Embed Size (px)

Citation preview

© 2012 Pearson Prentice Hall. All rights reserved.

Customer Profitability Analysisand Sales-Variance Analysis

© 2012 Pearson Prentice Hall. All rights reserved.

Customer Revenues and Customer Costs

Customer-profitability analysis is the reporting and analysis of revenues earned from customers and costs incurred to earn those revenues.

An analysis of customer differences in revenues and costs can provide insight into why differences exist in the operating income earned from different customers.

© 2012 Pearson Prentice Hall. All rights reserved.

Customer RevenuesPrice discounting is the reduction of selling prices

to encourage increases in customer purchases.Lower sales price is a trade-off for larger sales

volumes.Discounts should be tracked by customer and

salesperson.

© 2012 Pearson Prentice Hall. All rights reserved.

Customer Cost AnalysisCustomer cost hierarchy categorizes costs

related to customers into different cost pools on the basis of different: Types of drivers Cost-allocation bases Degrees of difficulty in determining cause-and-

effect or benefits-received relationships

© 2012 Pearson Prentice Hall. All rights reserved.

Customer Cost Hierarchy Example1. Customer output unit-level costs2. Customer batch-level costs3. Customer-sustaining costs4. Distribution-channel costs5. Corporate-sustaining costs

© 2012 Pearson Prentice Hall. All rights reserved.

Other Factors in Evaluating Customer Profitability

Likelihood of customer retentionPotential for sales growthLong-run customer profitabilityIncreases in overall demand from having

well-known customersAbility to learn from customers

© 2012 Pearson Prentice Hall. All rights reserved.

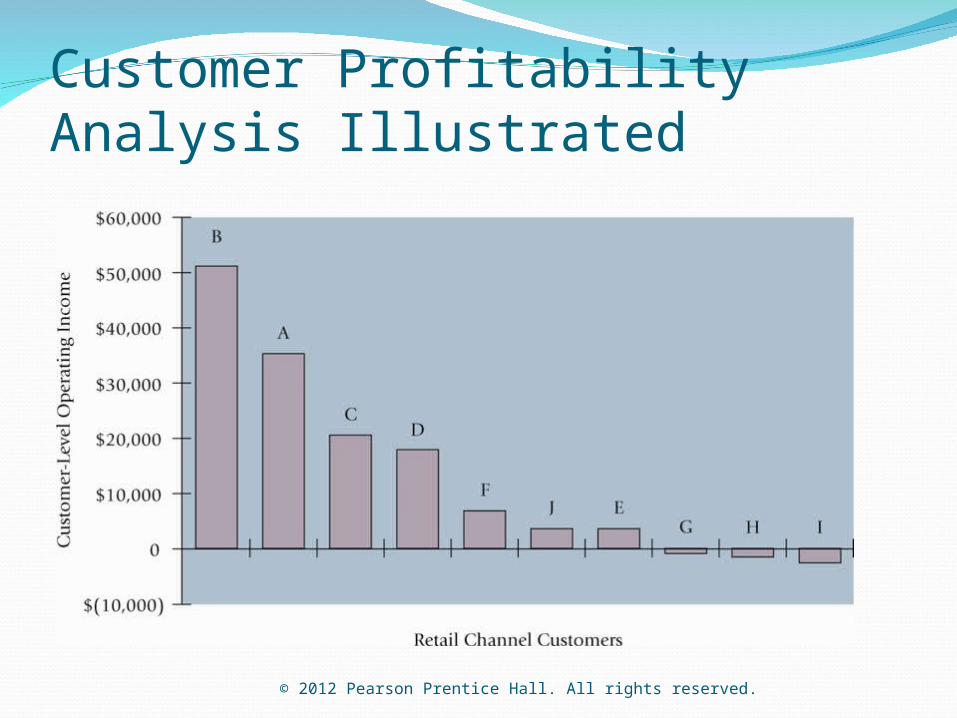

Customer Profitability Analysis Illustrated

© 2012 Pearson Prentice Hall. All rights reserved.

Customer Profitability Analysis Illustrated

© 2012 Pearson Prentice Hall. All rights reserved.

Customer Profitability Analysis Illustrated

© 2012 Pearson Prentice Hall. All rights reserved.

Customer Profitability Analysis Illustrated

© 2012 Pearson Prentice Hall. All rights reserved.

Sales VariancesLevel 1: Static-budget variance—the

difference between an actual result and the static-budgeted amount

Level 2: Flexible-budget variance—the difference between an actual result and the flexible-budgeted amount

Level 2: Sales-volume varianceLevel 3: Sales-quantity varianceLevel 3: Sales-mix variance

(c) 2012 Pearson Prentice Hall. All rights reserved.

Sales-Mix VarianceMeasures shifts between selling more or

less of higher or lower profitable products

Budgeted Sales-Mix

Percentage

Actual Sales-Mix Percentage

XBudgeted

Contribution Margin per Unit

Sales-Mix Variance =

Actual Units of

All Products

Sold

X

© 2012 Pearson Prentice Hall. All rights reserved.

Sales-Quantity Variance

Budgeted Units of all

Products Sold

Actual Units of All Products Sold

Budgeted Contribution

Margin per Unit

Sales-Quantity Variance

=

Budgeted Sales-Mix

PercentageX X

© 2012 Pearson Prentice Hall. All rights reserved.

Flexible-Budget and Sales-Volume Variances Illustrated

© 2012 Pearson Prentice Hall. All rights reserved.

Sales-Mix and Sales–Quantity Variances Illustrated

© 2012 Pearson Prentice Hall. All rights reserved.

Sales Variances Summarized

© 2012 Pearson Prentice Hall. All rights reserved.