Embed Size (px)

Citation preview

© 2003 McGraw-Hill Ryerson Limited.

Money, Banking and Money, Banking and the Financial Sectorthe Financial Sector

13 - 2

© 2003 McGraw-Hill Ryerson Limited.

IntroductionIntroduction

Real goods and services are exchanged in the real sector of the economy.

For every real transaction, there is a financial transaction that mirrors it.

13 - 3

© 2003 McGraw-Hill Ryerson Limited.

IntroductionIntroduction

The financial sector is central to almost all macroeconomic debates because behind every real transaction, there is a financial transaction that mirrors it.

13 - 4

© 2003 McGraw-Hill Ryerson Limited.

IntroductionIntroduction

All trade in the goods market involves both the real sector and the financial sector.

13 - 5

© 2003 McGraw-Hill Ryerson Limited.

Why Is the Financial Why Is the Financial Sector So Important to Sector So Important to Macro?Macro? The financial sector is important to

macroeconomics because of its role in channeling savings back into the circular flow.

13 - 6

© 2003 McGraw-Hill Ryerson Limited.

Why Is the Financial Why Is the Financial Sector So Important to Sector So Important to Macro?Macro? Savings are returned to the circular flow

in the form of consumer loans, business loans, and loans to government.

13 - 7

© 2003 McGraw-Hill Ryerson Limited.

Why Is the Financial Why Is the Financial Sector So Important to Sector So Important to Macro?Macro? Savings are channeled into the financial

sector when individuals buy financial assets such as stocks or bonds and back into the spending stream as investment.

For every financial asset there is a corresponding financial liability.

13 - 8

© 2003 McGraw-Hill Ryerson Limited.

Why Is the Financial Why Is the Financial Sector So Important to Sector So Important to Macro?Macro?

Financial assets such as stocks and bonds, are obligations or financial liabilities of the issuer.

13 - 9

© 2003 McGraw-Hill Ryerson Limited.

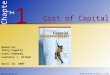

LoansSaving

Gov’t

House-holds

Corpor-ations

Pension fundsCDsSavings

depositsChequing

depositsStocksBondsGovernment

SecuritiesLife insurance

Outflowfrom

spendingstream

The Financial Sector as The Financial Sector as a Conduit for Savings, a Conduit for Savings, Fig. 13-1, p 307Fig. 13-1, p 307

Large business loans

Small business loans

Venture capital loans

Construction loans

Investment loans

Gov’t

House-holds

Corpor-ations

Inflowfrom

spendingstream

Financial sector

13 - 10

© 2003 McGraw-Hill Ryerson Limited.

The Role of Interest The Role of Interest Rates in the Financial Rates in the Financial SectorSector While price is the mechanism that

balances supply and demand in the real sector, interest rates do the same in the financial sector.

13 - 11

© 2003 McGraw-Hill Ryerson Limited.

The Role of Interest The Role of Interest Rates in the Financial Rates in the Financial SectorSector The interest rate is the price paid for

use of a financial asset. Bonds are promises to pay a certain

amount plus interest in the future.

13 - 12

© 2003 McGraw-Hill Ryerson Limited.

The Role of Interest The Role of Interest Rates in the Financial Rates in the Financial SectorSector When financial assets such as bond

make fixed interest payments, the price of the financial asset is determined by the market interest rate.

13 - 13

© 2003 McGraw-Hill Ryerson Limited.

The Role of Interest The Role of Interest Rates in the Financial Rates in the Financial SectorSector When interest rates rise, the value of

the flow of payments from fixed-interest-rate bonds goes down because more can be earned on new bonds that pay the new, higher interest.

13 - 14

© 2003 McGraw-Hill Ryerson Limited.

The Role of Interest The Role of Interest Rates in the Financial Rates in the Financial SectorSector As the market interest rates go up, price

of the bond goes down. As the market interest rates go down,

the price of the bond goes up.

13 - 15

© 2003 McGraw-Hill Ryerson Limited.

The Definition and The Definition and Functions of MoneyFunctions of Money Money is a highly liquid financial asset.

To be liquid means to be easily changeable into another asset or good.

Social customs and standard practices are central to the liquidity of money.

13 - 16

© 2003 McGraw-Hill Ryerson Limited.

The Definition and The Definition and Functions of MoneyFunctions of Money Money is generally accepted in

exchange for other goods. Money is used as a reference in valuing

other goods. Money can be stored as wealth.

13 - 17

© 2003 McGraw-Hill Ryerson Limited.

The Canadian Central The Canadian Central Bank: Bank of CanadaBank: Bank of Canada Bank of Canada – The Canadian

central bank whose liabilities (bank notes) serve as cash in Canada.

13 - 18

© 2003 McGraw-Hill Ryerson Limited.

Bank of CanadaBank of Canada

A bank is a financial institution whose primary function is holding money for, and lending money to, individuals and firms.

Individuals’ deposits in savings and chequing accounts serve the same function as does currency and are also considered money.

13 - 19

© 2003 McGraw-Hill Ryerson Limited.

Functions of MoneyFunctions of Money

Money is a medium of exchange. Money is a unit of account. Money is a store of wealth.

13 - 20

© 2003 McGraw-Hill Ryerson Limited.

Money As a Medium of Money As a Medium of ExchangeExchange Without money, we would have to

barter—a direct exchange of goods and services.

Money facilitates exchange by reducing the cost of trading.

13 - 21

© 2003 McGraw-Hill Ryerson Limited.

Money As a Medium of Money As a Medium of ExchangeExchange Money does not have to have any

inherent value to function as a medium of exchange.

All that is necessary is that everyone believes that other people will exchange it for their goods.

13 - 22

© 2003 McGraw-Hill Ryerson Limited.

Money As a Medium of Money As a Medium of ExchangeExchange The Bank of Canada’s job is to not

issue too much or too little money.

If there is too much money, compared to the goods and services at existing prices, the goods and services will sell out, or the prices will rise.

13 - 23

© 2003 McGraw-Hill Ryerson Limited.

Money As a Medium of Money As a Medium of ExchangeExchange If there is too little money, compared to

the goods and services at existing prices, there will be a shortage of money and people will have to resort to barter, or prices will fall.

13 - 24

© 2003 McGraw-Hill Ryerson Limited.

Money As a Unit of Money As a Unit of AccountAccount Money prices are actually relative

prices. A single unit of account saves our

limited memories and helps us make reasonable decisions based on relative costs.

13 - 25

© 2003 McGraw-Hill Ryerson Limited.

Money As a Unit of Money As a Unit of AccountAccount Money is a useful unit of account only

as long as its value relative to other prices does not change too quickly.

In a hyperinflation, all prices rise so much that our frame of reference is lost and money loses its usefulness as a unit of account.

13 - 26

© 2003 McGraw-Hill Ryerson Limited.

Money as a Store of Money as a Store of WealthWealth Money is a financial asset. It is simply a government bond that

pays no interest.

13 - 27

© 2003 McGraw-Hill Ryerson Limited.

Money as a Store of Money as a Store of WealthWealth As long as money is serving as a

medium of exchange, it automatically also serves as a store of wealth.

13 - 28

© 2003 McGraw-Hill Ryerson Limited.

Money as a Store of Money as a Store of WealthWealth Money’s usefulness as a store of wealth

also depends upon how well it maintains its value.

Hyperinflations destroy money’s usefulness as a store of value.

13 - 29

© 2003 McGraw-Hill Ryerson Limited.

Money as a Store of Money as a Store of WealthWealth Our ability to spend money for goods

makes it worthwhile to hold money even though it does not pay interest.

13 - 30

© 2003 McGraw-Hill Ryerson Limited.

Alternative Measures of Alternative Measures of MoneyMoney Since it is difficult to define money

unambiguously, economists have defined different measures of money.

They are called M1, M2 and M3, M1+, M2+ and M2++.

13 - 31

© 2003 McGraw-Hill Ryerson Limited.

Alternative Measures of Alternative Measures of Money: M1Money: M1 M1 consists of currency in circulation

and chequing account balances at chartered banks.

Chequing account deposits are included in all definitions of money.

13 - 32

© 2003 McGraw-Hill Ryerson Limited.

Alternative Measures of Alternative Measures of Money: M2Money: M2 M2 is made up of M1 plus personal

savings deposits, and non personal notice deposits (that can be withdrawn only after prior notice) held at chartered banks.

Time deposits are also called certificates of deposit (CDs), or term deposits.

13 - 33

© 2003 McGraw-Hill Ryerson Limited.

Alternative Measures of Alternative Measures of Money: M2Money: M2 The money in savings accounts is

counted as money because it is readily available.

13 - 34

© 2003 McGraw-Hill Ryerson Limited.

Alternative Measures of Alternative Measures of Money: M2Money: M2 All M2 components are highly liquid and

play an important role in providing reserves and lending capacity for chartered banks.

13 - 35

© 2003 McGraw-Hill Ryerson Limited.

Alternative Measures of Alternative Measures of Money: M2Money: M2 The M2 definition is important because

economic research has shown that the M2 definition often most closely correlates with the price level and economic activity.

13 - 36

© 2003 McGraw-Hill Ryerson Limited.

Beyond M2: “The Beyond M2: “The Pluses”Pluses” Numerous financial assets also have

some attributes of money. That is why they are included in some measures of money.

There are measures for M3, M1+, M2+ and beyond.

13 - 37

© 2003 McGraw-Hill Ryerson Limited.

Beyond M2: “The Beyond M2: “The Pluses”Pluses” The broadest measure is M2++. It includes almost all assets that can be

turned into cash on short notice. Broader concepts of asset liquidity have

gained greater appeal than the measures of money, because money measures have been rapidly changing.

13 - 38

© 2003 McGraw-Hill Ryerson Limited.

Beyond M2: “The Beyond M2: “The Pluses”Pluses” M1, M2 and M3 measures only include

deposits held at chartered banks. Measures containing a “+” also include

deposits at other financial institutions (near banks).

13 - 39

© 2003 McGraw-Hill Ryerson Limited.

Distinguishing Between Distinguishing Between Money and CreditMoney and Credit Credit card balances cannot be money

since they are assets of a bank. In a sense, they are the opposite of

money.

13 - 40

© 2003 McGraw-Hill Ryerson Limited.

Distinguishing Between Distinguishing Between Money and CreditMoney and Credit Credit cards are prearranged loans. Credit cards affect the amount of money

people hold. Generally, credit card holders carry less

cash.

13 - 41

© 2003 McGraw-Hill Ryerson Limited.

Banks and the Creation Banks and the Creation of Moneyof Money Banks are both borrowers and lenders.

Banks take in deposits and use the money they borrow to make loans to others.

Banks make a profit by charging a higher interest on the money they lend out than they pay for the money they borrow.

13 - 42

© 2003 McGraw-Hill Ryerson Limited.

Banks and the Creation Banks and the Creation of Moneyof Money Banks can be analyzed from the

perspective of asset management and liability management.

13 - 43

© 2003 McGraw-Hill Ryerson Limited.

Banks and the Creation Banks and the Creation of Moneyof Money Asset management is how a bank

handles its loans and other assets. Liability management how a bank

attracts deposits and how it pays for them.

13 - 44

© 2003 McGraw-Hill Ryerson Limited.

How Banks Create How Banks Create MoneyMoney Banks create money because a bank’s

liabilities are defined as money. When a bank incurs liabilities it creates

money. When a bank places the proceeds of a

loan it makes to you in your chequing account, it is creating money.

13 - 45

© 2003 McGraw-Hill Ryerson Limited.

The First Step in the The First Step in the Creation of MoneyCreation of Money The Bank of Canada creates money by

simply printing currency and exchanging it for bonds.

Currency is a financial asset to the bearer and a liability to the Bank of Canada.

13 - 46

© 2003 McGraw-Hill Ryerson Limited.

The Second Step in the The Second Step in the Creation of MoneyCreation of Money The bearer deposits the currency in a

chequing account at the bank. The bank holds your money and keeps

track of it until you write a cheque.

13 - 47

© 2003 McGraw-Hill Ryerson Limited.

Banking and Banking and GoldsmithsGoldsmiths In the past, gold was used as payment

for goods and services. But gold is heavy and the likelihood of

being robbed was great.

13 - 48

© 2003 McGraw-Hill Ryerson Limited.

From Gold to Gold From Gold to Gold ReceiptsReceipts It was safer to leave gold with a

goldsmith who gave you a receipt. The receipt could be exchanged for gold

whenever you needed gold.

13 - 49

© 2003 McGraw-Hill Ryerson Limited.

From Gold to Gold From Gold to Gold ReceiptsReceipts People soon began using the receipts

as money since they knew the receipts were backed 100 percent by gold.

At this point, there were two forms of money – gold and gold receipts.

13 - 50

© 2003 McGraw-Hill Ryerson Limited.

The Third Step in the The Third Step in the Creation of MoneyCreation of Money Little gold was redeemed, so the

goldsmith began making loans by issuing more receipts than he had gold.

He charged interest on the newly created gold receipts.

13 - 51

© 2003 McGraw-Hill Ryerson Limited.

The Third Step in the The Third Step in the Creation of MoneyCreation of Money When the goldsmith began making

loans by issuing more receipts than he had in gold, he created money.

13 - 52

© 2003 McGraw-Hill Ryerson Limited.

The Third Step in the The Third Step in the Creation of MoneyCreation of Money The gold receipts were backed partly by

gold and partly by people’s trust that the goldsmith would pay off in gold on demand.

13 - 53

© 2003 McGraw-Hill Ryerson Limited.

The Third Step in the The Third Step in the Creation of MoneyCreation of Money The goldsmith soon realized that he

could make more money in interest than he could earn in goldsmithing.

The goldsmith had become a banker.

13 - 54

© 2003 McGraw-Hill Ryerson Limited.

Banking Is ProfitableBanking Is Profitable

As the goldsmiths became wealthy, others started competing in offering to hold gold for free, or even offering to pay for the privilege of holding the public’s gold.

13 - 55

© 2003 McGraw-Hill Ryerson Limited.

Banking Is ProfitableBanking Is Profitable

That is why most banks today are willing to hold the public’s money at no charge – they can lend it out and in the process, make profits.