Embed Size (px)

Citation preview

© 2003 McGraw-Hill Ryerson Limited

55Chapt

er

Chapt

er Operating and Financial

LeverageOperating and Financial

Leverage

McGraw-Hill Ryerson ©2003 McGraw-Hill Ryerson Limited

Prepared by:

Terry FegartySeneca College

Revised ByP Chua

© 2003 McGraw-Hill Ryerson Limited

Chapter 5 - Outline

What is Leverage?Break-even AnalysisOperating LeverageFinancial LeverageCombined or Total LeverageSummary and Conclusions

PPT 5-2

© 2003 McGraw-Hill Ryerson Limited

What is Leverage?

In general terms, leverage means the use of force and effects to produce a more than normal results from a given action

In other words, leverage is the advantage generated by using a lever

Example, using a jack to lift a car

In Finance, leverage is the use of fixed costs to magnify the potential return to a firm

2 types of fixed costs: fixed operating costs = rent, salaries, etc. fixed financial costs = interest costs from debt

PPT 5-3

© 2003 McGraw-Hill Ryerson Limited

What is Leverage?

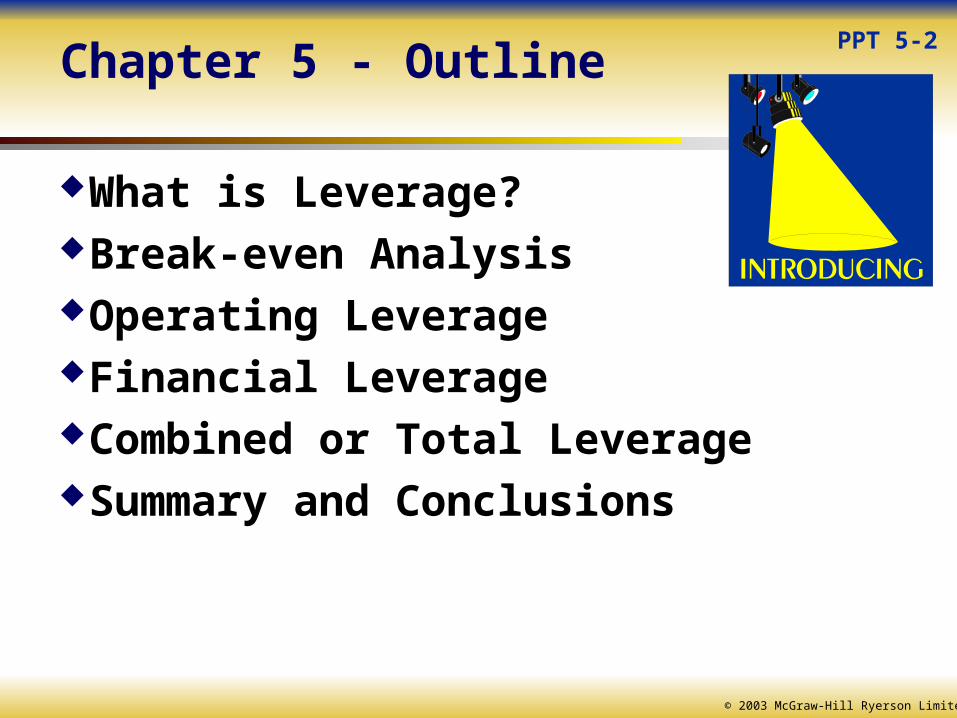

Leverage can magnify returns to common stockholders but can also increase risk

Management has almost complete control over this risk introduced through the use of leverage (fixed costs)

The degree in the use of leverage depends on management’s attitude toward risk and the nature of its business, among others.

Three types of leverage with reference to the firm’s income statement: Operating leverage, Financial leverage, and Combined (Total) leverage.

Leverage is measured on the profitability range of operations.

© 2003 McGraw-Hill Ryerson Limited

What is Leverage?

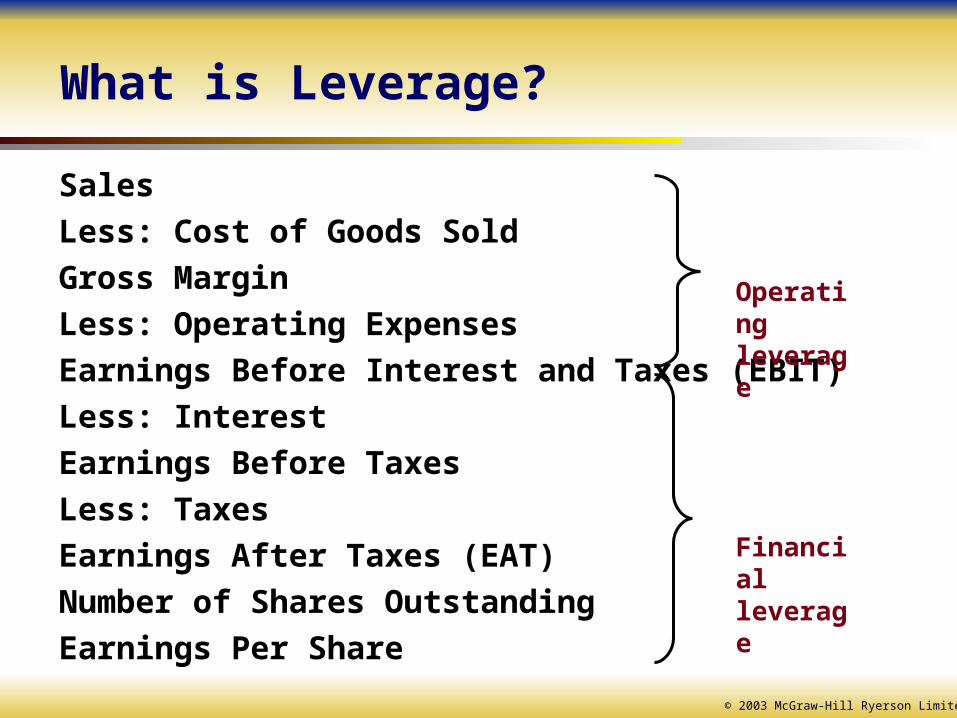

Sales

Less: Cost of Goods Sold

Gross Margin

Less: Operating Expenses

Earnings Before Interest and Taxes (EBIT)

Less: Interest

Earnings Before Taxes

Less: Taxes

Earnings After Taxes (EAT)

Number of Shares Outstanding

Earnings Per Share

Operatingleverage

Financialleverage

© 2003 McGraw-Hill Ryerson Limited

What is Leverage?

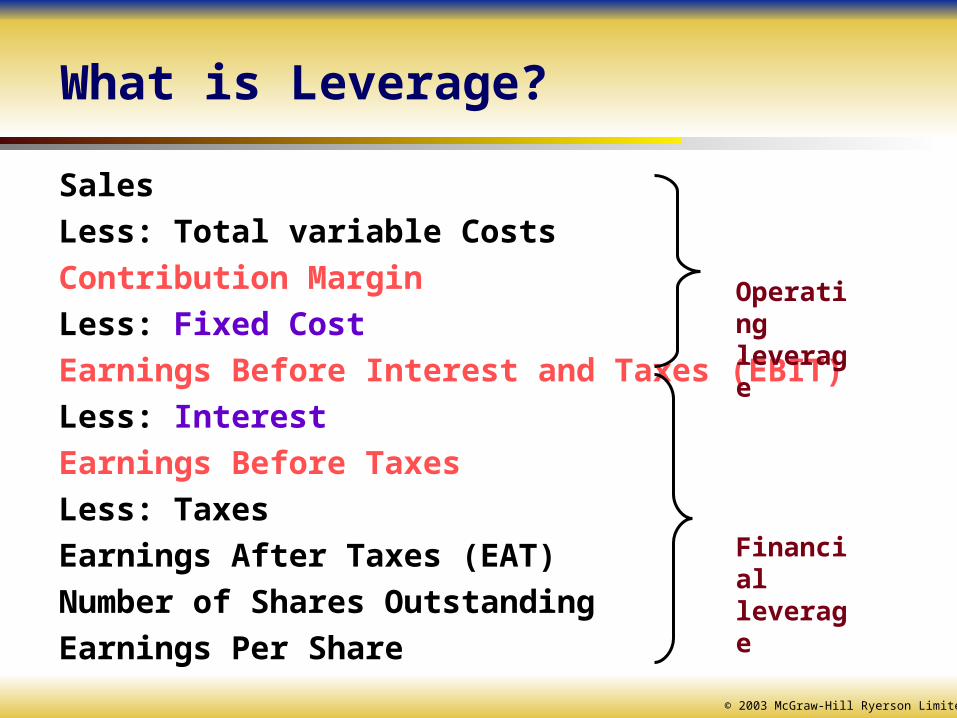

Sales

Less: Total variable Costs

Contribution Margin

Less: Fixed Cost

Earnings Before Interest and Taxes (EBIT)

Less: Interest

Earnings Before Taxes

Less: Taxes

Earnings After Taxes (EAT)

Number of Shares Outstanding

Earnings Per Share

Operatingleverage

Financialleverage

© 2003 McGraw-Hill Ryerson Limited

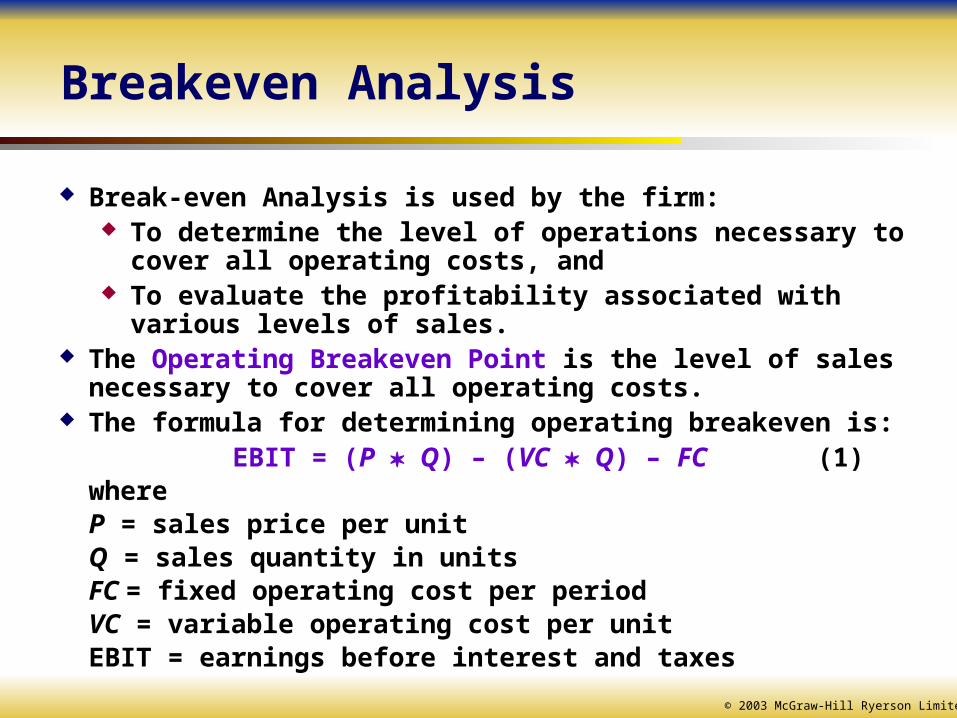

Breakeven Analysis

Break-even Analysis is used by the firm: To determine the level of operations necessary to cover all operating

costs, and To evaluate the profitability associated with various levels of sales.

The Operating Breakeven Point is the level of sales necessary to cover all operating costs.

The formula for determining operating breakeven is: EBIT = (P Q) – (VC Q) – FC (1)

whereP = sales price per unitQ = sales quantity in unitsFC = fixed operating cost per periodVC = variable operating cost per unitEBIT = earnings before interest and taxes

© 2003 McGraw-Hill Ryerson Limited

Breakeven Quantity

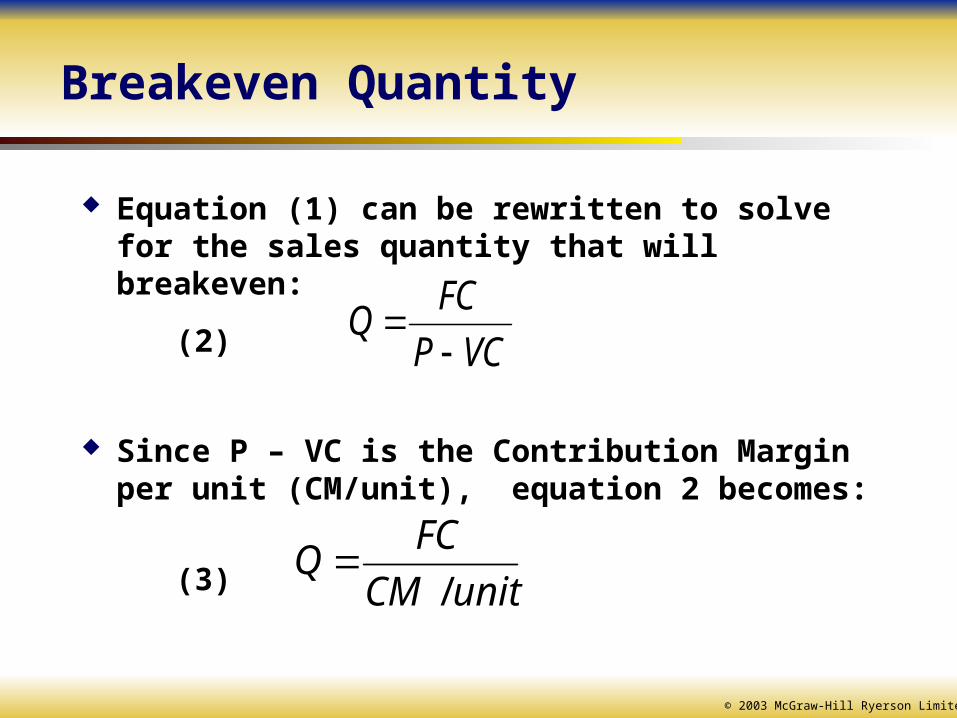

Equation (1) can be rewritten to solve for the sales quantity that will breakeven:

(2)

Since P – VC is the Contribution Margin per unit (CM/unit), equation 2 becomes:

(3)

VCP

FCQ

unitCM

FCQ

/

© 2003 McGraw-Hill Ryerson Limited

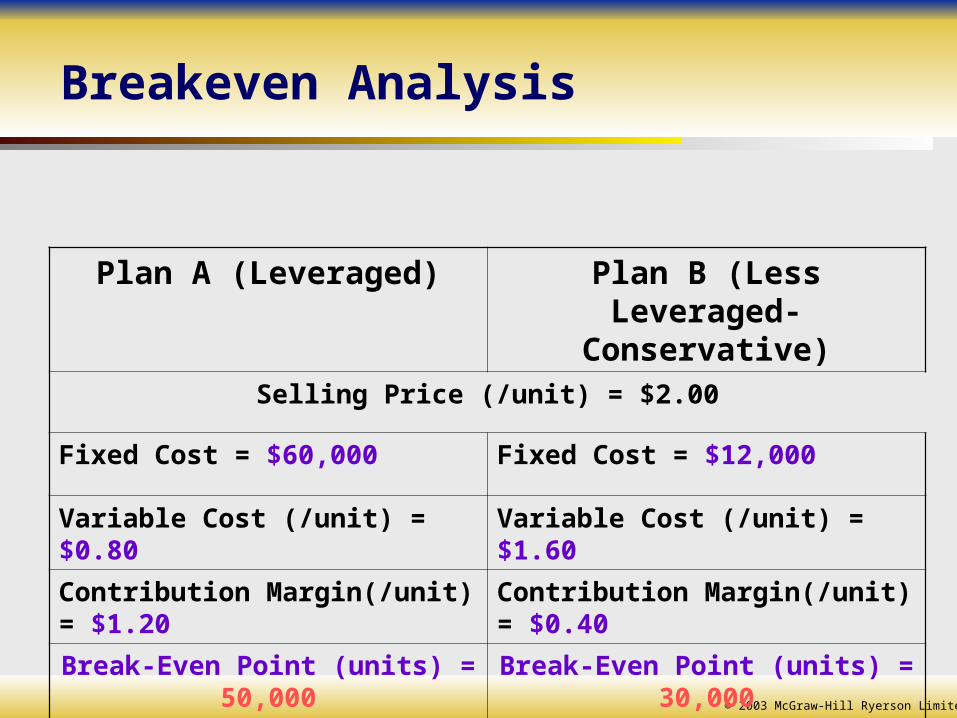

Breakeven Analysis

Plan A (Leveraged) Plan B (Less Leveraged-Conservative)

Selling Price (/unit) = $2.00

Fixed Cost = $60,000 Fixed Cost = $12,000

Variable Cost (/unit) = $0.80 Variable Cost (/unit) = $1.60

Contribution Margin(/unit) = $1.20 Contribution Margin(/unit) = $0.40

Break-Even Point (units) = 50,000 Break-Even Point (units) = 30,000

© 2003 McGraw-Hill Ryerson Limited

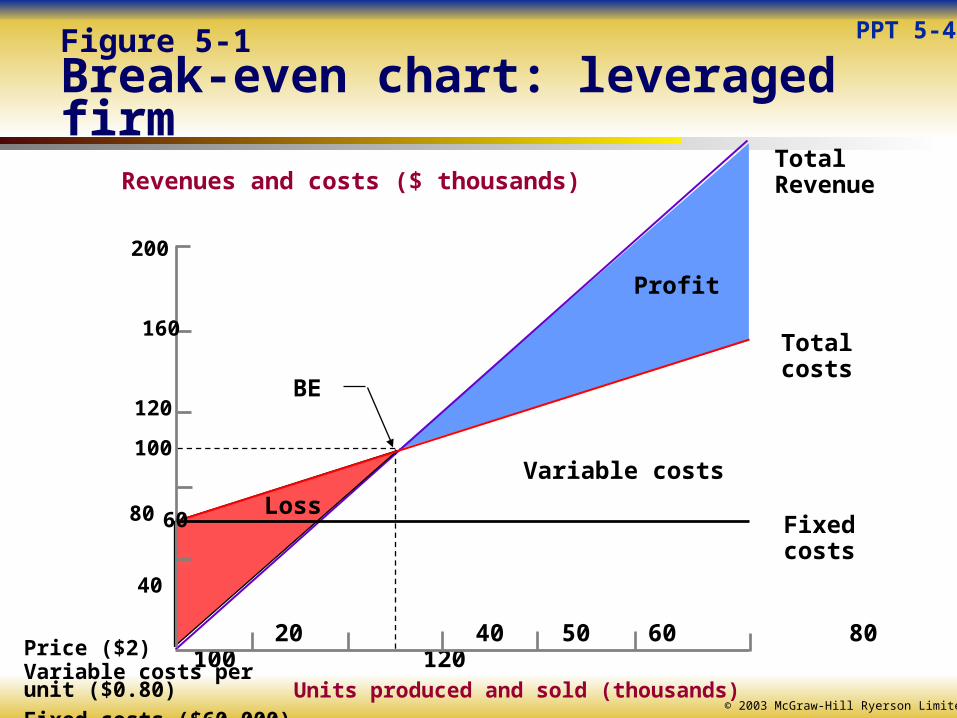

PPT 5-4Figure 5-1Break-even chart: leveraged firm

Revenues and costs ($ thousands)

20 40 50 60 80 100 120

TotalRevenue

Totalcosts

Variable costs

Fixedcosts

Profit

BE

Loss

Units produced and sold (thousands)

200

160

120

100

80

60

40

Price ($2)Variable costs per unit ($0.80)

Fixed costs ($60,000)

© 2003 McGraw-Hill Ryerson Limited

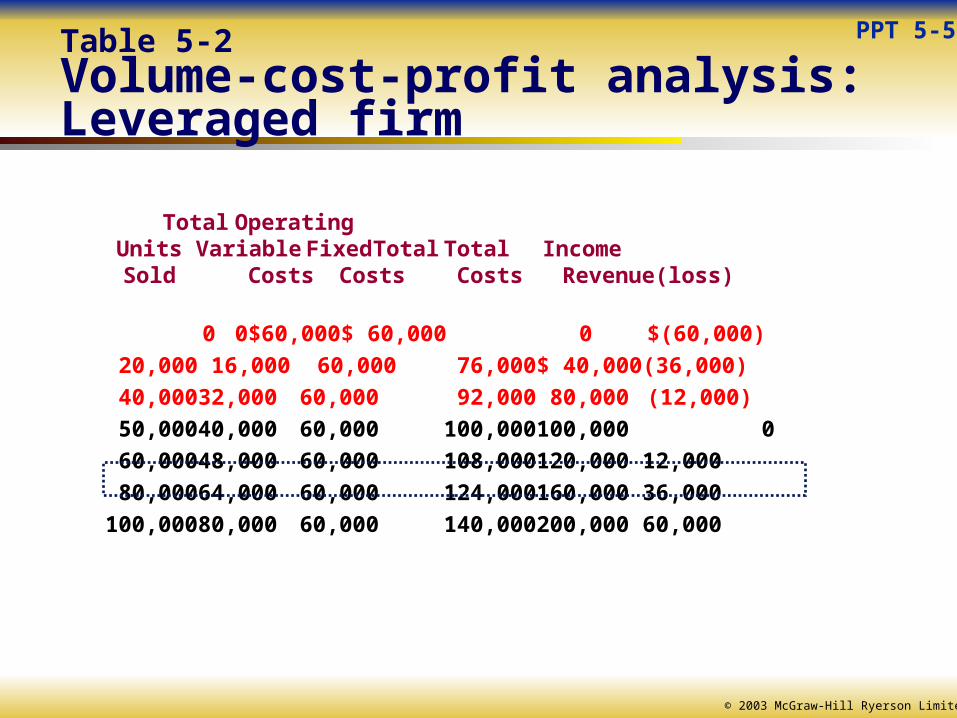

Table 5-2Volume-cost-profit analysis: Leveraged firm

Total OperatingUnits Variable Fixed Total Total IncomeSold Costs Costs Costs Revenue (loss)

0 0 $60,000 $ 60,000 0 $(60,000)

20,000 16,000 60,000 76,000 $ 40,000 (36,000)

40,000 32,000 60,000 92,000 80,000 (12,000)

50,000 40,000 60,000 100,000 100,000 0

60,000 48,000 60,000 108,000 120,000 12,000

80,000 64,000 60,000 124,000 160,000 36,000

100,000 80,000 60,000 140,000 200,000 60,000

PPT 5-5

© 2003 McGraw-Hill Ryerson Limited

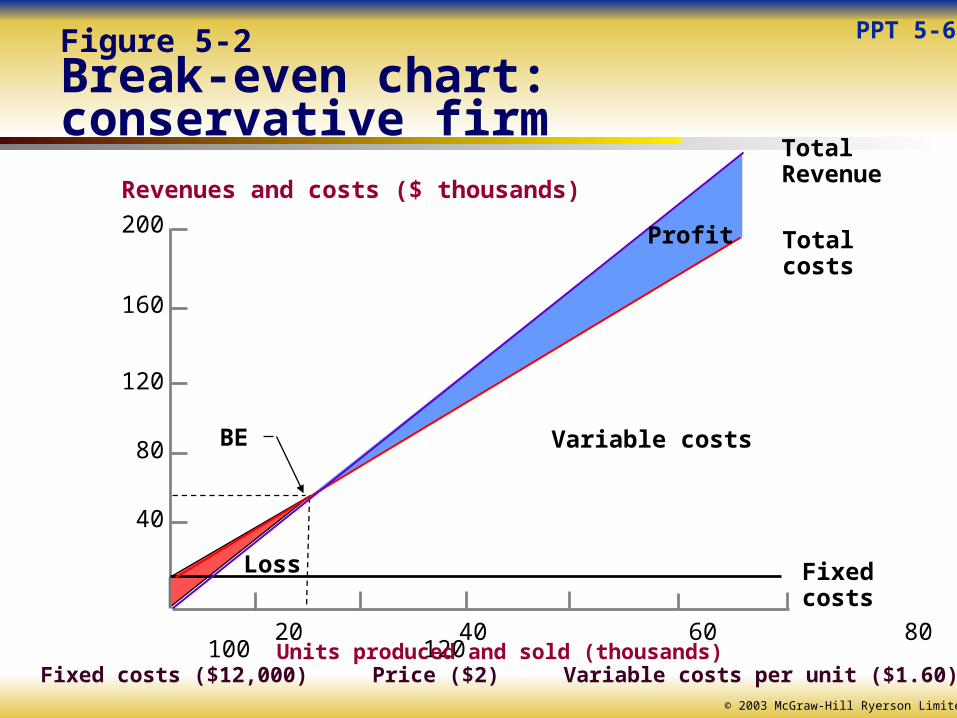

PPT 5-6Figure 5-2Break-even chart: conservative firm

Revenues and costs ($ thousands)

200

160

120

80

40

20 40 60 80 100 120

TotalRevenue

Totalcosts

Variable costs

Fixedcosts

Profit

BE

Loss

Units produced and sold (thousands)Fixed costs ($12,000) Price ($2) Variable costs per unit ($1.60)

© 2003 McGraw-Hill Ryerson Limited

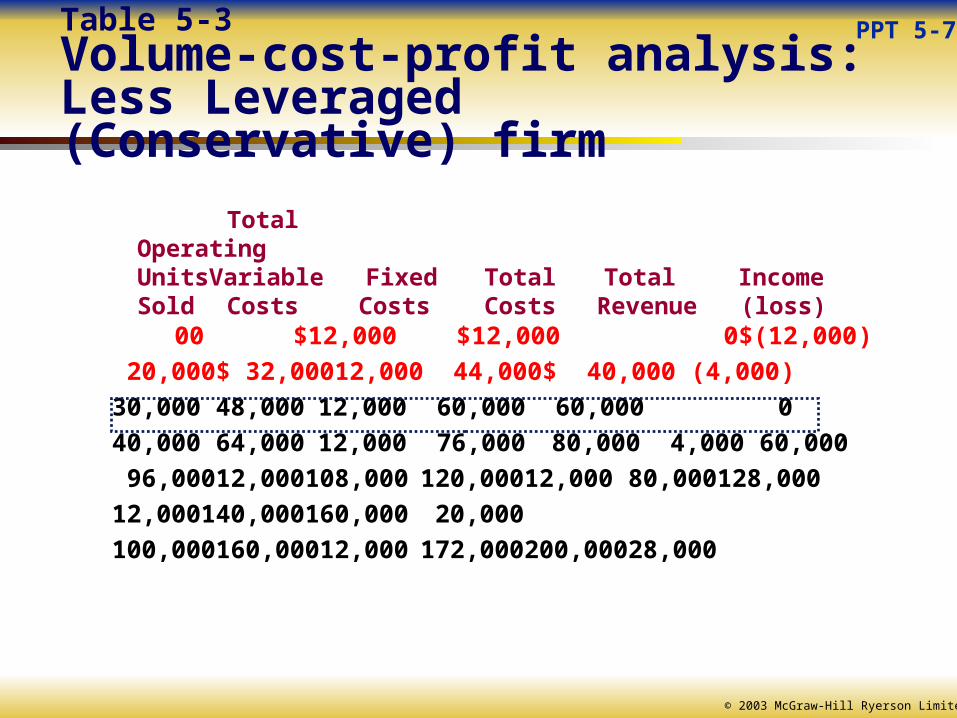

Table 5-3Volume-cost-profit analysis: Less Leveraged (Conservative) firm

0 0 $12,000 $ 12,000 0 $(12,000.)

20,000 $ 32,000 12,000 44,000 $ 40,000 (4,000.)

30,000 48,00012,000 60,000 60,000 0 40,000

64,00012,000 76,000 80,000 4,000 60,000 96,000

12,000108,000120,00012,000 80,000 128,000 12,000

140,000 160,000 20,000

100,000 160,000 12,000 172,000 200,000 28,000

Total OperatingUnits Variable Fixed Total Total IncomeSold Costs Costs Costs Revenue (loss)

PPT 5-7

© 2003 McGraw-Hill Ryerson Limited

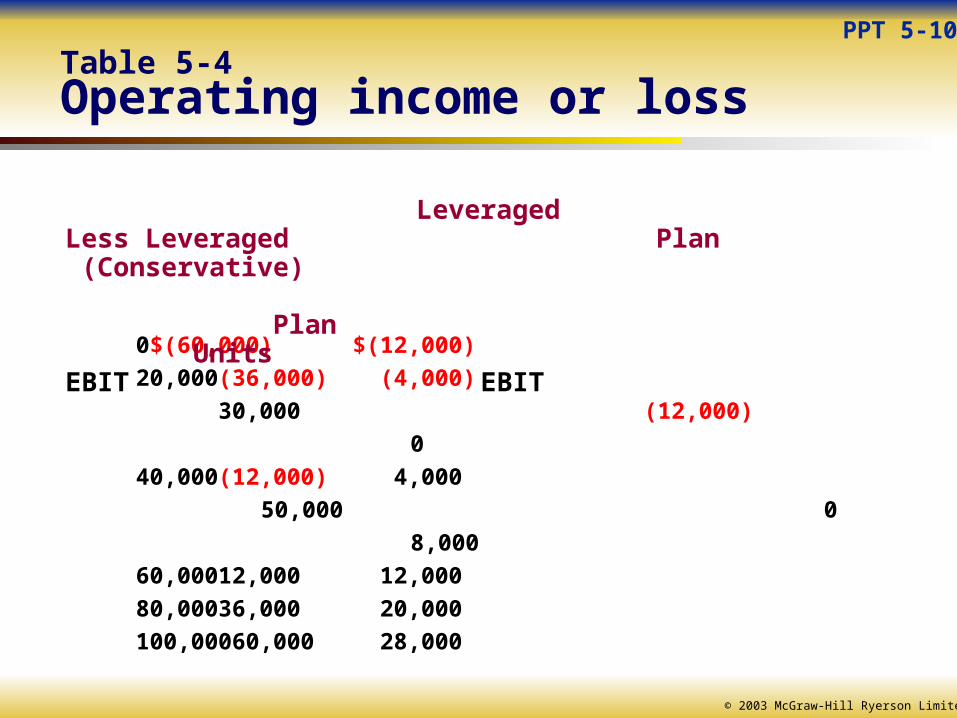

0 $(60,000) $(12,000)

20,000 (36,000) (4,000)

30,000 (12,000) 0

40,000 (12,000) 4,000

50,000 0 8,000

60,000 12,000 12,000

80,000 36,000 20,000

100,000 60,000 28,000

Leveraged Less Leveraged Plan (Conservative) Plan

Units EBIT EBIT

PPT 5-10

Table 5-4Operating income or loss

© 2003 McGraw-Hill Ryerson Limited

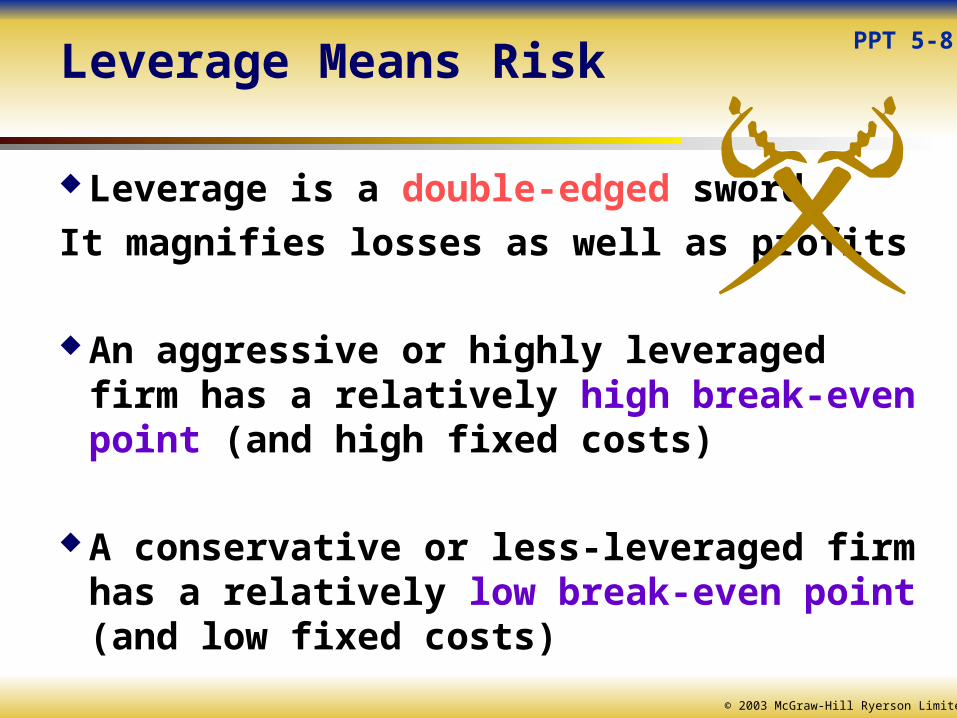

Leverage Means Risk

Leverage is a double-edged sword

It magnifies losses as well as profits

An aggressive or highly leveraged firm has a relatively high break-even point (and high fixed costs)

A conservative or less-leveraged firm has a relatively low break-even point (and low fixed costs)

PPT 5-8

© 2003 McGraw-Hill Ryerson Limited

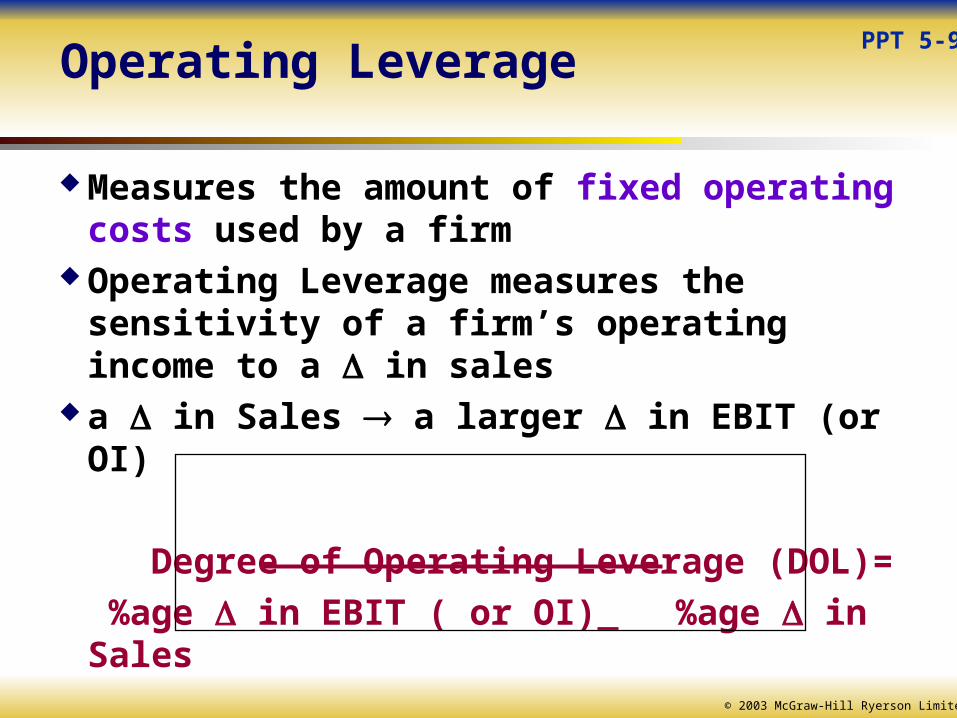

Operating Leverage

Measures the amount of fixed operating costs used by a firm

Operating Leverage measures the sensitivity of a firm’s operating income to a in sales

a in Sales a larger in EBIT (or OI)

Degree of Operating Leverage (DOL)=

%age in EBIT ( or OI) %age in Sales

PPT 5-9

© 2003 McGraw-Hill Ryerson Limited

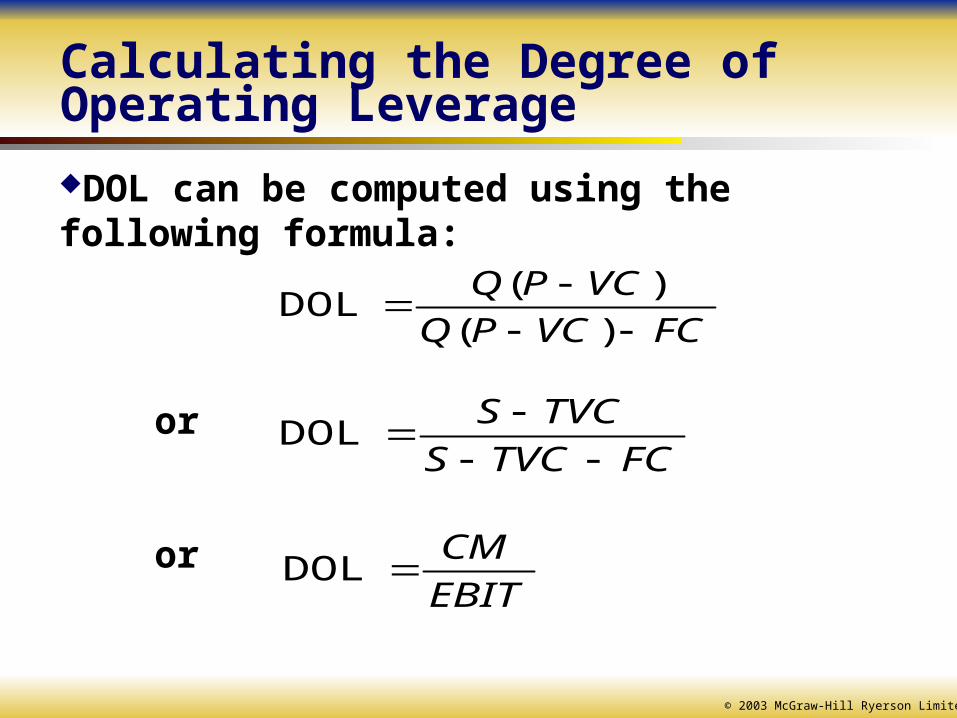

Calculating the Degree of Operating Leverage

DOL can be computed using the following formula:

or

or

FCVCPQ

VCPQ

)(

)( DOL

FCTVCS

TVCS

DOL

EBIT

CM DOL

© 2003 McGraw-Hill Ryerson Limited

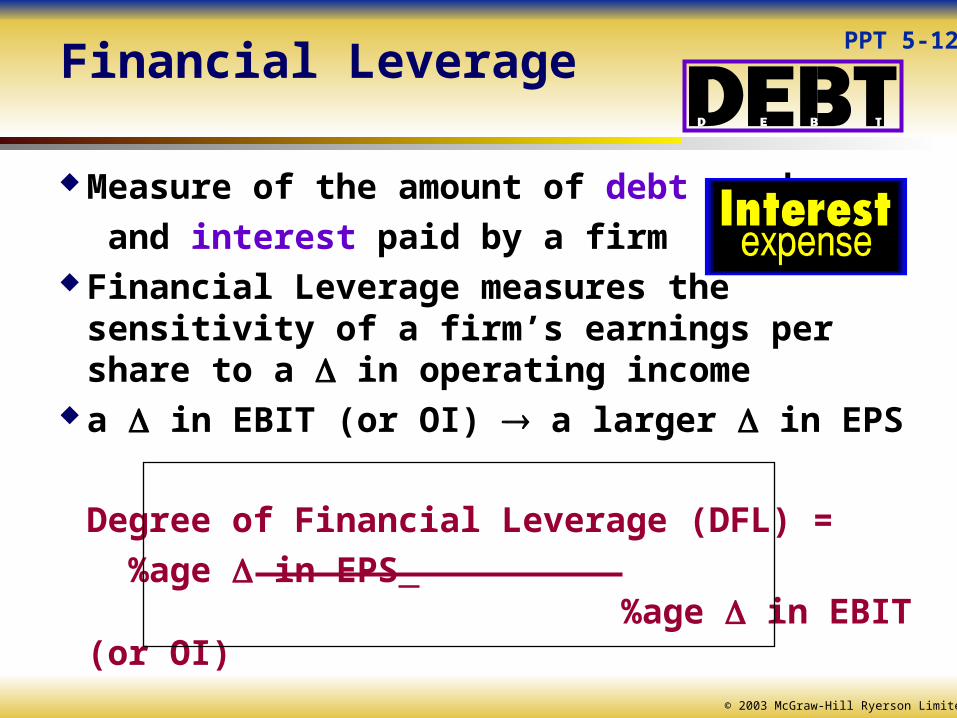

Financial Leverage

Measure of the amount of debt used

and interest paid by a firm Financial Leverage measures the sensitivity of a

firm’s earnings per share to a in operating income a in EBIT (or OI) a larger in EPS

Degree of Financial Leverage (DFL) =

%age in EPS %age in EBIT (or OI)

PPT 5-12

© 2003 McGraw-Hill Ryerson Limited

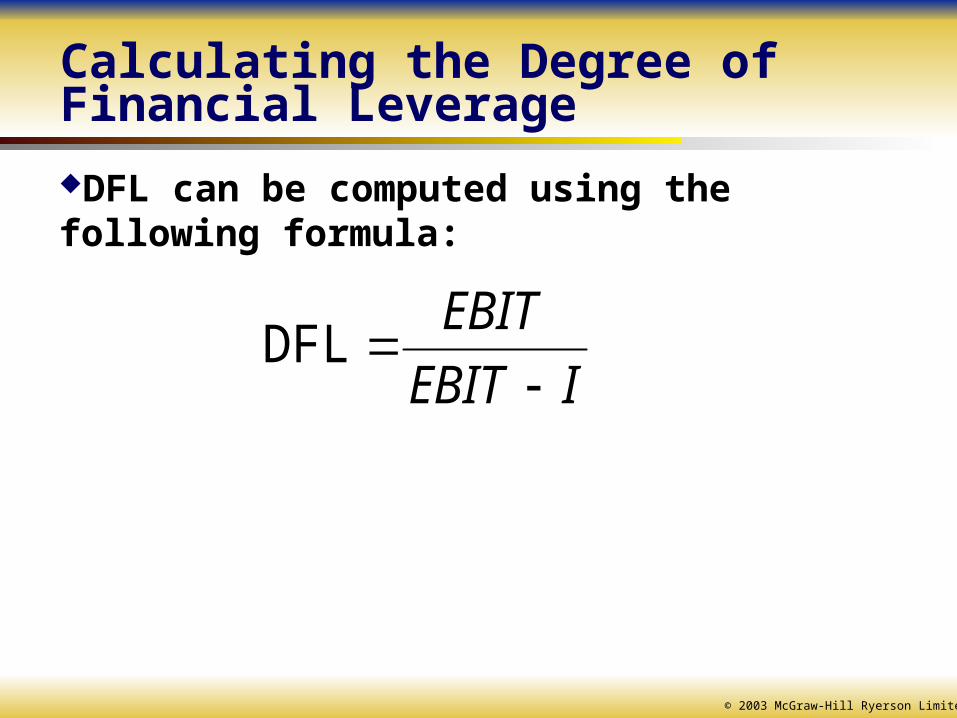

Calculating the Degree of Financial Leverage

DFL can be computed using the following formula:

IEBIT

EBIT

DFL

© 2003 McGraw-Hill Ryerson Limited

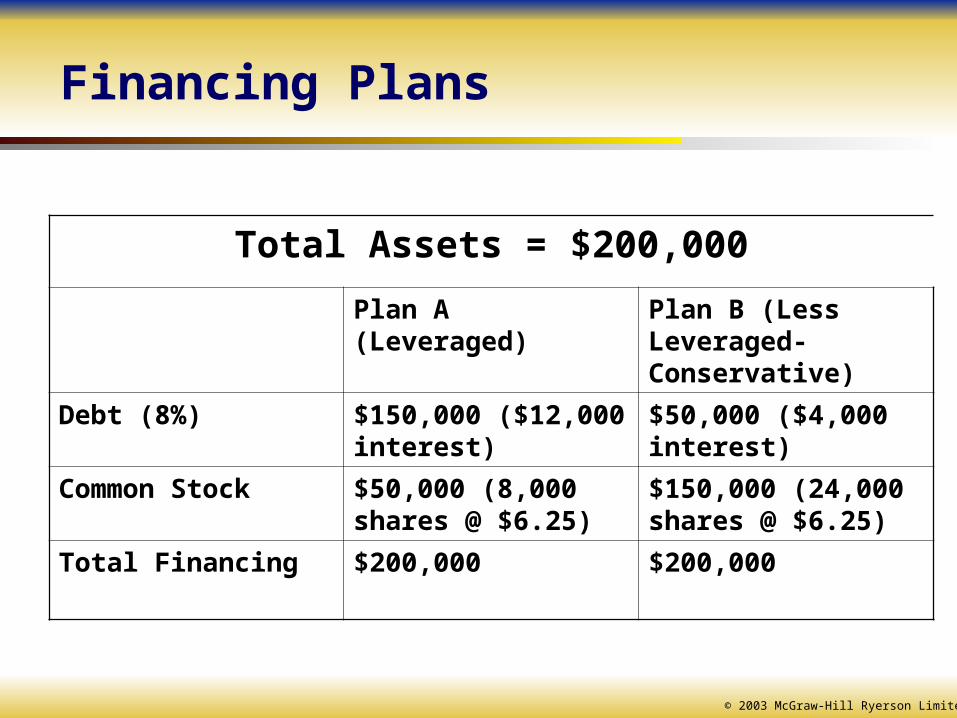

Financing Plans

Total Assets = $200,000

Plan A (Leveraged) Plan B (Less Leveraged-Conservative)

Debt (8%) $150,000 ($12,000 interest)

$50,000 ($4,000 interest)

Common Stock $50,000 (8,000 shares @ $6.25)

$150,000 (24,000 shares @ $6.25)

Total Financing $200,000 $200,000

© 2003 McGraw-Hill Ryerson Limited

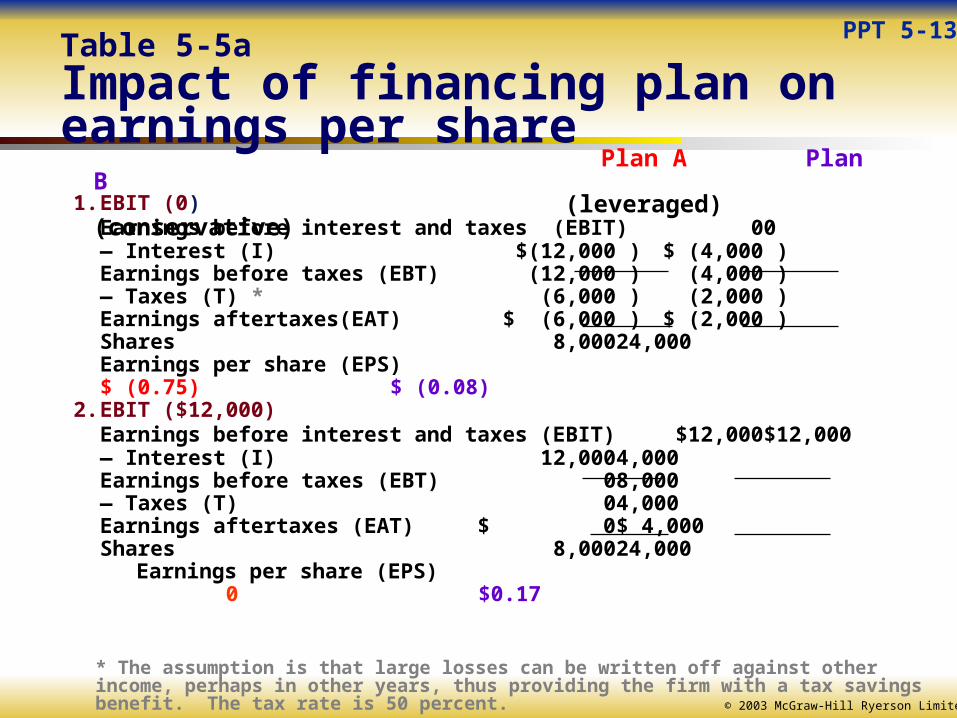

1. EBIT (0)Earnings before interest and taxes (EBIT) 0 0— Interest (I) $(12,000.) $ (4,000.)Earnings before taxes (EBT) (12,000.) (4,000.)— Taxes (T) * (6,000.) (2,000.)Earnings aftertaxes(EAT) $ (6,000.) $ (2,000.)Shares 8,000 24,000Earnings per share (EPS) $ (0.75) $ (0.08)

2. EBIT ($12,000)Earnings before interest and taxes (EBIT) $12,000 $12,000— Interest (I) 12,000 4,000Earnings before taxes (EBT) 0 8,000— Taxes (T) 0 4,000Earnings aftertaxes (EAT) $ 0 $ 4,000Shares 8,000 24,000

Earnings per share (EPS) 0 $0.17

Plan A Plan B(leveraged)

(conservative)

* The assumption is that large losses can be written off against other income, perhaps in other years, thus providing the firm with a tax savings benefit. The tax rate is 50 percent.

PPT 5-13Table 5-5a Impact of financing plan on earnings per share

© 2003 McGraw-Hill Ryerson Limited

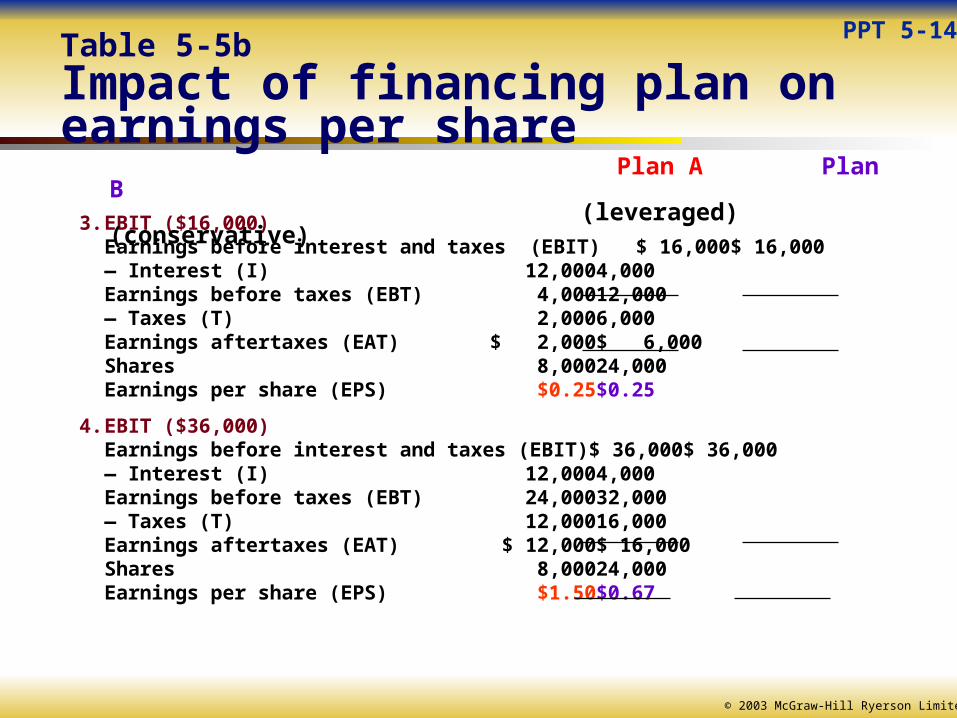

3. EBIT ($16,000)Earnings before interest and taxes (EBIT) $ 16,000 $ 16,000— Interest (I) 12,000 4,000Earnings before taxes (EBT) 4,000 12,000— Taxes (T) 2,000 6,000Earnings aftertaxes (EAT) $ 2,000 $ 6,000Shares 8,000 24,000Earnings per share (EPS) $0.25 $0.25

4. EBIT ($36,000)Earnings before interest and taxes (EBIT) $ 36,000 $ 36,000— Interest (I) 12,000 4,000Earnings before taxes (EBT) 24,000 32,000— Taxes (T) 12,000 16,000Earnings aftertaxes (EAT) $ 12,000 $ 16,000Shares 8,000 24,000Earnings per share (EPS) $1.50 $0.67

Plan A Plan B(leveraged)

(conservative)

PPT 5-14Table 5-5b Impact of financing plan on earnings per share

© 2003 McGraw-Hill Ryerson Limited

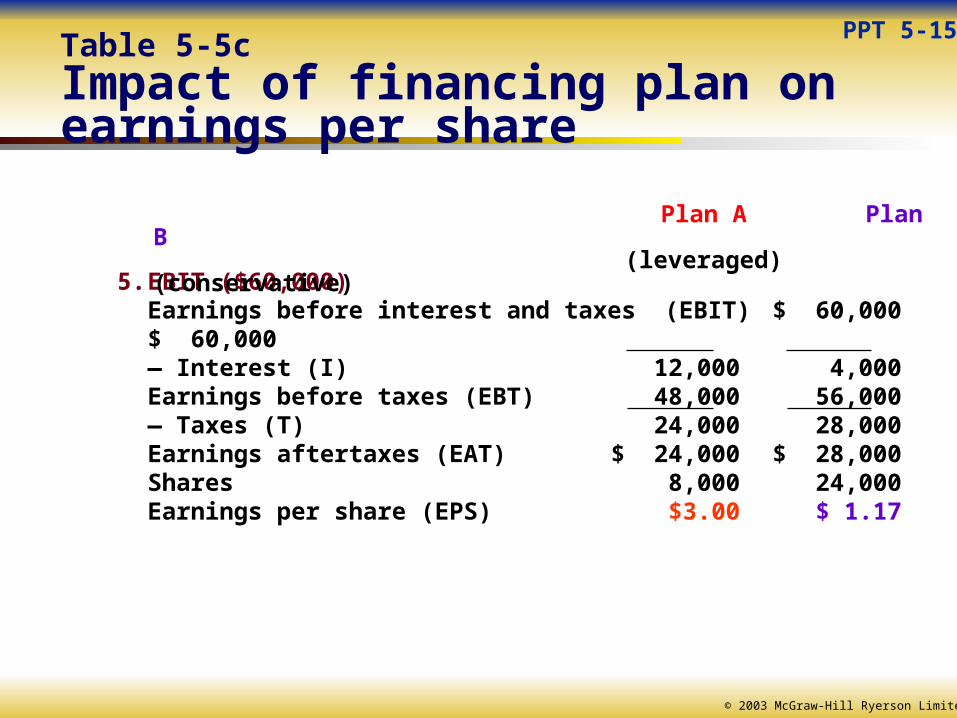

5. EBIT ($60,000)Earnings before interest and taxes (EBIT) $ 60,000 $ 60,000— Interest (I) 12,000 4,000Earnings before taxes (EBT) 48,000 56,000— Taxes (T) 24,000 28,000Earnings aftertaxes (EAT) $ 24,000 $ 28,000Shares 8,000 24,000Earnings per share (EPS) $3.00 $ 1.17

Plan A Plan B(leveraged)

(conservative)

PPT 5-15Table 5-5c Impact of financing plan on earnings per share

© 2003 McGraw-Hill Ryerson Limited

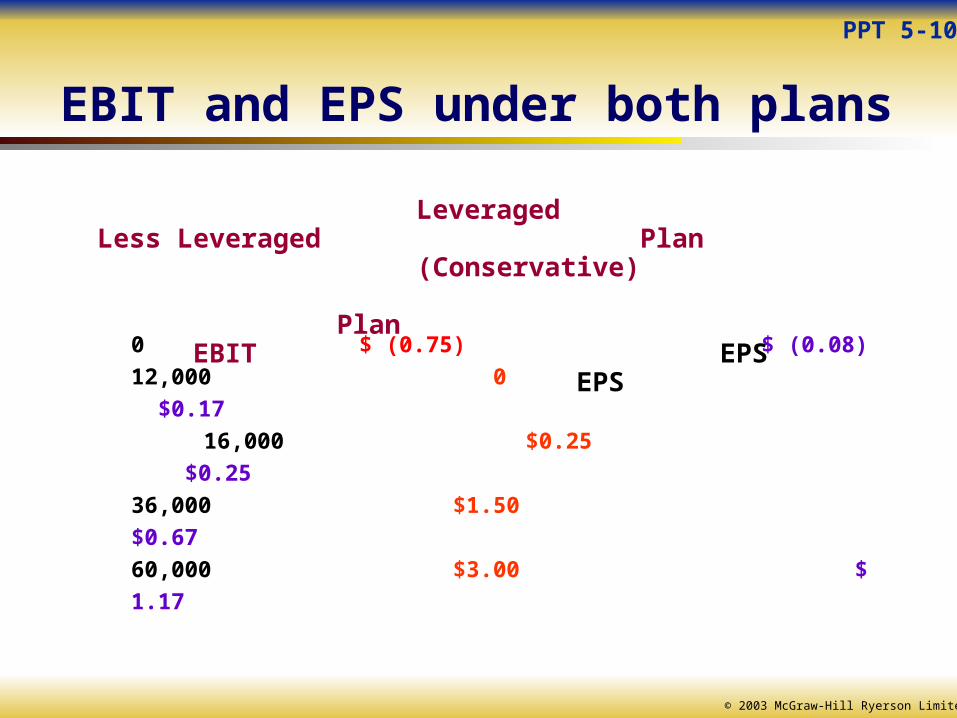

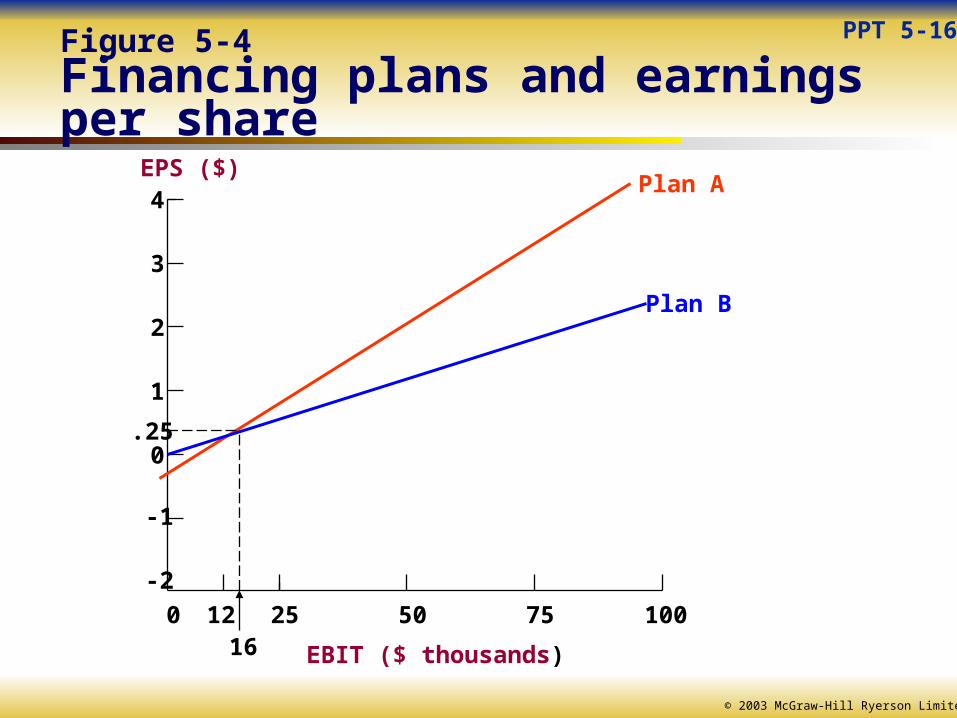

0 $ (0.75) $ (0.08)

12,000 0 $0.17

16,000 $0.25 $0.25

36,000 $1.50 $0.67

60,000 $3.00 $ 1.17

Leveraged Less Leveraged Plan (Conservative) Plan

EBIT EPS EPS

PPT 5-10

EBIT and EPS under both plans

© 2003 McGraw-Hill Ryerson Limited

PPT 5-16Figure 5-4Financing plans and earnings per share

4

3

2

1

0

-1

-2

120 25 50 75 100

EBIT ($ thousands)

EPS ($)

16

.25

Plan A

Plan B

© 2003 McGraw-Hill Ryerson Limited

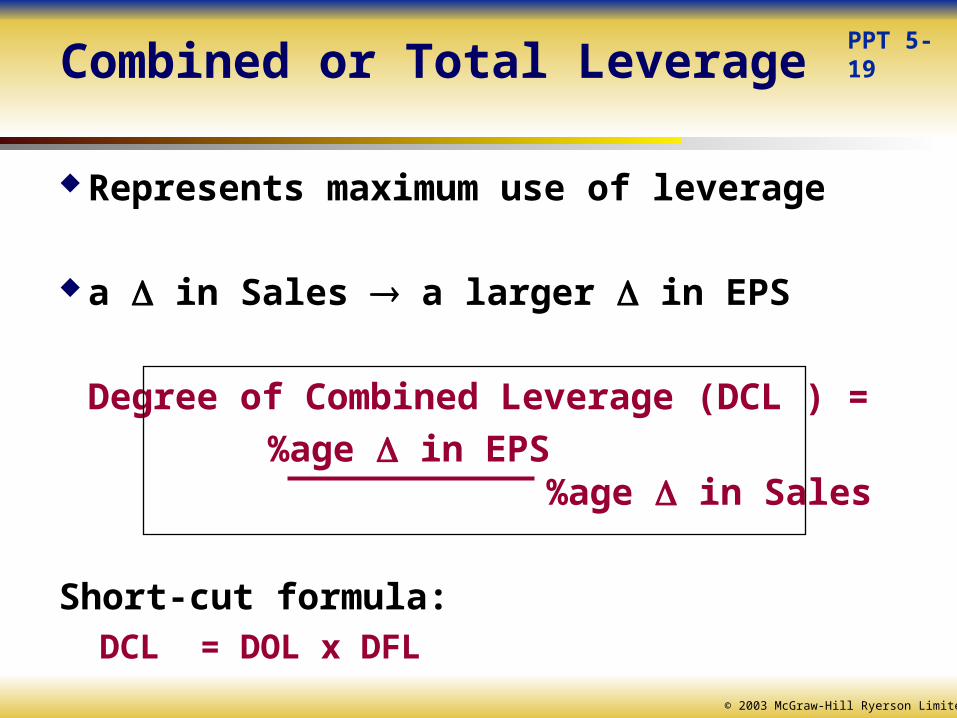

Combined or Total Leverage

Represents maximum use of leverage

a in Sales a larger in EPS

Degree of Combined Leverage (DCL ) =

%age in EPS %age in Sales

Short-cut formula:DCL = DOL x DFL

PPT 5-19

© 2003 McGraw-Hill Ryerson Limited

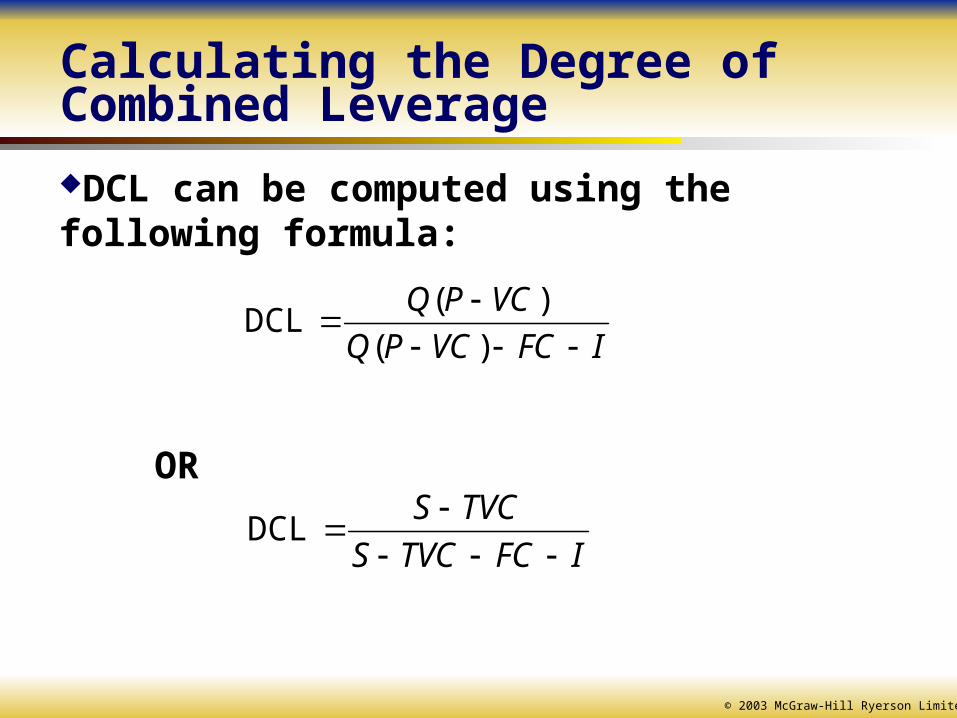

Calculating the Degree of Combined Leverage

DCL can be computed using the following formula:

OR

IFCVCPQ

VCPQ

)(

)( DCL

IFCTVCS

TVCS

DCL

© 2003 McGraw-Hill Ryerson Limited

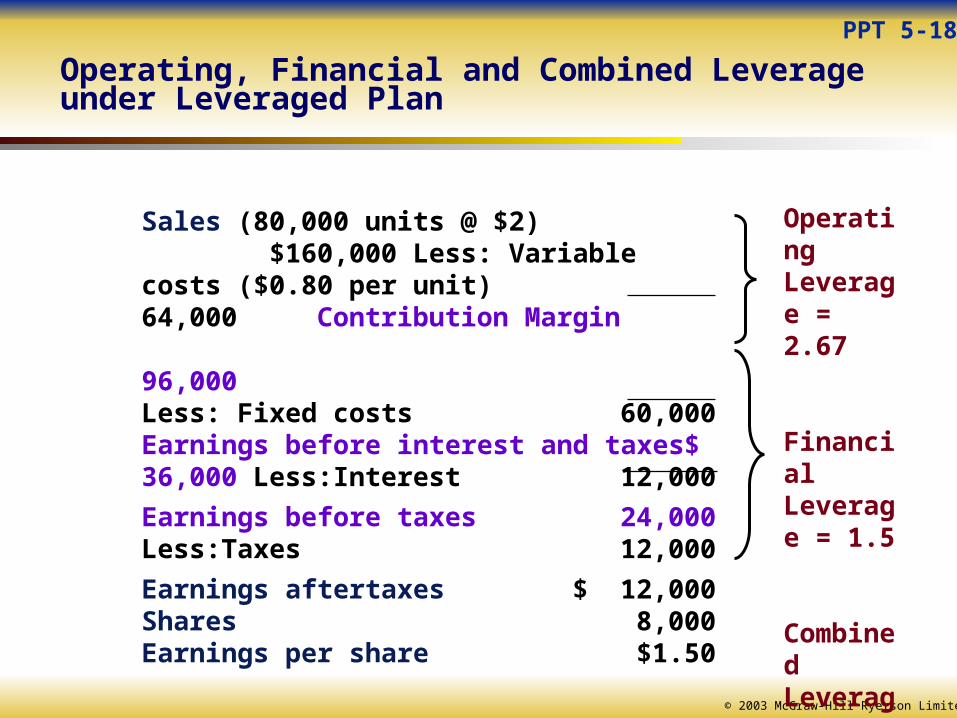

Sales (80,000 units @ $2) $160,000 Less: Variable costs ($0.80 per unit) 64,000 Contribution Margin 96,000Less: Fixed costs 60,000Earnings before interest and taxes$ 36,000 Less:Interest 12,000

Earnings before taxes 24,000Less:Taxes 12,000

Earnings aftertaxes $ 12,000Shares 8,000Earnings per share $1.50

OperatingLeverage = 2.67

FinancialLeverage = 1.5

Combined Leverage=4

PPT 5-18

Operating, Financial and Combined Leverage under Leveraged Plan

© 2003 McGraw-Hill Ryerson Limited

Sales (80,000 units @ $2) $160,000 Less: Variable costs ($1.60 per unit) 128,000 Contribution Margin 32,000Less: Fixed costs 12,000Earnings before interest and taxes$ 20,000 Less:Interest 4,000

Earnings before taxes 16,000Less:Taxes 8,000

Earnings aftertaxes $ 8,000Shares 24,000Earnings per share $0.33

OperatingLeverage = 1.6

FinancialLeverage = 1.25

Combined Leverage=2

PPT 5-18

Operating, Financial and Combined Leverage under Less Leveraged (Conservative) Plan

© 2003 McGraw-Hill Ryerson Limited

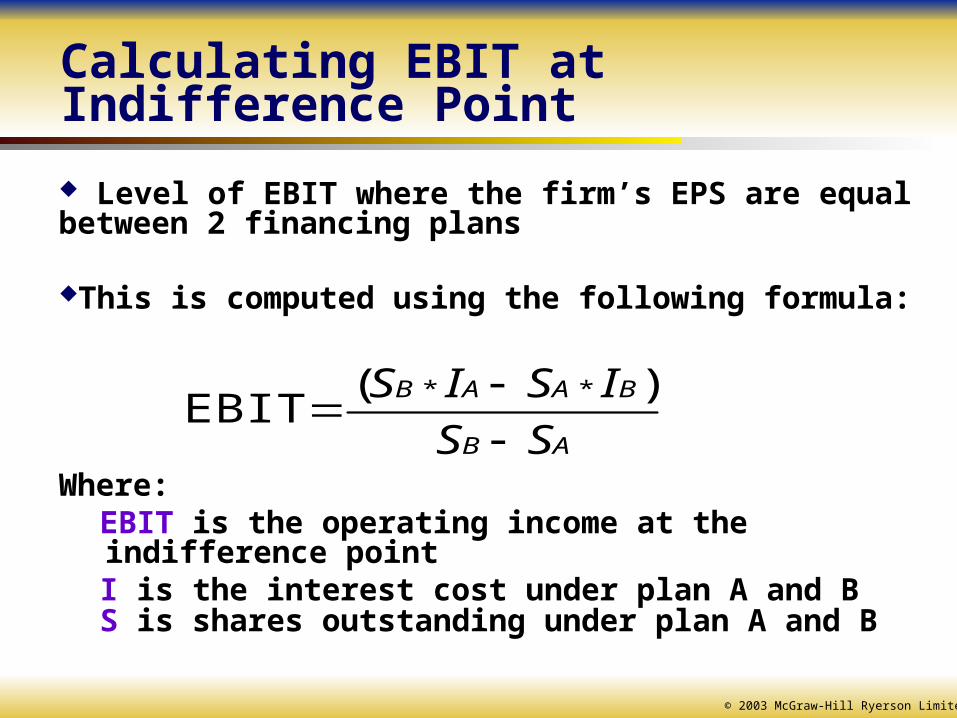

Calculating EBIT at Indifference Point

Level of EBIT where the firm’s EPS are equal between 2 financing plans

This is computed using the following formula:

Where:EBIT is the operating income at the indifference pointI is the interest cost under plan A and BS is shares outstanding under plan A and B

AB

BAAB

SS

ISIS

)(

EBIT**

© 2003 McGraw-Hill Ryerson Limited

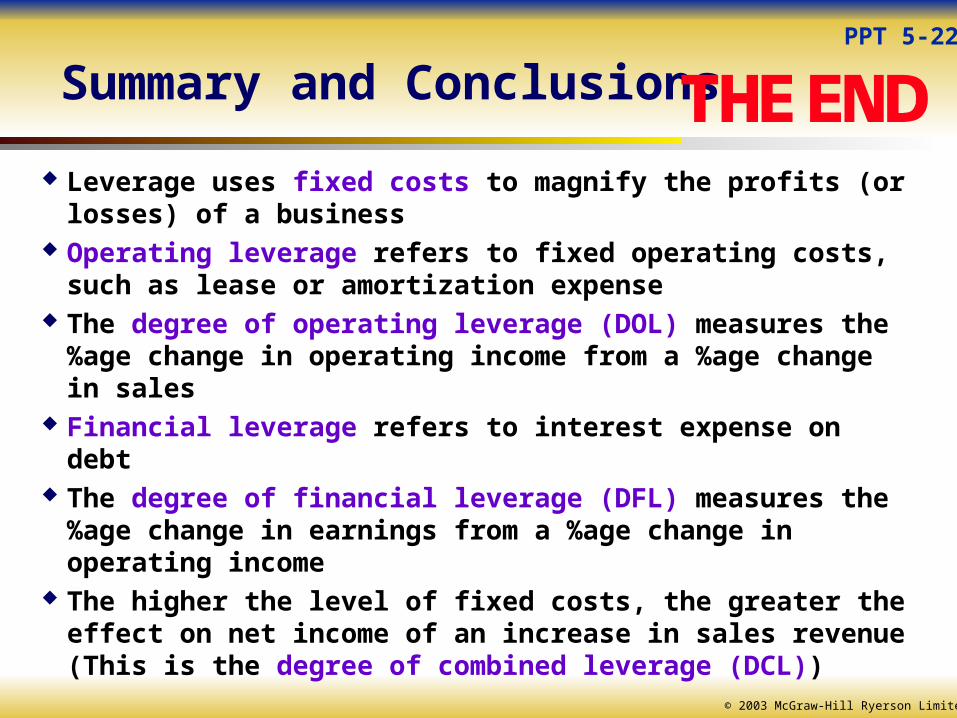

Summary and Conclusions

Leverage uses fixed costs to magnify the profits (or losses) of a business

Operating leverage refers to fixed operating costs, such as lease or amortization expense

The degree of operating leverage (DOL) measures the %age change in operating income from a %age change in sales

Financial leverage refers to interest expense on debt The degree of financial leverage (DFL) measures the %age

change in earnings from a %age change in operating income The higher the level of fixed costs, the greater the effect on

net income of an increase in sales revenue (This is the degree of combined leverage (DCL))

PPT 5-22