Embed Size (px)

Citation preview

Analysis of the Global Dimensional Metrology Market in the

Aerospace Industry Adoption of Large CMMs and Laser Trackers will Lead to Strong Market Growth

NC94-30

November 2013

2 NC94-30

Research Team

Aravind Govindan

Senior Research Analyst

Measurement & Instrumentation

Research Manager

Vijay Mathew

Program Manager

Measurement & Instrumentation

For more information:

Jeannette Garcia

Corporate Communications

Measurement & Instrumentation

+1.210.477.8427

Lead Analyst

3 NC94-30

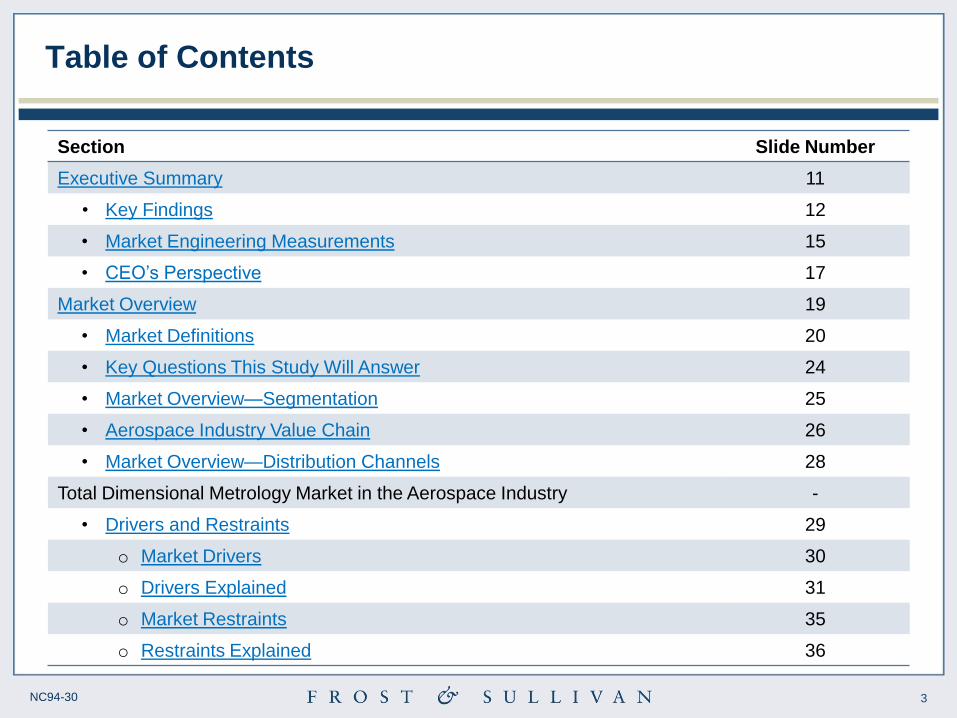

Table of Contents

Section Slide Number

Executive Summary 11

• Key Findings 12

• Market Engineering Measurements 15

• CEO’s Perspective 17

Market Overview 19

• Market Definitions 20

• Key Questions This Study Will Answer 24

• Market Overview—Segmentation 25

• Aerospace Industry Value Chain 26

• Market Overview—Distribution Channels 28

Total Dimensional Metrology Market in the Aerospace Industry -

• Drivers and Restraints 29

o Market Drivers 30

o Drivers Explained 31

o Market Restraints 35

o Restraints Explained 36

4 NC94-30

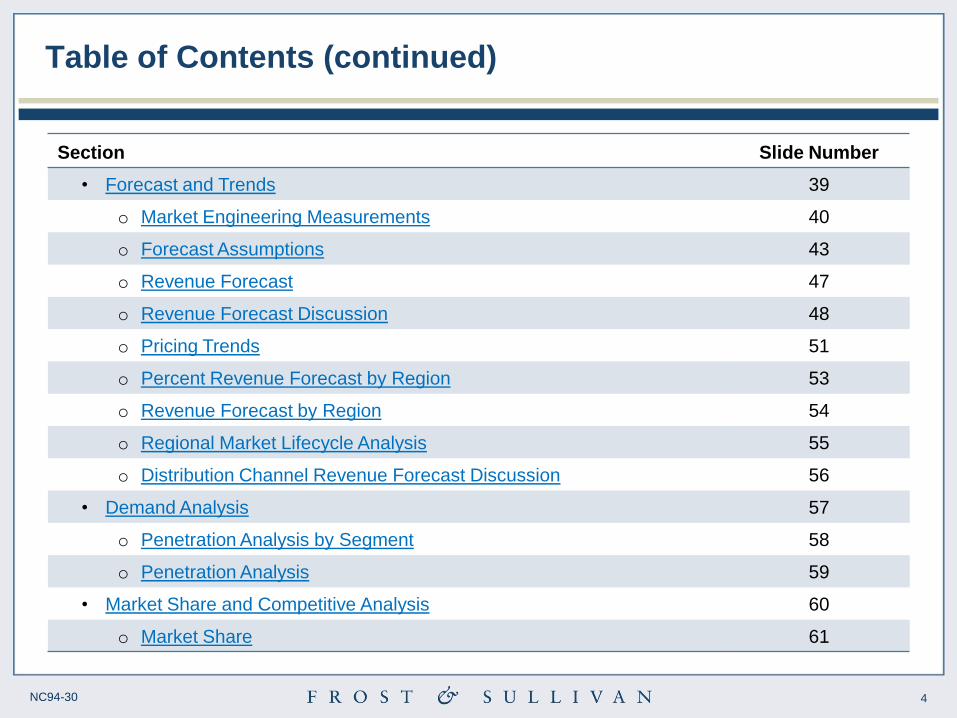

Table of Contents (continued)

Section Slide Number

• Forecast and Trends 39

o Market Engineering Measurements 40

o Forecast Assumptions 43

o Revenue Forecast 47

o Revenue Forecast Discussion 48

o Pricing Trends 51

o Percent Revenue Forecast by Region 53

o Revenue Forecast by Region 54

o Regional Market Lifecycle Analysis 55

o Distribution Channel Revenue Forecast Discussion 56

• Demand Analysis 57

o Penetration Analysis by Segment 58

o Penetration Analysis 59

• Market Share and Competitive Analysis 60

o Market Share 61

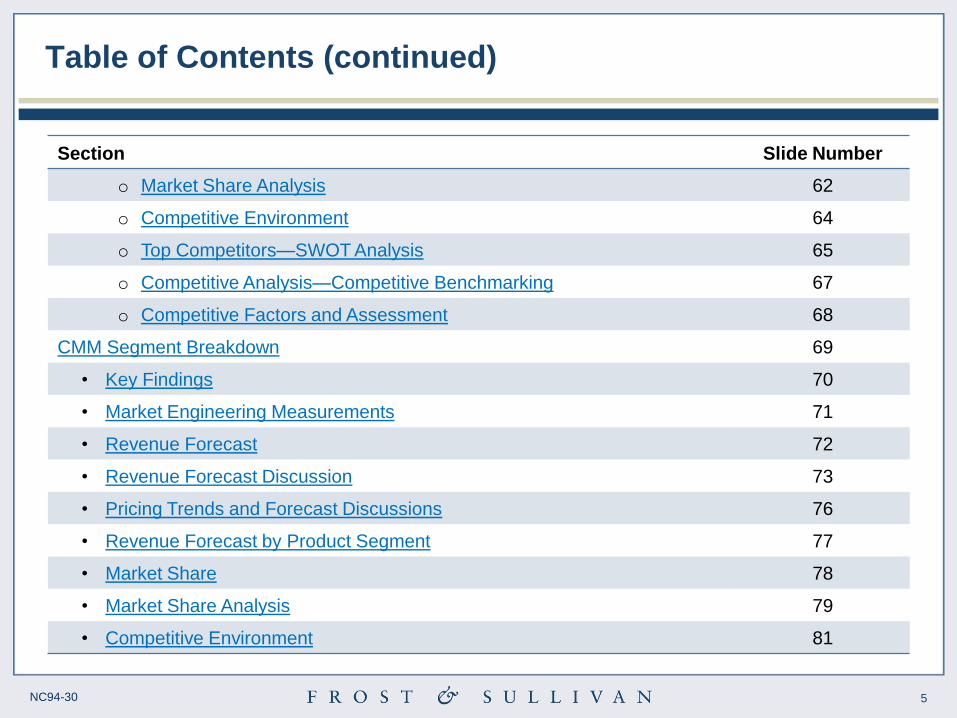

5 NC94-30

Section Slide Number

o Market Share Analysis 62

o Competitive Environment 64

o Top Competitors—SWOT Analysis 65

o Competitive Analysis—Competitive Benchmarking 67

o Competitive Factors and Assessment 68

CMM Segment Breakdown 69

• Key Findings 70

• Market Engineering Measurements 71

• Revenue Forecast 72

• Revenue Forecast Discussion 73

• Pricing Trends and Forecast Discussions 76

• Revenue Forecast by Product Segment 77

• Market Share 78

• Market Share Analysis 79

• Competitive Environment 81

Table of Contents (continued)

6 NC94-30

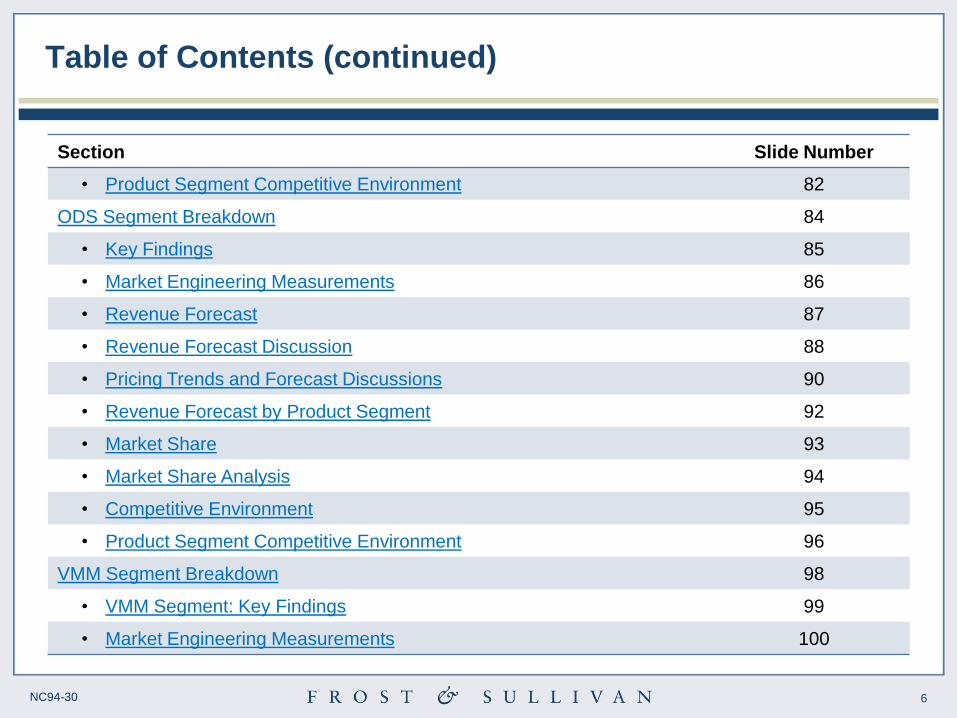

Table of Contents (continued)

Section Slide Number

• Product Segment Competitive Environment 82

ODS Segment Breakdown 84

• Key Findings 85

• Market Engineering Measurements 86

• Revenue Forecast 87

• Revenue Forecast Discussion 88

• Pricing Trends and Forecast Discussions 90

• Revenue Forecast by Product Segment 92

• Market Share 93

• Market Share Analysis 94

• Competitive Environment 95

• Product Segment Competitive Environment 96

VMM Segment Breakdown 98

• VMM Segment: Key Findings 99

• Market Engineering Measurements 100

7 NC94-30

Table of Contents (continued)

Section Slide Number

• Revenue Forecast 101

• Revenue Forecast Discussion 102

• Pricing Trends and Forecast Discussions 104

• Revenue Forecast by Product Segment 105

• Market Share 106

• Competitive Environment 107

• Product Segment Competitive Environment 108

Measurement Gages Segment Breakdown 110

• Key Findings 111

• Market Engineering Measurement 112

• Revenue Forecast 113

• Revenue Forecast Discussion 114

• Pricing Trends and Forecast Discussions 116

• Revenue Forecast by Product Segment 117

• Market Share 118

8 NC94-30

Table of Contents (continued)

Section Slide Number

• Competitive Environment 119

• Product Segment Competitive Environment 120

Key Application Area Breakdown 122

• Key Findings 124

• Market Overview- Key Application Areas Segmentation 124

• Overview of Key Application Areas 125

• Custom Solutions—Market Overview 126

• Overview of Dimensional Metrology Products for Aerostructure Application Area

127

• Market Share 129

• Market Share Analysis 130

• Framework Conceptualized by Leading Dimensional Metrology Companies 132

North America Breakdown 133

• Revenue Forecast 134

• Revenue Forecast Discussion 135

• Competitive Environment 136

9 NC94-30

Table of Contents (continued)

Section Slide Number

Europe Breakdown 137

• Revenue Forecast 138

• Revenue Forecast Discussion 139

• Competitive Environment 140

Asia-Pacific Breakdown 141

• Revenue Forecast 142

• Revenue Forecast Discussion 143

• Competitive Environment 145

Rest of World Breakdown 146

• Revenue Forecast 147

• Revenue Forecast Discussion 148

• Competitive Environment 149

The Last Word 150

• The Last Word—3 Big Predictions 151

10 NC94-30

Table of Contents (continued)

Section Slide Number

• Legal disclaimer 152

Appendix 153

• Market Engineering Methodology 154

• Additional Sources of Information 155

• List of Other Participants 156

• Learn More—Next Steps 159

11 NC94-30

Executive Summary

12 NC94-30

• In 2012, the total global dimensional metrology market in the aerospace industry

generated $482.9 million in revenue.

• The coordinate measuring machines (CMM) segment is expected to grow at a

compound annual growth rate (CAGR) of 4.0% from 2012 to 2017.

• Frost & Sullivan foresees the dimensional metrology market will gain support from the

economic revival to achieve moderate growth throughout the forecast period.

• A significant factor driving demand for the dimensional metrology market is the

increasing need for high accuracy because of growing fuel efficiency initiatives

undertaken by aerospace manufacturers.

• Key factors expected to impact demand include increasing interest of aerospace

manufacturers in building up a regional aerospace supplier base and moving aerospace

manufacturing plants to Asia-Pacific (APAC).

• A growing supplier base in the aerospace industry will likely bring in market opportunities

for the dimensional metrology market. Growing Tier II and III aerospace suppliers will

likely procure low- and mid-range priced dimensional metrology machines.

• Some key factors restraining market demand are related to limited government program

funding because of tight budgets in the aerospace industry, the wide variety of

dimensional metrology solutions available, and a slow technology adoption rate.

Key Findings

Source: Frost & Sullivan

13 NC94-30

Key Findings (continued)

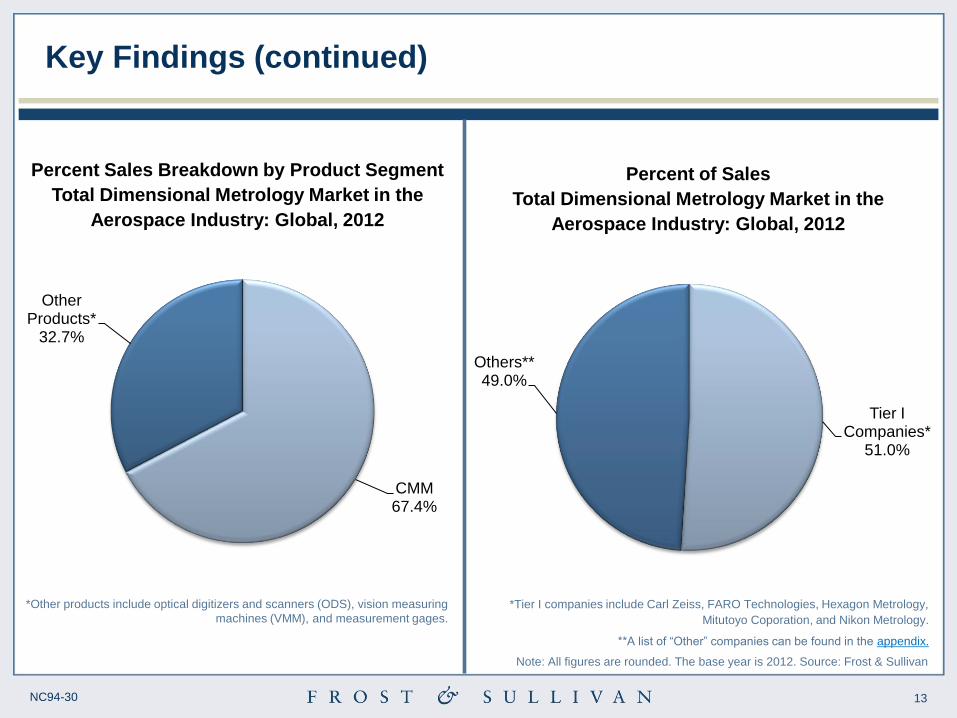

CMM 67.4%

Other Products*

32.7%

Percent Sales Breakdown by Product Segment

Total Dimensional Metrology Market in the

Aerospace Industry: Global, 2012

Tier I Companies*

51.0%

Others** 49.0%

Percent of Sales

Total Dimensional Metrology Market in the

Aerospace Industry: Global, 2012

*Tier I companies include Carl Zeiss, FARO Technologies, Hexagon Metrology,

Mitutoyo Coporation, and Nikon Metrology.

**A list of “Other” companies can be found in the appendix.

*Other products include optical digitizers and scanners (ODS), vision measuring

machines (VMM), and measurement gages.

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan

14 NC94-30

Key Findings (continued)

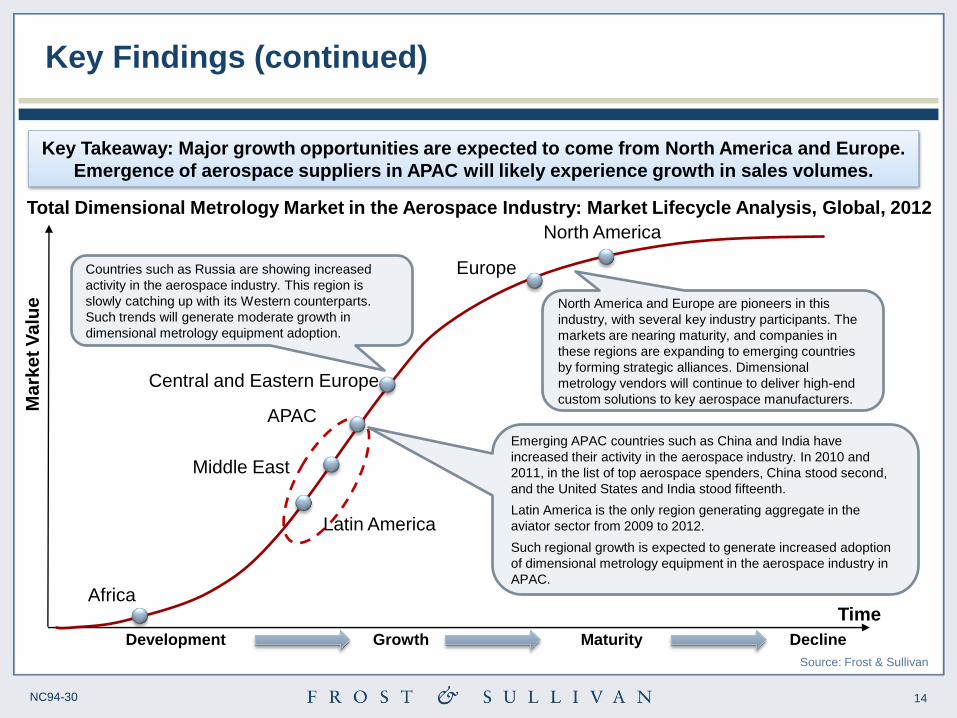

North America

Europe

Central and Eastern Europe

Middle East

Maturity Development Growth

Africa

APAC

Decline

Time

Ma

rket

Va

lue

North America and Europe are pioneers in this

industry, with several key industry participants. The

markets are nearing maturity, and companies in

these regions are expanding to emerging countries

by forming strategic alliances. Dimensional

metrology vendors will continue to deliver high-end

custom solutions to key aerospace manufacturers.

Countries such as Russia are showing increased

activity in the aerospace industry. This region is

slowly catching up with its Western counterparts.

Such trends will generate moderate growth in

dimensional metrology equipment adoption.

Latin America

Emerging APAC countries such as China and India have

increased their activity in the aerospace industry. In 2010 and

2011, in the list of top aerospace spenders, China stood second,

and the United States and India stood fifteenth.

Latin America is the only region generating aggregate in the

aviator sector from 2009 to 2012.

Such regional growth is expected to generate increased adoption

of dimensional metrology equipment in the aerospace industry in

APAC.

Total Dimensional Metrology Market in the Aerospace Industry: Market Lifecycle Analysis, Global, 2012

Key Takeaway: Major growth opportunities are expected to come from North America and Europe.

Emergence of aerospace suppliers in APAC will likely experience growth in sales volumes.

Source: Frost & Sullivan

15 NC94-30

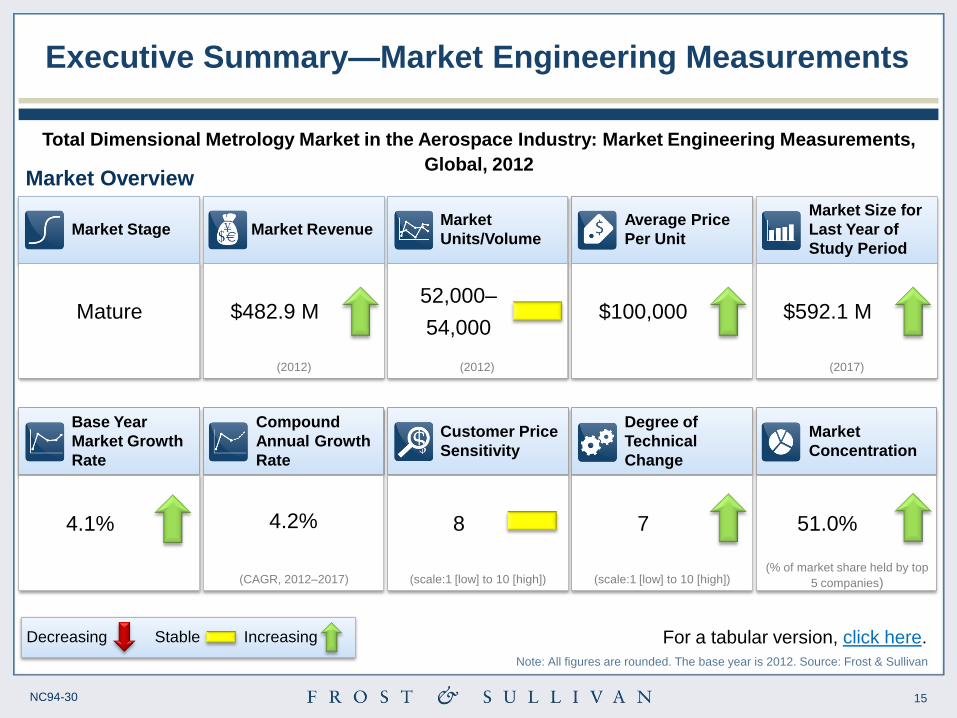

Compound

Annual Growth

Rate

4.2%

(CAGR, 2012–2017)

Market

Concentration

51.0%

(% of market share held by top

5 companies)

Executive Summary—Market Engineering Measurements

Market Stage

Mature

Market

Units/Volume

52,000–

54,000

(2012)

Average Price

Per Unit

$100,000

Market Size for

Last Year of

Study Period

$592.1 M

(2017)

Customer Price

Sensitivity

8

(scale:1 [low] to 10 [high])

Degree of

Technical

Change

7

(scale:1 [low] to 10 [high])

Market Revenue

$482.9 M

(2012)

Total Dimensional Metrology Market in the Aerospace Industry: Market Engineering Measurements,

Global, 2012

Base Year

Market Growth

Rate

4.1%

For a tabular version, click here.

Market Overview

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan

Stable Increasing Decreasing

16 NC94-30

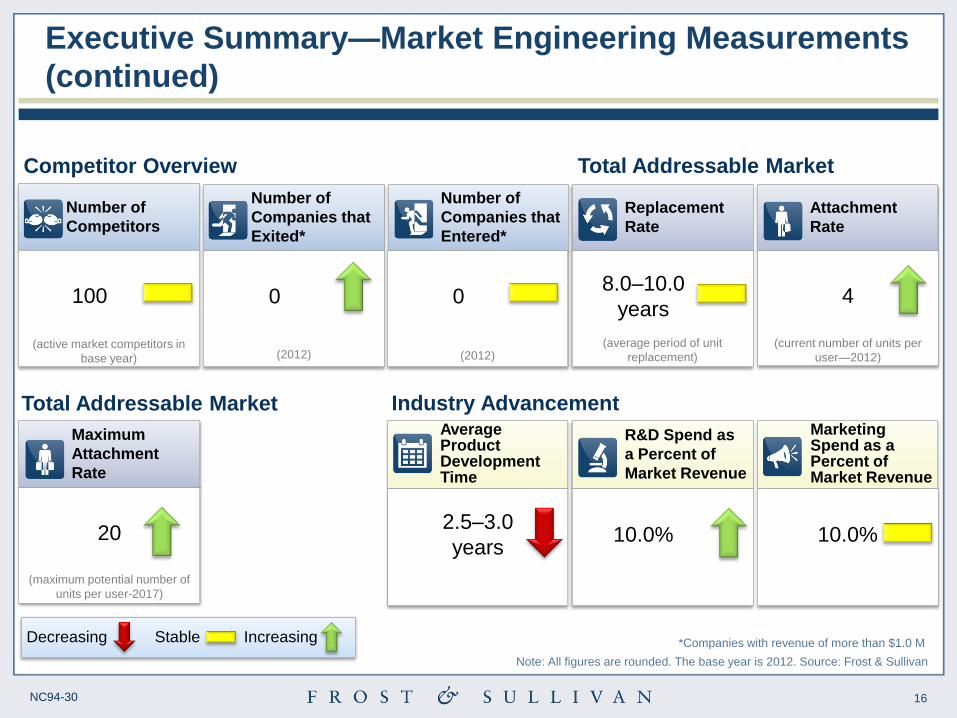

Replacement

Rate

8.0–10.0

years

(average period of unit

replacement)

Average Product Development Time

2.5–3.0

years

Number of

Companies that

Exited*

0

(2012)

Number of

Companies that

Entered*

0

(2012)

Number of

Competitors

100

(active market competitors in

base year)

Attachment

Rate

4

(current number of units per

user—2012)

Executive Summary—Market Engineering Measurements

(continued)

Competitor Overview

Total Addressable Market

Total Addressable Market

Industry Advancement Marketing Spend as a Percent of Market Revenue

10.0%

R&D Spend as

a Percent of

Market Revenue

10.0%

Maximum

Attachment

Rate

20

(maximum potential number of

units per user-2017)

*Companies with revenue of more than $1.0 M

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan

Stable Increasing Decreasing

17 NC94-30

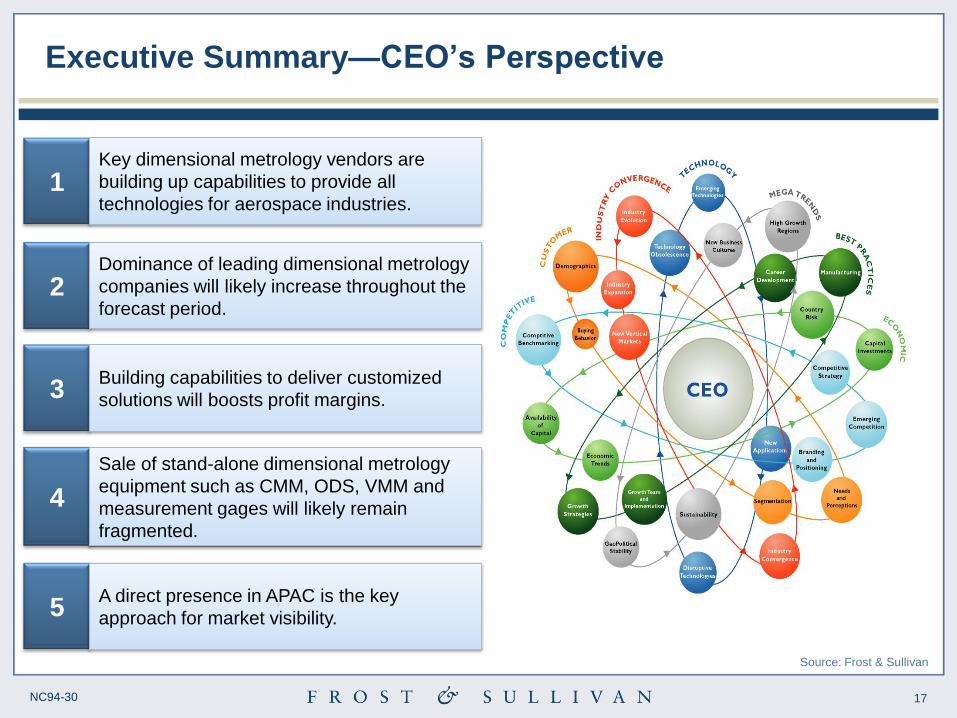

Executive Summary—CEO’s Perspective

2 Dominance of leading dimensional metrology

companies will likely increase throughout the

forecast period.

3 Building capabilities to deliver customized

solutions will boosts profit margins.

4

Sale of stand-alone dimensional metrology

equipment such as CMM, ODS, VMM and

measurement gages will likely remain

fragmented.

5 A direct presence in APAC is the key

approach for market visibility.

1 Key dimensional metrology vendors are

building up capabilities to provide all

technologies for aerospace industries.

Source: Frost & Sullivan

18 NC94-30

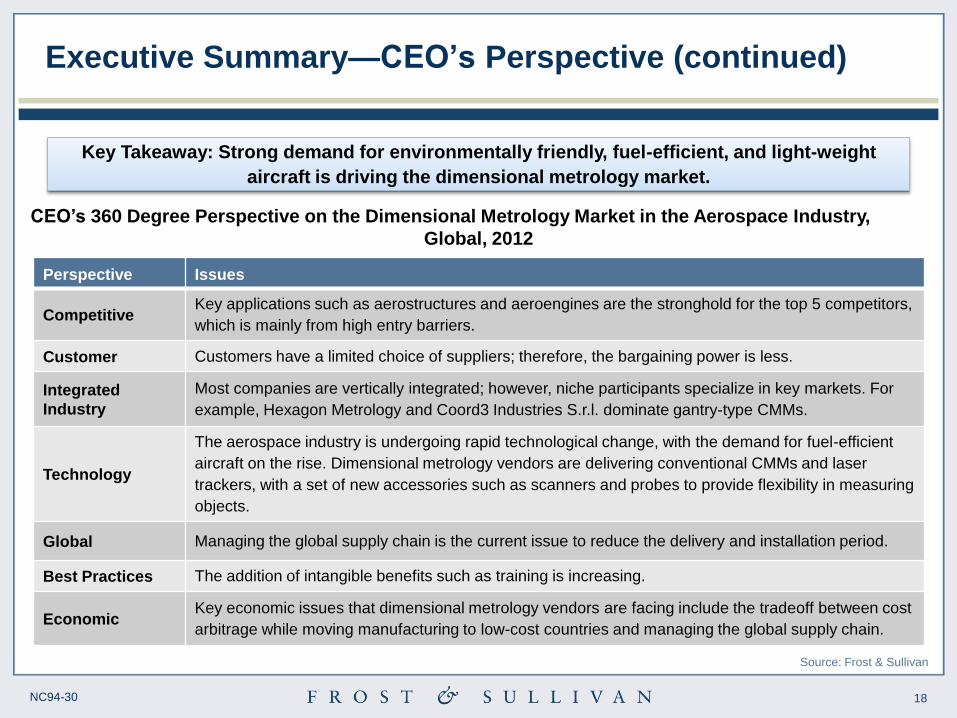

Executive Summary—CEO’s Perspective (continued)

Key Takeaway: Strong demand for environmentally friendly, fuel-efficient, and light-weight

aircraft is driving the dimensional metrology market.

CEO’s 360 Degree Perspective on the Dimensional Metrology Market in the Aerospace Industry,

Global, 2012

Perspective Issues

Competitive Key applications such as aerostructures and aeroengines are the stronghold for the top 5 competitors,

which is mainly from high entry barriers.

Customer Customers have a limited choice of suppliers; therefore, the bargaining power is less.

Integrated

Industry

Most companies are vertically integrated; however, niche participants specialize in key markets. For

example, Hexagon Metrology and Coord3 Industries S.r.l. dominate gantry-type CMMs.

Technology

The aerospace industry is undergoing rapid technological change, with the demand for fuel-efficient

aircraft on the rise. Dimensional metrology vendors are delivering conventional CMMs and laser

trackers, with a set of new accessories such as scanners and probes to provide flexibility in measuring

objects.

Global Managing the global supply chain is the current issue to reduce the delivery and installation period.

Best Practices The addition of intangible benefits such as training is increasing.

Economic Key economic issues that dimensional metrology vendors are facing include the tradeoff between cost

arbitrage while moving manufacturing to low-cost countries and managing the global supply chain.

Source: Frost & Sullivan

19 NC94-30

Market Overview

20 NC94-30

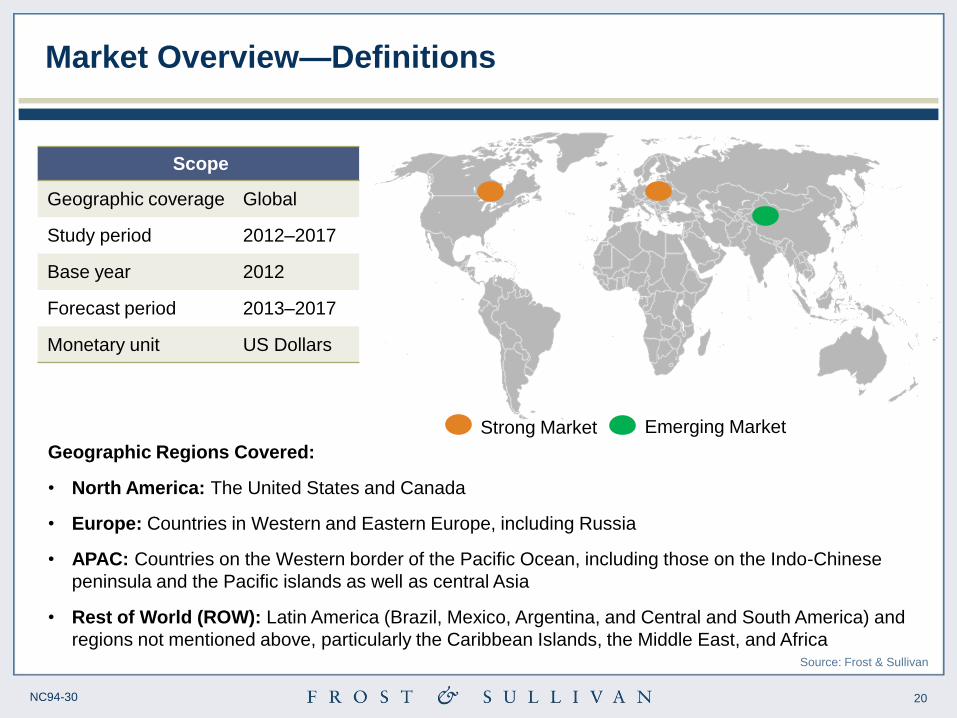

Market Overview—Definitions

Scope

Geographic coverage Global

Study period 2012–2017

Base year 2012

Forecast period 2013–2017

Monetary unit US Dollars

Geographic Regions Covered:

• North America: The United States and Canada

• Europe: Countries in Western and Eastern Europe, including Russia

• APAC: Countries on the Western border of the Pacific Ocean, including those on the Indo-Chinese

peninsula and the Pacific islands as well as central Asia

• Rest of World (ROW): Latin America (Brazil, Mexico, Argentina, and Central and South America) and

regions not mentioned above, particularly the Caribbean Islands, the Middle East, and Africa

Strong Market Emerging Market

Source: Frost & Sullivan

21 NC94-30

Market Overview—Definitions (continued)

Coordinate Measuring Machines (CMM)

• Bridge-type machines have a horizontal frame supported by 2 vertical columns. The machine arm is

vertically suspended to measure the work piece.

• Gantry-type machines have housing that covers the entire structure, which must be measured,

inspected, or scanned. This machine is well suited for inspection applications in the automotive,

aerospace, and heavy transportation industries.

• Horizontal arm machines have flexible, vertical support and a horizontal arm that supports the probe.

• Articulated arm machines are portable devices with articulated or multi-axis arms. The probes can be

placed in different directions, which increases flexibility.

Optical Digitizers and Scanners (ODS)

• 3D Laser Scanners: The basic function of laser scanners is the complete imaging of an object to obtain

many coordinate points that are used in the reconstruction of the image in 3 dimensions. The main

components include a scan head and a platform for movement along directions that are integrated

together by manufacturers. With the required software, the inspection is performed after mounting the

object on a rotary table. Laser scanners can be used alone or in conjunction with fixed CMMs or portable

arms. Each configuration has its own specific applications that take into account its capabilities.

• Laser Trackers: According to the working principle of a laser tracker, the system transmits a laser signal

to a target that is retroreflective, meaning it reflects light back to its source with limited scattering and is

held against the object that is to be measured. The reflected light repeats the same path and reenters the

tracker, which helps to calculate the distance using an interferometer. Source: Frost & Sullivan

22 NC94-30

Market Overview—Definitions (continued)

• Laser trackers are used primarily for distance measurement by collecting coordinate data, which in turn

creates an accurate replicate on a local coordinate system. Hence, the laser tracker is often used in

multiple positions to gather information about the required object.

• White Light Scanners: Operating on the basis of white light interferometry, a white light scanner is used

to note a series of data points across the vertical axis. Both the shape and phase of the interferogram

are used to determine the object's physical geometrical features. Applying Fourier analysis to the data

converts it into the spatial frequency domain, making it possible to create an accurate representation.

Unlike CMMs, a main advantage of white light scanners is that the information generated can be used

without the need for data handling by experts. However, these scanners have limitations such as the

long duration needed to complete measurements, especially when using software to process the image.

Vision Measuring Machines (VMM)

• Measuring Microscopes: These microscopes are the oldest optical measurement systems worldwide.

They are constructed using 2 compound microscopes to perform both 2- and 3-dimensional (3D)

measurements. Initially an analog instrument, today’s technological advancement has led to an

interfacing with computers for better analysis.

• Profile Projectors: These projectors are the most common piece of vision equipment with a simple

design. The image of the examined object is projected onto a screen with a 2-dimensional (2D) axis for

measurements and for reference. Profile projectors can be classified as horizontal or vertical, depending

if the line of vision is parallel or perpendicular to the ground.

Source: Frost & Sullivan

23 NC94-30

Market Overview—Definitions (continued)

• Multi-sensor Systems: The working principle behind such systems involves measuring the test piece by

means of different probes, both contact and non contact. With instant capture and analysis using the most

advanced video systems, multi-sensor systems can be categorized into manual and automated systems.

The automated systems use computer numeric control (CNC) to make automatic measurements.

Measurement Gages

• Height Gage: A typical height gage has a vertical column attached to a flexible unit. The protruding arm

measures the work piece. Different types of height gages include vernier, dial, digital dial, and electronic

digital. Typical accessories for a height gage include riser blocks, scribers, probes, software, and granite

surface probes. A height gage can be used in several applications that range from a mere go/no-go type of

application to mapping a complex part.

• Plug and Bore Gage: Plug gages are preferred when volumes are high and tolerances are tighter. Two

kinds of gages include adjustable capacity and fixed size. Plug gages are known for their repeatability and

resistance to wear, and they are best when used with electronic data collection systems. Adjustable bore

gages are preferred by end users because of cost.

• Ring Gage: These gages are cylindrical measuring devices whose primary applications include measuring

size and roundness of the workpiece and as a reference point completing other measuring devices.

• Depth Gage: These gages are used to measure the depth of holes, cavities, and/or other parts. Depth gage

configurations include dial, digital, depth micrometer, thread, flush pin gages, and vernier.

Key Applications

This segment includes a detailed analysis of key application areas such as aerostructures and aeroengines.

Source: Frost & Sullivan

24 NC94-30

Market Overview—Key Questions This Study Will Answer

Is the market growing, how long will it continue to grow, and at what rate?

Which of the dimensional metrology market segments is presenting major growth opportunities?

What are the latest key technological trends present in the global dimensional metrology market in

the aerospace industry? What impact do these trends have on the industry?

How will the structure of the market change with time?

Are the products/services offered today meeting customer needs, or is there additional development

needed?

Are the vendors in the space ready to go it alone, or do they need partnerships to take their

business to the next level?

Source: Frost & Sullivan

25 NC94-30

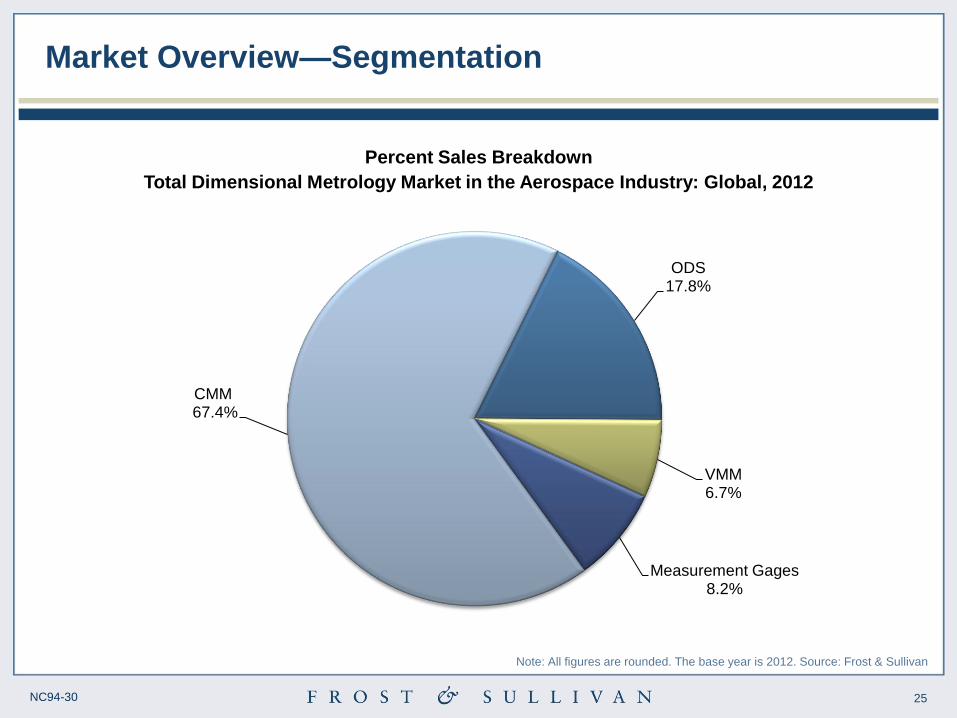

Market Overview—Segmentation

CMM 67.4%

ODS 17.8%

VMM 6.7%

Measurement Gages 8.2%

Percent Sales Breakdown

Total Dimensional Metrology Market in the Aerospace Industry: Global, 2012

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan

26 NC94-30

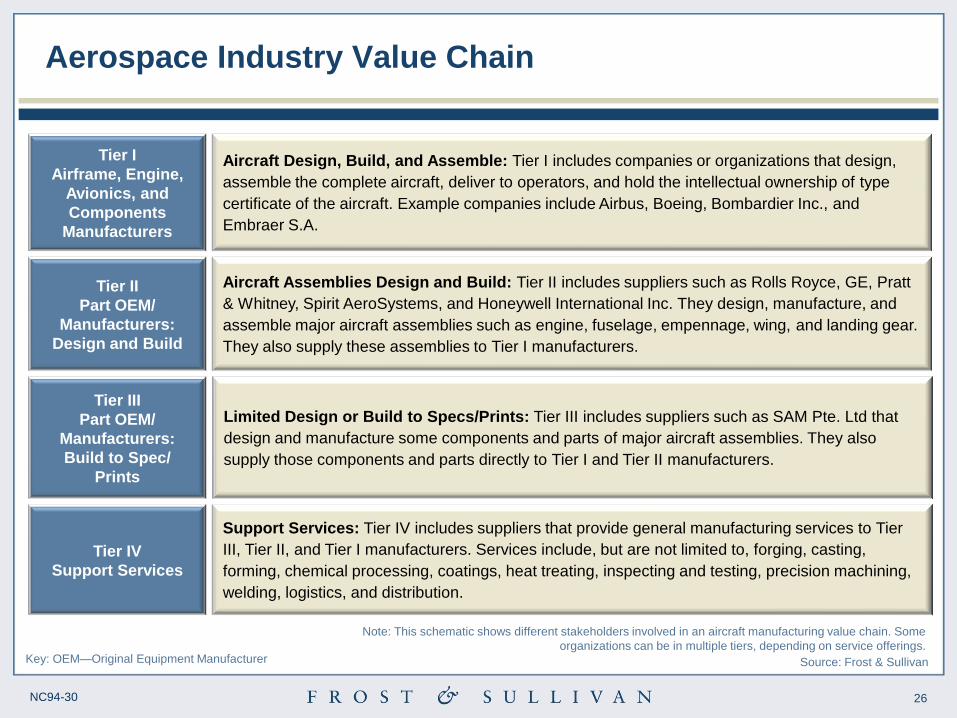

Aerospace Industry Value Chain

Aircraft Design, Build, and Assemble: Tier I includes companies or organizations that design,

assemble the complete aircraft, deliver to operators, and hold the intellectual ownership of type

certificate of the aircraft. Example companies include Airbus, Boeing, Bombardier Inc., and

Embraer S.A.

Tier I

Airframe, Engine,

Avionics, and

Components

Manufacturers

Support Services: Tier IV includes suppliers that provide general manufacturing services to Tier

III, Tier II, and Tier I manufacturers. Services include, but are not limited to, forging, casting,

forming, chemical processing, coatings, heat treating, inspecting and testing, precision machining,

welding, logistics, and distribution.

Tier IV

Support Services

Tier II

Part OEM/

Manufacturers:

Design and Build

Aircraft Assemblies Design and Build: Tier II includes suppliers such as Rolls Royce, GE, Pratt

& Whitney, Spirit AeroSystems, and Honeywell International Inc. They design, manufacture, and

assemble major aircraft assemblies such as engine, fuselage, empennage, wing, and landing gear.

They also supply these assemblies to Tier I manufacturers.

Tier III

Part OEM/

Manufacturers:

Build to Spec/

Prints

Limited Design or Build to Specs/Prints: Tier III includes suppliers such as SAM Pte. Ltd that

design and manufacture some components and parts of major aircraft assemblies. They also

supply those components and parts directly to Tier I and Tier II manufacturers.

Note: This schematic shows different stakeholders involved in an aircraft manufacturing value chain. Some

organizations can be in multiple tiers, depending on service offerings. Key: OEM—Original Equipment Manufacturer Source: Frost & Sullivan

27 NC94-30

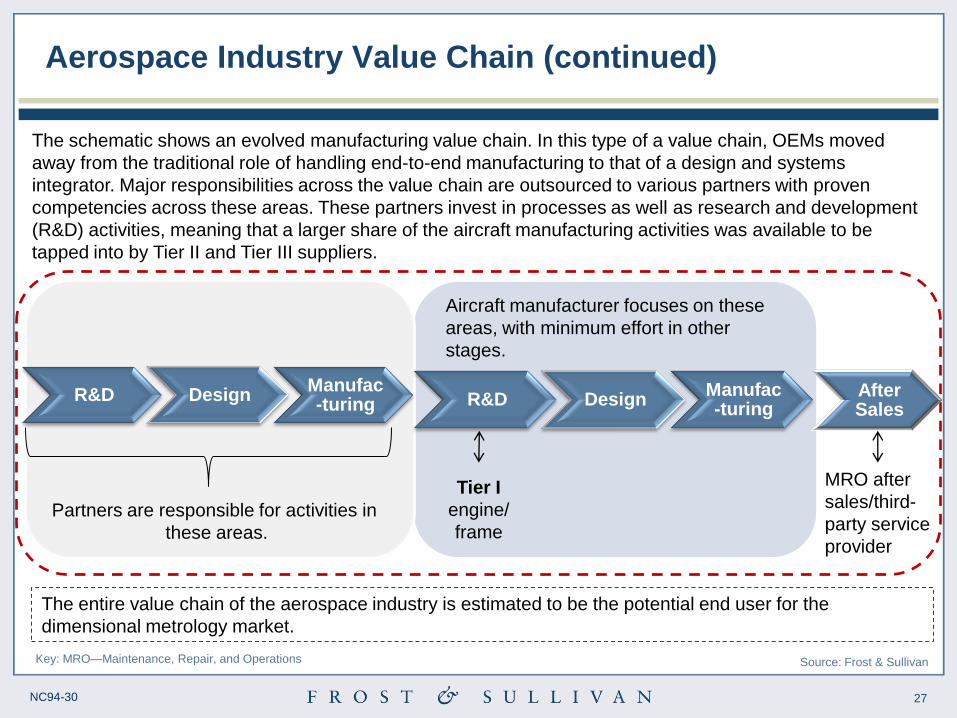

Aerospace Industry Value Chain (continued)

R&D Design Manufac-turing

Partners are responsible for activities in

these areas.

R&D Design Manufac-turing

Tier I

engine/

frame

Aircraft manufacturer focuses on these

areas, with minimum effort in other

stages.

After Sales

MRO after

sales/third-

party service

provider

The entire value chain of the aerospace industry is estimated to be the potential end user for the

dimensional metrology market.

The schematic shows an evolved manufacturing value chain. In this type of a value chain, OEMs moved

away from the traditional role of handling end-to-end manufacturing to that of a design and systems

integrator. Major responsibilities across the value chain are outsourced to various partners with proven

competencies across these areas. These partners invest in processes as well as research and development

(R&D) activities, meaning that a larger share of the aircraft manufacturing activities was available to be

tapped into by Tier II and Tier III suppliers.

Key: MRO—Maintenance, Repair, and Operations Source: Frost & Sullivan

28 NC94-30

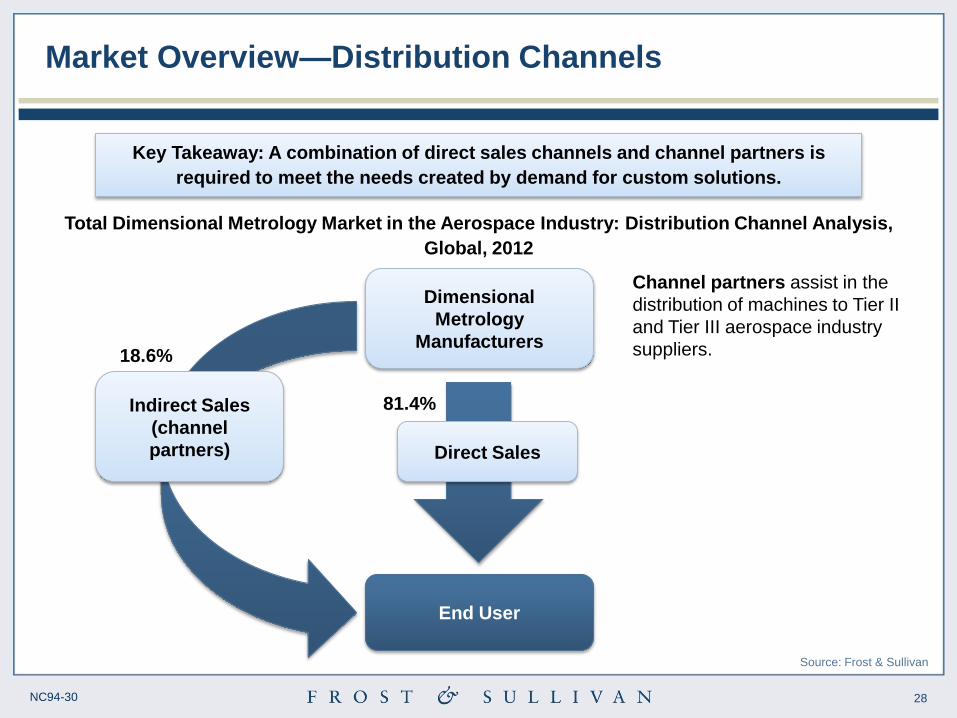

Market Overview—Distribution Channels

Dimensional

Metrology

Manufacturers

End User

Indirect Sales

(channel

partners) Direct Sales

Total Dimensional Metrology Market in the Aerospace Industry: Distribution Channel Analysis,

Global, 2012

81.4%

Key Takeaway: A combination of direct sales channels and channel partners is

required to meet the needs created by demand for custom solutions.

18.6%

Channel partners assist in the

distribution of machines to Tier II

and Tier III aerospace industry

suppliers.

Source: Frost & Sullivan

29 NC94-30

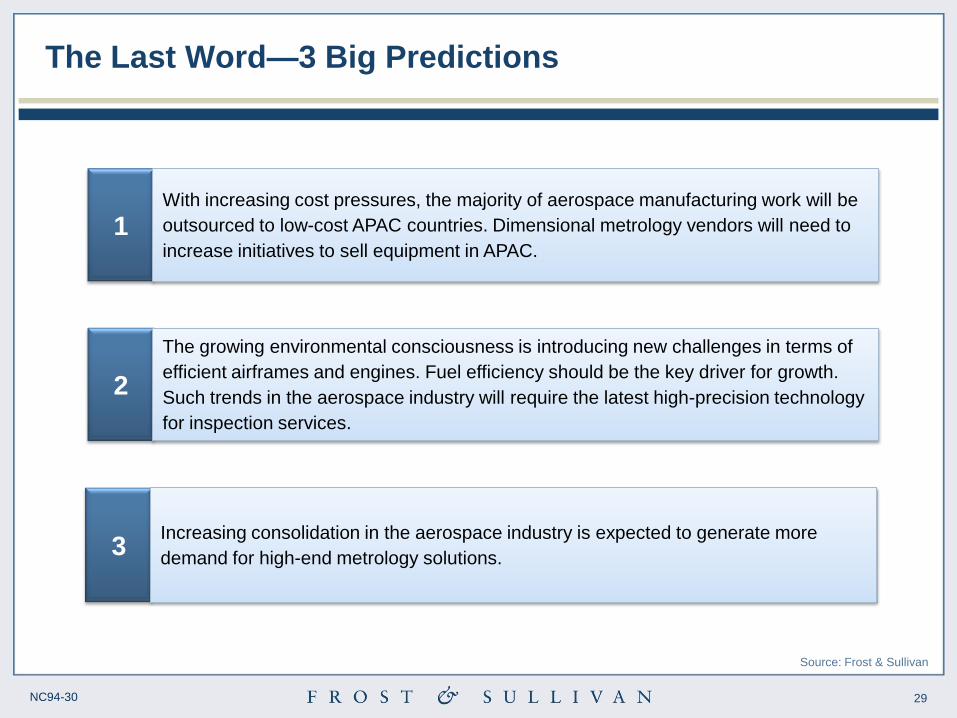

The Last Word—3 Big Predictions

2

The growing environmental consciousness is introducing new challenges in terms of

efficient airframes and engines. Fuel efficiency should be the key driver for growth.

Such trends in the aerospace industry will require the latest high-precision technology

for inspection services.

3 Increasing consolidation in the aerospace industry is expected to generate more

demand for high-end metrology solutions.

1 With increasing cost pressures, the majority of aerospace manufacturing work will be

outsourced to low-cost APAC countries. Dimensional metrology vendors will need to

increase initiatives to sell equipment in APAC.

Source: Frost & Sullivan

30 NC94-30

Legal Disclaimer

Frost & Sullivan takes no responsibility for any incorrect information supplied to us by

manufacturers or users. Quantitative market information is based primarily on interviews and

therefore is subject to fluctuation. Frost & Sullivan research services are limited publications

containing valuable market information provided to a select group of customers. Our

customers acknowledge, when ordering or downloading, that Frost & Sullivan research

services are for customers’ internal use and not for general publication or disclosure to third

parties. No part of this research service may be given, lent, resold or disclosed to

noncustomers without written permission. Furthermore, no part may be reproduced, stored in

a retrieval system, or transmitted in any form or by any means, electronic, mechanical,

photocopying, recording or otherwise, without the permission of the publisher.

For information regarding permission, write to:

Frost & Sullivan

331 E. Evelyn Ave. Suite 100

Mountain View, CA 94041

31 NC94-30

Appendix

32 NC94-30

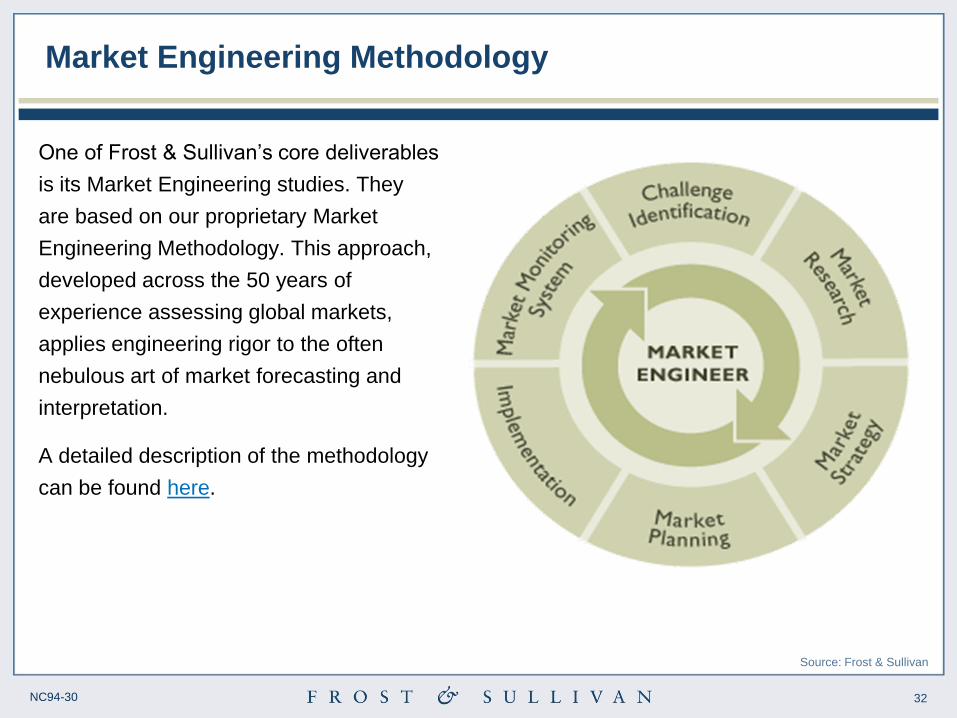

Market Engineering Methodology

One of Frost & Sullivan’s core deliverables

is its Market Engineering studies. They

are based on our proprietary Market

Engineering Methodology. This approach,

developed across the 50 years of

experience assessing global markets,

applies engineering rigor to the often

nebulous art of market forecasting and

interpretation.

A detailed description of the methodology

can be found here.

Source: Frost & Sullivan

33 NC94-30

Additional Sources of Information

Recently published deliverables in the dimensional metrology market

• Analysis of the Global Metrology Services Market

• Analysis of the Global Laser Micrometry Market

• Metrology Market for Automotive Applications

• Analysis of Vision Measuring Machines Market

• World Metrology Software Market

• World Coordinated Measuring Machines Market

• Analysis of the Dimensional Metrology Market in Emerging Economies

• Analysis of the Global Dimensional Metrology Market in the Medical Device Industry

Upcoming deliverables expected to be published in 2013

• Analysis of the Dimensional Metrology Probes and Scanners Market

• Analysis of Global Measurement Gages Market

Source: Frost & Sullivan

34 NC94-30

Learn More—Next Steps

• Talk to an analyst

• Take our DNA Survey

• Arrange a Growth Workshop

• Explore the Growth Excellence Matrix 2.0

Source: Frost & Sullivan