Embed Size (px)

Citation preview

© 2012 Rockwell Publishing

Financing Residential Real Estate

Lesson 14:

Fair Lending and Consumer Protection

© 2012 Rockwell Publishing

Introduction

This lesson will cover:federal fair lending lawsconsumer protection lawspredatory lending

© 2012 Rockwell Publishing

Fair Lending Laws

Residential mortgage loan transactions subject to:

Equal Credit Opportunity ActFair Housing ActCommunity Reinvestment ActHome Mortgage Disclosure Act

© 2012 Rockwell Publishing

Fair Lending Laws

Equal Credit Opportunity Act (ECOA): passed in 1974, applies to business and consumer credit.

Consumer credit: extended to individual for personal, family, or household purposes.

Includes residential mortgage loans.

Equal Credit Opportunity Act

© 2012 Rockwell Publishing

Equal Credit Opportunity Act

Prohibits discrimination based on:race/colorreligionnational originsexmarital statusage

Protected categories

© 2012 Rockwell Publishing

Equal Credit Opportunity Act

Also prohibits discrimination against applicant who:

receives income from public assistance exercised rights under federal credit laws

Protected categories

© 2012 Rockwell Publishing

Equal Credit Opportunity Act

Lenders cannot discriminate against applicants when:

interviewing and communicating analyzing financesoffering credit terms

Prohibited actions

© 2012 Rockwell Publishing

Equal Credit Opportunity Act

Lenders:cannot discourage anyone from applying

for loanmust apply credit guidelines to everyone in

same manner

Prohibited actions

© 2012 Rockwell Publishing

Equal Credit Opportunity Act

Provided information isn’t used to discriminate, lenders can ask about:

agemarital statusnumber and ages of dependents (but not

childbearing plans)

Permissible questions

© 2012 Rockwell Publishing

Equal Credit Opportunity Act

Lenders:have up to 30 days to notify whether

application accepted or rejected

If rejected:specific reason for decision, orright to inquire further within 60 days

Notifying applicants

© 2012 Rockwell Publishing

Fair Lending Laws

Federal Fair Housing Act: 1968 law, applies to transactions involving one- to four-unit residential properties.

Fair Housing Act

© 2012 Rockwell Publishing

Fair Housing Act

Prohibits lending discrimination based on:racecolornational originreligionsexdisabilityfamilial status

Protected categories

© 2012 Rockwell Publishing

Fair Housing Act

Illegal for lenders to do any of the following for discriminatory reasons:

refuse to provide information about mortgage loans

refuse to make mortgage loanimpose different terms or conditions on

mortgage loan

Prohibited actions

© 2012 Rockwell Publishing

Fair Housing Act

Redlining: refusal to make loans secured by property located in certain neighborhoods based on race or ethnic background of residents.

Can refuse loan in certain neighborhood when:property values actually decliningbased on objective economic criteriawithout regard to racial, ethnic composition

Redlining

© 2012 Rockwell Publishing

Fair Lending Laws

Community Reinvestment Act (CRA): 1977 law encourages lenders to serve more low- and moderate-income people living in areas where lenders do business.

Addresses redlining.Applies to depository institutions.Doesn’t apply to independent mortgage

companies.

Community Reinvestment Act

© 2012 Rockwell Publishing

Community Reinvestment Act

Institutions must submit reports on home and business loans they’ve made.

Evaluated during bank examinations.Taken into account when lender wants to

expand operations.

CRA compliance

© 2012 Rockwell Publishing

Community Reinvestment Act

Lenders not required to lower underwriting standards.

“Safe and sound” lending practices should still be used.

Goal: move beyond negative assumptions that lead to redlining and other discrimination.

CRA and underwriting standards

© 2012 Rockwell Publishing

Fair Lending Laws

Home Mortgage Disclosure Act (HMDA): 1975, helps government monitor if lenders are fulfilling obligation to serve housing needs of community.

Facilitates enforcement of fair housing act prohibitions (example: redlining).

Applies to large institutional lenders doing business in metropolitan areas.

Home Mortgage Disclosure Act

© 2012 Rockwell Publishing

Home Mortgage Disclosure Act

Lenders must submit annual reports to government on residential mortgage loans originated or purchased during fiscal year.

Includes purchase loans, home improvement loans, refinancing.

Doesn’t include home equity loans for other purposes (credit consolidation).

Requires annual reports

© 2012 Rockwell Publishing

Home Mortgage Disclosure Act

For each loan or application, lender must provide:

dollar amount and type of loan purpose of loanwhether application was request for

preapproval and if denied or approvedborrower’s race, ethnicity, sex, and gross

annual incometype and location of property

Loan data

© 2012 Rockwell Publishing

Home Mortgage Disclosure Act

HMDA:implemented by Federal Reserve Board’s

Regulation C2004 and 2008 amendments require lenders

to include information about loan costs, terms

high-cost loans may alert regulators to predatory lending practices

Predatory lending

© 2012 Rockwell Publishing

SummaryFair Lending Laws

• Equal Credit Opportunity Act

• Redlining

• Fair Housing Act

• Community Reinvestment Act

• Home Mortgage Disclosure Act

• Predatory lending

© 2012 Rockwell Publishing

Consumer Protection Laws

Federal consumer protection laws that apply to mortgage loan transactions:

Truth in Lending ActReal Estate Settlement Procedures Act

© 2012 Rockwell Publishing

Consumer Protection Laws

Truth in Lending Act (TILA): 1968.Implemented by Federal Reserve Board’s

Regulation Z.Regulates content and timing of disclosure

of interest rates, finance charges.

Truth in Lending Act

© 2012 Rockwell Publishing

Truth in Lending Act

Applies only to consumer loans.Consumer loan: loan used for personal,

family, or household purposes.

Consumer loan is covered by TILA if it will be repaid in more than four installments (or is subject to finance charges) and is either:

for $50,000 or less, orsecured by real property.

Loans covered by TILA

© 2012 Rockwell Publishing

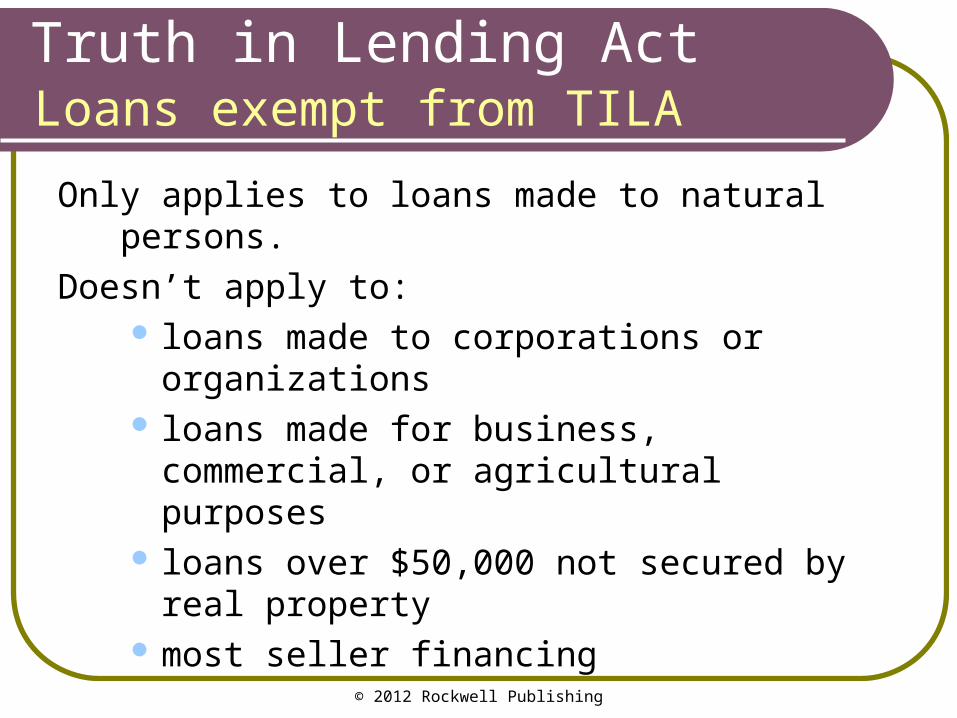

Truth in Lending Act

Only applies to loans made to natural persons.

Doesn’t apply to: loans made to corporations or

organizations loans made for business, commercial,

or agricultural purposes loans over $50,000 not secured by real

property most seller financing

Loans exempt from TILA

© 2012 Rockwell Publishing

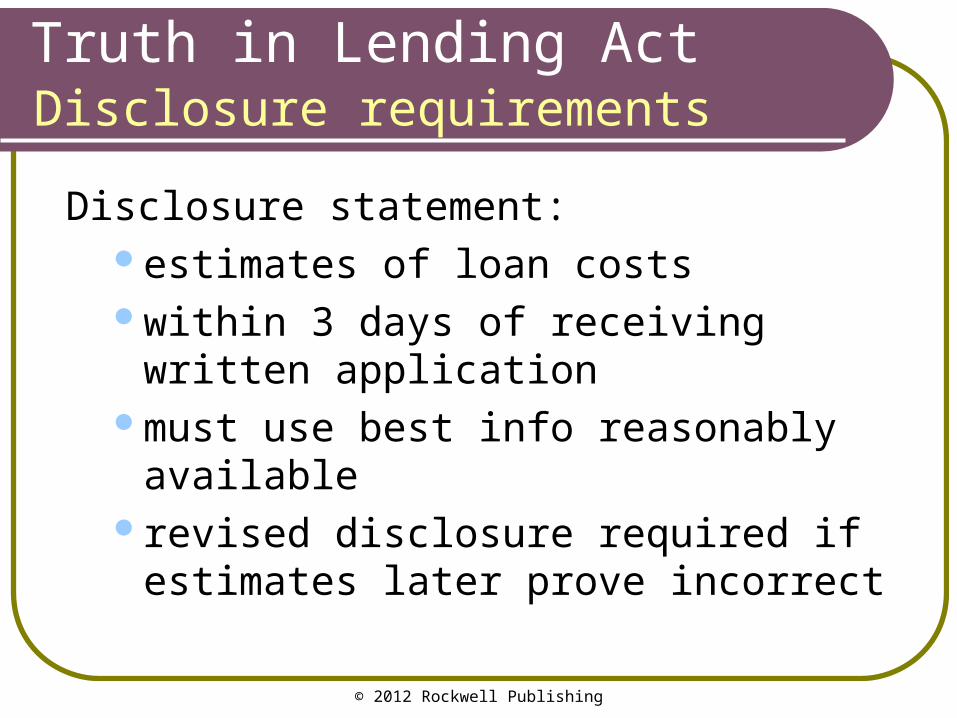

Truth in Lending Act

Disclosure statement:estimates of loan costswithin 3 days of receiving written

applicationmust use best info reasonably availablerevised disclosure required if estimates

later prove incorrect

Disclosure requirements

© 2012 Rockwell Publishing

Truth in Lending Act

Two most important disclosures:total finance charge

“Dollar amount your credit will cost you”annual percentage rate (APR)

“Cost of your credit as a yearly rate”

Disclosure requirements

© 2012 Rockwell Publishing

TILA Disclosure Requirements

Total finance charge: sum of fees and charges borrower will pay in connection with loan.

Includes interest. May also include:

origination fee, discount pointsfinder’s fee, service chargemortgage insurance premiumsguaranty feemortgage broker’s fee

Total finance charge

© 2012 Rockwell Publishing

TILA Disclosure Requirements

application feeappraisal feedocument prep feenotary feecredit report feesurvey feetitle report fee

title insurance premiumspest inspection feeflood inspection feeimpoundspoints paid by sellerlate payment feesfees for default

Total finance charge

Doesn’t include:

© 2012 Rockwell Publishing

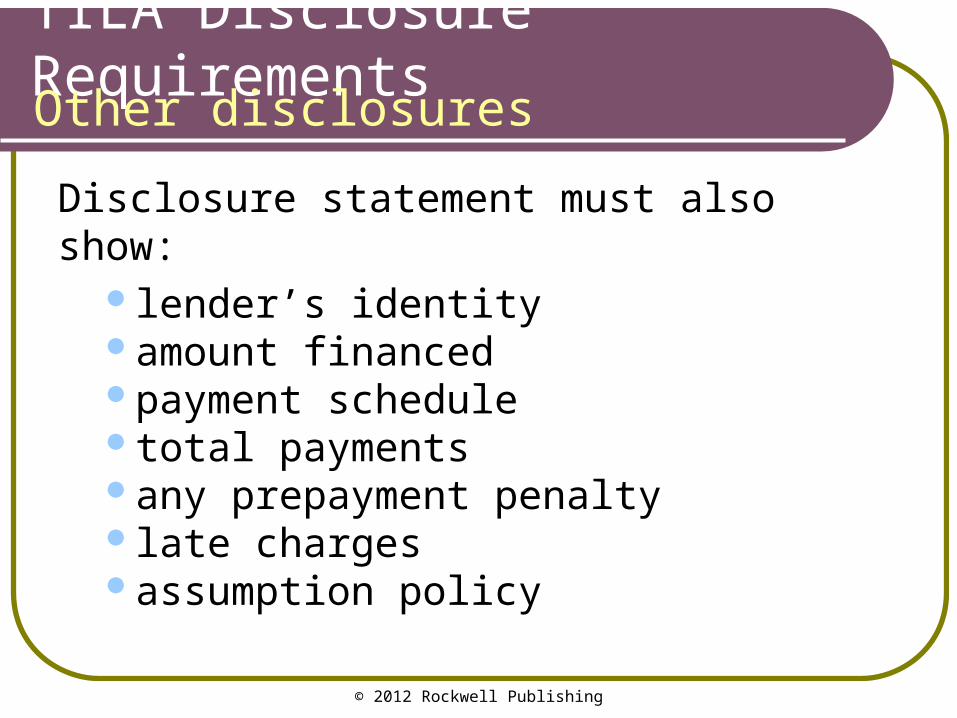

TILA Disclosure Requirements

Disclosure statement must also show:lender’s identityamount financedpayment scheduletotal paymentsany prepayment penaltylate chargesassumption policy

Other disclosures

© 2012 Rockwell Publishing

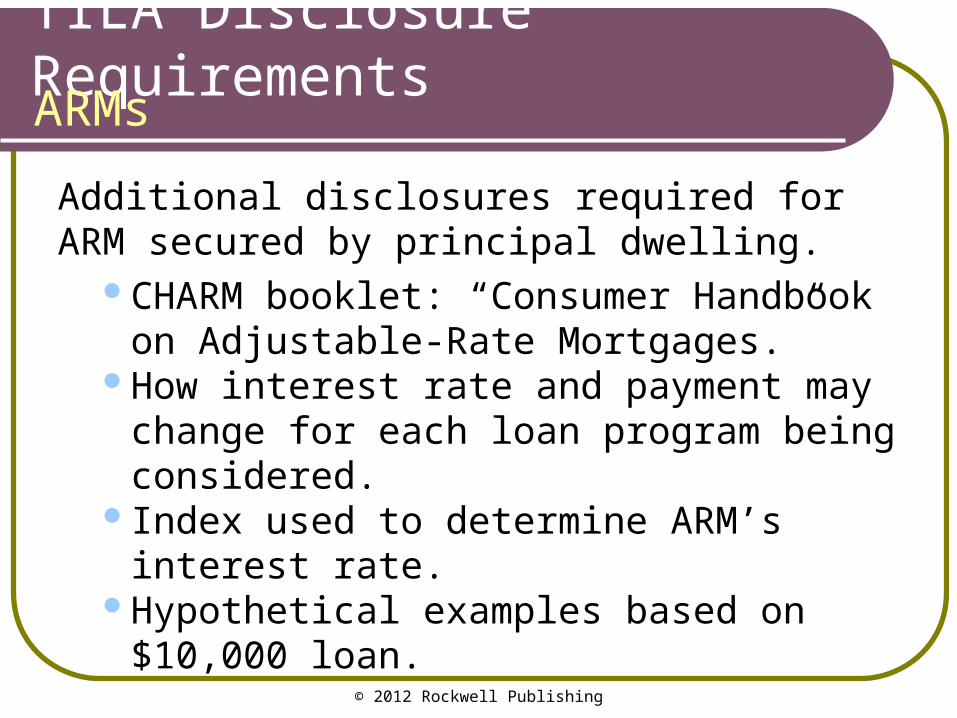

TILA Disclosure Requirements

Additional disclosures required for ARM secured by principal dwelling.

CHARM booklet: “Consumer Handbook on Adjustable-Rate Mortgages.”

How interest rate and payment may change for each loan program being considered.

Index used to determine ARM’s interest rate.

Hypothetical examples based on $10,000 loan.

ARMs

© 2012 Rockwell Publishing

TILA Disclosure Requirements

Lender must notify borrower each time interest rate is being adjusted.

Effect of adjustment on payment, loan balance, and other aspects of loan.

If payment amount will change: notice sent at least 25 days, but no more than 120 days, before new payment due.

If payment amount won’t change: notice sent at least once a year.

ARM adjustment notice

© 2012 Rockwell Publishing

Truth in Lending Act

When security property is borrower’s principal residence, borrower may rescind loan agreement within 3 days of:

signing agreement,receiving disclosure statement, orreceiving notice of right of rescission.

Right of rescission

© 2012 Rockwell Publishing

Truth in Lending Act

Notice of right to rescind:can’t be part of other TILA disclosures or

documentsmust be separate documentdoesn’t expire for 3 years if borrower never

receives statement or notice

Right of rescission

© 2012 Rockwell Publishing

Truth in Lending Act

Right of rescission only applies to:home equity loansrefinancing with new lender

Doesn’t apply to:purchase loansconstruction loans

Right of rescission

© 2012 Rockwell Publishing

Truth in Lending Act

Advertising rules apply to anyone who advertises consumer credit, not just lenders.

Rules prohibit:bait and switch tacticsmisleading ads

Advertising under TILA

© 2012 Rockwell Publishing

Truth in Lending Act

Always legal to state cash price or APR in ad.If particular “trigger” terms are used, rest of

terms must also be disclosed. Trigger terms: downpayment, interest rate,

monthly payment. Ads for loans with variable rates (ARMs):

rates/terms may change can’t advertise loan as “fixed”

Advertising under TILA

© 2012 Rockwell Publishing

SummaryTruth in Lending Act

• Regulation Z

• Consumer loan

• Annual percentage rate

• Total finance charge

• ARM disclosures

• Adjustment notice

• Right of rescission

• Advertising rules

© 2012 Rockwell Publishing

Consumer Protection Laws

Real Estate Settlement Procedures Act (RESPA): 1974, enforced by Consumer Financial Protection Bureau (CFPB)

Affects how closing is handled in most residential mortgage transactions.

Applies to any professional involved in process. Includes real estate agents.

RESPA

© 2012 Rockwell Publishing

RESPA

Two main goals:to provide borrowers with information

about all financing fees and closing coststo eliminate kickbacks and referral fees

that increase borrowers’ costs

Purpose of law

© 2012 Rockwell Publishing

RESPA

RESPA applies to all federally related loan transactions.

Includes most residential mortgage loans.Includes almost all institutional lenders.

Covered transactions

© 2012 Rockwell Publishing

RESPA

Federally related loan:

1. secured by residential property with (or land used to build) up to four dwelling units (includes condos, mobile homes), AND

2. lender is federally regulated, has federally insured accounts, is assisted by federal government, sells loans to secondary market agency, or makes more than $1 million in real estate loans per year.

Covered transactions

© 2012 Rockwell Publishing

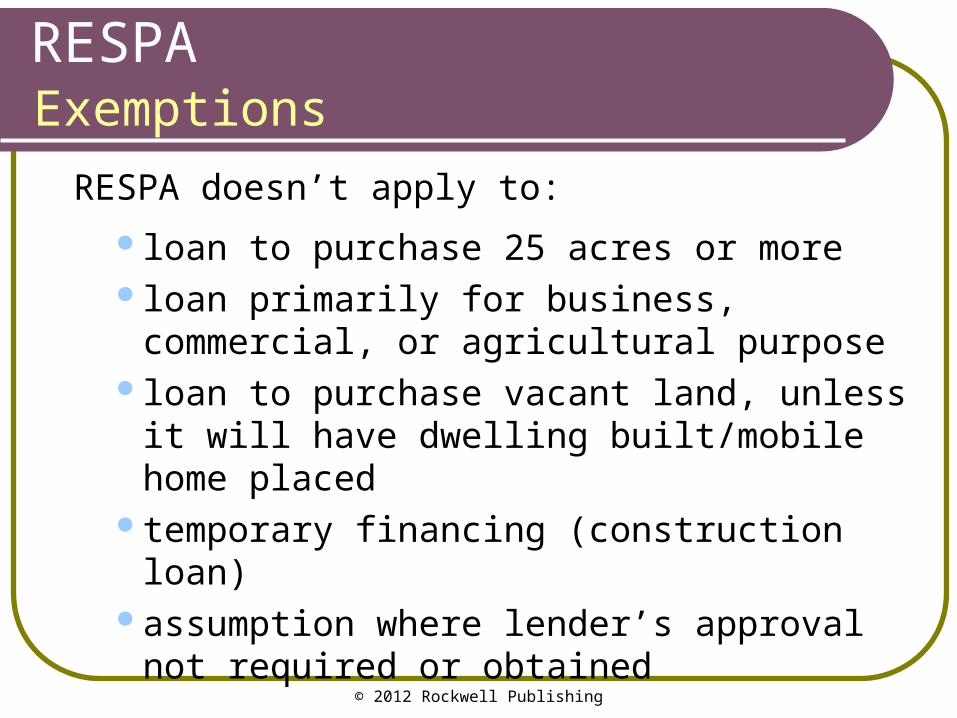

RESPA

RESPA doesn’t apply to:

loan to purchase 25 acres or moreloan primarily for business, commercial, or

agricultural purposeloan to purchase vacant land, unless it will

have dwelling built/mobile home placedtemporary financing (construction loan)assumption where lender’s approval

not required or obtained

Exemptions

© 2012 Rockwell Publishing

RESPA Requirements, Restrictions

1. Within 3 days of written application, lender must give loan applicant:

booklet about settlement procedures

mortgage servicing disclosure statement

good faith estimate of closing costs

Disclosures to loan applicant

© 2012 Rockwell Publishing

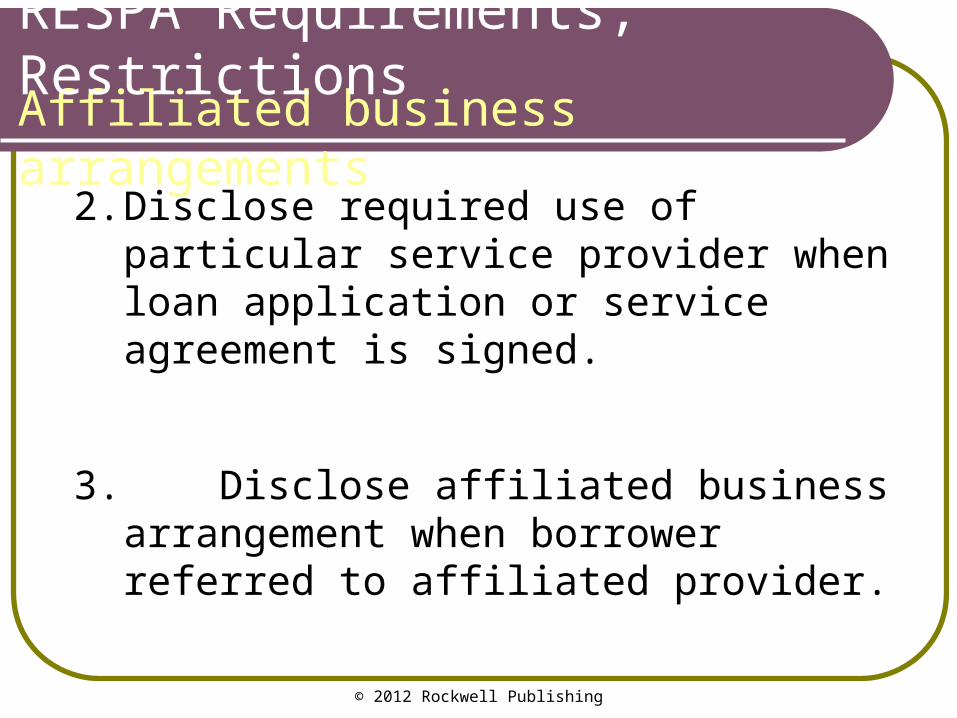

2. Disclose required use of particular service provider when loan application or service agreement is signed.

3. Disclose affiliated business arrangement when borrower referred to affiliated provider.

Affiliated business arrangementsRESPA Requirements, Restrictions

© 2012 Rockwell Publishing

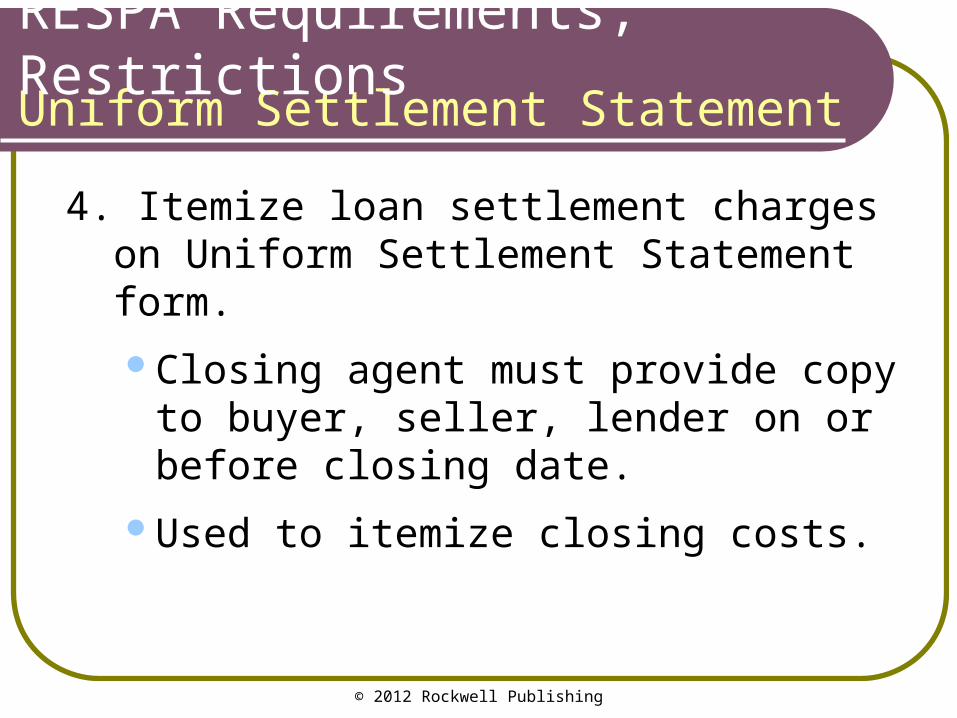

4. Itemize loan settlement charges on Uniform Settlement Statement form.

Closing agent must provide copy to buyer, seller, lender on or before closing date.

Used to itemize closing costs.

Uniform Settlement StatementRESPA Requirements, Restrictions

© 2012 Rockwell Publishing

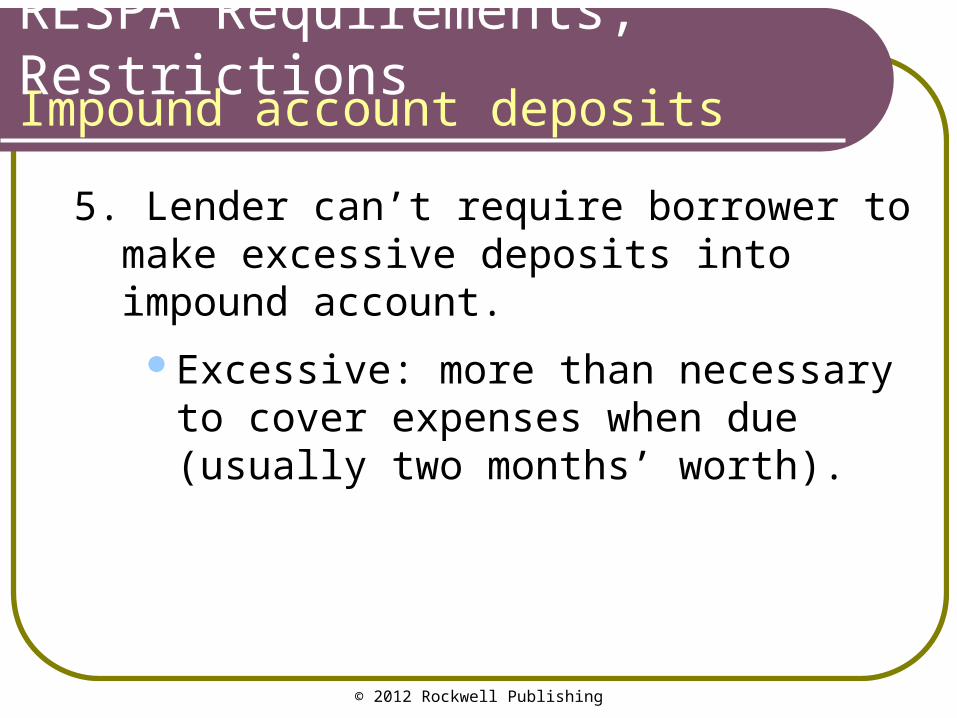

5. Lender can’t require borrower to make excessive deposits into impound account.

Excessive: more than necessary to cover expenses when due (usually two months’ worth).

Impound account depositsRESPA Requirements, Restrictions

© 2012 Rockwell Publishing

6. Lender or service provider may not:

give or receive kickbacks or referral fees

accept unearned fees

charge a document preparation fee for required disclosures (Uniform Settlement Statement, impound account statement, TILA disclosures)

Kickbacks and unearned feesRESPA Requirements, Restrictions

© 2012 Rockwell Publishing

7. Property seller may not require buyer to use particular title insurance company.

Choice of title companyRESPA Requirements, Restrictions

© 2012 Rockwell Publishing

As of 2010, lenders are required to use new:standardized form for good faith estimate

(GFE)version of Uniform Settlement Statement

RESPA rule changes in 2010RESPA Requirements, Restrictions

© 2012 Rockwell Publishing

New rules for lenders:give applicants GFE earlier in process to

facilitate comparison shoppingplace strict limits (“tolerances”) on cost

increases between time of GFE estimates and closing

explain costs/tradeoff of choices encourage “volume discounts”

RESPA rule changes in 2010RESPA Requirements, Restrictions

© 2012 Rockwell Publishing

SummaryRESPA

• Federally related loan transaction

• Settlement service provider

• Affiliated business arrangement

• Kickback or referral fee

• Unearned fee

• Good faith estimate (GFE)

• Uniform Settlement Statement

© 2012 Rockwell Publishing

Predatory Lending

Predatory lending: practices unscrupulous mortgage lenders and brokers use to take advantage of unsophisticated borrowers for profit. Includes:

Tactics that are always abusive.Lending practices and loan terms misused

for predatory purposes.

© 2012 Rockwell Publishing

Predatory Lending Practices

Predatory steering: steering buyer towards more expensive loan when buyer could qualify for less expensive loan.

Steering

© 2012 Rockwell Publishing

Predatory Lending Practices

Fee packing: charging interest rates, points, or processing fees that far exceed norm and aren’t justified by cost of services provided.

Includes charging for unnecessary products or features that increase cost of loan.

Fee packing

© 2012 Rockwell Publishing

Predatory Lending Practices

Equity stripping: foreclosure rescue scam; results in “stripping away” of homeowner’s equity by buying home and selling back to owner with less favorable pricing and/or terms.

Equity stripping

© 2012 Rockwell Publishing

Predatory Lending Practices

Loan flipping: encouraging home owner to refinance repeatedly over short period, when there’s no real benefit in doing so.

Loan flipping

© 2012 Rockwell Publishing

Predatory Lending Practices

Property flipping: purchasing property at discount, then quickly reselling for inflated price.

Illegal if real estate agent, appraiser, and/or lender fraudulently makes unsophisticated buyer believe property is worth more than it is.

Property flipping

© 2012 Rockwell Publishing

Predatory Lending Practices

Disregarding buyer’s capacity to pay: making loan based only on property’s value without considering borrower’s ability to afford payments.

Disregarding capacity to pay

© 2012 Rockwell Publishing

Predatory Lending Practices

Impound waivers: not requiring borrower to make monthly impound account deposits for property taxes and insurance.

Encourages buyers to borrow more.Increases risk of default on loan.

Impound waivers

© 2012 Rockwell Publishing

Predatory Lending Practices

Loan in excess of value: loaning borrower more than property’s actual value.

Usually involves fraudulent appraisal.

Loan in excess of value

© 2012 Rockwell Publishing

Predatory Lending Practices

Negative amortization schemes: deliberately making loan with payments that don’t cover interest.

Unpaid interest added to principal.

Negative amortization

© 2012 Rockwell Publishing

Predatory Lending Practices

Balloon payment abuses: making partially amortized or interest-only loan that has low monthly payments, without disclosing that large balloon payment is required after short period.

Balloon payments

© 2012 Rockwell Publishing

Predatory Lending Practices

Fraud: misrepresenting or concealing unfavorable loan terms or excessive fees, falsifying documents, or using other fraudulent means to induce borrower to enter loan agreement.

Fraud

© 2012 Rockwell Publishing

Predatory Lending Practices

High-pressure sales tactics: telling prospective borrowers that they must decide immediately, no other lender will loan them money, etc.

High-pressure tactics

© 2012 Rockwell Publishing

Predatory Lending Practices

Advance payments from loan proceeds: requiring some of borrower’s mortgage payments to be paid at closing, out of loan proceeds.

Advance loan payments

© 2012 Rockwell Publishing

Predatory Lending Practices

Excessive or unfair prepayment penalties: imposing unusually large penalty, failing to limit penalty period, and/or charging penalty even if loan is prepaid because property is being sold.

Prepayment penalties

© 2012 Rockwell Publishing

Predatory Lending Practices

Unfair default interest rate: increasing loan’s interest rate by excessive amount when borrower defaults.

Default interest rate

© 2012 Rockwell Publishing

Predatory Lending Practices

Discretionary call provision: including call provision (acceleration clause) that allows lender to accelerate loan at any time, not just because payments are delinquent or property is being sold.

Call provision

© 2012 Rockwell Publishing

Predatory Lending Practices

Single-premium credit life insurance: requiring borrowers to purchase policy with single large premium due at closing.

Credit life insurance

© 2012 Rockwell Publishing

Predatory Lending Practices

Predatory loan servicers may:charge improper late feesfail to credit paymentsinstitute foreclosure against borrowers

not in default

Loan servicing

© 2012 Rockwell Publishing

Predatory Lending

Targeted victims of predatory lending tend to be uninformed and/or in vulnerable circumstances:

elderlylimited educationlimited Englishlow incomein debtpoor credit historylive in redlined neighborhood

Targeted victims

© 2012 Rockwell Publishing

Predatory Lending

Laws designed to stop predatory lending practices:

federalstate

Predatory lending laws

© 2012 Rockwell Publishing

Predatory Lending Laws

Home Ownership and Equity Protection Act (HOEPA): provisions added to TILA in 1994.

Only applies to home equity and refinance loans that:

are classified as high-cost, and are secured by principal residence.

Doesn’t apply to purchase loans.

Federal law

© 2012 Rockwell Publishing

Federal Predatory Lending Law

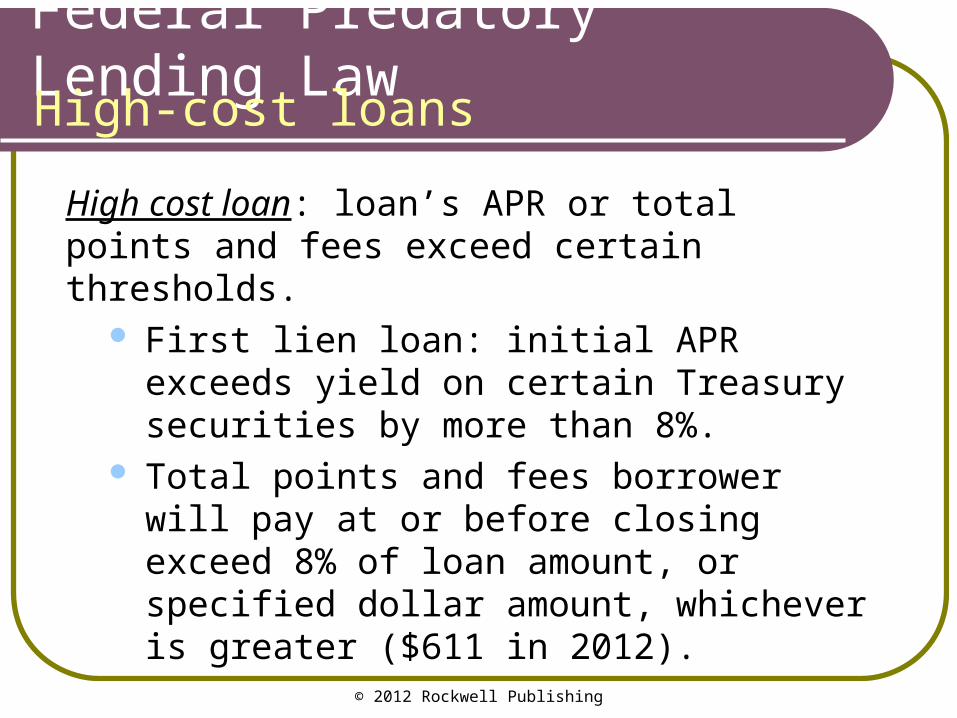

High cost loan: loan’s APR or total points and fees exceed certain thresholds.

First lien loan: initial APR exceeds yield on certain Treasury securities by more than 8%.

Total points and fees borrower will pay at or before closing exceed 8% of loan amount, or specified dollar amount, whichever is greater ($611 in 2012).

High-cost loans

© 2012 Rockwell Publishing

Federal Predatory Lending Law

2008: new provisions added to TILA and Regulation Z to provide consumers with greater protection against predatory lending.

Established new category: higher-priced loans.

Higher-priced loans

© 2012 Rockwell Publishing

Federal Predatory Lending Law

Higher-priced loan category:purchase loans as well as home equity

and refinance loanslower cost thresholds

Higher-priced loans

© 2012 Rockwell Publishing

Federal Predatory Lending Law

Recent consumer protection requirements for higher-priced and high-cost loans.

Lender can’t make loan without considering borrower’s ability to repay.

For high-cost (HOEPA) loans: no prepayment penalty allowed.

For higher-priced loans: no prepayment penalty after first two years or if loan has variable payments during first four years.

Higher-priced and high-cost loans

© 2012 Rockwell Publishing

Federal Predatory Lending Law

Since April, 2010, lenders required to: establish escrow (impound) account for

first-lien loans require borrower to make deposits for

property taxes and insurance

Higher-priced and high-cost loans

© 2012 Rockwell Publishing

Federal Predatory Lending Law

HOEPA’s high-cost loans continue to be subject to several existing rules.

Loan term less than 5 years: loan can’t be structured so that balloon payment necessary.

Negative amortization isn’t allowed.Interest rate can’t be raised after default.

High-cost-only rules

© 2012 Rockwell Publishing

State Predatory Lending Laws

Coverage and provisions of state laws vary.Some apply only to home equity and

refinance loans.Others also apply to purchase loans.

Coverage

© 2012 Rockwell Publishing

State Predatory Lending Laws

State laws address recent concern: need for consumer protection during loan modification process (after borrower defaults or is about to default on home loan).

Protection for distressed borrowers

© 2012 Rockwell Publishing

SummaryPredatory Lending

• Steering• Fee packing• Equity stripping• Loan flipping• Property flipping• HOEPA• High-cost loan• Higher-priced loan