Embed Size (px)

Citation preview

© 2004 Pearson Addison-Wesley. All rights reserved 1-1

ECON 304Money and Banking

Instructor: Bernard Malamud

–Office: BEH 502

Phone (702) 895 –3294

Fax: 895 – 1354

»Email: [email protected]

Website: www.unlv.edu/faculty/bmalamud

Office hours: M 2:30 – 4:30 pm; W 3:30 – 5:30 pm

And by appointment

© 2004 Pearson Addison-Wesley. All rights reserved 1-2

Money,Banking, and Financial Markets

Why Study Financial Markets?

1. Channel funds from savers to investors, thereby promoting economic efficiency

2. Affect personal wealth and behavior of business firms

Why Study Banking and Financial Institutions?

1. Financial Intermediation

Helps get funds from savers to investors

2. Banks and Money Supply

Crucial role in creation of money

3. Financial Innovation

Why Study Money and Monetary Policy?

1. Influence on business cycles, inflation, and interest rates

© 2004 Pearson Addison-Wesley. All rights reserved 1-3

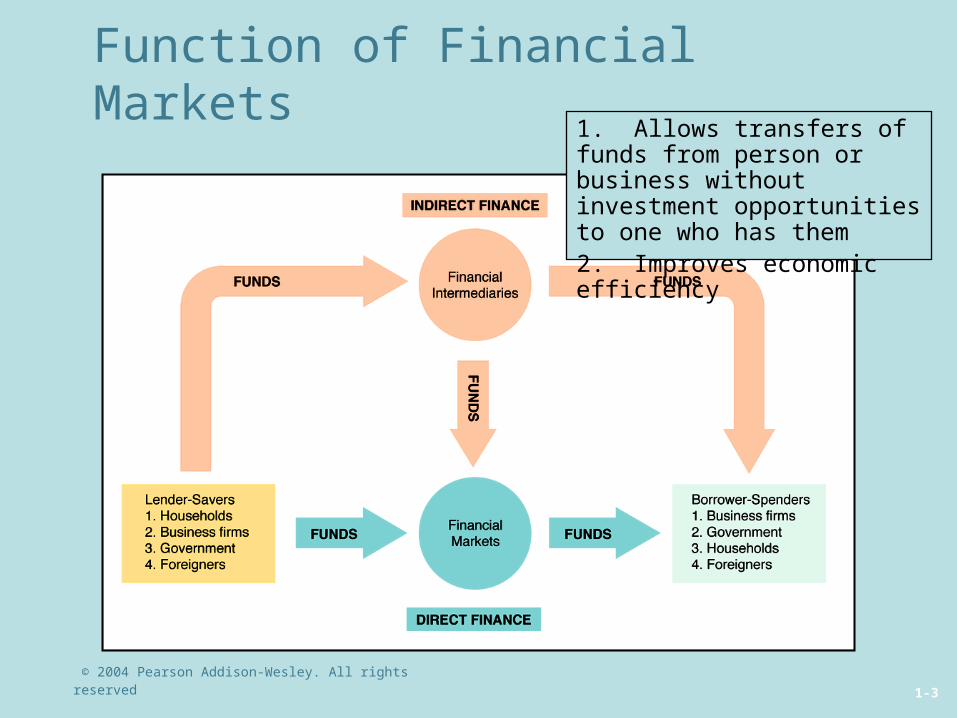

Function of Financial Markets1. Allows transfers of funds from person or business without investment opportunities to one who has them2. Improves economic efficiency

© 2004 Pearson Addison-Wesley. All rights reserved 1-4

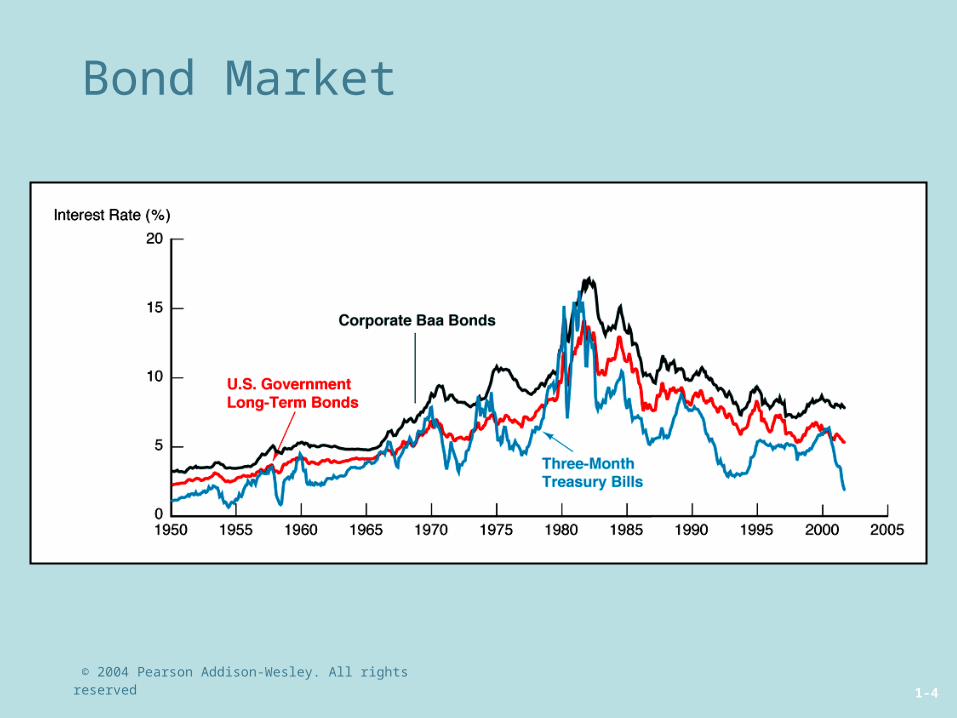

Bond Market

© 2004 Pearson Addison-Wesley. All rights reserved 1-5

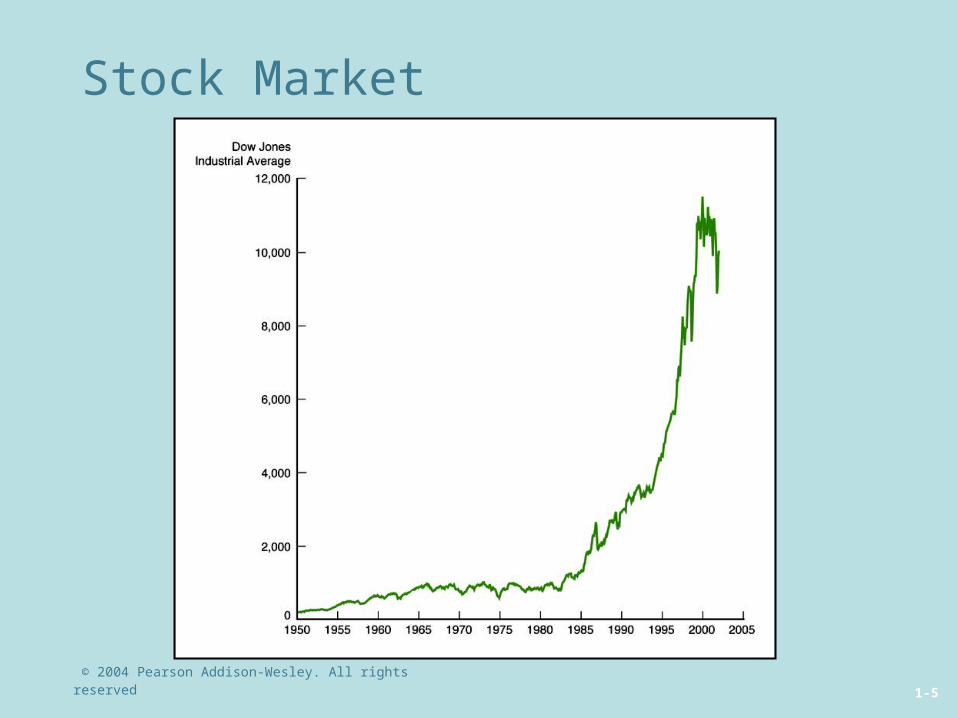

Stock Market

© 2004 Pearson Addison-Wesley. All rights reserved 1-6

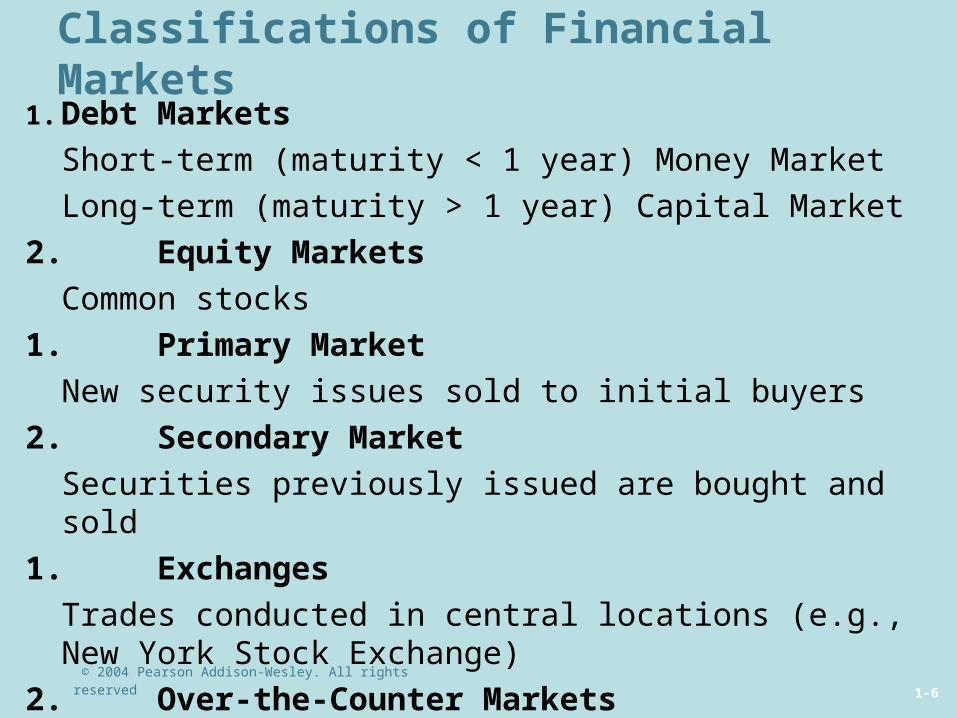

Classifications of Financial Markets1. Debt Markets

Short-term (maturity < 1 year) Money Market

Long-term (maturity > 1 year) Capital Market

2. Equity Markets

Common stocks

1. Primary Market

New security issues sold to initial buyers

2. Secondary Market

Securities previously issued are bought and sold

1. Exchanges

Trades conducted in central locations (e.g., New York Stock Exchange)

2. Over-the-Counter Markets

Dealers at different locations buy and sell

© 2004 Pearson Addison-Wesley. All rights reserved 1-7

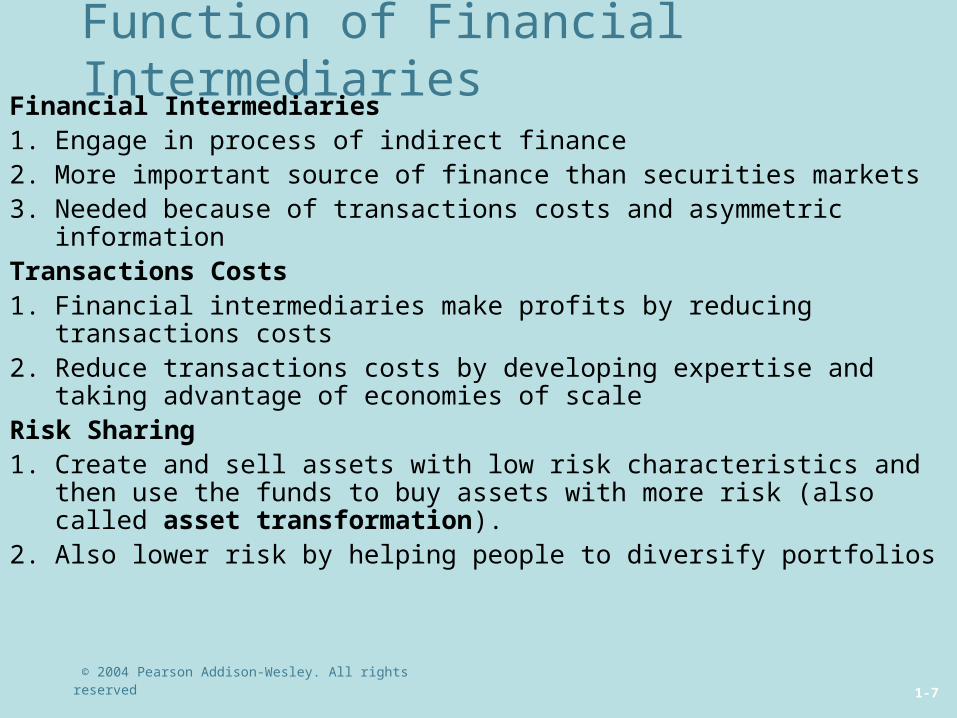

Function of Financial IntermediariesFinancial Intermediaries1. Engage in process of indirect finance2. More important source of finance than securities markets3. Needed because of transactions costs and asymmetric informationTransactions Costs1. Financial intermediaries make profits by reducing transactions costs2. Reduce transactions costs by developing expertise and taking

advantage of economies of scaleRisk Sharing1. Create and sell assets with low risk characteristics and then use the

funds to buy assets with more risk (also called asset transformation).2. Also lower risk by helping people to diversify portfolios

© 2004 Pearson Addison-Wesley. All rights reserved 1-8

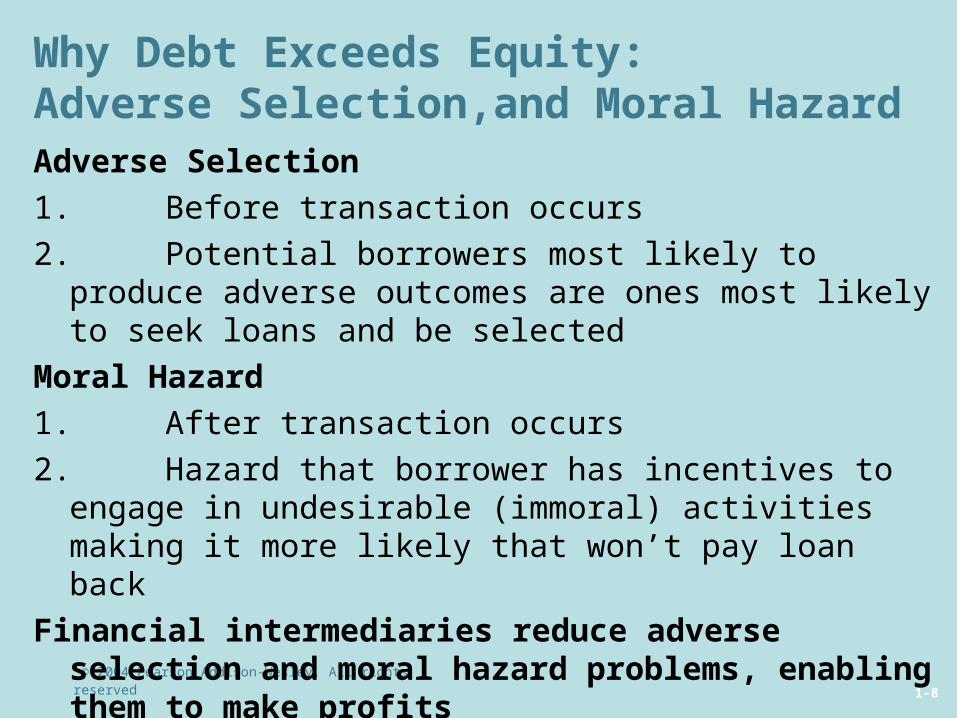

Why Debt Exceeds Equity:Adverse Selection,and Moral HazardAdverse Selection

1. Before transaction occurs

2. Potential borrowers most likely to produce adverse outcomes are ones most likely to seek loans and be selected

Moral Hazard

1. After transaction occurs

2. Hazard that borrower has incentives to engage in undesirable (immoral) activities making it more likely that won’t pay loan back

Financial intermediaries reduce adverse selection and moral hazard problems, enabling them to make profits

© 2004 Pearson Addison-Wesley. All rights reserved 1-9

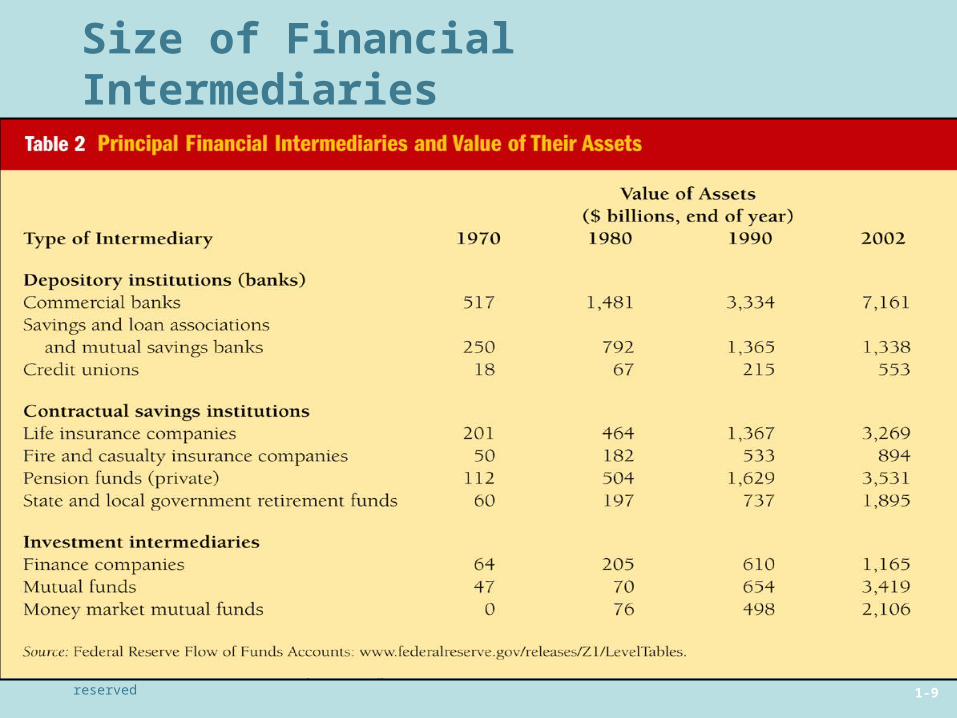

Size of Financial Intermediaries

© 2004 Pearson Addison-Wesley. All rights reserved 1-10

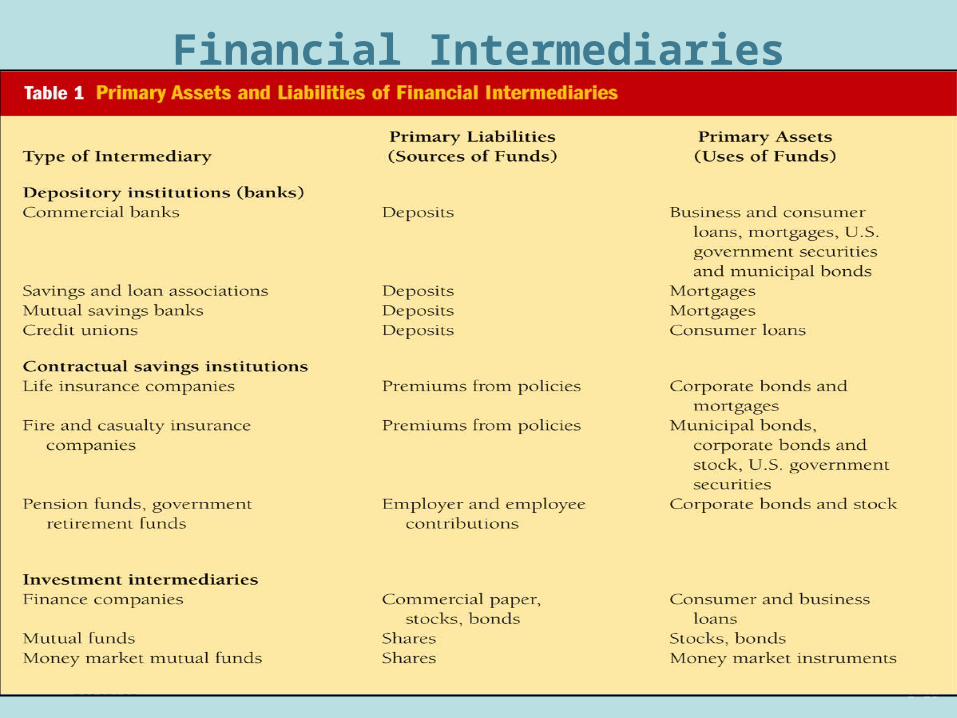

Financial Intermediaries

© 2004 Pearson Addison-Wesley. All rights reserved 1-11

Regulation of Financial Markets and Intermediaries

1. Increase information to investors

A. Decreases adverse selection and moral hazard problems

B. SEC forces corporations to disclose information

2. Ensuring the soundness of financial intermediaries

A. Prevents financial panics

B. Chartering, reporting requirements, restrictions on assets and activities, deposit insurance, and anti-competitive measures

But, the trend …

… financial innovation and deregulation

© 2004 Pearson Addison-Wesley. All rights reserved 1-12

Money: What and WhyEconomist’s Meaning of Money1. Anything that is generally accepted in payment for goods and services2. Not the same as wealth or income

Functions of Money1. Medium of exchange2. Unit of account3. Store of value

Evolution of Payments System1. Precious metals like gold and silver2. Paper currency (fiat money)3. Checks4. Electronic means of payment5. Electronic money: Debit cards, Stored-value cards, Smart cards, E-

cash

© 2004 Pearson Addison-Wesley. All rights reserved 1-13

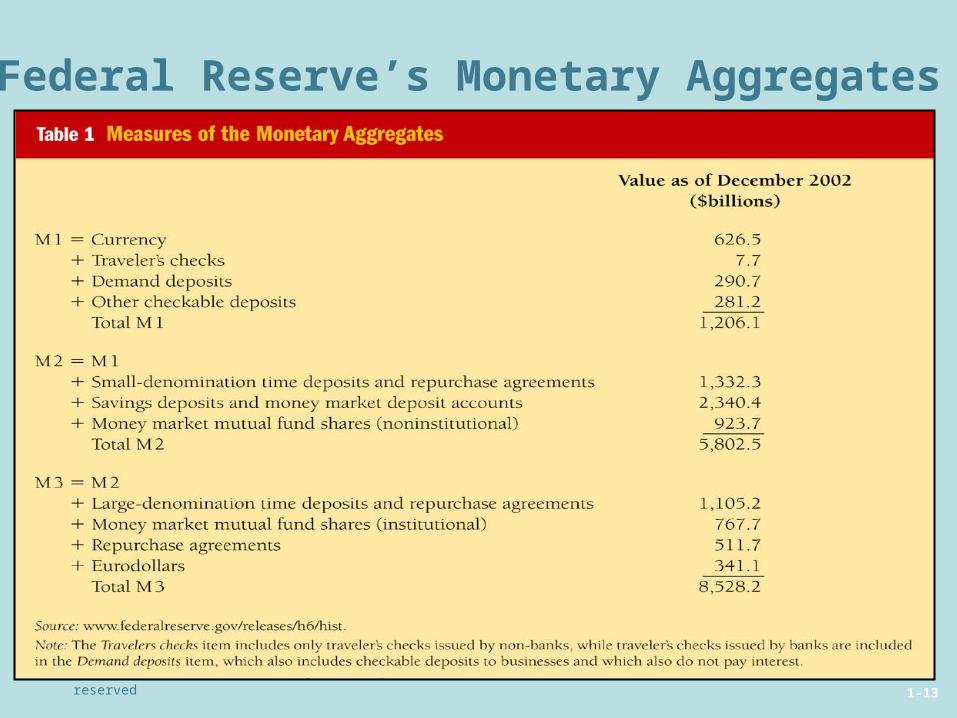

Federal Reserve’s Monetary Aggregates

© 2004 Pearson Addison-Wesley. All rights reserved 1-14

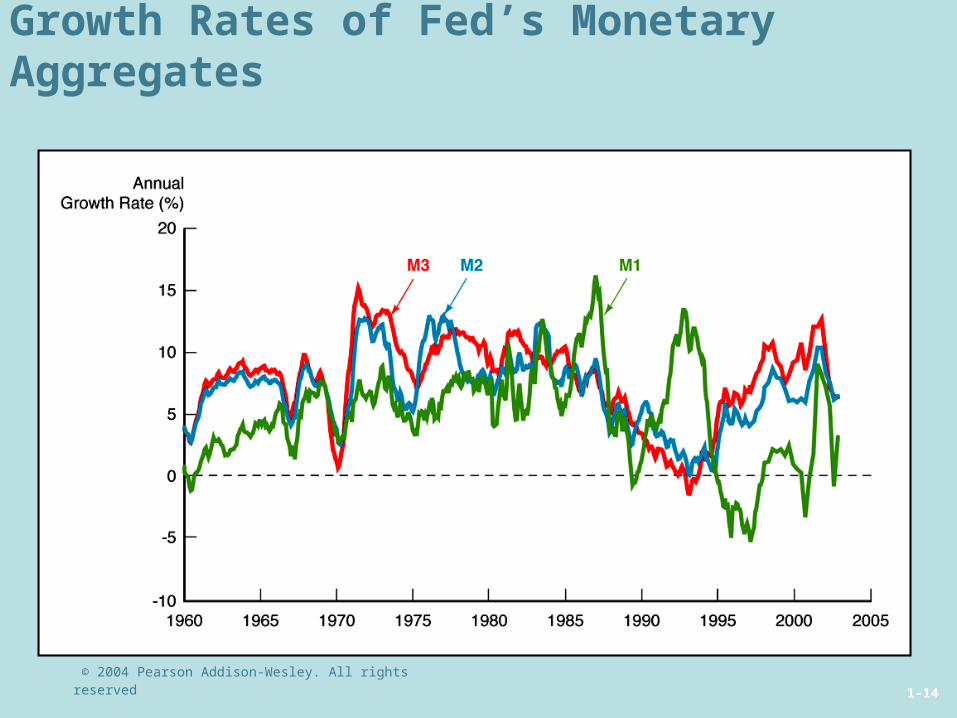

Growth Rates of Fed’s Monetary Aggregates

© 2004 Pearson Addison-Wesley. All rights reserved 1-15

© 2004 Pearson Addison-Wesley. All rights reserved 1-16

© 2004 Pearson Addison-Wesley. All rights reserved 1-17

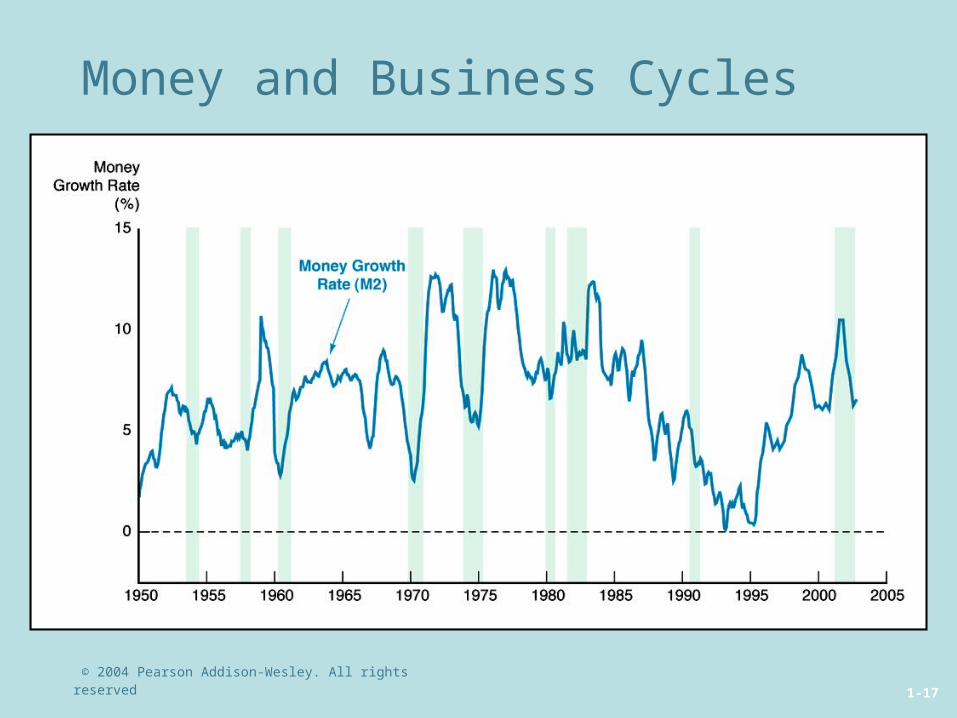

Money and Business Cycles

© 2004 Pearson Addison-Wesley. All rights reserved 1-18

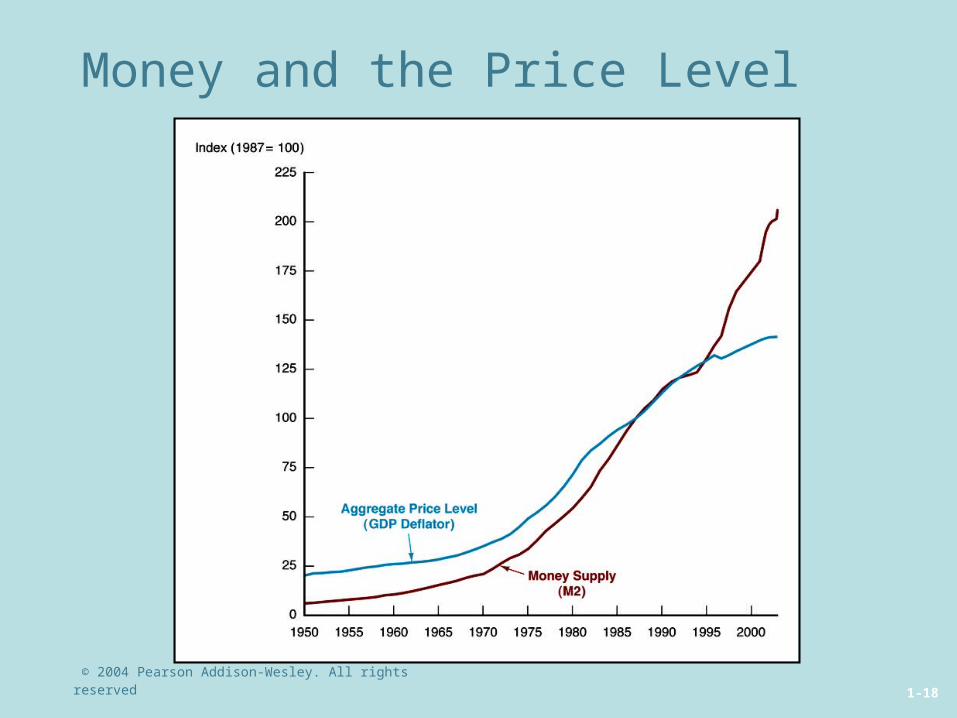

Money and the Price Level

© 2004 Pearson Addison-Wesley. All rights reserved 1-19

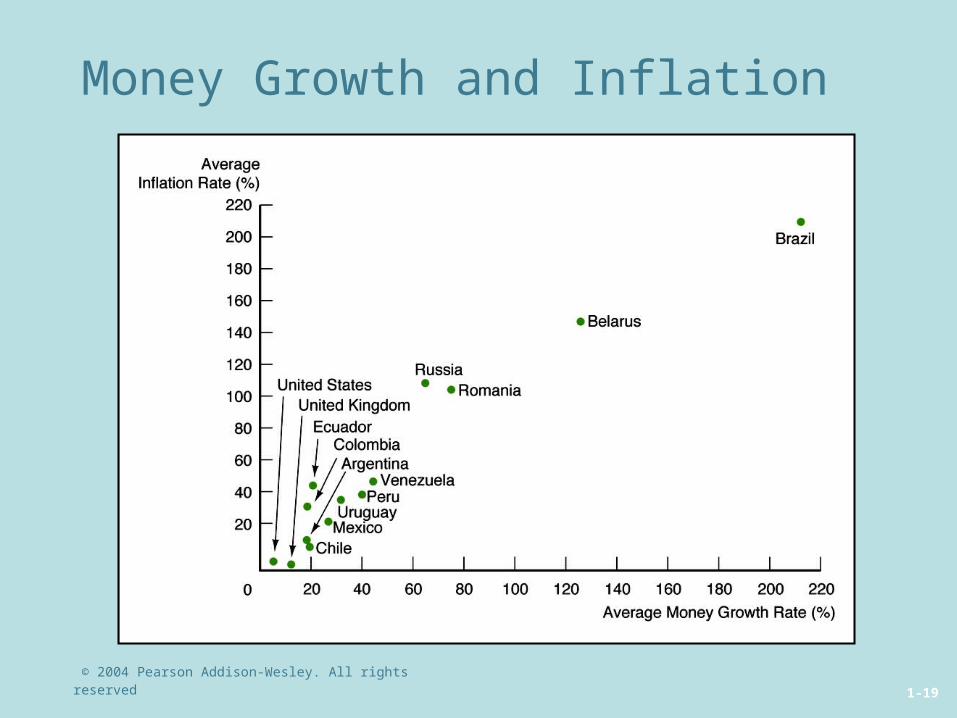

Money Growth and Inflation

© 2004 Pearson Addison-Wesley. All rights reserved 1-20

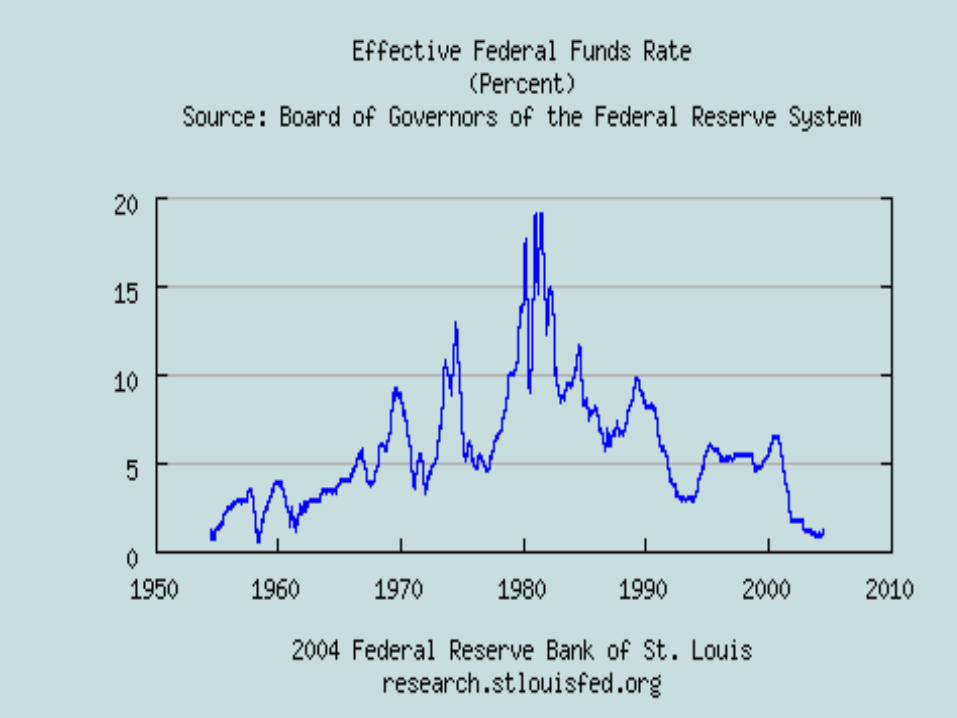

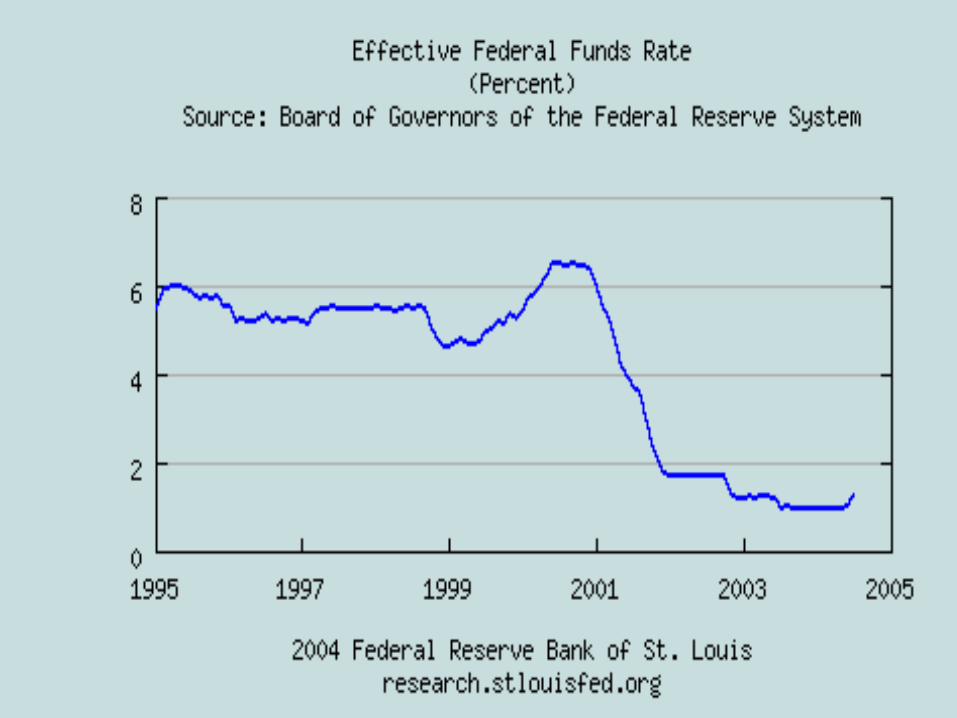

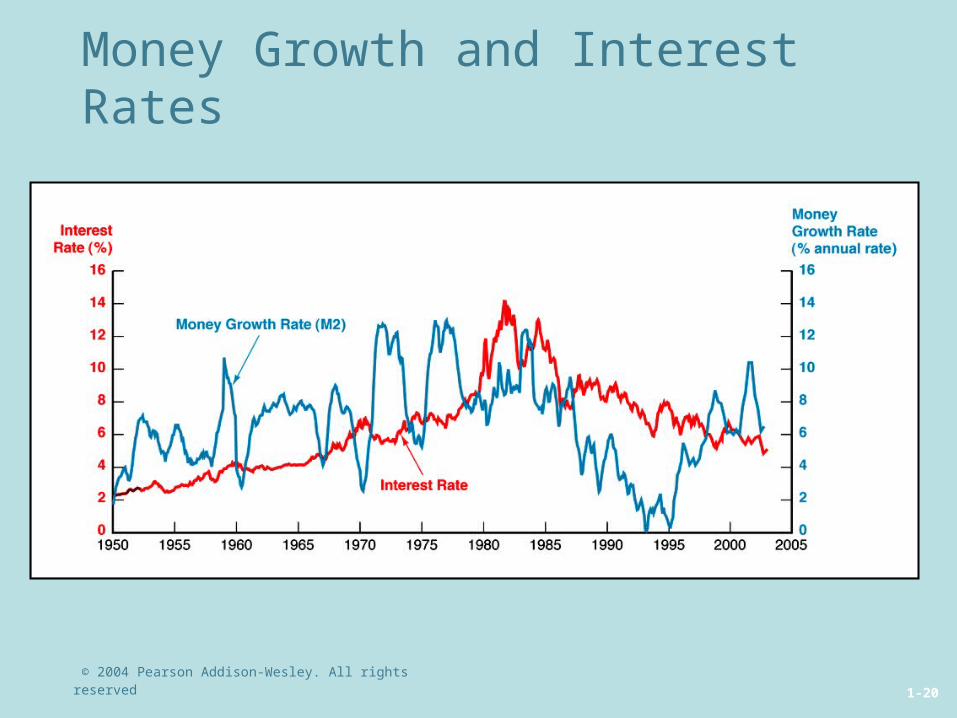

Money Growth and Interest Rates

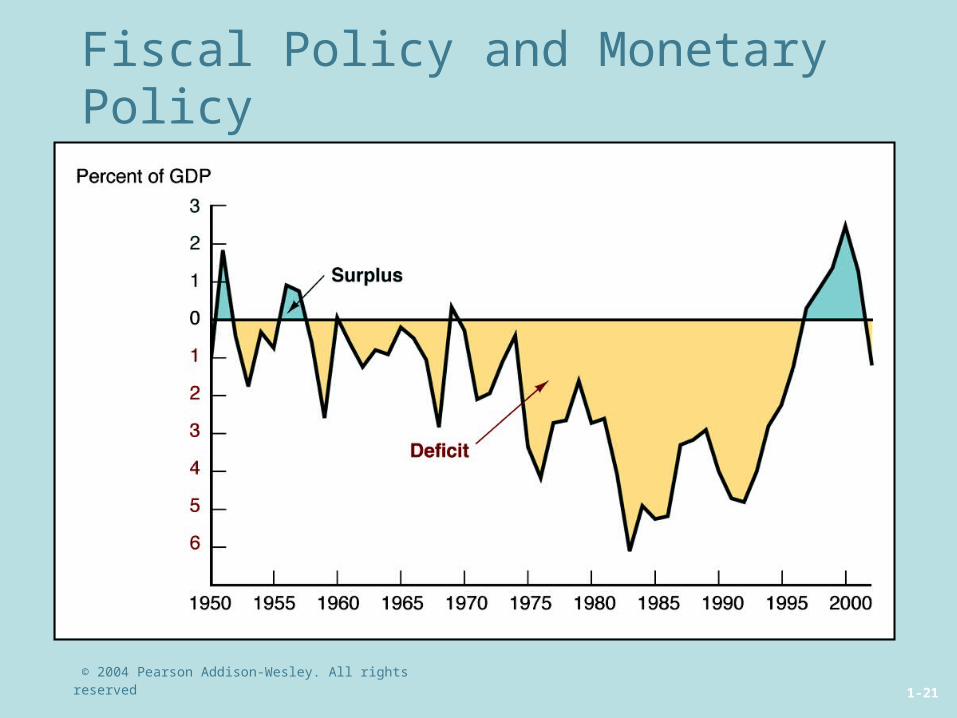

© 2004 Pearson Addison-Wesley. All rights reserved 1-21

Fiscal Policy and Monetary Policy