Embed Size (px)

Citation preview

Thinking in RandomnessStatistical Methods in Finance

Lecture 3

Ta-Wei Huang

December 7, 2016

Ta-Wei Huang Thinking in Randomness December 7, 2016 1 / 28

Table of Contents

In this week, I’d like to tell the story behind the randomness, that is, howto think about our data in an uncertain world.

1 Random Vector and Matrix

2 Why Random Vectors?

3 Random Sample

4 Next Lecture

Ta-Wei Huang Thinking in Randomness December 7, 2016 2 / 28

Table of Contents

In this week, I’d like to tell the story behind the randomness, that is, howto think about our data in an uncertain world.

1 Random Vector and Matrix

2 Why Random Vectors?

3 Random Sample

4 Next Lecture

Ta-Wei Huang Thinking in Randomness December 7, 2016 2 / 28

Table of Contents

In this week, I’d like to tell the story behind the randomness, that is, howto think about our data in an uncertain world.

1 Random Vector and Matrix

2 Why Random Vectors?

3 Random Sample

4 Next Lecture

Ta-Wei Huang Thinking in Randomness December 7, 2016 2 / 28

Table of Contents

In this week, I’d like to tell the story behind the randomness, that is, howto think about our data in an uncertain world.

1 Random Vector and Matrix

2 Why Random Vectors?

3 Random Sample

4 Next Lecture

Ta-Wei Huang Thinking in Randomness December 7, 2016 2 / 28

Random Vector and Matrix

Review: Random Vector

Definition 3.1.1 (Random Vector)

A random vector X =

[X1

...Xn

]is a vector whose elements X1, · · · , Xn are

random variables.

Definition 3.1.2 (Joint Distribution Function)

Let (Ω,F ,P) be a probability space and X = [X1 · · · Xn]′ a random

vector. The joint distribution function of X is defined by

FX(x1, · · · , xn) = P(X1 ≤ x1, · · · , X1 ≤ xn),∀x1, · · · , xn ∈ R.

The joint pdf is given by fX(x1, · · · , xn) = ∂n

∂x1···∂xnFX(x1, · · · , xn).

Ta-Wei Huang Thinking in Randomness December 7, 2016 3 / 28

Random Vector and Matrix

Review: Marginal Distribution and Expectation

Definition 3.1.3 (Marginal Distribution and Expectation)

The marginal distribution of Xi is given by

fXi(xi) =∫· · ·

∫fX(x1, · · · , xn)dx1 · · · dxi−1dxi+1 · · · dxn.

The expectation of Xi is E[Xi] =∫∞−∞ fXi(xi)dxi.

The variance of Xi is var[Xi] = E[(Xi − E[Xi])2].

The covariance of Xi and Xj is

cov[Xi, Xj ] = E[(Xi − E[Xi])(Xj − E[Xj ])].

Now, we’d like to generalize the expectation, variance and covariance of a

random variable to the case of a random vector.

Ta-Wei Huang Thinking in Randomness December 7, 2016 4 / 28

Random Vector and Matrix

Expectation and Covariance Matrix

We can summarize information of means, variances, and covariances of

jointly distributed random variables by the following definitions.

Definition 3.1.4 (Expectation of a Random Vector)

The expectation of a random vector X is E[X] =

[ E[X1]

...E[Xn]

]≡ µ.

Definition 3.1.5 (Covariance Matrix)

The covariance matrix of a random vector X is

cov(X) = Σ = E[(X−µ)(X−µ)′] =

var[X1] cov[X1,X2] ··· cov[X1,Xn]

......

. . ....

cov[Xn,X1] cov[Xn,X2] ··· var[Xn]

.Ta-Wei Huang Thinking in Randomness December 7, 2016 5 / 28

Random Vector and Matrix

Covariance Matrix of Two Random Vectors

Definition 3.1.6 (Covariance Matrix)

Let X =

[X1

...Xp

]and Y =

[Y1

...Yq

]be two random vectors. The covariance

matrix of X and Y is defined as

cov(X,Y) = E[(X−µX)(Y−µY)′] =

cov[X1,Y1] cov[X1,Y2] ··· cov[X1,Yq ]

......

. . ....

cov[Xp,Y1] cov[Xp,Y2] ··· cov[Xp,Yq ]

.Note that here cov(X,Y) = cov(Y,X)′.

Ta-Wei Huang Thinking in Randomness December 7, 2016 6 / 28

Random Vector and Matrix

Propositions

Proposition 3.1.7 (Linear Combination of Random Vector)

Let a = [a1 · · · an]′ be a coefficient matrix and X a random vector. Then

the linear combination a′X is a scalar and

E[a′X] = a′µ =∑n

i=1 aiE[Xi];

cov[a′X] = a′Σa =∑n

i=1

∑nj=1 aiajcov[Xi, Xj ].

Proof.

E[a′X] = E[∑n

i=1 aiXi] =∑n

i=1 aiE[Xi] = a′E[X] = a′µ.

cov[a′X] = E[(a′X− a′µ)(a′X− a′µ)′]

= E[a′(X− µ)(X− µ)′a] = a′E[(X− µ)(X− µ)′]a = a′Σa.

Ta-Wei Huang Thinking in Randomness December 7, 2016 7 / 28

Random Vector and Matrix

Properties of a Covariance Matrix 1-1

Proposition 3.1.8 (Properties of a Covariance Matrix 1)

Let a = [a1 · · · an]′ and An×n be coefficient matrices and X a random

vector with mean µ and covariance matrix Σ. Then,

1 Σ = E(XX′)− µµ′;

2 cov(AX + a) = AΣA′;

3 Σ is a symmetric positive semi-definite matrix.

Proof. To prove (1), we have Σ = E[(X− µ)(X− µ)′]

= E[(X− µ)(X′ − µ′)] = E(XX′ −Xµ′ + µX ′ − µµ′)

= E(XX′)− E(X)µ′ + µE(X)′ − µµ′a = E(XX′)− µµ′.

Ta-Wei Huang Thinking in Randomness December 7, 2016 8 / 28

Random Vector and Matrix

Properties of a Covariance Matrix 1-2

Proof. It is similar to prove (2) by the way mentioned in page 7.

To prove 3, we need the result of spectral decomposition.

Let λ1, ..., λs be the eigenvalues of Σ and e1, ..., es the corresponding

normalized eigenvectors. By the spectral decomposition, we can write

Σ = PΛP ′, where P = [e1 · · · es] and Λ = diag(λ1, ..., λs).

Then, for any n-by-1 vector x, we have

x′Σx = x′PΛP ′x =

n∑i=1

(√λix′ei)

2 ≥ 0.

Therefore, the covariance matrix Σ is a positive semi-definite matrix.

Ta-Wei Huang Thinking in Randomness December 7, 2016 9 / 28

Random Vector and Matrix

Properties of a Covariance Matrix 2

Proposition 3.1.9 (Properties of a Covariance Matrix 2)

Let X,X1,X2 be p× 1 random vectors, a a p× 1 constant vector, Y a

q × 1 random vector, b a q × 1 constant vector, and A,B two q × p

matrices. Then the following properties hold.

1 cov(X1 + X2,Y) = cov(X1,Y) + cov(X2,Y);

2 cov(AX + a, B′Y + b) = Acov(X,Y)B;

3 if X,Y are independent, then cov(X,Y) = 0.

Proof. Skip! Try to prove by your own! (Hint: Use definition.)

Ta-Wei Huang Thinking in Randomness December 7, 2016 10 / 28

Random Vector and Matrix

Random Matrix

Definition 3.1.10 (Random Matrix)

A matrix

Xn×p =

X11 X12 ··· X1p

......

. . ....

Xn1 Xn2 ··· Xnp

is called a random matrix if its each entry Xij is a random variable.

There are two ways to think about a random matrix. We often consider

the column vector as one variable with n outcomes and the row vector as

an observed item with p measurements.

Ta-Wei Huang Thinking in Randomness December 7, 2016 11 / 28

Why Random Vectors?

A Simple Market Model 1

The position in risky securities can be specified as the number of shares of

stock held by an investor.

Definition 3.2.1 (Stock Price)

The price of the share i at time t will be denoted by Si(t).

The current stock price Si(0) is known to all investors

The future price Si(t), t > 0 remains uncertain

The return on stock i at time t is Ri(t) = Si(t)−Si(t−1)Si(t−1) .

Ta-Wei Huang Thinking in Randomness December 7, 2016 12 / 28

Why Random Vectors?

A Simple Market Model 2

The risk-free position can be described as the amount held in a bank

account. As an alternative to keeping money in a bank, investors may

choose to invest in bonds.

Definition 3.2.2 (Bond Price)

The price of one bond at time t will be denoted by B(t) with a fixed

risk-free interest rate r.

Here we do not consider a stochastic risk-free rate.

Example

Assume that the continuous risk-free rate is Rf . Then the bond price at

time t is B(t) = B(0) exp rt.

Ta-Wei Huang Thinking in Randomness December 7, 2016 13 / 28

Why Random Vectors?

A Simple Market Model 3

Our task is to build a mathematical model of a market of financial

securities. A crucial first stage is concerned with the properties of the

mathematical objects involved.

Assumption 3.2.3

The future stock price Si(t) is a random variable with at least two different

values. The future price B(t) of the risk-free security is a known number.

There are still some important assumptions, but we omit it since they are

out of the scope.

Ta-Wei Huang Thinking in Randomness December 7, 2016 14 / 28

Why Random Vectors?

A Simple Market Model 4

Now, suppose an investor forms a portfolio by putting w0 in the risk-free

asset B(t) and w1, ..., wi, ..., wN in risky stocks S1(t), ..., Si(t).

The payoff vector of the bond and stocks is P =

B(t)S1(t)

...SN (t)

.

The weight vector of assets is w′ = (w0 w1 · · · wN ).

Ta-Wei Huang Thinking in Randomness December 7, 2016 15 / 28

Why Random Vectors?

A Simple Market Model 5

The value of that portfolio at time t is

V (t) = w′P = (w0 w1 · · · wN )

B(t)S1(t)

...SN (t)

= w0B(t) +∑N

i=1wiSi(t).

Questions

What is the mean of the value of that portfolio?

What is the variance of the value of that portfolio?

Ta-Wei Huang Thinking in Randomness December 7, 2016 16 / 28

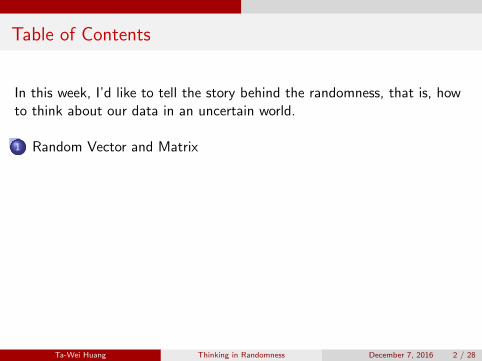

Why Random Vectors?

A Simple Market Model 6

You can directly calculate the mean and variance by:

E(V (t) = E[w0B(t) +

N∑i=1

wiSi(t)] = w0B(t) +

N∑i=1

wiE[Si(t)]

var[V (t)] =

N∑i=1

w2i var[Si(t)] +

∑i 6=j

wiwjcov[Si(t), Sj(t)]

Question

However, throughout this method, we cannot directly see the relationships

among different stocks, especially when using software to do that job. Is

there any good way to present all information about means, variances and

covariances among those assets?

Ta-Wei Huang Thinking in Randomness December 7, 2016 17 / 28

Why Random Vectors?

A Simple Market Model 7

We can also apply the random vector concept to this problem.

E(V (t)) = w′E[P] = (w0 w1 · · · wN )

B(t)E[S1(t)]

...E[SN (t)]

var[V (t)] = w′Σ w =

w′

0 0 ··· 0

var[S1(t)] cov[S1(t),S2(t)] ··· cov[S1(t),SN (t)]

......

. . ....

cov[SN (t),S1(t)] cov[SN (t),S2(t)] ··· var[SN (t)]

w

Ta-Wei Huang Thinking in Randomness December 7, 2016 18 / 28

Why Random Vectors?

Summary

From here, we can clearly see two things.

In classical view, the price bond position B(t) is fixed at any time t.

Since the stock position S1(t), · · · , SN (t) has the feature of

randomness, we assume that the random vector of stock prices

follows a joint normal distribution (a very simple assumption).

Ta-Wei Huang Thinking in Randomness December 7, 2016 19 / 28

Random Sample

Collect the Sample

Suppose that you want to know the profitability of a specific industry in

the world. Then, you need to do the following steps:

1 Find a proxy of the profitability. ⇒ EPS, Profit Margin, etc.

2 Collect a representative ”sample.”

⇒ Random sampling, cluster sampling, etc.

3 Make assumption and then do the statistical modeling.

⇒ Normality assumption, i.i.d assumption, GARCH assumption.

Here, we use mathematical concepts to present the above steps.

Ta-Wei Huang Thinking in Randomness December 7, 2016 20 / 28

Random Sample

Random Sample: One Variable Case 1

Definition 3.3.1 (Random Sample)

If the random variables X1, · · · , Xn ∼ f(x|θ) are independent and

identically distributed (iid), then these random variables constitute a

random sample of size n from the common distribution f(x|θ).

1 For n companies, each of them has an uncertain profitability proxy Xi.

2 X1, · · · , Xn are independently chosen from the population.

⇒ What is the population in this case?

3 Statistical assumptions: assume that X1, · · · , Xn have a common

distribution f(x|θ).

Ta-Wei Huang Thinking in Randomness December 7, 2016 21 / 28

Random Sample

Random Sample: One Variable Case 2

Figure: What is a random sample?

Ta-Wei Huang Thinking in Randomness December 7, 2016 22 / 28

Random Sample

Random Sample: Multivariate Case

Definition 3.3.2 (Random Sample)

Let X =

X11 X12 ··· X1p

......

. . ....

Xn1 Xn2 ··· Xnp

=

X′1

...X′

n

be a random matrix.

We say that X is a random sample if X1, · · · ,Xn are independent and

identically distributed (iid) with joint pdf f(x1, · · · , xp|θ).

Note that each vector Xi = [Xi1 · · · Xip]′ is a bundle of n variables on

a single item i. The definition suggests that

1 The n items are independent and identically distributed.

2 The p variables may have correlation depicted by the joint pdf.

Ta-Wei Huang Thinking in Randomness December 7, 2016 23 / 28

Random Sample

Take a Look at the Dataset

The dataset given below is regarded as a realization of a random matrix X.

X1 X2 · · · Xp

Item 1 x11 x12 · · · x1p

Item 2 x21 x22 · · · x2p...

......

......

Item n xn1 xn2 · · · xnp

Nonparametric analysis: no specific distribution is assigned to

Xi = [Xi1 · · · Xip]′.

Parametric Estimation: Xi = [Xi1 · · · Xip]′ follows a specific

distribution f(x1, · · · , xp|θ) with parameter(s) θ.

Ta-Wei Huang Thinking in Randomness December 7, 2016 24 / 28

Random Sample

Nonparametric Method: Kernel Density Estimation 1

Let x1, · · · , xN be a realization of a random sample X1, · · · , XN . A

natural local estimate of the density function has the form

f(x0) =# xi ∈ B(x0, λ)

Nλ,

where B(x0, λ) is an open ball with center x0 and radius λ.

The above estimator is very naive, and most of time we use another

estimator called Parzen estimate, which is more complicated.

Ta-Wei Huang Thinking in Randomness December 7, 2016 25 / 28

Random Sample

Nonparametric Method: Kernel Density Estimation 2

Here is an simple example. The data x is 1000 random number generating

from a longnormal distribution with mean 1 and standard deviation 0.5.

The following graph shows results of density estimation.

Ta-Wei Huang Thinking in Randomness December 7, 2016 26 / 28

Random Sample

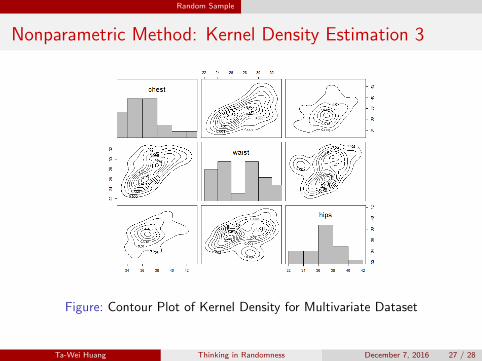

Nonparametric Method: Kernel Density Estimation 3

Figure: Contour Plot of Kernel Density for Multivariate Dataset

Ta-Wei Huang Thinking in Randomness December 7, 2016 27 / 28

Next Lecture

The Next Lecture

In next lecture, I’ll introduce a very popular parametric statistical model -

the linear model.

Ta-Wei Huang Thinking in Randomness December 7, 2016 28 / 28

![(Pseudo) Randomness [2ex]](https://img.pdfslide.us/doc/110x75/61570689a097e25c765040f3/pseudo-randomness-2ex.jpg)