Embed Size (px)

Citation preview

F ^^

erra

,^ ,ü ^^ 3 ^ 1F ^^y+ t^ ; ,t^ ^r 4 s ^'^X " 3x^^ zs: ^ r ^ ; s ;`t ^ a^^` ^`

f^ ^.,l k `a ^^:; Y a+ti y^a

Tf.n{`' S- Gl eEy .,

y 1lt^ ^P Afv.G Y { 7t U b .,kf t ^Y 4 t b ,

9 yr. yr, i : ^ 5^y ^. .',^ S 1 ^

3 M1v }p ; ¡+'^g;^:.},^^

_ _ 1. Y. f •':. _ tn tia ^ a `h . ,+ d

rf

erg} 4.'..

a tryL

E ¿t+ras C s^jg¿ ^ .^ A

w

t4iF^ F^ J' S^j^.Y, _J 3

tic 4°SA..

AS65AACopyright © 1994by South-Western Publishing Co.Cincinnati, Ohio

I T©PInternational Thomson PublishingSouth-Westem Publishing Co. is an ITP Company. The HP trademark is used under license.

Portions of this work have been reprinted by permission of the President and Fellowsof Harvard College.

Ah Rights Reserved. No part of this book may be reproduced, storage in a retrieval sys-tem, or transmitted, in any form or by any mean, electronic or mechanical, photocopying,recording, or otherwise, without the prior written permission of the copyright holder. Thecopyright on each case in this book unless otherwise noted is held by the President and Fel-lows of Harvard College and they are published herein by express permission. Permissionrequests to use individual Harvard copyrighted cases should be directed to the PermissionManager, Harvard Business School Publishing Division, Boston, MA 02163.

Case material of the Harvard Graduate School of Business Ad -iinistration is made possibleby the cooperation of business firms and other organizations which may wish to remainanonymous by having narres, quantities, and other identifying details disguised whilemaintaining basic relationships. Cases are prepared as the basis for class discussion ratherthan to illustrate either effective or ineffective handling of an administrative situation.

ISBN: 0-538-83310-6

123456 7890D2 1098 76543

Printed in the United States of America

Library of Congress Catalog-in-Publication Data

Bruns, William J.

Accounting for managers: text and cases/William J. Bruns, Jr.p. cm.

ISBN 0-538-83310-61. Managerial accountitig. 2. Managerial accounting—Case studies.

I. Title.HF5657.4.B78 1994658.15'11--dc20

93-8521CIP

Sponsoring Editor: Mark R. HubbleSenior Developmental Editor: Ken MartinProduction Editor/Trainer: Leslie KauffmanProduction Editor I: Crystal ChapinCover and Interior Designer: Tom HubbardCover Photograph: Comstock, Inc.Marketing Manager: Martin W. LewisSponsoring Representative: Lynne Riesinger

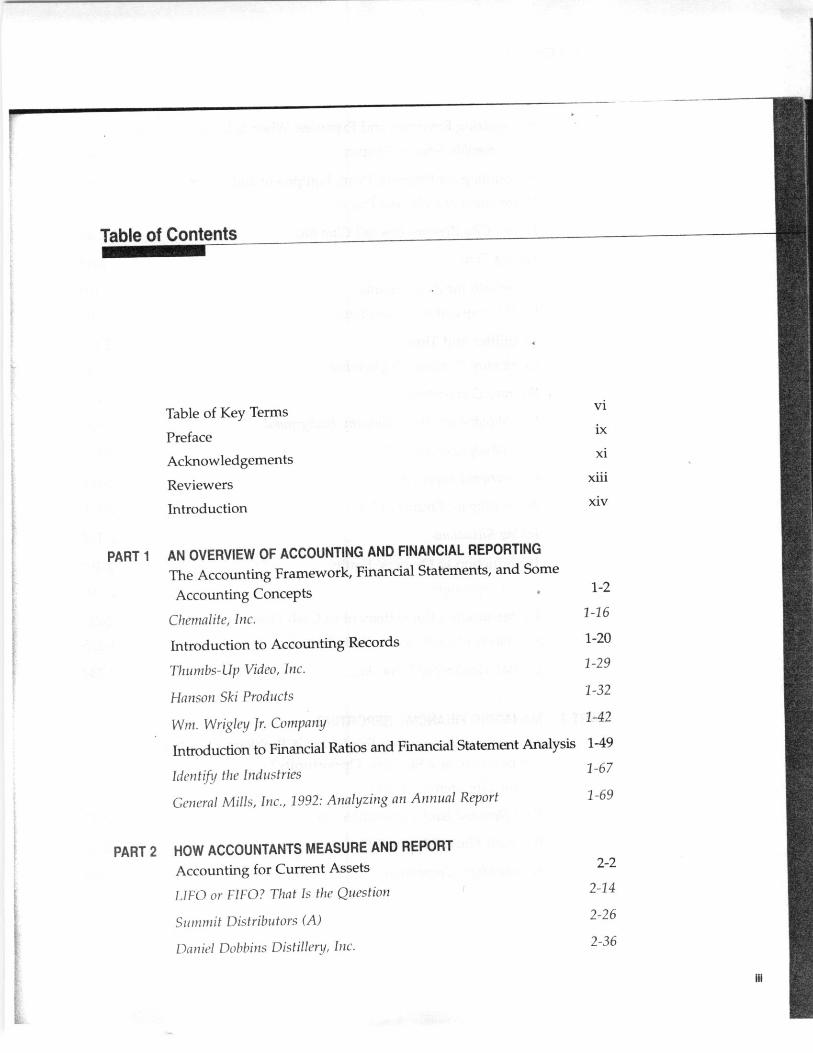

Table of Contents

Table of Key Tercosvi

Prefaceix

Acknowledgements xi

Reviewersxiii

Introductionxiv

PART 1 AN OVERVIEW OF ACCOUNTING AND FINANCIAL REPORTINGThe Accounting Framework, Financial Statements, and Some

Accounting Concepts 1-2

Clu',nalite, Inc. 1-16

Introduction to Accounting Records 1-20

Titwnbs-Up Video, Inc. 1-29

Hanson Ski Products 1-32

Wrn. Wri1cy Jr. Conipany 1-42

Introduction to Financial Ratios and Financial Statement Analysis 1-49

Idlctttify fue industries 1-67

General Milis, Inc., 1992: Analijzing an Annual Report 1-69

PART 2 HOW ACCOUNTANTS MEASURE AND REPORTAccounting for Current Assets 2-2

L11 C) or FIFO? T1uat Is Nre Question 2-14

Swnzmit Distributors (A) 2-26

Daniel Dobbins Distillery, Inc. 2-36

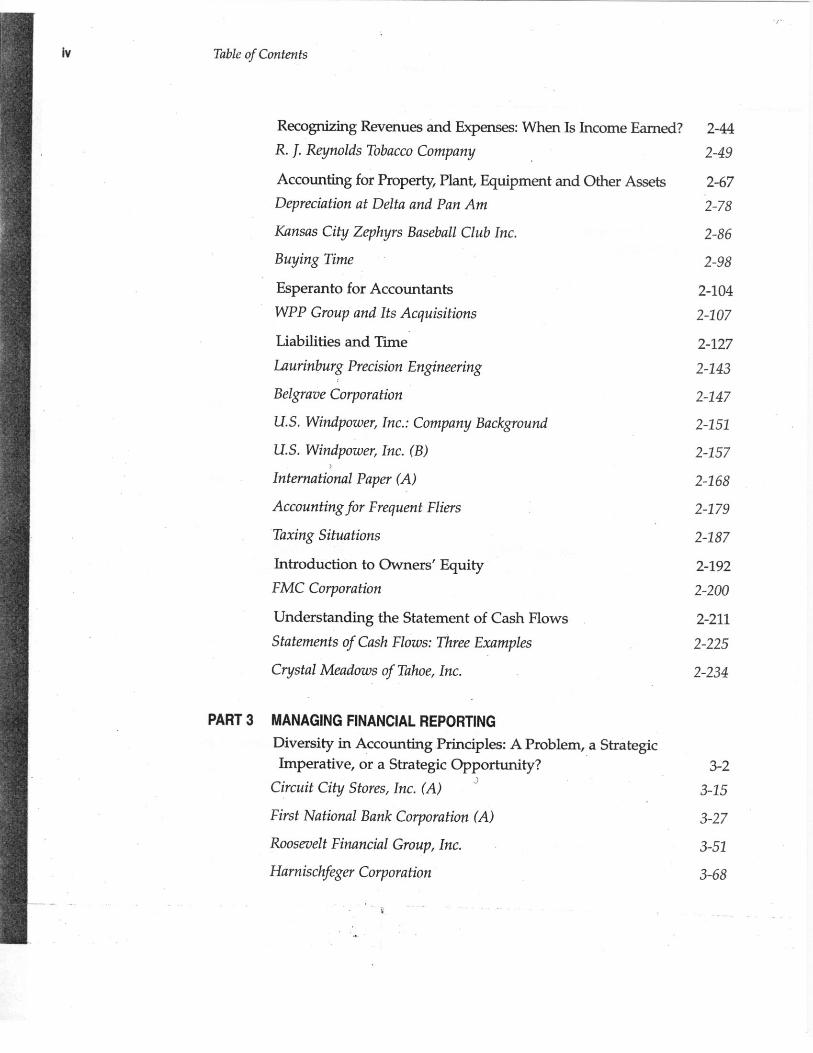

iv Table of Contents

Recognizing Revenues and Expenses: When Is Income Earned? 2-44

R. J. Reynolds Tobacco Company 2-49

Accounting for Property, Plant, Equipment and Other Assets 2-67

Depreciation at Delta and Pan Am 2-78

Kansas City Zephyrs Baseball Club Inc. 2-86

Buying Time 2-98

Esperanto for Accountants 2-104

WPP Group and Its Acquisitions 2-107

Liabilities and Time 2-127

Laurinburg Precision Engineering 2-143

Belgrave Corporation 2-147

U.S. Windpower, Inc.: Company Background 2-151

U.S. Windpower, Inc. (B) 2-157

International Paper (A) 2-168

Accounting for Frequent Fliers 2-179

Taxing Situations 2-187

Introduction to Owners' Equity 2-192

FMC Corporation 2-200

Understanding the Statement of Cash Flows 2-211

Statements of Cash Flows: Three Examples 2-225

Crystal Meadows of Tahoe, Inc. 2-234

PART 3 MANAGING FINANCIAL REPORTING

Diversity in Accounting Principies: A Problem, a Strategic

Imperative, or a Strategic Opportunity? 3-2

Circuit City Stores, Inc. (A) 3-15

First National Bank Corporation (A) 3-27

Roosevelt Financial Group, Inc. 3-51

Harnischfeger Corporation 3-68

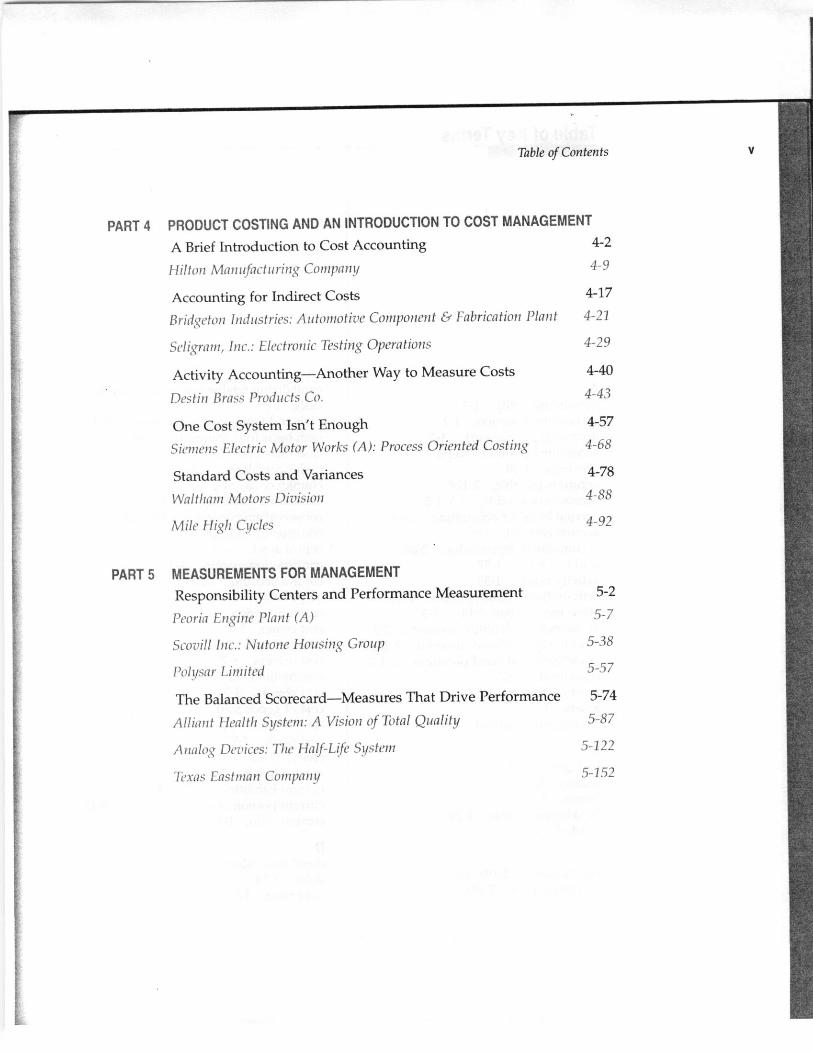

Table of Contents v

PART 4 PRODUCT COSTING AND AN INTRODUCTION TO COST MANAGEMENT

A Brief Introduction to Cost Accounting 4-2

1 ti//oit Mrztritfactoriu' Cnrrrpamrmi 4-9

Accounting for Indirect Costs 4-17

L3ridtc°toti lrtdirst ir's f1rito)notiz'e Componcrzt & Fabricatiot Plarit 4-21

Seli,i rrznt, ¡tic.: El ctroiiic Testiti Operatiotrs 429

Activity Accounting—Another Way to Measure Costs 4-40

Detiri Brass 1'rui1acts Cr. 4-43

One Cost System Isn't Enough 4-57

Sieiu e ,is Electric Motor Works (A): Procc ess Oriente ed CostinlZ 4-68

Standard Costs and Variances 4-78

Walthanr Motoors Divishu¡ 4-88

Mile FIigh Cycle 4-92

PART 5 MEASUREMENTS FOR MANAGEMENT

Responsibility Centers and Performance Measurement 5-2

1 eoria Il'iig ite Plan! (A) 5-7

Scovill ¡tic.: Nutone Housíng Group J-38

Poli/sar 1.irriitcd 5-57

The Balanced Scorecard—Measures That Drive Performance 5-74

Alliaant Heealtlr St/stt eni: A Vision nf Iota! Qualiti 5-87

Analog De°z v ices: Tlic Half-Life Systeur 5-122

Ti'ias Eastnian Conrpariii 5-752

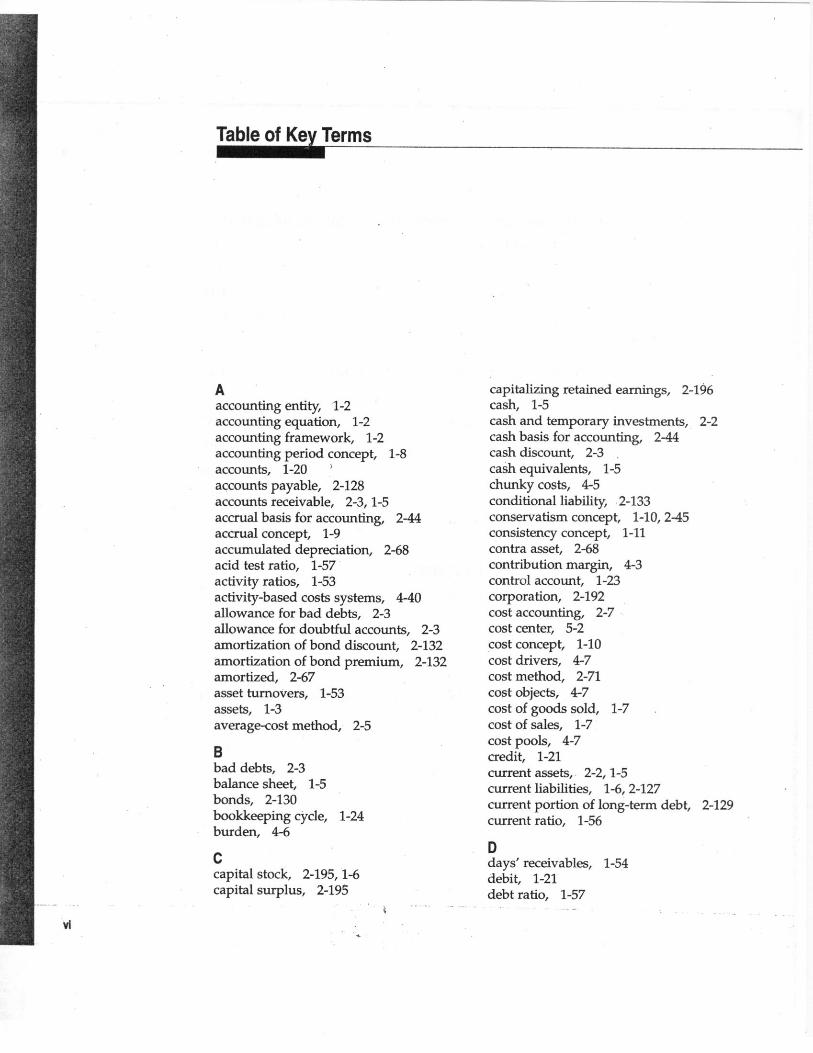

Table of Kev Terms

Aaccounting entity, 1-2accounting equation, 1-2accounting framework, 1-2accounting period concept, 1-8accounts, 1-20accounts payable, 2-128accounts receivable, 2-3, 1-5accrual basis for accounting, 2-44accrual concept, 1-9accumulated depreciation, 2-68acid test ratio, 1-57activity ratios, 1-53activity-based costs systems, 4-40allowance for bad debts, 2-3allowance for doubtful accounts, 2-3amortization of bond discount, 2-132amortization of bond premium, 2-132amortized, 2-67asset turnovers, 1-53assets, 1-3average-cost method, 2-5

Bbad debts, 2-3balance sheet, 1-5bonds, 2-130bookkeeping cycle, 1-24burden, 4-6

Ccapital stock, 2-195,1-6capital surplus, 2-195

capitalizing retained earnings, 2-196cash, 1-5cash and temporary investments, 2-2cash basis for accounting, 2-44cash discount, 2-3 .cash equivalents, 1-5chunky costs, 4-5conditional liability, 2-133conservatism concept, 1-10, 2-45consistency concept, 1-11contra asset, 2-68contribution margin, 4-3control account, 1-23corporation, 2-192cost accounting, 2-7cost center, 5-2cost concept, 1-10cost drivers, 4-7cost method, 2-71cost objects, 4-7cost of goods sold, 1-7cost of sales, 1-7cost pools, 4-7credit, 1-21current assets, 2-2, 1-5current liabilities, 1-6, 2-127current portion of long-term debt, 2-129current ratio, 1-56

Ddays' receivables, 1-54debit, 1-21debt ratio, 1-57

m

E

earnings per share, 1-52effective interest rate, 2-131entity concept, 1-10EPS, 1-52equities, 1-3equity method, 2-71esperanto, 2-104expense center, 5-2

FFIFO, 2-5financial performance center,first-in, first-out, 2-5fixed assets, 2-67foreign currency translation,

G

GAAP, 1-5general ledger, 1-20generally accepted accounting

principies, 1-5going concern, 1-10goodwill, 1-6, 2-72gross margin, 4-3

journal, 1-20

L

last-in, first-out, 2-5ledger, 1-20lessee, 2-133lessor, 2-133leverage, 1-57leveraged buyout, 2-198liabilities, 1-6liability, 2-127

current and noncurrent, 2-127

LIFO, 2-5long-term debt, 2-129long-term debts, 1-6

viiTable of Key Terms

declining balance depreciation, 2-69deferred credits, 2-128deferred taxes, 2-135depletion, 2-67depreciable cost, 2-68depreciation, 2-67direct costs, 4-6discount, 2-131dividend payout, 1-60dividend yield ratio, 1-59double entry, 1-20du Pont model, 1-60

Mmarketable securities, 1-5matching concept, 1-9, 2-44, 2-67materiality concept, 1-11mergers, 2-197minority interest in subsidiaries, 2-71money measurement concept, 1-9

5-3 Nnet earnings, 1-8net income, 1-8

2-197 noncurrent liability, 2-127nonvariable costs, 4-5normal operating cycle, 1-5notes receivable, 1-5

0

operating expenses, 1-7. operating income, 1-7overhead cost, 4-6

ppaid-in-capital in excess of par, 2-195partnership, 2-192PE, 1-59percentage-of-completion method, 2-47postretirement benefits, 2-134

2-5 premium, 2-131

2-5 prepaid expenses, 1-6, 2-7

2-5 prevailing market interest rate, 2-131price earnings ratio, 1-59product guarantees, 2-134profit center, 5-3

1

income statement, 1-7indirect costs, 4-6insolvent, 1-56inventory, 2-4, 1-5

average-cost method,first-in, first-out (FIFO),last-in, first-out (LIFO),

inventory cost flows, 2-4inventory turnover, 1-55investment centers, 5-3

Vi¡¡ Table of Key Terms

profit margin, 1-53profitability ratios, 1-50proprietorship, 2-192proven, 1-22

Qquick assets, 1-57

Rrealization concept, 1-9, 2-44realized, 2-46recognition concepts, 1-9reconciliations, 2-213residual income, 5-3responsibility centers, 4-3retained earnings, 1-6return on assets, 1-50return on equity, 1-52return on invested capital, 1-51return on investment, 1-50revenue recognition, 2-45revenue recognitiop rule, 2-46revenues, 1-7ROA, 1-50ROE, 1-52ROI, 1-50ROIC, 1-51

Ssalvage value, 2-68semivariable costs, 4-5solvency ratios, 1-56special journal, 1-22specific identification system, 2-4stated value, 2-195

statement of cash flows, 1-4, 1-8, 2-211statement of changes in financial

position, 2-219statement of earnings, 1-4statement of financial position, 1-4statement of income, 1-4step-function costs, 4-5stock distribution, 2-196stock dividends, 2-196stock splits, 2-196stockholder's equity, 1-6straight-line depreciation, 2-68subsidiary ledger, 1-23sum-of-years' digits method, 2-69

Tt account, 1-22takeovers, 2-197times interest earned, 1-58treasury stock, 2-196, 1-7trial balance, 1-22

uunearned revenue, 2-128

Vvariable costs, 4-5variances, 4-3

Wworking capital turnover, 1-56

Yyield, 2-131

e

Preface

ccounting systems, information, and reports have the potential toprovide managers with critical data and information about their organizationsand those of customers and competitors. Unfortunately, however, many man-agers never learn how to use and exploit that potential. The complexity ofmodere accounting systems and standards can be daunting in spite of the ap-parent simplicity of basic accounting frameworks. Untrained in the complexi-ties, many managers retreat from accounting, content to let the accountants dothe accounting, and never to admit their uneasiness with accounting informa-

tion and reports.Accountingfor Managers was written with the belief that managers must

learn to work with accounting and accountants, but they do not need to learnhow to be accountants themselves. Managers need to know what accountantsdo and what they do not do. They need to know the vocabulary, perspectives,and bias that underlie accounting processes and reports. Managers need toknow how to ask accountants for data and information they want, and theyneed to know how to use accounting as a strategic tool. But managers do not

need to become accountants themselves.In 1989, the faculty of the Harvard Business School established a new re-

quired course titled Financial Reporting and Management Accounting . Al-

though the charter and objectives for the course were vague, the mandato wasto create an accounting course that would focus on what accountants do andwhy they do it, rather than how they do it. The course was to focus on howmanagers could manage better because of what accountants do, and howmanagers could use accounting reports, systems, and information as effec-

tively as possible.Case studies are an ideal way to achieve these objectives because they il-

lustrate and describe what accountants do and provide a basis for discussionsabout alternatives and implications of accounting standards, procedures, andreports. Cases allow the reader to understand that accountants make choices

Ix

i

x Prcface

that determine whai information managers as well as outsiders will see andthe form it will Cake. If the manager needs other information or wants to piesena añother accounting picture, the manager needs to Interviene and to pro-vide direction through questions or requests. By doing so, the manager usesaccounting as a tool to accomplish his or her objectives.

Sor ie of the case studies in Accounting for Managers look deceptn elyeasy, while others look iinpossibly difficult. The formen are usually more com-plex than thev. look because of the nuances that underlie any accounting. Thelatter can usually be broken finto casy-to-understand parts because of thepower of the basic accounting inodels that underlie financial reporting, product costitlg, and measurements for control. The majority of cases are based oninformation gathered from actual organizations and present real problemsrxianagers had to solve.

Most case studies contain ainbiguities and complexities that preclúd.e anyyy single correct answer. Individual study of cases is best followed by small

group and class discussions. In these exchanges, learning is enhanced. Therole of the instructor or discussion leader is to assure that alternative analysesand conclusions are carefully considerad along with their imphcations. Thegoal for everyone in a case discussion shoúld:be to improve his or her abilityto approach, analyze, asid reach conclúsions about the next newspaper ormagazine storv about accounting, or the next case or problem he or she willencounter.

Accounting is too important to managers, organizations, and societies to.: Y L

rP 3be left to accountants alone. Accounting information is often a basis for deci-sions. Accounting reports are often the basis on which the effectiveness ofstewardship, decisions, and actions are evaluated. Effective managers are al-ways aware of thc potentials and problems that accountants and accouultingnroc ,ses can create. Ynur studv of this text and the case situations hérein

^, kan <

Acknowledgements

any people have helped to create and improve Accounting forManagers. More than 4,000 students in the MBA Classes of 1990, 1991, 1992,1993 and 1994 have commented, made suggestions, and corrected errors in

many of the cases and chapters that comprise this book.The colleagues with whom I have been privileged to teach this material in

a group-teaching, file-sharing environment have contributed much and havehelped to improve it. These include Mary Barth, Chuck Christenson, Julie Her-tenstein, Sharon McKinnon, Ken Merchant, Amy Sweeney, Pete Wilson andKaren Wruck (all of whom also authored material included in AccountingforManagers), as well as Marc Epstein, Dave Hawkins, Gerald Holtz, Dick Nolan

and Kiran Verma.Other faculty contributors to this book include Bob Anthony, Robin Coo-

per, Bob Kaplan, Jane Linder, Krishna Palepu, John Shank, Bob Simons, PeterTurney, and Dave Wilson. 1 appreciate their allowing me to include some of

their cases and notes.Five research associates contributed greatly to this project, and 1 acknow-

ledge the great contributions of Dave Ellison, Susan Harmeling, Terry Nichols,

Eric Petro and Marc Zablatsky.The Harvard Business School and Dean John H. McArthur provided sup-

port and a conducive environment for what has been one of the most satisfy-

ing teaching assignments of my career. Forbes and the Harvard Business

Review each agreed to allow me to reprint articles.Finally, special thanks are due to the group who helped to put this

material together. The staff of the Word Processing Center at the HarvardBusiness School provided invaluable help in making the cases and notesreadable, and their service went beyond that which I had any right toexpect. My assistant, Patty Powers, kept the project on schedule. Hercheerful acceptance of unreasonable demands for countless drafts re-vised on tight deadlines will not be forgotten. At South-Western Pub-

xi

xíi Acknowkdgements_

lishing, thecontribution of Ken Martin and Crystal Chapin also de-serve special mention.

Finally, my wife, Shay, supported this project with affection, help, andneeded criticism. She read drafts, improved presentations, contributedideas, and taught several cases to her students before making suggestionsabout how they could be iznpro ed. Her ideas are to be found throughoutthis book.

y

William j. BrunS, JrBoston, Massachusetts

f

,S

y

i

3

á

• ^ I 's" 1• ..

r1, 1 } Ly Fi F 1

1

Reviewers

The following faculty used the manuscript for this text in their

courses and provided valuable feedback:

G. Peter Wilson (Harvard)Mary E. Barth (Harvard)Amy P Sweeney (Harvard)Marc Epstein (Harvard)David F. Hawkins (Harvard)Sharon M. McKinnon (Northeastem)Kenneth Merchant (University of Southern California)Kiran Verma (University of Massachusetts—Boston)Gerald Holtz (Boston University)Julie H. Hertenstein (Northeastern)

xiii

Introduction

Accountingfor Managers is a text for managers who want to makethe most of accounting information in the business environment. It is not acomprehensive accounting text, and readers are broadly exposed to the way inwhich accountants contribute to organizations and some of the things thatevery manager should know accountants do.

WHY MANAGERS NEED TO KNOW WHAT ACCOUNTANTS DO

Accountants are the scorekeepers who observe, measure, and report on theeconomic aspects of organizations. Using the rules and procedures that havebeen developed over many years, they measure the effects of economic activi-ties. Managers have played important roles in the development of these rulesand procedures, and they will continue to do so as those principies and prac-tices evolve in the future. Managers who know something about the statusand use of accounting standards will be more effective in telling their storyand in getting the information they really need.

Account;ng is also a language system that facilitates efficient communica-tion about economic aspects of organizations between managers. Standardizedterminology developed and used by accountants facilitates discussion of complexaspects of economic conditions and the performance of organizations. Ti man-agers do not have some idea of the vocabulary and accounting methodology,communication in the organization becomes more awkward and inefficient. Inturn, the possibility of confusion or mistakes grows larger.

Copyright © 1992 by the President and Fellows of Harvard College. Harvard Business Schoolcase 192-152.

Introduction xv

Accountants maintain records that can become the basis for financial re-ports. Such reports can summarize the financial status of the organization atone or more points in time, and they may describe how the financial structureand strength of the organization has changed over a period of time.

Financial reports are important to managers for two reasons. First, they allowmanagers to evaluate how their strategies and decisions are affecting the eco-nomic status and viability of their organization. By comparing the expected re-sults to those that have been reported by accountants, managers can judge theirown success and decide whether changes in strategy or decisions are appropriatefor the future. Second, sine external parties often have interests in the financialstatus and success of organizations, financial statements are commonly used torepórt on those interests. Managers need a basic understanding of the way inwhich accountants surnmarize economic activities and prepare financial reports,so they can assess how their actions will appear to others both inside and outsideof the organization.

The structure of financial reports is part of the language that accountingbrings finto an organization. As managers try to anticipate how their decisionsmight affect the organization, the framework provided by financial reports is oftena useful way of summarizing the possible effects and consequences of actions.

Accounting records are often the most comprehensive records that any or-ganization maintains. As a result, those records can óften provide informationthat is useful to managers in trying to solve problems or in deciding between al-ternative decisions or courses of action they might take. By knowing what kind ofinformation is kept in accounting records and by knowing where it would likelybe maintained, managers can much more efficiently request needed informationand understand the proper use of that information for decisions at hand.

AN OVERVIEW OF THE TEXT

Accounting for Managers has five parts:

Part I provides an overview of accounting and financial reporting. The ac-counting framework and some accounting concepts are introduced so thatmanagers can immediately begin working with financial statements.

Part II is concerned with how accountants measure and report on assets,liabilities, and the equities different parties have in an organization. In thispart, classifications and elements of financial statements are examined sepa-rately to give managers an understanding of some of the difficulties that bothmanagers and accountants have in measuring and describing the economicsubstance of an organization.

Part III introduces the idea that managers can choose a reporting strategyin presenting their organization to those who may request and use financialstatements. A combination of accounting policies that underlie a set of finan-

í

xvi Introduction

cial statements can be desc ribed as conservative or aggressive. By taking anactive role in the financial reporting process, managers can minimize the risk

that their strategic direc tions will be misunderstood by outsiders who seek tounderstand and appraise an organization based on financial statements alone.

Part IV is concerned with procedures accountants use in estimating prod-uct costs and provides an introduction to cost management. Accounting forcosts is primarily an activity that takes place for the benefit of m anagers. Prod-uct costs are useful for pricing and product line decisions. In addition, meas-urements of product costs can be compared against expectations in determin-ing whether or not planned efficiencies have been attained.

Part V continues the emphasis begun in Part IV on useful measurementsfor managers. Because of their expertise, accountants are often called upon bymanagers to make measurements, to communicate, to motivate, and to pro-vide a basis of evaluation of parts of an organization and the products or serv-ices that it provides. The case studies in Part V illustrate how some organiza-tions have sought to improve their intemal measurement and managementsystems to benefit from their knowledge that what gets measured matters.

A BRIEF SUMMARY OF TEXT OBJECTIVES

Six objectives have guided the development and selection of the text and casestudies that comprise Accounting for Managers. When you have finished thistext, you sho?.ild:

• Be familiar with the accounting framework and how it is used in evaluatingeconomic conditions and success and in decision making in organizations.

• Have a sense for the conceptual basis of accounting as it is carried out inorganizations today.

• Be familiar with financial statements, accounting reports, and the vocabu-lary found within them.

• Have a sense for how managers use a reporting strategy in communicat-ing with each other and with parties extemal to their organiza tion.

• Understand the complexity of determining and using information on thecost of pi oducts and services produced by an organization.

• Understand the power of measurements in coordinating, mo tivating and evalu-ating the activities of employees and managers in modem organiza tions.

Some of the case studies are based on situations where managers are try-ing to solve ene or more complex problems that may not have a solution thatwill satisfy ti ie objec tives and needs of all the affected parties. In other cases,complex problems have been greatly simplified using hypothe tical situa tionsand descript ; ons to allow students to discover why problems in accountingoften demand extensive examination and discussion.

^^ 4

r