Embed Size (px)

Citation preview

Improving the view of thin file customers

Frans Potgieter

Alternative Data in Credit Risk

SEPTEMBER 2016

Agenda

Definitions

Thin File Population

Alternative Data Sources

Case Studies

3 | © TransUnion. LLC All Rights Reserved

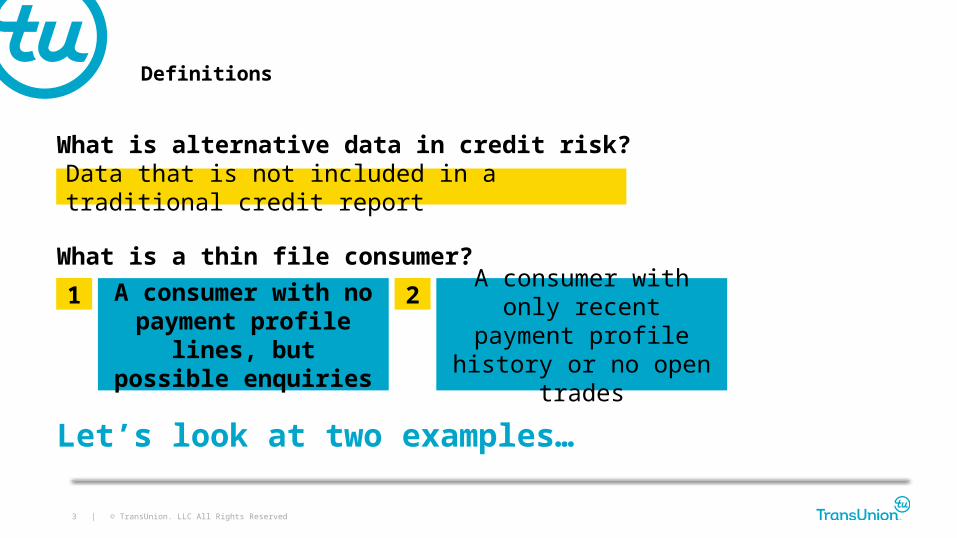

Definitions

What is alternative data in credit risk?

What is a thin file consumer?

Let’s look at two examples…

Data that is not included in a traditional credit report

A consumer with no payment profile lines, but possible enquiries

A consumer with only recent payment profile

history or no open trades

1 2

4 | © TransUnion. LLC All Rights Reserved

Thin File Population - Meet

John

5 | © TransUnion. LLC All Rights Reserved

Thin File Population - Meet

Jack

6 | © TransUnion. LLC All Rights Reserved

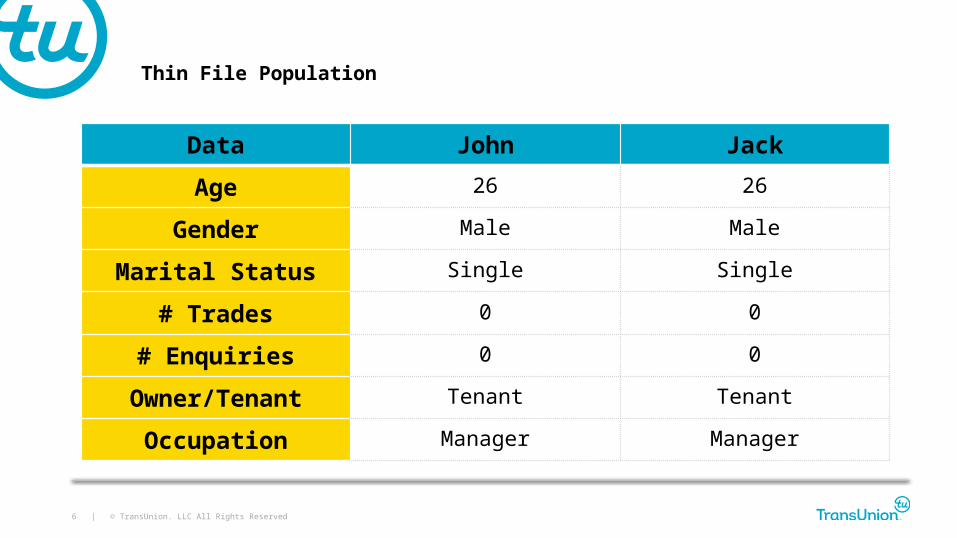

Thin File Population

Data John JackAge 26 26

Gender Male Male

Marital Status Single Single

# Trades 0 0

# Enquiries 0 0

Owner/Tenant Tenant Tenant

Occupation Manager Manager

7 | © TransUnion. LLC All Rights Reserved

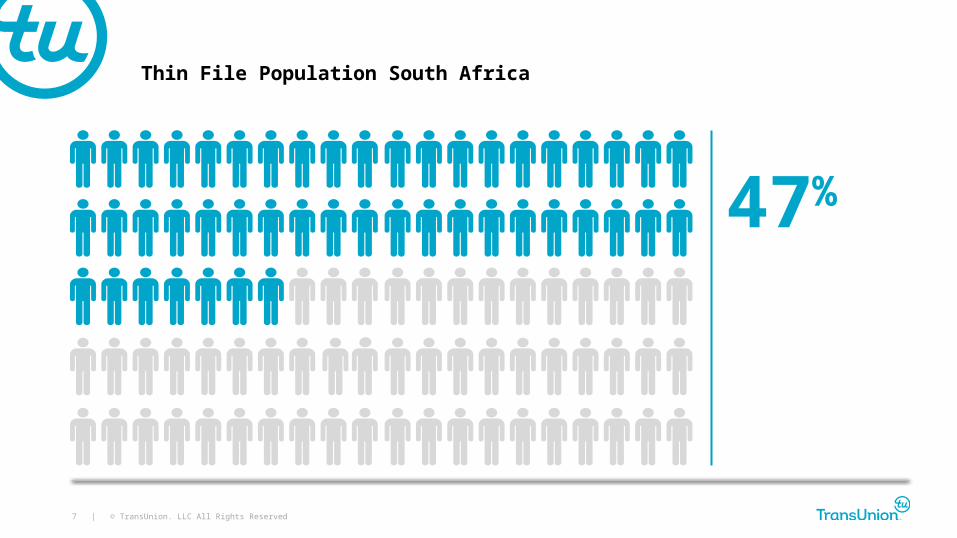

Thin File Population South Africa

47%

8 | © TransUnion. LLC All Rights Reserved

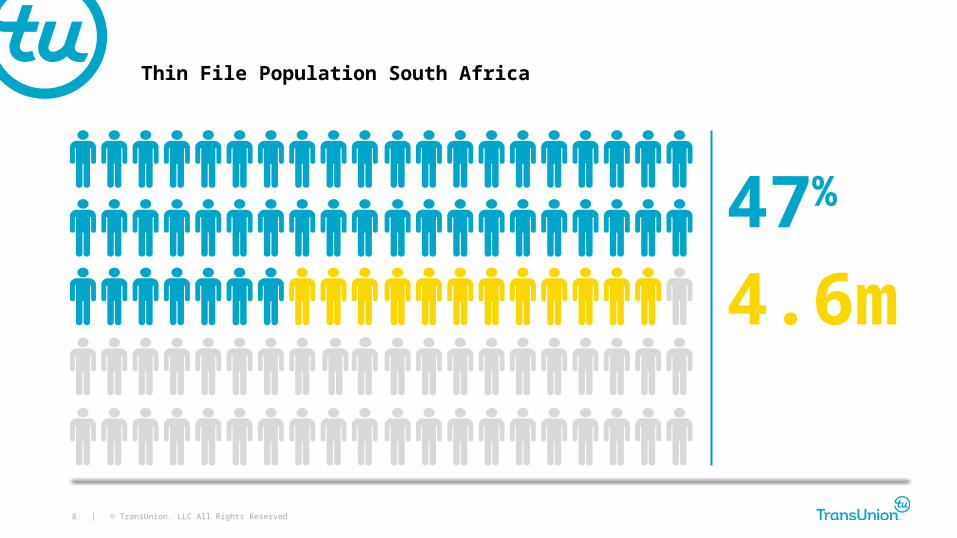

47%

Thin File Population South Africa

4.6m

9 | © TransUnion. LLC All Rights Reserved

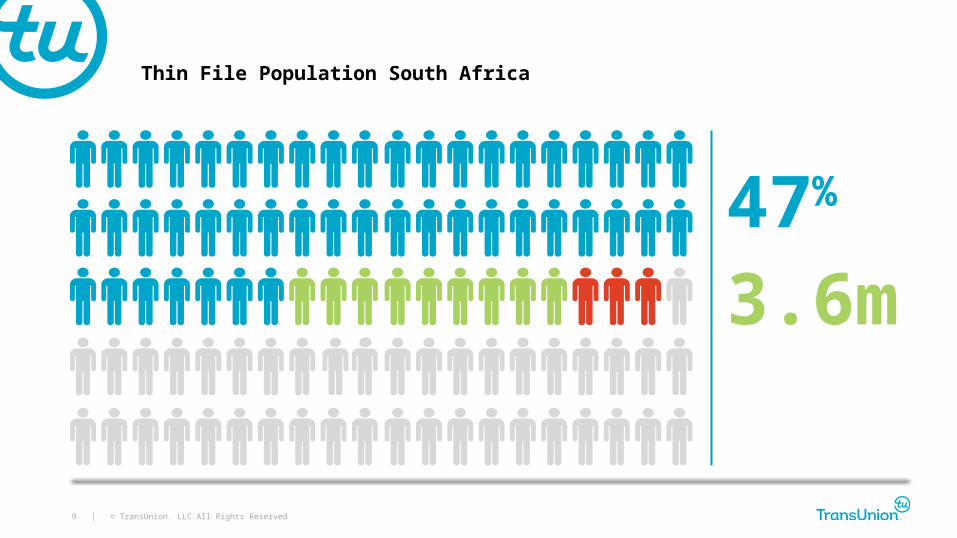

47%

Thin File Population South Africa

3.6m

10 | © TransUnion. LLC All Rights Reserved

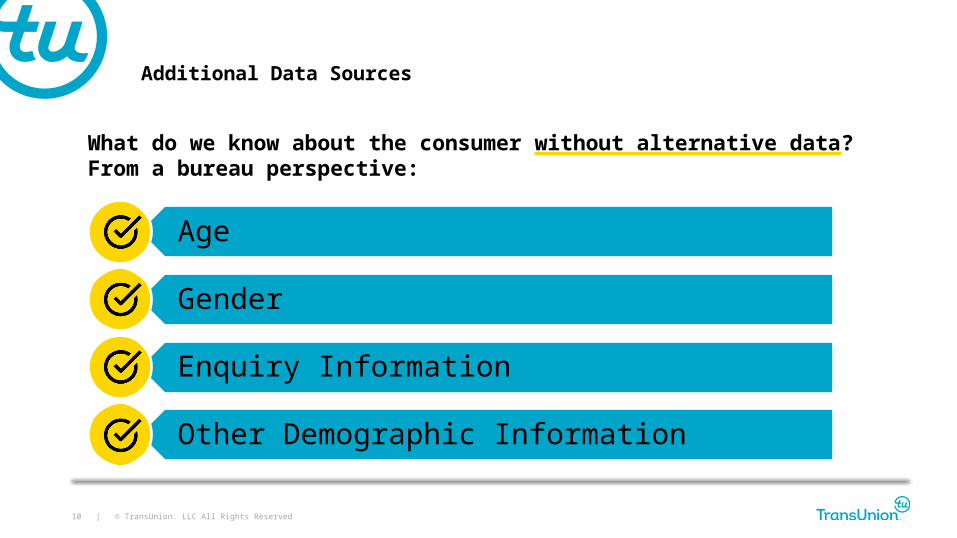

What do we know about the consumer without alternative data? From a bureau perspective:

Age

Gender

Enquiry Information

Other Demographic Information

Additional Data Sources

11 | © TransUnion. LLC All Rights Reserved

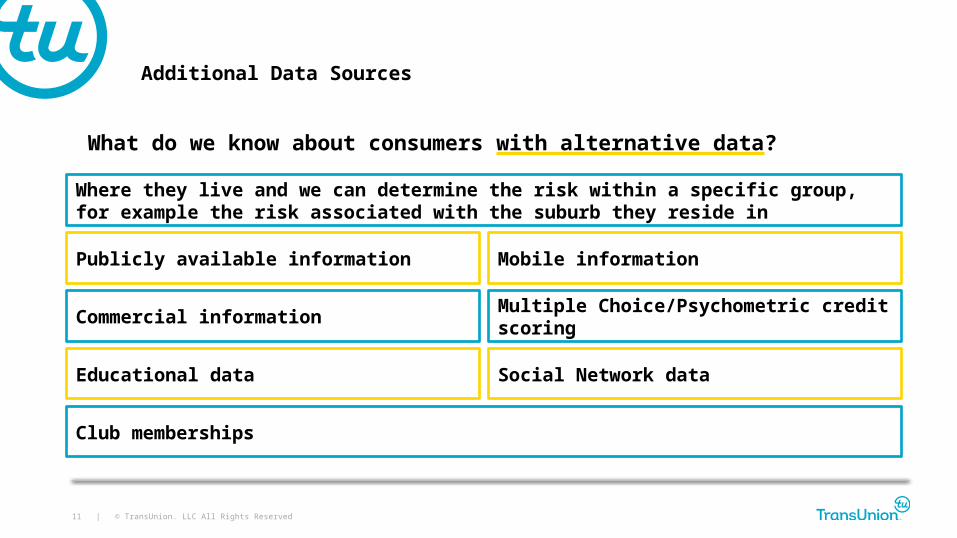

What do we know about consumers with alternative data?

Additional Data Sources

Where they live and we can determine the risk within a specific group, for example the risk associated with the suburb they reside in

Publicly available information Mobile information

Commercial information Multiple Choice/Psychometric credit scoring

Educational data Social Network data

Club memberships

12 | © TransUnion. LLC All Rights Reserved

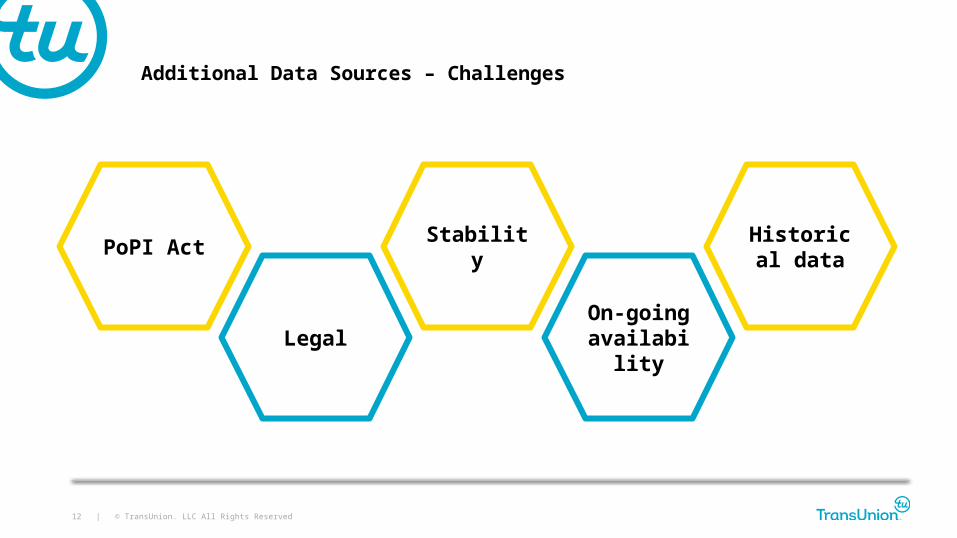

Additional Data Sources – Challenges

PoPI Act

Legal

Stability

On-going availability

Historical data

13 | © TransUnion. LLC All Rights Reserved

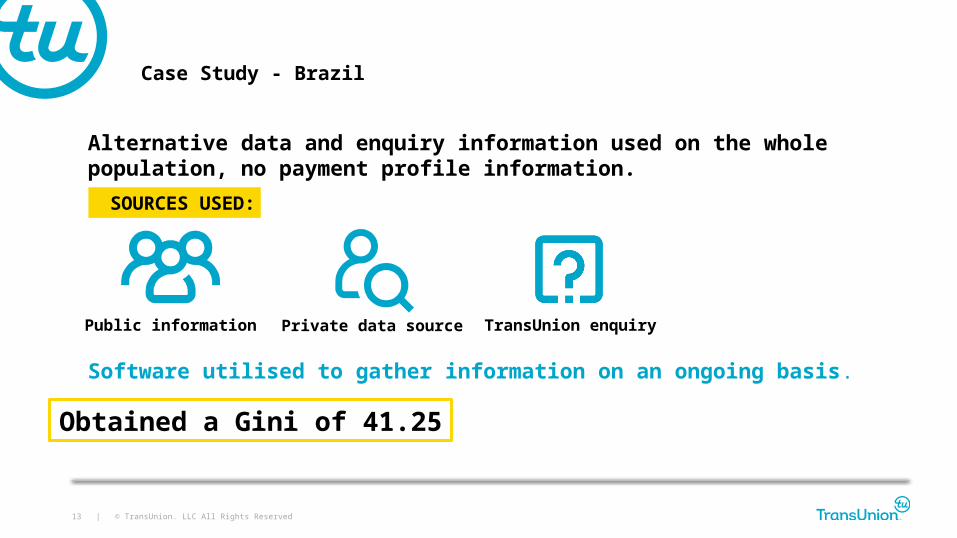

Software utilised to gather information on an ongoing basis.

Case Study - Brazil

Alternative data and enquiry information used on the whole population, no payment profile information. SOURCES USED:

Public information Private data source TransUnion enquiry

Obtained a Gini of 41.25

14 | © TransUnion. LLC All Rights Reserved

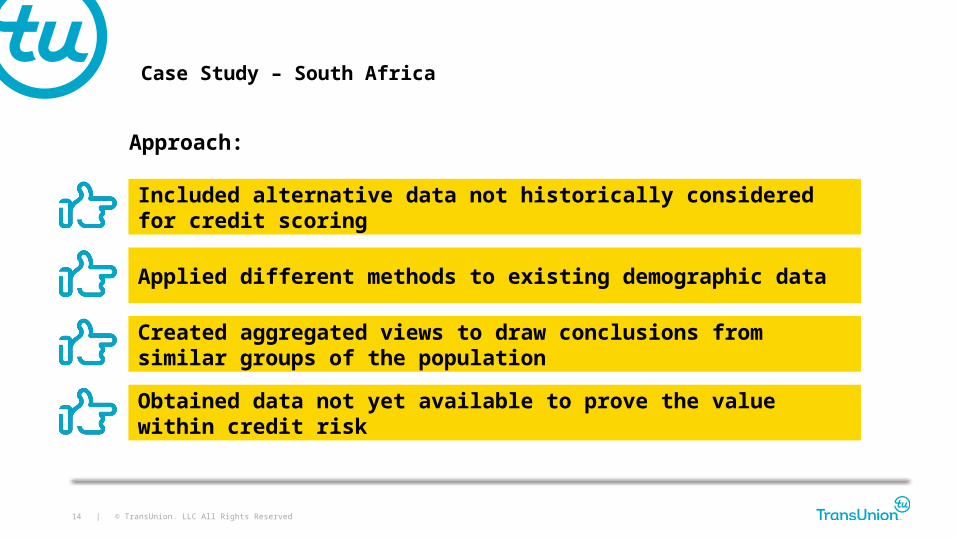

Approach:

Case Study – South Africa

Obtained data not yet available to prove the value within credit risk

Created aggregated views to draw conclusions from similar groups of the population

Applied different methods to existing demographic data

Included alternative data not historically considered for credit scoring

15 | © TransUnion. LLC All Rights Reserved

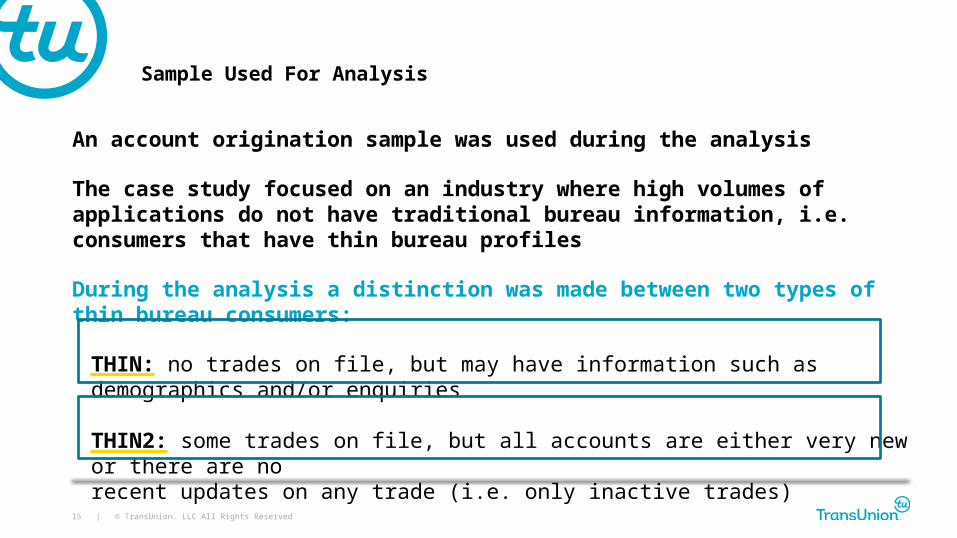

An account origination sample was used during the analysis

The case study focused on an industry where high volumes of applications do not have traditional bureau information, i.e. consumers that have thin bureau profiles

During the analysis a distinction was made between two types of thin bureau consumers:

THIN: no trades on file, but may have information such as demographics and/or enquiries

THIN2: some trades on file, but all accounts are either very new or there are norecent updates on any trade (i.e. only inactive trades)

Sample Used For Analysis

16 | © TransUnion. LLC All Rights Reserved

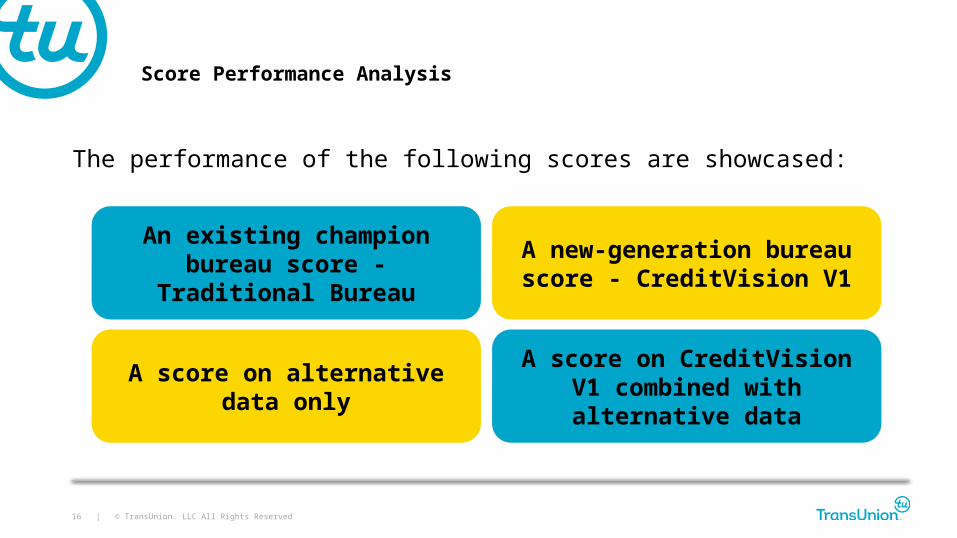

The performance of the following scores are showcased:

Score Performance Analysis

A score on CreditVision V1 combined with alternative data

A score on alternative data only

A new-generation bureauscore - CreditVision V1

An existing champion bureau score - Traditional Bureau

17 | © TransUnion. LLC All Rights Reserved

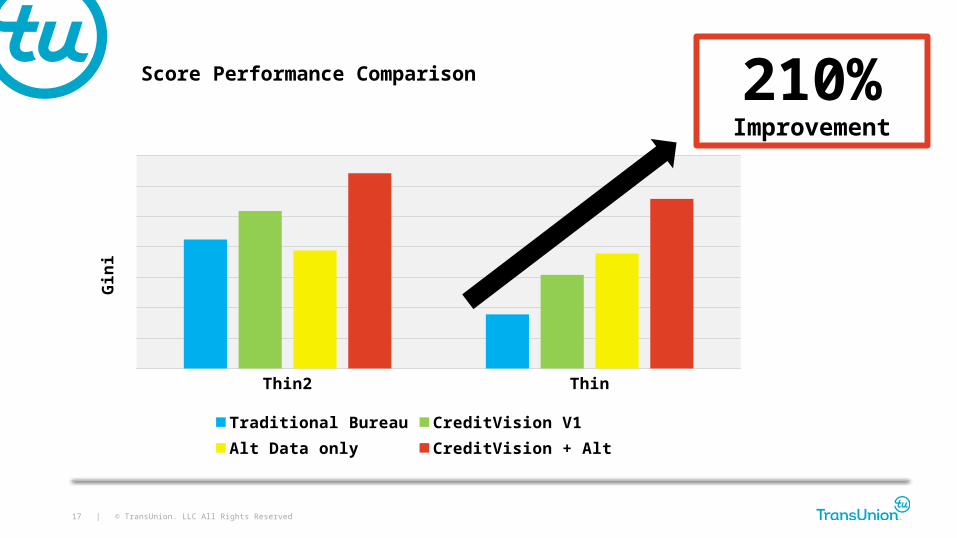

Thin2 Thin

Traditional Bureau CreditVision V1 Alt Data only CreditVision + Alt

Gin

i

Score Performance Comparison 210% Improvement

18 | © TransUnion. LLC All Rights Reserved

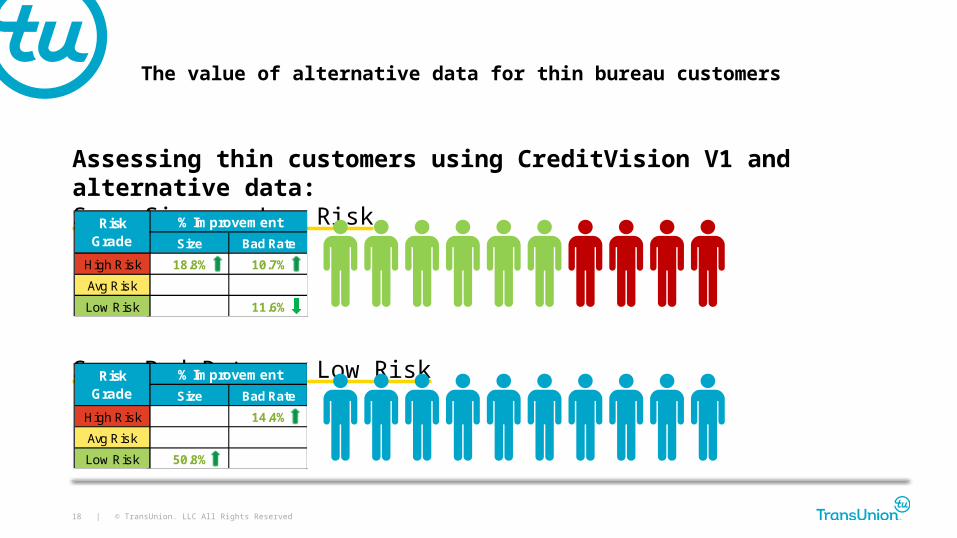

Assessing thin customers using CreditVision V1 and alternative data:Same Size on Low Risk

Same Bad Rate on Low Risk

Size Bad Rate Size Bad Rate Size Bad RateHigh Risk 37.8 32.4 44.9 35.9 18.8% 10.7%Avg Risk 37.6 25.4 29.5 23.7

Low Risk 24.6 17.5 25.6 15.5 11.6%

Risk Grade

Size Bad Rate Size Bad Rate Size Bad RateHigh Risk 37.8 32.4 39.1 37.1 14.4%Avg Risk 37.6 25.4 23.7 25.8

Low Risk 24.6 17.5 37.1 17.3 50.8%

CV + Alt % Improvement

Size Bad Rate Size Bad Rate Size Bad RateHigh Risk 37.8 32.4 44.9 35.9 18.8% 10.7%Avg Risk 37.6 25.4 29.5 23.7

Low Risk 24.6 17.5 25.6 15.5 11.6%

% Improvement

Size Bad Rate Size Bad Rate Size Bad RateHigh Risk 37.8 32.4 44.9 35.9 18.8% 10.7%Avg Risk 37.6 25.4 29.5 23.7

Low Risk 24.6 17.5 25.6 15.5 11.6%

Risk Grade

The value of alternative data for thin bureau customers

19 | © TransUnion. LLC All Rights Reserved

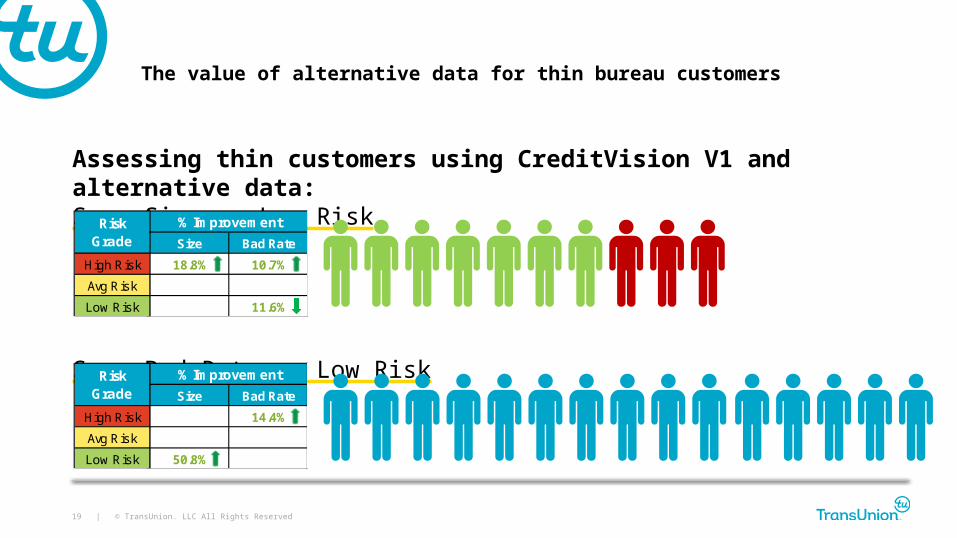

Assessing thin customers using CreditVision V1 and alternative data:Same Size on Low Risk

Same Bad Rate on Low Risk

Size Bad Rate Size Bad Rate Size Bad RateHigh Risk 37.8 32.4 44.9 35.9 18.8% 10.7%Avg Risk 37.6 25.4 29.5 23.7

Low Risk 24.6 17.5 25.6 15.5 11.6%

Risk GradeSize Bad Rate Size Bad Rate Size Bad Rate

High Risk 37.8 32.4 44.9 35.9 18.8% 10.7%Avg Risk 37.6 25.4 29.5 23.7

Low Risk 24.6 17.5 25.6 15.5 11.6%

% Improvement

The value of alternative data for thin bureau customers

Size Bad Rate Size Bad Rate Size Bad RateHigh Risk 37.8 32.4 39.1 37.1 14.4%Avg Risk 37.6 25.4 23.7 25.8

Low Risk 24.6 17.5 37.1 17.3 50.8%

CV + Alt % ImprovementSize Bad Rate Size Bad Rate Size Bad Rate

High Risk 37.8 32.4 44.9 35.9 18.8% 10.7%Avg Risk 37.6 25.4 29.5 23.7

Low Risk 24.6 17.5 25.6 15.5 11.6%

Risk Grade

20 | © TransUnion. LLC All Rights Reserved

Large portion of SA population is classified as ‘thin file’

True portfolio growth should come from: Thin file customers and new market entrants

Being the first to provide credit to a consumer results in long-term loyalty

Alternative data is very predictive in credit risk and assists in identifying your future good customers

Conclusion

v

vv QUESTIONS?