Embed Size (px)

Citation preview

Number of subscribers is key to pay-TV stocks’ performance

This week, major domestic/global pay-TV operators announced their net subscriber addition

numbers. KT Skylife (053210) posted net subscriber additions of 10,800 in September, more

than triple that of August (2,904). Meanwhile, Netflix (NFLX US), a US streaming internet TV

provider, reported net subscriber additions of 3.3m for 3Q16, more than double that of

2Q16. In particular, 97% of net additions came from regions other than the US.

We believe subscriber base expansion is positive for pay-TV operators’ earnings, since

monthly fixed-rate service revenue is their basic business model.

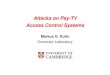

Figure 1. Net increase in KT Skylife’s subscribers jumped 3.7x MoM, sending the stock up

Notes: Subscriber data is a lagging indicator; Subscriber data displayed with a time lag of one month to show stock price

response to subscriber addition announcements

Source: KT Skylife, Thomson Reuters, Mirae Asset Daewoo Research

Figure 2. 3Q16 Netflix net subscribers up 2.3x QoQ, sending the stock higher

Notes: Subscriber data is a lagging indicator; Stock price is as of the earnings release date, as that is when quarter-end net

subscriber additions are announced. Source: Netflix, Bloomberg, Mirae Asset Daewoo Research

Media/Pay-TV (Overweight/Maintain)

Focus on fundamentals and industry trends

� Pay-TV operators: Increase in the number of subscribers; Subscriber performance is

driving major domestic/global players’ share price movements

� Industry trends: Time to focus on profitability of IPTV service; Increasing penetration

of technologically advanced services (UHD/DCS)

� Industry leader: Focus on KT Skylife (053210), in light of fundamentals and industry

trends

Issue Comment

October 20, 2016

Mirae Asset Daewoo Co., Ltd.

[Telecom Service / Media]

Jee-hyun Moon

+822-768-3615

Nu-ri Ha

+822-768-4130

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

-15

-10

-5

0

5

10

15

20

1/14 4/14 7/14 10/14 1/15 4/15 7/15 10/15 1/16 4/16 7/16 10/16

(W)('000 people)

Net increase in subscribers over the previous month (L)

KT Skylife's stock price (R)

20

50

80

110

140

0

2

4

6

8

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

(US$)(mn people)

Net increase in quarterly subscribers (L)

Netflix's stock price (R)

Media/Pay-TV

2

October 20, 2016

Mirae Asset Daewoo Research

Domestic pay-TV market trend

1) IPTV subscribers soon to exceed those of cable SOs

The most noteworthy trend in the domestic pay-TV market is that the number of

subscribers to telcos’ IPTV services has increased to the level of cable SOs, and is

anticipated to surpass that level next year. As of end-2Q16, the total number of IPTV

subscribers came in at 13mn (vs. 14mn for cable SOs).

In our view, an increasingly important variable for the IPTV business is the IPTV-

broadband internet service bundling rate. Broadband internet subscriptions serve as the

basis for the IPTV business, as broadband networks allow for two-way TV services. The

service bundling rate—i.e., IPTV subscribers divided by broadband internet

subscribers—is projected to reach 83% for KT by the end of this year, with SK Broadband

and LG Uplus exceeding 70% each. The uptrend in the bundling rate should ease

marketing competition going forward.

We believe the rapid quantitative growth in telcos’ IPTV businesses (increase in

subscribers) is expected to peak in the foreseeable future. As telcos’ IPTV margin growth

appears to be accelerating in 2H16, IPTV’s earnings contribution is anticipated to expand

next year.

Figure 3. Gap between cable SO subscribers and telcos’ IPTV subscribers narrowing

Note: 2Q subscribers are based on end-Jun.; Cable SO subscribers are based on end-Apr.

Source: Respective companies’ data, MSIP, KCTA, Mirae Asset Daewoo Research

Figure 4. Rate of bundling of telcos’ IPTV and broadband internet approaching 80% recently;

Now time to turn focus to profitability rather than quantitative growth

Note: IPTV is a two-way TV service provided by broadband internet networks; Broadband internet subscriptions are the basis

for IPTV subscriptions; Rate of bundling is calculated as IPTV subscribers divided by broadband internet subscribers

Source: Respective companies’ data, Mirae Asset Daewoo Research

14,932 14,905 14,846 14,780 14,424 14,459

4,919

6,529

8,614 10,637

12,282 13,000

3,262 3,791 4,181 4,261 4,310 4,338

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

11 12 13 14 15 2Q16

('000 persons) Cable SO IPTV Satellite

39.3

83.0

23.4

76.0

30.7

71.8

0

20

40

60

80

100

11 12 13 14 15 16F

(%)

KT

SK Broadband

LG Uplus

Media/Pay-TV

3

October 20, 2016

Mirae Asset Daewoo Research

2) Retransmission fee negotiations imminent

Currently, terrestrial TV networks charge pay-TV operators a retransmission fee of W280

per digital TV subscriber per month. The fee, or cost per subscriber (CPS), is negotiated

once a year. In the current negotiations, terrestrial networks are pushing for the fee to

be increased to up to W430.

For pay-TV operators, fees paid to terrestrial TV networks for carrying their content

(channels and programs) are major cost drivers. While pay-TV operators can increase

monthly subscription revenue and ancillary revenue (from VOD and shopping channel

fees) by expanding their subscriber base, leverage effect and profit growth will be

limited if content fees rise in tandem.

The government has organized a retransmission council to draw up CPS guidelines; the

Korea Communications Commission will release the guidelines on October 20th. While

the guidelines are advisory, not mandatory, we still think they are noteworthy

considering that they are the first such guidelines issued by the government and could

affect CPS negotiations, which must be finalized by year-end.

3) UHD broadcasting imminent

Terrestrial broadcasters are anticipated to start ultra-high-definition (UHD; resolution of

3840×2160) broadcasting in February 2017. Current plans call for UHD broadcasting to

be phased in beginning in Seoul and neighboring areas in February and being extended

into other metropolitan and smaller cities/districts through 2021. UHD broadcasting as a

percentage of overall broadcasting is slated to start at 5% in 2017, and increase to 25%

in 2020, 50% in 2023, and 100% in 2027.

When HD broadcasting (1920×1080) was first introduced, terrestrial broadcasters played

a key role in its spread; HD broadcasting was begun in 2001, and analog broadcasting

was completely phased out by end-2012. With terrestrial broadcasters moving to HD

broadcasting, pay-TV operators have accelerated the digital conversion. The digital

conversion rate stands at 78% for pay-TV operators and 53% for cable system operators.

Considering terrestrial broadcasters’ plans to start UHD broadcasting starting next year,

we believe that pay-TV operators with UHD infrastructure and content will gain traction.

Figure 5. Terrestrial networks to start UHD broadcasting around capital area in Feb. 2017;

UHD programming to be phased in starting at 5%, with target of 100% by 2027

Source: MSIP, KCC, Mirae Asset Daewoo Research

Media/Pay-TV

4

October 20, 2016

Mirae Asset Daewoo Research

Focus on KT Skylife in light of fundamentals and industry trend

Among domestic pay-TV operators, we believe KT Skylife deserves attention in light of 1)

net subscriber growth and 2) the industry trend of rising penetration of technologically

advanced services, including UHD and dish convergence solutions (DCS).

From a short-term perspective, the company delivered net subscriber growth MoM in

September despite a lower number of operating days. In addition, the company has

been displaying rapid platform revenue growth this year, aided by increasing fee

revenue from home shopping channels. In the medium to long term, the company is

likely to benefit from 1) the upcoming era of UHD broadcasting thanks to its ability to

launch UHD broadcasting services with relatively small investment and 2) improvements

in the business environment stemming from the government’s recent approval of DCS.

Table 1. Monthly subscribers: Net increase in Sep. 2016 is noteworthy in the short-term (‘000 people)

2015 Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sep. Oct. Nov. Dec.

Number of total subscribers 4,262 4,260 4,262 4,269 4,280 4,292 4,301 4,307 4,312 4,314 4,314 4,310

SkyLife 1,930 1,933 1,941 1,953 1,971 1,988 2,008 2,023 2,041 2,058 2,075 2,093 OTS 2,332 2,327 2,321 2,316 2,310 2,305 2,292 2,283 2,271 2,256 2,240 2,216 Net increase (persons) 644 -1,288 1,428 7,145 11,083 12,242 8,126 6,030 5,181 2,288 764 -4,996

2016 Jan. Feb. Mar. Apr. May Jun. Jul. Aug. Sep.

Number of total subscribers 4,310 4,310 4,311 4,317 4,325 4,338 4,345 4,348 4,359 SkyLife 2,111 2,128 2,147 2,169 2,193 2,219 2,244 2,262 2,283 OTS 2,199 2,182 2,164 2,148 2,131 2,119 2,101 2,086 2,075 Net increase (persons) 434 248 596 5,998 7,257 13,824 6,677 2,904 10,800

Note: SkyLife is satellite only; OTS stands for Olleh TV Skylife, which is bundled with KT IPTV

Source: Company data, Mirae Asset Daewoo Research

Table 2. Earnings trend and forecast (Wbn, %)

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16F 4Q16F 2014 2015 2016F

Revenue 147 154 161 164 150 161 165 170 623 626 646 Service 90 89 89 88 87 86 86 88 378 356 346 Platform 34 39 43 46 41 50 51 53 130 162 195 Cost-related 11 11 13 12 11 11 11 10 53 47 42 Other 13 14 17 18 12 15 17 18 62 62 62

OP 30 31 14 23 23 29 17 24 78 98 93 OP margin 20.6 20.1 8.5 13.8 15.4 18.0 10.6 14.0 12.5 15.6 14.4

Net profit 22 26 9 18 18 22 13 18 56 74 71 Net margin 14.7 16.7 5.6 11.0 12.0 13.7 8.0 10.5 8.9 11.9 11.0

Note: Based on non-consolidated K-IFRS; OP expected to recover on return of commission fees paid in 1Q15-2Q15;

Assuming expenses related to Broadcasting Development Fund to be incurred in 3Q16

Source: Company data, Mirae Asset Daewoo Research

Figure 6. Concept map of DCS service, officially approved by

MSIP in Oct. 2016

Figure 7. KT Skylife has provided the largest number of UHD

exclusive channels in Korea (5 channels)

Note: DCS (dish convergence solution) business expected to be introduced in

capital area in Dec. and nationwide next year

Source: MSIP, Mirae Asset Daewoo Research

Source: Company data, Mirae Asset Daewoo Research

Media/Pay-TV

5

October 20, 2016

Mirae Asset Daewoo Research

APPENDIX 1

Important Disclosures & Disclaimers

2-Year Rating and Target Price History

Company (Code) Date Rating Target Price Company (Code) Date Rating Target Price

KT Skylife(053210) 07/27/2016 Trading Buy 21,000 04/24/2015 Buy 24,000

04/26/2016 Trading Buy 18,000 01/28/2015 Trading Buy 20,000

01/26/2016 Trading Buy 17,000 10/30/2014 Trading Buy 23,000

10/27/2015 Buy 25,000 10/06/2014 Trading Buy 25,000

07/28/2015 Buy 29,000

Equity Ratings Distribution

Buy Trading Buy Hold Sell

69.27% 17.07% 13.66% 0.00%

* Based on recommendations in the last 12-months (as of September 30, 2016)

Disclosures

As of the publication date, Mirae Asset Daewoo Co., Ltd. and/or its affiliates do not have any special interest with the subject company and do not own 1%

or more of the subject company's shares outstanding.

Analyst Certification

The research analysts who prepared this report (the “Analysts”) are registered with the Korea Financial Investment Association and are subject to

Korean securities regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws and regulations

thereof. Opinions expressed in this publication about the subject securities and companies accurately reflect the personal views of the Analysts

primarily responsible for this report. Mirae Asset Daewoo Co., Ltd. (“Mirae Asset Daewoo”) policy prohibits its Analysts and members of their

households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do not serve as an officer, director or

advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or any

other benefits from the subject companies in the past 12 months and have not been promised the same in connection with this report. No part of

the compensation of the Analysts was, is, or will be directly or indirectly related to the specific recommendations or views contained in this report

but, like all employees of Mirae Asset Daewoo, the Analysts receive compensation that is impacted by overall firm profitability, which includes

revenues from, among other business units, the institutional equities, investment banking, proprietary trading and private client division. At the

time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the Analyst or

Mirae Asset Daewoo except as otherwise stated herein.

Disclaimers

This report is published by Mirae Asset Daewoo, a broker-dealer registered in the Republic of Korea and a member of the Korea Exchange.

Information and opinions contained herein have been compiled from sources believed to be reliable and in good faith, but such information has

not been independently verified and Mirae Asset Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness,

accuracy, completeness or correctness of the information and opinions contained herein or of any translation into English from the Korean

language. If this report is an English translation of a report prepared in the Korean language, the original Korean language report may have been

made available to investors in advance of this report. Mirae Asset Daewoo, its affiliates and their directors, officers, employees and agents do not

accept any liability for any loss arising from the use hereof. This report is for general information purposes only and it is not and should not be

construed as an offer or a solicitation of an offer to effect transactions in any securities or other financial instruments. The intended recipients of

this report are sophisticated institutional investors who have substantial knowledge of the local business environment, its common practices, laws

Stock Ratings Industry Ratings

Buy : Relative performance of 20% or greater Overweight : Fundamentals are favorable or improving

Trading Buy : Relative performance of 10% or greater, but with volatility Neutral : Fundamentals are steady without any material changes

Hold : Relative performance of -10% and 10% Underweight : Fundamentals are unfavorable or worsening

Sell : Relative performance of -10%

Ratings and Target Price History (Share price (─), Target price (▬), Not covered (■), Buy (▲), Trading Buy (■), Hold (●), Sell (◆))

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months.

* Although it is not part of the official ratings at Mirae Asset Daewoo Co., Ltd., we may call a trading opportunity in case there is a technical or short-term

material development.

* The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of

future earnings.

* The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic

conditions.

0

10,000

20,000

30,000

40,000

Oct 14 Oct 15 Oct 16

(W) KT Skylife

Media/Pay-TV

6

October 20, 2016

Mirae Asset Daewoo Research

and accounting principles and no person whose receipt or use of this report would violate any laws and regulations or subject Mirae Asset

Daewoo and its affiliates to registration or licensing requirements in any jurisdiction should receive or make any use hereof. Information and

opinions contained herein are subject to change without notice and no part of this document may be copied or reproduced in any manner or form

or redistributed or published, in whole or in part, without the prior written consent of Mirae Asset Daewoo. Mirae Asset Daewoo, its affiliates and

their directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may make a

purchase or sale, or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or

otherwise, in each case either as principals or agents. Mirae Asset Daewoo and its affiliates may have had, or may be expecting to enter into,

business relationships with the subject companies to provide investment banking, market-making or other financial services as are permitted

under applicable laws and regulations. The price and value of the investments referred to in this report and the income from them may go down

as well as up, and investors may realize losses on any investments. Past performance is not a guide to future performance. Future returns are not

guaranteed, and a loss of original capital may occur.

Distribution

United Kingdom: This report is being distributed by Daewoo Securities (Europe) Ltd. in the United Kingdom only to (i) investment professionals

falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth

companies and other persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons

together being referred to as “Relevant Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should

not act or rely on this report or any of its contents.

United States: This report is distributed in the U.S. by Daewoo Securities (America) Inc., a member of FINRA/SIPC, and is only intended for major

institutional investors as defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by

their acceptance thereof represent and warrant that they are a major institutional investor and have not received this report under any express or

implied understanding that they will direct commission income to Mirae Asset Daewoo or its affiliates. Any U.S. recipient of this document wishing

to effect a transaction in any securities discussed herein should contact and place orders with Daewoo Securities (America) Inc., which accepts

responsibility for the contents of this report in the U.S. The securities described in this report may not have been registered under the U.S.

Securities Act of 1933, as amended, and, in such case, may not be offered or sold in the U.S. or to U.S. persons absent registration or an applicable

exemption from the registration requirements.

Hong Kong: This document has been approved for distribution in Hong Kong by Daewoo Securities (Hong Kong) Ltd., which is regulated by the

Hong Kong Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This

report is for distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong

Kong (Cap. 571, Laws of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person.

All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact

Mirae Asset Daewoo or its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations

and not subject Mirae Asset Daewoo and its affiliates to any registration or licensing requirement within such jurisdiction.

Mirae Asset Daewoo International Network

Mirae Asset Daewoo Co., Ltd. (Seoul) Daewoo Securities (Hong Kong) Ltd. Daewoo Securities (America) Inc.

Head Office

34-3 Yeouido-dong, Yeongdeungpo-gu

Seoul 150-716

Korea

Two International Finance Centre

Suites 2005-2012

8 Finance Street, Central

Hong Kong, China

320 Park Avenue

31st Floor

New York, NY 10022

United States

Tel: 82-2-768-3026 Tel: 85-2-2845-6332 Tel: 1-212-407-1000

Daewoo Securities (Europe) Ltd. Daewoo Securities (Singapore) Pte., Ltd. PT. Daewoo Securities Indonesia

41st Floor, Tower 42

25 Old Broad St.

London EC2N 1HQ

United Kingdom

Six Battery Road #11-01

Singapore, 049909

Equity Tower Building Lt.50

Sudirman Central Business District Jl.

Jendral Sudirman Kav. 52-53, Jakarta Selatan

Indonesia 12190

Tel: 44-20-7982-8000 Tel: 65-6671-9845 Tel: 62-21-515-1140

Beijing Representative Office Shanghai Representative Office Ho Chi Minh Representative Office

2401A, 24th Floor, East Tower, Twin Towers

B-12 Jianguomenwai Avenue

Chaoyang District, Beijing 100022

China

Room 38T31, 38F SWFC

100 Century Avenue

Pudong New Area, Shanghai 200120

China

Suite 2103, Saigon Trade Center

37 Ton Duc Thang St,

Dist. 1, Ho Chi Minh City,

Vietnam

Tel: 86-10-6567-9299 Tel: 86-21-5013-6392 Tel: 84-8-3910-6000

Daewoo Investment Advisory (Beijing) Co., Ltd. Daewoo Securities (Mongolia) LLC

2401B, 24th Floor, East Tower, Twin Towers

B-12 Jianguomenwai Avenue,

Chaoyang District, Beijing 100022

China

#406, Blue Sky Tower, Peace Avenue 17

1 Khoroo, Sukhbaatar District

Ulaanbaatar 14240

Mongolia

Tel: 86-10-6567-9699 Tel: 976-7011-0807