Embed Size (px)

Citation preview

1

VISUALIZING MACHINE LEARNING

PYCON 2017, DELHI

INCREASINGLY, OUR BEST MODELS ARE BLACK-BOX

3

TELECOM CHURN

“Churn of customers is a

particularly severe problem in

the telecom industry.

The challenge is to identify

the propensity of churn up to

a month in advance, even

before a customer moves out,

so that proactive

interventions can begin”

4

OK

WASTED

Marketing cost

Rs 40

MISSED

Acquisition cost

Rs 80OK

No churn Churn

No

ch

urn

Ch

urn

Prediction

Act

ual

8.3% 0.0%

MISSED WASTED

6.61

COST PER CUST.

0.0%

IMPROVEMENT

Base

MODELS

5

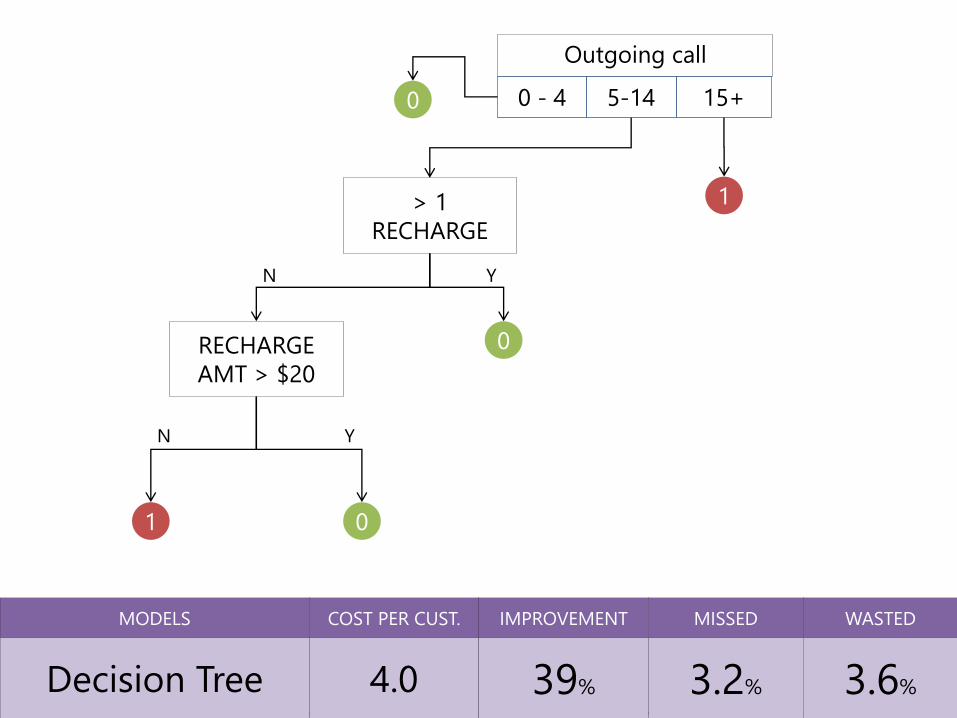

Outgoing call

0 0 - 4 15+5-14

1

RECHARGE

AMT > $20

01

YN

> 1

RECHARGE

0

N Y

3.2% 3.6%

MISSED WASTED

4.0

COST PER CUST.

39%

IMPROVEMENT

Decision Tree

MODELS

60.6% 2.5%

MISSED WASTED

2.21

COST PER CUST.

66%

IMPROVEMENT

SVM

MODELS

OK

WASTED

Marketing

cost

$1.8

MISSED

Acquisition

cost

$4.1

OK

No churn ChurnN

o c

hu

rnC

hu

rnPrediction

Act

ual

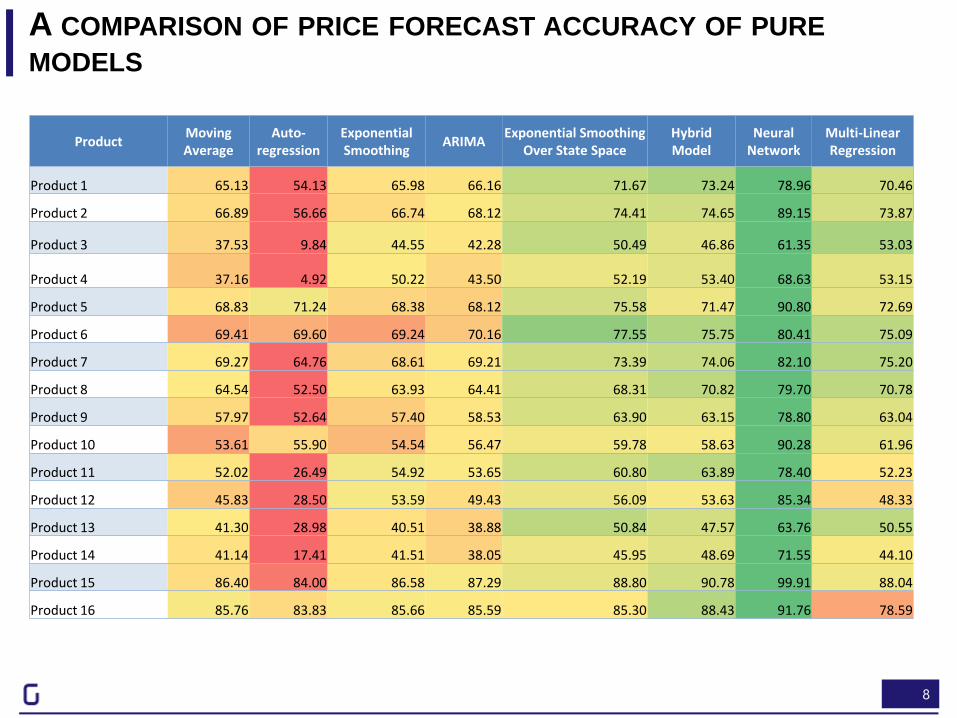

PRICE FORECASTING FOR AN

ASIAN AGRICULTURAL ENTERPRISE

Problem Approach Outcome

A Gramener Advanced Analytics Case Study

A leading agricultural

enterprise wanted price

forecasts for their products in

order to plan inventory

release to optimise revenue.

Incorrect timing was leading

either to loss of revenue or

unsold inventory.

Gramener applied a suite of

price forecasting models

based on internal and

external factors.

The models were evaluated

on multiple test datasets to

select one that minimised

median absolute deviation.

The model was able to

forecast the price to an

accuracy of 88%.

Within the first quarter of

deploying the model, the

revenue uplift attributable

directly to pricing was +3.2%.

8

A COMPARISON OF PRICE FORECAST ACCURACY OF PURE

MODELS

ProductMoving Average

Auto-regression

Exponential Smoothing

ARIMAExponential Smoothing

Over State SpaceHybridModel

Neural Network

Multi-Linear Regression

Product 1 65.13 54.13 65.98 66.16 71.67 73.24 78.96 70.46

Product 2 66.89 56.66 66.74 68.12 74.41 74.65 89.15 73.87

Product 3 37.53 9.84 44.55 42.28 50.49 46.86 61.35 53.03

Product 4 37.16 4.92 50.22 43.50 52.19 53.40 68.63 53.15

Product 5 68.83 71.24 68.38 68.12 75.58 71.47 90.80 72.69

Product 6 69.41 69.60 69.24 70.16 77.55 75.75 80.41 75.09

Product 7 69.27 64.76 68.61 69.21 73.39 74.06 82.10 75.20

Product 8 64.54 52.50 63.93 64.41 68.31 70.82 79.70 70.78

Product 9 57.97 52.64 57.40 58.53 63.90 63.15 78.80 63.04

Product 10 53.61 55.90 54.54 56.47 59.78 58.63 90.28 61.96

Product 11 52.02 26.49 54.92 53.65 60.80 63.89 78.40 52.23

Product 12 45.83 28.50 53.59 49.43 56.09 53.63 85.34 48.33

Product 13 41.30 28.98 40.51 38.88 50.84 47.57 63.76 50.55

Product 14 41.14 17.41 41.51 38.05 45.95 48.69 71.55 44.10

Product 15 86.40 84.00 86.58 87.29 88.80 90.78 99.91 88.04

Product 16 85.76 83.83 85.66 85.59 85.30 88.43 91.76 78.59

WE NEED A WAY OF

UNDERSTANDING BLACK-BOX MODELS

LET’S EXPLORE ONE BLACK-BOX

MODELK-MEANS CLUSTERING

WE UNDERSTAND THROUGH

VISUAL SUMMARIES

12

SEGMENTING INDIA’S DISTRICTS BASED ON BEHAVIOUR

Previously, the client was treating contiguous regions as a

homogenous entity, from a channel content perspective.

To deliver targeted content, we divided India into 6

clusters based on their demographic behaviour.

Specifically, three composite indices were created based

on the economic development lifecycle:

• Education (literacy, higher education) that leads to...

• Skilled jobs (in mfg or services) that leads to...

• Purchasing power (higher income, asset ownership)

Districts were divided (at the average cut-off) by:

Offering targeted content to these clusters will reach a

more homogenous demographic population.

Skilled

Poorer Richer

Unskilled Skilled

Uneducated Educated Uneducated Educated

Unskilled

Purchasing power

Skilled jobs

Education

Poor Breakout Aspirant Owner Business Rich

PoorRural, uneducated agri

workers. Young population

with low income and asset

ownership. Mostly in Bihar,

Jharkhand, UP, MP.

BreakoutRural, educated agri workers

poised for skilled labour.

Higher asset ownership. Parts

of UP, Bihar, MP.

AspirantRegions with skilled labour

pools but low purchasing

power. Cusp of economic

development. Mostly WB,

Odisha, parts of UP

OwnerRegions with unskilled labour

but high economic prosperity

(landlords, etc.) Mostly AP,

TN, parts of Karnataka,

Gujarat

BusinessLower education but working

in skilled jobs, and

prosperous. Typical of

business communities. Parts

of Gujarat, TN, Urban UP,

Punjab, etc

RichUrban educated

population

working in skilled

jobs. All metros,

large cities, parts

of Kerala, TN

The 6 clusters are

13

How to classify clients by behaviour

Using customers’ ad spend patterns, categories of

purchase, periodicity, price points and impact,

Gramener accurately classified clients to

1. Offer personalised deals

2. Create new products

Big buyers across categories at

low price points

P&GCadbury

Reckitt

HUL1

Big buyers across categories

with better price & viewership

Godrej L’OrealITC GSK J&J

Amazon Coke

2

Mid-buyers across categories

with avg price & viewership

4

Heinz AppleFuture GroupLIC Ford Amul

Large clientsMedium clientsSmall clientsTiny clients

Size legend

Each box contains a

cluster of advertisers

with similar behaviour

FMCG

Auto

Telecom

E-commerce

Electronics

Retail

BFSI

Infrequent Hindi Movie ads in

regular slots at high price

5

Getit TVS QuickrLenovo HPAircelAxis MRFMicrosoft ICICI Ceat

Motorola

Infrequent Hindi GEC advts

with high TVR/ very low price

6

Saavn Voltas PNB

Birla SunlifeJivraj Tea Pitambari

Summercool Home Appliances

Frequent regional channel ads

with low viewership

7PepperfryShoppers Stop

Bank of Maharashtra

Raja Biscuits

Cookme Spices

Pran Foods

Dipros

Metro Dairy

Koel Fashions

Meghbela

Big buyers across categories

with low regional advertising

3

NestleMaruti AirtelOLX Samsung

Dabur

Occasional Hindi GEC advts at

moderate price points

United Biscuits8

Expedia

BigBasketSulekha

Union Bank

Yes Bank Piaggio

BMW

Hitachi

Occasional regional and Hindi

GEC ads at high price

9

PayTMFranklin Templeton

Duroflex

Mother’s Recipe

Anchor Electricals

AdvertiserClustering

Transform variables to

minimize correlation

Cluster customers to

minimise overlap

Profile clusters to interpret

their characteristics

WE UNDERSTAND BY

ABSTRACTIONS

15

16

LET’S EXAMINE CURRENCY FORECASTS

17

68% correlation

between AUD & EUR

Plot of 6 month daily

AUD - EUR values

Block of correlated

currencies

… clustered

hierarchically

WHAT YOU SHOULD TAKE AWAY

BLACK-BOX MODELS ARE

INCREASINGLY ACCURATE

BLACK-BOX MODELS NEED

INTERPRETATION (EVEN

MORE)

BUILD VISUAL SUMMARIES TO

EXPLAIN MODELS

MOVE UP & DOWN THE

LADDER OF ABSTRACTION

TOOLS ARE LESS IMPORTANT THAN TECHNIQUE

19

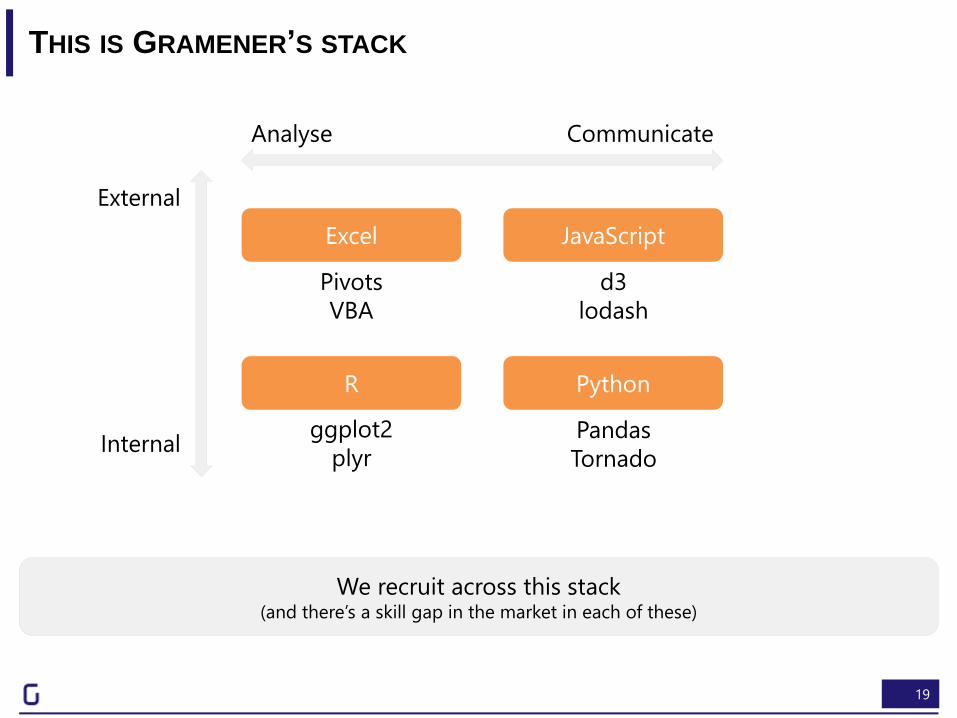

THIS IS GRAMENER’S STACK

PythonR

JavaScriptExcel

Pandas

Tornado

d3

lodash

Pivots

VBA

ggplot2

plyr

Analyse Communicate

External

Internal

We recruit across this stack(and there’s a skill gap in the market in each of these)