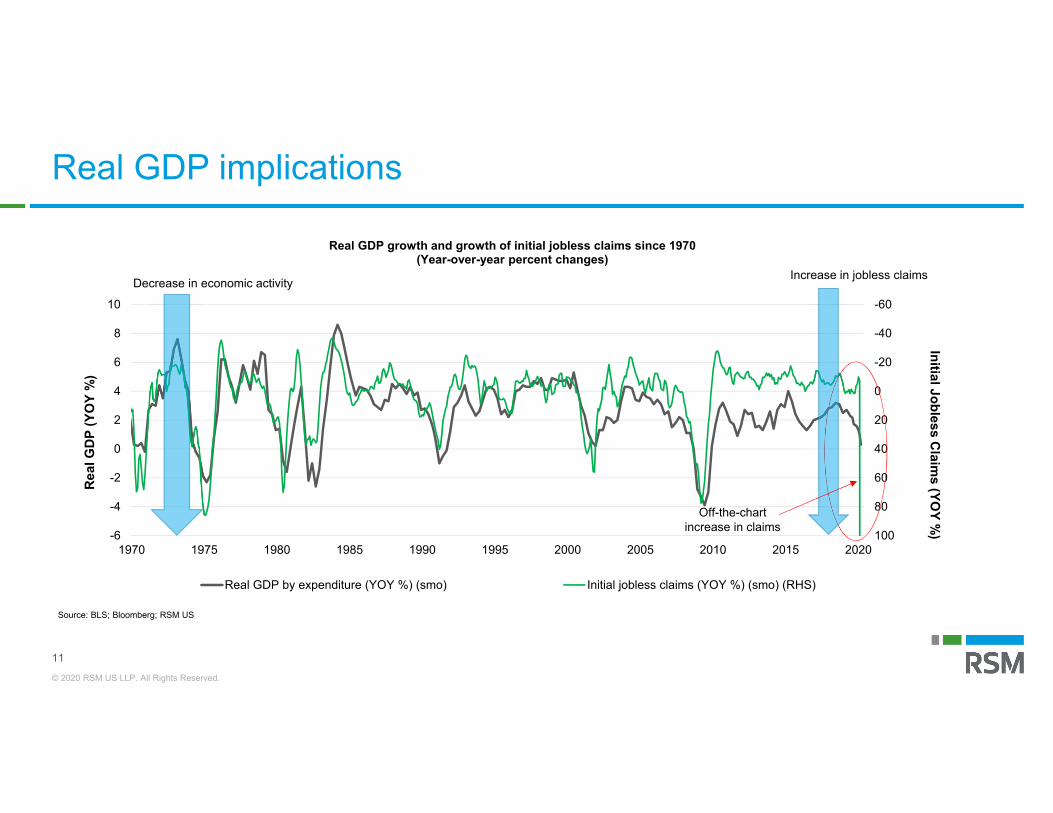

Real GDP growth and growth of initial jobless claims since 1970(Year-over-year percent changes)

Real GDP by expenditure (YOY %) (smo) Initial jobless claims (YOY %) (smo) (RHS)

Source: BLS; Bloomberg; RSM US

Decrease in economic activityIncrease in jobless claims

Off-the-chartincrease in claims

© 2020 RSM US LLP. All Rights Reserved.

Polling question

Assuming a full reopening of the economy, do you anticipate changing your attitude toward shopping and spending ?

a) No change; I will shop and spend the same as beforeb) I may be slightly more cautious c) I intend to permanently change my shopping and spending behavior

12

© 2020 RSM US LLP. All Rights Reserved.

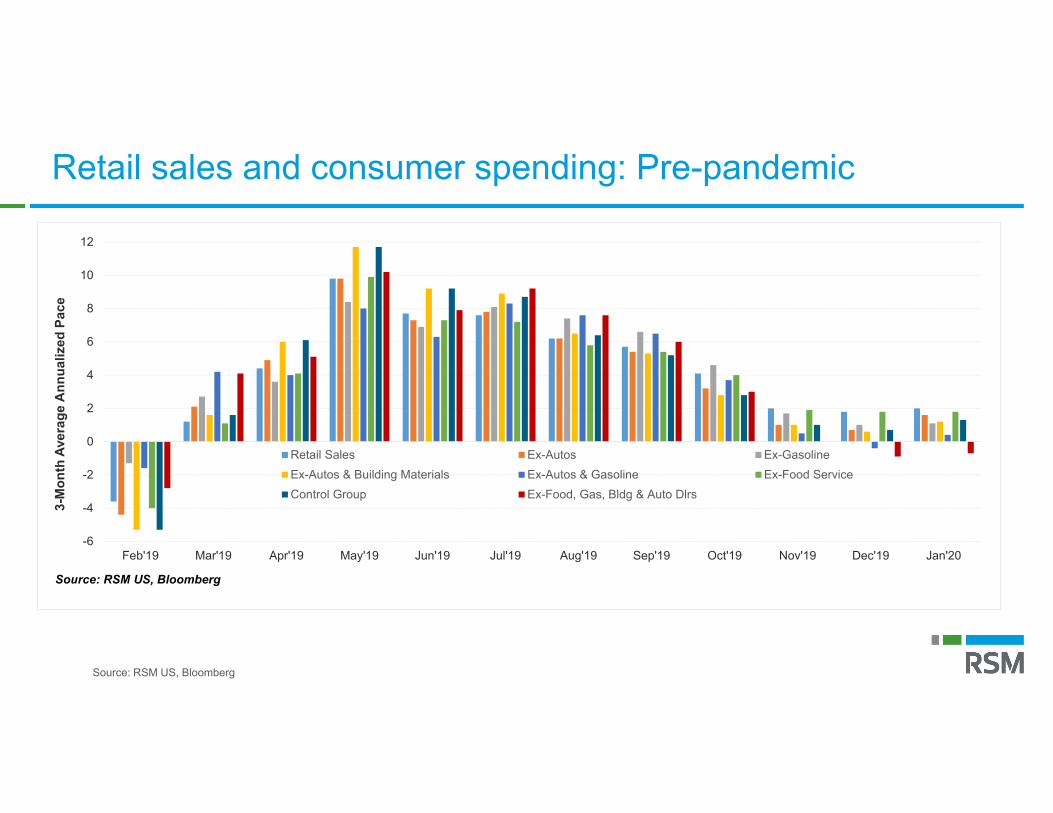

Retail sales and consumer spending: Pre-pandemic

13Source: RSM US, Bloomberg

-6

-4

-2

0

2

4

6

8

10

12

Feb'19 Mar'19 Apr'19 May'19 Jun'19 Jul'19 Aug'19 Sep'19 Oct'19 Nov'19 Dec'19 Jan'20

3-M

onth

Ave

rage

Ann

ualiz

ed P

ace

Retail Sales Ex-Autos Ex-GasolineEx-Autos & Building Materials Ex-Autos & Gasoline Ex-Food ServiceControl Group Ex-Food, Gas, Bldg & Auto Dlrs

Source: RSM US, Bloomberg

© 2020 RSM US LLP. All Rights Reserved.

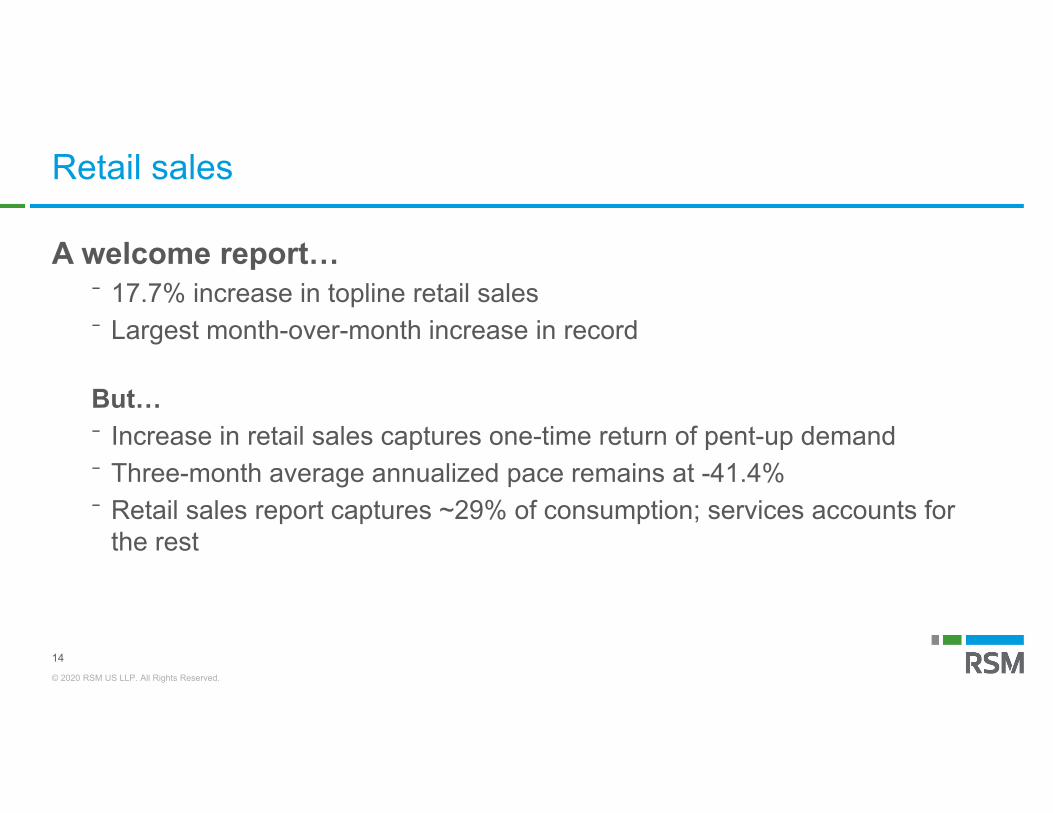

Retail sales

A welcome report…⁻ 17.7% increase in topline retail sales⁻ Largest month-over-month increase in record

But…⁻ Increase in retail sales captures one-time return of pent-up demand⁻ Three-month average annualized pace remains at -41.4%⁻ Retail sales report captures ~29% of consumption; services accounts for

the rest

14

© 2020 RSM US LLP. All Rights Reserved.

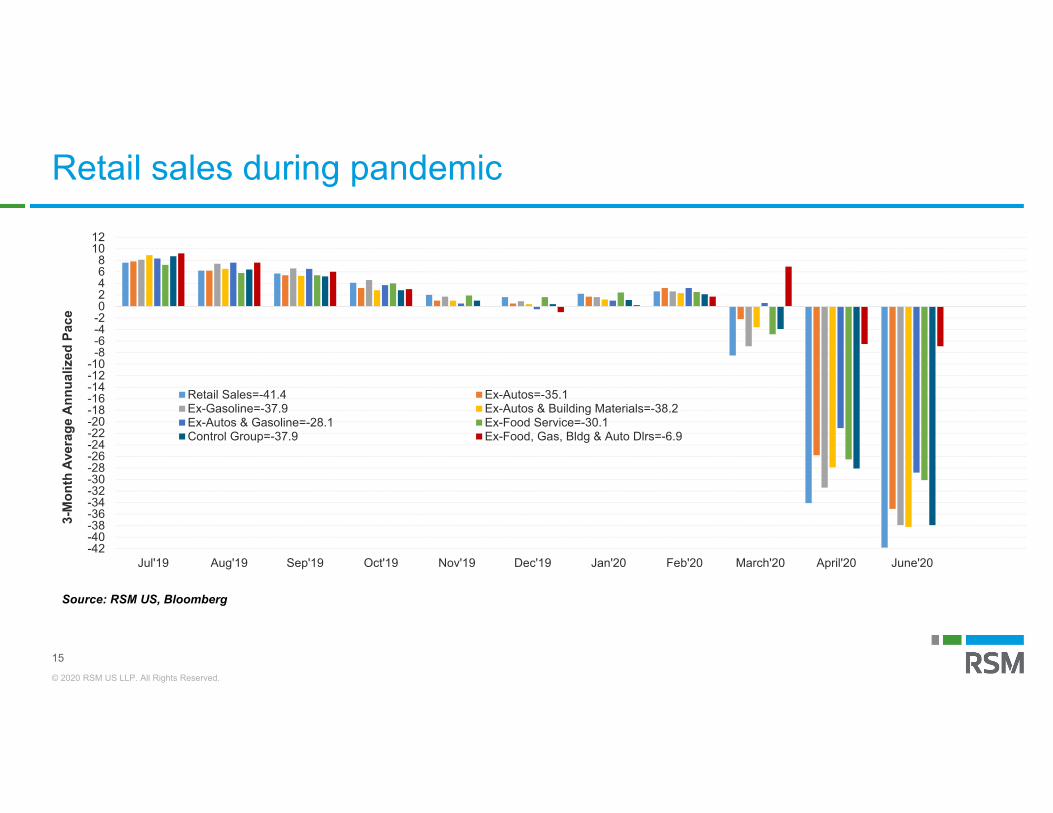

Retail sales during pandemic

15

-42-40-38-36-34-32-30-28-26-24-22-20-18-16-14-12-10

-8-6-4-202468

1012

Jul'19 Aug'19 Sep'19 Oct'19 Nov'19 Dec'19 Jan'20 Feb'20 March'20 April'20 June'20

3-M

onth

Ave

rage

Ann

ualiz

ed P

ace

Retail Sales=-41.4 Ex-Autos=-35.1Ex-Gasoline=-37.9 Ex-Autos & Building Materials=-38.2Ex-Autos & Gasoline=-28.1 Ex-Food Service=-30.1Control Group=-37.9 Ex-Food, Gas, Bldg & Auto Dlrs=-6.9

Source: RSM US, Bloomberg

© 2020 RSM US LLP. All Rights Reserved.

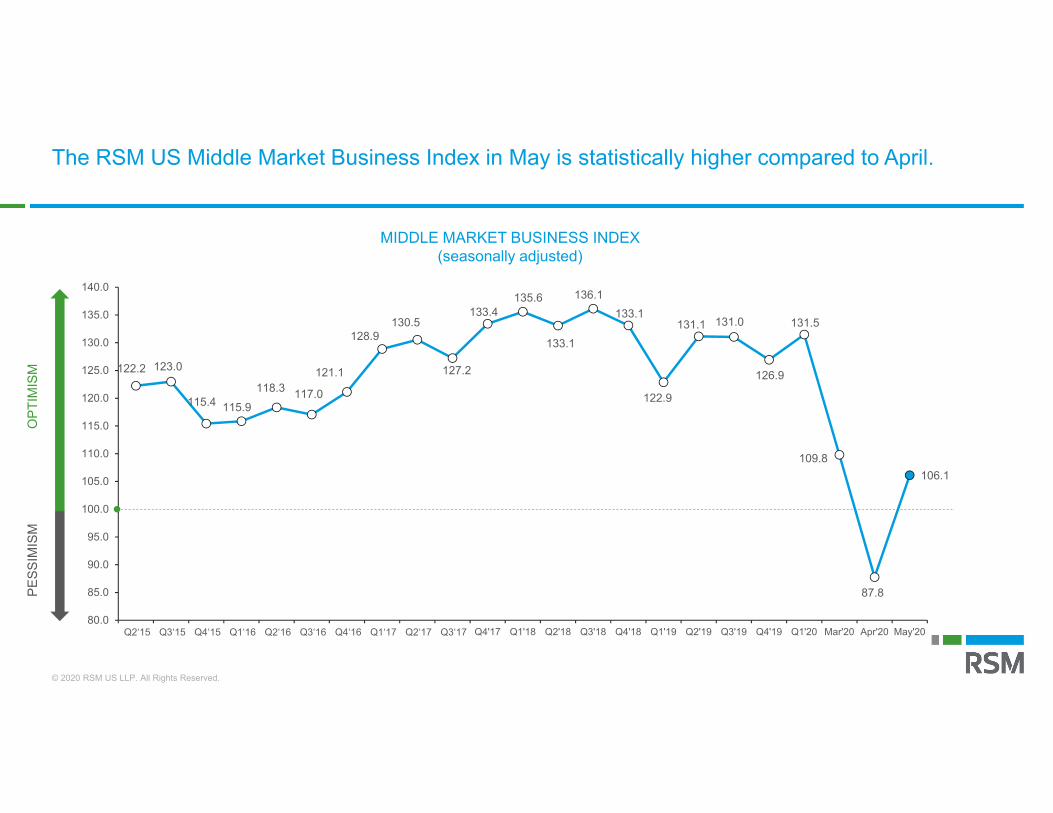

The RSM US Middle Market Business Index in May is statistically higher compared to April.

MIDDLE MARKET BUSINESS INDEX(seasonally adjusted)

122.2 123.0

115.4 115.9118.3 117.0

121.1

128.9130.5

127.2

133.4135.6

133.1

136.1133.1

122.9

131.1 131.0

126.9

131.5

109.8

87.8

106.1

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

125.0

130.0

135.0

140.0

Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘16 Q3‘16 Q4‘16 Q1‘17 Q2‘17 Q3‘17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19 Q2'19 Q3'19 Q4'19 Q1'20 Mar'20 Apr'20 May'20

PESS

IMIS

MO

PTIM

ISM

© 2020 RSM US LLP. All Rights Reserved.

Polling question

What are your expectations regarding the general economy over the next six months? Do you expect the general economy will…

a) Increaseb) Remain unchangedc) Worsen

17

© 2020 RSM US LLP. All Rights Reserved.

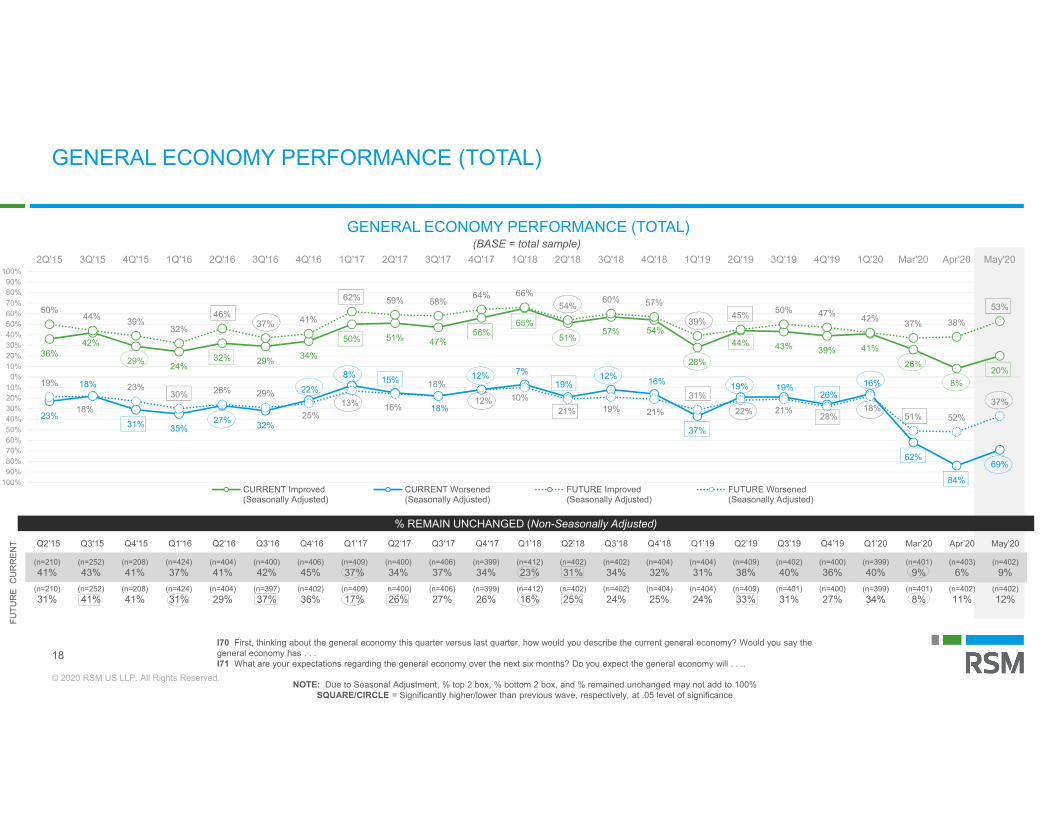

GENERAL ECONOMY PERFORMANCE (TOTAL)

18

36%42%

29% 24%32% 29% 34%

50% 51% 47%56%

65%51%

57% 54%

28%

44% 43% 39% 41%

26%

8%20%

23%

18%

31% 35%27% 32%

22%8% 15%

18%

12% 7%19%

12% 16%

37%

19% 19%26%

16%

62%

84%

69%

50%44% 39%

32%46%

37% 41%

62% 59% 58%64% 66%

54%60% 57%

39%45% 50% 47% 42% 37% 38%

53%

19%

18%

23%30% 26% 29%

25%13% 16%

18%

12% 10%21% 19% 21%

31%

22% 21%28%

18%51% 52%

37%

100%90%80%70%60%50%40%30%20%10%

0%10%20%30%40%50%60%70%80%90%

100%2Q'15 3Q'15 4Q'15 1Q'16 2Q'16 3Q'16 4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 Mar'20 Apr'20 May'20

GENERAL ECONOMY PERFORMANCE (TOTAL)

CURRENT Improved(Seasonally Adjusted)

CURRENT Worsened(Seasonally Adjusted)

FUTURE Improved(Seasonally Adjusted)

FUTURE Worsened(Seasonally Adjusted)

Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘16 Q3‘16 Q4‘16 Q1‘17 Q2‘17 Q3‘17 Q4‘17 Q1’18 Q2’18 Q3’18 Q4’18 Q1’19 Q2’19 Q3’19 Q4’19 Q1’20 Mar’20 Apr’20 May’20

(n=210) (n=252) (n=208) (n=424) (n=404) (n=400) (n=406) (n=409) (n=400) (n=406) (n=399) (n=412) (n=402) (n=402) (n=404) (n=404) (n=409) (n=402) (n=400) (n=399) (n=401) (n=403) (n=402)41% 43% 41% 37% 41% 42% 45% 37% 34% 37% 34% 23% 31% 34% 32% 31% 38% 40% 36% 40% 9% 6% 9%

(n=210) (n=252) (n=208) (n=424) (n=404) (n=397) (n=402) (n=409) n=400) (n=406) (n=399) (n=412) (n=402) (n=402) (n=404) (n=404) (n=409) (n=401) (n=400) (n=399) (n=401) (n=402) (n=402)31% 41% 41% 31% 29% 37% 36% 17% 26% 27% 26% 16% 25% 24% 25% 24% 33% 31% 27% 34% 8% 11% 12%

% REMAIN UNCHANGED (Non-Seasonally Adjusted)

(BASE = total sample)

I70 First, thinking about the general economy this quarter versus last quarter, how would you describe the current general economy? Would you say the general economy has . . .I71 What are your expectations regarding the general economy over the next six months? Do you expect the general economy will . . ..

NOTE: Due to Seasonal Adjustment, % top 2 box, % bottom 2 box, and % remained unchanged may not add to 100%SQUARE/CIRCLE = Significantly higher/lower than previous wave, respectively, at .05 level of significance

FUTU

RE

CU

RR

ENT

© 2020 RSM US LLP. All Rights Reserved.

Polling question

If you had to work remotely for an extended period of time, how much longer do you think you could effectively perform your job duties from home?

a) One monthb) Two monthsc) Three monthsd) Indefinitely

19

© 2020 RSM US LLP. All Rights Reserved.

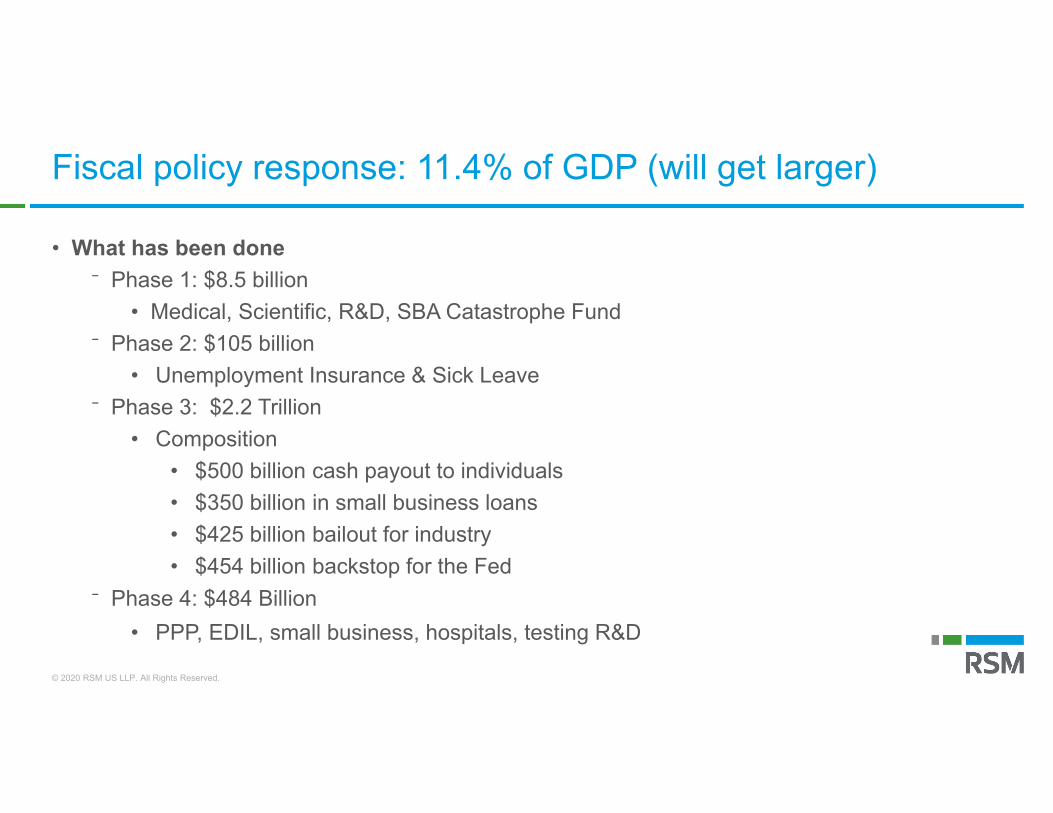

Fiscal policy response: 11.4% of GDP (will get larger)

• What has been done⁻ Phase 1: $8.5 billion

• Medical, Scientific, R&D, SBA Catastrophe Fund⁻ Phase 2: $105 billion

• Unemployment Insurance & Sick Leave⁻ Phase 3: $2.2 Trillion

• Composition• $500 billion cash payout to individuals• $350 billion in small business loans• $425 billion bailout for industry• $454 billion backstop for the Fed

⁻ Phase 4: $484 Billion • PPP, EDIL, small business, hospitals, testing R&D

© 2020 RSM US LLP. All Rights Reserved.

Monetary policy response

• Policy rate to zero⁻ Temporary yield targeting or capping yields likely ⁻ Negative rate policy not on table… yet⁻ $6 trillion in liquidity commitments

• Restart quantitate easing : $700 billion⁻ Large scale asset purchases to accelerate

• Loans to banks at 0%• Open trillion dollar swap lines• Liquidity &lending facilities

⁻ 9 different lending facilities⁻ Main Street Lending Program

21

© 2020 RSM US LLP. All Rights Reserved.

Polling question

How ready are you to return to working from the office?a) I prefer to return the officeb) I prefer to continue working from home

22

© 2020 RSM US LLP. All Rights Reserved.

How long before US back to full production?

• How Long?⁻ Scenario one: single pandemic wave

• US economy should begin to recover in Q4 2020⁻ Scenario two: second pandemic wave

• US economy will endure regionalized lockdowns• Recovery in second half of 2021

⁻ Scenario three: persistent pandemic waves• US economy will endure regionalized lockdowns• Recovery in 2022

• Steps to Fully Reopening Economy⁻ A consistent decrease in the number of cases⁻ The ability to test, isolate and trace⁻ Sufficient amount of health-care infrastructure available if re-emergence⁻ Effective therapy and vaccine available to entire population

23

© 2020 RSM US LLP. All Rights Reserved.

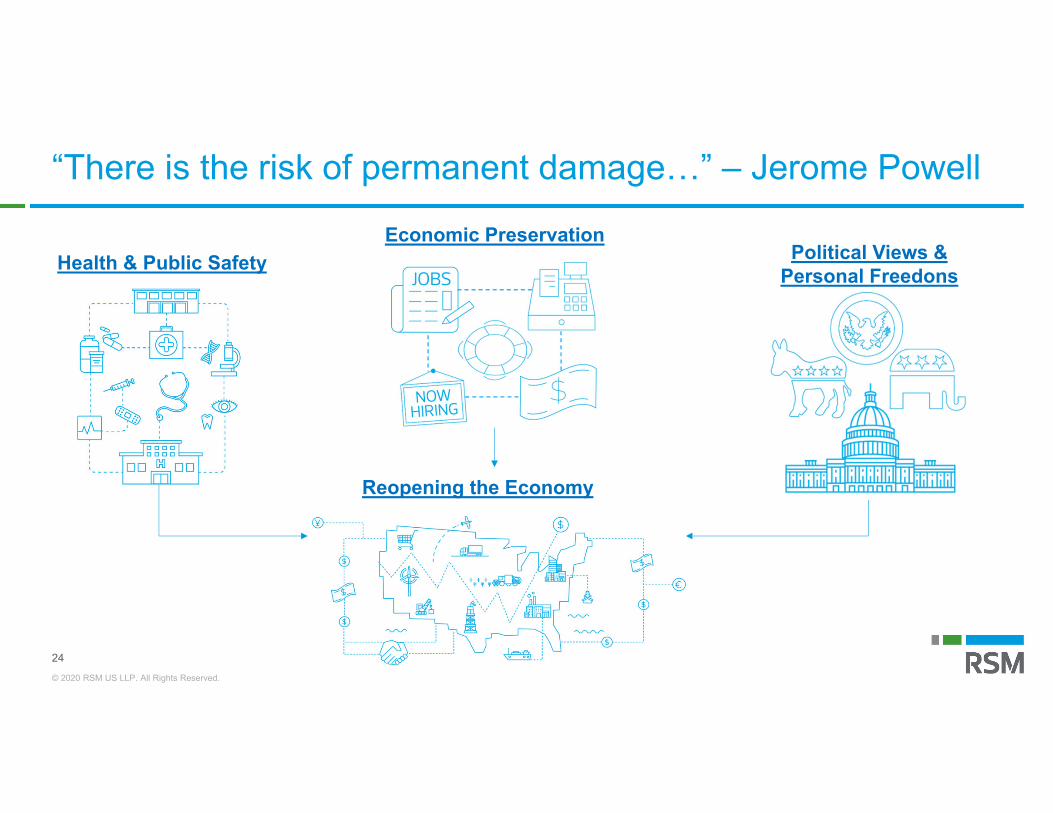

“There is the risk of permanent damage…” – Jerome Powell

24

Health & Public SafetyEconomic Preservation

Political Views & Personal Freedons

Reopening the Economy

© 2020 RSM US LLP. All Rights Reserved.

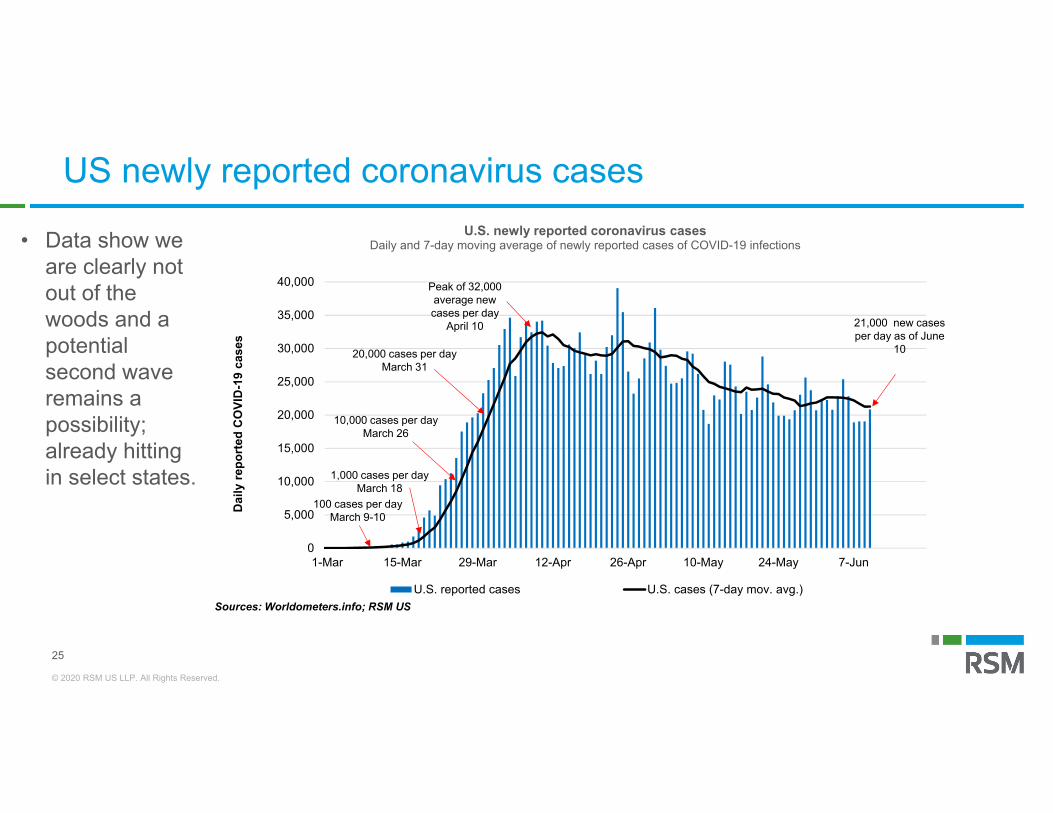

25

US newly reported coronavirus cases

• Data show we are clearly not out of the woods and a potential second wave remains a possibility; already hitting in select states.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1-Mar 15-Mar 29-Mar 12-Apr 26-Apr 10-May 24-May 7-Jun

Dai

ly re

port

ed C

OVI

D-1

9 ca

ses

U.S. newly reported coronavirus casesDaily and 7-day moving average of newly reported cases of COVID-19 infections

U.S. reported cases U.S. cases (7-day mov. avg.)Sources: Worldometers.info; RSM US

Peak of 32,000 average newcases per day

April 10

1,000 cases per day March 18

10,000 cases per day March 26

20,000 cases per day March 31

21,000 new cases per day as of June

10

100 cases per day March 9-10

© 2020 RSM US LLP. All Rights Reserved.

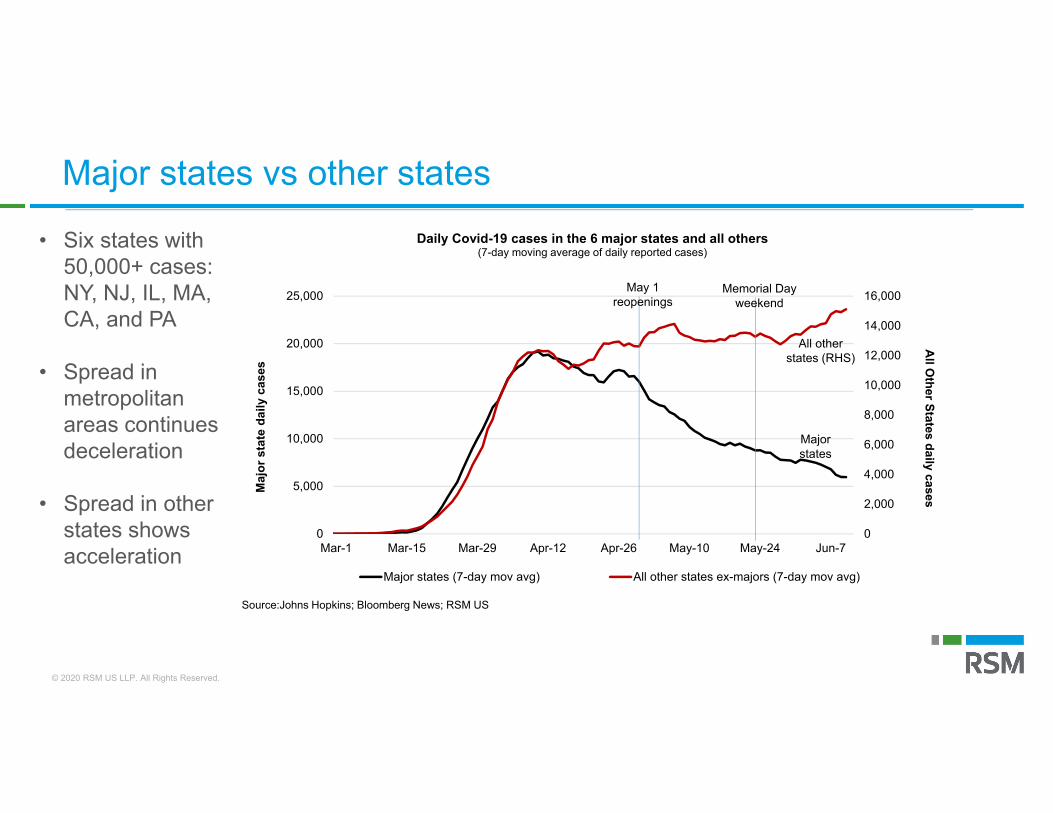

Major states vs other states

• Six states with 50,000+ cases: NY, NJ, IL, MA, CA, and PA

• Spread in metropolitan areas continues deceleration

• Spread in other states shows acceleration

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

0

5,000

10,000

15,000

20,000

25,000

Mar-1 Mar-15 Mar-29 Apr-12 Apr-26 May-10 May-24 Jun-7

All O

ther States daily casesMaj

or s

tate

dai

ly c

ases

Daily Covid-19 cases in the 6 major states and all others (7-day moving average of daily reported cases)

Major states (7-day mov avg) All other states ex-majors (7-day mov avg)

Source:Johns Hopkins; Bloomberg News; RSM US

Majorstates

All other states (RHS)

May 1reopenings

Memorial Dayweekend

© 2020 RSM US LLP. All Rights Reserved.

State

Out

door

/rec

Ret

ail

Food

/drin

kG

room

ing

Ente

rtain

men

tW

orsh

ipIn

dust

ries

Colorado 2 2 2 1 2 0 2Idaho 2 1.5 1.5 1.5 0 1 0

Montana 2 2 0 2 0 2 2Utah 2 2 2 2 0 0 0

Wyoming 2 2 2 2 0 1 2Alaska 2 2 0 0 0 0 2

Arizona 2 2 2 2 0 0 0California 0 2 0 0 0 0 0

Hawaii 2 2 0 2 0 2 2Nevada 2 2 0 0 0 0 2Oregon 1.5 1.5 0 0 0 1.5 1.5

Washington 1.5 1.5 0 0 0 0 0

Stay-home restrictions

States reopening status by sector

Source: BloombergNEF, New York Times, ABC News, U.S. Census; Note: Data as of May 27, 2020.

Color Legend0 Shutdown 1 Opening soon

1.5 Partially open2 Reopened

State

Out

door

/rec

Ret

ail

Food

/drin

kG

room

ing

Ente

rtain

men

tW

orsh

ipIn

dust

ries

Connecticut 2 2 2 1 2 0 2Maine 1.5 1.5 1.5 1.5 0 1 0Mass 2 2 0 2 0 2 2

New Hamp. 2 2 2 2 0 0 0Rhode Is. 2 2 2 2 0 1 2Vermont 2 2 0 0 0 0 2

Delaware 2 2 2 2 0 0 0DC 0 2 0 0 0 0 0

Maryland 2 2 0 2 0 2 2New Jersey 2 2 0 0 0 0 2

New York 1.5 1.5 0 0 0 1.5 1.5Penn 1.5 1.5 0 0 0 0 0

Florida 2 2 2 0 2 2 0Georgia 2 0 2 2 2 0 0

N. Carolina 2 2 2 2 0 0 0S. Carolina 2 2 2 2 0 0 0

Virginia 1.5 1.5 1.5 1.5 0 1.5 0W. Virginia 2 2 2 2 1 0 0

State

Out

door

/rec

Ret

ail

Food

/drin

kG

room

ing

Ente

rtain

men

tW

orsh

ipIn

dust

ries

Illinois 2 2 1 2 0 0 0Indiana 2 2 2 2 2 2 2

Iowa 2 2 2 2 2 2 0Kansas 2 2 2 2 2 2 2

Kentucky 1 2 2 2 1 2 2Michigan 1.5 1.5 1.5 0 0 0 1.5

Minnesota 0 2 1 1 0 2 2Missouri 2 2 2 2 2 0 0

Nebraska 1 0 1.5 1.5 1 1.5 0N. Dakota 2 0 2 2 2 0 0

Ohio 2 2 2 2 0 0 2Oklahoma 2 0 2 2 2 2 2S. Dakota 2 2 2 2 2 2 2

Tennessee 1.5 1.5 1.5 1.5 0 0 0Wisconsin 2 2 0 2 0 0 0

Alabama 2 2 2 2 2 0 0Arkansas 2 0 2 2 2 0 0Louisiana 2 2 2 2 2 2 0

Mississippi 2 2 2 2 2 0 0New Mexico 1.5 1.5 0 1.5 0 1.5 1.5

Texas 2 2 2 2 2 0 2

States continue to reopen and now most have loosened restrictions on retail activities and outdoor recreation, though the status of industries is more varied

© 2020 RSM US LLP. All Rights Reserved.

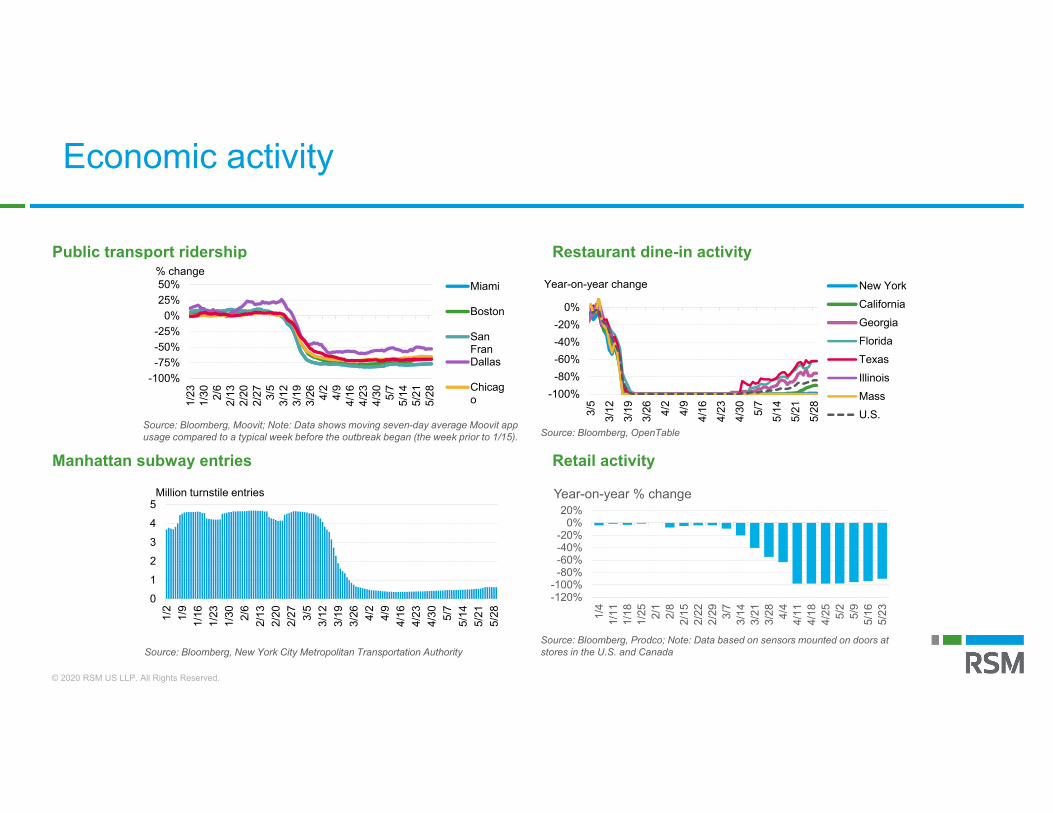

Public transport ridership Restaurant dine-in activity

Manhattan subway entries Retail activity

Economic activity

Source: Bloomberg, OpenTableSource: Bloomberg, Moovit; Note: Data shows moving seven-day average Moovit app usage compared to a typical week before the outbreak began (the week prior to 1/15).

Source: Bloomberg, New York City Metropolitan Transportation Authority

-120%-100%-80%-60%-40%-20%

0%20%

1/4

1/11

1/18

1/25 2/1

2/8

2/15

2/22

2/29 3/7

3/14

3/21

3/28 4/4

4/11

4/18

4/25 5/2

5/9

5/16

5/23

Year-on-year % change

Source: Bloomberg, Prodco; Note: Data based on sensors mounted on doors at stores in the U.S. and Canada

0

1

2

3

4

5

1/2

1/9

1/16

1/23

1/30 2/6

2/13

2/20

2/27 3/5

3/12

3/19

3/26 4/2

4/9

4/16

4/23

4/30 5/7

5/14

5/21

5/28

Million turnstile entries

-100%-75%-50%-25%

0%25%50%

1/23

1/30 2/6

2/13

2/20

2/27 3/5

3/12

3/19

3/26 4/2

4/9

4/16

4/23

4/30 5/7

5/14

5/21

5/28

% changeMiami

Boston

SanFranDallas

Chicago -100%

-80%-60%-40%-20%

0%

3/5

3/12

3/19

3/26 4/

24/

94/

164/

234/

30 5/7

5/14

5/21

5/28

Year-on-year change New YorkCaliforniaGeorgiaFloridaTexasIllinoisMassU.S.

© 2020 RSM US LLP. All Rights Reserved.

Source: Bloomberg, Prodco; Note: Data based on sensors mounted on doors at stores in the U.S. and Canada

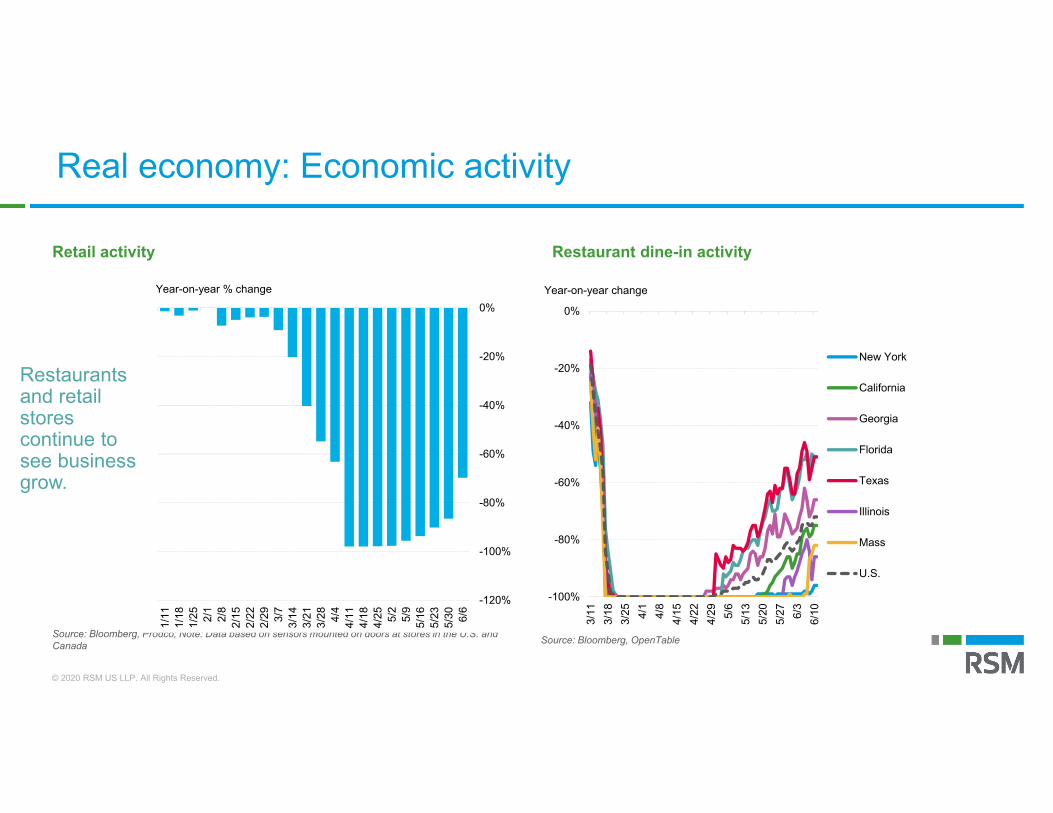

Retail activity Restaurant dine-in activity

Restaurants and retail stores continue to see business grow.

Source: Bloomberg, OpenTable

RTRFIMTD Index

-100%

-80%

-60%

-40%

-20%

0%

3/11

3/18

3/25 4/1

4/8

4/15

4/22

4/29 5/6

5/13

5/20

5/27 6/3

6/10

Year-on-year change

New York

California

Georgia

Florida

Texas

Illinois

Mass

U.S.

-120%

-100%

-80%

-60%

-40%

-20%

0%

6/6

5/30

5/23

5/165/

95/

24/

254/

184/

114/4

3/28

3/21

3/143/

72/

292/

222/

152/8

2/1

1/25

1/18

1/11

Year-on-year % change

Real economy: Economic activity

© 2020 RSM US LLP. All Rights Reserved.

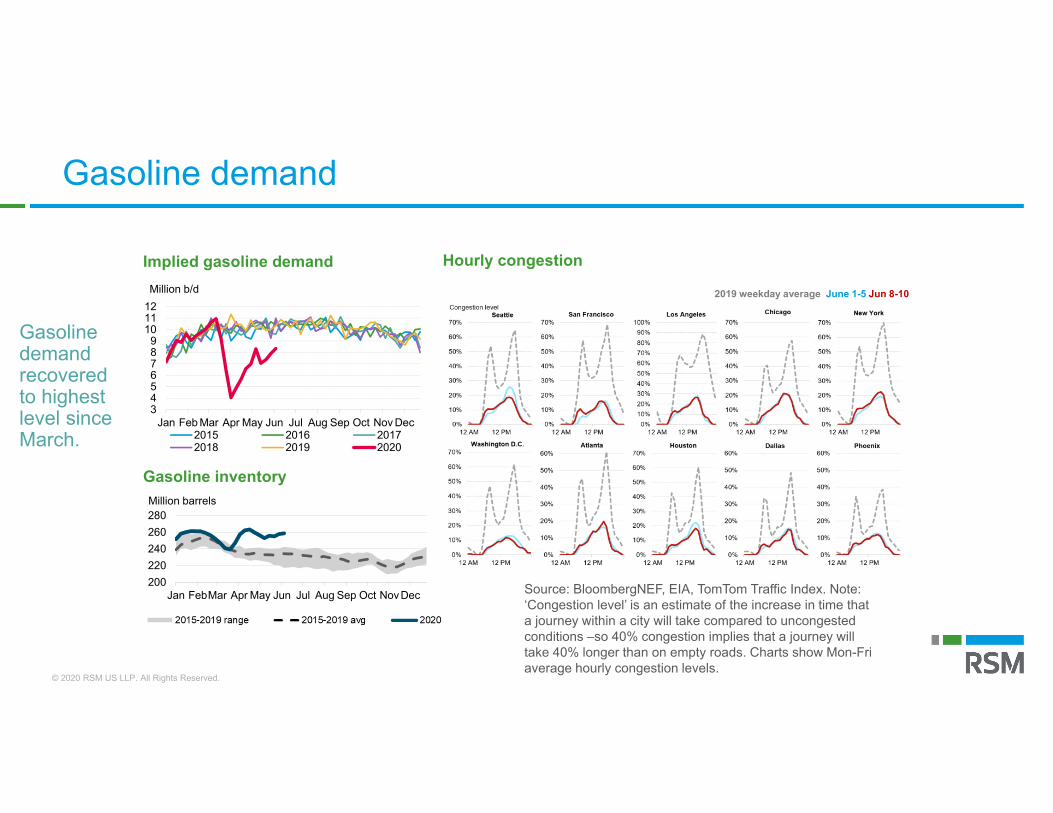

Source: BloombergNEF, EIA, TomTom Traffic Index. Note: ‘Congestion level’ is an estimate of the increase in time that a journey within a city will take compared to uncongested conditions –so 40% congestion implies that a journey will take 40% longer than on empty roads. Charts show Mon-Fri average hourly congestion levels.

Gasoline demand recovered to highest level since March.

2019 weekday average June 1-5 Jun 8-10

Implied gasoline demand Hourly congestion

Gasoline inventory

200220240260280

Jan FebMar Apr May Jun Jul Aug Sep Oct NovDec

Million barrels

3456789

101112

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Million b/d

2015 2016 20172018 2019 2020

Gasoline demand

© 2020 RSM US LLP. All Rights Reserved.

Polling question

When will you be comfortable flying again? a) Right nowb) Pretty soonc) Not until there is a Covid-19 vaccine

31

© 2020 RSM US LLP. All Rights Reserved.

30

32

34

36

38

40

42

44

46

48

50

Jan

Feb

Mar Apr

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

Million barrels

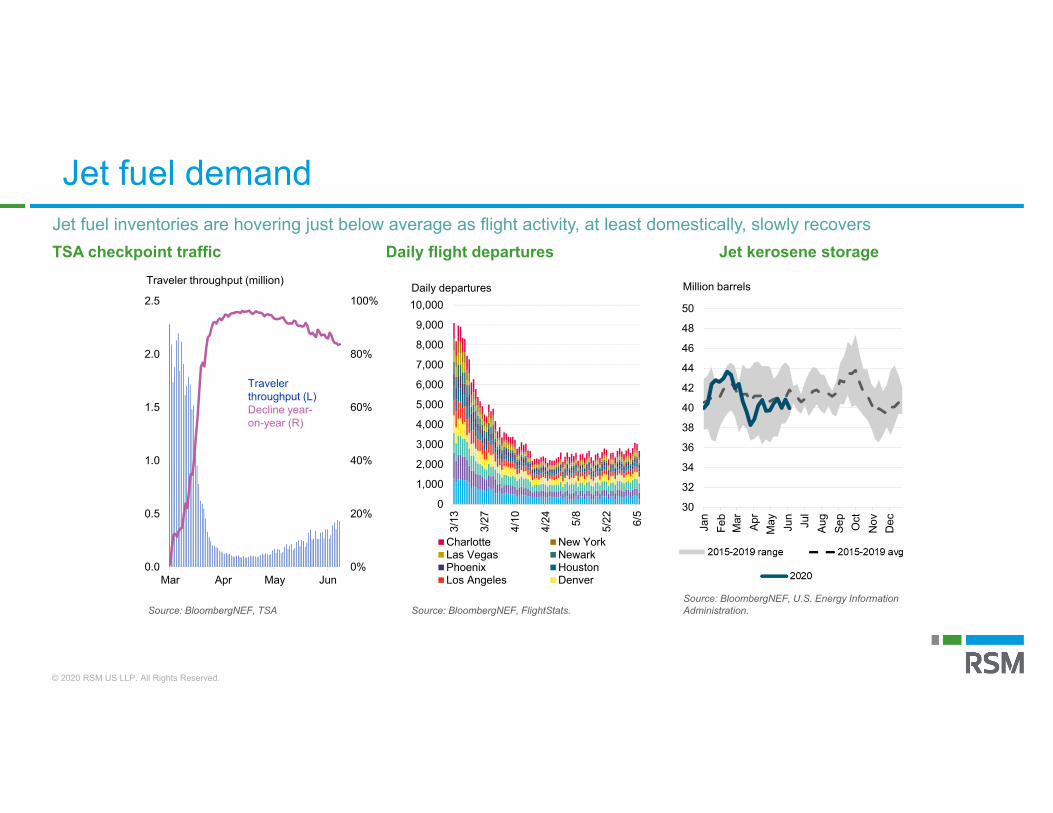

TSA checkpoint traffic Daily flight departures Jet kerosene storageJet fuel inventories are hovering just below average as flight activity, at least domestically, slowly recovers

Source: BloombergNEF, TSA Source: BloombergNEF, FlightStats. Source: BloombergNEF, U.S. Energy Information Administration.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

3/13

3/27

4/10

4/24 5/8

5/22 6/5

Daily departures

Charlotte New YorkLas Vegas NewarkPhoenix HoustonLos Angeles Denver

0%

20%

40%

60%

80%

100%

0.0

0.5

1.0

1.5

2.0

2.5

Mar Apr May Jun

Traveler throughput (million)

Traveler throughput (L)Decline year-on-year (R)

Jet fuel demand

© 2020 RSM US LLP. All Rights Reserved.

Source: BloombergNEF, FlightStats

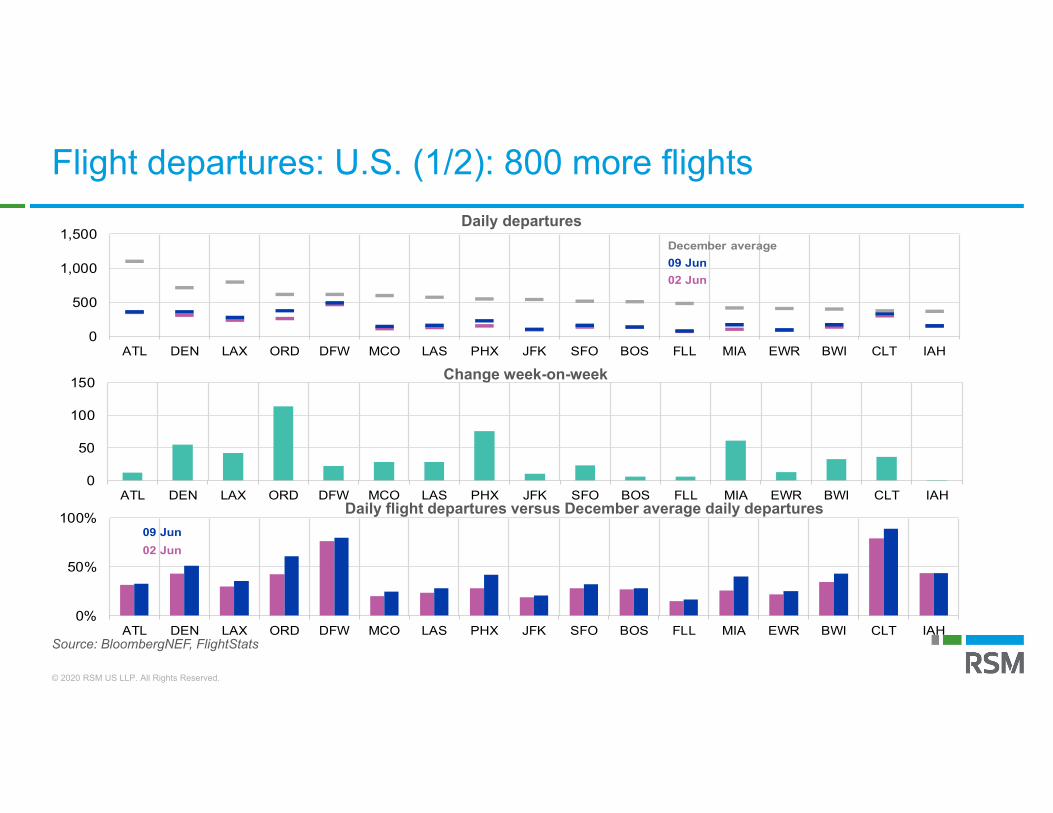

Flight departures: U.S. (1/2): 800 more flights

Daily flight departures versus December average daily departures

Change week-on-week

Daily departures

0

500

1,000

1,500

ATL DEN LAX ORD DFW MCO LAS PHX JFK SFO BOS FLL MIA EWR BWI CLT IAH

09 Jun02 Jun

December average

0

50

100

150

ATL DEN LAX ORD DFW MCO LAS PHX JFK SFO BOS FLL MIA EWR BWI CLT IAH

0%

50%

100%

ATL DEN LAX ORD DFW MCO LAS PHX JFK SFO BOS FLL MIA EWR BWI CLT IAH

09 Jun02 Jun

© 2020 RSM US LLP. All Rights Reserved.

Source: BloombergNEF, FlightStats

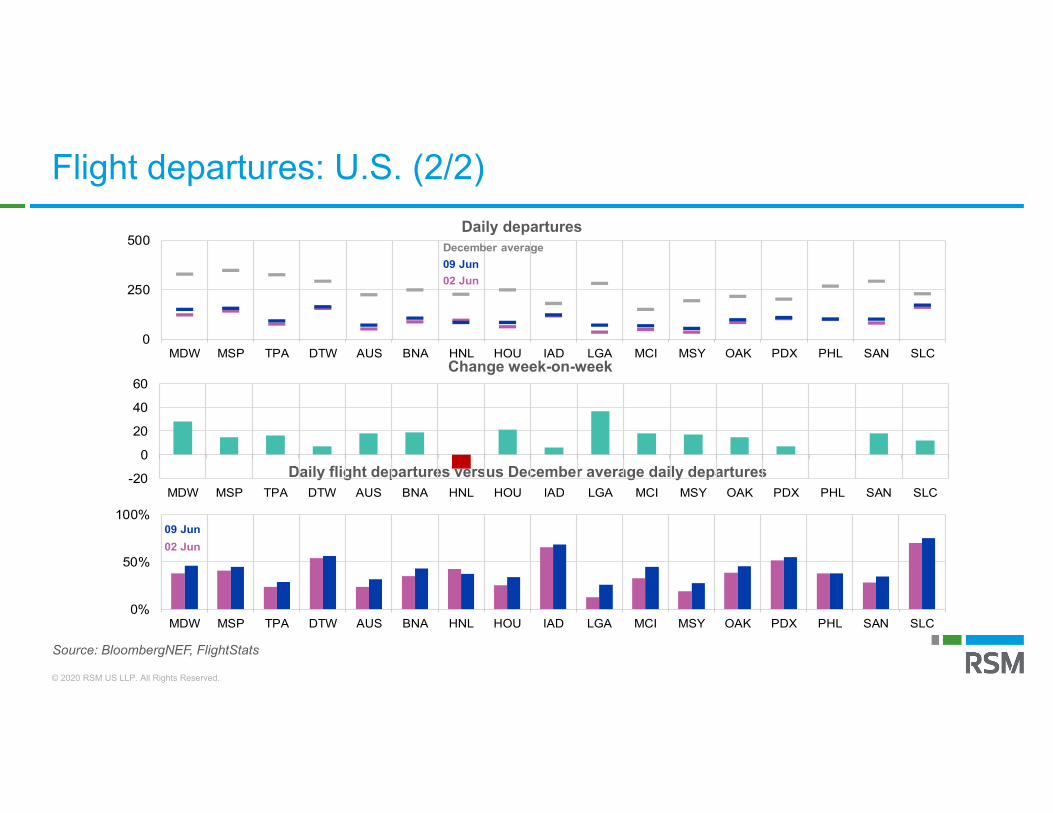

Flight departures: U.S. (2/2)

Daily flight departures versus December average daily departures

Change week-on-week

Daily departures

0

250

500

MDW MSP TPA DTW AUS BNA HNL HOU IAD LGA MCI MSY OAK PDX PHL SAN SLC

09 Jun02 Jun

December average

-20

0

20

40

60

MDW MSP TPA DTW AUS BNA HNL HOU IAD LGA MCI MSY OAK PDX PHL SAN SLC

0%

50%

100%

MDW MSP TPA DTW AUS BNA HNL HOU IAD LGA MCI MSY OAK PDX PHL SAN SLC

09 Jun02 Jun

© 2020 RSM US LLP. All Rights Reserved.

Source: TSA, BloombergNEF

TSA checkpoint traffic

0%

20%

40%

60%

80%

100%

0.0

0.5

1.0

1.5

2.0

2.5

Mar Apr May Jun

Traveler throughput (million)

Traveler throughput (L)Decline year-on-year (R)

© 2020 RSM US LLP. All Rights Reserved.

US outlook: What could go right?

Positive themes• Growth acceleration

⁻ Business investment awakens⁻ Innovation takes off⁻ 5G changes current urban vs rural divide (new demand driven)⁻ Health care spending as a percentage of GDP drops

• Employment growth solid⁻ Unemployment rate at historic low⁻ Automation of jobs creates new, better employment opportunities (reconstitute)⁻ Wage growth resumes; household balance sheets very clean (top two quintiles)

• Positive risks to the economic outlook⁻ Peak polarization passes; collaboration defines coming decade⁻ Policy addresses key challenges; labor market, unbalanced growth

36

© 2020 RSM US LLP. All Rights Reserved.

Thank you!

• For more information on these topics and more, visit our Coronavirus Resource Center, updated on a daily basis.

© 2020 RSM US LLP. All Rights Reserved.

This document contains general information, may be based on authorities that are subject to change, and is not a substitute for professional advice or services. This document does not constitute audit, tax, consulting, business, financial, investment, legal or other professional advice, and you should consult a qualified professional advisor before taking any action based on the information herein. RSM US LLP, its affiliates and related entities are not responsible for any loss resulting from or relating to reliance on this document by any person. Internal Revenue Service rules require us to inform you that this communication may be deemed a solicitation to provide tax services. This communication is being sent to individuals who have subscribed to receive it or who we believe would have an interest in the topics discussed.

RSM US LLP is a limited liability partnership and the U.S. member firm of RSM International, a global network of independent audit, tax and consulting firms. The member firms of RSM International collaborate to provide services to global clients, but are separate and distinct legal entities that cannot obligate each other. Each member firm is responsible only for its own acts and omissions, and not those of any other party. Visit rsmus.com/aboutus for more information regarding RSM US LLP and RSM International.

RSM, the RSM logo and the power of being understood are registered trademarks of RSM International Association.

© 2020 RSM US LLP. All Rights Reserved.

RSM US LLP

AddressCityPhone

+1 800 274 3978rsmus.com

38